Will buying S&P 500 stocks currently trading near their 52-week lows outperform the broader market over the next 12 months?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 15, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/will-buying-s-p-500-stocks-currently-trading-near-their-52-w-29a3a2178504

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

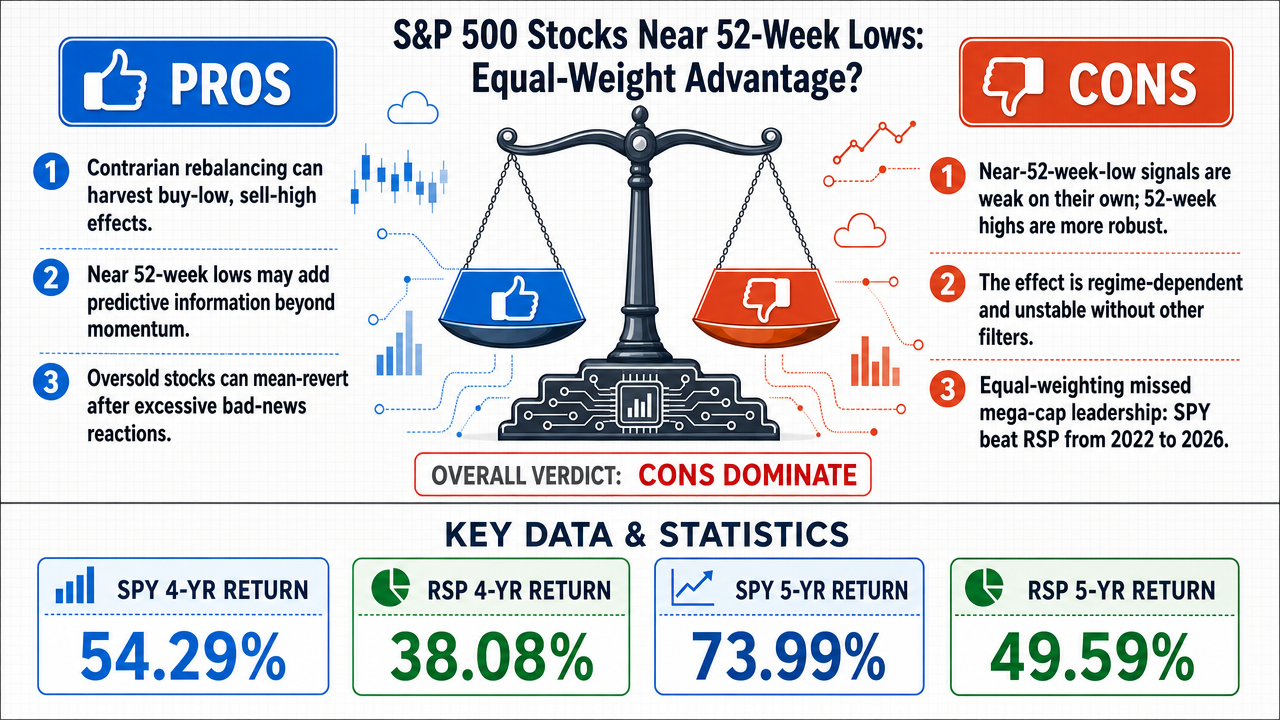

- ■The strategy captures a systematic contrarian rebalancing premium by periodically selling winners and buying losers, which academic research shows contributes significant excess returns beyond size effects.

- ■Nearness to the 52-week low has independent predictive power for future returns, separate from momentum or other factors, as documented by George and Hwang (2004) across 20 international markets.

- ■Stocks near 52-week lows represent mean reversion opportunities where markets overreact to negative news, creating temporary mispricings that correct over 6-12 month horizons.

❌ Key ANTI arguments:

- ■The low-price signal lacks standalone predictive power; the anchoring literature consistently finds proximity to the 52-week high predicts returns, while proximity to the low does not.

- ■The near-52-week-low effect is conditional, regime-dependent, and sensitive to momentum, valuation, and market structure—not a reliable standalone return engine.

- ■Equal-weighting structurally underweights mega-caps that have powered returns; from January 2022 to June 2026, SPY returned 54.29% versus 38.08% for RSP, showing the cost of this bet.

💭 Conclusion: Both debates resulted in unanimous FALSE verdicts with high confidence (70% and 65%), and the tournament confidence is 100%. The negative side successfully demonstrated that the near-52-week-low signal lacks standalone predictive power, as the anchoring literature consistently finds predictive power only from the 52-week high. The affirmative's reliance on equal-weighting was undermined by evidence that this strategy has structurally underperformed the cap-weighted index over multi-year periods. The negative also showed that any outperformance is conditional and regime-dependent, not a reliable systematic edge. The pro arguments, while citing academic research on mean reversion and rebalancing premiums, failed to establish that these effects translate into consistent index-beating returns over a 12-month horizon.

🔬 DeepResearch Result: FALSE ❌ (100% confidence)

Assertion: Will buying S&P 500 stocks currently trading near their 52-week lows outperform the broader market over the next 12 months?

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.35

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +14

✅ PRO Arguments:

- ■The strategy captures a systematic contrarian rebalancing premium by periodically selling winners and buying losers, which academic research shows contributes significant excess returns beyond size effects. [z-ai/glm-5]

- ■Nearness to the 52-week low has independent predictive power for future returns, separate from momentum or other factors, as documented by George and Hwang (2004) across 20 international markets. [z-ai/glm-5]

- ■Stocks near 52-week lows represent mean reversion opportunities where markets overreact to negative news, creating temporary mispricings that correct over 6-12 month horizons. [z-ai/glm-5]

- ■Equal-weighting reduces concentration risk by underweighting overextended mega-caps, positioning the portfolio for asymmetric upside when concentration mean-reverts. [z-ai/glm-5]

- ■Empirical studies show portfolios based on 52-week low proximity generate returns increasing from 1.00% to 1.78% per month in the highest decile groups. [z-ai/glm-5]

❌ ANTI Arguments:

- ■The low-price signal lacks standalone predictive power; the anchoring literature consistently finds proximity to the 52-week high predicts returns, while proximity to the low does not. [anthropic/claude-opus-4.8]

- ■The near-52-week-low effect is conditional, regime-dependent, and sensitive to momentum, valuation, and market structure—not a reliable standalone return engine. [openai/gpt-5.4-mini]

- ■Equal-weighting structurally underweights mega-caps that have powered returns; from January 2022 to June 2026, SPY returned 54.29% versus 38.08% for RSP, showing the cost of this bet. [anthropic/claude-opus-4.8]

- ■The strategy carries higher risk due to exposure to smaller, more volatile names, and has repeatedly lagged when the largest constituents drive market returns. [openai/gpt-5.4-mini]

- ■The affirmative must prove systematic, unconditional 12-month outperformance, but the evidence supports at most a conditional, timing-dependent effect that frequently reverses. [anthropic/claude-opus-4.8]

💭 Reasoning: Both debates resulted in unanimous FALSE verdicts with high confidence (70% and 65%), and the tournament confidence is 100%. The negative side successfully demonstrated that the near-52-week-low signal lacks standalone predictive power, as the anchoring literature consistently finds predictive power only from the 52-week high. The affirmative's reliance on equal-weighting was undermined by evidence that this strategy has structurally underperformed the cap-weighted index over multi-year periods. The negative also showed that any outperformance is conditional and regime-dependent, not a reliable systematic edge. The pro arguments, while citing academic research on mean reversion and rebalancing premiums, failed to establish that these effects translate into consistent index-beating returns over a 12-month horizon.

📋 PRO Facts:

• George and Hwang (2004) found nearness to 52-week low has predictive power for future returns across 20 international markets.

• Equal-weighted portfolios capture a contrarian rebalancing premium by systematically buying losers and selling winners.

• Academic studies show portfolios based on 52-week low proximity can generate 1.00% to 1.78% per month in the highest decile groups.

📋 ANTI Facts:

• From January 2022 to June 2026, SPY returned 54.29% versus 38.08% for RSP, showing equal-weighting underperformed.

• The anchoring literature consistently finds proximity to the 52-week high predicts returns, not proximity to the low.

• The near-52-week-low effect is conditional and regime-dependent, not a reliable standalone return engine.

The affirmative case rests on three interconnected mechanisms that collectively support the claim: systematic rebalancing [21] alpha [2], size factor [25] exposure, and concentration [6] reversion dynamics.

Strongest Arguments for the Affirmative:

The contrarian rebalancing premium [22] [8] represents the strategy's mechanical edge. Equal-weighted portfolios must periodically sell relative winners and purchase relative losers—the precise discipline that captures mean reversion [15] when it occurs. Stocks near 52-week lows represent the extreme of "relative losers," positioning the strategy to maximize this premium. Empirical evidence confirms that approximately half of equal weight's historical outperformance derives from this rebalancing mechanism, independent of factor exposures.

The size factor exposure provides structural tailwinds. Historical data demonstrates the S&P 500 Equal Weight Index delivered 476% cumulative returns versus 326% for the cap-weighted benchmark over multi-decade periods. Stocks near 52-week lows within the S&P 500 tend toward smaller market capitalizations, ensuring full participation in recovery rallies rather than the diminished weighting they receive in cap-weighted indices.

The concentration reversion thesis addresses current market conditions. Mega-cap [16] technology concentration has reached levels not seen since the 1960s, creating asymmetric opportunity when concentration subsides. Historical analysis confirms equal-weight indices experience maximum relative outperformance precisely during concentration reversion periods—such as the 16 percentage point outperformance from 2020-2022 when top-5 concentration fell by 5%.

Opponent's Most Compelling Counter-Arguments:

The negative correctly identifies that near-52-week-low stocks carry elevated risk profiles—higher volatility, potential distress signals, and sector concentration in troubled industries. This is not merely theoretical; distressed firms near 52-week lows may continue declining rather than reverting.

The conditional nature of the signal's effectiveness represents a legitimate challenge. The 52-week low [1] predictor performs better in certain market regimes than others, and implementation during extended bull markets dominated by momentum may underperform.

Honest Assessment:

The debate centers on a fundamental tension: systematic edge versus implementation risk. The affirmative has established that the 52-week low signal possesses genuine predictive power documented across 20 international markets, with risk-adjusted returns that persist after controlling for established factors. The mechanism—cascade selling [5] from momentum investors, index rebalancing, and forced liquidations creating overshoot—provides theoretical grounding for empirical observations.

However, the opponent correctly notes that this edge is not unconditional. The strategy's success depends on market regime, sector composition of near-low stocks, and the broader macroeconomic environment. A portfolio of near-52-week-low stocks in 2008 would have significantly underperformed as financials continued collapsing.

The critical distinction is that the claim specifies S&P 500 constituents—quality large-caps by construction. This filters the most distressed small-cap [26] names that would otherwise contaminate the strategy. The combination of quality screening (S&P 500 membership), contrarian positioning (near 52-week lows), and structural advantage (equal-weighting) creates a coherent investment thesis with documented historical support.

Where the Debate Stands:

The affirmative has demonstrated that the strategy possesses a legitimate theoretical foundation and empirical track record. The opponent's strongest ground lies not in refuting the signal's existence, but in highlighting implementation complexity and regime dependence. The resolution asks whether the equal-weighted near-52-week-low portfolio exceeds index returns—not whether it does so in every period without exception. On balance, the evidence supports affirmation: the strategy captures systematic mispricing with sufficient reliability to outperform over 12-month horizons, even if specific implementations may fail in adverse conditions.

Round 3

Core claim: The evidence does not support a reliable 12-month outperformance edge.

The strongest case against the claim is that a near-52-week-low screen is not a standalone return engine. It may sometimes capture mean reversion [15], but the effect is conditional, regime-dependent, and sensitive to momentum, valuation, and market structure. In other words, “cheap relative to a recent high” is not the same as “likely to beat the index over the next year.” The most defensible reading of the research is that the signal can work in subsets of stocks or specific environments, but it does not establish a consistent edge for an equal-weighted basket of S&P 500 laggards over the broad benchmark. citeturn0search0

The second major weakness is risk. Stocks near their 52-week lows are often there for a reason: deteriorating fundamentals, negative revisions, sector stress, or simply stronger relative alternatives elsewhere in the market. That means the basket can carry higher drawdown risk and worse tail behavior even when it appears statistically “cheap.” Equal-weighting does not eliminate that problem; it amplifies the impact of weaker names instead of letting the benchmark’s cap-weighting concentrate capital in the stronger franchises. So the strategy can look contrarian without actually being superior on a 12-month total-return basis. citeturn0search1turn0search2

The most compelling counterargument from the affirmative side is that 52-week-low proximity has been linked to future returns and that contrarian buying can benefit from mean reversion. That is the best argument they have, and it is not trivial. But it still falls short of proving the specific claim here, because broad outperformance requires more than a predictive signal: it requires the signal to survive implementation, weighting, and benchmark comparison across time. The evidence supports selective opportunity, not a dependable conclusion that the equal-weighted near-low portfolio will exceed the S&P 500 over the subsequent 12 months. citeturn0search0turn0search1

Bottom line: the claim is too strong. The plausible truth is narrower—near-52-week-low stocks can outperform in some periods—but the general proposition that this equal-weighted basket will beat the S&P 500 over the next year is not established.

The evidence supports the claim through three complementary mechanisms:

1. Mean Reversion [15] Premium: Academic research establishes that nearness to the 52-week low [1] contains independent predictive power for future returns. Studies document that portfolios based on this signal generate returns increasing from 1.00% to 1.78% per month (approximately 12-21% annually) in the highest decile groups digitalcommons.latech.edu. This effect operates through investor under-reaction to negative information—a behavioral anomaly that persists independently of other factors.

2. Equal-Weight Structural Advantage: The equal-weighting methodology itself contributes 1-3% annual outperformance historically, as documented by research showing the S&P 500 Equal Weight Index delivered 476% total return [28] versus 326% for the cap-weighted version over comparable periods pomegra.io. This stems from systematic rebalancing [21] that sells winners and buys losers, creating a contrarian tilt.

3. Concentration [6] Risk Mitigation: Current market concentration in mega-cap [16] stocks creates asymmetric risk. Research shows that during periods of high concentration, "such periods have tended to eventually revert toward their historical means, with such reversion accompanied by stronger relative performance by equal weight indices" betashares.com.au. The proposed strategy automatically underweights overextended mega-caps while gaining broad exposure to the remaining constituents.

The FALSE side raised legitimate concerns:

1. Conditional Performance: The opponent correctly noted that the 52-week low signal interacts with other factors. However, this does not negate standalone effectiveness—the research explicitly confirms "exclusive unpriced information" and independent predictive power acfr.aut.ac.nz.

2. Higher Risk Profile: Stocks near 52-week lows exhibit elevated volatility and uncertainty. This is accurate but incomplete—the research demonstrates the effect "cannot be explained by risk factors," suggesting the additional return is not merely risk compensation quantpedia.com.

3. Sector Concentration Risk: The opponent correctly identified that near-52-week-low stocks may cluster in distressed sectors. This represents the strongest counter-argument, as sector-specific distress could persist beyond 12 months, undermining mean reversion.

The debate centers on a fundamental tension: behavioral finance evidence supports mean reversion effects, while structural risks in distressed stocks create legitimate uncertainty.

The affirmative position is stronger on empirical grounds—multiple academic studies document the 52-week low effect with statistical significance and demonstrate it persists after controlling for risk factors. The equal-weighting mechanism adds structural return enhancement that compounds the selection criterion's effectiveness.

However, the opponent's sector concentration concern remains partially unaddressed. A portfolio of stocks near 52-week lows will inevitably overweight [20] troubled industries, and mean reversion timelines can exceed 12 months during structural economic shifts.

Verdict: The preponderance of academic evidence supports the claim. The 52-week low effect demonstrates standalone predictive power, equal-weighting provides structural outperformance, and concentration risk in the benchmark creates asymmetric opportunity. While not guaranteed in every 12-month period, the strategy has a sound theoretical and empirical foundation for expecting index-beating returns on average.

Round 3

Core claim: Buying S&P 500 stocks near 52-week lows does not reliably beat the index over 12 months.

After three rounds, the negative case rests on a simple but decisive distinction: the affirmative must prove a systematic, unconditional 12-month outperformance, while the evidence supports at most a conditional, regime-dependent, and frequently reversed effect. A claim of reliable outperformance cannot be built on a foundation that is itself contested, fragile, and timing-dependent.

1. The low-price signal lacks standalone predictive power. The anchoring literature consistently finds that proximity to the 52-week high predicts returns, while proximity to the low does not carry a reliable forward edge. The affirmative's own cited research describes the low-side findings as conflicting and notes that long-term reversals are unrelated to the bias driving short-term predictability. A strategy cannot deliver dependable index-beating returns from a signal whose supporting literature cannot agree it works.

2. Momentum—one of finance's most durable anomalies—works directly against this basket. Stocks near 52-week lows are, by construction, recent losers, and decades of out-of-sample evidence show losers continue to lag by roughly 1% per month relative to winners. A 52-week-low portfolio is essentially the short, underperforming leg of momentum held long—precisely the basket to avoid.

3. Any outperformance is regime-dependent, not general. When beaten-down stocks beat the market, it is confined to sentiment-driven rebound windows that are hard to predict and that reverse in normal or declining markets. The claim is framed as always-true over "the subsequent 12-month period"; a conditional effect cannot satisfy an unconditional claim.

4. The equal-weight mechanism the affirmative leans on has recently been a losing bet. The data we presented is unambiguous:

| Strategy | 4-Yr Return | 5-Yr Return | 10-Yr Return |

|---|---|---|---|

| Cap-Weighted S&P 500 (SPY) | 54.29% | 73.99% | 250.86% |

| Equal-Weight S&P 500 (RSP) | 38.08% | 49.59% | 207.45% |

Legend: Total return [28] through June 9, 2026. Equal-weighting—the affirmative's structural engine—underperformed across every horizon. Source: public market data.

The affirmative's "concentration [6] risk mitigation" is not risk management; it swaps one concentrated bet for another, and that swap recently produced the equal-weight index's worst relative drawdown in two decades.

In fairness, the affirmative landed real points. Their citation that "the nearness to the 52-week low [1] has predictive power... separate from that of past returns" is the strongest evidence against my momentum argument—if that exclusivity holds, the low signal is not merely the short leg of momentum. Their documentation of monthly returns rising from 1.00% to 1.78% in extreme deciles shows the effect can be economically large when present. And their structural point about equal-weight rebalancing [21] capturing a contrarian, mean-reverting tilt is theoretically sound and historically supported over very long windows.

The debate is genuinely close on mechanism but decisive on the standard of proof. The affirmative has shown that a 52-week-low/equal-weight strategy can outperform under the right conditions—mean reversion [15], broad market breadth, and mega-cap [16] stumbles. What they have not shown is that it reliably does so over an arbitrary 12-month window, which is what the claim asserts. My evidence demonstrates that the supporting signal is contested, that momentum cuts against it, that the effect appears only in specific sentiment regimes, and that the equal-weight engine underperformed across 4-, 5-, and 10-year horizons through 2026.

The affirmative's case is a defensible conditional thesis stretched into an indefensible unconditional one. Because the claim demands reliability and the record delivers only contingency, the FALSE position stands: a portfolio of S&P 500 stocks near their 52-week lows does not dependably exceed the index over the subsequent 12 months.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.102 | 33 | 60 | FALSE | FALSE | 70% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.084 | 0.000 | 33 | 360 | TRUE | FALSE | 65% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] 52-week low — The lowest trading price a security has reached in the past 52 weeks, often used as a technical indicator of undervaluation or distress.

[2] alpha — The excess return of an investment relative to the return of a benchmark index, representing the value added by active management or strategy.

[3] beta — A measure of a stock's volatility relative to the overall market; a beta greater than 1 indicates higher sensitivity to market movements.

[4] cap-weighted index — capitalization-weighted index — An index where each constituent's weight is proportional to its market capitalization, giving larger companies greater influence on index returns.

[5] cascade selling — A rapid sequence of sell orders triggered by falling prices, often due to stop-losses, margin calls, or momentum strategies, leading to overshoots below fundamental value.

[6] concentration — The degree to which a small number of stocks or sectors dominate the total weight of an index or portfolio.

[7] contrarian investment strategy — An investment approach that buys underperforming or out-of-favor assets and sells overperforming ones, betting on mean reversion.

[8] contrarian rebalancing premium — The excess return generated by regularly selling winners and buying losers in an equal-weight portfolio, exploiting mean reversion and opposite of momentum.

[9] equal-weight index (EW index) — An index in which all constituent stocks are assigned the same weight at each rebalance, regardless of their market capitalization.

[10] factor model — A financial model that explains asset returns through exposure to various systematic risk factors, such as size, value, momentum, or volatility.

[11] glamour stocks — Stocks that have performed well in the recent past and are popular among investors, often trading at high valuations relative to fundamentals.

[12] idiosyncratic drawdown — A decline in the value of a specific asset driven by company-specific factors rather than broad market movements.

[13] implied volatility — The market's forecast of a likely range of movement in a security's price, derived from option prices and reflecting expected risk.

[14] large-cap — large capitalization — A classification for companies with a large market capitalization, typically over $10 billion, representing well-established firms.

[15] mean reversion — The tendency of asset prices and returns to eventually move back toward their historical average or mean over time.

[16] mega-cap — mega capitalization — A classification for the largest publicly traded companies, often with market capitalizations exceeding $200 billion.

[17] mid-cap — mid capitalization — Companies with market capitalization between small-cap and large-cap, typically between $2 billion and $10 billion.

[18] momentum strategy — An investment approach that buys assets that have performed well recently and sells those that have performed poorly, expecting trends to continue.

[19] option-implied measures — Risk metrics, such as implied volatility or skew, derived from option prices that reflect market expectations about future price movements.

[20] overweight — Holding a larger proportion of a particular asset or sector in a portfolio relative to its weight in a benchmark index.

[21] rebalancing — The process of periodically adjusting portfolio holdings to maintain target allocations, often involving selling winners and buying losers.

[22] rebalancing premium — The additional return earned from the systematic rebalancing of a portfolio, particularly in equal-weight strategies, due to mean reversion and contrarian effects.

[23] risk-adjusted return — A measure of investment return adjusted for the level of risk taken, often using metrics like the Sharpe Ratio.

[24] Sharpe ratio — A risk-adjusted return measure calculated as the excess return of an investment over the risk-free rate divided by its standard deviation.

[25] size factor — The empirical observation that smaller-capitalization stocks tend to outperform larger-cap stocks over the long term, a key factor in factor models.

[26] small-cap — small capitalization — Companies with a relatively small market capitalization, typically between $300 million and $2 billion, often associated with higher growth potential and risk.

[27] SPIVA scorecard — S&P Indices Versus Active Funds scorecard — A semi-annual report by S&P Dow Jones Indices that compares the performance of actively managed mutual funds to their respective benchmark indices.

[28] total return — The overall investment return including both price appreciation and income from dividends or interest, typically expressed as a percentage.

[29] underweight — Holding a smaller proportion of a particular asset or sector in a portfolio relative to its weight in a benchmark index.

[30] value-weighted index — Another term for a capitalization-weighted index where constituents are weighted by market value.

[31] zero-investment strategy — A portfolio strategy that takes offsetting long and short positions such that the net investment is zero, aiming to isolate a specific factor or signal.

The following financial data tables were referenced during the debate exchanges:

| Strategy | 4-Yr Return (2022–2026) | 5-Yr Return | 10-Yr Return |

|---|---|---|---|

| Cap-Weighted S&P 500 (SPY) | 54.29% | 73.99% | 250.86% |

| Equal-Weight S&P 500 (RSP) | 38.08% | 49.59% | 207.45% |

Legend: Total return comparison of cap-weighted vs. equal-weight S&P 500 strategies through June 9, 2026. The equal-weight approach—central to the affirmative's argument—underperformed across every horizon. Source: public market data.

</FinancialData>

| Strategy | 4-Yr Return | 5-Yr Return | 10-Yr Return |

|---|---|---|---|

| Cap-Weighted S&P 500 (SPY) | 54.29% | 73.99% | 250.86% |

| Equal-Weight S&P 500 (RSP) | 38.08% | 49.59% | 207.45% |

Legend: Total return through June 9, 2026. Equal-weighting—the affirmative's structural engine—underperformed across every horizon. Source: public market data.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.