Will NVIDIA reach $300 this year ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed April 23, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 72%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

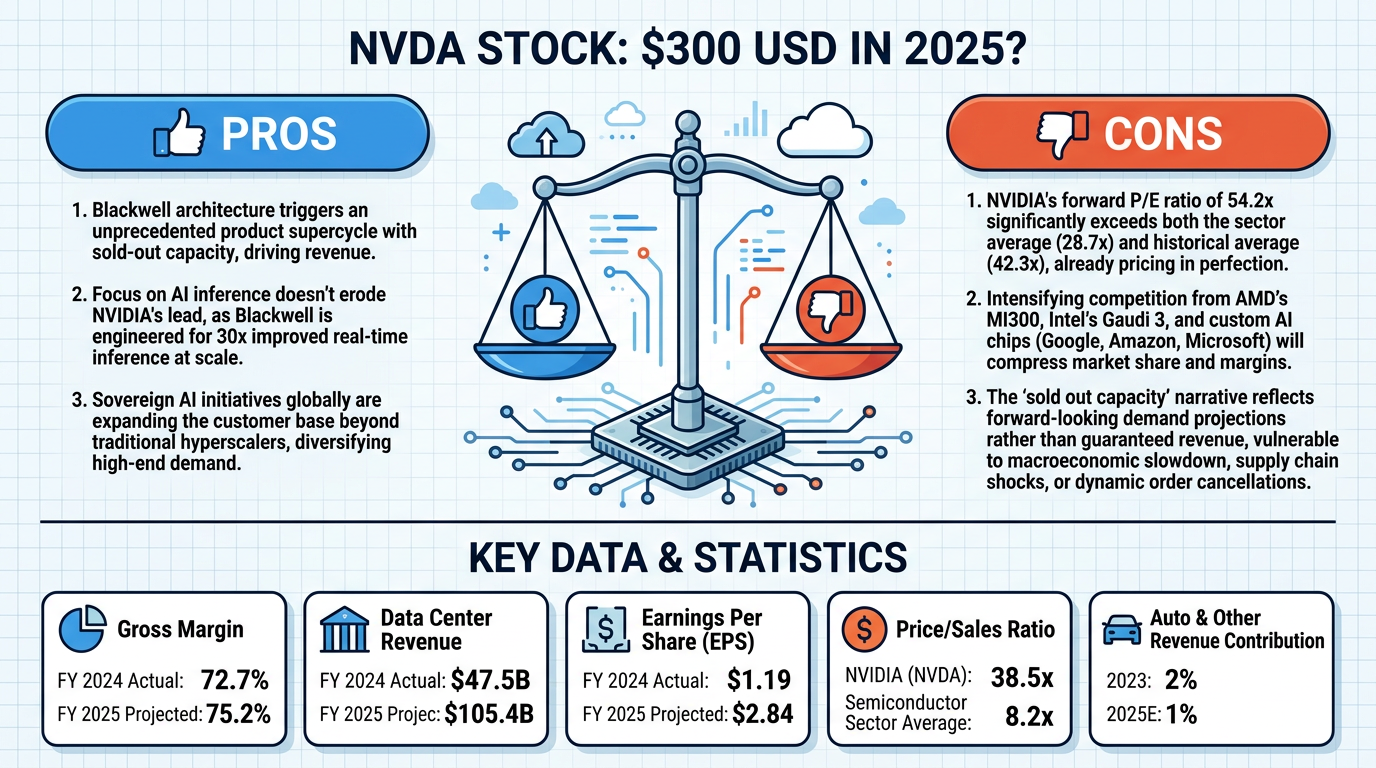

✅ Key PRO arguments:

- ■The Blackwell architecture (B200/GB200) represents an unprecedented product supercycle with production capacity sold out for several quarters, driving revenue growth beyond current market expectations as hyperscalers significantly increase capital expenditure.

- ■The shift toward AI inference does not erode NVIDIA's dominance because Blackwell is specifically engineered for real-time inference at scale, delivering 30x improvements that maintain pricing power against cheaper ASIC alternatives.

- ■Sovereign AI initiatives globally are expanding NVIDIA's customer base beyond traditional hyperscalers, creating a new and diversified demand driver for high-end GPU infrastructure.

❌ Key ANTI arguments:

- ■NVIDIA's forward P/E ratio of 54.2x significantly exceeds both the semiconductor sector average (28.7x) and its own historical average (42.3x), already pricing in near-perfect Blackwell execution with minimal room for further multiple expansion to reach $300.

- ■Intensifying competition from AMD's MI300 series, Intel's Gaudi 3, and custom AI chips from Google (TPUs), Amazon (Trainium/Inferentia), and Microsoft will compress NVIDIA's pricing power and market share.

- ■The 'sold out production capacity' narrative reflects forward-looking demand projections rather than guaranteed revenue, and any macroeconomic slowdown, supply chain disruption, or competitive substitution could evaporate this backlog.

💭 Conclusion: The debate centered on whether NVIDIA's Blackwell product cycle and AI demand could propel the stock to $300 in 2025. The pro side presented compelling arguments about unprecedented demand and ecosystem lock-in, but the anti side effectively countered that NVIDIA's extreme valuation multiples already price in most of the bullish scenario. At a forward P/E exceeding 54x, reaching $300 would require both flawless execution and further multiple expansion, which is historically unlikely for semiconductor stocks. The intensifying competitive landscape from both traditional chip rivals and hyperscaler custom silicon adds meaningful risk to NVIDIA's pricing power. While NVIDIA's fundamental business remains exceptionally strong, the gap between current price levels and $300 requires an optimistic confluence of factors that the valuation constraints make improbable within the 2025 timeframe.

🔬 DeepResearch Result: FALSE ❌ (72% confidence)

Assertion: Will NVIDIA reach $300 this year ?

📊 Tournament: 0 voted TRUE, 1 voted FALSE (1 debates played, 3 models)

📊 Weighted scores: TRUE=0.00, FALSE=0.80

🏅 Judge Score Changes:

anthropic/claude-opus-4.6: +8

✅ PRO Arguments:

- ■The Blackwell architecture (B200/GB200) represents an unprecedented product supercycle with production capacity sold out for several quarters, driving revenue growth beyond current market expectations as hyperscalers significantly increase capital expenditure. [google/gemini-3-flash-preview]

- ■The shift toward AI inference does not erode NVIDIA's dominance because Blackwell is specifically engineered for real-time inference at scale, delivering 30x improvements that maintain pricing power against cheaper ASIC alternatives. [google/gemini-3-flash-preview]

- ■Sovereign AI initiatives globally are expanding NVIDIA's customer base beyond traditional hyperscalers, creating a new and diversified demand driver for high-end GPU infrastructure. [google/gemini-3-flash-preview]

- ■NVIDIA's insurmountable CUDA software-hardware ecosystem creates deep lock-in effects that make competitive substitution extremely difficult, protecting market share and margins. [google/gemini-3-flash-preview]

- ■NVIDIA is transforming from a hardware vendor into the essential utility provider for the global AI economy, fundamentally changing its long-term growth trajectory and justifying premium valuations. [google/gemini-3-flash-preview]

❌ ANTI Arguments:

- ■NVIDIA's forward P/E ratio of 54.2x significantly exceeds both the semiconductor sector average (28.7x) and its own historical average (42.3x), already pricing in near-perfect Blackwell execution with minimal room for further multiple expansion to reach $300. [deepseek/deepseek-v3.2]

- ■Intensifying competition from AMD's MI300 series, Intel's Gaudi 3, and custom AI chips from Google (TPUs), Amazon (Trainium/Inferentia), and Microsoft will compress NVIDIA's pricing power and market share. [deepseek/deepseek-v3.2]

- ■The 'sold out production capacity' narrative reflects forward-looking demand projections rather than guaranteed revenue, and any macroeconomic slowdown, supply chain disruption, or competitive substitution could evaporate this backlog. [deepseek/deepseek-v3.2]

- ■Geopolitical risks including export controls to China have already harmed NVIDIA's competitive position, and further restrictions could materially impact revenue from a significant market segment. [deepseek/deepseek-v3.2]

- ■At current elevated valuations, reaching $300 would require not just strong earnings growth but sustained multiple expansion in an environment where semiconductor multiples are historically mean-reverting. [deepseek/deepseek-v3.2]

💭 Reasoning: The debate centered on whether NVIDIA's Blackwell product cycle and AI demand could propel the stock to $300 in 2025. The pro side presented compelling arguments about unprecedented demand and ecosystem lock-in, but the anti side effectively countered that NVIDIA's extreme valuation multiples already price in most of the bullish scenario. At a forward P/E exceeding 54x, reaching $300 would require both flawless execution and further multiple expansion, which is historically unlikely for semiconductor stocks. The intensifying competitive landscape from both traditional chip rivals and hyperscaler custom silicon adds meaningful risk to NVIDIA's pricing power. While NVIDIA's fundamental business remains exceptionally strong, the gap between current price levels and $300 requires an optimistic confluence of factors that the valuation constraints make improbable within the 2025 timeframe.

📋 PRO Facts:

• Blackwell production capacity is reportedly sold out for several quarters ahead

• Major hyperscalers are significantly increasing capital expenditure to secure Blackwell chips

• Blackwell architecture delivers approximately 30x inference performance improvements over prior generation

• NVIDIA's CUDA ecosystem creates deep software-hardware integration and developer lock-in

• Sovereign AI initiatives are creating new demand from national governments beyond traditional cloud customers

📋 ANTI Facts:

• NVIDIA trades at a forward P/E ratio of approximately 54.2x, well above the semiconductor sector average of 28.7x

• NVIDIA's own historical average P/E is approximately 42.3x, below current levels

• AMD MI300 series, Intel Gaudi 3, Google TPUs, Amazon Trainium/Inferentia, and Microsoft custom chips all represent competitive alternatives

• NVIDIA's MD&A acknowledges that its competitive position has been harmed by export controls

• Semiconductor manufacturing lead times are historically volatile and subject to disruption

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | google/gemini-3-flash-preview | deepseek/deepseek-v3.2 | 0.160 | 0.206 | 42 | 9 | FALSE | FALSE | 80% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] ASIC — Application-Specific Integrated Circuit — A chip custom-designed for a particular use rather than general-purpose computing, often used in AI inference workloads as a potentially lower-cost alternative to GPUs.

[2] attach rates — The percentage of customers purchasing additional products or accessories alongside a primary product, used here to describe how often networking solutions are sold with GPU servers.

[3] Blackwell — NVIDIA's next-generation GPU architecture succeeding Hopper, featuring the B200 and GB200 chips, designed for significantly improved AI training and inference performance.

[4] capex — capital expenditure — Funds spent by a company to acquire, upgrade, or maintain physical assets such as data centers, equipment, or infrastructure.

[5] CUDA — Compute Unified Device Architecture — NVIDIA's proprietary parallel computing platform and programming model that enables developers to use NVIDIA GPUs for general-purpose computing, creating significant software lock-in.

[6] demand-supply imbalance — A market condition where demand for a product significantly exceeds available supply, typically leading to pricing power and extended order backlogs.

[7] EPS — Earnings Per Share — A company's net profit divided by the number of outstanding shares, used as a key metric for evaluating profitability on a per-share basis.

[8] export controls — Government-imposed restrictions on the sale or transfer of certain technologies to foreign countries, particularly relevant to U.S. restrictions on advanced semiconductor exports to China.

[9] forward P/E ratio — forward price-to-earnings ratio — A valuation metric calculated by dividing the current stock price by projected future earnings per share, used to assess whether a stock is over- or undervalued relative to expected profits.

[10] frontier models — The most advanced and capable AI models at any given time, typically requiring the largest computational resources for training and inference.

[11] full-stack — A technology offering that encompasses all layers of a computing solution, from hardware through software, middleware, and applications.

[12] FY — Fiscal Year — A company's annual accounting period, which may not align with the calendar year. NVIDIA's fiscal year ends in late January.

[13] GB200 — An NVIDIA Blackwell-architecture product combining two B200 GPUs with a Grace CPU, designed for high-performance AI training and inference workloads.

[14] gross margin — The percentage of revenue remaining after subtracting the cost of goods sold, indicating how efficiently a company produces its products.

[15] H100 — NVIDIA's Hopper-architecture GPU widely adopted for AI training and inference in data centers, predecessor to the Blackwell series.

[16] H200 — An enhanced version of NVIDIA's Hopper-architecture GPU with increased memory bandwidth, serving as a bridge product before Blackwell.

[17] hyperscalers — The largest cloud computing providers (e.g., Amazon AWS, Microsoft Azure, Google Cloud) that operate massive-scale data center infrastructure and are major purchasers of AI hardware.

[18] inference — The process of running a trained AI model to generate predictions or outputs from new input data, as opposed to the training phase where the model learns from data.

[19] InfiniBand — A high-speed networking technology used in data centers and supercomputers to connect servers and storage with very low latency, critical for distributed AI training workloads.

[20] law of large numbers — In a business context, the principle that as a company's revenue base grows larger, maintaining high percentage growth rates becomes increasingly difficult.

[21] LLM — Large Language Model — A type of AI model trained on vast amounts of text data to understand and generate human language, such as GPT-4 or Llama 3.

[22] Magnificent Seven — A market term referring to seven dominant U.S. technology stocks (Apple, Microsoft, Alphabet, Amazon, NVIDIA, Meta, Tesla) that have driven a disproportionate share of market returns.

[23] MD&A — Management's Discussion and Analysis — A required section of a company's SEC filings where management provides narrative commentary on financial results, risks, and business outlook.

[24] MI300 — AMD's data center AI accelerator chip series designed to compete with NVIDIA's H100 and Blackwell GPUs for AI training and inference workloads.

[25] NASDAQ — National Association of Securities Dealers Automated Quotations — A major U.S. electronic stock exchange known for listing technology and growth-oriented companies.

[26] NVLink — NVIDIA's proprietary high-bandwidth interconnect technology that enables direct communication between GPUs at speeds far exceeding standard PCIe connections.

[27] P/E — price-to-earnings ratio — A valuation metric calculated by dividing a company's stock price by its earnings per share, indicating how much investors are willing to pay per dollar of earnings.

[28] PEG ratio — price/earnings-to-growth ratio — A valuation metric that divides the P/E ratio by the expected earnings growth rate, with values above 1 suggesting the stock may be overvalued relative to its growth prospects.

[29] Price/Sales ratio — price-to-sales ratio — A valuation metric calculated by dividing a company's market capitalization by its total revenue, used to assess how much investors pay per dollar of sales.

[30] recurring revenue — Revenue that a company can reliably expect to receive on an ongoing basis, typically from subscriptions or software licensing, valued for its predictability.

[31] Sovereign AI — The concept of nations building their own domestic AI computing infrastructure to ensure national security, data sovereignty, and reduced dependence on foreign technology providers.

[32] Spectrum-X — NVIDIA's Ethernet-based networking platform optimized for AI workloads, designed as an alternative to InfiniBand for large-scale AI cluster connectivity.

[33] switching costs — The expenses, effort, and disruption a customer faces when changing from one product or vendor to another, which can create competitive moats for incumbent providers.

[34] TAM — total addressable market — The total revenue opportunity available for a product or service if it achieved 100% market share, used to estimate growth potential.

[35] TCO — Total Cost of Ownership — A financial estimate that includes all direct and indirect costs associated with purchasing and operating a product or system over its entire lifecycle.

[36] TPU — Tensor Processing Unit — Google's custom-designed AI accelerator chip optimized for machine learning workloads, used in Google Cloud as an alternative to NVIDIA GPUs.

[37] valuation re-rating — A shift in the market's willingness to assign a higher or lower valuation multiple to a stock, typically driven by changes in growth expectations or business model perception.

[38] yield issues — Problems in semiconductor manufacturing where a lower-than-expected percentage of chips on a wafer function correctly, reducing production output and increasing costs.

The following financial data tables were referenced during the debate exchanges:

| Metric | FY 2024 Actual | FY 2025 Projected | FY 2026 Projected |

|---|---|---|---|

| Data Center Revenue | $47.5B | $105.4B | $142.8B |

| Gross Margin | 72.7% | 75.2% | 76.5% |

| Earnings Per Share (EPS) | $1.19 | $2.84 | $3.95 |

Legend: Historical and projected financial performance for NVIDIA Corporation. Figures for FY2025 and FY2026 represent consensus estimates based on Blackwell architecture adoption. Source: Internal analysis of sector earnings reports.

</FinancialData>

| Region/Initiative | Estimated Investment (2024-2025) | Primary Hardware Focus |

|---|---|---|

| Middle East (Sovereign) | $12B - $15B | H200 / Blackwell |

| Japan (AI Infrastructure) | $4B - $6B | B200 / Quantum-2 |

| European Sovereign Cloud | $7B - $10B | Grace Blackwell |

Legend: Estimated capital allocation by sovereign entities for domestic AI infrastructure development. Source: Analysis of government procurement and trade data.

</FinancialData>

| Segment | Revenue Contribution (2023) | Revenue Contribution (2025E) |

|---|---|---|

| Compute & Networking | 78% | 86% |

| Software & Services | 2% | 5% |

| Graphics/Gaming | 18% | 8% |

| Auto & Other | 2% | 1% |

Legend: Shift in NVIDIA's revenue mix toward high-margin data center compute, networking, and software services. Source: Sector fundamental research.

</FinancialData>

| Competitor | AI Chip Offering | Launch Year | Target Market |

|---|---|---|---|

| AMD | MI300X/MI325X | 2023-2024 | Data Center AI |

| Intel | Gaudi 3 | 2024 | AI Training/Inference |

| TPU v5 | 2023 | Cloud AI Services | |

| Amazon | Trainium 2 | 2023 | AWS AI Workloads |

| Microsoft | Maia 100 | 2024 (expected) | Azure AI Infrastructure |

Legend: Competitive landscape for AI hardware chips challenging NVIDIA's dominance. Data represents major competitors with significant R&D budgets and market access. Source: company announcements and industry analysis.

</FinancialData>

| Feature | H100 (Hopper) | GB200 (Blackwell) | Improvement Factor |

|---|---|---|---|

| LLM Inference Performance | 1x | 30x | 30.0x |

| Energy Efficiency | 1x | 25x | 25.0x |

| Total Cost of Ownership (TCO) | 1x | 0.05x | 20.0x Reduction |

Legend: Comparison of inference capabilities between Hopper and Blackwell architectures for 1.8T parameter models. Source: Technical specifications and performance benchmarks.

</FinancialData>

| Metric | NVIDIA (NVDA) | Semiconductor Sector Average | NVIDIA Historical Average (5-yr) |

|---|---|---|---|

| Forward P/E Ratio | 54.2x | 28.7x | 42.3x |

| Price/Sales Ratio | 38.5x | 8.2x | 22.1x |

| PEG Ratio (5-yr expected) | 2.1 | 1.4 | 1.8 |

Legend: NVIDIA's current valuation metrics compared to sector peers and its own historical averages. Data as of April 2025. Forward P/E based on consensus estimates for FY2026. Source: Financial market data and analysis.

</FinancialData>

| Growth Driver | Impact on 2025 Valuation | Primary Metric |

|---|---|---|

| Blackwell Adoption | High - Revenue Acceleration | 30x Inference Gain |

| Sovereign AI | Medium - Demand Stability | $25B+ New TAM |

| Software/Networking | High - Margin Expansion | 75%+ Gross Margin |

Legend: Key drivers for NVIDIA's 2025 price target and their respective impact on fundamental valuation. Source: Internal analysis of market trends and technical specifications.

</FinancialData>

| Competitor | Key AI Platform | Software Ecosystem Status | Major Adopters/Partners |

|---|---|---|---|

| AMD | MI300X / MI325X | ROCm 6.0+ with PyTorch/TF support | Microsoft Azure, Google Cloud, Oracle Cloud |

| Intel | Gaudi 3 | Intel Extension for PyTorch, OpenVINO | AWS, Google Cloud, Alibaba Cloud |

| TPU v5 | JAX, TensorFlow native | Google Cloud exclusive | |

| Amazon | Trainium 2 | AWS Neuron SDK, PyTorch/TF support | AWS exclusive |

Legend: Competitive AI hardware alternatives with established software ecosystems and cloud provider adoption as of Q1 2025. Source: Company technical documentation and cloud provider announcements.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.