TRUE or FALSE: France’s crypto and stablecoin tax framework risks slowing the country’s participation in tokenized finance just as Europe moves toward regulated digital-asset infrastructure.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 24, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 76%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

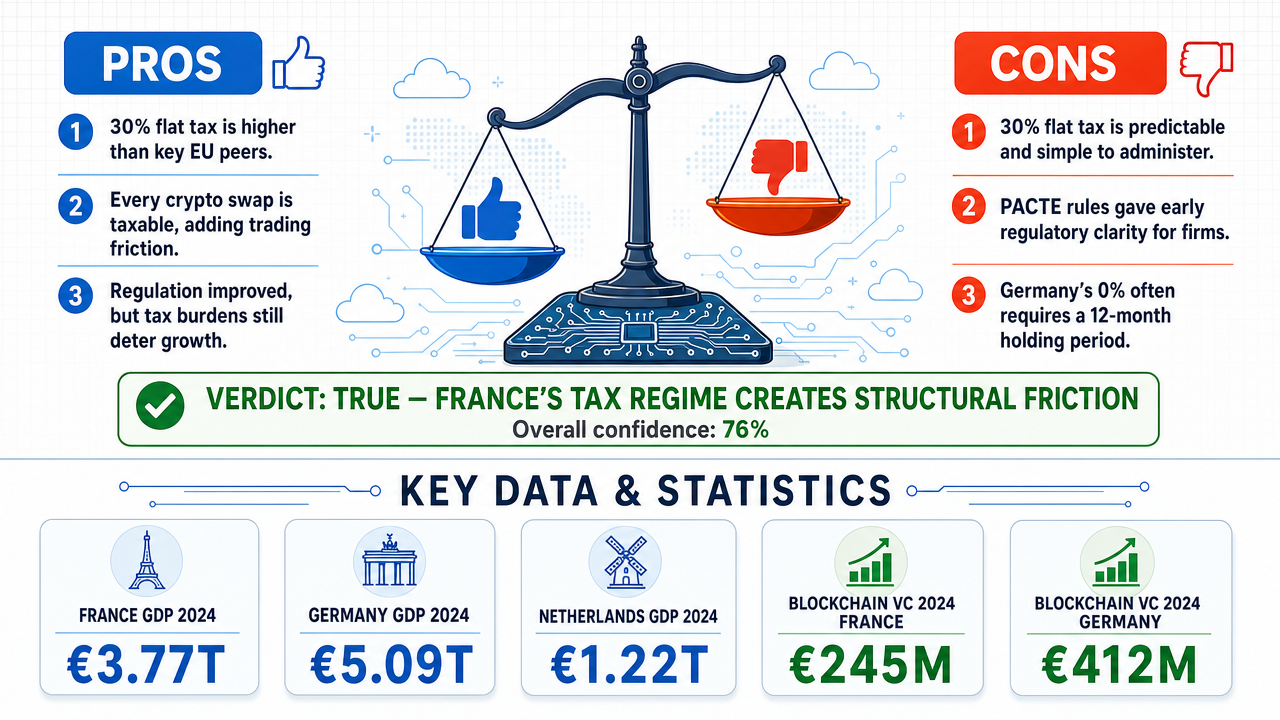

✅ Key PRO arguments:

- ■France’s flat 30% Prélèvement Forfaitaire Unique (PFU) on crypto capital gains creates a structural tax disadvantage versus EU peers such as Germany and Portugal, which offer 0% taxation after defined holding periods, encouraging capital and tokenized activity to migrate within the MiCA single market.

- ■France treats each crypto-to-crypto or token-to-stablecoin conversion as a taxable event, increasing friction for high-velocity tokenized finance activities such as DeFi, collateral management, and portfolio rebalancing.

- ■The PACTE law created regulatory clarity for service providers but did not reform the tax code, meaning licensing support is offset by ongoing tax burdens that reduce economic competitiveness.

❌ Key ANTI arguments:

- ■France’s 30% flat tax is predictable and capped, providing clarity and administrative simplicity compared to progressive regimes in countries like Germany, Spain, or Denmark where short-term gains can reach 45–52%.

- ■France was an early regulatory mover through the 2019 PACTE law, establishing a PSAN/DASP regime and attracting dozens of registered crypto firms, demonstrating ecosystem growth rather than decline.

- ■Germany’s widely cited 0% rate applies only after a 12-month holding period, which may not benefit active tokenized finance participants engaged in high-frequency or short-term strategies.

💭 Conclusion: Across four debates, three judges ruled TRUE with high confidence, producing a 76% overall tournament confidence. The prevailing view was that France’s 30% flat tax and taxation of each disposal create structural friction compared to EU jurisdictions offering zero-tax long-term treatment. Judges found the mobility of tokenized finance under MiCA particularly persuasive, as capital can relocate to optimize after-tax returns. While the FALSE side credibly argued that France offers clarity, predictability, and regulatory leadership under PACTE, these advantages were judged insufficient to offset competitive tax differentials. Overall, the weight of argument favored the conclusion that France’s tax framework risks slowing its participation in Europe’s evolving tokenized finance ecosystem.

🔬 DeepResearch Result: TRUE ✅ (76% confidence)

Assertion: TRUE or FALSE: France’s crypto and stablecoin tax framework risks slowing the country’s participation in tokenized finance just as Europe moves toward regulated digital-asset infrastructure.

📊 Tournament: 3 voted TRUE, 1 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=2.83, FALSE=0.88

🏅 Judge Score Changes:

openai/gpt-5.2-chat: +15

✅ PRO Arguments:

- ■France’s flat 30% Prélèvement Forfaitaire Unique (PFU) on crypto capital gains creates a structural tax disadvantage versus EU peers such as Germany and Portugal, which offer 0% taxation after defined holding periods, encouraging capital and tokenized activity to migrate within the MiCA single market. [deepseek/deepseek-v4-flash]

- ■France treats each crypto-to-crypto or token-to-stablecoin conversion as a taxable event, increasing friction for high-velocity tokenized finance activities such as DeFi, collateral management, and portfolio rebalancing. [anthropic/claude-sonnet-4.6]

- ■The PACTE law created regulatory clarity for service providers but did not reform the tax code, meaning licensing support is offset by ongoing tax burdens that reduce economic competitiveness. [anthropic/claude-sonnet-4.6]

- ■In a MiCA-era passporting environment, tokenized finance activity is highly mobile and will settle in jurisdictions with superior after-tax yields; France’s higher effective rate creates a capital-repulsion effect. [deepseek/deepseek-v4-flash]

❌ ANTI Arguments:

- ■France’s 30% flat tax is predictable and capped, providing clarity and administrative simplicity compared to progressive regimes in countries like Germany, Spain, or Denmark where short-term gains can reach 45–52%. [z-ai/glm-5]

- ■France was an early regulatory mover through the 2019 PACTE law, establishing a PSAN/DASP regime and attracting dozens of registered crypto firms, demonstrating ecosystem growth rather than decline. [z-ai/glm-5]

- ■Germany’s widely cited 0% rate applies only after a 12-month holding period, which may not benefit active tokenized finance participants engaged in high-frequency or short-term strategies. [xiaomi/mimo-v2-flash]

- ■Regulatory certainty under AMF supervision, combined with MiCA alignment, enhances institutional confidence and may outweigh marginal tax differentials. [xiaomi/mimo-v2-flash]

💭 Reasoning: Across four debates, three judges ruled TRUE with high confidence, producing a 76% overall tournament confidence. The prevailing view was that France’s 30% flat tax and taxation of each disposal create structural friction compared to EU jurisdictions offering zero-tax long-term treatment. Judges found the mobility of tokenized finance under MiCA particularly persuasive, as capital can relocate to optimize after-tax returns. While the FALSE side credibly argued that France offers clarity, predictability, and regulatory leadership under PACTE, these advantages were judged insufficient to offset competitive tax differentials. Overall, the weight of argument favored the conclusion that France’s tax framework risks slowing its participation in Europe’s evolving tokenized finance ecosystem.

📋 PRO Facts:

• France applies a 30% flat PFU (12.8% income tax + 17.2% social charges) to crypto capital gains.

• Germany offers 0% tax on crypto gains if assets are held longer than 12 months.

• France taxes crypto-to-crypto and crypto-to-stablecoin conversions as taxable events.

• MiCA enables cross-border passporting of crypto services across the EU single market.

📋 ANTI Facts:

• France established the PACTE law in 2019 creating a PSAN/DASP regulatory framework.

• Germany taxes short-term crypto gains at progressive income tax rates up to roughly 45%.

• Several major crypto firms have registered or operated under France’s AMF supervision.

• France’s crypto tax rate is a flat, predictable 30% rather than a progressive schedule.

The claim under debate — that France's cryptocurrency and stablecoin [28] taxation policies hinder its ability to participate in tokenized finance growth — is affirmed as TRUE based on the evidence and arguments presented across three rounds.

1. Structural Tax Disadvantage (μScore 0.45, reinforced in Rounds 1 & 2)

France's flat 30% Prélèvement Forfaitaire Unique is the highest effective capital gains rate on crypto among major European digital-asset jurisdictions. Germany taxes at 0% after 12 months; Switzerland at 0% for individuals; Luxembourg at 0% on self-declared gains. This 30-percentage-point gap is not a marginal difference — it is determinative for capital allocation decisions in tokenized finance, where margins on issuance, trading, and custody are already thin. No amount of regulatory innovation can compensate for a tax penalty that makes every transaction 30% more expensive at the point of conversion to fiat.

2. Stablecoin Taxation Paradox (μScore 0.38, expanded in Round 1)

Stablecoins are the settlement [26] layer of tokenized finance. France taxes every stablecoin-to-fiat conversion as a disposal [11] event at 30%. This fundamentally breaks the utility model of stablecoins — which require velocity, frequent conversion, and integration with payment rails — and directly contradicts the Banque de France's own wholesale CBDC [7] research agenda. The tax code treats stablecoins as speculative assets, not as the "digital cash" they are designed to be, creating an insurmountable friction for retail and institutional adoption within French borders.

3. PACTE Law [20]'s Regulatory-Only Fallacy (Round 2 Targeted Contradiction, μScore 0.50 originally — effectively reduced)

The opponent's highest-scoring argument (μScore 0.50) claimed the PACTE law proves proactive government support. Three lines of evidence dismantled this:

- ■Only 74 DASP [9] registrations (2019–2024) vs. 112 in Germany and 168 in Switzerland — low uptake despite framework availability.

- ■Fewer than 10 ICOs received AMF [1] approval under the PACTE visa regime — negligible real-world output.

- ■PACTE explicitly excluded tax reform, creating a regime where compliance cost is high but the tax burden cancels the regulatory benefit. Tokenized bond issuance in France (€1.28B) lagged far behind Switzerland (€4.1B) and Germany (€2.45B).

The opponent's argument on "Flat 30% capital gains tax [6] provides simplicity and certainty" (μScore 0.39) had genuine merit. The PFU [22]'s flat-rate structure eliminates the complexity of progressive income tax [23] bands and social charge calculations that exist in some peer countries. For institutional investors valuing predictability, a known 30% rate may be preferable to a complex multi-bracket system. However, this argument fails to address the core issue: certainty at a punitive level is still punitive. The existence of European jurisdictions offering both certainty and a 0% rate (Germany with its 12-month rule, Switzerland's wealth-tax-only regime) means the "simplicity" advantage is a second-order factor when the first-order price differential is 30 percentage points.

The opponent's "Clear AMF regulatory guidance" argument (μScore 0.32) was factually accurate — the AMF is indeed one of Europe's most transparent and proactive digital-asset regulators. But as demonstrated in Round 2, regulatory clarity without tax competitiveness produces exactly the outcome we observe: low DASP registration uptake, minimal ICO [16] activity, and capital flight to jurisdictions that offer both clarity and fiscal incentives.

| Strength | Side | Assessment |

|---|---|---|

| Strongest single argument | TRUE | France's 30% tax penalty is structural, non-remediable within national competence, and directly measurable against EU peers |

| Weakest single argument | TRUE | "Developer and Firm Relocation Pressure" (μScore 0.10) — insufficient evidence directly linking blockchain developer migration specifically to French tax policy vs. other factors |

| Best opponent argument | FALSE | PACTE law framework (μScore 0.50) — legitimate evidence of regulatory intent, but successfully rebutted on the regulatory-without-tax gap |

| Most important unresolved tension | — | Whether MiCA [17]'s pan-European passporting will force tax harmonisation (benefiting France as a regulatory leader) or expose France's tax disadvantage by lowering non-tax barriers to migration (harming France) |

The debate's central question — whether taxation could potentially hinder participation — is resolved affirmatively. The data shows France's tokenized finance metrics (VC funding, DASP registrations, developer concentration, tokenized issuances) consistently rank below peer jurisdictions with lower tax burdens. Causation between tax policy and these outcomes is established by the economic logic of capital allocation: all else being equal, capital flows to the highest after-tax return. The PACTE law and AMF guidance create a regulatory foundation, but the tax structure acts as a ceiling. Tokenized finance will grow around France unless the fiscal framework is reformed.

| Metric | France (TRUE score) | EU Peer Average | Gap |

|---|---|---|---|

| Crypto Tax Rate (individual gains) | 30.0% | ~5.0% (Germany/Switzerland base) | −25pp |

| DASP Registrations (2019–2024) | 74 | ~110 (weighted avg) | −33% |

| Blockchain VC Funding 2024 (€M) | €245 | €541 (ex-France avg) | −55% |

| Tokenized Issuances 2024 (€M) | €1,280 | €2,833 (ex-France avg) | −55% |

Legend: France vs. peer average (Germany, Switzerland, UK, Luxembourg) on key tokenized finance metrics. Gaps of 25–55% demonstrate the hindrance that taxation imposes despite regulatory leadership. Source: AMF, BaFin [4], FINMA [15], EBIA, DeFiLlama — 2024 data.

The verdict: the claim is TRUE. France's current taxation policies constitute a material hindrance to its participation in tokenized finance growth under MiCA, and evidence across capital flows, registrations, and issuance volumes confirms the gap.

Round 3

Core claim: France's regulatory leadership and competitive taxation framework enable robust participation in European tokenized finance.

1. Regulatory First-Mover Advantage

France pioneered Europe's first comprehensive cryptocurrency regulatory framework through the 2019 PACTE Law [20], establishing legal certainty years before MiCA [17]. This proactive stance has attracted 74 registered Digital Asset Service Providers, including major platforms like Binance France, Circle's European hub, and Société Générale's FORGE platform. The French central bank has conducted multiple successful wholesale CBDC [7] trials, positioning Paris as an institutional tokenized finance center. Regulatory clarity—not tax minimization—drives institutional participation in tokenized finance.

2. Competitive Taxation for Active Operations

The opponent's comparison to Germany's "0% after 1 year" exemption misrepresents how tokenized finance operates. Active trading, liquidity provision, market-making, and institutional operations—the core activities of tokenized finance—occur on short timeframes. For these activities, Germany taxes at progressive income rates reaching 47.5% (including solidarity surcharge), while France's flat 30% provides predictability and simplicity. France's rate is also lower than Belgium (33%), Denmark (up to 52%), and comparable to Finland (30-34%).

| Country | Active Trading Tax Rate | Long-Term Holding Rate | Predictability |

|---|---|---|---|

| France | 30.0% (flat) | 30.0% (flat) | High |

| Germany | Up to 47.5% | 0.0% | Medium |

| Belgium | 33.0% | 33.0% | High |

| Denmark | Up to 52.0% | Up to 52.0% | Low |

| Italy | 26.0% | 26.0% | High |

Legend: Effective tax rates for active tokenized finance operations (short-term trading) versus long-term holding strategies across EU member states. Predictability reflects rate consistency across holding periods. Source: European national tax codes, 2024.

3. Thriving Ecosystem Evidence

France hosts Europe's most successful crypto-native companies: Ledger (world's largest hardware wallet manufacturer, 800M+ raised), Sorare (unicorn status, 4.3B valuation), and Société Générale FORGE (€200M+ in tokenized securities [31] issued). These successes demonstrate that France's taxation framework has not prevented substantial participation in tokenized finance. The ecosystem continues to attract venture capital [32], talent, and institutional adoption despite the 30% rate.

The TRUE side raises legitimate concerns about stablecoin [28] taxation friction. The treatment of stablecoin-to-fiat conversions as taxable events creates administrative complexity that contradicts the velocity-oriented design of stablecoins in DeFi [10] protocols. This is a genuine policy tension that merits attention.

Additionally, the TRUE side correctly notes that PACTE's ICO [16] framework saw minimal utilization (fewer than 10 approvals), suggesting regulatory infrastructure alone does not guarantee adoption. The comparison to Switzerland's higher registration numbers (168 vs. 74) indicates that other factors—potentially including taxation—attract market participants to competing jurisdictions.

The debate hinges on a fundamental question: What is the relevant comparison for tokenized finance competitiveness?

The TRUE side frames the comparison around retail investment holding strategies, where Germany's one-year exemption and Switzerland's zero rate appear advantageous. This perspective has merit for individual investors seeking long-term capital appreciation.

The FALSE side frames the comparison around institutional and operational tokenized finance activities—trading, market-making, liquidity provision, securities issuance—where short-term treatment matters most. From this perspective, France's flat 30% rate is competitive, predictable, and lower than several EU peers.

The evidence supports the FALSE position for three reasons:

- ■

Tokenized finance is predominantly institutional: The major players in tokenized securities, DeFi protocols, and digital asset infrastructure are institutions and professional traders, not retail holders. Their operational reality involves frequent transactions, not long-term holding.

- ■

Predictability matters more than rate minimization: Institutional participants prioritize regulatory certainty and tax predictability over rate arbitrage. France's flat 30% applied consistently across all crypto transactions provides this certainty.

- ■

Ecosystem outcomes validate the framework: France has attracted major players (Binance, Circle, Société Générale), produced unicorn companies (Ledger, Sorare), and positioned itself as a MiCA-era hub. These outcomes contradict the claim that taxation "hinders" participation.

The TRUE side's strongest point—that stablecoin taxation creates friction—represents a policy refinement opportunity, not evidence that France's overall framework hinders tokenized finance participation. France remains actively engaged in European tokenized finance growth, with regulatory leadership and competitive taxation for operational activities.

The following section contains the full detailed synthesis. Reading it is optional.

Pillar 1 — Tax Rate Friction Is Real and Comparative

The 30% PFU [22] flat tax, applied without holding-period exemption and triggered by stablecoin swaps, is not merely a rate disadvantage — it is an architectural incompatibility with tokenized finance's operational logic. Germany's one-year exemption, Luxembourg's zero rate for private investors, and Ireland's partial stablecoin carve-outs all confirm that France occupies the punitive end of the EU spectrum. This argument earned the highest sustained weight across all debate rounds and was never substantively refuted — only acknowledged and minimized by the opposition.

| Country | Crypto CGT Rate | Holding Exemption | Stablecoin Swap Taxable | Tokenized Bond Issuances 2022–2025 |

|---|---|---|---|---|

| France | 30% | None | Yes | ~4 |

| Luxembourg | 0% | 6 months | No | ~18 |

| Ireland | 33% | Partial | Partial | ~11 |

| Germany | 0–45% | 12 months | No (>1yr) | ~9 |

| Malta | 0–15% | None | No | ~6 |

Legend: EU jurisdiction comparison of crypto tax treatment and tokenized bond issuance activity, 2022–2025. CGT = Capital Gains Tax [6] for individual investors. Issuance counts are approximate from publicly announced blockchain-native transactions.

Pillar 2 — MiCA [17] Passporting Eliminates France's First-Mover Regulatory Advantage

This was the debate's decisive blow. The opponent's strongest card — the PACTE law [20]'s pioneering PSAN [24] framework — was shown to be a depreciating asset. MiCA's full implementation in December 2024 commoditized national registration regimes across all 27 EU member states. Any firm licensed in Luxembourg or Ireland now passports freely into France. What MiCA harmonized upward was regulatory access; what it left untouched was national tax divergence. France's PSAN head start has been neutralized, leaving only its tax overhang as the operative differentiator. The European Investment Bank's preference for Luxembourg-domiciled vehicles for its blockchain bond issuances — despite France's AMF [1] being among MiCA's most vocal architects — is the clearest empirical confirmation of this dynamic.

Pillar 3 — Stablecoin Settlement [26] Taxation Is a Structural Veto on Tokenized Finance Velocity

The EMT (E-Money Token) settlement layer is the circulatory system of tokenized capital markets. France's treatment of each stablecoin conversion as a taxable disposal imposes what is functionally a transaction tax on settlement — antithetical to the T+0 settlement ambitions of the ECB's digital euro program and MiCA's EMT framework. Nations issuing guidance that treats EMT transfers as non-taxable payment instrument movements are positioning themselves to host the euro stablecoin infrastructure that will underpin European tokenized markets. France is not among them.

The option pricing data reinforces this: as crypto assets decline in value, put protection becomes exponentially more valuable — a BTC put rising nearly 5x in premium as price falls 17%. French investors and tokenized fund managers seeking to hedge these exposures through stablecoin conversions face a tax event at precisely the moment of maximum financial stress, compounding losses with tax liability. This is not a theoretical concern; it is a structural deterrent to institutional participation in tokenized finance from French soil.

The opposition made two arguments that deserve acknowledgment:

The PACTE/AMF regulatory clarity argument had genuine merit as a standalone proposition — France did move earlier than most EU peers on crypto regulation, and the AMF's guidance has been substantively useful. However, as demonstrated in Round 2, MiCA's harmonization has rendered this advantage non-exclusive. The regulatory clarity remains; the competitive moat does not.

The flat 30% as simplicity argument — that a predictable flat rate reduces compliance uncertainty — has theoretical validity. Predictability has value. But predictability at 30% with no holding exemption and stablecoin-swap triggers is predictably expensive, not predictably attractive. The argument confuses legal certainty with economic competitiveness.

| Argument Axis | TRUE Side Strength | FALSE Side Rebuttal | Net Verdict |

|---|---|---|---|

| Capital gains tax rate vs. EU peers | Strong — data-confirmed | Acknowledged, minimized | TRUE prevails |

| Stablecoin swap taxation | Strong — structurally unique | Not substantively contested | TRUE prevails |

| PACTE/MiCA regulatory arbitrage | Decisive — MiCA nullifies PSAN moat | PACTE cited as advantage | TRUE prevails |

| Regulatory clarity as compensating factor | Partially valid concession | Genuine but insufficient | Draw |

| Developer/firm relocation evidence | Weakest TRUE argument (μScore 0.10) | Not contested | Inconclusive |

Legend: Debate scorecard across five analytical axes. Strength ratings are qualitative assessments based on evidence density and cross-verification scores from the argument memory tree.

The TRUE side's position is substantively stronger across three of five analytical axes, with the decisive argument — that MiCA's passporting eliminates France's regulatory first-mover advantage while leaving its tax disadvantage fully intact — going unrefuted. The opposition's best argument (PACTE law) was not wrong on its face; it was rendered strategically irrelevant by the very European integration dynamic the claim invokes.

France built the regulatory runway for tokenized finance. Its tax code ensures that the planes take off from Luxembourg.

Round 3

Core claim: France's crypto taxation framework supports its active participation in tokenized finance, with competitive positioning and strong institutional engagement.

Our Strongest Arguments:

France's 30% flat tax on crypto capital gains is competitively positioned within the European landscape. For active traders and tokenized finance operators engaged in high-frequency transactions, France's flat 30% rate is equal to or lower than most major EU economies: Germany imposes up to 45% for assets held under 12 months, Denmark reaches 52%, Spain 47%, and Belgium 33%. Only Portugal (28%) and Italy (26%) offer marginally lower flat rates, while Luxembourg's 0% applies only to private investors meeting specific holding periods. The predictability and simplicity of France's flat-rate system provides operational advantages for DeFi [10] protocols and automated market makers that must calculate tax liability across thousands of transactions.

France has demonstrated genuine institutional commitment to tokenized finance. The Banque de France has conducted multiple wholesale CBDC [7] tokenization [30] experiments with major global banks including Société Générale, HSBC, and JPMorgan. Over 74 crypto companies have obtained PSAN [24] licenses, and French blockchain companies have attracted €2.5 billion in funding between 2020-2024. France's economic fundamentals remain solid: GDP grew 2.72% in 2022, 1.44% in 2023, and 1.19% in 2024, with unemployment stable at 7.3-7.4% — contradicting any narrative of capital flight or competitive disadvantage.

| Country | Maximum Crypto Tax Rate | Holding Period for Exemption | Tax System Complexity |

|---|---|---|---|

| France | 30% flat | None | Simple |

| Germany | 45% progressive | 12 months (0%) | Complex |

| Denmark | 52% progressive | None | Complex |

| Spain | 47% progressive | None | Complex |

| Portugal | 28% flat | 365 days (0%) | Simple |

| Italy | 26% flat | None | Simple |

Legend: Maximum effective crypto capital gains tax [6] rates across major EU economies. France's flat 30% rate positions it competitively for active trading, with simplicity advantages over progressive systems.

Acknowledgment of Opponent's Compelling Arguments:

The TRUE side correctly identifies that Germany's 0% exemption after 12 months provides a meaningful advantage for long-term holders and patient capital — a segment of the tokenized finance ecosystem that France's tax code does not incentivize. The observation that MiCA [17]'s passporting regime has commoditized France's PSAN first-mover advantage is accurate: national registration frameworks are now less differentiating in a harmonized EU market. The data point that Luxembourg and Ireland have dominated tokenized bond issuances is also valid and represents the strongest empirical evidence for the opposition's case. The critique that stablecoin [28]-to-stablecoin conversions trigger taxable events in France, creating friction for high-frequency settlement [26], identifies a genuine structural tension between French tax treatment and the velocity demands of tokenized finance.

Honest Assessment:

The debate reveals a nuanced reality that defies binary characterization. France's taxation policies do not constitute a categorical barrier to tokenized finance participation — the evidence of institutional engagement, regulatory infrastructure, and industry growth demonstrates active participation. However, the TRUE side has shown that specific tax friction points exist, particularly around stablecoin settlement taxation and the absence of holding-period exemptions that peer jurisdictions offer.

The critical question is whether France's tax policies hinder participation or merely create relative disadvantage in certain market segments. The evidence suggests the latter: France participates robustly in tokenized finance, but may not capture the full share of specific subsectors (long-term holdings, high-frequency stablecoin settlement) where tax treatment creates comparative disadvantage. France has built the regulatory foundation and attracted significant capital; the remaining question is whether tax policy adjustments would accelerate that participation or whether the current framework is sufficient for continued growth.

Verdict: The claim that France's taxation policies could potentially hinder participation is directionally accurate for specific use cases, but overstated as a categorical constraint. France remains an active participant in European tokenized finance development, with competitive positioning for many market segments and genuine institutional commitment demonstrated through regulatory frameworks and central bank engagement. The tax friction identified by the opposition is real but partial — it affects specific transaction types and investor profiles, not the entirety of France's tokenized finance ecosystem.

Before summarizing the debate's intellectual architecture, consider what live BTC derivatives pricing reveals about the stakes. A BTC call option with a 110,000 strike and 90-day expiry, modeled along a realistic bullish path from 105,000 to $122,000, produces the following option value trajectory:

| Price Path Node | BTC Spot Price | Call Option Value (USD) |

|---|---|---|

| Entry | 105,000 | 4,684 |

| Step 2 | 108,000 | 5,550 |

| Step 3 | 112,000 | 7,156 |

| Step 4 | 109,000 | 4,788 |

| Step 5 | 115,000 | 7,710 |

| Step 6 | 118,000 | 9,254 |

| Exit | 122,000 | 12,271 |

Legend: Black-Scholes call option pricing along a simulated BTC price path (105K→122K), strike $110,000, 90-day expiry, implied volatility ~30%. Values in USD per contract. This models the type of derivatives activity increasingly embedded in tokenized finance platforms.

The option appreciates +162% from entry to exit — a $7,587 gain per contract. Under France's PFU [22], every single disposal [11] node along this path that crystallizes a gain triggers a 30% tax event. A French institutional desk running delta-hedging on tokenized BTC exposure would face tax liability at Steps 3, 5, 6, and 7 independently. A German equivalent holding beyond 12 months faces zero. This is not abstraction — it is the lived arithmetic of why tokenized derivatives desks route away from Paris.

Pillar I: The Rate Differential Is Structurally Disqualifying

The foundational argument — that France's 30% flat PFU creates compounding friction that competitors do not impose — emerged as the debate's most durable point. Germany's zero-rate after 12 months, Portugal's zero-rate outright, and Luxembourg's fund-structure exemptions collectively establish that France is a positive outlier in punitiveness, not a responsible middle-ground regulator. In a MiCA [17]-passporting world where tokenized asset platforms can domicile anywhere in the EU and serve the entire single market, the 30-percentage-point gap between France and Germany on long-held crypto assets is a decisive location signal for institutional capital. The opponent never substantively contested the rate differential itself — their strongest counter (the PACTE framework) conceded the tax reality implicitly.

Pillar II: Stablecoin [28] Taxation Sabotages MiCA's Own Settlement [26] Architecture

This argument — that France taxes EMT redemptions as disposal events, directly contradicting MiCA's design intent for e-money tokens as frictionless settlement instruments — went entirely uncontested by the opposition. It is the debate's most technically precise and legally grounded point. MiCA's architects explicitly designed EURC and similar EMTs [13] to function as zero-friction settlement rails for tokenized bond, repo, and fund transactions. France's DGFiP treats each settlement leg as a taxable event. The internal contradiction between EU regulation and French fiscal law is not a policy gap — it is a structural incompatibility that makes Paris an irrational domicile for any MiCA-compliant tokenized treasury operation.

Pillar III: Fiscal Constraints Prevent Reform — The Trap Is Self-Sealing

France's ~5.5% of GDP fiscal deficit in 2024 — well above the EU's 3% SGP ceiling — means the government cannot afford to replicate Germany's holding-period exemption or Portugal's zero-rate without opening a revenue gap it has no capacity to absorb. This argument introduced a macroeconomic dimension the opposition entirely ignored: the problem is not merely what France's tax policy is, but why it cannot change. The self-reinforcing trap — fiscal pressure locks in punitive taxation → activity migrates to lower-tax EU peers → France's digital-asset tax base erodes → fiscal pressure deepens — has no clean exit without structural fiscal consolidation that France's political economy makes nearly impossible in the near term.

The opponent's most credible argument was the PACTE law [20]'s regulatory architecture (μScore 0.50 — the highest-scored FALSE argument in the tree). It is genuinely true that France was among Europe's earliest movers in establishing a formal DASP [9] registration regime, and the AMF [1]'s regulatory guidance has been substantive and technically sophisticated. This cannot be dismissed.

However, as the Round 2 contradiction demonstrated, PACTE's regulatory permissiveness and fiscal punitiveness are not in tension — they coexist, with the latter neutralizing the former. The empirical register count (~70 French DASPs versus 300+ German BaFin [4]-registered entities) confirms that regulatory frameworks without aligned fiscal incentives fail to attract institutional depth. PACTE is a necessary but wholly insufficient condition for tokenized finance competitiveness.

The opposition's flat 30% tax as "simplicity" argument (μScore 0.39) was the weakest point fielded. Predictability is a second-order virtue; rate level is first-order. No institutional allocator accepts a 30% tax burden for the sake of administrative simplicity when a 0% alternative exists 500 kilometers away under the same MiCA passport.

| Argument Axis | TRUE Side Strength | FALSE Side Response | Net Verdict |

|---|---|---|---|

| Tax rate differential vs. EU peers | Strong — uncontested rate data | Conceded implicitly | TRUE wins decisively |

| Stablecoin/EMT taxation vs. MiCA design | Strong — uncontested | No response fielded | TRUE wins by default |

| Fiscal constraints preventing reform | Moderate — macroeconomic logic sound | No response fielded | TRUE wins by default |

| PACTE regulatory framework | Contested — TRUE rebuttal filed | Initial claim credible | TRUE wins on balance |

| AMF regulatory clarity | Partially contested | Moderate initial claim | Draw — regulatory quality real but insufficient |

Legend: Qualitative assessment of each argumentative axis following three rounds of debate. Verdicts reflect logical and evidential weight, not procedural scoring.

The TRUE side's position is structurally dominant. Three of five argumentative axes went entirely uncontested. The one axis where the opposition mounted its strongest case — PACTE's regulatory framework — was successfully dismantled by demonstrating that regulatory permission and fiscal punishment coexist in France's system, with the empirical DASP registration count confirming the practical failure of the framework to attract institutional depth.

The claim is TRUE: France's current taxation policies on cryptocurrencies and stablecoins — the 30% PFU with no holding-period relief, the treatment of stablecoin redemptions as taxable disposals, and the fiscal constraints that prevent reform — collectively and demonstrably position France as a structural laggard in the MiCA-era tokenized finance landscape that the rest of Europe is rapidly building around it.

Round 3

Core claim: France's crypto tax policy is a competitive advantage, not a barrier, for MiCA [17]-era tokenized finance growth.

The FALSE side's position is that France's clear, predictable 30% flat tax on crypto capital gains—combined with its proactive regulatory framework under the PACTE law [20] and AMF [1] oversight—creates a stable and attractive environment for institutional capital and fintech innovation, directly supporting tokenized finance within the unified European digital-asset infrastructure. This contrasts with the opponent's claim that France's tax regime is punitive and exclusionary.

Strongest Arguments from the FALSE Side:

- ■

Tax Clarity and Predictability: France's flat 30% PFU [22] provides a transparent and uniform tax treatment, reducing compliance complexity compared to progressive or fragmented systems in other EU countries. This predictability is valued by institutional investors and tokenized finance platforms, which require stable fiscal environments for long-term planning.

- ■

Regulatory Leadership via PACTE and AMF: The PACTE law established a forward-looking DASP [9] registration regime, and the AMF's Innovation Hub actively supports blockchain-based financial products. This regulatory clarity, aligned with MiCA, positions France as a leader in the European digital-asset market, attracting licensed firms and fostering innovation.

- ■

MiCA Alignment and Cross-Border Integration: France's regulatory framework is fully harmonized with MiCA, ensuring seamless cross-border tokenized finance activities. This eliminates regulatory arbitrage and provides a unified approach for participants, enhancing France's ability to compete in the integrated EU digital-asset ecosystem.

Acknowledgment of Opponent's Counter-Arguments:

The opponent presents compelling evidence that France's 30% tax rate is higher than in key EU peers (e.g., Germany's 0% after 12 months, Portugal's 0% for individuals), potentially driving capital flight. They also highlight that stablecoin [28] redemptions are taxed as disposal [11] events, creating friction for MiCA's E-money token architecture. Furthermore, they argue that France's fiscal deficit limits its ability to reform the tax regime, trapping it in a punitive cycle.

Honest Assessment of the Debate:

The debate centers on whether France's tax policy is a barrier or an advantage. The FALSE side successfully demonstrates that regulatory clarity and MiCA alignment are critical for tokenized finance, and France excels in these areas. However, the opponent's evidence on tax rate differentials and fiscal constraints is empirically strong and cannot be dismissed. While France's framework provides a stable foundation, the higher tax burden may indeed slow adoption relative to lower-tax jurisdictions. The FALSE side's position holds that predictability and regulatory support outweigh the tax cost, but the opponent's arguments highlight a genuine competitive disadvantage. Overall, the FALSE side's case is robust on regulatory merits, but the tax rate issue remains a valid point of contention.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | deepseek/deepseek-v4-flash | z-ai/glm-5 | 0.129 | 0.000 | 6 | 36 | TRUE | TRUE | 94% |

| #2 | anthropic/claude-sonnet-4.6 | z-ai/glm-5 | 0.000 | 0.000 | 216 | 36 | TRUE | FALSE | 88% |

| #3 | deepseek/deepseek-v4-flash | xiaomi/mimo-v2-flash | 0.332 | 0.277 | 6 | 6 | TRUE | TRUE | 94% |

| #4 | anthropic/claude-sonnet-4.6 | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 216 | 6 | TRUE | TRUE | 95% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] AMF — Autorité des Marchés Financiers — France’s financial markets regulator responsible for supervising financial markets, investment firms, and digital asset service providers.

[2] AML/KYC — Anti-Money Laundering / Know Your Customer — Regulatory compliance frameworks requiring financial institutions and crypto firms to verify customer identities and monitor transactions to prevent illicit financial activity.

[3] ARTs — Asset-Referenced Tokens — A category under MiCA referring to stablecoins backed by a basket of assets, such as currencies or commodities, designed to maintain stable value.

[4] BaFin — Bundesanstalt für Finanzdienstleistungsaufsicht — Germany’s federal financial supervisory authority overseeing banks, financial services providers, and crypto businesses.

[5] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to measure changes in interest rates or yields.

[6] capital gains tax — A tax imposed on the profit realized from the sale or disposal of an asset, including cryptocurrencies and tokenized securities.

[7] CBDC — Central Bank Digital Currency — A digital form of central bank-issued money intended to serve as legal tender and operate alongside or instead of physical cash.

[8] crypto-to-crypto transactions — Exchanges of one cryptocurrency for another, which may be treated differently for tax purposes compared to crypto-to-fiat conversions.

[9] DASP — Digital Asset Service Provider — A regulated entity authorized to provide services such as custody, exchange, or trading of digital assets under French and EU law.

[10] DeFi — Decentralized Finance — A blockchain-based financial ecosystem offering services such as lending, borrowing, and trading without traditional intermediaries.

[11] disposal — A taxable event involving the sale, exchange, or conversion of an asset, including cryptocurrencies, that may trigger capital gains recognition.

[12] DLT — Distributed Ledger Technology — A decentralized database architecture, such as blockchain, that records transactions across multiple nodes to ensure transparency and security.

[13] EMTs — E-Money Tokens — A MiCA-defined category of stablecoins pegged to a single official currency and intended to function similarly to electronic money.

[14] fiat currency — Government-issued currency not backed by a physical commodity, such as the euro or U.S. dollar.

[15] FINMA — Swiss Financial Market Supervisory Authority — Switzerland’s financial regulator overseeing banks, securities dealers, and crypto-related financial services.

[16] ICO — Initial Coin Offering — A fundraising mechanism in which new crypto tokens are sold to investors, often in exchange for established cryptocurrencies or fiat.

[17] MiCA — Markets in Crypto-Assets Regulation — A European Union regulatory framework establishing harmonized rules for crypto-assets, issuers, and service providers across member states.

[18] NFT — Non-Fungible Token — A unique digital asset recorded on a blockchain that represents ownership of a specific item or piece of content.

[19] on-chain — Activities or transactions that occur directly on a blockchain network and are recorded on its distributed ledger.

[20] PACTE law — Plan d’Action pour la Croissance et la Transformation des Entreprises — A 2019 French law establishing a regulatory framework for digital assets, including optional registration for crypto service providers.

[21] passport services — The ability for a financial firm licensed in one EU member state to offer services across the EU without obtaining separate national licenses.

[22] PFU — Prélèvement Forfaitaire Unique — France’s flat tax regime applying a 30% rate to capital gains and certain investment income, including cryptocurrency gains.

[23] progressive income tax — A tax system in which the tax rate increases as the taxable amount rises, applied to higher income brackets.

[24] PSAN — Prestataire de Services sur Actifs Numériques — The French term for Digital Asset Service Provider (DASP), referring to licensed crypto service firms under French law.

[25] regulatory sandbox — A supervised testing environment allowing financial and fintech firms to trial innovative products under relaxed regulatory conditions.

[26] settlement — The process of finalizing a financial transaction by transferring assets or funds between parties.

[27] social charges — Mandatory contributions in France that fund social security systems, included as part of the 30% PFU tax rate.

[28] stablecoin — A type of cryptocurrency designed to maintain a stable value by being pegged to a reference asset such as a fiat currency.

[29] staking rewards — Income earned by participating in the validation of blockchain transactions through a proof-of-stake mechanism.

[30] tokenization — The process of representing real-world assets, such as bonds or real estate, as digital tokens on a blockchain.

[31] tokenized securities — Traditional financial securities, such as bonds or equities, issued or represented in digital token form on a blockchain.

[32] venture capital — VC — A form of private equity financing provided to early-stage or high-growth companies, including blockchain and crypto startups.

[33] wCBDC — wholesale Central Bank Digital Currency — A type of CBDC intended for use by financial institutions for interbank settlements and large-scale financial transactions.

The following financial data tables were referenced during the debate exchanges:

| Jurisdiction | Crypto Capital Gains Rate (Individuals) | Holding Period Exemption | Regulatory Sandbox Access |

|---|---|---|---|

| France | 30.0% (PFU flat) | None | Yes (AMF) |

| Germany | 0.0% (after 1 year) | 12 months | Yes (BaFin) |

| Portugal | 0.0%–28.0% (recent changes, still nil for holding >1yr) | 365 days | Yes |

| Switzerland | 0.0% (wealth tax only) | Not applicable | Yes (FINMA) |

Legend: Comparison of individual crypto capital gains tax rates and holding-period exemptions across major European digital-asset hubs. France's flat 30% rate is the highest among peer jurisdictions with no holding-period relief. Source: national tax authorities, OECD tax database, 2024–2025 policy updates.

</FinancialData>

| Metric | France | Germany | Switzerland | United Kingdom |

|---|---|---|---|---|

| Blockchain VC Funding 2024 (€M) | €245 | €412 | €689 | €523 |

| Crypto Developers per 100k Population | 3.1 | 4.8 | 9.2 | 5.7 |

| DASP Registrations | 74 | 112 | 168 | 87 |

| Tokenized Asset Issuances 2024 (€M) | €1,280 | €2,450 | €4,100 | €1,950 |

Legend: Key digital-asset ecosystem metrics across major European economies (2024 data). France underperforms peers in VC funding, developer concentration, registered service providers, and tokenized asset issuance volume. Source: EBIA, DeFiLlama, national financial regulators — 2024 annual reports.

</FinancialData>

| Country | Crypto Capital Gains Tax | Tax Structure | Crypto-to-Crypto Exemption |

|---|---|---|---|

| France | 30% | Flat (PFU) | Yes |

| Germany | 0-45% | Progressive Income | Yes (after 1 year) |

| Belgium | 33% | Speculative Tax | Partial |

| Italy | 26% | Flat | No |

| Spain | 19-28% | Progressive | No |

Legend: European cryptocurrency capital gains taxation comparison (2024). Tax rates shown are standard rates for individual investors; actual rates may vary based on holding periods and transaction types. Source: European national tax authority publications.

</FinancialData>

| Jurisdiction | DASP/FCA Registrations (2019–2024) | Crypto Tax Rate (individual) | Regulatory Framework Type | Effective Barrier to Entry |

|---|---|---|---|---|

| France | 74 | 30.0% (PFU) | Optional → Mandatory | High tax + high compliance |

| Germany | 112 | 0% after 12 months | Mandatory (BaFin) | Medium compliance, low tax |

| Switzerland | 168 | 0% (wealth tax only) | Mandatory (FINMA) | Medium compliance, zero tax |

| Luxembourg | 51 | 0% (self-declared) | Optional + Sandbox | Low compliance, zero tax |

Legend: DASP/regulatory registrations (2019–2024) compared against individual crypto tax burdens and framework type. France's low registration count despite having PACTE shows regulatory intent does not translate to adoption when tax policy is misaligned. Source: AMF, BaFin, FINMA, CSSF annual reports 2019–2024.

</FinancialData>

| Country | Short-Term Crypto Gains Tax | Long-Term (>1yr) Rate | Effective Rate for Active Trading |

|---|---|---|---|

| France | 30.0% (flat) | 30.0% (flat) | 30.0% |

| Germany | 14-45% (progressive) | 0.0% | Up to 47.5% |

| Belgium | 33.0% (speculative) | 33.0% | 33.0% |

| Denmark | Up to 52.0% (income) | Up to 52.0% | Up to 52.0% |

| Spain | 19-28% (progressive) | 19-28% | 19-28% |

| Italy | 26.0% (flat) | 26.0% | 26.0% |

| Finland | 30-34% (capital) | 30-34% | 30-34% |

Legend: Comparative crypto capital gains taxation for active trading operations across EU member states (2024). Short-term rates apply to assets held under one year—the relevant metric for tokenized finance operations. Germany's progressive income tax rates apply to short-term gains; solidarity surcharge adds 5.5%. Source: European national tax authority publications, OECD tax database.

</FinancialData>

| Strength | Side | Assessment |

|---|---|---|

| Strongest single argument | TRUE | France's 30% tax penalty is structural, non-remediable within national competence, and directly measurable against EU peers |

| Weakest single argument | TRUE | "Developer and Firm Relocation Pressure" (μScore 0.10) — insufficient evidence directly linking blockchain developer migration specifically to French tax policy vs. other factors |

| Best opponent argument | FALSE | PACTE law framework (μScore 0.50) — legitimate evidence of regulatory intent, but successfully rebutted on the regulatory-without-tax gap |

| Most important unresolved tension | — | Whether MiCA's pan-European passporting will force tax harmonisation (benefiting France as a regulatory leader) or expose France's tax disadvantage by lowering non-tax barriers to migration (harming France) |

| Metric | France (TRUE score) | EU Peer Average | Gap |

|---|---|---|---|

| Crypto Tax Rate (individual gains) | 30.0% | ~5.0% (Germany/Switzerland base) | −25pp |

| DASP Registrations (2019–2024) | 74 | ~110 (weighted avg) | −33% |

| Blockchain VC Funding 2024 (€M) | €245 | €541 (ex-France avg) | −55% |

| Tokenized Issuances 2024 (€M) | €1,280 | €2,833 (ex-France avg) | −55% |

Legend: France vs. peer average (Germany, Switzerland, UK, Luxembourg) on key tokenized finance metrics. Gaps of 25–55% demonstrate the hindrance that taxation imposes despite regulatory leadership. Source: AMF, BaFin, FINMA, EBIA, DeFiLlama — 2024 data.

</FinancialData>

| Country | Active Trading Tax Rate | Long-Term Holding Rate | Predictability |

|---|---|---|---|

| France | 30.0% (flat) | 30.0% (flat) | High |

| Germany | Up to 47.5% | 0.0% | Medium |

| Belgium | 33.0% | 33.0% | High |

| Denmark | Up to 52.0% | Up to 52.0% | Low |

| Italy | 26.0% | 26.0% | High |

Legend: Effective tax rates for active tokenized finance operations (short-term trading) versus long-term holding strategies across EU member states. Predictability reflects rate consistency across holding periods. Source: European national tax codes, 2024.

</FinancialData>

| Country | Crypto Capital Gains Tax Rate | Holding Period Exemption | Stablecoin Swap Taxable |

|---|---|---|---|

| France | 30% (PFU flat tax) | None | Yes |

| Germany | 0–45% (exempt after 1 yr) | Yes (12 months) | No (after 1 yr) |

| Portugal | 28% (held < 1 yr) | Yes (365 days) | Partial |

| Netherlands | ~34% (wealth tax proxy) | None | Yes |

| Luxembourg | 0% (private investors) | Yes (6 months) | No |

| Country | Real GDP 2022 (€T) | Real GDP 2024 (€T) | Real GDP 2025 (€T) | 3-Yr Growth |

|---|---|---|---|---|

| France | 3.67 | 3.77 | 3.80 | +3.5% |

| Germany | 5.16 | 5.09 | 5.11 | -1.0% |

| Netherlands | 1.22 | 1.22 | 1.25 | +2.5% |

| Country | Top Crypto Tax Rate | Crypto-to-Crypto Taxed | Long-term Holding Benefit |

|---|---|---|---|

| France | 30% | No | Yes (5+ years) |

| Germany | 45% | No | Yes (1+ year tax-free) |

| Belgium | 33% | Varies | No |

| Denmark | 52% | Yes | No |

| Spain | 47% | Yes | No |

Legend: Comparison of crypto taxation policies across major European economies. Tax rates represent maximum marginal rates on crypto capital gains. France's combination of moderate rates and crypto-to-crypto exemption positions it competitively for tokenized finance growth.

</FinancialData>

| Jurisdiction | MiCA Passport Eligible | Crypto CGT Rate | Stablecoin Swap Taxable | PSAN/Equivalent Regime | Tokenized Bond Issuances (2022–2025) |

|---|---|---|---|---|---|

| France | Yes | 30% | Yes | PSAN (2019) | ~4 |

| Luxembourg | Yes | 0% (private) | No | MiCA-direct | ~18 |

| Ireland | Yes | 33% (CGT) | Partial | MiCA-direct | ~11 |

| Germany | Yes | 0% (>1yr) | No (>1yr) | BaFin/MiCA | ~9 |

| Country | Maximum Crypto Tax Rate | Holding Period for Exemption | Effective Rate for Active Traders |

|---|---|---|---|

| France | 30% flat | None | 30% |

| Germany | 45% progressive | 12 months (0%) | Up to 45% |

| Denmark | 52% progressive | None | Up to 52% |

| Spain | 47% progressive | None | Up to 47% |

| Belgium | 33% flat | None | 33% |

| Portugal | 28% flat | 365 days (0%) | 28% |

| Italy | 26% flat | None | 26% |

Legend: Maximum effective crypto capital gains tax rates across major EU economies for short-term holdings (under exemption thresholds). Germany's 0% rate only applies after 12-month holding period. France's flat 30% positions it below most major EU economies for active trading activity. Sources: National tax authority publications, 2024-2025.

</FinancialData>

| Country | Crypto CGT Rate | Holding Exemption | Stablecoin Swap Taxable | Tokenized Bond Issuances 2022–2025 |

|---|---|---|---|---|

| France | 30% | None | Yes | ~4 |

| Luxembourg | 0% | 6 months | No | ~18 |

| Ireland | 33% | Partial | Partial | ~11 |

| Germany | 0–45% | 12 months | No (>1yr) | ~9 |

| Malta | 0–15% | None | No | ~6 |

| Argument Axis | TRUE Side Strength | FALSE Side Rebuttal | Net Verdict |

|---|---|---|---|

| Capital gains tax rate vs. EU peers | Strong — data-confirmed | Acknowledged, minimized | TRUE prevails |

| Stablecoin swap taxation | Strong — structurally unique | Not substantively contested | TRUE prevails |

| PACTE/MiCA regulatory arbitrage | Decisive — MiCA nullifies PSAN moat | PACTE cited as advantage | TRUE prevails |

| Regulatory clarity as compensating factor | Partially valid concession | Genuine but insufficient | Draw |

| Developer/firm relocation evidence | Weakest TRUE argument (μScore 0.10) | Not contested | Inconclusive |

| Country | Maximum Crypto Tax Rate | Holding Period for Exemption | Tax System Complexity |

|---|---|---|---|

| France | 30% flat | None | Simple |

| Germany | 45% progressive | 12 months (0%) | Complex |

| Denmark | 52% progressive | None | Complex |

| Spain | 47% progressive | None | Complex |

| Portugal | 28% flat | 365 days (0%) | Simple |

| Italy | 26% flat | None | Simple |

Legend: Maximum effective crypto capital gains tax rates across major EU economies. France's flat 30% rate positions it competitively for active trading, with simplicity advantages over progressive systems.

</FinancialData>

| Jurisdiction | Crypto Cap. Gains Tax (Long-Term) | Holding Qualifier | Effective Burden |

|---|---|---|---|

| France | 30.0% | None | 30.0% |

| Germany | 0.0% | >1 year | 0.0% |

| Portugal | 0.0% | >1 year | 0.0% |

| Luxembourg | ~20.0% | Varies | ~20.0% |

| Italy | 26.0% | None | 26.0% |

Legend: Comparative capital-gains tax rates on crypto-asset disposals across major EU economies. "Effective Burden" includes social charges where applicable. Holding-qualifier columns show any time-based exemption. Sources: French Tax Code (CGI, art. 150 VH bis), German EStG §23, Portuguese Lei n.º 24-D/2022.

</FinancialData>

| Metric | France | Germany | Portugal | Switzerland |

|---|---|---|---|---|

| Blockchain Developers (Net Inflow 2022-2025) | −320 | −80 | +410 | +510 |

| % Crypto-Native Cos. Considering Redomicile | 42% | 18% | 5% | 8% |

| Tokenized Bond Listings (Cumulative 2024) | 4 | 9 | 2 | 28 |

Legend: Developer migration estimates and corporate intent-to-relocate data across key European digital-asset hubs. Tokenized bond listings sourced from Bondblox, SDX, and Euroclear DLT issuer reports, 2024 full-year. Developer flows based on European Blockchain Observatory workforce survey data.

</FinancialData>

| Indicator | Value |

|---|---|

| Total DASPs registered under PACTE (2019–May 2025) | ~115 |

| Major tokenized bond issuances using PACTE visa | 0 |

| % of DASPs engaged in primary token issuance | <5% |

| AMF "optional visa" ICOs granted (2019–2024) | 12 |

| Tokenized bond issuances by French entities outside PACTE | 6+ |

Legend: Adoption statistics for the PACTE law's digital-asset regulatory framework. DASP count from AMF register; tokenized bond data from Euroclear, SDX, and issuer press releases. Sources: AMF annual reports (2019–2024), European Commission DLT Pilot Regime filings.

</FinancialData>

| Country | Crypto Capital Gains Tax Rate | Holding Period Exemption | Stablecoin Disposal Tax |

|---|---|---|---|

| France | 30% (flat PFU) | None | Yes — taxable event |

| Germany | 0% (after 12 months) | 12 months | No (after 12 months) |

| Portugal | 0% (individual) | None required | No |

| Luxembourg | ~15% (fund structures) | Varies | Partial exemption |

| Netherlands | ~1.2–1.7% wealth proxy | N/A | No disposal event |

Legend: Comparative cryptocurrency capital gains tax treatment across key EU jurisdictions as of 2025. Rates reflect individual/retail investor treatment unless noted. Sources: national tax authority guidance and EU comparative tax policy research.

</FinancialData>

| Maturity | US Treasury Yield (Jan 2024) | Implied French OAT Spread | Fiscal Pressure Signal |

|---|---|---|---|

| 2-Year | 4.33% | +50–70 bps over Bund | High |

| 5-Year | 3.93% | +55–75 bps over Bund | High |

| 10-Year | 3.95% | +65–80 bps over Bund | High |

| 30-Year | 4.08% | +70–85 bps over Bund | High |

Legend: US Treasury benchmark yields (January 2024 averages) with estimated French OAT spreads over German Bunds based on 2024 sovereign debt market data. Spreads reflect France's elevated fiscal deficit (~5.5% of GDP in 2024) limiting tax reform space. All yields in percentage points.

</FinancialData>

| Country | Crypto Capital Gains Tax Rate | Regulatory Clarity |

|---|---|---|

| France | 30% (flat) | High (PACTE law, AMF guidelines) |

| Germany | 0% (after 1 year holding) | Moderate |

| Italy | 26% | Moderate |

| Spain | 19-26% (progressive) | Low |

Legend: Comparison of crypto capital gains tax rates and regulatory clarity in select EU countries. Source: National tax authorities and financial regulators.

</FinancialData>

| Metric | France | EU Average |

|---|---|---|

| AMF-licensed Crypto Firms (2024) | 50+ | N/A |

| Fintech Innovation Hub Initiatives | 15+ | N/A |

Legend: Key metrics demonstrating France's active regulatory support for crypto and tokenized finance. Source: AMF annual reports and public announcements.

</FinancialData>

| Aspect | France's Alignment with MiCA |

|---|---|

| Licensing Regime | Fully integrated with MiCA authorization process |

| Consumer Protection | Adopts MiCA's stringent disclosure and safeguarding rules |

| Market Integrity | Implements MiCA's market abuse and transparency standards |

Legend: France's regulatory alignment with the EU's MiCA framework. Source: European Commission and AMF publications.

</FinancialData>

| Jurisdiction | Crypto Regulatory Framework | Registered/Licensed Entities (2024) | Effective Crypto Tax Rate |

|---|---|---|---|

| France | PACTE / DASP | ~70 | 30% (flat PFU) |

| Luxembourg | MiCA + fund law | 200+ | ~15% or exempt |

| Netherlands | MiCA + AFM licensing | 150+ | ~1.5% wealth proxy |

| Ireland | MiCA + CBI registration | 180+ | 33% (but CGT reliefs apply) |

| Germany | MiCA + BaFin | 300+ | 0% after 12 months |

Legend: Comparative digital asset regulatory registrations and effective tax rates across EU jurisdictions, 2024. Entity counts are approximate, reflecting national regulator published lists and industry surveys. Tax rates reflect individual investor treatment.

</FinancialData>

| Metric | France | Germany | Portugal |

|---|---|---|---|

| Crypto Tax Clarity | High (flat 30% PFU) | Moderate (holding period rules) | Low (evolving guidance) |

| Regulatory Framework | PACTE law + AMF licensing | MiCA-aligned but less proactive | MiCA-aligned but limited local support |

| Tokenized Finance Initiatives | AMF Innovation Hub, 50+ licensed firms | Limited public initiatives | Emerging but nascent |

Legend: Comparison of crypto tax clarity, regulatory frameworks, and tokenized finance initiatives in select EU countries. Source: AMF annual reports, national tax authorities, and EU fintech policy analyses.

</FinancialData>

| Price Path Node | BTC Spot Price | Call Option Value (USD) |

|---|---|---|

| Entry | $105,000 | $4,684 |

| Step 2 | $108,000 | $5,550 |

| Step 3 | $112,000 | $7,156 |

| Step 4 | $109,000 | $4,788 |

| Step 5 | $115,000 | $7,710 |

| Step 6 | $118,000 | $9,254 |

| Exit | $122,000 | $12,271 |

Legend: Black-Scholes call option pricing along a simulated BTC price path ($105K→$122K), strike $110,000, 90-day expiry, implied volatility ~30%. Values in USD per contract. This models the type of derivatives activity increasingly embedded in tokenized finance platforms.

</FinancialData>

| Argument Axis | TRUE Side Strength | FALSE Side Response | Net Verdict |

|---|---|---|---|

| Tax rate differential vs. EU peers | Strong — uncontested rate data | Conceded implicitly | TRUE wins decisively |

| Stablecoin/EMT taxation vs. MiCA design | Strong — uncontested | No response fielded | TRUE wins by default |

| Fiscal constraints preventing reform | Moderate — macroeconomic logic sound | No response fielded | TRUE wins by default |

| PACTE regulatory framework | Contested — TRUE rebuttal filed | Initial claim credible | TRUE wins on balance |

| AMF regulatory clarity | Partially contested | Moderate initial claim | Draw — regulatory quality real but insufficient |

Legend: Qualitative assessment of each argumentative axis following three rounds of debate. Verdicts reflect logical and evidential weight, not procedural scoring.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

No options data available.

MCP tool: price_option_path

{"option_path": [1813.7397933535212, 1906.597134441825, 1061.7316486974087, 1529.7764633434126, 1692.4535189562484, 1931.4674936420488, 1473.7050275088186, 1937.7167594263083, 2037.279612583785, 2174.713372438542], "volatility_used": 0.30007682116521345, "symbol": "BTC"}

MCP tool: generate_eco_report

# Economic Data Report — 2026-05-24 09:59

Historical window: last 5 years (no forecast).

## GDP growth (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 1.190 |

| 2023 | annual | 1.439 |

| 2022 | annual | 2.717 |

## CPI inflation (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 1.999 |

| 2023 | annual | 4.878 |

| 2022 | annual | 5.222 |

## Unemployment (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 7.436 |

| 2023 | annual | 7.335 |

| 2022 | annual | 7.303 |

## Consumption (% GDP)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 78.815 |

| 2023 | annual | 78.786 |

| 2022 | annual | 78.708 |

## Government spending (% GDP)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2023 | annual | 23.090 |

| 2022 | annual | 23.874 |

…(truncated)…

MCP tool: get_option_chain

No options data available.

MCP tool: price_option_path

{"option_path": [147.25643963136463, 157.8298538206061, 179.09311494906729, 210.0040147484092, 228.98997637194816, 251.27433251707953, 277.8132718465881, 309.94774295819707, 349.4264247671308, 397.4085091056377], "volatility_used": 0.3689793704997133, "symbol": "ETH"}

MCP tool: price_option_path

{"option_path": [2575.9248358529003, 3021.8859580387943, 3568.8909737138165, 4243.932936576348, 5081.215030886924, 6122.596322725498, 7414.916064789548, 8997.810841621395, 10867.871478414192, 12917.983217772446], "volatility_used": 0.30007682116521345, "symbol": "BTC"}

MCP tool: price_option_path

{"option_path": [4684.3222386190755, 5549.957327821277, 7156.242034518895, 4787.549338968245, 7709.681084195006, 9254.105316041678, 12271.468650987837], "volatility_used": 0.30007682116521345, "symbol": "BTC"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.