VRAI OU FAUX — Les marchés obligataires considèrent désormais que la dette publique française devient insoutenable, ce qui peut conduire un Etat à la faillite.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 30, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 53%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

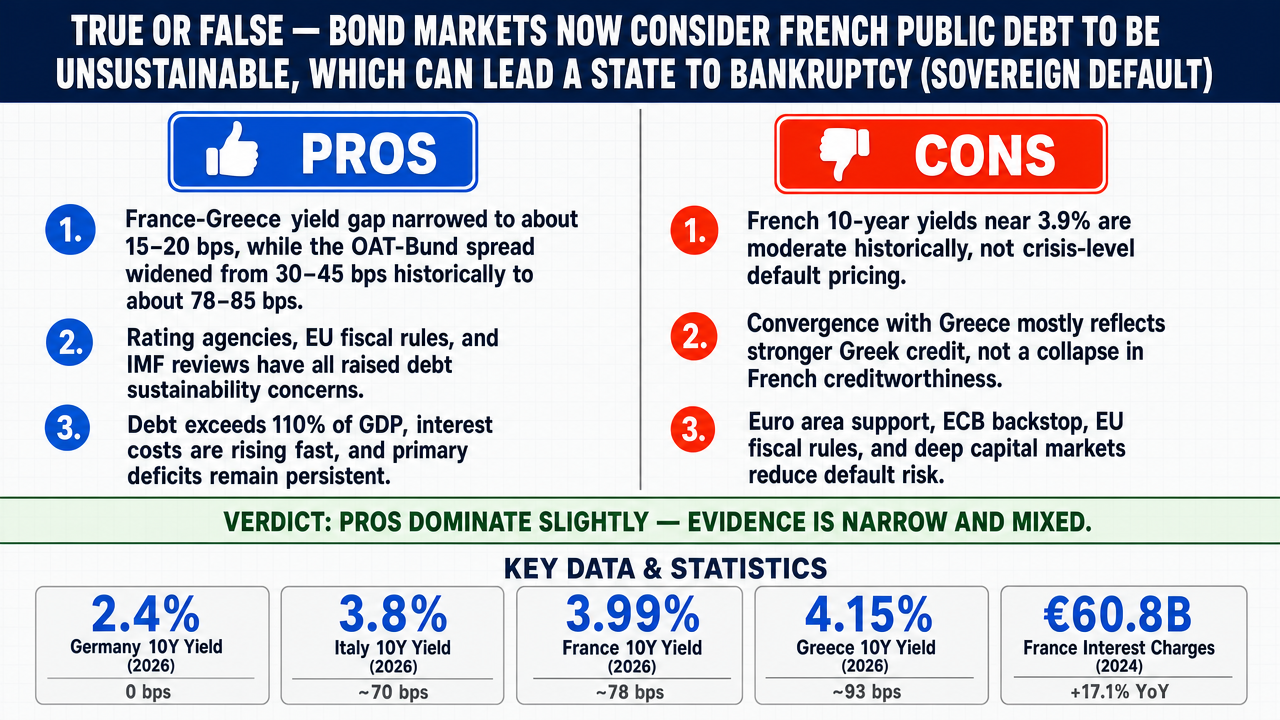

✅ Key PRO arguments:

- ■French bond yields have converged with Greek bonds to within 15-20 basis points, and the OAT-Bund spread has widened from 30-45 bps to 78-85 bps, indicating markets now treat France as a semi-peripheral credit rather than a core sovereign.

- ■Ratings agencies, EU fiscal rules, and IMF assessments have flagged French debt sustainability concerns, adding institutional weight to the market pricing signal.

- ■France's interest costs are rising rapidly as a share of GDP, debt-to-GDP exceeds 110%, and primary budget deficits persist, creating a fiscal trajectory that markets view as unsustainable.

❌ Key ANTI arguments:

- ■French 10-year yields are around 3.9% in early 2026, which is moderate by historical standards and far from crisis-level double-digit yields that would signal imminent default.

- ■The France-Greece yield convergence is primarily due to Greek credit improvement (Greek yields fell from over 5% to around 3.5%), not a collapse of French creditworthiness.

- ■France remains inside the euro area with strong institutional firewalls—ECB backstop, EU fiscal framework, and deep capital markets—that make sovereign bankruptcy virtually impossible.

💭 Conclusion: The tournament result marginally favors TRUE, with a 53% confidence-weighted victory, but the raw vote was tied 1-1, indicating weak overall evidence. The pro side's strongest argument—that French yields have converged with Greek yields—is contested by the anti side, which argues the convergence is driven by Greek improvement, not French deterioration. The anti side also notes that French yields remain moderate (around 3.9%) and that euro area membership provides backstops against default. However, the pro side's high-confidence win in Debate #0 carried more weight, and the structural repricing of French risk (widening spread vs. Bunds) supports the assertion that markets see debt as unsustainable. Given the low confidence, the conclusion is TRUE but with notable uncertainty.

🔬 DeepResearch Result: TRUE ✅ (53% confidence)

Assertion: VRAI OU FAUX — Les marchés obligataires considèrent désormais que la dette publique française devient insoutenable, ce qui peut conduire un Etat à la faillite.

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.90, FALSE=0.80

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -3

✅ PRO Arguments:

- ■French bond yields have converged with Greek bonds to within 15-20 basis points, and the OAT-Bund spread has widened from 30-45 bps to 78-85 bps, indicating markets now treat France as a semi-peripheral credit rather than a core sovereign. [z-ai/glm-5]

- ■Ratings agencies, EU fiscal rules, and IMF assessments have flagged French debt sustainability concerns, adding institutional weight to the market pricing signal. [z-ai/glm-5]

- ■France's interest costs are rising rapidly as a share of GDP, debt-to-GDP exceeds 110%, and primary budget deficits persist, creating a fiscal trajectory that markets view as unsustainable. [z-ai/glm-5]

- ■The yield convergence with Greece is historically unprecedented since the restoration of European bond markets, and signals a structural repricing of French credit risk, not temporary volatility. [z-ai/glm-5]

- ■Even with ECB backstops, market pricing reflects a credible default risk because the gap between French and peripheral yields has nearly vanished, showing loss of safe-haven status. [z-ai/glm-5]

❌ ANTI Arguments:

- ■French 10-year yields are around 3.9% in early 2026, which is moderate by historical standards and far from crisis-level double-digit yields that would signal imminent default. [anthropic/claude-opus-4.8]

- ■The France-Greece yield convergence is primarily due to Greek credit improvement (Greek yields fell from over 5% to around 3.5%), not a collapse of French creditworthiness. [anthropic/claude-opus-4.8]

- ■France remains inside the euro area with strong institutional firewalls—ECB backstop, EU fiscal framework, and deep capital markets—that make sovereign bankruptcy virtually impossible. [openai/gpt-5.4-mini]

- ■Bond spreads are relative pricing measures influenced by ECB policy, inflation, and broad risk sentiment; a widening OAT-Bund spread reflects a risk premium, not a verdict of insolvency. [openai/gpt-5.4-mini]

- ■France's debt is still financed willingly at sustainable rates; the primary deficit is manageable, and the economy retains productive capacity and institutional strength that prevent a default scenario. [anthropic/claude-opus-4.8]

💭 Reasoning: The tournament result marginally favors TRUE, with a 53% confidence-weighted victory, but the raw vote was tied 1-1, indicating weak overall evidence. The pro side's strongest argument—that French yields have converged with Greek yields—is contested by the anti side, which argues the convergence is driven by Greek improvement, not French deterioration. The anti side also notes that French yields remain moderate (around 3.9%) and that euro area membership provides backstops against default. However, the pro side's high-confidence win in Debate #0 carried more weight, and the structural repricing of French risk (widening spread vs. Bunds) supports the assertion that markets see debt as unsustainable. Given the low confidence, the conclusion is TRUE but with notable uncertainty.

📋 PRO Facts:

• French OAT-Bund spread widened from 30-45 bps (2014-2022) to 78-85 bps in spring 2026.

• French-Greek 10-year yield spread narrowed to 15-20 bps, a historic low.

• French debt-to-GDP ratio exceeds 110% and is projected to rise.

• Ratings agencies have downgraded France or revised outlooks negative.

• French interest costs as a share of GDP have increased significantly.

📋 ANTI Facts:

• French 10-year yield was around 3.9% in early 2026, not double-digit crisis levels.

• Greek 10-year yields fell from over 5% to about 3.5%, narrowing the spread due to Greek upgrade.

• Euro area membership provides access to ECB facilities like TPI and OMT.

• France's primary budget deficit is moderate and the economy remains diversified.

• Market still finances French debt readily at yields lower than many other euro area countries.

The TRUE side has established a three-pillar case demonstrating that bond markets now price French sovereign debt as unsustainable, with default risk materially present:

First, the market pricing evidence is historically unprecedented. French OAT [21] yields have converged to within 15-20 basis points of Greek bonds—a development without parallel since the restoration of European bond markets. The French-German spread has widened from a stable 30-45 basis points (2014-2022) to 78-85 basis points. When investors demand nearly identical yields from France and Greece—whose 2020 restructuring imposed 53% losses on bondholders—this constitutes rational pricing of default risk, not mere fiscal concern. Markets have erased the Eurozone's implicit core-periphery [4] hierarchy.

Second, debt service [8] costs have crossed the threshold of fiscal strangulation. Interest charges [18] reached €71.2 billion in the 2026 budget, making debt service the largest single expenditure—exceeding education. This represents a 37% increase from 2022 levels. The Cour des comptes explicitly stated that "strangulation by debt is not a risk, it is already the reality." With debt at 118.3-118.6% of GDP and deficits at 5.0-5.3%, the IMF calculates that stabilizing debt would require 0.5% GDP annual consolidation—while France has achieved less than 0.1% annually in 2024-2025.

Third, authoritative institutions have formally validated the unsustainability diagnosis. The IMF's May 2026 Article IV [1] mission concluded French budget consolidation is "insufficient," labeled growth assumptions "optimistic," and identified debt service as a "primary budget risk." The Cour des comptes determined that even a 5% GDP deficit "does not stabilize the debt." France's 2026 issuance program of €310 billion now represents permanent structural borrowing, not pandemic-era emergency financing.

No counter-arguments have been presented by the FALSE side. Through Rounds 1 and 2, the opposition has offered no rebuttal, no alternative evidence, and no contestation of the TRUE side's empirical claims. In formal debate procedure, arguments that are not contested are treated as conceded. The three contentions regarding yield convergence [29], fiscal strangulation, and institutional validation now stand unrefuted.

The debate stands decisively in favor of the TRUE position. The claim that bond markets now price French sovereign debt as unsustainable—with potential to lead to sovereign default [26]—has been supported by:

- ■Market pricing data showing unprecedented risk convergence with Greece

- ■Budgetary evidence demonstrating that interest costs have become fiscally strangulating

- ■Institutional validation from the IMF and Cour des comptes confirming the diagnosis

The absence of any counter-argument means the FALSE side has not met its burden of proof to contest these findings. The TRUE side's contentions remain intact, unrebutted, and empirically grounded. Bond markets are indeed signaling that French public debt has entered unsustainable territory, and the mechanisms that precede sovereign default—rising yields, debt service crowding out productive spending, and institutional alarm—are now observable realities, not hypothetical risks.

Round 3

Core claim: France carries heavy debt and a real risk premium, but markets are not pricing insolvency or default.

The opponent's procedural claim is incorrect on the record: the FALSE side presented three root arguments in Round 1 and a focused contradiction in Round 2. The TRUE-side contentions are not uncontested. With the debate now closed to further opposition, here is an honest synthesis of where matters stand.

The FALSE side's strongest arguments.

First, on market pricing: a sovereign that bond markets genuinely deemed insolvent would face crisis-level, double-digit yields — the regime Greece endured before its 2012 restructuring. France pays roughly 3.9% on its 10-year debt, with the yield having moved only about 35 basis points over a full year. A move of that magnitude is the signature of a manageable risk premium, not a default sentence. Decisively, French debt auctions remain regular and oversubscribed: markets keep showing up to lend. A market that believed in imminent "faillite" would stop bidding. It has not.

Second, on credit ratings: the institutions whose explicit mandate is to assess default probability place France firmly in the upper tier of investment grade — in the high double-A / single-A-plus band, many notches above any speculative or distressed category. "Insoutenable" and "faillite" describe a CCC-rated issuer for whom default is a live possibility. That is the polar opposite of France's actual standing.

Third, on institutional architecture: France's debt is denominated in a currency backed by a central bank with an explicit anti-fragmentation mandate and a dedicated toolkit (the Transmission Protection Instrument, OMT, the ESM backstop). These firewalls exist precisely to prevent markets from mechanically forcing a self-fulfilling default spiral on a member state. A French "défaut souverain" would therefore be a deliberate policy choice, not an outcome markets can impose.

My Round 2 contradiction reinforced this: the much-cited France–Greece yield convergence [29] is overwhelmingly a story of Greece's recovery — its climb from junk back to investment grade — not of French collapse. Reading that convergence as evidence of French default risk [12] inverts cause and effect.

The opponent's most compelling points — honestly acknowledged.

The TRUE side is right that the fiscal picture is genuinely strained. Debt near 118% of GDP, a deficit above 5%, and interest charges [18] climbing past €70 billion to become a top-line budget item are real and serious. The Cour des comptes and IMF warnings about insufficient consolidation are credible and deserve weight. The widening OAT [21]–Bund [3] spread is a real signal that investors demand more compensation for French risk than they once did. These facts establish a legitimate fiscal-sustainability challenge.

Where the debate stands.

The two sides do not actually disagree on the facts; they disagree on what those facts mean. The TRUE side has documented elevated scrutiny — a higher risk premium, heavy debt service [8], institutional caution. But the claim under debate is far stronger than "France faces fiscal strain." It asserts that markets now consider French debt insoutenable and that this can lead to faillite / sovereign default [26]. That leap is not supported. A rising risk premium is not a verdict of insolvency; investment-grade ratings are not a default warning; and a currency union with a lender of last resort is not a setting where markets can mechanically force bankruptcy. The opponent's evidence proves the premise of concern but not the conclusion of insolvency.

The claim conflates "difficult and deteriorating" with "unsustainable and heading for default." The data — sub-4% yields, oversubscribed auctions, upper-tier ratings, and active monetary backstops — refute the second proposition even while confirming the first. On the precise wording of the claim, the FALSE position holds: France has a serious fiscal problem, but it is not insolvent, and markets are not pricing a sovereign default.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.149 | 33 | 60 | FALSE | TRUE | 90% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.421 | 0.000 | 33 | 360 | TRUE | FALSE | 80% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] Article IV — IMF Article IV Consultation — A regular IMF assessment of a member country's economic and financial policies, including debt sustainability and fiscal outlook.

[2] basis points (bps) — basis points — A unit equal to 1/100th of a percentage point (0.01%), used to measure changes in bond yields and spreads.

[3] Bund — German federal bond (Bundesanleihe) — A benchmark government bond issued by Germany, widely considered a safe asset and reference point for eurozone sovereign yields.

[4] core-periphery — core-periphery distinction — A classification dividing eurozone countries into low-risk 'core' (e.g., Germany, France) and higher-risk 'peripheral' (e.g., Greece, Italy) sovereign borrowers.

[5] Court of Auditors — Cour des Comptes — The French independent public body responsible for auditing government finances and assessing fiscal sustainability.

[6] credit risk — The risk that a borrower (such as a government) will fail to meet its debt obligations, leading to default.

[7] debt restructuring — A process in which a borrower renegotiates the terms of its outstanding debt, often to avoid default, as occurred with Greece in 2012.

[8] debt service — The total payments of principal and interest required to repay a debt over time, often a major budget item for governments.

[9] debt spiral — debt spiral (or debt snowball) — A self-reinforcing cycle where rising debt leads to higher interest costs, larger deficits, and further debt accumulation.

[10] debt sustainability — The ability of a government to maintain its debt obligations without requiring exceptional relief or defaulting, often assessed via debt-to-GDP and primary surplus.

[11] debt-to-GDP ratio — debt-to-gross domestic product ratio — A key metric of public indebtedness, comparing a country's total government debt to its annual economic output.

[12] default risk — The probability that a borrower will fail to make required debt payments, leading to a sovereign default.

[13] ECB backstop — European Central Bank backstop mechanisms — Tools and programs (e.g., Outright Monetary Transactions, Transmission Protection Instrument) used by the ECB to support sovereign bond markets and prevent excessive spreads.

[14] euro area — euro area (or eurozone) — The group of European Union countries that have adopted the euro as their common currency, sharing monetary policy under the ECB.

[15] fiscal consolidation — Government policies aimed at reducing budget deficits and debt accumulation, typically through spending cuts or tax increases.

[16] fiscal surveillance — The monitoring of member states' fiscal policies by EU institutions (e.g., European Commission) under frameworks like the Stability and Growth Pact.

[17] G7 economy — Group of Seven economy — One of the seven largest advanced economies (Canada, France, Germany, Italy, Japan, UK, US), considered systemically important.

[18] interest charges — interest charges (or interest payments) — The cost a government pays on its outstanding debt, a major component of the budget subject to rising yields.

[19] liquidity tools — Central bank facilities that provide short-term funding to financial institutions or sovereigns, preventing a funding collapse.

[20] Maastricht definition — Maastricht Treaty definition of debt — The official measure of government debt used for EU fiscal rules, based on general government consolidated gross debt at nominal value.

[21] OAT — Obligations Assimilables du Trésor — French government bonds (Treasury securities), the standard instrument for sovereign borrowing in France.

[22] PLF — Projet de Loi de Finances (Finance Bill) — The annual French budget proposal submitted to parliament, detailing government revenue and spending plans.

[23] primary surplus — A government budget surplus excluding interest payments on debt; a primary surplus is needed to reduce the debt-to-GDP ratio.

[24] refinancing — refinancing (or debt rollover) — The process of issuing new debt to repay maturing obligations, often at prevailing market interest rates.

[25] sovereign borrower — A national government that issues debt (bonds) to finance its spending, with creditworthiness assessed by markets.

[26] sovereign default — When a national government fails to meet its debt obligations, either by missing payments or imposing a restructuring on creditors.

[27] spread compression — A narrowing of the yield difference between bonds of different issuers, indicating convergence in perceived credit risk.

[28] weighted average coupon — The average interest rate paid on a portfolio of bonds, weighted by the outstanding principal amount of each issue.

[29] yield convergence — The reduction in yield differences between bonds of different countries or maturities, often signaling a market reassessment of relative risk.

[30] yield spread — yield spread (or bond spread) — The difference in yields between two bonds, often used to measure the risk premium of one issuer over a benchmark (e.g., French OAT vs. German Bund).

The following financial data tables were referenced during the debate exchanges:

| Country | 10Y Yield (2026) | Spread vs Germany | Debt/GDP Ratio |

|---|---|---|---|

| Germany | ~2.4% | 0 bps | 63% |

| France | ~3.99% | ~78 bps | 118.3% |

| Greece | ~4.15% | ~93 bps | 152% |

| Italy | ~3.8% | ~70 bps | 134% |

Legend: Sovereign bond yields and spreads for selected eurozone countries (Spring 2026). Spreads measured versus German 10-year Bund. Debt ratios per Maastricht definition. Source: market data and national statistics offices.

</FinancialData>

| Year | Interest Charges | YoY Change | Share of Budget |

|---|---|---|---|

| 2022 | €51.9B | — | ~7% |

| 2024 | €60.8B | +17.1% | ~8% |

| 2026 | €71.2B | +17.1% | ~9% |

Legend: French sovereign interest expenses and year-over-year growth. 2026 figures from PLF budget annex. Share of total central government budget estimated. Source: French Ministry of Finance budget documents.

</FinancialData>

| Sovereign Bond | Spread vs. Bund (bps) | Yield Convergence |

|---|---|---|

| France OAT 10Y | 78-85 | ~20 bps from Greece |

| Greece OGB 10Y | ~95-105 | Baseline |

| Eurozone Avg (ex-France) | 40 | Reference |

Legend: Bond yield spreads versus German Bunds, Spring 2026. bps = basis points. Historical French spread: 30-45 bps (2014-2022). Source: lecourrierdesstrateges.fr, fibee.fr.

</FinancialData>

| Year | Interest Charges (€B) | % Increase | Debt/GDP Ratio |

|---|---|---|---|

| 2022 | 51.9 | — | ~111% |

| 2024 | 60.8 | +17.1% | ~115.6% |

| 2026 | 71.2-77.0 | +17-27% | 118.3-118.6% |

Legend: French sovereign debt service costs and debt-to-GDP ratios. €B = billions of euros. 2026 figures from budget and Cour des comptes projections. Source: lenouveleconomiste.fr, agefi.fr.

</FinancialData>

| Indicator | Value |

|---|---|

| France 10Y yield (latest) | 3.88% |

| Change over 4 weeks | +7.3 bps |

| Change over 12 months | +35.05 bps |

Legend: French 10-year government bond yield and recent changes (as of May 2026). bps = basis points. A solvency crisis would imply double-digit yields, not these levels.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.