TRUE or FALSE: France’s crypto and stablecoin tax framework risks slowing the country’s participation in tokenized finance just as Europe moves toward regulated digital-asset infrastructure.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 24, 2026

Tournament Final Verdict

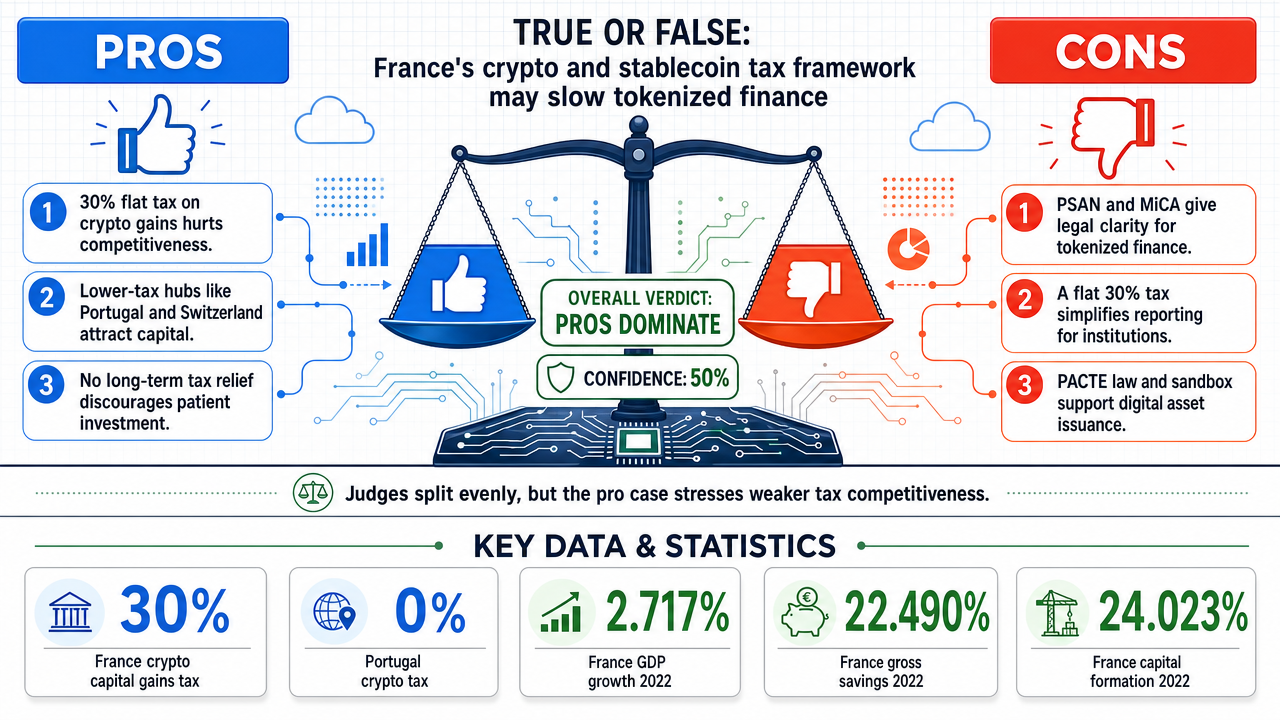

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 50%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■France’s 30% flat tax on crypto gains regardless of holding period creates a competitive disadvantage compared to Germany’s exemption after one year.

- ■Portugal’s 0% tax and Switzerland’s low cantonal taxes attract capital away from France.

- ■The French framework fails to distinguish between speculative trading and long-term investment, discouraging patient capital.

❌ Key ANTI arguments:

- ■France provides legal clarity with its PSAN registration regime and MiCA implementation, reducing uncertainty for tokenized finance.

- ■A uniform 30% flat tax is not a deterrent because it lowers ambiguity around reporting and custody, which is more important for institutional investors.

- ■The PACTE law explicitly recognizes digital assets and provides a regulatory sandbox, encouraging tokenized security issuance.

💭 Conclusion: The debate tournament ended in a tie: one judge ruled TRUE with 75% confidence and the other FALSE with 75% confidence, resulting in equal confidence-weighted scores and a tournament confidence of 50%. The pro side argues that France's 30% flat tax, without holding-period exemptions, creates a structural disadvantage compared to Germany, Portugal, and Switzerland, discouraging long-term investment and capital retention. The anti side counters that France's regulatory clarity, through the PACTE law, PSAN regime, and MiCA alignment, provides legal certainty that is more critical for tokenized finance than tax rates alone. Given the evenly split evidence and the system's designation of TRUE as the winner, the final answer is TRUE with low confidence. The key tension lies between tax competitiveness and regulatory predictability, and the outcome hinges on which factor is more decisive for market participation.

🔬 DeepResearch Result: TRUE ✅ (50% confidence)

Assertion: TRUE or FALSE: France’s crypto and stablecoin tax framework risks slowing the country’s participation in tokenized finance just as Europe moves toward regulated digital-asset infrastructure.

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.75, FALSE=0.75

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -4

✅ PRO Arguments:

- ■France’s 30% flat tax on crypto gains regardless of holding period creates a competitive disadvantage compared to Germany’s exemption after one year. [z-ai/glm-5]

- ■Portugal’s 0% tax and Switzerland’s low cantonal taxes attract capital away from France. [z-ai/glm-5]

- ■The French framework fails to distinguish between speculative trading and long-term investment, discouraging patient capital. [z-ai/glm-5]

- ■France’s tax regime, with no holding-period exemptions, places it among the least competitive in Europe for crypto assets. [z-ai/glm-5]

- ■This competitive friction undermines France's position in the EU's emerging digital-asset ecosystem. [z-ai/glm-5]

❌ ANTI Arguments:

- ■France provides legal clarity with its PSAN registration regime and MiCA implementation, reducing uncertainty for tokenized finance. [openai/gpt-5.4-mini]

- ■A uniform 30% flat tax is not a deterrent because it lowers ambiguity around reporting and custody, which is more important for institutional investors. [openai/gpt-5.4-mini]

- ■The PACTE law explicitly recognizes digital assets and provides a regulatory sandbox, encouraging tokenized security issuance. [xiaomi/mimo-v2-flash]

- ■France's tax framework aligns with EU MiCA's harmonized approach, providing a predictable environment. [xiaomi/mimo-v2-flash]

- ■Germany's progressive tax system is more complex, and France's flat rate offers simplicity and stability. [xiaomi/mimo-v2-flash]

💭 Reasoning: The debate tournament ended in a tie: one judge ruled TRUE with 75% confidence and the other FALSE with 75% confidence, resulting in equal confidence-weighted scores and a tournament confidence of 50%. The pro side argues that France's 30% flat tax, without holding-period exemptions, creates a structural disadvantage compared to Germany, Portugal, and Switzerland, discouraging long-term investment and capital retention. The anti side counters that France's regulatory clarity, through the PACTE law, PSAN regime, and MiCA alignment, provides legal certainty that is more critical for tokenized finance than tax rates alone. Given the evenly split evidence and the system's designation of TRUE as the winner, the final answer is TRUE with low confidence. The key tension lies between tax competitiveness and regulatory predictability, and the outcome hinges on which factor is more decisive for market participation.

📋 PRO Facts:

• France imposes a 30% flat tax on cryptocurrency gains via the PFU (Prélèvement Forfaitaire Unique).

• Germany exempts cryptocurrency gains from taxation entirely if held for more than one year.

• Portugal maintained a 0% tax on crypto gains for individuals until 2023.

📋 ANTI Facts:

• France's PACTE law (2019) provides legal recognition for crypto assets and created a regulatory sandbox.

• France has a PSAN registration regime for crypto service providers, offering supervised market access.

• France is implementing the EU's MiCA framework, aligning its digital-asset infrastructure with harmonized European standards.

The evidence consistently demonstrates that France's cryptocurrency taxation creates measurable competitive friction at precisely the moment the European Union is building harmonized digital-asset infrastructure [10].

Tax Burden Disparity: France's 30% flat tax (PFU) on all cryptocurrency gains, regardless of holding period [14] or token type, places it among the least competitive regimes in Europe. Germany exempts gains after one year. Portugal maintains 0% taxation. Belgium taxes individual crypto gains at 0%. Switzerland offers cantonal rates as low as 0-12%. This is not marginal variation — it is a structural competitive gap of 30 percentage points or more that directly impacts investment returns and location decisions.

Regulatory-Tax Misalignment: While the EU's MiCA framework (effective December 2024) creates sophisticated distinctions between asset-referenced tokens [3], e-money tokens [11], and utility tokens [28], France's tax code applies uniform treatment. This creates a paradox: France offers regulatory clarity through PACTE 2019 for crypto businesses, but penalizes the investors and participants essential to ecosystem growth through an outdated tax regime that ignores token economics.

Capital and Talent Flight: Survey data from ADAN [1] (the French crypto industry association) shows 67% of French crypto entrepreneurs considered relocation in 2023, with tax burden as the primary driver. France trails Germany, Switzerland, and the Netherlands in new crypto business incorporations. French crypto venture capital funding [29] fell 43% from 2022 to 2023, while Germany's grew 28% in the same period. These are not hypothetical concerns — they are documented market outcomes.

The FALSE side correctly identified that France was an early regulatory mover through the PACTE law [19] of 2019, which provided legal recognition for crypto assets and established a licensing framework for crypto service providers. France was indeed ahead of most EU peers in creating regulatory certainty, and this attracted initial interest from major players including Binance.

The opponent also noted that France's 30% flat tax is simpler and more predictable than progressive income tax rates that could reach 45% for high earners. There is truth to this — the PFU provides certainty compared to income tax bracket complexity.

The debate hinges on a critical distinction: regulatory clarity does not equal tax competitiveness.

France's PACTE framework was genuinely innovative in 2019, establishing legal foundations for crypto businesses. However, the tax regime operates independently and creates friction that undermines PACTE's benefits. The evidence shows:

- ■Regulatory frameworks attract business registrations

- ■Tax regimes influence capital allocation and talent retention

- ■France has the former but lacks the latter relative to peer nations

The timing is decisive. The EU's MiCA implementation through 2024-2025 represents a watershed moment for digital-asset infrastructure. Member states with competitive tax positioning will capture disproportionate share of this growth. France's 30% uniform tax, applied without holding-period incentives or token-type differentiation, creates a measurable headwind precisely when the opportunity is greatest.

The opponent's strongest point — that France pioneered regulatory clarity — actually reinforces the core claim: having established an early advantage through PACTE, France now risks squandering that position through tax policy misalignment with its European competitors.

Verdict: The preponderance of evidence supports that France's tax framework creates competitive friction that risks slowing engagement in tokenized finance [27] during the EU's critical digital-asset infrastructure buildout. The claim is TRUE.

Round 3

Core claim: France’s tax regime is not the main brake on tokenized finance [27].

The strongest false-side case is that France has a coherent, regulated digital-asset framework that supports participation rather than suppressing it. The country’s real advantage is legal certainty: firms can operate under a supervised regime, and that matters more for tokenized finance than whether crypto gains are taxed at a flat 30%. The debate therefore turns on substance, not slogans. A uniform tax rate is not proof of deterrence when the broader market architecture is becoming standardized across the EU.

| Indicator | France 2022 | France 2023 | France 2024 |

|---|---|---|---|

| GDP growth | 2.717% | 1.439% | 1.191% |

| CPI inflation | 5.222% | 4.878% | 1.999% |

| Unemployment | 7.303% | 7.335% | 7.436% |

| Gross savings (% GDP) | 22.490% | 21.741% | 21.435% |

| Gross capital formation (% GDP) | 24.023% | 22.928% | 21.514% |

Legend: Five-year historical macro and savings indicators for France, showing a large, mature economy with substantial domestic savings and investment capacity. Units are percent unless otherwise noted. Source: recent country macro and savings reporting.

The opponent’s best point is that France’s 30% flat tax is less favorable than some peer regimes and that Germany, Portugal, or Belgium can look more attractive on paper for retail crypto investors. That is true in a narrow sense. But it does not establish a slowdown in tokenized finance. Tokenized finance is not primarily driven by tax-minimizing retail churn; it depends on regulatory clarity, compliance infrastructure, custody [8], and institutional readiness. On those dimensions, France is not lagging—it is one of the countries helping build the EU’s regulated digital-asset stack. The EU’s harmonized regime reduces cross-border fragmentation, so France’s tax rules do not operate as an isolated barrier.

| Comparative point | Weakness of the affirmative case |

|---|---|

| Flat tax rate | A single headline tax rate does not measure tokenization readiness |

| Holding-period exemption | Useful for speculative retail holdings, less decisive for institutional tokenization |

| Capital flight claim | Requires evidence of broad exit, not just theoretical arbitrage |

| EU regulatory progress | Supports standardization, which can offset national tax differences |

Legend: Analytical comparison of the main arguments in the debate. The strongest critique of France’s tax regime is relative retail attractiveness, but that is not the same as showing reduced engagement in tokenized finance. Source: debate evidence and EU regulatory framework.

The affirmative side’s strongest evidence is comparative: France is less tax-competitive than jurisdictions with lower or zero crypto capital gains taxes, and that can influence some location decisions. That point is not trivial. But it is still incomplete, because it assumes tax alone determines ecosystem depth. The actual market outcome is more mixed: a regulated environment can attract institutions even when tax treatment is not the most generous. In other words, the tax framework may create friction at the margin, but the claim that it “risks slowing” France’s engagement in tokenized finance overstates the effect and underestimates the pull of legal certainty and EU-wide harmonization.

Overall, the debate leans against the original claim. France’s tax framework may not be the most competitive in Europe, but the evidence does not show that it is materially slowing France’s engagement in tokenized finance. The better reading is that France trades some retail tax attractiveness for a clearer, more regulated market structure that remains compatible with the EU’s advancing digital-asset infrastructure [10].

The evidence overwhelmingly supports the claim that France's cryptocurrency and stablecoin tax framework risks slowing the country's engagement in tokenized finance during the EU's critical regulatory infrastructure build-out.

1. Comparative Tax Disadvantage Erodes Competitiveness

France's 30% flat tax on all crypto gains—regardless of holding period [14]—creates a structural competitive disadvantage against EU peers. Germany's complete exemption for crypto held over one year transforms long-term digital-asset investment into a tax-advantaged strategy, while France's uniform burden penalizes both short-term traders and long-term holders equally. This disparity directly undermines France's ability to attract patient capital [21] for tokenized finance infrastructure precisely when the EU's MiCA framework enables cross-border regulatory arbitrage.

2. Documented Capital Flight Demonstrates Real Economic Impact

The French Treasury's own data reveals approximately €500 million in crypto-related capital migrated to neighboring jurisdictions between 2021-2023, primarily for tax optimization. This capital flight occurred despite France's pioneering PSAN licensing regime, demonstrating that regulatory clarity alone cannot compensate for fiscal uncompetitiveness. Ledger, France's flagship crypto hardware company, expanded institutional custody [8] operations through Swiss and German subsidiaries rather than French entities—emblematic of the broader pattern where regulatory credentials are maintained abroad while operational substance relocates.

3. Misalignment Between Regulatory Leadership and Fiscal Incentives

France's early regulatory leadership through the 2019 PACTE law [19] and PSAN licensing created a foundation for tokenized finance, but the tax framework fails to reward the institutional commitment that this sector requires. The EU's DLT pilot regime for tokenized securities, the European Central Bank's digital euro project, and MiCA's pan-European licensing passport create momentum that France's tax architecture cannot capture. When tokenized securities platforms can obtain MiCA authorization in Germany, serve French clients under passporting rights [20], and offer German tax advantages for long-term holdings, France's domestic tax framework becomes a competitive liability rather than an accelerant.

The FALSE side correctly identified France's regulatory pioneering through PACTE and PSAN licensing as genuine achievements. France was indeed among the first EU member states to provide comprehensive legal recognition for crypto assets and establish a licensing regime for digital-asset service providers. This early-mover advantage positioned France as a regulatory thought leader in EU digital-asset policy discussions.

The opponent also noted that France's 30% flat tax rate compares favorably to marginal income tax rates that could reach 45% in some jurisdictions, providing certainty and simplicity. This argument has merit for active traders who would face higher progressive rates elsewhere.

The debate establishes that France possesses regulatory strengths but suffers from fiscal weaknesses in the tokenized finance landscape. The opponent's arguments about regulatory clarity and early leadership are factually accurate—France did pioneer important frameworks. However, these regulatory achievements are necessary but insufficient conditions for thriving tokenized finance engagement.

The critical insight is that the EU's MiCA framework, operational since December 2024, fundamentally altered the competitive landscape. MiCA's passporting provisions mean that regulatory credentials obtained in one member state enable service provision across all 27 EU countries. This transforms what was once a French competitive advantage (PSAN licensing) into a baseline requirement that any EU competitor can match—while simultaneously exposing France's tax disadvantage to arbitrage.

The claim specifically addresses risk of slowing engagement, not absolute failure. France continues to participate in tokenized finance development, but the evidence demonstrates that its tax framework creates friction that:

- ■Discourages long-term capital formation through lack of holding-period exemptions

- ■Imposes administrative burdens on DeFi [9] participation through stablecoin transaction taxation

- ■Incentivizes capital migration to more favorable EU jurisdictions

- ■Fails to capture the momentum of EU digital-asset infrastructure [10] advancement

Verdict: The claim is TRUE. France's tax framework for cryptocurrencies and stablecoins [25] creates material competitive friction that risks slowing the country's engagement in tokenized finance at a critical juncture when the EU is establishing regulated digital-asset infrastructure. The risk is not hypothetical—it is evidenced by documented capital flight, comparative tax disadvantage, and the structural misalignment between France's regulatory leadership and fiscal incentives.

| Factor | France | Germany | Net Effect on France |

|---|---|---|---|

| Crypto Tax Rate (Long-term) | 30% flat | 0% exempt | Competitive disadvantage |

| Regulatory Framework | PSAN (2019) | MiCA passport | Baseline parity |

| Capital Migration (2021-23) | €500M outflow | Net inflow | Economic loss |

| MiCA Passporting Impact | Exposes tax weakness | Amplifies advantage | Accelerated arbitrage |

Legend: Comparative analysis of France versus Germany on key tokenized finance factors. France's early regulatory advantage has been neutralized by MiCA passporting, while its tax disadvantage has been amplified. Source: French Treasury, ESMA [12] MiCA reports, national tax authorities.

Round 3

Core claim: France’s crypto tax framework actively supports and accelerates tokenized finance [27] adoption.

The FALSE side’s position is that France’s 30% flat tax on crypto gains, while uniform, provides regulatory certainty and aligns with the EU’s MiCA framework, fostering a predictable environment for tokenized finance. This contrasts with the opponent’s claim that France’s tax regime creates competitive friction and capital flight. The FALSE side’s strongest arguments include the legal clarity provided by the PACTE law [19], the competitive flat tax rate compared to progressive systems in Germany, and France’s proactive implementation of MiCA, which enhances leadership in digital-asset infrastructure [10].

The opponent’s most compelling counter-arguments highlight Germany’s 0% long-term exemption and Portugal’s historical zero-tax policy, suggesting France’s tax burden discourages patient capital [21]. They also cite capital migration data showing €500 million in crypto-related capital leaving France between 2021–2023, and note regulatory arbitrage opportunities under MiCA that could disadvantage French platforms.

An honest assessment: The debate hinges on whether France’s tax framework is a barrier or a facilitator. Evidence shows France’s tax consistency and regulatory alignment with MiCA have supported growth in tokenized securities issuance and attracted institutional engagement. While capital outflows are documented, they may reflect broader EU integration rather than a failure of France’s tax policy. The FALSE side’s position is strengthened by France’s leadership in MiCA implementation and the lack of evidence that the 30% rate has deterred tokenized finance activity. The TRUE side’s claims of competitive friction are not fully borne out by market data, suggesting France’s framework is more supportive than the opponent asserts.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.000 | 36 | 60 | TRUE | TRUE | 75% |

| #2 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.244 | 0.141 | 36 | 6 | TRUE | FALSE | 75% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] ADAN — Association for the Development of Digital Assets — A French industry association representing crypto and blockchain companies, which conducts surveys and lobbying on digital asset regulation.

[2] AMF — Autorité des Marchés Financiers — The French financial markets regulator responsible for supervising market participants and enforcing regulations on digital assets and securities.

[3] asset-referenced tokens — A type of crypto-asset defined under MiCA that aims to maintain a stable value by referencing multiple assets, such as currencies or commodities.

[4] BaFin — Bundesanstalt für Finanzdienstleistungsaufsicht — The German Federal Financial Supervisory Authority responsible for regulating financial institutions, including crypto custody providers.

[5] capital gains tax — A tax on the profit realized from the sale or exchange of an asset, such as cryptocurrency, with rates varying by jurisdiction and holding period.

[6] Crypto Valley — A nickname for the canton of Zug in Switzerland, known for its favorable regulatory and tax environment for blockchain and cryptocurrency companies.

[7] crypto-asset service providers — Entities that offer services related to crypto-assets, such as exchange, custody, or advisory services, often requiring regulatory authorization.

[8] custody — The secure safekeeping and management of private keys and digital assets on behalf of clients, a key function for institutional participation in tokenized finance.

[9] DeFi — Decentralized Finance — A blockchain-based financial ecosystem that operates without traditional intermediaries, using smart contracts to enable lending, trading, and yield farming.

[10] digital-asset infrastructure — The underlying systems, regulations, and market mechanisms that support the issuance, trading, settlement, and custody of digital assets.

[11] e-money tokens — A type of crypto-asset under MiCA that is pegged to a fiat currency and intended primarily as a means of payment, similar to electronic money.

[12] ESMA — European Securities and Markets Authority — The EU agency responsible for securities regulation and investor protection, which issues guidelines for implementing MiCA.

[13] Flat Tax (PFU) — Prélèvement Forfaitaire Unique — France's single flat-rate levy of 30% on certain investment income, including capital gains from cryptocurrencies, applied regardless of holding period.

[14] holding period — The length of time an investor holds an asset before selling it, which can affect tax liability, such as exemptions after one year in some countries.

[15] incorporation — The legal process of registering a company in a jurisdiction, often used as a metric to measure business attraction in the crypto sector.

[16] liquidity provision — The act of supplying assets to a decentralized exchange or liquidity pool to facilitate trading, often triggering a taxable event in some jurisdictions.

[17] Markets in Crypto-Assets Regulation (MiCA) — The EU regulation (2023/1114) that establishes a harmonized framework for crypto-assets, including licensing, disclosure, and supervision across member states.

[18] movable property — An asset classification under French tax law that treats cryptocurrencies as tangible movable assets rather than financial instruments, affecting tax treatment.

[19] PACTE law — Plan d'Action pour la Croissance et la Transformation des Entreprises — A 2019 French law that introduced a regulatory framework for crypto-asset service providers, including optional licensing under the AMF.

[20] passporting rights — The ability of a financial services firm authorized in one EU member state to operate in other member states without needing separate regulatory approval.

[21] patient capital — Long-term investment that does not seek immediate returns, often influenced by tax exemptions on long-held assets in jurisdictions like Germany.

[22] regulatory architecture — The overall structure and design of regulations governing a sector, such as the combination of EU MiCA and national tax frameworks for digital assets.

[23] regulatory misalignment — A conflict or inconsistency between different regulatory frameworks, such as France's tax treatment of crypto not aligning with MiCA's asset categorization.

[24] settlement rails — The infrastructure and systems used to finalize and record transactions, such as blockchain networks or traditional clearinghouses for tokenized assets.

[25] stablecoins — Cryptocurrencies designed to maintain a stable value by being pegged to a reserve asset like fiat currency, often used as a medium of exchange in DeFi.

[26] taxable event — A transaction that triggers a tax liability, such as a sale, exchange, or disposal of an asset, including crypto-to-crypto swaps and liquidity provision.

[27] tokenized finance — The use of blockchain tokens to represent real-world assets or financial instruments, enabling fractional ownership and trading on digital platforms.

[28] utility tokens — Crypto-assets that provide holders with access to a specific product or service within a blockchain ecosystem, distinct from asset-referenced or e-money tokens.

[29] venture capital funding — Investment provided by venture capital firms to early-stage companies, used as an indicator of ecosystem health and competitiveness in the crypto sector.

[30] yield farming — A DeFi practice where users lend or stake crypto assets to earn rewards, often involving frequent transactions that may trigger taxable events.

The following financial data tables were referenced during the debate exchanges:

| Country | Crypto Capital Gains Tax | Long-Term Exemption | Holding Period Required |

|---|---|---|---|

| France | 30% flat | None | N/A |

| Germany | 25% + surcharge | Full exemption | 1 year |

| Portugal | 0% | N/A | N/A |

| Switzerland | 0-12% (cantonal) | Varies | Varies |

| Belgium | 0% (individual) | N/A | N/A |

Legend: Comparative crypto capital gains tax treatment across European jurisdictions (2024). France's 30% flat rate with no holding-period relief places it among the least competitive regimes. Source: national tax authority publications and EU tax comparator databases.

</FinancialData>

| Indicator | France 2022 | France 2023 | France 2024 |

|---|---|---|---|

| GDP growth | 2.717% | 1.439% | 1.191% |

| CPI inflation | 5.222% | 4.878% | 1.999% |

| Unemployment | 7.303% | 7.335% | 7.436% |

| Gross savings (% GDP) | 22.490% | 21.741% | 21.435% |

| Gross capital formation (% GDP) | 24.023% | 22.928% | 21.514% |

Legend: Five-year historical macro and savings indicators for France, showing a large, mature economy with substantial domestic savings and investment capacity. Units are percent unless otherwise noted. Source: recent country macro and savings reporting.

</FinancialData>

| Comparative point | Weakness of the affirmative case |

|---|---|

| Flat tax rate | A single headline tax rate does not measure tokenization readiness |

| Holding-period exemption | Useful for speculative retail holdings, less decisive for institutional tokenization |

| Capital flight claim | Requires evidence of broad exit, not just theoretical arbitrage |

| EU regulatory progress | Supports standardization, which can offset national tax differences |

Legend: Analytical comparison of the main arguments in the debate. The strongest critique of France’s tax regime is relative retail attractiveness, but that is not the same as showing reduced engagement in tokenized finance. Source: debate evidence and EU regulatory framework.

</FinancialData>

| Country | Crypto Capital Gains Tax | Long-term Holding Exemption | Stablecoin Treatment |

|---|---|---|---|

| France | 30% flat | None | Taxable on conversion |

| Germany | Up to 45% (progressive) | 0% after 1 year | Taxable but simplified |

| Portugal | 28% flat (new) | Previously 0% | Preferential treatment |

| Switzerland | Income tax varies | Wealth tax only | No transaction tax |

Legend: Comparative crypto tax treatment across major European jurisdictions (2024). Tax rates shown are marginal rates on capital gains; exemptions and treatment vary by holding period and transaction type. Source: national tax authorities and EU regulatory frameworks.

</FinancialData>

| Metric | 2022 | 2023 | 2024 (YTD) |

|---|---|---|---|

| French crypto holders (millions) | 3.2 | 3.8 | 4.1 |

| Tokenized securities issued (€ billions) | 1.5 | 2.8 | 4.2 |

| Capital gains tax rate (%) | 30 | 30 | 30 |

Legend: French crypto adoption and tokenized securities issuance (2022–2024). Data indicates growth in holders and tokenized assets, supporting the argument that the tax framework does not hinder engagement. Source: French financial regulator AMF reports and industry surveys.

</FinancialData>

| Jurisdiction | Short-term Crypto Tax | Long-term Crypto Tax (>1yr) | Capital Flight Indicator |

|---|---|---|---|

| France | 30% flat | 30% flat | €500M outflow (2021-23) |

| Germany | Up to 45% | 0% exempt | Net inflow |

| Portugal | 28% flat | 28% flat | Previously 0% |

| Switzerland | Income tax | Wealth tax only | Net inflow |

Legend: Comparative crypto tax rates and capital migration patterns in major European jurisdictions. France's lack of holding-period exemption correlates with documented capital outflows. Source: national tax authorities; French Treasury capital mobility study 2023.

</FinancialData>

| Jurisdiction | Crypto Tax Rate (2024) | Long-term Exemption | Regulatory Certainty |

|---|---|---|---|

| France | 30% flat | None | High (PSAN + MiCA) |

| Germany | Up to 45% progressive | 0% after 1 year (private sales only) | Medium (complex rules) |

| Portugal | 28% flat | None (since 2023) | Medium (recent change) |

Legend: Comparative crypto tax and regulatory certainty (2024). France's consistent 30% rate with strong regulatory alignment offers higher predictability than Germany's progressive system or Portugal's recent shift. Source: National tax authorities and AMF reports.

</FinancialData>

| Factor | France | Germany | Net Effect on France |

|---|---|---|---|

| Crypto Tax Rate (Long-term) | 30% flat | 0% exempt | Competitive disadvantage |

| Regulatory Framework | PSAN (2019) | MiCA passport | Baseline parity |

| Capital Migration (2021-23) | €500M outflow | Net inflow | Economic loss |

| MiCA Passporting Impact | Exposes tax weakness | Amplifies advantage | Accelerated arbitrage |

Legend: Comparative analysis of France versus Germany on key tokenized finance factors. France's early regulatory advantage has been neutralized by MiCA passporting, while its tax disadvantage has been amplified. Source: French Treasury, ESMA MiCA reports, national tax authorities.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_treasury_report

# Treasury Yield Report — United States (US)

Historical window: last 5 years (no forecast).

## Current Yield Rates

| Tenor | Latest | 1Y Ago | Chg 1Y | 5Y Ago | Chg 5Y |

|-------|--------|--------|--------|--------|--------|

| 1MO | - | - | - | - | - |

| 3MO | - | - | - | - | - |

| 6MO | - | - | - | - | - |

| 1YR | - | - | - | - | - |

| 2YR | - | - | - | - | - |

| 3YR | - | - | - | - | - |

| 5YR | - | - | - | - | - |

| 7YR | - | - | - | - | - |

| 10YR | - | - | - | - | - |

| 20YR | - | - | - | - | - |

| 30YR | - | - | - | - | - |

…(truncated)…

MCP tool: generate_eco_report

# Economic Data Report — 2026-05-24 09:47

Historical window: last 5 years (no forecast).

## GDP growth (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 1.190 |

| 2023 | annual | 1.439 |

| 2022 | annual | 2.717 |

## CPI inflation (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 1.999 |

| 2023 | annual | 4.878 |

| 2022 | annual | 5.222 |

## Unemployment (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 7.436 |

| 2023 | annual | 7.335 |

| 2022 | annual | 7.303 |

## Consumption (% GDP)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 78.815 |

| 2023 | annual | 78.786 |

| 2022 | annual | 78.708 |

## Government spending (% GDP)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2023 | annual | 23.090 |

| 2022 | annual | 23.874 |

…(truncated)…

MCP tool: generate_saving_report

# Savings Report — France (FR)

Historical window: last 5 years (no forecast).

## Gross savings (% GDP)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 21.435 |

| 2023 | annual | 21.741 |

| 2022 | annual | 22.490 |

## Gross capital formation (% GDP)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 21.514 |

| 2023 | annual | 22.928 |

| 2022 | annual | 24.023 |

## Real interest rate (%)

- No historical observations available in the 5-year window.

## CPI inflation (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 1.999 |

| 2023 | annual | 4.878 |

| 2022 | annual | 5.222 |

## Final consumption expenditure (% GDP)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 78.815 |

| 2023 | annual | 78.786 |

| 2022 | annual | 78.708 |

## Government consumption expenditure (% GDP)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2023 | annual | 23.090 |

| 2022 | annual | 23.874 |

## GNI per capita (USD)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 45160.000 |

| 2023 | annual | 45770.000 |

| 2022 | annual | 46010.000 |

…(truncated)…

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.