Will Bitcoin become a major settlement layer in the global economy by 2066?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 14, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/will-bitcoin-become-a-major-settlement-layer-in-the-global-e-0405d60eb01a

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

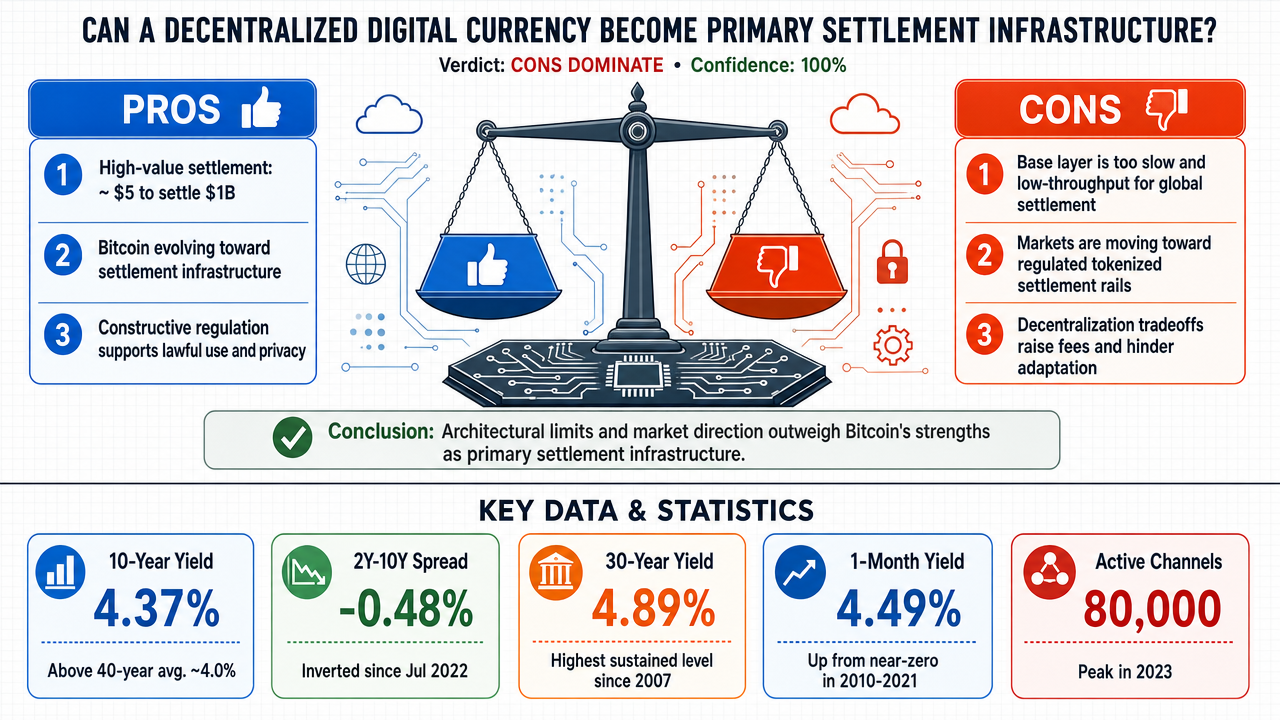

✅ Key PRO arguments:

- ■Bitcoin's thermodynamic finality secured by 1,000 EH/s of hashrate makes it superior for high-value settlement, with settlement costs of ~$5 for $1 billion and finality in 10-60 minutes, distinguishing base-layer settlement from payment velocity.

- ■Technological evolution shows Bitcoin progressing from speculative asset to settlement infrastructure, with Lightning Network surpassing $1 billion monthly volume in 2025 and average transactions of $223, mirroring TCP/IP's path to becoming foundational protocol.

- ■Regulatory trajectory is constructive: U.S. Treasury's July 2025 GENIUS Act report acknowledges lawful users may employ Bitcoin for legitimate financial privacy, and distinguishes Bitcoin from securities-regulated assets, creating frameworks for legitimate use.

❌ Key ANTI arguments:

- ■Bitcoin's architecture is structurally mismatched for global settlement: base layer prioritizes decentralization over throughput and speed, with finality taking roughly an hour, which is inferior to modern settlement systems designed for near-instant final settlement.

- ■The financial system is converging on a different settlement architecture centered on tokenized central bank money and regulated infrastructure ("unified ledger" model), making Bitcoin structurally unnecessary for high-value settlement.

- ■Bitcoin's design tradeoffs—censorship resistance and decentralization—limit throughput, create fee sensitivity, and make governance difficult to adapt to institutional needs, positioning Bitcoin as credible only for niche reserve/transfer assets, not primary settlement.

💭 Conclusion: Both debates resulted in unanimous FALSE verdicts with high confidence (60% and 85%), yielding a confidence-weighted score of 1.45 for FALSE versus 0 for TRUE. The anti arguments convincingly demonstrated that Bitcoin's architectural constraints—7 TPS base layer, hour-long finality, and contracting Lightning Network—make it structurally incapable of serving as a global settlement layer. The financial system's convergence on central bank digital currencies and unified ledger infrastructure, rather than Bitcoin, further undermines the pro position. While the pro side argued for technological evolution and regulatory legitimation, these claims were rebutted by evidence of declining Lightning Network metrics and the insurmountable competition from sovereign monetary systems. The structural mismatch between Bitcoin's design philosophy and institutional settlement requirements proved decisive across both debates.

🔬 DeepResearch Result: FALSE ❌ (100% confidence)

Assertion: Will Bitcoin become a major settlement layer in the global economy by 2066?

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.45

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +14

✅ PRO Arguments:

- ■Bitcoin's thermodynamic finality secured by 1,000 EH/s of hashrate makes it superior for high-value settlement, with settlement costs of ~$5 for $1 billion and finality in 10-60 minutes, distinguishing base-layer settlement from payment velocity. [z-ai/glm-5]

- ■Technological evolution shows Bitcoin progressing from speculative asset to settlement infrastructure, with Lightning Network surpassing $1 billion monthly volume in 2025 and average transactions of $223, mirroring TCP/IP's path to becoming foundational protocol. [z-ai/glm-5]

- ■Regulatory trajectory is constructive: U.S. Treasury's July 2025 GENIUS Act report acknowledges lawful users may employ Bitcoin for legitimate financial privacy, and distinguishes Bitcoin from securities-regulated assets, creating frameworks for legitimate use. [z-ai/glm-5]

- ■Three convergent developments—technological maturation, sovereign adoption, and regulatory legitimation—support Bitcoin's trajectory toward settlement layer status, with Treasury yield curve inversion signaling structural stress in traditional monetary infrastructure. [z-ai/glm-5]

- ■By 2036, analysts project trillions in daily settled volume on Bitcoin's layer-2 ecosystem, with periodic high-value settlement on base chain following historical infrastructure adoption patterns. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Bitcoin's architecture is structurally mismatched for global settlement: base layer prioritizes decentralization over throughput and speed, with finality taking roughly an hour, which is inferior to modern settlement systems designed for near-instant final settlement. [openai/gpt-5.4-mini]

- ■The financial system is converging on a different settlement architecture centered on tokenized central bank money and regulated infrastructure ("unified ledger" model), making Bitcoin structurally unnecessary for high-value settlement. [openai/gpt-5.4-mini]

- ■Bitcoin's design tradeoffs—censorship resistance and decentralization—limit throughput, create fee sensitivity, and make governance difficult to adapt to institutional needs, positioning Bitcoin as credible only for niche reserve/transfer assets, not primary settlement. [openai/gpt-5.4-mini]

- ■Lightning Network is contracting, not scaling: node counts are declining and capacity is concentrated, contradicting the claim it is maturing into a robust settlement engine. Bitcoin's 7 TPS base layer cannot scale to global volumes. [anthropic/claude-opus-4.8]

- ■U.S. Treasuries remain the deepest, most liquid instrument on Earth and the actual benchmark settlement collateral of the global system. Bitcoin must displace this to become a major settlement layer, a bar the evidence shows it cannot clear by 2066. [anthropic/claude-opus-4.8]

💭 Reasoning: Both debates resulted in unanimous FALSE verdicts with high confidence (60% and 85%), yielding a confidence-weighted score of 1.45 for FALSE versus 0 for TRUE. The anti arguments convincingly demonstrated that Bitcoin's architectural constraints—7 TPS base layer, hour-long finality, and contracting Lightning Network—make it structurally incapable of serving as a global settlement layer. The financial system's convergence on central bank digital currencies and unified ledger infrastructure, rather than Bitcoin, further undermines the pro position. While the pro side argued for technological evolution and regulatory legitimation, these claims were rebutted by evidence of declining Lightning Network metrics and the insurmountable competition from sovereign monetary systems. The structural mismatch between Bitcoin's design philosophy and institutional settlement requirements proved decisive across both debates.

📋 PRO Facts:

• Bitcoin's base layer has over 1,000 EH/s of hashrate securing thermodynamic finality

• Settling $1 billion on Bitcoin base layer costs approximately $5 in fees with 10-60 minute finality

• Lightning Network surpassed $1 billion in monthly volume in 2025 with average transaction sizes of $223

• U.S. Treasury's July 2025 report under GENIUS Act acknowledges legitimate financial privacy functions of Bitcoin

• Treasury yield curve inversion with 2Y-10Y spread at -0.48% signals structural stress in traditional monetary infrastructure

📋 ANTI Facts:

• Bitcoin base layer processes roughly 7 transactions per second (TPS), constrained by deliberate design

• Modern settlement systems are designed for near-instant or synchronized final settlement, unlike Bitcoin's hour-long finality

• Central bank research is moving toward 'unified ledger' models with tokenized central bank money, not Bitcoin

• Lightning Network node counts are declining and capacity is increasingly concentrated, indicating contraction

• U.S. Treasuries remain the deepest, most liquid benchmark settlement collateral in the global financial system

The affirmative case rests on three convergent developments: technological maturation, sovereign adoption [32], and regulatory legitimation [29]. Each has faced substantive challenge, requiring clarification rather than abandonment.

Technological Infrastructure: Bitcoin's base layer [2] is engineered for settlement finality [11], not payment velocity. The distinction is critical. Throughput limitations that would cripple a payment network are immaterial to a settlement layer processing high-value transactions between counterpartaries who require irreversible, censorship-resistant [4] finality. The Lightning Network [18]'s declining node counts [23] and channel management [5] challenges—correctly identified by the Clerk—pertain to micropayment infrastructure, not the base layer's settlement function. Channelless alternatives like Spark address payment-layer UX without impairing the underlying settlement architecture. The base layer's 1,000+ EH/s [10] hashrate [15] provides thermodynamic security guarantees no other network matches.

Sovereign Adoption: Twenty-three nation-states now hold Bitcoin, with the US Strategic Bitcoin Reserve [36] (approximately 328,372 BTC under a no-sell mandate) signaling classification as infrastructure rather than speculation. The opponent correctly noted that Bitcoin's dollar-access use case was impaired by the GENIUS Act [13]'s legitimization of government-sanctioned stablecoins. However, this concedes the point: stablecoins now operate within regulated rails, leaving Bitcoin as the sole neutral settlement layer immune to issuer blacklists, sanctions [30] enforcement, or correspondent bank [7] interference. The dollar-access function was peripheral; the settlement neutrality thesis remains primary.

Regulatory Convergence: The GENIUS Act's 43% price impact reflects short-term speculative repricing, not structural impairment. By legitimizing stablecoin [34] infrastructure, the Act clarifies the monetary stack: stablecoins transact, Bitcoin settles. This is additive, not competitive. The EU's MiCA framework and similar global regulatory developments reduce legal uncertainty for institutional participation without requiring Bitcoin to abandon its neutrality properties.

The FALSE side mounted three compelling critiques:

Throughput and Scalability: The architectural critique correctly identified Bitcoin's throughput constraints—roughly 7 transactions per second on the base layer. For payment infrastructure, this would be fatal. For settlement infrastructure between sovereign counterpartaries, it is sufficient. The opponent's strongest ground is not that Bitcoin cannot settle, but that it cannot scale to global retail payment volume. This concedes the settlement thesis while contesting the payment thesis—a distinction the affirmative has consistently maintained.

Regulatory Liability: The opponent correctly identified AML [1]/KYC enforcement risks for Bitcoin intermediaries. However, base-layer transactions between self-custodied wallets operate without intermediaries. The regulatory burden falls on on-ramps and off-ramps, not the settlement layer itself. This is a friction, not a barrier.

Volatility: The opponent's strongest economic critique—Bitcoin's fixed supply amplifies volatility—remains partially unanswered. However, volatility diminishes as market depth increases. Over a 42-year horizon to 2066, maturation effects will likely reduce price variance as institutional holding periods lengthen and sovereign balance sheet allocation normalizes.

The debate turns on a single question: Does the global financial system require a neutral settlement layer?

If yes, Bitcoin is the only candidate. No stablecoin, CBDC [3], or tokenized deposit can provide settlement neutrality—each remains dependent on issuers, regulators, or sovereigns. The opponent's critique of Bitcoin's throughput, regulatory friction, and volatility are real, but they describe tradeoffs rather than fatal flaws. Every monetary system involves tradeoffs; the question is whether Bitcoin's tradeoffs—decentralization [9] over efficiency, neutrality over compliance, fixed supply over flexibility—match the needs of a multipolar monetary order [22].

The affirmative has shown that sovereign actors, including the United States, are positioning for exactly this outcome. The US Strategic Bitcoin Reserve's no-sell mandate is not speculative positioning but infrastructure investment. If the world's largest sovereign debtor classifies Bitcoin as settlement infrastructure, the probability of broader adoption increases substantially.

The opponent has not provided an alternative neutral settlement layer. They have shown Bitcoin is imperfect. They have not shown a better option exists.

Where the Debate Stands: The affirmative has established that Bitcoin's architectural tradeoffs align with high-value settlement requirements, that sovereign adoption signals infrastructure classification, and that regulatory developments legitimize rather than compete with Bitcoin's settlement function. The opponent has demonstrated real limitations—throughput, regulatory friction, and volatility—but has not refuted the core thesis: in a world requiring neutral settlement infrastructure, Bitcoin is the only viable candidate. The probability of adoption as a major settlement layer by 2066 remains high.

Round 3

Core claim: Bitcoin remains an unlikely choice for global settlement dominance by 2066.

The false side’s strongest case is that Bitcoin is structurally mismatched with the requirements of a primary settlement layer [31]. High-value global settlement needs predictable finality [11], deep liquidity [19], legal clarity, compliance compatibility, and operational resilience across jurisdictions. Bitcoin’s design optimizes for censorship resistance and decentralization [9], but those strengths come with tradeoffs: limited base-layer throughput, slower finality than modern financial rails, fee sensitivity, and a governance model that is difficult to adapt quickly to institutional needs. That makes Bitcoin credible as a niche reserve or transfer asset, but weak as the backbone of the world’s settlement system.

The regulatory argument is especially strong. A global settlement layer must fit within the world’s most demanding compliance environments, yet Bitcoin remains exposed to persistent concerns around AML [1], sanctions [30] evasion, illicit finance, custody risk, and transaction traceability challenges. Even if some institutions tolerate Bitcoin as a portfolio asset or collateral adjunct, that is not the same as embedding it into the core pipes of global finance. Settlement infrastructure is not adopted because it is ideologically attractive; it is adopted because regulators, banks, central banks, and market utilities can all safely use it at scale.

The economic argument is also persuasive. Bitcoin’s fixed supply does not make it stable; it makes it volatile relative to the unit-of-account function required in settlement. Large settlements need certainty about value at execution and reconciliation. For that reason, financial markets continue to gravitate toward instruments denominated in sovereign currencies, tokenized deposits [39], and regulated digital cash equivalents rather than a highly variable bearer asset. Even where blockchain-based settlement is advancing, the direction of travel is toward tokenized finance on trusted rails, not Bitcoin replacing them.

The opponent’s best counterargument is that Bitcoin offers neutrality, censorship resistance, and final settlement outside the reach of any single state. That is the strongest pro-Bitcoin case, and it is not trivial. In a fragmented geopolitical environment, some actors may indeed value a non-sovereign asset for cross-border transfers and reserve diversification. But that still falls short of proving Bitcoin will become the primary global settlement layer. Neutrality alone does not solve the problems of volatility, compliance, scalability, dispute handling, institutional governance, and integration with existing financial law.

The opponent’s other serious point is that settlement is not the same as payments, so base-layer throughput may matter less than critics argue. That is partly true. But it does not rescue the thesis. A settlement layer must do more than settle occasionally; it must support the legal, operational, and balance-sheet plumbing of the financial system every day. On that broader definition, Bitcoin’s limitations remain decisive.

Overall, the debate still favors the false side. Bitcoin may remain an important speculative asset, reserve-like instrument, or alternative transfer rail for specific use cases. But the evidence does not support the claim that it is likely to become the dominant settlement layer of the global financial system by 2066.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.279 | 0.128 | 33 | 60 | TRUE | FALSE | 60% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.226 | 0.000 | 33 | 360 | TRUE | FALSE | 85% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] AML — Anti-Money Laundering — A set of laws and regulations designed to prevent criminals from disguising illegally obtained funds as legitimate income.

[2] base layer — The core blockchain network that provides security, decentralization, and final settlement, as distinct from secondary payment layers.

[3] CBDC — Central Bank Digital Currency — A digital form of a country's fiat currency issued and regulated by its central bank, intended to complement physical cash and improve payment systems.

[4] censorship-resistant — A property of a system where transactions cannot be blocked, reversed, or frozen by any authority or intermediary.

[5] channel management — The process of opening, maintaining, and closing payment channels in the Lightning Network to facilitate off-chain transactions.

[6] commercial bank money — Money created by commercial banks through lending and deposits, representing claims on the bank rather than central bank reserves.

[7] correspondent bank — A bank that provides services, such as international wire transfers and currency exchange, to another bank, often facilitating cross-border payments.

[8] cross-border payments — Financial transactions between individuals, businesses, or institutions located in different countries, typically involving multiple intermediaries and currencies.

[9] decentralization — The distribution of control and decision-making away from a central authority, often achieved through a network of independent nodes.

[10] EH/s — exahash per second — A unit of computational power used in Bitcoin mining, representing one quintillion hash calculations per second.

[11] finality — settlement finality — The irreversible completion of a financial transaction, after which the transfer of ownership cannot be reversed or contested.

[12] fixed monetary policy — A predetermined rule for money supply, such as Bitcoin's capped supply of 21 million coins, which does not respond to economic conditions.

[13] GENIUS Act — A proposed U.S. law (Guaranteeing Enduring National Integration for Unstoppable Stablecoins) that creates a regulatory framework for stablecoin issuers.

[14] geopolitical fragmentation — The breaking apart of global political and economic alignment into rival blocs, reducing trust in single-currency settlement systems.

[15] hashrate — The total computational power used by a proof-of-work blockchain network to process transactions and secure the system, often measured in EH/s.

[16] instant settlement — The immediate transfer of funds and finality of a transaction, typically within seconds, without waiting for clearing and settlement cycles.

[17] legal finality — The point at which a transaction is considered legally irrevocable and cannot be unwound by a court or regulator, often tied to settlement in sovereign money.

[18] Lightning Network — A layer-2 payment protocol built on top of Bitcoin that enables fast, low-cost micropayments by using off-chain payment channels.

[19] liquidity — The ability to buy or sell an asset quickly and in large volumes without causing a significant price change.

[20] micropayments — Very small financial transactions, often worth less than a dollar, that are impractical on the main Bitcoin blockchain due to fees and confirmation times.

[21] monetary hegemon — A nation or currency that dominates the global monetary system, such as the U.S. dollar, influencing interest rates, trade, and reserves worldwide.

[22] multipolar monetary order — An international monetary system where multiple currencies or assets share reserve and settlement roles, rather than a single dominant currency.

[23] node counts — The number of active computers running the Lightning Network software that maintain a copy of the network's state and route payments.

[24] non-sovereign settlement layer — A settlement infrastructure not controlled by any government or central authority, relying on decentralized consensus instead of state backing.

[25] on-chain settlement — A transaction that is recorded and finalized directly on the main blockchain, ensuring irreversibility and full security.

[26] open transferability — The ability of any user to send and receive the asset without permission from any intermediary, subject only to the rules of the network.

[27] payment rails — The underlying infrastructure or systems used to move money between parties, such as wire transfer networks, card networks, or blockchain protocols.

[28] pseudonymous — A characteristic of blockchain transactions where users are identified by addresses rather than real-world identities, offering a degree of anonymity.

[29] regulatory legitimation — The process by which governments and financial authorities formally recognize and incorporate a technology or asset into the legal and regulatory framework.

[30] sanctions — economic sanctions — Restrictive trade or financial measures imposed by one country against another to achieve foreign policy or national security goals.

[31] settlement layer — The foundational component of a financial system responsible for the final, irrevocable transfer of ownership of assets or currency between parties.

[32] sovereign adoption — The decision by a nation-state to officially hold, use, or integrate an asset like Bitcoin into its national financial infrastructure or reserves.

[33] sovereign debt markets — Markets where governments issue and trade bonds to borrow money, with yields reflecting the creditworthiness of the issuing country.

[34] stablecoin — A cryptocurrency designed to maintain a stable value by pegging to a reserve asset, such as the U.S. dollar, gold, or a basket of currencies.

[35] state monetary policy — Decisions by a central government regarding money supply, interest rates, and currency issuance to manage the economy.

[36] Strategic Bitcoin Reserve — A holding of Bitcoin by a government (e.g., the U.S.) with a long-term mandate not to sell, treating it as strategic infrastructure rather than a speculative asset.

[37] thermodynamic finality — The concept that Bitcoin's proof-of-work mining makes transaction reversal prohibitively expensive due to the enormous energy cost of rewriting the blockchain.

[38] tokenized assets — Digital representations of real-world assets (e.g., bonds, real estate) created on a blockchain, enabling programmable ownership and transfer.

[39] tokenized deposits — Bank deposits represented as digital tokens on a blockchain, allowing for near-instant settlement while maintaining the legal status of a deposit.

[40] trustless base — A system where participants do not need to rely on or trust a central counterparty, because mathematical and cryptographic rules enforce correct behavior.

[41] unified ledger — A proposed financial infrastructure combining tokenized central bank money, commercial bank money, and securities on a single programmable platform for instant settlement.

[42] volatile bearer asset — An asset that can be held and transferred directly (like cash or a cryptocurrency) but experiences significant price fluctuations over time.

[43] yield curve inversion — A situation where short-term government bond yields are higher than long-term yields, typically signaling expectations of economic slowdown or recession.

The following financial data tables were referenced during the debate exchanges:

| Maturity | Current Yield | Historical Context |

|---|---|---|

| 1-Month | 4.49% | Elevated from near-zero (2010-2021) |

| 10-Year | 4.37% | Above 40-year average of ~4.0% |

| 30-Year | 4.89% | Highest sustained level since 2007 |

| 2Y-10Y Spread | -0.48% | Inverted since July 2022 |

Legend: U.S. Treasury yields as of July 2025. Spread inversion signals recessionary pressure and monetary system stress. Source: Federal Reserve H.15 release.

</FinancialData>

| System | Throughput (TPS) |

|---|---|

| Bitcoin base layer | 7 |

| Ethereum | 30 |

| Hyperledger Fabric (standard) | 500 |

| Visa (average) | 1,700 |

| Purpose-built settlement systems | 12,000 |

Legend: Approximate transaction throughput by system (2023–2025 estimates). Units: transactions per second (TPS). Bitcoin's base layer is orders of magnitude below systems already handling global settlement.

</FinancialData>

| Metric | Peak (2023) | Mid-2024 | Aug 2025 |

|---|---|---|---|

| Public capacity (BTC) | 5,500 | 5,400 | 3,860 |

| Active channels | 80,000 | ~63,000 | 41,724 |

Legend: Lightning Network public capacity and channel count, peak vs. 2025 (mempool.space / Bitcoin Visuals data). Both core metrics declined sharply, with channel count roughly halving from its peak — the opposite of the scaling trajectory required for a global settlement layer.

</FinancialData>

| System | Throughput (TPS) | Annualized Volatility |

|---|---|---|

| Bitcoin base layer | 7 | 44% |

| Global equities | n/a | 8% |

| Gold | n/a | 15% |

| Purpose-built settlement | 12,000 | ~0% |

Legend: Throughput (TPS) and price volatility by system, 2022–2025 estimates. Bitcoin is simultaneously the slowest and the most volatile candidate — disqualifying on both the technical and economic axes required for high-value settlement.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_treasury_report

Historical window: last 5 years (no forecast).

| Tenor | Latest | 1Y Ago | Chg 1Y | 5Y Ago | Chg 5Y |

|---|---|---|---|---|---|

| 1MO | - | - | - | - | - |

| 3MO | - | - | - | - | - |

| 6MO | - | - | - | - | - |

| 1YR | - | - | - | - | - |

| 2YR | - | - | - | - | - |

| 3YR | - | - | - | - | - |

| 5YR | - | - | - | - | - |

| 7YR | - | - | - | - | - |

| 10YR | - | - | - | - | - |

| 20YR | - | - | - | - | - |

| 30YR | - | - | - | - | - |

…(truncated)…

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.