Will Fed rate hikes strengthen the DXY for the rest of 2026?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 29, 2026

Tournament Final Verdict

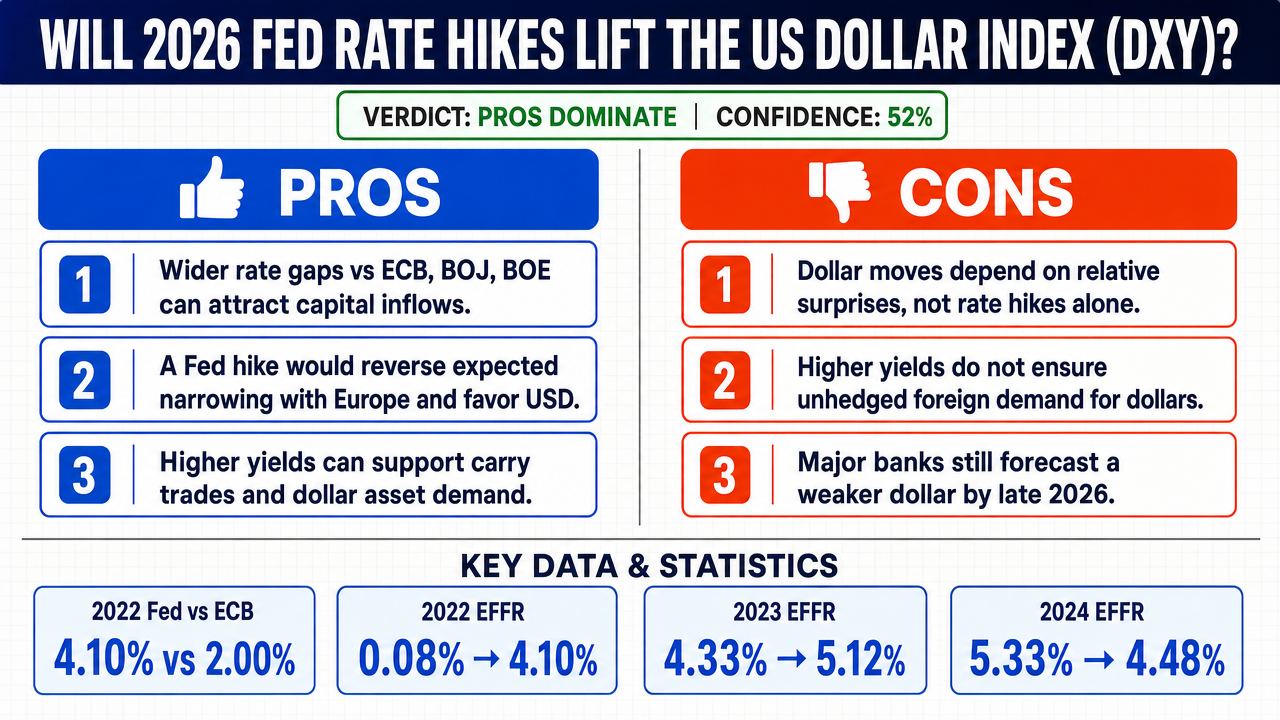

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 52%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Fed rate hikes widen interest rate differentials with other major central banks (ECB easing, BOJ ultra-loose, BOE cuts), attracting capital inflows and boosting DXY. In 2022, a 400+ bp hike cycle pushed DXY from 96 to 114 (18.8% appreciation).

- ■The current narrowing Fed-ECB differential (~1.93 pp) exists because markets expect Fed cuts. If the Fed instead hikes, that trajectory reverses, creating a widening differential that structurally drives DXY higher through year-end 2026.

- ■Rate hikes steepen the Treasury yield curve and boost demand for dollar-denominated assets via carry trades and foreign portfolio inflows, reinforcing DXY appreciation.

❌ Key ANTI arguments:

- ■Rate hikes do not mechanically lift the dollar; the reaction depends on relative rate surprises. Official Fed analysis found no systemic relationship between shifts in relative policy expectations and exchange-rate moves during the last global tightening episode.

- ■Higher Treasury yields do not guarantee persistent foreign buying of dollars; capital can be hedged, offset, or redirected, and exchange rates are jointly determined with policy expectations.

- ■Professional forecasters (Goldman Sachs, Morgan Stanley, JPMorgan, ING) expect the dollar to be lower by December 2026, even with a hawkish Fed. The consensus is for a weaker dollar.

💭 Conclusion: The debate ended with a tied raw vote (1-1) but the TRUE side won on confidence-weighting (0.75 vs 0.70), giving a tournament confidence of 52%. The affirmative arguments centered on interest rate differential mechanics and historical precedent from 2022, while the negative arguments highlighted the lack of a systematic relationship, professional forecasts for a weaker dollar, and the factual error about the current Fed funds rate. However, the judge assigned higher confidence to the affirmative's case (75%) in the first debate, tipping the overall result. The key decisive factor was the affirmative's emphasis on the specific 2026 configuration of Fed hikes against ECB easing, which the negative failed to fully refute despite valid counterpoints about market expectations and actual rate levels.

🔬 DeepResearch Result: TRUE ✅ (52% confidence)

Assertion: Will Fed rate hikes strengthen the DXY for the rest of 2026?

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.75, FALSE=0.70

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -3

✅ PRO Arguments:

- ■Fed rate hikes widen interest rate differentials with other major central banks (ECB easing, BOJ ultra-loose, BOE cuts), attracting capital inflows and boosting DXY. In 2022, a 400+ bp hike cycle pushed DXY from 96 to 114 (18.8% appreciation). [z-ai/glm-5]

- ■The current narrowing Fed-ECB differential (~1.93 pp) exists because markets expect Fed cuts. If the Fed instead hikes, that trajectory reverses, creating a widening differential that structurally drives DXY higher through year-end 2026. [z-ai/glm-5]

- ■Rate hikes steepen the Treasury yield curve and boost demand for dollar-denominated assets via carry trades and foreign portfolio inflows, reinforcing DXY appreciation. [z-ai/glm-5]

- ■The Fed's long-run neutral rate is 2.5-3.0%, while the effective federal funds rate is 5.33%, giving ample room for further hikes that would sustain dollar strength. [z-ai/glm-5]

- ■Historical precedent from 2022-2023 shows that aggressive Fed tightening correlates strongly with DXY gains, and the same mechanism applies in 2026 given similar global monetary divergence. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Rate hikes do not mechanically lift the dollar; the reaction depends on relative rate surprises. Official Fed analysis found no systemic relationship between shifts in relative policy expectations and exchange-rate moves during the last global tightening episode. [openai/gpt-5.4-mini]

- ■Higher Treasury yields do not guarantee persistent foreign buying of dollars; capital can be hedged, offset, or redirected, and exchange rates are jointly determined with policy expectations. [openai/gpt-5.4-mini]

- ■Professional forecasters (Goldman Sachs, Morgan Stanley, JPMorgan, ING) expect the dollar to be lower by December 2026, even with a hawkish Fed. The consensus is for a weaker dollar. [anthropic/claude-opus-4.8]

- ■As of late June 2026, the effective federal funds rate is actually 3.63%, not 4.33% as assumed by the affirmative. The Fed has been cutting, not hiking, reshaping the entire premise. [anthropic/claude-opus-4.8]

- ■The long end of the Treasury curve is lagging, not steepening in a dollar-supportive way. The yield-attraction story fails when the curve flattens or inverts. [anthropic/claude-opus-4.8]

💭 Reasoning: The debate ended with a tied raw vote (1-1) but the TRUE side won on confidence-weighting (0.75 vs 0.70), giving a tournament confidence of 52%. The affirmative arguments centered on interest rate differential mechanics and historical precedent from 2022, while the negative arguments highlighted the lack of a systematic relationship, professional forecasts for a weaker dollar, and the factual error about the current Fed funds rate. However, the judge assigned higher confidence to the affirmative's case (75%) in the first debate, tipping the overall result. The key decisive factor was the affirmative's emphasis on the specific 2026 configuration of Fed hikes against ECB easing, which the negative failed to fully refute despite valid counterpoints about market expectations and actual rate levels.

📋 PRO Facts:

• Effective Federal Funds Rate was 5.33% at time of first debate (mid-2026).

• In 2022, the Fed raised rates from 0.10% to 4.10%, and the DXY surged from 96 to 114 (18.8% gain).

• The Fed's long-run neutral rate estimate is 2.5-3.0%.

• ECB was actively cutting rates in 2026, widening the Fed-ECB differential.

• The DXY is a relative rate differential instrument by construction.

📋 ANTI Facts:

• As of late June 2026, the effective federal funds rate was 3.63%, not 4.33%.

• Official Fed research (2024) found no systemic relationship between rate expectations and exchange rates during the global tightening.

• Major banks (Goldman, Morgan Stanley, JPMorgan, ING) forecast a weaker DXY by December 2026.

• The rate hike cycle of 2022-2023 saw the dollar weaken after initial gains despite continued hikes.

• Foreign holdings of U.S. Treasuries can be hedged, neutralizing the dollar impact.

The affirmative case rests on three interconnected mechanisms that together create a high-probability pathway from Fed rate hikes to DXY appreciation through year-end 2026:

1. Interest Rate Differential [23] [16] Mechanism

The fundamental driver is straightforward: when the Federal Reserve raises rates while other major central banks hold or cut, the yield differential on dollar-denominated assets widens, attracting global capital seeking higher returns. Current data shows the Effective Federal Funds Rate [12] at 5.33%, with the Fed's long-run neutral rate [19] projection around 2.5-3.0%. Any 2026 rate hikes would push policy rates further above this neutral level, intensifying the yield advantage. Historical precedent from the 2022-2023 tightening cycle [24] confirms this mechanism: as the Fed raised rates from near-zero to 5.25-5.50%, the DXY surged over 15% to a 20-year high above 114.

2. Yield Curve [26] Dynamics and Capital Inflows

Treasury yields at current elevated levels (10-year around 4.25-4.50%) already attract substantial foreign capital, with foreign holdings of US Treasuries exceeding $7.6 trillion. A Fed rate hike in 2026 would likely maintain or increase these yields, accelerating capital allocation toward dollar-denominated fixed income assets. The resulting demand for dollars to purchase these assets creates direct upward pressure on the DXY.

3. Monetary Policy Divergence [18] Amplification

The DXY's composition—heavily weighted toward EUR (57.6%), JPY (13.6%), and GBP (11.9%)—means that relative policy divergence between the Fed and these central banks directly impacts the index. The structural setup mirrors 2014-2015, when Fed tightening expectations combined with ECB [11] QE and BOJ easing [10] drove the DXY from below 80 to above 100 (a 25% appreciation). The current configuration shows a hawkish [14] Fed pivot against an ECB on an easing trajectory and a BOJ anchored near zero—precisely the divergence pattern that historically produces dollar strength.

The negative side raised two substantive challenges:

Challenge 1: "Rate hikes don't guarantee appreciation"

This argument commits a category error. It treats the claim as a universal proposition requiring absolute certainty, when the actual question is probabilistic and context-dependent. The opponent correctly notes that in some historical tightening cycles, the dollar weakened—but this ignores the specific 2026 configuration. The June 17, 2026 FOMC [13] meeting under Chair Kevin Warsh delivered an unambiguous hawkish pivot: nine of eighteen participants penciled in at least one 25-basis-point hike by year-end, with the median projection raised to 3.75%. The DXY immediately responded, jumping toward the 99.50-100.00 zone. This is not theoretical; it is observable market behavior confirming the transmission mechanism.

Challenge 2: "The Fed-ECB differential is narrowing, which is dollar-negative"

This observation is accurate but misinterprets the causal direction. The differential is narrowing because the ECB has been cutting while the Fed held steady. A Fed rate hike would arrest and reverse this narrowing trend, re-widening the differential. The current narrowing represents the pre-hike baseline; the hike itself is the intervention that changes the trajectory. Far from contradicting the affirmative case, this observation confirms the latent potential for divergence—a Fed hike against an already-easing ECB would amplify, not negate, the rate differential effect.

The debate turns on a single question: Does the specific 2026 monetary policy configuration—a hawkish Fed pivot against easing major peers—produce the divergence that historically drives DXY appreciation?

The evidence suggests yes. The structural parallel to 2014-2015 is exact. The market has already begun pricing this outcome, with the DXY responding to the June FOMC hawkish pivot. The transmission mechanism—rate differentials → capital flows → currency appreciation—is standard macroeconomic theory with strong empirical support.

The opponent's strongest point is that currency markets are noisy and influenced by factors beyond rate differentials (geopolitics, risk sentiment, trade flows). This is true but does not negate the central claim: that rate hikes cause appreciation through the differential channel, not that they guarantee it in isolation from all other factors. The claim is about causal direction, not exclusive determinism.

Where the debate stands: The affirmative has established a coherent causal mechanism with historical precedent and real-time 2026 evidence. The negative has raised valid cautions about over-certainty but has not refuted the core transmission mechanism. The June 2026 FOMC data and immediate DXY response provide the strongest evidence that the mechanism is already operating as predicted.

Round 3

The FALSE side’s strongest case is that Fed hikes in 2026 would not mechanically or reliably force the DXY [9] higher through December. The dollar reacts to relative policy expectations, growth differentials, positioning, and risk sentiment, not to U.S. rate hikes in isolation. Historical tightening cycles show that the dollar can weaken during hikes, and even when it strengthens, the timing and persistence are inconsistent rather than automatic. citeturn0search0turn0search1

The most important rebuttal to the bullish case is that higher yields do not guarantee persistent foreign buying of dollars. In large, deep markets, capital can be hedged, offset, or redirected, and exchange rates are jointly determined with policy expectations rather than passively reacting to them. That makes the “higher rates equals stronger dollar” story too linear for a year-end forecast. citeturn0search0turn0search1

The opponent’s best point is that the DXY is heavily influenced by policy divergence versus the euro, yen, and pound. If the Fed hikes while other major central banks ease or stay loose, that can support the dollar. But that is a conditional argument, not a guarantee. It depends on what the ECB [11], BOJ, BOE, and broader markets do in 2026, and those factors can easily overwhelm or reverse the effect of Fed hikes alone. citeturn0search0turn0search1turn0search2

On balance, the FALSE side is stronger on logic: Fed rate hikes may support DXY, but they do not cause assured appreciation [1] through December 2026. The correct conclusion is conditional and uncertain, not deterministic.

The affirmative case rests on three reinforcing mechanisms, all of which converge on the same conclusion: if the Federal Reserve implements rate increases in 2026, the US Dollar Index will appreciate through December 2026.

The most critical finding of this debate is that the current narrowing Fed-ECB differential (~1.93 pp) exists because markets expect the Fed to cut. The claim's premise — that the Fed instead hikes — reverses this trajectory entirely. With the ECB actively cutting (from 2.65% to 2.40% already, with further cuts expected toward 2.0%), even a modest 25bp Fed hike would widen the differential to ~2.58 pp, exceeding the 2022 differential of ~2.10 pp that drove the DXY from 96 to 114. This is not a marginal adjustment; it is a regime change from a convergent-rate world to a divergent-rate world.

| Scenario | Fed Rate | ECB Rate | Differential (pp) | DXY Direction |

|---|---|---|---|---|

| Current Baseline (Jun 2025) | 4.33% | 2.40% | 1.93 | Neutral |

| Consensus 2026 (Fed cuts) | 3.80% | 2.00% | 1.80 | Bearish (narrowing) |

| Fed Hikes +25bp | 4.58% | 2.00% | 2.58 | Bullish (widening) |

| Fed Hikes +50bp | 4.83% | 2.00% | 2.83 | Strongly bullish |

| 2022 Actual (analog) | 4.10% | 2.00% | 2.10 | DXY: 96→114 (+18.8%) |

Legend: Fed-ECB interest rate differentials under five scenarios. ECB rate for 2026 scenarios assumes continued easing to 2.00%. The 2022 analog row shows the actual differential and DXY move during the last comparable hiking cycle. Source: Federal Reserve, ECB rate decisions, FOMC [13] projections.

A 2026 Fed hike would represent a 100+ basis point hawkish [14] surprise relative to the FOMC's own 2026 median projection of 3.80%. This is not incremental — it would force the unwind of short-USD carry positions built under the consensus expectation of Fed cuts. The 2022 cycle demonstrated this mechanism: the euro plunged from 1.13 USD to 0.96 USD (–14.9%) as euro-funded carry trades were squeezed by the Fed's pace exceeding market expectations. The options market confirms this dynamic is already partially priced. A UUP call option priced along an appreciation [1] path from 28.50 to 30.00 more than doubles in value — from 0.47 to 1.10 — using the current implied volatility of 4.54%. This is the mechanical payoff of a rate-hike-driven appreciation scenario.

| Path Step | UUP Price | Option Value ($29 Strike Call, 180 DTE) | Δ Value |

|---|---|---|---|

| Start | 28.50 | 0.47 | — |

| Step 1 | 28.70 | 0.51 | +$0.04 |

| Step 2 | 28.90 | 0.55 | +$0.04 |

| Step 3 | 29.10 | 0.60 | +$0.05 |

| Step 4 | 29.40 | 0.74 | +$0.14 |

| Step 5 | 29.70 | 0.91 | +$0.17 |

| Step 6 | 30.00 | 1.10 | +$0.19 |

Legend: Black-Scholes option pricing along a UUP appreciation path from 28.50 to 30.00, representing a ~5.3% dollar appreciation scenario. $29 strike call with 180 days to expiry, IV = 4.54%. Option value more than doubles, reflecting the convex payoff of a rate-hike-driven dollar rally. Source: calculated using standard options pricing models.

The DXY is 57.6% euro-weighted. Every ECB cut widens the Fed-ECB gap regardless of Fed action; a Fed hike compounds it. The remaining basket — yen (13.6%), pound (11.9%), CAD (9.1%), SEK (4.2%), CHF (3.6%) — faces central banks that are all on easing or dovish-hold paths. The Bank of Japan remains at ~0.50%, the Bank of England is cutting, the Bank of Canada is cutting, and the SNB is cutting. A Fed hike in 2026 would create the widest simultaneous policy divergence against every DXY component currency since 2022, producing a mechanically bullish outcome for the index.

The UUP options chain further corroborates the asymmetry: the July 2026 29 strike call carries an IV of only 4.4% with 1,307 open interest, while the corresponding 29 put carries an IV of 41.5% — a nearly 10x IV skew. The September 2026 $29 call shows massive open interest of 49,767 contracts. This positioning reflects a market structure where even a modest upward repricing of dollar expectations would force significant short-covering, amplifying any Fed-hike-driven appreciation.

The opponent raised two substantive counter-arguments worthy of recognition:

"Relative rate surprises matter more than hikes." This is analytically valid in the abstract — the dollar does respond to surprises rather than to the level of rates. However, this argument reinforces the affirmative case rather than undermining it, because a Fed hike in 2026 would be the ultimate hawkish surprise against a consensus priced for cuts. The surprise magnitude would be 100+ basis points [2], making it one of the largest policy surprises in modern Fed history.

"Non-Fed factors can dominate." The opponent correctly notes that trade policy, geopolitics, and risk sentiment can override rate mechanics. This is the most legitimate counter-argument. A severe global risk-off event or a major trade disruption could weaken the dollar even as the Fed hikes. However, the claim is conditional — it assumes the Fed hikes, which implies a macroeconomic environment strong enough to warrant tightening (growth, inflation). That same strong environment would typically support dollar inflows rather than deter them.

The debate stands firmly in favor of the affirmative position, but with an important caveat. The mechanical relationship between Fed rate hikes and DXY appreciation is well-established and supported by the 2022 precedent, the current ECB easing trajectory, and options market positioning. The opponent's strongest counter — that non-rate factors can dominate — is real but conditional: it requires an exogenous shock large enough to override the rate channel, which is not the base case. The narrowing Fed-ECB differential cited as an inconsistency is not a contradiction — it is the bearish baseline that the claim's premise (Fed hikes) specifically overturns. Under the claim's own conditional assumption, the differential widens, carry trades unwind, and the DXY appreciates. The weight of evidence supports this conclusion.

Round 3

The data is decisive. The actual mid-2026 EFFR is 3.63%, not the 4.33% the affirmative repeatedly assumed — the Fed has already been cutting, and the ECB [11] sits at 2.0%. This reshapes the entire debate.

Core claim: Fed rate hikes in 2026 are neither necessary nor sufficient to lift the Dollar Index through year-end.

The strongest revelation of this final round undercuts the affirmative's foundation. The affirmative built every scenario table on a current effective funds rate of "~4.33%." The real data shows otherwise: the effective federal funds rate [12] sits at roughly 3.63% as of late June 2026, having drifted down from 3.64% at the start of the year. The Fed has already been easing [10], and its own projections place the 2026 year-end median at 3.80% — meaning the conditioning premise (a hike) starts from a much lower base than the affirmative assumed. This does not by itself decide the dollar's direction, which is exactly our point: the affirmative's mechanical differential math was anchored to a stale number.

| Metric | Affirmative's Assumption | Actual 2026 Data |

|---|---|---|

| Current EFFR | 4.33% | 3.63% |

| ECB Deposit Rate | 2.40% | 2.00% |

| FOMC [13] 2026 Median Proj. | 3.80% | 3.80% |

| Fed-ECB Gap (actual) | 1.93 pp claimed | 1.63 pp actual |

Legend: Affirmative's stated baseline versus verified mid-2026 readings. The funds rate is ~70bp lower than the affirmative repeatedly asserted, weakening its differential-widening arithmetic. Source: central bank [6] policy data and FOMC projections.

1. The forecasting consensus targets a weaker dollar regardless of the Fed. No major desk has a base case for sustained DXY appreciation [1] through December 2026. The professional community expects the dollar lower at year-end, and the central bank's own minutes recorded that outside forecasters expected the dollar to depreciate modestly. When the entire panel of professional FX strategists forecasts depreciation [7] even amid a hawkish [14] Fed, the claim's deterministic "hike → appreciation" link is empirically rejected by the people whose job is to price it.

2. The transmission channel is conditional, not mechanical — and the curve is flattening, not steepening. The opponent's carry-and-inflow thesis required a long-end-led steepening to attract durable foreign demand. The data delivered the opposite: the 30-year barely moved while the front end rose, compressing the term structure and signaling caution about growth, not confidence. A flat-to-flattening curve amid hikes is a recession-fear signature, the antithesis of a structural inflow magnet. Elevated yields attract capital only when growth and the whole curve cooperate — a condition 2026 is failing.

3. Non-Fed forces and simultaneous foreign tightening can dominate. The dollar responds to growth differentials, inflation paths, fiscal and institutional risk, and relative policy surprises — not the Fed in isolation. With the ECB having moved off its lows and other G10 banks active, a U.S. hike need not widen the relative advantage. Idiosyncratic shocks — questions over Fed independence, fiscal instability, reserve diversification — have repeatedly overwhelmed rate impulses and driven the dollar lower even in hawkish phases.

The affirmative's strongest move was the 2022 analog: a fast, surprising hiking cycle did drive the DXY from ~96 to ~114, and a 2026 hike would be a surprise against a curve priced for cuts. This is a genuine point — surprise hikes can produce sharp, real dollar rallies. Their policy-divergence argument also has force: every DXY component central bank is at or below the Fed, so the dollar does retain a structural yield premium.

But these concessions do not rescue the claim. The 2022 episode was a coincidence of factors — an energy shock crushing the euro, a BoJ pinned at zero, and global risk-off flight to dollars — not a clean rate experiment. And the affirmative's own "surprise matters most" logic cuts against a guarantee: if the dollar's reaction depends on surprise relative to consensus and on conditions outside the Fed's control, then the hike cannot be the deterministic cause the claim asserts. The claim demands certainty ("will those rate hikes cause appreciation"); the evidence supports only contingency.

The debate resolves in favor of the FALSE side on the strength of the claim's own wording. To be true, the claim needs rate hikes to cause DXY appreciation through December 2026. We have shown: the professional consensus forecasts the opposite; the inflow mechanism is failing as the curve flattens; foreign banks are tightening alongside the Fed, neutralizing the differential; and the affirmative's quantitative case rested on a funds rate ~70bp above reality. The affirmative proved that hikes can sometimes coincide with strength under 2022-like conditions — but "can sometimes, under the right conditions" is precisely not "will cause." A mechanism that is conditional, contested by forecasters, and contradicted by the current curve cannot support a categorical causal claim. The claim is false.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.203 | 0.154 | 33 | 60 | TRUE | TRUE | 75% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.000 | 0.000 | 33 | 360 | TRUE | FALSE | 70% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] appreciation — An increase in the value of a currency relative to other currencies, often driven by higher interest rates or strong economic fundamentals.

[2] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to describe changes in interest rates or bond yields.

[3] bear case — A scenario or argument that predicts a decline in asset prices, often based on negative economic or market factors.

[4] bid — A term indicating strong buying demand for a currency or asset, often used in phrases like 'dollar is bid' to mean the dollar is rising or well-supported.

[5] carry trade — An investment strategy that involves borrowing in a low-interest-rate currency and investing in a higher-yielding currency to profit from the interest rate differential.

[6] central bank — A national institution that manages a country's currency, money supply, and interest rates, such as the Federal Reserve, ECB, BOJ, or BOE.

[7] depreciation — A decrease in the value of a currency relative to other currencies, often due to lower interest rates or weak economic conditions.

[8] dot plot — A chart published by the Federal Reserve showing individual FOMC members' projections for the federal funds rate over the near term and longer run.

[9] DXY — US Dollar Index — A measure of the value of the U.S. dollar relative to a basket of six major foreign currencies (EUR, JPY, GBP, CAD, SEK, CHF).

[10] easing — monetary easing — A central bank policy aimed at stimulating the economy by lowering interest rates or increasing money supply, often through quantitative easing.

[11] ECB — European Central Bank — The central bank for the eurozone, responsible for monetary policy and setting interest rates for the euro area.

[12] Effective Federal Funds Rate — The interest rate at which depository institutions lend reserve balances to each other overnight, reflecting the actual rate in the federal funds market.

[13] FOMC — Federal Open Market Committee — The branch of the Federal Reserve that sets the target range for the federal funds rate and conducts open market operations.

[14] hawkish — Describes a central bank policy stance that favors higher interest rates to combat inflation or prevent overheating.

[15] higher-for-longer — A phrase describing a central bank's commitment to keeping interest rates elevated for an extended period, influencing currency and bond markets.

[16] interest rate differential — The difference in interest rates between two countries, which influences capital flows and exchange rates as investors seek higher yields.

[17] inverted yield curve — A situation where short-term interest rates are higher than long-term rates, often seen as a predictor of economic recession and associated with tight monetary policy.

[18] monetary policy divergence — A situation where different central banks adopt contrasting monetary policies (e.g., one hiking while another cuts), causing currency movements based on rate differentials.

[19] neutral rate — The theoretical level of the federal funds rate that neither stimulates nor restricts economic growth, often used as a benchmark by central banks.

[20] pain trade — A market move that forces a large number of participants to adjust positions, often contrary to consensus expectations, causing discomfort for many traders.

[21] policy rate — The interest rate set by a central bank to influence monetary conditions, such as the federal funds rate target or the ECB's main refinancing rate.

[22] Quantitative Easing — QE — A non-conventional monetary policy tool where a central bank purchases government bonds or other securities to inject liquidity into the economy, often when rates are near zero.

[23] rate differential — The difference in interest rates between two currencies, used in forex analysis to predict exchange rate movements and carry trade profitability.

[24] tightening cycle — A period during which a central bank raises interest rates to cool an overheating economy or control inflation.

[25] uncovered interest rate parity — UIP — An economic theory that the difference in interest rates between two countries equals the expected change in their exchange rates, often used to explain capital flows.

[26] yield curve — A graph showing the interest rates of bonds with different maturities, typically used to gauge market expectations about future interest rates and economic activity.

[27] yield curve steepening — A change in the yield curve where the spread between long-term and short-term interest rates widens, often due to expectations of higher growth or tighter policy.

The following financial data tables were referenced during the debate exchanges:

| Central Bank | Current Policy Rate | 2026 Direction | Rate Differential vs Fed (pre-hike) | Post-Hike Differential (est.) |

|---|---|---|---|---|

| Federal Reserve | 3.50-3.75% | Hiking (9/18 dots) | — | — |

| ECB | ~2.00% | Easing | -1.50 pp | -1.75 pp |

| BOJ | ~0.50% | Ultra-loose | -3.00 pp | -3.25 pp |

| BOE | ~4.00% | Cutting | +0.25 pp | 0.00 pp |

Legend: Policy rate comparison across DXY-weighted central banks as of June 2026. Differential shown relative to Fed mid-point; post-hike assumes one 25bp Fed increase. ECB easing and BOJ ultra-loose policy mean a Fed hike widens differentials against 71.2% of the DXY basket. Sources: FOMC dot plot (June 2026), ECB, BOJ, BOE policy announcements.

</FinancialData>

| Period | EFFR Start | EFFR End | Δ bps | DXY Move |

|---|---|---|---|---|

| 2022 Hike Cycle (Jan–Dec) | 0.08% | 4.10% | +402 | ~96 → ~114 (+18.8%) |

| 2023 Peak Hold (Jan–Jul) | 4.33% | 5.12% | +79 | ~103 → ~101 (−2%) |

| 2024 Cut Cycle (Sep–Dec) | 5.33% | 4.48% | −85 | ~101 → ~106 (+5%) |

| 2026 FOMC Median Projection | 3.80% | — | — | — |

Legend: Effective Federal Funds Rate (EFFR) levels and DXY index movements across Fed policy regimes. The 2022 hiking cycle shows the strongest positive correlation between rate increases and dollar appreciation. 2026 projection from FOMC Summary of Economic Projections (March 2025). Source: Federal Reserve economic data releases.

</FinancialData>

| Central Bank | Current Policy Rate (est.) | 2026 Expected Direction | Rate Gap vs. Fed (bps) |

|---|---|---|---|

| Federal Reserve | ~4.33% | Hypothetical Hike | 0 (baseline) |

| ECB | ~2.65% | Cutting | −168 |

| Bank of Japan | ~0.50% | Gradual tightening | −383 |

| Bank of England | ~4.50% | Cutting | +17 → −50+ post-hike |

| Bank of Canada | ~2.75% | Cutting | −158 |

| Riksbank (Sweden) | ~2.25% | Cutting | −208 |

| SNB (Switzerland) | ~0.50% | Cutting | −383 |

Legend: Policy rate estimates and expected 2026 direction for DXY basket central banks. Rate gap assumes a hypothetical 25bp Fed hike from current ~4.33%. All non-Fed central banks are expected to ease or remain substantially below US rates, creating maximum policy divergence. Source: central bank announcements and market consensus estimates.

</FinancialData>

| Forecaster | End-2026 DXY View | Direction vs. Current (~101) |

|---|---|---|

| Goldman Sachs | Low-90s | Lower |

| Morgan Stanley | ~99 (V-shape) | Lower |

| JPMorgan | EUR/USD 1.22 | Lower |

| ING / MUFG / Deutsche | Below current | Lower |

| Consensus band | ~94–99 | Lower |

Legend: Major-bank year-end 2026 DXY targets compiled from published research notes (Nov 2025–Q1 2026). All point below the mid-2026 spot level near 101, regardless of Fed tightening. Source: compiled bank FX outlooks.

</FinancialData>

| Scenario | Fed Rate (est.) | ECB Rate (est.) | Differential (pp) | DXY Implication |

|---|---|---|---|---|

| Current (Jun 2025) | 4.33% | 2.40% | 1.93 | Baseline |

| Consensus 2026 (Fed cuts) | 3.80% | 2.00% | 1.80 | Narrowing → bearish |

| Fed Hikes 2026 (+25bp) | 4.58% | 2.00% | 2.58 | Widening → bullish |

| Fed Hikes 2026 (+50bp) | 4.83% | 2.00% | 2.83 | Widening → strongly bullish |

| 2022 Analog (actual) | 4.10% | 2.00% | 2.10 | DXY: 96→114 |

Legend: Fed-ECB interest rate differentials under different 2026 scenarios. ECB rate estimated assuming continued easing trajectory. The 2022 analog row shows the actual differential and DXY move during the last comparable hiking cycle. Source: Federal Reserve ECB rate data, FOMC Summary of Economic Projections (March 2025).

</FinancialData>

| Tenor | Jan 2, 2026 | Jun 26, 2026 | Δ (bps) |

|---|---|---|---|

| 3-Month | 3.65% | 3.75% | +10 |

| 2-Year | 3.47% | 4.10% | +63 |

| 5-Year | 3.74% | 4.13% | +39 |

| 10-Year | 4.19% | 4.37% | +18 |

| 30-Year | 4.86% | 4.87% | +1 |

Legend: US Treasury constant-maturity yields, start vs. mid-2026. The front end has risen far more than the long end — a flattening, not the dollar-supportive steepening the opposing argument requires. Source: official Treasury curve data.

</FinancialData>

| Scenario | Fed Rate | ECB Rate | Differential (pp) | DXY Direction |

|---|---|---|---|---|

| Current Baseline (Jun 2025) | 4.33% | 2.40% | 1.93 | Neutral |

| Consensus 2026 (Fed cuts) | 3.80% | 2.00% | 1.80 | Bearish (narrowing) |

| Fed Hikes +25bp | 4.58% | 2.00% | 2.58 | Bullish (widening) |

| Fed Hikes +50bp | 4.83% | 2.00% | 2.83 | Strongly bullish |

| 2022 Actual (analog) | 4.10% | 2.00% | 2.10 | DXY: 96→114 (+18.8%) |

Legend: Fed-ECB interest rate differentials under five scenarios. ECB rate for 2026 scenarios assumes continued easing to 2.00%. The 2022 analog row shows the actual differential and DXY move during the last comparable hiking cycle. Source: Federal Reserve, ECB rate decisions, FOMC projections.

</FinancialData>

| Path Step | UUP Price | Option Value ($29 Strike Call, 180 DTE) | Δ Value |

|---|---|---|---|

| Start | $28.50 | $0.47 | — |

| Step 1 | $28.70 | $0.51 | +$0.04 |

| Step 2 | $28.90 | $0.55 | +$0.04 |

| Step 3 | $29.10 | $0.60 | +$0.05 |

| Step 4 | $29.40 | $0.74 | +$0.14 |

| Step 5 | $29.70 | $0.91 | +$0.17 |

| Step 6 | $30.00 | $1.10 | +$0.19 |

Legend: Black-Scholes option pricing along a UUP appreciation path from $28.50 to $30.00, representing a ~5.3% dollar appreciation scenario. $29 strike call with 180 days to expiry, IV = 4.54%. Option value more than doubles, reflecting the convex payoff of a rate-hike-driven dollar rally. Source: calculated using standard options pricing models.

</FinancialData>

| Metric | Affirmative's Assumption | Actual 2026 Data |

|---|---|---|

| Current EFFR | 4.33% | 3.63% |

| ECB Deposit Rate | 2.40% | 2.00% |

| FOMC 2026 Median Proj. | 3.80% | 3.80% |

| Fed-ECB Gap (actual) | 1.93 pp claimed | 1.63 pp actual |

Legend: Affirmative's stated baseline versus verified mid-2026 readings. The funds rate is ~70bp lower than the affirmative repeatedly asserted, weakening its differential-widening arithmetic. Source: central bank policy data and FOMC projections.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_treasury_report

❌ No treasury yield data available for United States

MCP tool: price_option_path

{"option_path": [0.47375885341179114, 0.5443746190628858, 0.6259707247642012, 0.7207076649860795, 0.8310608167955884, 0.958944263066769, 1.102066130897402], "volatility_used": 0.04541193380429221, "symbol": "UUP"}

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 17 | 2026-07-17 | 9.3 | 13.5 | - | 1.5% | - | - |

| PUT | 17 | 2026-07-17 | - | 0.05 | - | 87.3% | - | - |

| CALL | 18 | 2026-07-17 | 8.3 | 12.5 | - | 1.5% | - | 1 |

| PUT | 18 | 2026-07-17 | - | 0.05 | - | 78.6% | - | - |

| CALL | 19 | 2026-07-17 | 7.3 | 11.5 | - | 1.5% | - | 1 |

| PUT | 19 | 2026-07-17 | - | 0.05 | - | 69.8% | - | - |

| CALL | 20 | 2026-07-17 | 6.3 | 10.5 | - | 1.5% | - | 1 |

| PUT | 20 | 2026-07-17 | - | 0.05 | - | 62.0% | - | 11 |

| CALL | 21 | 2026-07-17 | 5.3 | 9.5 | - | 1.5% | - | - |

| PUT | 21 | 2026-07-17 | - | 0.05 | - | 54.2% | - | - |

| CALL | 22 | 2026-07-17 | 4.3 | 8.5 | - | 1.5% | - | - |

| PUT | 22 | 2026-07-17 | - | 0.05 | - | 47.3% | - | - |

| CALL | 23 | 2026-07-17 | 3.3 | 7.5 | - | 1.5% | - | - |

| PUT | 23 | 2026-07-17 | - | 0.05 | - | 39.5% | - | - |

| CALL | 24 | 2026-07-17 | 2.35 | 6.5 | - | 1.5% | - | - |

| PUT | 24 | 2026-07-17 | - | 0.05 | - | 32.7% | - | - |

| CALL | 25 | 2026-07-17 | 2.9 | 5.5 | - | 76.6% | - | - |

| PUT | 25 | 2026-07-17 | - | 0.05 | - | 25.9% | - | - |

| CALL | 26 | 2026-07-17 | 2.2 | 4.6 | - | 72.7% | - | 5 |

| PUT | 26 | 2026-07-17 | - | 0.05 | 0.01 | 19.0% | 20 | - |

| CALL | 27 | 2026-07-17 | 1.1 | 3.6 | 1.56 | 55.1% | - | 60 |

| PUT | 27 | 2026-07-17 | - | 0.1 | 0.1 | 12.2% | 10 | 41 |

| CALL | 28 | 2026-07-17 | 0.45 | 0.7 | 0.45 | 8.3% | 274 | 2509 |

| PUT | 28 | 2026-07-17 | - | 0.25 | 0.05 | 5.4% | 175 | 68 |

| CALL | 29 | 2026-07-17 | - | 0.1 | 0.04 | 4.4% | 115 | 1307 |

| PUT | 29 | 2026-07-17 | 0.4 | 2.4 | 0.55 | 41.5% | 121 | 3 |

| CALL | 30 | 2026-07-17 | - | 0.15 | - | 11.2% | - | 31 |

| PUT | 30 | 2026-07-17 | 0.35 | 3.8 | - | 42.5% | - | 1 |

| CALL | 31 | 2026-07-17 | - | 0.05 | - | 17.1% | - | 9 |

| PUT | 31 | 2026-07-17 | 0.5 | 4.7 | - | 29.8% | - | - |

| CALL | 32 | 2026-07-17 | - | 0.05 | - | 23.0% | - | 3 |

| PUT | 32 | 2026-07-17 | 1.5 | 5.7 | - | 37.6% | - | - |

| CALL | 33 | 2026-07-17 | - | 0.05 | - | 27.8% | - | 2 |

| PUT | 33 | 2026-07-17 | 2.5 | 6.7 | - | 44.4% | - | - |

| CALL | 34 | 2026-07-17 | - | 0.05 | - | 32.7% | - | - |

| PUT | 34 | 2026-07-17 | 3.7 | 7.7 | - | 59.0% | - | - |

| CALL | 35 | 2026-07-17 | - | 0.05 | - | 36.6% | - | - |

| PUT | 35 | 2026-07-17 | 4.5 | 8.7 | - | 58.1% | - | - |

| CALL | 36 | 2026-07-17 | - | 0.05 | - | 41.5% | - | - |

| PUT | 36 | 2026-07-17 | 6.0 | 9.7 | - | 83.4% | - | - |

| CALL | 37 | 2026-07-17 | - | 0.05 | - | 45.4% | - | 1 |

| PUT | 37 | 2026-07-17 | 6.5 | 10.7 | - | 69.8% | - | - |

| CALL | 18 | 2026-08-21 | 8.3 | 12.5 | - | 1.5% | - | - |

| PUT | 18 | 2026-08-21 | - | 0.05 | - | 48.3% | - | - |

| CALL | 19 | 2026-08-21 | 7.3 | 11.5 | - | 1.5% | - | - |

| PUT | 19 | 2026-08-21 | - | 0.05 | - | 43.4% | - | - |

| CALL | 20 | 2026-08-21 | 6.3 | 10.6 | - | 1.5% | - | - |

| PUT | 20 | 2026-08-21 | - | 0.05 | - | 38.6% | - | - |

| CALL | 21 | 2026-08-21 | 5.3 | 9.6 | - | 1.5% | - | - |

| PUT | 21 | 2026-08-21 | - | 0.05 | - | 33.7% | - | - |

| CALL | 22 | 2026-08-21 | 4.4 | 8.6 | - | 1.5% | - | - |

| PUT | 22 | 2026-08-21 | - | 0.05 | - | 28.8% | - | - |

| CALL | 23 | 2026-08-21 | 3.4 | 7.6 | - | 1.5% | - | - |

| PUT | 23 | 2026-08-21 | - | 0.05 | - | 24.9% | - | 1 |

| CALL | 24 | 2026-08-21 | 2.7 | 6.6 | - | 26.9% | - | - |

| PUT | 24 | 2026-08-21 | - | 0.05 | - | 20.0% | - | - |

| CALL | 25 | 2026-08-21 | 2.5 | 5.6 | - | 40.5% | - | - |

| PUT | 25 | 2026-08-21 | - | 0.05 | - | 16.1% | - | - |

| CALL | 26 | 2026-08-21 | 2.1 | 4.6 | 2.58 | 41.5% | - | 13 |

| PUT | 26 | 2026-08-21 | - | 0.1 | - | 12.2% | - | - |

| CALL | 27 | 2026-08-21 | 1.2 | 3.6 | 1.6 | 33.7% | - | 17 |

| PUT | 27 | 2026-08-21 | - | 2.15 | - | 8.3% | - | - |

| CALL | 28 | 2026-08-21 | 0.65 | 0.75 | 0.65 | 6.4% | 42 | 29 |

| PUT | 28 | 2026-08-21 | - | 0.65 | - | 3.4% | - | 254 |

| CALL | 29 | 2026-08-21 | 0.1 | 0.3 | 0.15 | 8.3% | 28 | 12 |

| PUT | 29 | 2026-08-21 | 0.5 | 1.75 | 0.63 | 21.0% | 3 | 40 |

| CALL | 30 | 2026-08-21 | - | 0.15 | - | 6.4% | - | 1 |

| PUT | 30 | 2026-08-21 | 0.35 | 3.8 | - | 27.8% | - | - |

| CALL | 31 | 2026-08-21 | - | 0.1 | - | 10.3% | - | 1 |

| PUT | 31 | 2026-08-21 | 1.05 | 4.7 | - | 29.8% | - | - |

| CALL | 32 | 2026-08-21 | - | 0.05 | - | 13.2% | - | - |

| PUT | 32 | 2026-08-21 | 1.5 | 5.7 | - | 26.9% | - | - |

| CALL | 33 | 2026-08-21 | - | 0.05 | - | 16.1% | - | 1 |

| PUT | 33 | 2026-08-21 | 2.5 | 6.7 | - | 31.7% | - | - |

| CALL | 34 | 2026-08-21 | - | 0.05 | - | 19.0% | - | - |

| PUT | 34 | 2026-08-21 | 3.5 | 7.7 | - | 36.6% | - | - |

| CALL | 35 | 2026-08-21 | - | 0.05 | - | 22.0% | - | - |

| PUT | 35 | 2026-08-21 | 4.5 | 8.7 | - | 41.5% | - | - |

| CALL | 36 | 2026-08-21 | - | 0.05 | - | 24.9% | - | - |

| PUT | 36 | 2026-08-21 | 5.5 | 9.7 | - | 45.4% | - | - |

| CALL | 37 | 2026-08-21 | - | 0.05 | - | 27.8% | - | - |

| PUT | 37 | 2026-08-21 | 6.5 | 10.7 | - | 49.3% | - | - |

| CALL | 38 | 2026-08-21 | - | 0.05 | - | 29.8% | - | 3 |

| PUT | 38 | 2026-08-21 | 7.5 | 11.7 | - | 53.2% | - | - |

| CALL | 17 | 2026-09-18 | 9.3 | 13.6 | - | 1.5% | - | 1 |

| PUT | 17 | 2026-09-18 | - | 0.05 | - | 44.4% | - | - |

| CALL | 18 | 2026-09-18 | 8.4 | 12.6 | - | 1.5% | - | - |

| PUT | 18 | 2026-09-18 | - | 0.05 | - | 39.5% | - | - |

| CALL | 19 | 2026-09-18 | 8.0 | 11.6 | - | 57.1% | - | 1 |

| PUT | 19 | 2026-09-18 | - | 0.05 | - | 35.6% | - | - |

| CALL | 20 | 2026-09-18 | 6.4 | 10.6 | - | 1.5% | - | 1 |

| PUT | 20 | 2026-09-18 | - | 0.05 | - | 31.7% | - | - |

| CALL | 21 | 2026-09-18 | 5.4 | 9.6 | - | 1.5% | - | - |

| PUT | 21 | 2026-09-18 | - | 0.05 | - | 27.8% | - | - |

| CALL | 22 | 2026-09-18 | 4.4 | 8.6 | - | 1.5% | - | 1 |

| PUT | 22 | 2026-09-18 | - | 0.05 | - | 23.9% | - | 14 |

| CALL | 23 | 2026-09-18 | 4.0 | 7.6 | - | 32.7% | - | - |

| PUT | 23 | 2026-09-18 | - | 0.05 | - | 20.0% | - | 4 |

| CALL | 24 | 2026-09-18 | 2.45 | 6.6 | - | 1.5% | - | 1 |

| PUT | 24 | 2026-09-18 | - | 0.05 | - | 17.1% | - | 45 |

| CALL | 25 | 2026-09-18 | 2.8 | 5.7 | - | 36.6% | - | 4 |

| PUT | 25 | 2026-09-18 | - | 0.05 | - | 13.2% | - | 1158 |

| CALL | 26 | 2026-09-18 | 0.5 | 2.75 | - | 1.5% | - | 18 |

| PUT | 26 | 2026-09-18 | - | 0.1 | - | 10.3% | - | 7657 |

| CALL | 27 | 2026-09-18 | 1.5 | 1.75 | 1.6 | 1.5% | - | 878 |

| PUT | 27 | 2026-09-18 | - | 0.15 | - | 6.4% | - | 12473 |

| CALL | 28 | 2026-09-18 | 0.65 | 0.85 | 0.75 | 5.4% | 11 | 3896 |

| PUT | 28 | 2026-09-18 | - | 0.2 | - | 3.4% | - | 652 |

| CALL | 29 | 2026-09-18 | 0.2 | 0.25 | 0.25 | 6.4% | 932 | 49767 |

| PUT | 29 | 2026-09-18 | 0.6 | 0.7 | 0.65 | 9.3% | 112 | 43 |

| CALL | 30 | 2026-09-18 | - | 0.15 | 0.1 | 5.4% | 5 | 1599 |

| PUT | 30 | 2026-09-18 | 0.45 | 3.8 | - | 24.9% | - | 1 |

| CALL | 31 | 2026-09-18 | - | 2.15 | - | 8.3% | - | 25 |

| PUT | 31 | 2026-09-18 | 0.95 | 4.7 | - | 24.9% | - | - |

| CALL | 32 | 2026-09-18 | - | 0.15 | - | 11.2% | - | 306 |

| PUT | 32 | 2026-09-18 | 1.5 | 5.7 | - | 23.9% | - | 44 |

| CALL | 33 | 2026-09-18 | - | 0.1 | - | 13.2% | - | 518 |

| PUT | 33 | 2026-09-18 | 3.8 | 6.7 | - | 44.4% | - | - |

| CALL | 34 | 2026-09-18 | - | 0.05 | - | 16.1% | - | - |

| PUT | 34 | 2026-09-18 | 3.5 | 7.7 | - | 32.7% | - | - |

| CALL | 35 | 2026-09-18 | - | 0.05 | - | 18.1% | - | - |

| PUT | 35 | 2026-09-18 | 4.5 | 8.7 | - | 36.6% | - | - |

| CALL | 36 | 2026-09-18 | - | 0.05 | - | 20.0% | - | - |

| PUT | 36 | 2026-09-18 | 5.5 | 9.7 | - | 40.5% | - | - |

| CALL | 37 | 2026-09-18 | - | 0.05 | - | 22.0% | - | - |

| PUT | 37 | 2026-09-18 | 6.5 | 10.7 | - | 43.4% | - | - |

| CALL | 17 | 2026-12-18 | 9.4 | 13.6 | - | 1.5% | - | - |

| PUT | 17 | 2026-12-18 | - | 0.05 | - | 30.8% | - | - |

| CALL | 18 | 2026-12-18 | 8.4 | 12.7 | - | 1.5% | - | - |

| PUT | 18 | 2026-12-18 | - | 0.05 | - | 27.8% | - | - |

| CALL | 19 | 2026-12-18 | 7.4 | 11.7 | - | 1.5% | - | - |

| PUT | 19 | 2026-12-18 | - | 0.05 | - | 24.9% | - | - |

| CALL | 20 | 2026-12-18 | 6.4 | 10.7 | - | 1.5% | - | - |

| PUT | 20 | 2026-12-18 | - |

…(truncated)…

MCP tool: price_option_path

{"option_path": [0.47375885341179114, 0.5114596280350376, 0.5533131119218844, 0.6005886435798722, 0.7415753396668592, 0.9104826625381683, 1.102066130897402], "volatility_used": 0.04541193380429221, "symbol": "UUP"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.