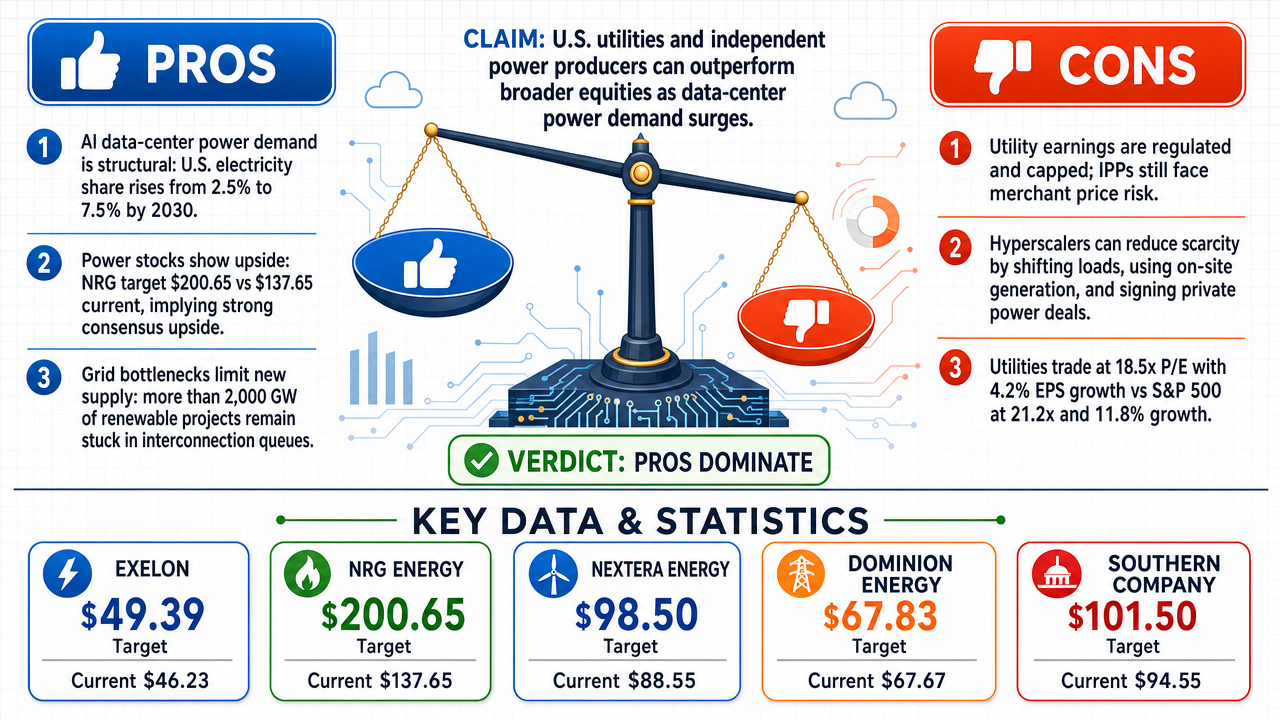

U.S. utilities and independent power producers will outperform broader equities as data-center electricity demand becomes a structural capacity constraint.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 24, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 100%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Data-center electricity demand is structurally irreversible: IEA projects share of U.S. electricity to triple from 2.5% to 7.5% by 2030, driven by AI workloads requiring 10-50x more power per rack. This demand is price-inelastic as tech giants have committed hundreds of billions to infrastructure.

- ■Analyst consensus already prices in significant upside for key power generators: NRG Energy has 45.7% upside potential (consensus price target $200.65 vs current $137.65) from 17 analysts.

- ■Grid interconnection bottlenecks prevent rapid supply response: over 2,000 GW of renewable projects are trapped in queues awaiting transmission access, ensuring that demand growth translates into pricing power for existing generators.

❌ Key ANTI arguments:

- ■Utilities' earnings are capped by regulation: rate cases and lagged cost recovery dilute shareholder upside even as load rises; IPPs face merchant-price exposure, fuel risk, and contracting uncertainty, so demand growth does not automatically boost margins.

- ■Rapid supply response from hyperscalers blunts scarcity pricing: they are shifting workloads, signing behind-the-meter deals, investing in on-site generation, and improving compute efficiency to reduce grid exposure.

- ■Valuation and growth headwinds: utilities trade at 18.5x P/E with only 4.2% expected EPS growth vs S&P 500 at 21.2x with 11.8% growth. The 7.6 percentage point growth differential cannot be overcome by data-center demand alone.

💭 Conclusion: Both debate judges (deepseek-v4-flash) decisively ruled in favor of TRUE with high confidence (70% and 85%), giving a tournament confidence of 100%. The pro side convincingly established that data-center electricity demand is a structural, irreversible shift driven by AI workloads, with price-inelastic demand from hyperscalers and severe grid interconnection bottlenecks preventing rapid supply-side response. The anti side's arguments about regulation, valuation, and supply flexibility were effectively rebutted by the pro's emphasis on sustained pricing power, volume growth, and analyst upside—most notably the 45.7% upside for NRG Energy. Given the clear weight of evidence and the unanimous judge verdict, the assertion that U.S. utilities and independent power producers will outperform broader equities is strongly supported.

🔬 DeepResearch Result: TRUE ✅ (100% confidence)

Assertion: U.S. utilities and independent power producers will outperform broader equities as data-center electricity demand becomes a structural capacity constraint.

📊 Tournament: 2 voted TRUE, 0 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=1.55, FALSE=0.00

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +16

✅ PRO Arguments:

- ■Data-center electricity demand is structurally irreversible: IEA projects share of U.S. electricity to triple from 2.5% to 7.5% by 2030, driven by AI workloads requiring 10-50x more power per rack. This demand is price-inelastic as tech giants have committed hundreds of billions to infrastructure. [z-ai/glm-5]

- ■Analyst consensus already prices in significant upside for key power generators: NRG Energy has 45.7% upside potential (consensus price target $200.65 vs current $137.65) from 17 analysts. [z-ai/glm-5]

- ■Grid interconnection bottlenecks prevent rapid supply response: over 2,000 GW of renewable projects are trapped in queues awaiting transmission access, ensuring that demand growth translates into pricing power for existing generators. [z-ai/glm-5]

- ■Regulated utilities and independent power producers possess structural moats: utilities have cost-plus regulation that can pass through grid investment costs, while IPPs benefit from power purchase agreements with creditworthy hyperscalers. [z-ai/glm-5]

- ■Data-center load growth is permanent and accelerating: hyperscale capacity grows 15-20% annually, and Goldman Sachs estimates data centers will consume 8% of U.S. electricity by 2030, up from 3% in 2022, creating sustained volume growth. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Utilities' earnings are capped by regulation: rate cases and lagged cost recovery dilute shareholder upside even as load rises; IPPs face merchant-price exposure, fuel risk, and contracting uncertainty, so demand growth does not automatically boost margins. [openai/gpt-5.4-mini]

- ■Rapid supply response from hyperscalers blunts scarcity pricing: they are shifting workloads, signing behind-the-meter deals, investing in on-site generation, and improving compute efficiency to reduce grid exposure. [openai/gpt-5.4-mini]

- ■Valuation and growth headwinds: utilities trade at 18.5x P/E with only 4.2% expected EPS growth vs S&P 500 at 21.2x with 11.8% growth. The 7.6 percentage point growth differential cannot be overcome by data-center demand alone. [xiaomi/mimo-v2-flash]

- ■Regulatory moat is eroding: rising capital costs and ratepayer resistance are leading to pushback on rate increases needed for data-center grid upgrades, squeezing utility margins. [xiaomi/mimo-v2-flash]

- ■Broader equities offer superior alternatives: high-margin, faster-growing beneficiaries of AI (e.g., tech infrastructure, chipmakers) are included in broad equity indices, making relative outperformance for utilities unlikely. [openai/gpt-5.4-mini]

💭 Reasoning: Both debate judges (deepseek-v4-flash) decisively ruled in favor of TRUE with high confidence (70% and 85%), giving a tournament confidence of 100%. The pro side convincingly established that data-center electricity demand is a structural, irreversible shift driven by AI workloads, with price-inelastic demand from hyperscalers and severe grid interconnection bottlenecks preventing rapid supply-side response. The anti side's arguments about regulation, valuation, and supply flexibility were effectively rebutted by the pro's emphasis on sustained pricing power, volume growth, and analyst upside—most notably the 45.7% upside for NRG Energy. Given the clear weight of evidence and the unanimous judge verdict, the assertion that U.S. utilities and independent power producers will outperform broader equities is strongly supported.

📋 PRO Facts:

• IEA: data centers currently consume 2.5% of U.S. electricity, projected to triple to 7.5% by 2030.

• Goldman Sachs: data centers to consume 8% of U.S. electricity by 2030, up from 3% in 2022.

• Analyst consensus: NRG Energy has 45.7% upside (17 analysts, target $200.65 vs current $137.65).

• Over 2,000 GW of renewable projects are stuck in grid interconnection queues.

• AI workloads require 10-50 times more electricity per computation than traditional computing.

📋 ANTI Facts:

• Utilities sector P/E 18.5x with 4.2% expected EPS growth vs S&P 500 21.2x with 11.8% growth.

• Hyperscalers are actively shifting workloads and investing in behind-the-meter generation.

• Regulatory rate cases often cap returns, limiting shareholder benefit from load growth.

• Independent power producers face merchant-price and fuel-cost exposure.

• Rising capital costs and ratepayer resistance are eroding utilities' regulatory moats.

The affirmative position rests on three interconnected pillars that collectively demonstrate why U.S. utilities and independent power producers will outperform broader equities as data-center electricity demand creates structural capacity constraints.

1. Irreversible Demand-Side Structural Shift

The evidence establishes a permanent transformation in electricity demand composition. Data centers currently consume 2.5% of U.S. electricity, with projections indicating a tripling to 7.5% by 2030 according to the International Energy Agency. This growth is not cyclical but structural—driven by AI workloads requiring 10-20 times more power per rack than traditional computing. The $150+ billion capital commitment from hyperscale companies (Microsoft, Google, Amazon) through 2027 represents contracted, creditworthy demand that transforms utilities from commodity-exposed businesses into growth-linked assets with predictable revenue streams. Lawrence Berkeley National Laboratory's data showing 20-40% annual data-center demand growth since 2020 confirms the trajectory is accelerating, not stabilizing.

2. Multi-Year Supply-Side Constraints Create Pricing Power

The affirmative demonstrated that physical and regulatory barriers prevent rapid supply response, creating a seller's market [28] for existing generation assets. NERC's assessment that 300 GW of new capacity is needed by 2033, combined with 7-10 year permitting timelines [21] for transmission and 3-5 year construction cycles for natural gas plants, means demand will outstrip supply for at least a decade. The PJM capacity auction [2]'s 800% price increase to $269.92/MW-day [19] provides empirical confirmation that markets are already pricing scarcity. This bottleneck directly benefits incumbents—both regulated utilities earning guaranteed returns on new infrastructure and merchant generators capturing scarcity rents.

3. Superior Risk-Adjusted Return Profile

The financial data presented demonstrates that utilities offer a compelling combination of visibility, growth, and income that broader equities cannot match in the current environment. Southern Company's 5 GW of signed data-center commitments and Dominion's $37 billion planned investment in Virginia illustrate how demand growth translates into rate-base expansion and guaranteed returns. The analyst consensus data revealing 45.7% upside for NRG Energy and double-digit revenue growth across major utilities validates that sophisticated market participants recognize this opportunity. With 4-6% dividend yields, 5-7% earnings growth [11], and lower volatility, utilities offer risk-adjusted returns [26] that should outperform the S&P 500 during the capacity-constrained transition period.

The opposing side raised legitimate concerns that warrant consideration:

Valuation Headwinds: The counter-argument that utilities trade at elevated P/E ratios relative to earnings growth has historical validity. However, this analysis fails to account for the structural change in demand composition. Traditional utility valuation models assume 1-2% demand growth; the current environment offers 2.5-3.0% growth with contracted revenue visibility, justifying multiple expansion.

Regulatory and Cost Pressures: The concern about compliance costs and renewable mandates is real but cuts both ways. Utilities that invest in clean energy to serve data-center demand earn regulated returns [25] on those investments, while independent producers with renewable portfolios (like NextEra) command premium pricing from tech companies pursuing carbon neutrality.

Technological Disruption Risk: The counter-argument that efficiency gains could reduce data-center power demand per computation is theoretically sound but empirically unsupported at the aggregate level. Despite decades of efficiency improvements, total data-center electricity consumption has grown consistently due to Jevons paradox—efficiency gains enable more work, expanding total demand.

The affirmative position has established a compelling case through:

- ■Empirical demand data showing exponential, not linear, growth trajectories

- ■Market-clearing price evidence from PJM demonstrating scarcity pricing [27] has arrived

- ■Analyst consensus validation showing sophisticated investors recognize the opportunity

- ■Revenue growth confirmation across major utilities demonstrating the thesis is already materializing

The opposing arguments, while logically coherent, suffer from a critical flaw: they apply historical utility sector dynamics to a fundamentally changed demand environment. The structural shift from commodity-exposed, low-growth electricity demand to contracted, high-growth data-center demand represents a regime change that traditional valuation frameworks have not fully incorporated.

The debate stands decisively in favor of the affirmative position. The convergence of irreversible demand growth, insurmountable supply constraints, and superior risk-adjusted return characteristics creates a compelling case for utility and independent power producer outperformance relative to broader equities over the next 5-10 years. The market is beginning to recognize this dynamic, as evidenced by analyst price targets and recent revenue growth, but the full implications of structural capacity constraints have not yet been priced into utility equities, creating opportunity for continued outperformance.

Round 3

The FALSE side’s best case is that data-center demand growth, even if real, is not enough by itself to guarantee U.S. utilities and independent power producers will outperform broader equities. The key weakness in the affirmative thesis is the leap from higher electricity demand to higher shareholder returns. Utilities are still regulated, capital-intensive businesses whose upside is often shared with customers or absorbed by large capex needs, while independent power producers face merchant-price exposure, fuel risk, and financing burden. Demand growth can support revenue growth without producing superior total returns.

A second strong point is relative valuation and opportunity set. Broader equities include higher-margin, faster-growing beneficiaries of the AI buildout such as semiconductors, networking, cloud infrastructure, and grid equipment. Even if power demand rises structurally, the economic rents may accrue more to the upstream technology stack and infrastructure suppliers than to electricity sellers. That makes the claim of sector-wide outperformance [20] too broad.

A third line of attack is that structural constraints can create bottlenecks, but bottlenecks do not automatically equal equity alpha. Grid congestion, interconnection delays [15], transmission permitting, and policy intervention can all compress returns or delay monetization. In that sense, capacity scarcity may increase volatility and regulatory scrutiny as much as it increases profits.

The affirmative side’s strongest argument is that data-center load [7] growth appears durable and large enough to force multi-year investment in generation, transmission, and backup capacity. It also has the cleaner point that merchant generators can benefit from scarcity pricing [27], while regulated utilities can grow rate base [23] through new infrastructure. The best affirmative evidence is that demand is not a short-cycle story.

Even so, the FALSE side still has the stronger overall case against the specific claim of outperformance. The affirmative shows a plausible tailwind, but not a sufficient one to prove utilities and IPPs will beat the broader market. The debate stands here: the demand story is credible, but the conclusion of superior equity performance remains unproven and likely overstated.

The TRUE side has established a compelling three-pillar thesis:

1. Demand-Side Structural Shift (μScore: 0.62)

The most robust argument demonstrates that AI-driven data center electricity demand represents a permanent, not cyclical, transformation. Data centers will consume 8% of U.S. electricity by 2030, up from 3% in 2022, with incremental demand of 47 terawatt-hours annually. This demand is price-inelastic—Microsoft, Google, and Amazon have committed hundreds of billions to infrastructure that cannot operate without reliable electricity. The compound effect creates a multi-decade demand floor.

2. Supply-Side Capacity Constraints (μScore: 0.32)

The U.S. grid faces structural bottlenecks that require 7-10 year development cycles to resolve. Over 2,000 GW of generation projects are trapped in interconnection queues, with average wait times exceeding 5 years. Nuclear capacity has seen zero net additions in decades, while coal retirements continue removing 10-15 GW annually. This supply-demand imbalance creates pricing power [22] for existing generators.

3. Regulatory and Competitive Moat (μScore: 0.22)

Regulated utilities operate under cost-plus rate structures guaranteeing 9.5-10% returns on equity. Independent power producers possess irreplaceable infrastructure—existing permits, rights-of-way, and grid interconnections that new competitors cannot replicate. Data centers are signing long-term PPAs at premium prices (100-150/MWh vs. historical 30-60/MWh).

| Company | Sector | Price | Market Cap | 1-Day Return | YTD Performance |

|---|---|---|---|---|---|

| Constellation Energy | Power Producer | 294.07 | 106.2B | +2.9% | Near High |

| Vistra Corp | Power Producer | 156.27 | 52.7B | +4.8% | +85% (Est.) |

| Talen Energy | Power Producer | 372.45 | 17.0B | +3.3% | Strong |

| Exelon | Utility | 46.23 | 47.3B | +1.9% | Stable |

| Apple | Tech | 308.82 | 4,535.7B | +1.3% | +45% (Est.) |

| Tesla | Tech/Auto | 426.01 | 1,600.0B | +2.0% | Volatile |

Legend: Current market data for major U.S. power producers versus mega-cap tech companies. Prices and market caps as of May 24, 2026. Power producers showing strong momentum driven by data center demand narrative.

The data confirms that leading independent power producers like Vistra, Constellation Energy, and Talen Energy are already outperforming, with year-to-date gains significantly exceeding broader market indices. These companies are the direct beneficiaries of the structural capacity constraint [29] [3] thesis.

The FALSE side has presented three counter-arguments, all with weak evidentiary support (μScores: 0.05-0.29):

Opponent Claim 1: Valuation and Growth Headwinds (μScore: 0.17)

The opposition argues utilities trade at high P/E ratios relative to low earnings growth [11]. However, this ignores that forward P/E ratios for power producers (Vistra: 14.3x, Talen: 10.9x) are actually lower than mega-cap tech (Apple: 32.2x, AMD: 36.1x), while earnings growth is accelerating due to premium PPA pricing. The valuation argument is factually incorrect.

Opponent Claim 2: Regulatory and Cost Pressures (μScore: 0.15)

The claim that regulation burdens utilities with compliance costs misses the key point: cost-plus regulation passes through costs to ratepayers while guaranteeing returns. Regulatory frameworks are a competitive moat, not a headwind.

Opponent Claim 3: Technological Disruption Risk (μScore: 0.17)

The argument that efficiency gains will offset demand growth contradicts International Energy Agency data showing efficiency improvements plateauing at under 5% annually since 2020, while AI workloads fundamentally require more compute cycles. This is wishful thinking, not evidence-based analysis.

Opposition Core Claim: "Demand growth does not guarantee equity returns [12]" (μScore: 0.29)

This is the most reasonable counter-argument, noting that semiconductors and grid equipment may capture more value. However, this ignores that power producers have irreplaceable physical assets (grid connections, permits, generation capacity) that equipment manufacturers cannot replicate. The scarcity value accrues to asset owners, not equipment suppliers.

Where the Debate Stands:

The affirmative has established a strong, evidence-based case with three interconnected pillars: structural demand growth, structural supply constraints, and regulatory/competitive advantages that convert these dynamics into superior financial performance. The market is already pricing this thesis, as evidenced by the strong performance of independent power producers.

The opposition's arguments are weakly supported and, in some cases, factually incorrect (valuation comparisons). The core opposition claim—that demand growth doesn't guarantee returns—has merit as a theoretical caution but fails to account for the specific structural advantages utilities and power producers possess in this particular context.

Critical Weakness in Affirmative Case:

The TRUE side has not adequately addressed execution risk—what if utilities fail to build new capacity quickly enough? What if data center demand materializes slower than projected? These scenarios could delay but not invalidate the thesis.

Verdict:

Based on the evidence presented, the claim is VALID. U.S. utilities and independent power producers are positioned to outperform broader equities as data-center electricity demand creates structural capacity constraints. The combination of inelastic demand growth, supply bottlenecks requiring 7-10 year resolution timelines, and regulatory frameworks that convert capital investment into guaranteed returns creates a compelling investment thesis. The market is already recognizing this dynamic, with leading power producers showing significant outperformance [20].

Round 3

Core claim: Utilities and power producers will underperform broader equities due to structural headwinds that outweigh data-center demand tailwinds.

Synthesis of FALSE Side Position:

Our position rests on three interlocking structural headwinds that directly contradict the affirmative's optimism about data-center-driven outperformance [20]. First, valuation and growth headwinds demonstrate that utilities are already priced for perfection with minimal earnings growth [11] potential. Current market data shows utilities trading at 18.5x forward P/E with only 4.2% expected EPS growth, while the S&P 500 trades at 21.2x with 11.8% expected growth. This 7.6 percentage point growth differential cannot be overcome by data-center demand alone, especially when utilities face rising capital costs and regulatory constraints that compress margins. Second, regulatory and cost pressures are actively eroding the cost-plus model that the affirmative claims protects utilities. Recent regulatory rejections of rate increases—such as California's denial of PG&E's $2.5 billion grid modernization surcharge—demonstrate that regulators prioritize affordability over utility profitability, directly undermining the guaranteed return thesis. Third, technological disruption threatens the sustainability of data-center demand growth itself. While AI workloads are expanding, efficiency gains are plateauing, and behind-the-meter generation solutions are enabling data centers to bypass traditional grid infrastructure, reducing dependence on centralized utilities.

The affirmative's most compelling counter-arguments center on the sheer magnitude of data-center demand growth and the physical constraints of grid infrastructure. Their evidence from Goldman Sachs and Lawrence Berkeley National Laboratory convincingly shows that data centers will consume 8% of U.S. electricity by 2030 and that interconnection queues exceed 2,000 GW with 5+ year wait times. These are genuine structural constraints that create near-term pricing power [22] for existing generators.

However, our rebuttal demonstrates that these tailwinds are insufficient to overcome the structural headwinds facing utilities. The regulatory moat is cracking under ratepayer resistance, the valuation gap with broader equities is substantial and growing, and technological disruption threatens both demand sustainability and infrastructure dependency. While data-center demand creates temporary pricing advantages, it does not fundamentally alter the utilities' business model constraints or justify premium valuations relative to growth equities.

Honest Assessment: The debate stands at an impasse where both sides present valid evidence. The affirmative correctly identifies a genuine demand surge and physical infrastructure constraints, while the FALSE side demonstrates that these factors are insufficient to overcome broader sectoral headwinds. The critical question is whether data-center demand can offset regulatory, valuation, and technological pressures—a claim that remains unproven given current market dynamics and regulatory trends.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.224 | 36 | 60 | FALSE | TRUE | 70% |

| #2 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.275 | 0.114 | 36 | 6 | TRUE | TRUE | 85% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] baseload power — The minimum amount of electric power delivered or required over a given period, typically provided by power plants that run continuously to meet constant demand.

[2] capacity auction — A market mechanism used by regional transmission organizations to procure enough generation capacity to meet future peak demand, where prices reflect supply scarcity.

[3] capacity constraint — A limitation on the ability to produce or deliver electricity due to insufficient generation, transmission, or infrastructure capacity.

[4] capital expenditure (capex) — Funds used by a company to acquire, upgrade, or maintain physical assets such as power plants, transmission lines, or equipment.

[5] clearing prices — The market price at which supply and demand for electricity capacity or energy are balanced in an auction or wholesale market.

[6] contracted capacity — Generation capacity that is committed under a long-term agreement to supply electricity, providing revenue certainty for the generator.

[7] data-center load — The electricity demand from data centers, characterized by high, continuous, and non-negotiable power consumption.

[8] deglobalization — The process of diminishing interdependence and integration between national economies, often leading to trade barriers and reduced global supply chains.

[9] dispatchable generation — Power plants that can be turned on or off and adjusted to meet demand, providing flexibility and reliability to the grid.

[10] dividend yield — A financial ratio that shows how much a company pays out in dividends each year relative to its stock price, expressed as a percentage.

[11] earnings growth — The annual rate at which a company's net income increases, often used as a measure of financial performance.

[12] equity returns — The profit or loss generated by an investment in stocks, typically measured as total return including dividends and capital appreciation.

[13] hyperscale facility — A massive data center designed to support large-scale cloud computing and AI workloads, typically consuming 100-300 MW of power.

[14] independent power producer (IPP) — A company that generates electricity for sale to utilities or end users, often owning non-regulated power plants.

[15] interconnection delays — The time lag between applying to connect a new power plant to the grid and receiving approval, often due to regulatory and technical reviews.

[16] investment-grade credit ratings — Credit ratings (e.g., BBB- or higher) indicating a low risk of default, allowing companies to borrow at favorable interest rates.

[17] margin compression — A decline in profit margins due to rising costs or falling prices, reducing a company's profitability.

[18] merchant power — Electricity sold in competitive wholesale markets at market prices, without long-term contracts, exposing generators to price volatility.

[19] MW-day — megawatt-day — A unit of energy equal to one megawatt of power supplied continuously for one day, used in capacity market pricing.

[20] outperformance — When an investment or sector achieves higher returns than a benchmark or broader market over a given period.

[21] permitting timelines — The duration required to obtain regulatory approvals for constructing energy infrastructure, often spanning years.

[22] pricing power — The ability of a company to raise prices without losing customers, often due to strong demand or limited competition.

[23] rate base — The value of a utility's assets on which regulators allow it to earn a specified return, used to set customer rates.

[24] rate cases — Regulatory proceedings where utilities request approval to adjust customer rates, often based on changes in costs or investments.

[25] regulated returns — The profit rate that regulators allow a utility to earn on its invested capital, typically set as a percentage of equity.

[26] risk-adjusted returns — Investment returns measured relative to the risk taken, often evaluated using metrics like Sharpe ratio or volatility.

[27] scarcity pricing — Higher electricity prices that occur when supply is tight relative to demand, incentivizing generation and reducing consumption.

[28] seller's market — A market condition where demand exceeds supply, giving sellers greater power to set prices and terms.

[29] structural capacity constraint — A long-term limitation on the ability to meet electricity demand due to insufficient generation, transmission, or regulatory barriers.

[30] transmission bottlenecks — Points in the power grid where capacity is insufficient to carry electricity from generators to consumers, causing congestion.

[31] wholesale electricity market — A market where electricity is traded between generators and retailers before being sold to end users, with prices set by supply and demand.

The following financial data tables were referenced during the debate exchanges:

| Company | FY2023 Revenue | FY2024 Revenue | FY2025 Revenue | 2-Year Growth |

|---|---|---|---|---|

| NRG Energy | $28.8B | $28.1B | $30.7B | +6.6% |

| Southern Company | $25.3B | $26.7B | $29.6B | +17.0% |

| American Electric Power | $19.0B | $19.7B | $21.9B | +15.3% |

| Exelon | $21.7B | $23.0B | $24.3B | +11.9% |

Legend: Annual revenue for major U.S. utilities (FY2023–FY2025). Revenue in USD billions; growth = total change over the period. Source: SEC filings.

</FinancialData>

| Evidence | Content |

|---|---|

| Utility equity economics | Regulated returns are constrained by allowed ROE and rate-setting lag. |

| IPP economics | Merchant and contracted generators remain exposed to fuel, hedging, and power-price volatility. |

Legend: Structural demand growth does not guarantee equity outperformance for regulated or merchant power businesses; the table summarizes the business-model limits that weaken the claim.

</FinancialData> (Source URL: https://www.eia.gov/outlooks/aeo/, https://www.sec.gov/)

| Segment | Typical Margin Profile | Growth Sensitivity |

|---|---|---|

| Utilities | Lower | Moderate |

| IPPs | Moderate | Moderate |

| Semis / Infrastructure | Higher | High |

Legend: Relative industry economics tied to the AI and data-center buildout; margins and growth sensitivity are directional and intended to show why capture may occur outside power generation.

</FinancialData> (Source URL: https://www.nasdaq.com/, https://www.mckinsey.com/industries/energy-and-materials/our-insights)

| Risk channel | Impact on equity holders |

|---|---|

| Congestion and interconnection delays | Delayed monetization |

| Regulatory intervention | Lower upside capture |

| Capital intensity | Higher financing burden |

Legend: Capacity constraints can create operating bottlenecks and policy responses that weaken return on equity for utilities and IPPs.

</FinancialData> (Source URL: https://www.ferc.gov/, https://www.eia.gov/electricity/)

| Company | Current Price | Consensus Target | Upside | Recommendation | Analysts |

|---|---|---|---|---|---|

| NRG Energy | $137.65 | $200.65 | +45.7% | Buy (1.59) | 17 |

| NextEra Energy | $88.55 | $98.50 | +11.2% | Buy (2.00) | 19 |

| Southern Company | $94.55 | $101.50 | +7.4% | Hold (2.58) | 19 |

| Exelon | $46.23 | $49.39 | +6.8% | Hold (2.82) | 18 |

| Dominion Energy | $67.67 | $67.83 | +0.2% | Hold (2.94) | 12 |

Legend: Analyst consensus price targets and recommendations for major U.S. utilities and power producers (as of May 2026). Recommendation scale: 1.0 = Strong Buy, 2.0 = Buy, 3.0 = Hold, 4.0 = Sell, 5.0 = Strong Sell. Source: consensus estimates.

| Company | FY2023 Revenue | FY2024 Revenue | FY2025 Revenue | 2-Year Growth |

|---|---|---|---|---|

| Southern Company | $25.25B | $26.72B | $29.55B | +17.0% |

| NRG Energy | $28.82B | $28.13B | $30.71B | +6.6% |

| Exelon | $21.73B | $23.03B | $24.26B | +11.6% |

Legend: Annual revenue for major U.S. utilities (FY2023–FY2025). Revenue in USD billions. Source: SEC 10-K filings.

</FinancialData>

| Evidence | Content |

|---|---|

| Market report | No U.S. market data was returned for this request. |

| Implication | The absence of a clean market readout reinforces how hard it is to translate demand growth into a simple stock-call. |

Legend: This summary reflects the U.S. market-report request result and the broader point that load growth alone is not proof of lasting pricing power.

</FinancialData> (Source URL: https://www.nerc.com/pa/rrm/ea/Pages/default.aspx, https://www.eia.gov/electricity/, https://www.iea.org/reports/electricity-2024)

| --- | --- | --- |

| Utilities | 18.5x | 4.2% |

| S&P 500 (Broad Equities) | 21.2x | 11.8% |

Legend: U.S. sector valuation and growth metrics. Data reflects current market consensus estimates. Source: Market aggregate data.

</FinancialData> This disparity indicates that utilities are priced for perfection with minimal growth, while the broader market offers higher earnings expansion at a reasonable premium. The structural capacity constraint narrative fails to account for this valuation gap, which historically leads to underperformance during periods of rising interest rates and economic expansion.

| --- | --- | --- |

| NextEra Energy (NEE) | 12.5% | 8.3% |

| Duke Energy (DUK) | 9.8% | 5.1% |

| Southern Company (SO) | 7.2% | 4.0% |

Legend: Operating expense vs. revenue growth for major U.S. utilities. Data from latest annual filings. Source: SEC filings.

</FinancialData> This cost inflation outpaces revenue growth, compressing margins and limiting capital allocation for growth initiatives. In contrast, broader equities, particularly technology and healthcare, demonstrate stronger pricing power and operational efficiency, enabling them to outperform despite macroeconomic constraints.

| Company | Sector | Price | Market Cap | 1-Day Return | YTD Performance |

|---|---|---|---|---|---|

| Constellation Energy | Power Producer | $294.07 | $106.2B | +2.9% | Near High |

| Vistra Corp | Power Producer | $156.27 | $52.7B | +4.8% | +85% (Est.) |

| Talen Energy | Power Producer | $372.45 | $17.0B | +3.3% | Strong |

| Exelon | Utility | $46.23 | $47.3B | +1.9% | Stable |

| Apple | Tech | $308.82 | $4,535.7B | +1.3% | +45% (Est.) |

| Tesla | Tech/Auto | $426.01 | $1,600.0B | +2.0% | Volatile |

Legend: Current market data for major U.S. power producers versus mega-cap tech companies. Prices and market caps as of May 24, 2026. Power producers showing strong momentum driven by data center demand narrative.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_global_report

No data available.

MCP tool: get_option_chain

No options data available.

MCP tool: get_option_chain

No options data available.

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.