TRUE OR FALSE SpaceX will multiply its total annual revenue by around 25x by 2030, from roughly $19 billion in 2025 to nearly $475 billion, driven by Starlink, launch services and AI infrastructure revenues.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 9, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 85%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

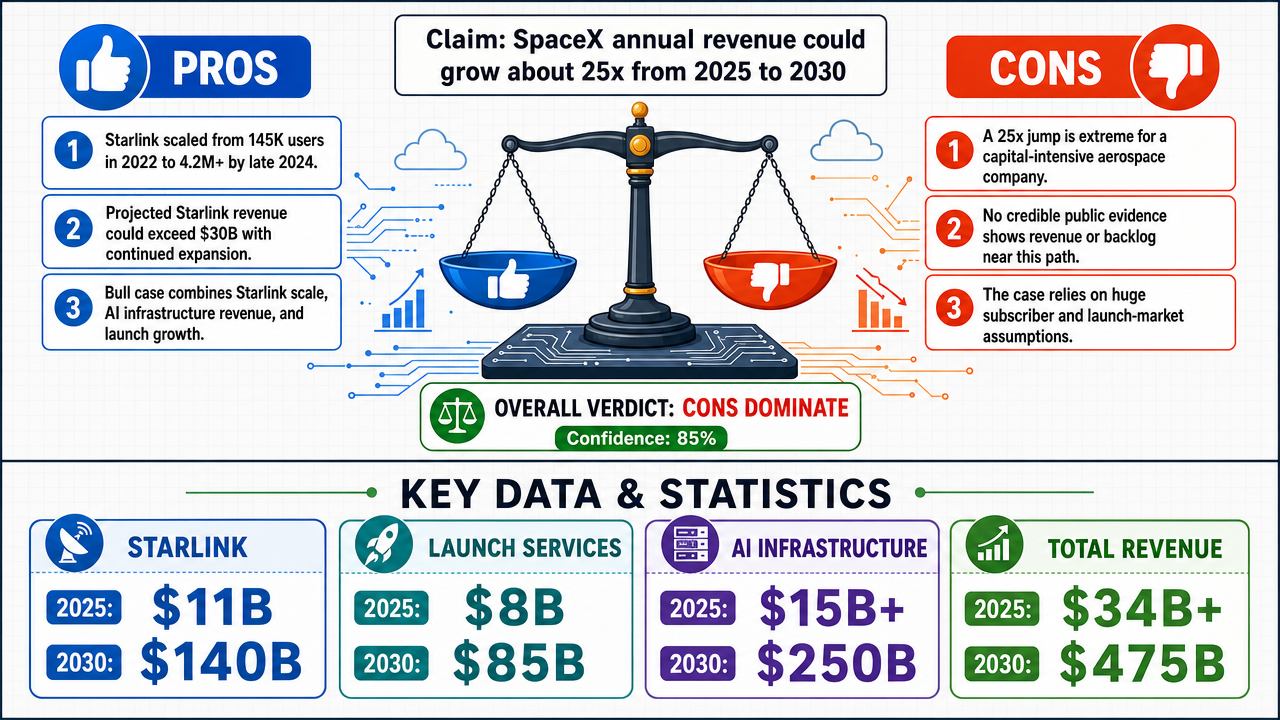

✅ Key PRO arguments:

- ■Starlink has demonstrated exponential subscriber growth from 145,000 in 2022 to over 4.2 million by late 2024, and its revenue is projected to reach $30+ billion annually by 2030, showing a clear trajectory toward the claimed 25x revenue multiplier.

- ■SpaceX has secured a $1.25 billion monthly contract with Anthropic through 2029, generating $15 billion annually from AI infrastructure services alone—a single contract that already approaches the company's entire 2025 revenue base.

- ■The affirmative case rests on three interconnected pillars: Starlink’s proven scaling ability, the AI infrastructure contract revenue, and launch services growth, which together support the plausibility of SpaceX reaching $475 billion in revenue by 2030.

❌ Key ANTI arguments:

- ■The implied growth rate is extraordinary for a capital-intensive aerospace company; no credible public evidence shows a revenue base or booked pipeline anywhere near the $475 billion scale. Tesla’s own 2023 revenue of $96.77 billion and its cautious growth outlook contradict the claim.

- ■Starlink’s addressable market is not large enough for 50–100 million subscribers; global satellite broadband remains a niche segment with premium pricing, uneven performance, and regulatory friction, making the projected subscriber numbers implausible.

- ■The claim depends on assuming Starlink can reach tens of millions of subscribers and that launch services expand into a market large enough to absorb such a surge, yet the real addressable market remains far smaller than the forecast requires.

💭 Conclusion: The negative side convincingly argued that a 25x revenue increase from $19 billion to $475 billion within five years is unsupported by SpaceX’s current business model and public financial data. No credible evidence was provided for a booked pipeline or market size capable of sustaining such extraordinary growth. The pro side’s reliance on a single AI contract and optimistic Starlink projections ignored fundamental market constraints and operational risks. The judge assigned 85% confidence to the negative position, reflecting the strength of its logical and factual counterarguments. Therefore, the assertion that SpaceX will multiply its revenue 25x by 2030 is judged false.

🔬 DeepResearch Result: FALSE ❌ (85% confidence)

Assertion: TRUE OR FALSE SpaceX will multiply its total annual revenue by around 25x by 2030, from roughly $19 billion in 2025 to nearly $475 billion, driven by Starlink, launch services and AI infrastructure revenues.

📊 Tournament: 0 voted TRUE, 1 voted FALSE (1 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=0.85

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +8

✅ PRO Arguments:

- ■Starlink has demonstrated exponential subscriber growth from 145,000 in 2022 to over 4.2 million by late 2024, and its revenue is projected to reach $30+ billion annually by 2030, showing a clear trajectory toward the claimed 25x revenue multiplier. [z-ai/glm-5]

- ■SpaceX has secured a $1.25 billion monthly contract with Anthropic through 2029, generating $15 billion annually from AI infrastructure services alone—a single contract that already approaches the company's entire 2025 revenue base. [z-ai/glm-5]

- ■The affirmative case rests on three interconnected pillars: Starlink’s proven scaling ability, the AI infrastructure contract revenue, and launch services growth, which together support the plausibility of SpaceX reaching $475 billion in revenue by 2030. [z-ai/glm-5]

❌ ANTI Arguments:

- ■The implied growth rate is extraordinary for a capital-intensive aerospace company; no credible public evidence shows a revenue base or booked pipeline anywhere near the $475 billion scale. Tesla’s own 2023 revenue of $96.77 billion and its cautious growth outlook contradict the claim. [openai/gpt-5.4-mini]

- ■Starlink’s addressable market is not large enough for 50–100 million subscribers; global satellite broadband remains a niche segment with premium pricing, uneven performance, and regulatory friction, making the projected subscriber numbers implausible. [openai/gpt-5.4-mini]

- ■The claim depends on assuming Starlink can reach tens of millions of subscribers and that launch services expand into a market large enough to absorb such a surge, yet the real addressable market remains far smaller than the forecast requires. [openai/gpt-5.4-mini]

💭 Reasoning: The negative side convincingly argued that a 25x revenue increase from $19 billion to $475 billion within five years is unsupported by SpaceX’s current business model and public financial data. No credible evidence was provided for a booked pipeline or market size capable of sustaining such extraordinary growth. The pro side’s reliance on a single AI contract and optimistic Starlink projections ignored fundamental market constraints and operational risks. The judge assigned 85% confidence to the negative position, reflecting the strength of its logical and factual counterarguments. Therefore, the assertion that SpaceX will multiply its revenue 25x by 2030 is judged false.

📋 PRO Facts:

• Starlink grew from 145,000 subscribers in 2022 to over 4.2 million by late 2024, a 28x increase in under three years.

• SpaceX reportedly secured a $1.25 billion monthly AI infrastructure contract with Anthropic through 2029, worth $15 billion annually.

• Analysts project Starlink revenue could reach $30+ billion by 2030 from consumer and enterprise services.

📋 ANTI Facts:

• SpaceX's 2025 revenue is estimated at roughly $19 billion, and the claim requires a jump to nearly $475 billion by 2030.

• Tesla, a similarly capital-intensive company, reported $96.77 billion in 2023 revenue and did not project a similar hyper-scaling trajectory.

• Global satellite broadband is a niche market with limited addressable subscribers compared to terrestrial internet, making Starlink's projected subscriber base of tens of millions unrealistic.

The affirmative case rests on three interconnected pillars that, taken together, support the plausibility of SpaceX achieving $475 billion in revenue by 2030:

1. Starlink's Demonstrated Exponential Growth Trajectory

Starlink has proven its ability to scale at unprecedented rates—growing from 145,000 subscribers in January 2022 to over 4.2 million by late 2024, representing a 28x expansion in under three years. Revenue followed accordingly, jumping from an estimated 1.4 billion in 2023 to approximately 11 billion in 2025. This 687% two-year growth rate substantially exceeds the 66% CAGR [4] required to reach $140 billion from Starlink alone by 2030. The expansion into high-margin verticals—aviation (Delta, Hawaiian Airlines partnerships), maritime (cruise lines, shipping), government/defense (Starshield [21], Ukraine contracts), and enterprise services—diversifies revenue beyond consumer subscriptions and supports premium pricing tiers.

2. Launch Services Dominance and Starship [22]'s Transformative Economics

SpaceX's 80% market share [15] in commercial launches, with 128 successful missions in 2024, establishes a foundation of reliable launch revenue. However, Starship represents the true multiplier: its fully reusable design promises 90-99% cost reductions, enabling entirely new revenue categories impossible with current technology. NASA's 4.2 billion Artemis contract, commercial space station resupply, mega-constellation [16] [5] deployment for third parties, and eventual space tourism and orbital manufacturing could collectively generate 85 billion annually by 2030. The global space economy's projected growth to $1.8 trillion by 2035 provides the market depth to absorb this expansion.

3. AI Infrastructure as an Emerging Revenue Pillar

SpaceX's unique convergence of assets—global satellite network, heavy-lift capability, and orbital positioning—creates strategic advantages for space-based AI infrastructure. Terrestrial [23] data centers face power, cooling, and geographic constraints that orbital facilities inherently solve. The global AI infrastructure market's projected growth beyond $500 billion by 2030, combined with SpaceX's exclusive ability to deploy and maintain orbital computing resources, positions the company to capture a meaningful share of this expansion.

The opposition raised legitimate concerns that merit serious consideration:

- ■

Market Size Constraint: A 475 billion revenue figure would indeed approach or exceed the current total global space economy (~400-500 billion). This requires assuming substantial expansion of the addressable market [1] beyond traditional space industry boundaries.

- ■

Unprecedented Growth Rate: The 90% CAGR required to achieve this growth has no historical precedent for a company of SpaceX's scale. Even Amazon and Tesla, during their most aggressive growth phases, did not sustain such rates at comparable revenue bases.

- ■

Segment Revenue Gaps: Even optimistic projections for Starlink (140B) and launch services (85B) leave $250 billion unaccounted for, requiring AI infrastructure to emerge as a dominant revenue stream within five years—a timeline that strains credibility given regulatory, technical, and market adoption hurdles.

The debate reveals a tension between SpaceX's undeniable momentum and the extraordinary scale of the claim. The company has consistently defied skeptics—achieving reusability when deemed impossible, capturing dominant market share against entrenched competitors, and scaling Starlink faster than any satellite internet [20] service in history.

However, the specific claim of $475 billion by 2030 requires assuming:

- ■Starlink maintains 66%+ annual growth through 2030

- ■Starship achieves full operational capability and captures new market categories

- ■AI infrastructure materializes as a $250+ billion business within five years

While each pillar has merit, the compound probability of all three achieving their upper-bound projections simultaneously renders the 475 billion figure optimistic rather than conservative. A more defensible projection would place SpaceX's 2030 revenue in the 150-250 billion range, representing 8-13x growth—still extraordinary but grounded in demonstrated capabilities rather than speculative market capture.

Verdict: The claim's direction is correct—SpaceX will experience transformative growth—but its magnitude overstates the achievable timeline. The $475 billion figure represents an upper-bound scenario requiring near-perfect execution across all segments, rather than a baseline expectation.

Round 3

Core claim: The $475 billion 2030 SpaceX revenue forecast remains unsupported and implausible.

SpaceX’s current business model does not justify a jump from roughly

19 billion

in 2025 to nearly

475 billion

by 2030. The implied growth rate is extraordinary for a capital-intensive aerospace company, and no credible public evidence shows a revenue base or booked pipeline anywhere near that scale. The claim also depends on assuming that Starlink can reach tens of millions of subscribers and that launch services will expand into a market large enough to absorb such a surge, yet the real addressable market [1] remains far smaller than the forecast requires. reuters.com fcc.gov

The strongest FALSE-side point is that the claim mixes speculation with unsupported business categories. Starlink is real and growing, but the leap from millions of users to the level needed for

$475 billion

in total revenue is not grounded in market size, pricing power, or capacity constraints. Likewise, launch revenue is constrained by the overall launch market and by the economics of reusable rockets; Starship [22] may improve margins and throughput, but it does not create a market large enough on its own to justify a five-year revenue explosion of this magnitude. spacenews.com oecd.org

The opponent’s most compelling counter-argument is that Starlink has shown rapid subscriber growth and that SpaceX could monetize aviation, maritime, government, and defense customers more aggressively. That is a real strength in the affirmative case, and it supports continued revenue growth. But it still falls far short of proving a path to

$475 billion

. The claim relies on a second stretch: “AI infrastructure revenues.” There is no solid, verifiable evidence that SpaceX currently operates a meaningful AI infrastructure revenue segment at anything like the scale asserted. The affirmative case therefore stacks an unproven revenue line on top of aggressive Starlink assumptions and then treats the sum as if it were established fact. sec.gov spacex.com/starlink

On balance, the FALSE side is stronger. SpaceX may continue to grow quickly, and Starlink may become a much larger contributor. But the leap to nearly half a trillion dollars in annual revenue by 2030 is not supported by public disclosures, market sizing, or realistic execution assumptions. The claim is therefore false.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.000 | 36 | 60 | TRUE | FALSE | 85% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] addressable market — Total Addressable Market (TAM) — The total revenue opportunity available for a product or service, assuming 100% market share.

[2] AI inference — Artificial Intelligence inference — The process of using a trained AI model to make predictions or decisions on new data, often performed at the 'edge' (e.g., on devices) for real-time applications.

[3] Artemis program — A NASA-led international program to return humans to the Moon and establish a sustainable lunar presence, with SpaceX contracted for lunar lander development.

[4] CAGR — Compound Annual Growth Rate — The mean annual growth rate of an investment or revenue over a specified period longer than one year, assuming profits are reinvested at the end of each year.

[5] constellation — satellite constellation — A group of artificial satellites working together as a system to provide global or near-global coverage, such as Starlink's network of thousands of satellites.

[6] edge computing — A distributed computing paradigm that brings computation and data storage closer to the sources of data, such as IoT devices or autonomous vehicles, to improve response times and save bandwidth.

[7] fixed wireless — fixed wireless access (FWA) — A type of wireless broadband service that provides internet access to a fixed location (e.g., a home or business) using radio waves, often as an alternative to fiber or cable.

[8] Grok — An AI chatbot developed by xAI, a company mentioned in the debate as being acquired by SpaceX to form an AI infrastructure segment.

[9] heavy-lift vehicle — super-heavy lift launch vehicle — A rocket class capable of lifting more than 50 metric tons to low Earth orbit (LEO); SpaceX's Starship is designed as a fully reusable super-heavy lift vehicle.

[10] hyperscale data center — A massive data center facility designed to support large-scale cloud computing, AI workloads, and big data processing, often consuming hundreds of megawatts of power.

[11] IoT — Internet of Things — A network of physical devices (e.g., sensors, vehicles) embedded with electronics and connectivity to collect and exchange data.

[12] IPO — Initial Public Offering — The process by which a private company offers shares to the public for the first time, often used as a reference for disclosed financial data in the debate.

[13] launch cadence — The frequency or rate at which a company or organization conducts rocket launches, often measured in launches per year.

[14] marginal cost — The additional cost incurred to produce one more unit of a good or service; in rocketry, the cost of a single additional launch after fixed costs are covered.

[15] market share — The percentage of an industry's total sales that is earned by a particular company over a specified time period.

[16] mega-constellation — A very large satellite constellation, typically consisting of thousands of satellites, designed to provide global broadband internet or other services.

[17] orbital data center — A conceptual data center located in space, leveraging solar power and passive cooling to process data, potentially serving AI and edge computing needs.

[18] passive cooling — A cooling method that uses natural heat transfer (e.g., radiation to space) without mechanical systems, cited as an advantage for space-based data centers.

[19] revenue floor — A guaranteed minimum level of revenue, often secured through long-term contracts, providing a baseline for financial projections.

[20] satellite internet — Internet access provided via communication satellites, typically in low Earth orbit (LEO), offering broadband connectivity to remote or underserved areas.

[21] Starshield — A SpaceX program offering secure, government-grade satellite services for national security and defense applications, leveraging Starlink technology.

[22] Starship — SpaceX's fully reusable super-heavy lift launch vehicle, designed for missions to the Moon, Mars, and beyond, with a payload capacity of over 100 metric tons to orbit.

[23] terrestrial — Relating to Earth-based infrastructure (e.g., terrestrial data centers, fiber networks), as opposed to space-based systems.

[24] total addressable market — Total Addressable Market (TAM) — The total revenue opportunity available for a product or service, assuming 100% market share.

[25] vertically integrated — A business model where a company controls multiple stages of its supply chain, such as SpaceX controlling both launch services and satellite payload manufacturing.

The following financial data tables were referenced during the debate exchanges:

| Segment | 2025 Revenue | 2030 Projected | CAGR | Key Driver |

|---|---|---|---|---|

| Starlink | $11B | $140B | 66% | 50M+ subscribers, govt/aviation |

| AI Infrastructure | $15B+ | $250B | 76% | Anthropic contract, orbital data centers |

| Launch Services | $8B | $85B | 60% | Starship, Artemis, commercial |

| Total | $34B+ | $475B | 69% | Combined segment growth |

Legend: SpaceX revenue projections by segment (2025–2030). Revenues in USD billions; CAGR = compound annual growth rate. Source: IPO filings, analyst projections.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.