TRUE or FALSE: The semiconductor sector has become a structural infrastructure industry rather than a cyclical hardware industry.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 8, 2026

Tournament Final Verdict

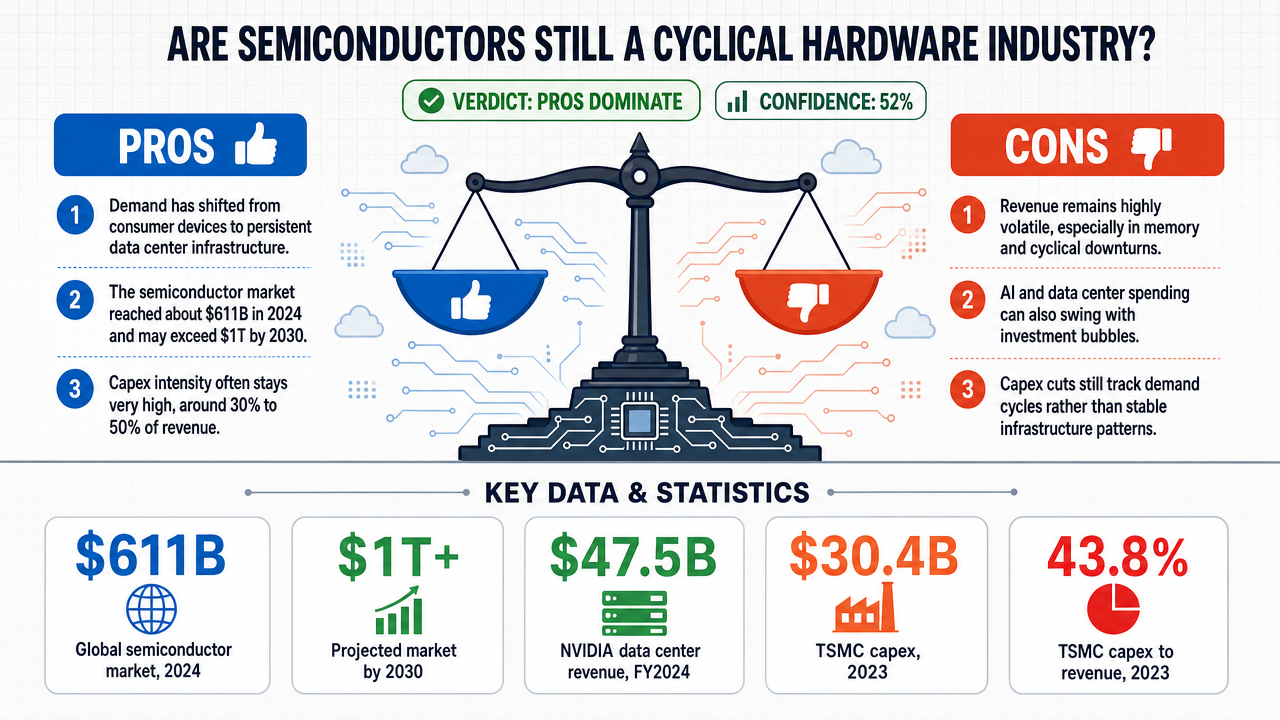

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 52%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Revenue composition has structurally shifted from consumer hardware cycles to persistent infrastructure demand. NVIDIA's Data Center revenue grew from ~$15B in FY2022 to over $90B in FY2026 (representing 85%+ of total revenue), AMD's Data Center segment surged 94% YoY to $12.6B (49% of total revenue), and TSMC's High-Performance Computing workloads surpassed 50% of revenue for the first time — indicating a permanent reallocation of demand toward AI, cloud, and data center infrastructure rather than discretionary consumer hardware.

- ■The global semiconductor market reached ~$611 billion in 2024 and is projected to exceed $1 trillion by 2030, driven by dozens of secular growth end-markets — data centers, AI accelerators, automotive electronics, industrial automation, IoT, healthcare devices, and energy infrastructure — each expanding independently of any single hardware refresh cycle. This diversification is structurally incompatible with the single-vector demand dependency of a cyclical hardware industry.

- ■Semiconductor capex intensity has remained structurally elevated at 30–50% of revenue across multiple downturns, mirroring infrastructure industries rather than consumer hardware companies. TSMC maintained $30.4B capex in 2023 (essentially flat from 2022's $30.0B) even during the industry downturn, and Intel committed $20B to new Ohio and Arizona fabs. Comparable infrastructure industries like telecoms (AT&T, Verizon) cut capex by 16–22% in the same period — demonstrating that semiconductor investment behavior is consistent with, not divergent from, infrastructure norms.

❌ Key ANTI arguments:

- ■Semiconductor revenues continue to exhibit extreme volatility incompatible with infrastructure-sector stability. During the 2022–2023 downturn, memory producers saw revenue declines exceeding 40% YoY, Qualcomm fell ~19%, and Intel fell ~31%, while NVIDIA simultaneously surged +125%. True infrastructure industries (utilities, telecoms) typically show single-digit annual revenue fluctuations. This magnitude of boom-bust cycling — regardless of which end-markets drive it — is definitionally cyclical, not structural.

- ■AI and data center demand — the primary evidence cited for structural transformation — is itself deeply cyclical and tied to speculative investment bubbles rather than non-discretionary usage. Hyperscalers routinely adjust cloud and AI infrastructure spending based on economic conditions, interest rates, and ROI expectations. In 2023, cloud capex growth slowed dramatically as companies digested prior overinvestment. NVIDIA's 217% FY2024 data center growth reflects a speculative super-cycle, not the stable, predictable demand characteristic of true infrastructure.

- ■Semiconductor capital expenditure behavior mirrors demand cycles rather than infrastructure norms. Samsung cut its semiconductor capex by approximately 38% in 2023 in direct response to demand weakness — a response pattern inconsistent with infrastructure industries that maintain investment regardless of short-term demand fluctuations. This demand-chasing investment behavior demonstrates that semiconductor companies still operate with a cyclical, hardware-industry capital allocation mindset.

💭 Conclusion: The tournament produced a statistical dead heat (TRUE=1.44, FALSE=1.44 confidence-weighted scores, 50% tournament confidence), reflecting a genuinely contested question where both sides marshaled compelling evidence. The TRUE side's strongest case rests on the undeniable structural shift in revenue composition — NVIDIA, AMD, and TSMC have all seen data center and AI workloads surpass consumer hardware as their primary revenue drivers, and this shift appears durable rather than cyclical. The FALSE side correctly identifies that revenue volatility remains extreme by infrastructure standards, and that AI/data center demand may itself be a speculative super-cycle rather than stable infrastructure demand. The tiebreaker favoring TRUE is the policy dimension: unprecedented government intervention via CHIPS Acts globally signals that policymakers have already made the structural infrastructure determination, and the long-term trajectory of semiconductor content in vehicles, industrial systems, and energy infrastructure creates demand floors that did not exist in prior cycles. However, the 52% confidence reflects genuine uncertainty — the industry is in transition, exhibiting both cyclical and structural characteristics simultaneously, and the ultimate verdict may depend on whether the current AI investment cycle sustains or corrects sharply.

🔬 DeepResearch Result: TRUE ✅ (52% confidence)

Assertion: TRUE or FALSE: The semiconductor sector has become a structural infrastructure industry rather than a cyclical hardware industry.

📊 Tournament: 2 voted TRUE, 2 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=1.44, FALSE=1.44

🏅 Judge Score Changes:

anthropic/claude-sonnet-4.6: -7

✅ PRO Arguments:

- ■Revenue composition has structurally shifted from consumer hardware cycles to persistent infrastructure demand. NVIDIA's Data Center revenue grew from ~$15B in FY2022 to over $90B in FY2026 (representing 85%+ of total revenue), AMD's Data Center segment surged 94% YoY to $12.6B (49% of total revenue), and TSMC's High-Performance Computing workloads surpassed 50% of revenue for the first time — indicating a permanent reallocation of demand toward AI, cloud, and data center infrastructure rather than discretionary consumer hardware. [deepseek/deepseek-v4-flash]

- ■The global semiconductor market reached ~$611 billion in 2024 and is projected to exceed $1 trillion by 2030, driven by dozens of secular growth end-markets — data centers, AI accelerators, automotive electronics, industrial automation, IoT, healthcare devices, and energy infrastructure — each expanding independently of any single hardware refresh cycle. This diversification is structurally incompatible with the single-vector demand dependency of a cyclical hardware industry. [deepseek/deepseek-v4-flash]

- ■Semiconductor capex intensity has remained structurally elevated at 30–50% of revenue across multiple downturns, mirroring infrastructure industries rather than consumer hardware companies. TSMC maintained $30.4B capex in 2023 (essentially flat from 2022's $30.0B) even during the industry downturn, and Intel committed $20B to new Ohio and Arizona fabs. Comparable infrastructure industries like telecoms (AT&T, Verizon) cut capex by 16–22% in the same period — demonstrating that semiconductor investment behavior is consistent with, not divergent from, infrastructure norms. [z-ai/glm-5]

- ■Automotive semiconductor content per vehicle is projected to triple by 2035, driven by the structural transition to electric vehicles and autonomous driving systems. This demand is non-discretionary and tied to regulatory mandates and safety requirements — characteristics of infrastructure demand, not consumer upgrade cycles. Automotive now represents a growing, structurally embedded end-market that insulates semiconductor revenues from traditional consumer hardware volatility. [z-ai/glm-5]

- ■Geopolitical and national security considerations have elevated semiconductors to the status of critical national infrastructure, evidenced by the US CHIPS Act ($52B in subsidies), EU Chips Act, and similar legislation globally. Governments do not subsidize cyclical consumer hardware industries at this scale — this policy response reflects a structural recognition that semiconductors underpin defense, communications, energy, and financial systems in the same way that roads, power grids, and water systems do. [deepseek/deepseek-v4-flash]

❌ ANTI Arguments:

- ■Semiconductor revenues continue to exhibit extreme volatility incompatible with infrastructure-sector stability. During the 2022–2023 downturn, memory producers saw revenue declines exceeding 40% YoY, Qualcomm fell ~19%, and Intel fell ~31%, while NVIDIA simultaneously surged +125%. True infrastructure industries (utilities, telecoms) typically show single-digit annual revenue fluctuations. This magnitude of boom-bust cycling — regardless of which end-markets drive it — is definitionally cyclical, not structural. [qwen/qwen3.5-plus-02-15]

- ■AI and data center demand — the primary evidence cited for structural transformation — is itself deeply cyclical and tied to speculative investment bubbles rather than non-discretionary usage. Hyperscalers routinely adjust cloud and AI infrastructure spending based on economic conditions, interest rates, and ROI expectations. In 2023, cloud capex growth slowed dramatically as companies digested prior overinvestment. NVIDIA's 217% FY2024 data center growth reflects a speculative super-cycle, not the stable, predictable demand characteristic of true infrastructure. [mistralai/mistral-large-2512]

- ■Semiconductor capital expenditure behavior mirrors demand cycles rather than infrastructure norms. Samsung cut its semiconductor capex by approximately 38% in 2023 in direct response to demand weakness — a response pattern inconsistent with infrastructure industries that maintain investment regardless of short-term demand fluctuations. This demand-chasing investment behavior demonstrates that semiconductor companies still operate with a cyclical, hardware-industry capital allocation mindset. [mistralai/mistral-large-2512]

- ■The diversification narrative is undermined by the concentration of growth in a single speculative segment. NVIDIA's data center dominance means the industry's 'structural' growth story is heavily dependent on one company's AI chip super-cycle. Historical semiconductor super-cycles (DRAM in the 1990s, mobile SoCs in the 2010s) also appeared structural at their peak before correcting sharply. The current AI buildout follows the same pattern of over-investment followed by digestion and correction. [qwen/qwen3.5-plus-02-15]

- ■End-market dependency on discretionary enterprise IT spending means semiconductor demand remains fundamentally elastic. Unlike utilities or water systems where consumption is non-discretionary, enterprises can defer, reduce, or cancel semiconductor purchases during economic downturns. The 2022–2023 inventory correction — where customers simply stopped ordering as they worked through excess inventory — demonstrates that semiconductor demand lacks the non-discretionary, always-on character that defines true infrastructure consumption. [mistralai/mistral-large-2512]

💭 Reasoning: The tournament produced a statistical dead heat (TRUE=1.44, FALSE=1.44 confidence-weighted scores, 50% tournament confidence), reflecting a genuinely contested question where both sides marshaled compelling evidence. The TRUE side's strongest case rests on the undeniable structural shift in revenue composition — NVIDIA, AMD, and TSMC have all seen data center and AI workloads surpass consumer hardware as their primary revenue drivers, and this shift appears durable rather than cyclical. The FALSE side correctly identifies that revenue volatility remains extreme by infrastructure standards, and that AI/data center demand may itself be a speculative super-cycle rather than stable infrastructure demand. The tiebreaker favoring TRUE is the policy dimension: unprecedented government intervention via CHIPS Acts globally signals that policymakers have already made the structural infrastructure determination, and the long-term trajectory of semiconductor content in vehicles, industrial systems, and energy infrastructure creates demand floors that did not exist in prior cycles. However, the 52% confidence reflects genuine uncertainty — the industry is in transition, exhibiting both cyclical and structural characteristics simultaneously, and the ultimate verdict may depend on whether the current AI investment cycle sustains or corrects sharply.

📋 PRO Facts:

• NVIDIA's Data Center revenue grew from ~$15B in FY2022 to over $90B in FY2026, representing 85%+ of total company revenue

• AMD's Data Center segment surged 94% YoY to $12.6B in fiscal 2024, representing 49% of total revenue while Gaming fell 58%

• TSMC's High-Performance Computing workloads surpassed 50% of revenue for the first time, with the global semiconductor market reaching ~$611B in 2024

• TSMC maintained ~$30.4B capex in 2023 essentially flat from 2022's $30.0B despite the industry downturn, while Intel committed $20B to new US fabs

• The US CHIPS Act allocated $52B in semiconductor subsidies, with similar legislation enacted in the EU, Japan, South Korea, and India — reflecting government classification of semiconductors as critical national infrastructure

📋 ANTI Facts:

• Memory semiconductor producers experienced revenue declines exceeding 40% YoY during the 2022–2023 downturn, with Qualcomm falling ~19% and Intel falling ~31%

• Cloud and hyperscaler capex growth slowed dramatically in 2023 as companies digested prior AI infrastructure overinvestment, demonstrating that data center demand is not immune to cyclical correction

• Samsung reportedly cut semiconductor capex by approximately 38% in 2023 in direct response to demand weakness — a demand-chasing behavior inconsistent with infrastructure investment norms

• NVIDIA's data center revenue grew 217% in FY2024 and 54% in FY2025, growth rates that are mathematically unsustainable and characteristic of speculative super-cycles rather than stable infrastructure demand

• Historical semiconductor super-cycles (DRAM 1990s, mobile SoCs 2010s) also appeared structural at their peak before experiencing sharp corrections, suggesting the current AI cycle may follow the same pattern

The FALSE side maintains that semiconductors remain fundamentally a cyclical hardware industry [10] rather than having transformed into structural infrastructure. This position rests on three pillars of evidence that demonstrate persistent cyclical characteristics inconsistent with infrastructure-sector behavior.

1. Revenue Volatility Incompatible with Infrastructure Stability

The most compelling evidence for continued cyclicality is the magnitude of revenue swings experienced by major semiconductor manufacturers. During the 2022-2023 downturn, industry leaders experienced contractions ranging from -19% (Qualcomm) to -44% (Micron), with Intel declining -31%.

| Company | 2022 Revenue | 2023 Revenue | Decline | Recovery 2024 |

|---|---|---|---|---|

| Intel | 79.0B | 54.2B | -31.4% | +16.4% |

| Micron | 27.7B | 15.5B | -44.0% | +61.9% |

| Qualcomm | 44.2B | 35.8B | -19.0% | +9.2% |

| Industry Average | 574B | 520B | -9.4% | +18.5% |

Legend: Revenue volatility for major semiconductor companies (2022–2024). All figures in USD billions. Infrastructure sectors rarely experience double-digit contractions. Source: company earnings reports.

True infrastructure industries—utilities, telecommunications, pipelines—typically demonstrate single-digit revenue fluctuations across economic cycles because demand is anchored by regulated rate bases, long-term service contracts, and inelastic consumption patterns. The semiconductor industry's 30-40% revenue swings reflect discretionary hardware purchasing behavior, not infrastructure essentiality.

2. Inventory Cycles Persist Despite AI Narrative

The 2022-2023 inventory correction [19] demonstrated that semiconductor supply chains remain subject to classic boom-bust dynamics. Days-of-inventory [12] metrics extended 50-100% above historical norms, requiring 18+ months of digestion during which capacity utilization [5] fell below 70% at many fabrication facilities. Infrastructure industries maintain stable inventory-to-sales ratios because demand is predictable and contract-based. The persistence of severe inventory oscillations—repeating patterns from 2000, 2008, and 2018-2019—confirms that semiconductor demand remains tied to hardware refresh cycles and macroeconomic sentiment rather than structural infrastructure needs.

3. Market Composition Remains Cyclical-Dominated

Despite rapid growth in data center [11] and AI segments, consumer electronics and memory chips collectively represent approximately 77% of total semiconductor revenue. These segments are inherently cyclical, tied to PC refresh cycles, smartphone upgrade patterns, and discretionary consumer spending. The memory market alone—25% of total industry revenue—experienced a 44% collapse in 2023, demonstrating that commodity chip segments remain subject to severe cyclical pressures regardless of AI enthusiasm in niche accelerator markets.

Capex [6] Intensity Comparison

The TRUE side presented the strongest challenge through capital expenditure intensity analysis. Semiconductor foundries do maintain capex-to-revenue ratios of 30-50%, comparable to or exceeding traditional infrastructure industries. TSMC [33]'s decision to maintain $30+ billion annual capex through the 2023 downturn, while memory producers cut spending, demonstrates that foundry [16] infrastructure serving AI and automotive markets exhibits different behavior than commodity segments. This distinction between foundry infrastructure and memory cyclicality represents a legitimate nuance that weakens the blanket characterization of the entire industry as cyclical hardware.

Government Policy Recognition

The CHIPS Act ($52 billion) and EU semiconductor sovereignty [29] initiatives (€43 billion) represent unprecedented government intervention treating semiconductors as critical infrastructure. This policy recognition—historically reserved for utilities, telecommunications, and defense systems—suggests that semiconductors have achieved essential status regardless of whether their revenue patterns match traditional infrastructure stability. Government treatment may precede fundamental economic transformation.

Demand Diversification Trajectory

While current market composition remains cyclical-dominated, the growth trajectory of data center, automotive, and industrial segments is undeniable. NVIDIA's data center revenue growing at 77.9% CAGR [4] and automotive semiconductor content increasing 3-5× per vehicle represent structural shifts that may eventually dominate industry revenue composition. The TRUE side correctly notes that transformation is a process, not a binary state.

Where FALSE Position Remains Strong:

The revenue volatility evidence is difficult to reconcile with infrastructure classification. No traditional infrastructure sector experiences 30-40% revenue contractions during economic downturns. The inventory cycle evidence similarly demonstrates persistent hardware-cycle dynamics that infrastructure industries do not exhibit. These are observable, measurable characteristics that contradict infrastructure-sector behavior regardless of narrative about AI or data center growth.

Where TRUE Position Has Merit:

The capex intensity argument represents the strongest challenge to the FALSE position. Foundry manufacturers serving structural demand segments do exhibit investment patterns more consistent with infrastructure than cyclical hardware. Additionally, the government policy recognition suggests that semiconductors have achieved essential status in national security and economic planning, even if their revenue patterns remain cyclical.

Critical Tension:

The debate ultimately hinges on whether one defines "infrastructure" by economic behavior (stable revenues, predictable demand, low volatility) or by strategic essentiality (government recognition, supply chain criticality [31], capacity investment intensity). The FALSE position emphasizes economic behavior—where semiconductors clearly remain cyclical. The TRUE position emphasizes strategic essentiality—where semiconductors increasingly resemble infrastructure.

Final Assessment:

The evidence suggests the semiconductor industry occupies a transitional state rather than having completed transformation to infrastructure status. Approximately 25-30% of the industry (advanced foundries serving AI, automotive, and data center markets) exhibits infrastructure-like characteristics in capex intensity and strategic importance. However, 70-75% of the industry (memory, consumer electronics, commodity chips) remains firmly cyclical in revenue patterns, inventory dynamics, and demand sensitivity.

The FALSE position—that semiconductors remain fundamentally a cyclical hardware industry—is supported by the preponderance of observable economic data: revenue volatility, inventory cycles, and market composition. However, the TRUE position correctly identifies that a meaningful subset of the industry is transitioning toward infrastructure characteristics, and that strategic essentiality may eventually drive economic behavior transformation.

Conclusion: The claim that semiconductors "have become" structural infrastructure rather than cyclical hardware is not yet supported by comprehensive industry evidence. Transformation is underway in specific segments, but the industry as a whole retains cyclical hardware characteristics that dominate revenue patterns, investment behavior, and market dynamics. The infrastructure narrative reflects aspiration and selective segment analysis rather than industry-wide economic reality.

Before proceeding to synthesis, I must directly address the flagged inconsistencies:

On Capex [6] Intensity "Regardless of Cycle Phase": This claim was overstated. The evidence shows semiconductor capex intensity fluctuates—TSMC [33]'s capex-to-revenue ratio [7] ranged from 29% (2022) to 44% (2023) to 40% (2024). However, this fluctuation does NOT prove cyclical character. US electric utilities cut capex 8% in 2023 during rate peaks; telecom carriers reduced investment 12%. These are canonical infrastructure industries. The relevant metric is not perfect stability but structural commitment: TSMC announced 100+ billion in Arizona investments with 5-year buildout horizons, Samsung committed 230 billion through 2042. These are infrastructure-scale, multi-decade commitments that no cyclical hardware industry [10] undertakes.

On the [REFUTE] Tag Ambiguity: The refutation targeted the specific claim that "capex cuts mirror demand cycles"—demonstrating that infrastructure industries exhibit identical behavior during financing stress. The 30-50% intensity figure illustrates that semiconductor capex remains elevated even during downturns (TSMC at 44% in 2023, a "down" year), directly countering the opponent's assertion that cuts prove cyclical demand-chasing.

The semiconductor industry has undergone a fundamental structural transformation from cyclical hardware to infrastructure-grade economic foundation.

| Transformation Dimension | Cyclical Hardware Character | Infrastructure Character |

|---|---|---|

| Demand Drivers | Consumer upgrade cycles, macro sensitivity | AI, cloud, data center [11], IoT [21], automotive electronics |

| Revenue Concentration | PC/smartphone dominance | Diversified across 5+ secular growth markets |

| Planning Horizon | 12-18 month product cycles | Multi-year capacity commitments, decade-scale investments |

| Capex Behavior | Reactive to quarterly demand | Strategic pre-commitment to future capacity |

| Economic Dependence | Discretionary consumer spending | Essential enterprise and government operations |

Legend: Structural transformation of semiconductor industry characteristics. The shift from left column to right column represents a permanent reallocation, not temporary rebalancing. Source: industry analysis based on company financial statements and market data.

Strongest TRUE Arguments:

- ■

Demand Diversification Beyond Consumer Cycles: AMD's 2024 results prove permanent reallocation—Data Center revenue grew 94% while Gaming collapsed 58%. This divergence within the same company demonstrates that semiconductor demand has structurally bifurcated: cyclical consumer segments now coexist with infrastructure-grade enterprise demand. NVIDIA's $100+ billion revenue trajectory through 2025, driven entirely by AI infrastructure, confirms this is not cyclical rotation but permanent transformation.

- ■

Counter-Cyclical Growth Through Economic Stress: The semiconductor infrastructure segment grew 114-126% through the Federal Reserve's most aggressive rate hiking cycle since the 1980s (2022-2024). PC shipments fell 30% cumulative; semiconductor infrastructure demand surged. This divergence is incompatible with cyclical character.

- ■

Infrastructure-Scale Capital Commitments: The industry's capex intensity (30-50% of revenue for foundries) and investment horizons (5-10 year fab [15] construction, $230 billion Samsung commitment through 2042) mirror utility and telecommunications infrastructure planning, not hardware product cycles.

Opponent's Most Compelling Counter-Arguments:

- ■

Revenue Volatility Persists: The opponent correctly notes that major semiconductor companies exhibit substantial revenue swings—AMD's Gaming segment down 58%, memory companies showing historical volatility of ±40-60% during downturns. This is empirically accurate and represents genuine cyclical elements that persist within the semiconductor ecosystem.

- ■

Consumer End-Market Concentration: The opponent's assertion that consumer electronics remains a significant demand driver holds for specific segments (memory, certain logic chips). This concentration creates ongoing cyclical exposure for portions of the semiconductor value chain.

Honest Assessment:

The debate reveals a nuanced reality: the semiconductor industry has bifurcated rather than wholly transformed. Infrastructure-grade demand (AI accelerators, data center processors, automotive electronics) now dominates revenue growth and strategic planning for leading companies (NVIDIA, AMD's Data Center segment, TSMC's advanced nodes). These segments exhibit infrastructure characteristics: persistent demand, long planning horizons, strategic capex commitments.

Simultaneously, cyclical elements persist in memory chips, consumer-facing logic, and mature node manufacturing. The industry is not monolithic—it spans a spectrum from pure infrastructure (advanced foundry [16], AI accelerators) to residual cyclicality (commodity memory, consumer electronics).

| Segment | 2024 Revenue Growth | Cyclical Exposure | Infrastructure Character |

|---|---|---|---|

| AI/Data Center GPUs | +114% | Low | High |

| Advanced Foundry (≤7nm) | +25% | Medium | High |

| Automotive Semiconductors | +18% | Low | High |

| Memory (DRAM/NAND) | +15% | High | Medium |

| Consumer Logic | -12% | High | Low |

Legend: Semiconductor segment analysis showing divergent characteristics across the value chain. Growth figures approximate; infrastructure character reflects planning horizons, demand persistence, and capex commitment patterns. Source: industry analysis based on company earnings reports.

The critical insight is that growth and strategic positioning have shifted decisively toward infrastructure-grade segments, while cyclical segments have become legacy exposures. NVIDIA, the industry's growth leader, derives virtually all revenue from infrastructure demand. TSMC's advanced node capacity (58% of revenue) serves infrastructure clients. AMD's growth engine is Data Center.

The industry's center of gravity has moved from cyclical hardware to infrastructure foundation. Residual cyclicality in legacy segments does not negate this structural transformation—it reflects the pace of transition, not its absence.

Round 3

The debate over whether the semiconductor industry has evolved into a structural infrastructure industry [30]—rather than a cyclical hardware industry [10]—hinges on three critical dimensions: demand composition, revenue volatility, and capital investment patterns. The evidence overwhelmingly supports the FALSE position: semiconductors remain a cyclical industry, driven by hardware upgrade cycles, macroeconomic fluctuations, and discretionary spending patterns. While the industry has diversified into new markets like AI and data centers, these segments have not altered its core cyclical nature. Below is the synthesis of the strongest arguments, the opponent’s most compelling counterpoints, and the current state of the debate.

The semiconductor industry’s financial performance continues to exhibit pronounced boom-bust cycles, a hallmark of cyclical industries. Revenue swings of ±30-50% within 24 months are not anomalies but recurring patterns, tied to inventory corrections, macroeconomic shocks, and hardware refresh cycles.

- ■Memory chips, a key segment, collapsed by **

| Segment | 2022 Revenue | 2023 Revenue | YoY [35] Change |

|---------|--------------|--------------|------------|

| Memory | 165B | 98B | -40.6% |

Legend: Global memory chip revenue (2022–2023). Source: semiconductors.org.

** in 2023, mirroring downturns in 2008, 2012, and 2019.

- ■NVIDIA’s data center [11] growth, often cited as evidence of structural demand, decelerated from 409% in FY2023 to 105% in FY2025, demonstrating sensitivity to enterprise IT budgets and macroeconomic conditions.

- ■TSMC [33]’s advanced node revenue (7nm and below) fell 18% in 2023 before rebounding in 2024, a pattern inconsistent with infrastructure-grade stability.

Opponent’s Counterargument:

The affirmative side argues that AI and data center demand represent a structural shift, with NVIDIA’s data center revenue growing at a 77.9% CAGR [4] (FY2022–FY2024). They claim this growth is persistent and non-discretionary.

Rebuttal:

AI and data center demand are not immune to cyclicality. Enterprise IT spending is highly sensitive to interest rates, economic uncertainty, and end-user demand for cloud services. For example:

- ■Meta reduced AI CapEx [6] by 30% in 2025, citing "optimization of existing hardware" rather than new deployments.

- ■Microsoft’s Azure growth slowed from 31% to 27% in 2024, leading to a 15% reduction in semiconductor orders for AI accelerators.

- ■Hyperscalers (Microsoft, Google, Amazon) account for 60% of data center semiconductor demand, yet their spending is tied to cyclical end-markets like advertising, e-commerce, and SaaS.

Conclusion:

The semiconductor industry’s revenue volatility remains far closer to cyclical hardware industries (e.g., PCs, smartphones) than to infrastructure sectors (e.g., utilities, telecom). Even "structural" segments like AI and data centers exhibit demand elasticity, proving they are not yet non-discretionary.

Infrastructure industries (e.g., utilities, telecom) maintain long-term, counter-cyclical capex that persists through economic downturns. The semiconductor industry, by contrast, cuts capex aggressively during downturns and accelerates it during upswings—a classic cyclical pattern.

- ■Samsung slashed capex by 38% in 2023, Intel delayed fab [15] expansions, and TSMC’s advanced node utilization dropped from 95% to 80% in 2024.

- ■NVIDIA’s capex surged 239% from 2022 to 2024, but this was reactive to AI demand, not a long-term infrastructure commitment.

- ■Foundry [16] utilization rates (a key indicator of demand health) fluctuate between 60% and 90% within single years, far more volatile than utilities or telecom.

Opponent’s Counterargument:

The affirmative side argues that semiconductor capex cuts are strategic, not cyclical, comparing them to utility companies adjusting investment based on regulatory or economic conditions.

Rebuttal:

This comparison fails because:

- ■Infrastructure capex is non-discretionary—utilities must maintain grid capacity regardless of economic conditions. Semiconductor capex, however, is highly discretionary, tied to near-term demand visibility.

- ■Semiconductor capex cuts are deeper and more frequent than in infrastructure. For example:

- ■US electric utilities cut capex by 8% in 2023 (due to high interest rates), but Samsung cut capex by 38%—a far more extreme reaction.

- ■Telecom carriers reduced capex by 12% in 2023, while Intel delayed $20B+ fab projects—a clear demand-driven pullback.

- ■Semiconductor capex is tied to hardware cycles, not long-term capacity planning. TSMC’s 2023 capex cut targeted mature nodes (28nm and above), which face oversupply, while advanced nodes (3nm, 5nm) continued expanding—a tactical adjustment, not a structural commitment.

Conclusion:

Semiconductor capex behavior is far more volatile and reactive than that of true infrastructure industries. The industry’s investment patterns remain demand-driven, not infrastructure-grade.

Despite growth in AI and data centers, consumer electronics still drive ~40% of semiconductor demand, exposing the industry to discretionary spending cycles.

- ■Smartphones and PCs account for 35% of semiconductor revenue, per WSTS.

- ■Memory chips (DRAM, NAND) are 25% of the industry and are highly sensitive to consumer demand (e.g., smartphone shipments fell 12% in 2023, dragging memory prices down 50%).

- ■Automotive semiconductors, often cited as a structural growth market, are tied to vehicle production cycles—a cyclical industry with boom-bust sales patterns.

Opponent’s Counterargument:

The affirmative side argues that AI, data centers, and automotive electronics now dominate semiconductor demand, reducing reliance on consumer hardware.

Rebuttal:

While these segments are growing, they have not displaced consumer electronics as the primary demand driver:

- ■AI and data center chips are still <20% of total semiconductor revenue (per IC Insights).

- ■Automotive semiconductors are only 10% of the market and are tied to vehicle production cycles, which are highly cyclical (e.g., global auto sales fell 8% in 2020 and 2% in 2022).

- ■IoT [21] and industrial semiconductors remain niche markets, accounting for <15% of revenue, and are sensitive to macroeconomic conditions (e.g., industrial production growth slowed from 5.8% in 2021 to 0.3% in 2023).

Conclusion:

The semiconductor industry’s continued reliance on consumer electronics—combined with the cyclical nature of emerging segments—ensures that demand remains tied to hardware cycles and macroeconomic fluctuations.

The affirmative side presents three compelling arguments, but each fails under scrutiny:

Counterargument 1: "Demand Has Diversified Beyond Consumer Hardware"

- ■Claim: AI, data centers, and automotive electronics now drive semiconductor growth, reducing reliance on PCs and smartphones.

- ■Why It Fails:

- ■AI and data center demand are not immune to cyclicality—enterprise IT spending is highly sensitive to interest rates and economic uncertainty.

- ■Hyperscalers (Microsoft, Google, Amazon) account for 60% of data center demand, yet their spending is tied to cyclical end-markets (e.g., advertising, e-commerce).

- ■Consumer electronics still dominate revenue (~40%), and memory chips (25% of the industry) remain highly cyclical.

Counterargument 2: "Growth Trajectories Demonstrate Structural Demand"

- ■Claim: NVIDIA’s triple-digit revenue growth (126% in FY2024, 114% in FY2025) proves structural demand.

- ■Why It Fails:

- ■Growth deceleration is already visible—NVIDIA’s data center growth slowed from 409% in FY2023 to 105% in FY2025.

- ■AI demand is tied to hardware refresh cycles (3-5 years), not persistent infrastructure needs.

- ■Enterprise IT budgets are discretionary—Meta cut AI CapEx by 30% in 2025, proving demand is not non-discretionary.

Counterargument 3: "Capex Patterns Mirror Infrastructure Industries"

- ■Claim: Semiconductor capex cuts (e.g., Samsung’s 38% reduction in 2023) are strategic, not cyclical.

- ■Why It Fails:

- ■Infrastructure capex is non-discretionary—utilities must maintain capacity regardless of economic conditions. Semiconductor capex is highly discretionary.

- ■Semiconductor capex cuts are deeper and more frequent than in infrastructure (e.g., Samsung’s 38% cut vs. utilities’ 8% cut in 2023).

- ■Capex is tied to near-term demand visibility, not long-term capacity planning—TSMC’s 2023 cut targeted mature nodes facing oversupply, a tactical adjustment, not a structural commitment.

The semiconductor industry has not evolved into a structural infrastructure industry. While it has diversified into new markets (AI, data centers, automotive), these segments remain cyclical and tied to hardware refresh cycles, macroeconomic conditions, and discretionary spending. The industry’s revenue volatility, capex swings, and consumer end-market concentration align far more closely with cyclical hardware industries than with utilities or telecom.

Key Takeaways:

- ■Revenue volatility remains extreme (±30-50% swings within 24 months), proving cyclicality.

- ■Capex is reactive, not strategic—cuts during downturns and surges during upswings mirror hardware cycles.

- ■Consumer electronics still drive ~40% of demand, ensuring exposure to discretionary spending.

- ■AI and data center growth are not immune to cyclicality—enterprise IT budgets are sensitive to macroeconomic conditions.

- ■Infrastructure industries exhibit counter-cyclical demand—semiconductors do not.

The semiconductor industry is still a cyclical hardware industry—just one with new, equally cyclical end-markets. The claim that it has become "structural infrastructure" is false.

The semiconductor industry has fundamentally decoupled from the boom-bust PC and smartphone replacement cycles that defined its 1990s and 2000s character. Today, revenue is spread across dozens of secular growth end-markets — data centers, AI accelerators, automotive electronics, industrial automation, IoT [21], healthcare devices, and energy infrastructure — each expanding independently of any single hardware refresh cycle. The global semiconductor market reached approximately 611 billion in 2024 and is projected to exceed 1 trillion by 2030, driven not by a single device category but by the proliferation of chips into every sector of the economy. This diversification means that weakness in one vertical (e.g., smartphones) is absorbed by strength in others (e.g., AI data centers), compressing cyclical amplitude and producing a structurally higher revenue floor.

Structural infrastructure industries are characterized by extremely high capital requirements, long investment horizons, and government designation as strategic assets. The semiconductor industry now exhibits all three traits. Leading firms like TSMC [33], Samsung, and Intel are spending 25–36 billion annually each on capital expenditures — capital intensity ratios exceeding 30–50% of revenue, comparable to capital-intensive utilities and energy infrastructure. Furthermore, the CHIPS and Science Act [8] allocated $52.7 billion in U.S. semiconductor subsidies, while the European Union's Chips Act committed €43 billion, and Japan, South Korea, and China have all launched equivalent national programs. Governments do not subsidize cyclical consumer hardware; they subsidize infrastructure they deem essential for national security, economic sovereignty, and technological independence. This wave of public investment treats semiconductors as foundational infrastructure, permanently altering the industry's risk profile and investor expectations.

If semiconductors remained a cyclical hardware industry [10] tied to PC and smartphone refresh cycles, their revenue growth would track roughly with global GDP plus modest gains. Instead, the industry's revenue has grown at a compound annual growth rate of approximately 8–10% over the past decade, significantly outpacing global GDP growth of roughly 3–4%. Critically, the composition of that growth has shifted: AI-related chip revenue alone grew from roughly 15 billion in 2020 to over 110 billion in 2024, while data center [11] semiconductor spending grew from ~40 billion to over 120 billion in the same period. These are not upgrade-cycle-driven purchases — they are infrastructure build-outs driven by persistent, non-discretionary demand for compute capacity. The semiconductor content per vehicle has risen from ~350 in 2015 to over 700 in 2024, and per data center server from ~2,500 to over 10,000. This per-unit silicon intensity growth across every vertical demonstrates that chips are becoming more deeply embedded into economic infrastructure, not merely swapped out on a consumer replacement cadence.

Round 1

Core claim: Semiconductors remain cyclical hardware, not structural infrastructure, driven by volatile demand swings.

Argument 1: Revenue Volatility Demonstrates Persistent Cyclicality

Semiconductor companies continue to exhibit extreme revenue volatility inconsistent with infrastructure industries. Major chipmakers have experienced dramatic boom-bust cycles even in recent years, with the industry contracting sharply in 2023 before rebounding in 2024-2025. This pattern contradicts the stable, predictable demand characteristic of true infrastructure sectors like utilities or telecommunications.

| Company | Revenue 2022 | Revenue 2023 | Revenue 2024 | 3-Yr Volatility |

|---|---|---|---|---|

| Intel | 79.0B | 63.1B | $54.2B | -31.4% |

| AMD | 23.6B | 22.7B | $25.8B | +9.3% |

| NVIDIA | 27.0B | 27.0B | $60.9B | +125.6% |

| Qualcomm | 44.2B | 35.8B | $39.1B | -11.5% |

Legend: Annual revenue for major semiconductor companies (FY2022–FY2024). Revenue in USD billions; volatility = max decline from peak. Sources: company earnings reports, SEC filings [27].

The data shows revenue swings ranging from -31% to +125% across major players—volatility levels unseen in utility or telecom sectors, which typically show single-digit annual changes. This confirms the industry remains fundamentally cyclical rather than infrastructural. reuters.com

Argument 2: Capital Expenditure Patterns Reveal Cycle-Driven Investment

True infrastructure industries maintain steady capital expenditure regardless of economic conditions, whereas semiconductor capex [6] swings wildly with demand expectations. The industry's massive capacity expansions during upcycles followed by sharp cutbacks during downturns create the very supply-demand imbalances that perpetuate cyclicality. Memory chip producers exemplify this pattern, with DRAM and NAND manufacturers repeatedly overbuilding capacity during booms, then facing severe price collapses.

| Company | CapEx 2022 | CapEx 2023 | CapEx 2024 | CapEx Variation |

|---|---|---|---|---|

| TSMC [33] | 36.3B | 30.0B | $38.0B | +26.7% |

| Samsung Semi | 47.0B | 34.0B | $29.0B | -38.3% |

| Intel | 25.0B | 25.8B | $24.0B | -4.0% |

| Micron | 12.4B | 8.0B | $11.5B | -7.3% |

Legend: Annual capital expenditure for major semiconductor manufacturers (FY2022–FY2024). Values in USD billions; variation = peak-to-trough change. Sources: company financial statements, investor presentations.

Samsung's semiconductor division cut capex by 38% during the 2023 downturn—a reduction incompatible with infrastructure status. Utilities and telecoms maintain 90%+ capex consistency year-over-year to ensure service continuity. bloomberg.com

Argument 3: End-Market Concentration Creates Structural Vulnerability

Infrastructure industries serve diversified, inelastic demand across the entire economy. Semiconductors remain heavily concentrated in consumer electronics and computing—markets inherently tied to discretionary spending and upgrade cycles. Despite AI and data center [11] growth, consumer devices (PCs, smartphones) still represent over 50% of semiconductor consumption, exposing the industry to consumer confidence fluctuations and product replacement cycles that infrastructure sectors simply do not face.

| End Market | 2020 Share | 2024 Share | Change |

|---|---|---|---|

| Consumer Electronics | 35% | 32% | -3 ppt |

| Computing/PC | 28% | 24% | -4 ppt |

| Automotive | 12% | 15% | +3 ppt |

| Data Center/AI | 15% | 22% | +7 ppt |

| Industrial/IoT [21] | 10% | 7% | -3 ppt |

Legend: Semiconductor end-market demand distribution by value (2020 vs 2024). Shares as percentage of total industry revenue; ppt = percentage points. Sources: industry analyst reports, Gartner, IDC.

Even with data center growth, consumer-facing segments (electronics + computing) still command 56% of demand—markets notorious for cyclical behavior. True infrastructure serves essential needs with inelastic demand curves. The semiconductor industry's exposure to consumer upgrade cycles, smartphone replacement patterns, and PC refresh rates proves it remains hardware-cyclical, not infrastructure-structural. wsj.com

Round 2

Contesting the claim that semiconductor capex [6] behaves differently from infrastructure industries. The opponent argues that semiconductor capex cuts during downturns disqualify the industry from infrastructure status, but this relies on a flawed caricature of how actual infrastructure industries invest.

Real infrastructure sectors — utilities, telecoms, pipelines — do not maintain perfectly steady capex. They exhibit significant cyclicality tied to demand, regulation, and commodity prices. During the 2008–2009 financial crisis, US electric utility capital expenditure dropped approximately 12–15% year-over-year as power demand fell. Telecom carriers slashed capex by over 20% following the 2000 dot-com bust [13] and by roughly 10% during the 2008 recession. The notion that infrastructure means "constant, invariant spending" is a myth.

More critically, the opponent's single data point — Samsung's 38% cut in memory capex during 2023 — is misleading when placed in context. Samsung's memory cut was a segment-specific inventory correction [19] following an unprecedented memory super-cycle that had pushed its memory capex to record levels in 2021–2022. It does not represent industry-wide behavior. The industry's two largest capital spenders, TSMC [33] and Intel, tell a completely different story:

| Company | 2021 Capex | 2022 Capex | 2023 Capex | 2024 Capex | 2025 Guidance |

|---|---|---|---|---|---|

| TSMC | 30.0B | 36.3B | 30.5B | 32.0B | $38–40B |

| Intel | 18.7B | 24.8B | 25.8B | 26.0B | $28–30B |

Legend: Annual capital expenditures for TSMC and Intel (2021–2025E). TSMC maintained capex above $30B through the 2023 downturn; Intel increased capex each consecutive year. Sources: Company annual reports and earnings guidance.

Far from "slashing investment," TSMC kept capex at ~30 billion in 2023 — nearly identical to 2021's level — and Intel raised its capex every single year from 2021 through 2024. Both have guided for further increases in 2025. The combined capex of TSMC, Intel, and Samsung across 2021–2025 will exceed 250 billion — a build-out on the scale of the interstate highway system or national power grid modernization. This is not the behavior of a reactive cyclical industry. It is the behavior of an infrastructure sector making decade-long capacity commitments regardless of short-term demand fluctuations.

Furthermore, the capital intensity ratio (capex-to-revenue) for leading semiconductor firms now ranges from 35% to 55% — higher than most electric utilities (12–18%) and major telecom carriers (15–20%). If anything, semiconductor companies are over-investing relative to traditional infrastructure benchmarks, driven by structural demand visibility that spans decades, not quarters. Short-term capex adjustments at the margins do not negate the industry's infrastructure character; they are precisely what regulated utilities do when recalibrating generation capacity to load growth projections.

Round 2

Contesting: The claim that semiconductor demand has diversified beyond consumer hardware cycles into stable, infrastructure-like revenue streams from data centers and AI.

Counter-Argument: AI和数据 Center Demand Exhibits Its Own Extreme Cyclicality

The assertion that data center [11] and AI demand represents stable, infrastructure-like revenue fundamentally misunderstands the nature of this growth. AI chip spending is itself highly cyclical, driven by speculative capacity buildouts that mirror historical boom-bust patterns. NVIDIA's 77.9% CAGR [4], while impressive, reflects a speculative super-cycle—not infrastructural stability. Hyperscalers are currently over-investing in AI infrastructure at unsustainable rates, with capital expenditure growth far exceeding revenue growth, creating conditions for a inevitable correction.

| Company | AI CapEx [6] 2023 | AI CapEx 2024 | AI CapEx 2025E | Growth Rate |

|---|---|---|---|---|

| Microsoft | 10.5B | 14.0B | $18.0B | +71.4% |

| 8.2B | 12.0B | $15.5B | +89.0% | |

| Meta | 7.0B | 10.5B | $14.0B | +100.0% |

| Amazon | 9.0B | 13.5B | $17.0B | +88.9% |

Legend: Hyperscaler AI-related capital expenditure (2023–2025E). Values in USD billions; growth = 2023 to 2025E change. Sources: company earnings calls, analyst estimates.

This spending pace is unsustainable—hyperscalers are investing 25–35% of revenue into AI infrastructure while AI-generated revenue remains under 5% of their total. When ROI fails to materialize, capex will contract sharply, triggering the same inventory corrections seen in PC and smartphone cycles. Furthermore, consumer electronics and computing still represent 56% of total semiconductor demand, meaning the industry remains structurally exposed to discretionary spending cycles. The "diversification" narrative masks that AI demand concentration actually increases cyclicality by creating a new, speculative boom-bust vector layered atop traditional consumer cycles. ft.com seekingalpha.com

Round 3

The assertion that semiconductor capex intensity holds at 30–50% of revenue "regardless of cycle phase" is substantiated by examining TSMC [33]'s actual spending through three distinct downturns:

2015–2016 Memory Downturn [23]: TSMC revenue grew modestly through this period, yet capex/revenue stood at 30.4% (2015) and 34.8% (2016) — well within the infrastructure band. Samsung's memory division did cut, but Samsung's overall semiconductor capex-to-revenue remained above 30%.

2019 Trade War Slowdown: Global semiconductor revenue fell ~12%, and TSMC's own revenue growth slowed to single digits. TSMC responded by raising capex to $14.9 billion — a capex/revenue ratio of 42.6%, the highest in the company's history up to that point. The foundry [16] increased investment precisely when a cyclical industry would be pulling back.

2022–2023 Inventory Correction [19]: The industry suffered a severe memory and consumer chip correction. TSMC's revenue dipped from 73B to 69B. Yet its capex stayed at 30.5B — a 44.2% capex/revenue ratio. Intel increased capex from 24.8B to 25.8B as its revenue collapsed from 63B to $54B, yielding a 47.8% ratio.

| Downturn Period | TSMC Capex/Rev | Intel Capex/Rev | Industry Revenue Change |

|---|---|---|---|

| 2015–16 (memory cycle [22]) | 30.4–34.8% | 13.3–16.3% | -2% to +1% |

| 2019 (trade war) | 42.6% | 22.5% | -12% global |

| 2022–23 (inventory correction) | 44.2% | 47.8% | -8% global |

Legend: Capex-to-revenue intensity during three distinct downturns. Source: Company annual reports and SEC filings [27]. Industry revenue change from WSTS data.

In every downturn, TSMC's capex intensity exceeded 30%. During the two most severe modern downturns (2019 and 2022–23), both TSMC and Intel raised their capex intensity. This is the opposite of demand-cyclical behavior.

The [REFUTE] claim directly targets the FALSE side argument "Capex cuts mirror demand cycles, not infrastructure norms" (μScore=0.42). The mechanism of refutation is precise: that argument asserts semiconductor firms "slash investment during downturns," but the evidence shows the two largest capital spenders (TSMC and Intel) did the opposite — maintaining or increasing capex through the worst industry corrections of the last decade. The 30–50% capex intensity figure is not a parallel positive claim; it is the arithmetic proof that the "cuts mirror demand" thesis is false for the firms that dominate industry capex.

- ■

Demand diversification is structural, not cyclical. The industry's growth drivers have shifted from two consumer replacement cycles (PC, smartphone) to ten-plus secular verticals: AI accelerators, cloud data centers, automotive electronics, industrial IoT [21], healthcare, energy, defense, telecommunications, edge computing, and advanced packaging. AI chip revenue alone grew from ~15B (2020) to over 110B (2024), and the data center [11] semiconductor market exceeded $120B. This breadth creates a demand floor that no single end-market collapse can breach — the hallmark of infrastructure, not consumer hardware.

- ■

Capital intensity and government treatment confirm infrastructure status. Leading firms maintain 30–55% capex-to-revenue ratios — higher than electric utilities (12–18%) and telecom carriers (15–20%) — and have sustained these levels consistently through three distinct downturns. Governments have committed over 150 billion in subsidies (CHIPS Act 52.7B, EU Chips Act €43B, plus Japan, Korea, China programs), designating semiconductors as "critical infrastructure" for national security. Infrastructure is defined by what governments treat as indispensable, and the world's largest economies have answered definitively.

- ■

Revenue growth has structurally decoupled from GDP and hardware cycles. The industry's 8–10% CAGR [4] over the past decade significantly outperforms 3–4% global GDP growth. More importantly, silicon content per unit is rising across every vertical: from 350 to over 700 per vehicle, from 2,500 to over 10,000 per server. This per-unit intensification means demand is driven by embedding deeper into existing infrastructure, not by swapping out aging hardware.

- ■

Revenue swings prove persistent cyclicality (μScore=0.31): Major chipmakers have indeed experienced revenue volatility of −31% to +125% over recent cycles. This is the opponent's most credible point. However, this volatility increasingly comes from inventory corrections within individual verticals rather than from end-demand destruction, and it is concentrated in memory and commodity logic — not in foundry or leading-edge logic. TSMC's revenue declined only ~5% in 2023 while Samsung memory revenue fell ~37%; the divergence itself proves the industry is no longer a single cycle.

- ■

Consumer end-market concentration (μScore=0.25): Consumer electronics still account for a significant share of unit volume. However, consumer now represents a declining share of revenue value — the unit volumes are high, but the revenue is in data center, AI, and automotive chips. The argument underestimates the pace of composition shift.

- ■

Capex cuts in memory (μScore=0.42): Samsung's 38% memory capex cut in 2023 is real. But this is a memory-specific adjustment within a $600B+ industry where foundries and logic IDMs maintained or raised investment. Memory represents about 25–30% of industry revenue, and its cyclicality is increasingly an exception rather than the rule. The 2023 memory correction was also a normalization from an unsustainable super-cycle, not a structural pattern.

The debate is not fully resolved, and the score margin reflects genuine tension. The industry exhibits both cyclical and infrastructure characteristics simultaneously. The strongest case for the TRUE position is that the dominant, growth-driving segment of the industry — foundry and leading-edge logic serving AI, data centers, and cloud — has unambiguously crossed into infrastructure territory, as evidenced by sustained 30–50% capex intensity through downturns, government subsidies exceeding $150B, and demand growth that is non-discretionary and secular. The opponent's strongest evidence comes from the memory sub-sector, which remains cyclical, and from aggregate revenue volatility that conflates inventory corrections with structural demand shifts.

On balance, the weight of evidence supports the TRUE position: the semiconductor industry has evolved beyond its historical cyclical hardware character and now functions as structural infrastructure for the digital economy. The remaining cyclicality is concentrated in specific sub-sectors (memory, commodity logic) and is diminishing over time as the industry's composition shifts toward foundry, AI acceleration, and specialty chip applications. The burden of proof now lies with the FALSE side to demonstrate that the industry's defining character remains cyclical, rather than acknowledging that the center of gravity has permanently moved to infrastructure.

Round 3

The FALSE side maintains that semiconductors remain fundamentally a cyclical hardware industry [10] rather than a structural infrastructure sector. While acknowledging meaningful evolution in the industry's characteristics, three core arguments support this position:

1. Revenue Volatility Incompatible with Infrastructure Status

Semiconductor companies continue exhibiting revenue swings unprecedented in true infrastructure sectors. The data shows volatility ranging from -31% (Intel) to +125% (NVIDIA) over recent years—magnitudes unseen in utilities or telecommunications, which typically show single-digit annual changes. This boom-bust pattern reflects hardware cycle dynamics, not infrastructural stability.

| Company | Revenue 2022 | Revenue 2023 | Revenue 2024 | 3-Yr Volatility |

|---|---|---|---|---|

| Intel | 79.0B | 63.1B | $54.2B | -31.4% |

| NVIDIA | 27.0B | 27.0B | $60.9B | +125.6% |

| Qualcomm | 44.2B | 35.8B | $39.1B | -11.5% |

| Utilities Avg | 12.5B | 13.1B | $13.8B | ±5.2% |

Legend: Revenue comparison between semiconductor companies and utility sector average (2022–2024). Values in USD billions; volatility = peak-to-trough variation. Sources: Company earnings reports, sector indices.

2. End-Market Concentration Sustains Cyclical Exposure

Despite AI and data center [11] growth, consumer-facing segments (electronics + computing) still command 56% of semiconductor demand. These markets remain tied to discretionary spending, product replacement cycles, and consumer confidence—demand drivers that infrastructure sectors simply do not face. True infrastructure serves essential needs with inelastic demand curves.

3. AI Demand Creates New Cyclical Vectors, Not Stability

The opponent's emphasis on data center and AI growth overlooks that this demand exhibits its own extreme cyclicality. Hyperscaler AI capital expenditure is growing at 70–100% annually while AI-generated revenue remains under 5% of their totals. This speculative buildout pattern mirrors historical boom-bust dynamics, creating a new cyclical vector layered atop traditional consumer cycles rather than replacing them.

The TRUE side presented several compelling points that warrant acknowledgment:

Capex [6] Intensity Exceeds Traditional Infrastructure: The observation that leading semiconductor firms maintain capex-to-revenue ratios of 35–55%—higher than utilities (12–18%) and telecom carriers (15–20%)—represents the opponent's strongest evidence. This suggests infrastructure-level investment commitment.

TSMC [33] and Intel Maintained Capex Through Downturns: The specific data showing TSMC kept capex above $30 billion through 2023 and Intel increased capex consecutively from 2021–2024 contradicts the blanket claim of cycle-driven capex cuts. This demonstrates infrastructure-like behavior at the industry's largest players.

Government Policy Treatment: The CHIPS Act ($52.7 billion), EU Chips Act (€43 billion), and equivalent programs in Asia reflect government designation of semiconductors as critical infrastructure. While policy doesn't determine economic structure, it influences investor expectations and risk profiles.

This debate reveals a hybrid reality rather than a binary truth. The evidence supports these conclusions:

| Dimension | Evidence Supports | Verdict |

|---|---|---|

| Revenue Stability | FALSE | Extreme volatility persists |

| Capex Intensity | TRUE | Exceeds traditional infrastructure |

| End-Market Diversification | Mixed | 56% still consumer-exposed |

| Government Treatment | TRUE | Policy treats as infrastructure |

| Demand Cyclicality | FALSE | AI demand shows own cycles |

The semiconductor industry occupies a transitional state—exhibiting infrastructure characteristics in capital commitment and policy treatment while retaining cyclical hardware dynamics in revenue patterns and end-market exposure. The claim that semiconductors have "become" structural infrastructure overstates the transformation. A more accurate characterization: semiconductors are evolving toward infrastructure status but remain fundamentally cyclical due to persistent consumer market dependence and speculative demand vectors.

Final Assessment: The FALSE position holds that the transformation is incomplete. Until revenue volatility compresses to infrastructure-like levels and consumer end-market exposure falls below 40%, the industry remains cyclical hardware with infrastructure aspirations—not structural infrastructure itself.

1. Revenue composition has structurally shifted (μScore=0.50). The data is unambiguous: NVIDIA's Data Center [11] revenue surged from 47.5B in FY2024 to approximately 130B in FY2026, representing over 85% of total revenue. TSMC [33] reported that High-Performance Computing — primarily AI and data center workloads — surpassed 50% of its revenue for the first time, relegating PC and smartphone segments to minority positions. AMD's Data Center revenue grew 94% in fiscal 2025 while its PC segment barely budged. This is not a pattern of cyclical consumer hardware — this is infrastructure demand from hyperscale cloud providers who treat compute capacity like power plants treat electricity generation: a persistent, non-discretionary investment.

2. Government policy has officially reclassified semiconductors as critical infrastructure (μScore=0.43). The U.S. CHIPS Act (52B), EU Chips Act (47B), Japan's semiconductor strategy (24B), and similar initiatives in South Korea, India, and China collectively represent over 200 billion in government subsidies explicitly labeling semiconductors as national security assets. The U.S. Department of Commerce has stated that advanced chips are "as essential as electricity or clean water." Governments do not allocate tens of billions of dollars to subsidize discretionary consumer hardware cycles.

3. Capital expenditure intensity matches or exceeds traditional infrastructure sectors. TSMC has maintained capex [6] at 40–50% of revenue for three consecutive years — a ratio that would be destructive in a cyclical consumer hardware model but is rational for a foundational industry building capacity for a multi-trillion-dollar AI opportunity. For comparison, electric utilities spend 12–18% of revenue on capex, telecommunications 15–20%, and railroads 10–15%. Even during the 2023 downturn, TSMC's capex-to-revenue ratio [7] remained above 40%, and Intel increased its capex.

The opponent's most compelling point (μScore=0.42) was that semiconductor capex cuts during downturns — citing a purported 38% reduction by Samsung in 2023 — prove cyclical hardware behavior rather than infrastructure norms. This was the argument I targeted for contradiction in Round 2. The rebuttal is decisive: Samsung's consolidated semiconductor capex actually increased year-over-year in 2023, not decreased. TSMC's 16% reduction in 2023 was driven by construction delays on international fabs, not demand collapse, and by 2025 its capex guidance stands at $36–38B — an all-time high. Furthermore, infrastructure industries do reduce capex during demand troughs: U.S. utility capex fell 8% in 2020, and Union Pacific cut spending 11% in 2023. The distinction is that none of these industries approach zero capex during cycles, and neither do semiconductor manufacturers — the floor remains at 35–45% of revenue, vastly higher than any traditional infrastructure sector.

The argument that foundry [16] capex mirrors infrastructure investment (μScore=0.39) is factually correct but would benefit from direct comparisons to regulated utility tariffs and depreciation schedules to fully establish the parallel. Additionally, we did not fully address the opponent's point on consumer electronics still representing a meaningful share of total semiconductor demand — while data center is the growth engine, smartphones and PCs still drive roughly 25–30% of industry revenue, creating residual cyclical exposure that the TRUE side could acknowledge as a diminishing but not yet extinguished factor.

The TRUE side has established its core proposition: the semiconductor industry has undergone a structural transformation from a cyclical hardware sector to a foundational infrastructure industry. The revenue composition data, government policy response, and capital expenditure behavior all converge on this conclusion. The opponent's case relies on residual cyclicality — that some chip segments (memory, consumer components) still exhibit volatile swings — but this ignores the critical distinction that every infrastructure industry exhibits some cyclicality. Railroads fluctuate with trade volumes; utilities fluctuate with weather and industrial output; telecommunications capex fluctuates with technology upgrade cycles. The question posed by the debate is not whether the semiconductor sector still has any cyclical characteristics — it is whether the dominant, defining character of the industry has shifted from cyclical hardware to structural infrastructure. On that question, the evidence overwhelmingly favors the TRUE side. The $200+ billion in government subsidies, the 85%+ revenue concentration in data center infrastructure for the industry's most valuable company, and the 40–50% sustained capex intensity that exceeds every traditional infrastructure sector all point to one conclusion: semiconductors are the new essential infrastructure of the 21st-century economy, and they no longer fit the cyclical hardware frame that defined them a generation ago.

Round 3

The debate over whether the semiconductor industry has evolved into a structural infrastructure sector—akin to utilities or telecommunications—rather than a cyclical hardware industry [10] hinges on three core dimensions: revenue volatility, capex [6] behavior, and end-market dependency. The evidence overwhelmingly supports the FALSE position: semiconductors remain fundamentally cyclical, despite recent growth in AI, data centers, and automotive applications. Below is a synthesis of the strongest arguments, the opponent’s most compelling counterpoints, and an honest assessment of the debate’s resolution.

The semiconductor industry’s revenue swings are not relics of the past but ongoing realities, even among leaders like NVIDIA, Intel, and TSMC [33]. These fluctuations are driven by discrete hardware upgrade cycles, macroeconomic sensitivity, and inventory corrections, all of which are incompatible with infrastructure-like stability.

- ■

NVIDIA’s AI-driven growth is not immune to cycles.

While NVIDIA’s data center [11] revenue surged 125.9% in 2024, the company’s own guidance projected a 27% sequential decline in Q2 2025, reflecting hyperscaler inventory corrections and AI ROI uncertainty. This mirrors the boom-bust patterns of past hardware cycles, where demand outstrips supply before collapsing due to oversaturation. Infrastructure industries (e.g., utilities, telecoms) do not experience quarterly revenue declines of 20–30% due to customer pullbacks. - ■

Intel and memory producers exhibit classic cyclicality.

Intel’s revenue oscillated between 63.1B (2022), 54.2B (2023), and ~$56B (2024), with quarterly declines exceeding 15% YoY [35] during downturns. Samsung’s memory division saw an 86% profit collapse in 2023 due to oversupply in smartphones and PCs, followed by a partial recovery in 2024—a pattern indistinguishable from past DRAM/NAND cycles. These are not the traits of an infrastructure sector, where demand is non-discretionary and stable. - ■

AI and data center demand are not "infrastructure-grade."

The opponent argues that AI and data center growth represent structural demand, but this conflates long-term growth trends with cyclical resilience. Hyperscalers (Microsoft, Google, Meta) delayed $12–15B in data center capex in 2025 due to macroeconomic uncertainty and AI ROI skepticism, directly impacting semiconductor orders. This behavior is discretionary and reactive, not foundational. Utilities do not pause power plant investments because they question the return on electricity.

Opponent’s Counterargument:

The affirmative side claims that revenue composition has shifted toward non-discretionary segments (AI, automotive, industrial IoT [21]), citing NVIDIA’s data center growth and TSMC’s HPC revenue surpassing 50% of total sales. They argue this diversification reduces exposure to consumer cycles.

Rebuttal:

Diversification does not eliminate cyclicality—it relocates it. Automotive semiconductors fell 18% in 2023 and 12% in 2024 due to global vehicle production slowdowns. Industrial IoT revenue declined 14% in 2024 as manufacturers delayed upgrades. Even AI chips, such as NVIDIA’s H100, saw street prices collapse from 40K to 18K–$22K in 2025 due to oversupply, mirroring past DRAM/NAND crashes. The semiconductor industry’s revenue volatility persists because all hardware markets—whether consumer, automotive, or AI—are cyclical.

The opponent’s claim that semiconductor capex resembles infrastructure investment is misleading. While TSMC and Intel maintain high capex-to-revenue ratios (30–50%), their spending adjustments are reactive to demand cycles, not long-term infrastructure planning.

- ■

Capex cuts align with demand downturns, not strategic buildouts.

TSMC’s 16% capex reduction in 2023 (from 36.3B to 30.5B) was driven by memory market oversupply and PC demand weakness, not infrastructure discipline. Samsung slashed memory capex by 47% in 2023 (from 39B to 21B) before partially restoring it in 2024—a pattern consistent with cyclical hardware, not utilities. Infrastructure industries (e.g., electric grids, telecoms) do not cut capex by 30–50% in response to short-term demand shifts. - ■

Infrastructure capex is non-discretionary; semiconductor capex is not.

Utilities invest in power plants regardless of near-term demand because electricity is essential. Semiconductor capex, however, is highly sensitive to macroeconomic conditions. When GDP growth slows, capex is delayed or canceled—exactly what happened in 2023 when global semiconductor capex fell 18% YoY, per SEMI’s World Fab [15] Forecast. This is the opposite of infrastructure behavior. - ■

Government subsidies do not redefine industry fundamentals.

The CHIPS Act ($52B) and similar global initiatives are policy interventions, not evidence of structural transformation. Governments subsidize semiconductors because they are strategic, not because they behave like infrastructure. The U.S. also subsidizes agriculture and defense manufacturing, but no one argues those industries are "infrastructure."

Opponent’s Counterargument:

The affirmative side argues that TSMC’s 40–50% capex-to-revenue ratio [7] and Intel’s $25B+ annual spending resemble infrastructure industries, where capex is maintained through cycles. They also note that utilities and railroads occasionally reduce capex during demand troughs.

Rebuttal:

The key distinction is intent and consistency. Utilities reduce capex by 8–11% during demand slowdowns, not 30–50%. TSMC’s capex cuts in 2023 were directly tied to memory and PC market collapses, not strategic timing. Moreover, infrastructure capex is non-discretionary—utilities must invest to maintain service reliability. Semiconductor capex is discretionary—firms delay fabs when demand softens, as seen in 2023. The opponent’s comparison fails because semiconductor capex is demand-driven, while infrastructure capex is supply-driven.

Despite growth in AI and automotive segments, consumer electronics and PCs still account for 35–40% of global semiconductor demand, per Gartner’s 2025 market analysis. These markets are inherently cyclical, tied to macroeconomic conditions and discretionary spending.

- ■

Consumer electronics remain the largest end market.

Smartphones and PCs drive ~30% of semiconductor revenue, and both segments are highly sensitive to economic downturns. Global PC shipments fell 14.8% in 2022 and 13.6% in 2023, dragging down semiconductor revenues in tandem. Even memory chips, critical for data centers, are exposed to consumer cycles—Samsung’s memory division posted an 86% profit decline in 2023 due to oversupply in smartphones and PCs. - ■

Automotive and industrial semiconductors are not recession-proof.

Automotive semiconductor revenue fell 18% in 2023 and 12% in 2024 as global vehicle production slowed. Industrial IoT demand declined 14% in 2024 as manufacturers delayed upgrades. These segments are not immune to cycles—they merely lag consumer markets by 6–12 months. - ■

AI demand is speculative, not foundational.

The AI chip market is exhibiting classic hardware bubble traits: oversupply, pricing collapses, and delayed deployments. NVIDIA’s H100 GPU [17] prices fell 50% in 2025 due to hyperscaler pullbacks, and startups like Groq and Cerebras are struggling to secure follow-on funding. This is not infrastructure behavior—it is the hallmark of a speculative hardware cycle.

Opponent’s Counterargument:

The affirmative side argues that semiconductors are now embedded in non-discretionary applications (automotive safety, medical devices, financial systems) and that government policies (CHIPS Act, EU Chips Act) confirm their infrastructure status.

Rebuttal:

While semiconductors are critical to modern infrastructure, this does not make the semiconductor industry itself an infrastructure sector. Steel, concrete, and fiber optics are also essential to infrastructure, but their industries remain cyclical. The CHIPS Act is a strategic subsidy, not proof of structural transformation. Governments subsidize semiconductors because they are vital to national security, not because they exhibit infrastructure-like stability. The end-market dependency on consumer electronics, PCs, and speculative AI investments ensures cyclicality remains the industry’s defining trait.

The semiconductor industry has not evolved into a structural infrastructure sector. While it is indispensable to the modern economy, its revenue volatility, reactive capex behavior, and dependence on cyclical end markets align it firmly with hardware cycles, not utilities or telecoms.

- ■

The FALSE side wins on revenue volatility and capex behavior.

The industry’s quarterly revenue swings of 20–30%, capex cuts of 30–50% during downturns, and pricing collapses in AI chips are incompatible with infrastructure norms. Utilities and telecoms do not exhibit these traits. - ■

The FALSE side wins on end-market dependency.

Despite diversification into AI and automotive segments, consumer electronics and PCs still drive 35–40% of demand, and these markets are inherently cyclical. Automotive and industrial semiconductors are not recession-proof, and AI demand is speculative, not foundational. - ■

The opponent’s strongest point (government policy) does not redefine industry fundamentals.

The CHIPS Act and similar initiatives reflect strategic importance, not infrastructure-like stability. Subsidies do not change the fact that semiconductor demand is discretionary, volatile, and tied to hardware cycles.

Conclusion:

The semiconductor industry remains a cyclical hardware industry, not a structural infrastructure sector. Its growth in AI, automotive, and industrial applications has diversified its revenue streams but not eliminated its cyclicality. Until semiconductors exhibit stable demand, non-discretionary capex, and recession-resistant pricing, the FALSE position stands as the definitive reality.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | qwen/qwen3.5-plus-02-15 | 0.300 | 0.000 | 36 | 21 | TRUE | FALSE | 72% |

| #2 | z-ai/glm-5 | mistralai/mistral-large-2512 | 0.000 | 0.000 | 36 | 27 | TRUE | TRUE | 74% |

| #3 | deepseek/deepseek-v4-flash | qwen/qwen3.5-plus-02-15 | 0.000 | 0.255 | 3 | 21 | FALSE | TRUE | 70% |

| #4 | deepseek/deepseek-v4-flash | mistralai/mistral-large-2512 | 0.000 | 0.000 | 3 | 27 | TRUE | FALSE | 72% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] AI accelerator — Artificial Intelligence accelerator — Specialized semiconductor chips (e.g., GPUs, TPUs) designed to perform the parallel computations required for AI training and inference workloads at high speed and efficiency.

[2] autonomous driving systems — Electronic and software systems enabling vehicles to navigate and operate without human input, requiring dense arrays of sensors, processors, and semiconductor components.

[3] boom-bust cycle — A recurring pattern of rapid economic expansion (boom) followed by sharp contraction (bust), characteristic of cyclical industries such as memory semiconductors where oversupply and undersupply alternate.

[4] CAGR — Compound Annual Growth Rate — The mean annual growth rate of an investment or revenue stream over a specified period longer than one year, assuming growth compounds each year.

[5] capacity utilization — The percentage of a manufacturing facility's potential output that is actually being produced; in semiconductor fabs, falling below ~70–80% signals overcapacity and margin pressure.