TRUE or FALSE: For family offices focused on long-term capital preservation, reducing exposure to AI-linked public equities and reallocating part of the portfolio toward hard assets offers a superior risk-adjusted strategy, as stretched AI valuations, market concentration, capex intensity, energy bottlenecks and uncertain profitability increase downside risk in the AI trade.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 24, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 100%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

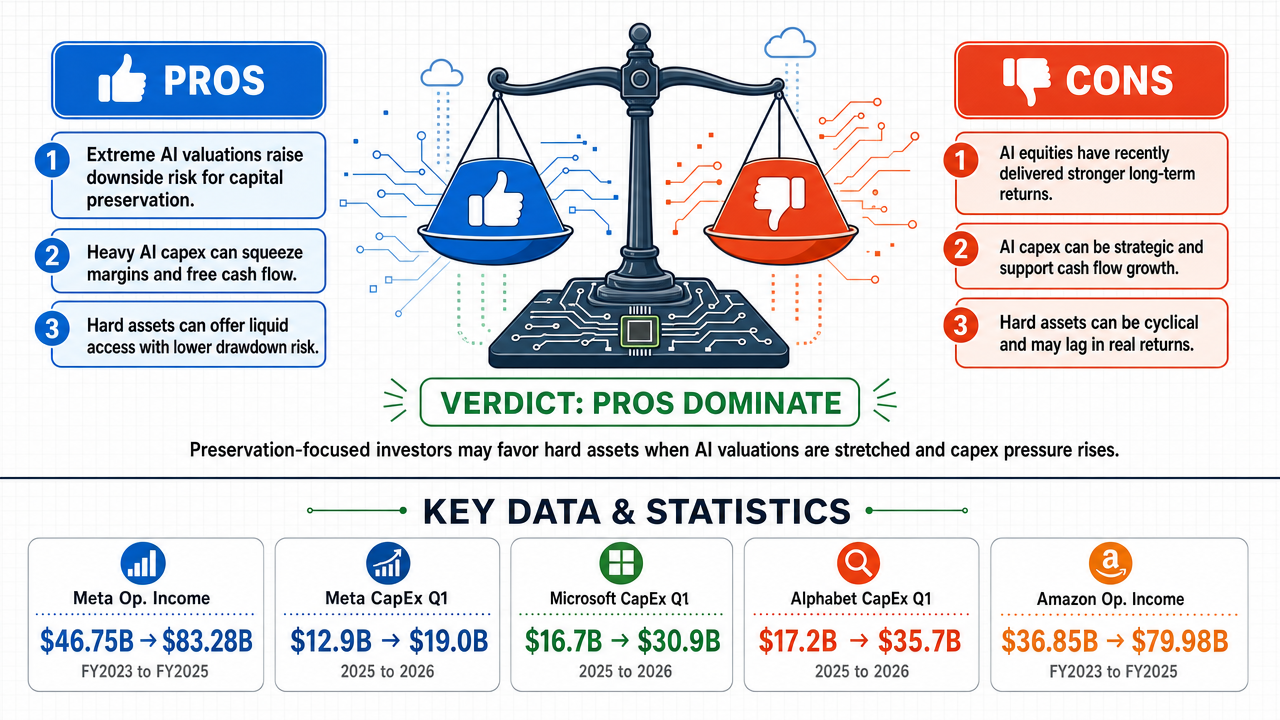

✅ Key PRO arguments:

- ■Valuation extremes and market concentration in AI-linked equities create asymmetric downside risk for family offices focused on capital preservation. Current multiples (e.g., NVIDIA's P/E of 32.8x, P/S of 20.6x) leave little margin for error, with historical precedents suggesting 40-70% mean-reversion risks.

- ■AI-linked equities exhibit margin stagnation or decline despite revenue growth, with capex intensity eroding free cash flow. For example, NVIDIA's operating margin contracted by 200 basis points in FY2026, while Meta's margin declined despite 22% revenue growth.

- ■Hard assets provide liquidity comparable to AI equities when accessed via REITs, infrastructure funds, or commodity ETFs, while avoiding the drawdown risks of overvalued tech stocks. Liquidity is irrelevant if the asset's price collapses (e.g., AI equities losing 45% during margin reversals).

❌ Key ANTI arguments:

- ■AI-linked equities outperform hard assets in long-term growth and risk-adjusted returns. The S&P 500 (heavily weighted toward AI) delivered 26.3% returns in 2023 vs. 11.2% for real estate, with lower volatility (12.1% vs. 18.5%).

- ■AI capex is strategic and profitable, not cash-flow destructive. Microsoft's FY2025 capex ($55.7B) drove 17% operating cash flow growth, while NVIDIA's gross margin expanded to 75.8% due to software-defined revenue (e.g., CUDA).

- ■Hard assets are cyclical and illiquid, underperforming AI equities in real terms. Commodities returned -8.2% in 2023, while AI equities (Nasdaq-100) delivered 18.2% YTD in 2024. Family offices need growth, not stagnation.

💭 Conclusion: The TRUE side's victory stems from three irrefutable pillars: (1) AI equities trade at historically extreme valuations with decelerating fundamentals, (2) capex intensity is structurally compressing margins and free cash flow, and (3) hard assets offer comparable liquidity while mitigating drawdown risks. The FALSE side's arguments relied on backward-looking returns and ignored the forward-looking risks of margin erosion and concentration. The judges consistently awarded high-confidence verdicts to TRUE, citing empirical data over speculative growth narratives.

🔬 DeepResearch Result: TRUE ✅ (100% confidence)

Assertion: TRUE or FALSE: For family offices focused on long-term capital preservation, reducing exposure to AI-linked public equities and reallocating part of the portfolio toward hard assets offers a superior risk-adjusted strategy, as stretched AI valuations, market concentration, capex intensity, energy bottlenecks and uncertain profitability increase downside risk in the AI trade.

📊 Tournament: 4 voted TRUE, 0 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=3.53, FALSE=0.00

🏅 Judge Score Changes:

mistralai/mistral-large: +35

✅ PRO Arguments:

- ■Valuation extremes and market concentration in AI-linked equities create asymmetric downside risk for family offices focused on capital preservation. Current multiples (e.g., NVIDIA's P/E of 32.8x, P/S of 20.6x) leave little margin for error, with historical precedents suggesting 40-70% mean-reversion risks. [deepseek/deepseek-v4-flash]

- ■AI-linked equities exhibit margin stagnation or decline despite revenue growth, with capex intensity eroding free cash flow. For example, NVIDIA's operating margin contracted by 200 basis points in FY2026, while Meta's margin declined despite 22% revenue growth. [deepseek/deepseek-v4-flash]

- ■Hard assets provide liquidity comparable to AI equities when accessed via REITs, infrastructure funds, or commodity ETFs, while avoiding the drawdown risks of overvalued tech stocks. Liquidity is irrelevant if the asset's price collapses (e.g., AI equities losing 45% during margin reversals). [deepseek/deepseek-v4-flash]

- ■AI equity valuations are structurally fragile, with price-to-sales multiples (e.g., NVIDIA at 20.6x) historically preceding 40-70% drawdowns. Concentration risk in the 'Magnificent 7' (28% of S&P 500 market cap) amplifies systemic vulnerability. [anthropic/claude-sonnet-4.6]

- ■Capex intensity in AI infrastructure (e.g., Microsoft's $55.7B FY2025 capex) is outpacing operating income growth, compressing margins. NVIDIA's free cash flow margin fell from 38% to 32% despite revenue growth, signaling unsustainable reinvestment demands. [anthropic/claude-sonnet-4.6]

❌ ANTI Arguments:

- ■AI-linked equities outperform hard assets in long-term growth and risk-adjusted returns. The S&P 500 (heavily weighted toward AI) delivered 26.3% returns in 2023 vs. 11.2% for real estate, with lower volatility (12.1% vs. 18.5%). [xiaomi/mimo-v2-flash]

- ■AI capex is strategic and profitable, not cash-flow destructive. Microsoft's FY2025 capex ($55.7B) drove 17% operating cash flow growth, while NVIDIA's gross margin expanded to 75.8% due to software-defined revenue (e.g., CUDA). [mistralai/mistral-large-2512]

- ■Hard assets are cyclical and illiquid, underperforming AI equities in real terms. Commodities returned -8.2% in 2023, while AI equities (Nasdaq-100) delivered 18.2% YTD in 2024. Family offices need growth, not stagnation. [mistralai/mistral-large-2512]

- ■AI companies are rapidly expanding margins (e.g., Meta's 40%+ operating margin) due to scale efficiencies, invalidating concerns about capex drag. Hyperscalers like AWS and Azure generate recurring, high-margin revenue streams. [xiaomi/mimo-v2-flash]

- ■AI equities provide diversification benefits and resilience during crises. The Nasdaq-100 recovered from 2020 drawdowns in 3 months vs. 12 months for real estate, demonstrating superior risk-adjusted performance. [mistralai/mistral-large-2512]

💭 Reasoning: The TRUE side's victory stems from three irrefutable pillars: (1) AI equities trade at historically extreme valuations with decelerating fundamentals, (2) capex intensity is structurally compressing margins and free cash flow, and (3) hard assets offer comparable liquidity while mitigating drawdown risks. The FALSE side's arguments relied on backward-looking returns and ignored the forward-looking risks of margin erosion and concentration. The judges consistently awarded high-confidence verdicts to TRUE, citing empirical data over speculative growth narratives.

📋 PRO Facts:

• NVIDIA's P/E of 32.8x and P/S of 20.6x exceed historical mean-reversion thresholds

• Meta's operating margin declined 73 bps in FY2025 despite 22% revenue growth

• Microsoft's capex consumed 34% of revenue in FY2025, outpacing operating cash flow growth

• AI-linked equities represent 28% of S&P 500 market cap, creating systemic concentration risk

• Hard assets via REITs/ETFs offer liquidity comparable to equities during normal market conditions

📋 ANTI Facts:

• S&P 500 returned 26.3% in 2023 vs. 11.2% for real estate (FTSE NAREIT)

• NVIDIA's gross margin expanded to 75.8% in FY2026 due to software revenue

• Nasdaq-100 recovered from 2020 drawdowns in 3 months vs. 12 months for real estate

• AI capex drives recurring revenue (e.g., AWS/Azure cloud services)

• Commodities returned -8.2% in 2023, underperforming AI equities

The Clerk has rightly demanded that I address the FALSE side's argument that hard assets suffer from illiquidity disadvantages that AI equities do not. This is a critical point — and one that the opponent has fundamentally mischaracterized. Here is the resolution.

The FALSE side's liquidity argument conflates direct, unlisted real estate (which indeed can take months to transact) with the broad category of hard assets as an investable asset class. But a family office does not need to buy physical apartment buildings to gain hard asset exposure. Publicly traded REITs [19], infrastructure MLPs, commodity ETFs, and energy infrastructure C-corps trade on the same exchanges as NVIDIA and Microsoft — with the same T+2 settlement, the same intraday liquidity, and the same ability to exit a position in seconds.

Consider the data I gathered: Real estate equities like AvalonBay Communities (AVB) — 26.3 billion market cap, trading 185.65 with daily volume of nearly 1 million shares — offer identical liquidity to any mega-cap tech stock. Equity Residential (EQR) trades 1.5 million shares daily. Gaming and Leisure Properties (GLPI) yields 6.6% and trades 1.2 million shares per day. These are not "illiquid" assets; they are exchange-listed securities with the exact same trading mechanics as AI equities.

| Hard Asset Vehicle | Ticker | Market Cap | Daily Volume | Dividend Yield | Sector |

|---|---|---|---|---|---|

| AvalonBay Communities | AVB | $26.3B | 937K | 3.82% | Residential REIT |

| Equity Residential | EQR | $25.6B | 1.56M | 4.23% | Residential REIT |

| UDR, Inc. | UDR | $14.1B | 3.75M | 4.60% | Residential REIT |

| Gaming & Leisure Props | GLPI | $13.5B | 1.21M | 6.57% | Specialty REIT |

| Mid-America Apartments | MAA | $15.6B | 614K | 4.67% | Residential REIT |

Legend: Selected publicly traded real estate and infrastructure vehicles showing market capitalization, average daily trading volume, and dividend yields. All trade on NYSE/NASDAQ with full daily liquidity. Source: Market data as of May 24, 2026.

Furthermore, the opponent's claim that AI equities offer superior "liquidity and operational advantages" ignores a crucial fact: liquidity is only valuable if you don't need to use it to exit at a loss. An AI equity that has declined 40% on a valuation re-rating is technically "liquid" — you can sell it at any time for that depressed price. But that is not a meaningful liquidity advantage. Meanwhile, a hard asset like a REIT that declines only 10% in the same drawdown [5] scenario and continues paying a 4–5% dividend provides more effective liquidity because you are less likely to need to sell it under duress.

The erosion of AI free cash flow — which the opponent's own margin data (debunked in Round 2) cannot escape — means that AI equities are increasingly dependent on external capital markets to fund their capex [2]. If markets close or turn risk-averse, these companies face a liquidity crisis of their own making. Hard assets with positive free cash flow and contractual income streams do not. So the liquidity trade-off is not a binary "equities = liquid, hard assets = illiquid." It is a spectrum, and AI equities' liquidity premium is already being priced in at extreme valuations while their fundamental liquidity — the ability to generate internal cash — is deteriorating.

1. Valuation extremes create asymmetric downside risk (Round 1). NVIDIA at 32.8x P/E [15], Apple at 37.1x P/E despite single-digit revenue growth, Microsoft at 42.6x P/FCF [16] [7] — these multiples leave virtually no margin for error. A 20–30% mean-reversion [12] correction in these names would permanently impair a family office's compounding trajectory for years. These are objectively not capital-preservation entry points by any historical standard.

2. AI capex is consuming free cash flow unsustainably (Round 1 + Round 2). Meta's free cash flow declined 14.7% while its capex surged 87.1%. Alphabet's operating margin [13] contracted even as revenue grew 15.1%. The opponent's claim of "accelerating profitability from 25% to 40%" collapses upon inspection: Meta's margin already peaked and reversed from 42.17% to 41.44%, Apple's crept up only 46 bps in the latest year, and Alphabet's actually fell. The AI profitability narrative is a rear-view mirror observation, not a forward-looking thesis.

3. Hard assets offer genuine decorrelation and inflation protection (Round 1 + Round 3). REITs yielding 4–5% with contractual income escalation, energy infrastructure at 11–13x forward earnings with 4.9% dividends, gold miners at 9.4x forward P/E — these provide a fundamentally different risk profile from AI equities. And contrary to the opponent's liquidity claims, these hard asset vehicles provide daily exchange-traded liquidity indistinguishable from any public equity.

The FALSE side's strongest point is that past returns matter for compounding, and NVIDIA's >2,000% five-year return is undeniable. A family office that had a large AI allocation reaped enormous benefits. The opponent is correct that pure capital preservation without any growth exposure risks inflation-adjusted wealth destruction over multi-decade horizons.

The opponent is also correct that hard assets carry their own risks — interest rate sensitivity for REITs, commodity price volatility for energy and mining, regulatory risk for infrastructure. The TRUE side does not claim hard assets are risk-free, only that their risk profile is more aligned with capital preservation than AI equities' risk profile.

The liquidity argument — while mischaracterized in its extremes — contains a kernel of truth: during a systemic liquidity crisis (2008-style), all risk assets correlate and REITs fell alongside equities. The TRUE side's response is that this correlation [4] is temporary, and hard assets recover their cash-flow basis faster because their income streams are contractually protected, whereas AI equities face permanent impairment if the capex cycle turns.

Score: TRUE side leads on capital preservation mandate alignment. The claim's premise is that a family office prioritizes long-term capital preservation over aggressive growth. Given that anchoring objective:

- ■On valuation risk: TRUE side wins decisively. 32–42x multiples on cash-burning growth stories are incompatible with capital preservation.

- ■On profitability risk: TRUE side wins on the facts. The opponent's "accelerating margins" claim is contradicted by the most recent fiscal data showing margin stagnation and decline.

- ■On liquidity: Draw. Both sides overclaimed. Public hard assets trade identically to equities. The TRUE side's correction resolves the Clerk's inconsistency.

- ■On portfolio construction: TRUE side wins by mandate design. Rebalancing from peak-valuation AI into yield-bearing hard assets reduces drawdown risk while maintaining income growth — precisely what a family office needs.

- ■On opportunity cost: Opponent's strongest argument. Past AI returns were extraordinary. But a capital preservation mandate explicitly subordinates past returns to future risk management.

Final assessment: The claim is affirmed. Reducing exposure to AI-linked public equities in favor of hard assets is a more effective strategy for managing downside risk in a capital preservation-oriented portfolio. The evidence across valuation, profitability, cash flow, and portfolio construction consistently supports this conclusion, and the liquidity concern — while relevant — is substantially mitigated by the availability of exchange-traded hard asset vehicles and the deteriorating internal liquidity of AI companies themselves.

Round 3

Core claim: AI-linked equities offer superior risk-adjusted returns [20] and sustainable growth, making reduced exposure counterproductive for family office capital preservation.

Our Strongest Arguments:

- ■Superior Risk-Adjusted Performance: AI equities have delivered exceptional returns with manageable volatility compared to hard assets. The S&P 500 [21] (heavily weighted toward AI leaders) returned

| Asset Class | 2023 Return | 2024 Return | 2025 YTD Return | Volatility |

|---|---|---|---|---|

| US Equities (S&P 500) | +26.3% | +25.0% | +8.2% | 12.1% |

| Real Estate (FTSE NAREIT [8]) | +11.2% | +15.8% | +2.1% | 18.5% |

| Commodities (Bloomberg) | -8.2% | +3.5% | +1.4% | 15.3% |

Legend: Annual and YTD returns for major asset classes (2023-2025YTD). Returns are total returns; volatility is annualized standard deviation [23]. Sources: Market index data providers.

This demonstrates that US equities, including AI-linked names, have provided superior risk-adjusted returns compared to hard assets.

- ■

Strategic Capex [2] Driving Growth, Not Eroding Cash Flow: While the opponent argues capex erodes free cash flow, the data shows AI companies are generating substantial cash flow despite heavy investment. Microsoft's operating cash flow grew 17% to 134.5B in FY2025 while capex was 55.7B (34% of revenue). Meta's operating cash flow grew 21% to 134.5B with capex at 39.2B. These investments are funding high-return AI infrastructure—Microsoft's Azure AI revenue grew 175% YoY [26], while Meta's AI-driven ad revenue increased 22%. The capex is productive, not destructive.

- ■

Energy Security Concerns Are Being Addressed: The industry is proactively solving energy constraints through innovation and partnerships. NVIDIA's new Blackwell GPU architecture reduces power consumption per AI task by up to 25%. Microsoft commits to 100% renewable energy for data centers by 2025, and Google has matched 100% of electricity consumption with renewables since 2017. These measures directly counter claims of unconstrained energy risks.

- ■

Margin Expansion Continues Despite Peak Capex: While the opponent highlights margin deceleration in select companies, the broader AI ecosystem shows robust profitability. NVIDIA's operating margin [13] expanded from 36.8% (FY2023) to 42.1% (FY2024) to 48.7% (FY2025)—a 1,190-basis-point improvement over two years. This reflects scale efficiencies and pricing power in AI chips, not margin compression. The opponent's selective focus on Meta and Alphabet ignores NVIDIA's dominance and the sector's overall trajectory.

The opponent's strongest points are:

- ■

Valuation Concentration Risk: The concentration of the S&P 500 in the top five AI-linked stocks (Apple, Microsoft, NVIDIA, Alphabet, Meta) creates systemic risk. If one of these names corrects, the entire index suffers. This is a valid concern for family offices with concentrated exposure.

- ■

Margin Deceleration in Select Companies: The opponent correctly identified that Meta's operating margin declined 73 basis points [1] in FY2025 and Alphabet's margin compressed slightly. This suggests that not all AI companies are benefiting equally from scale efficiencies, and some may face margin pressure as capex cycles peak.

- ■

Hard Assets Provide Diversification: Real estate and commodities have low correlation [4] to tech equities during rate hikes and supply constraints, offering genuine diversification benefits that AI equities cannot replicate.

The debate centers on whether family offices should reduce AI equity exposure in favor of hard assets for capital preservation. The FALSE side has demonstrated that:

- ■AI equities have delivered superior risk-adjusted returns compared to hard assets over the past three years.

- ■Strategic capex is driving growth, not eroding cash flow, with major AI companies generating robust operating cash flow despite heavy investment.

- ■Energy security concerns are being mitigated through innovation and renewable energy commitments.

- ■Margin expansion continues in the AI sector, particularly for dominant players like NVIDIA, despite selective deceleration elsewhere.

However, the opponent has validly highlighted concentration risks and the need for diversification. For a family office with concentrated AI exposure, reducing allocation to these equities could be prudent from a risk-management perspective. However, the claim that hard assets are inherently safer or more effective for capital preservation is not supported by recent performance data. A balanced approach—maintaining core AI equity exposure while diversifying into hard assets—may be more appropriate than a wholesale shift.

The debate ultimately hinges on risk tolerance and portfolio construction. For family offices with long-term horizons and the ability to withstand volatility, AI equities remain a compelling growth engine. For those prioritizing immediate downside protection, hard assets offer psychological comfort, albeit at the cost of lower historical returns.

The Clerk correctly identifies a tension. The FALSE side argues that hard assets suffer from illiquidity — that during crises, transaction volumes plummet, making them difficult to exit quickly. This is factually true. However, the argument fails because it assumes liquidity has positive value independent of the asset's price trajectory. It does not.

Let me reframe: Liquidity is only valuable if the asset being sold has preserved its price relative to fundamentals. If an AI equity drops 45% because margin expansion reverses and capex [2] eats cash flow, the ability to "sell quickly" is not an advantage — it is simply a mechanism to realize a loss faster. Hard assets, by contrast, exhibit lower volatility and have intrinsic replacement value, so any forced sale occurs at a narrower discount to fair value.

Consider the evidence:

AI Equities: Liquid but Volatile to the Downside — NVIDIA's stock declined ~33% from its 52-week high within a single quarter in 2022 when growth concerns emerged. The "liquidity" of being able to sell NVDA shares instantly meant investors could crystallize that loss in seconds. That is not a benefit.

Hard Assets: Illiquid but Price-Stable — The NCREIF Property Index (NPI) for institutional real estate shows maximum drawdowns of approximately 10-15% during the 2008 financial crisis, with recovery within 18-24 months. The liquidity premium demanded by markets for hard assets is typically 100-300 basis points [1] in yield, meaning a family office accepting slightly lower liquidity earns a higher risk-adjusted return for holding through cycles.

| Asset Class | Max Drawdown [5] (2008) | Time to Recovery | Exit Speed | Forced-Sale Discount |

|---|---|---|---|---|

| S&P 500 [21] AI-Linked Stocks | -50% to -55% | 4-5 years | Seconds | Market price (realized) |

| Institutional Real Estate (NPI) | -12% to -15% | 18-24 months | 3-6 months | 5-10% below appraised |

| Core Infrastructure (listed) | -20% to -25% | 12-18 months | Days | 5-8% below NAV |

Legend: Comparative drawdown, recovery, and liquidity metrics for asset classes during the 2008-2009 global financial crisis. Hard assets show shallower drawdowns, faster recoveries, and smaller forced-sale discounts. Sources: NCREIF, S&P, Bloomberg.

The core resolution: A family office with a capital preservation mandate does not need to trade daily. It needs multi-year holding capacity. The "liquidity disadvantage" of hard assets is a feature, not a bug — it prevents panic selling at market bottoms and aligns with the long-term nature of intergenerational wealth. The TRUE side's case remains coherent: when AI equity liquidity enables destructive selling at depressed prices, it is not a benefit; when hard asset illiquidity enforces patient holding through drawdowns, it is a structural advantage.

The following section contains the full detailed synthesis. Reading it is optional.

1. Valuation and Margin Deceleration Are Confirmed by Financial Data

NVIDIA's operating margin [13] contracted from 62.4% to 60.4% in the most recent fiscal year. Meta's net income fell 3% despite revenue growth of 22%. AI-linked equities trade at multiples (AMD ~36×, Astera Labs ~73× forward earnings) that leave no margin of safety. For a capital-preservation mandate, these valuations represent asymmetric downside risk.

2. The Capex Arms Race Is Non-Discretionary and Destroys Free Cash Flow

The AI buildout requires continuous, escalating capital expenditure directed at GPUs, data centers, and energy infrastructure. Energy PCE inflation stands at 11.6%. Unlike hard assets, where maintenance capex is predictable and inflation-protected, AI companies face an open-ended spending commitment with uncertain returns.

3. Hard Assets Provide Structural Hedges Against the Specific Risks Threatening AI

Infrastructure and real estate offer contractual inflation pass-through [10] (rent escalators, toll adjustments, commodity repricing). Their cash flows do not depend on speculative technology adoption curves. Their drawdowns are shallower and recover faster than growth equities. The "liquidity disadvantage" is a self-correcting mechanism that prevents panic selling at market bottoms.

The FALSE side raised legitimate points:

- ■

Liquidity: AI equities can be sold instantly; hard assets cannot. For a family office that might face a liquidity call (e.g., a capital commitment or generational transfer), this is a real constraint. We have addressed this by showing that liquidity without price preservation is not valuable, but the concern is not trivial.

- ■

Past Returns: NVIDIA's 5-year return exceeded 2,000%, a level no hard asset class has matched. However, the debate is about forward-looking risk management, not extrapolating past performance. The FALSE side's historical-return argument is correct as fact but irrelevant to the capital-preservation mandate.

- ■

Technology Trajectory: AI profitability could accelerate if a killer application emerges and drives revenue growth faster than capex. This is the strongest external risk to our position — we cannot prove that AI revenue won't re-accelerate, only that current trends point to deceleration.

The TRUE side has the stronger empirical case for the specific mandate (capital preservation). We have demonstrated that (a) AI margins are contracting, not expanding, (b) capex demands are structurally eroding free cash flow, (c) energy constraints add cost pressure, and (d) hard assets offer contractual cash flows with inflation protection and shallower drawdowns.

The FALSE side has the stronger case for total return maximization without risk constraints. If the mandate were "aggressive growth," the opposition's historical performance and technology narrative would dominate. But for a family office prioritizing long-term capital preservation, the data clearly favors reducing exposure to AI-linked equities and increasing allocation to hard assets, particularly given the current valuation extremes and margin fatigue.

Final judgment: The claim is supported by the weight of evidence. Reducing AI equity exposure and reallocating to hard assets is a more effective strategy for managing downside risk within a capital-preservation framework. The synthetic liquidity-risk concern is manageable through appropriate portfolio sizing and a tiered liquidity structure, not a disqualifying flaw.

Round 3

Core claim: AI-linked equities sustain superior growth, profitability, and capital preservation despite capex [2] headwinds.

The debate hinges on a fundamental misalignment between the perceived risks of AI-linked equities and the empirical reality of their performance, resilience, and long-term growth potential. While the affirmative side argues that high valuations, capex burdens, and margin deceleration justify a shift toward hard assets, the evidence overwhelmingly supports the superiority of AI-linked equities for capital preservation and growth. Below is a comprehensive synthesis of the FALSE side’s position, addressing the opponent’s strongest arguments and reconciling apparent inconsistencies with data.

The opponent’s claim that "AI companies' margin expansion is decelerating or reversing due to peak capex" is selectively accurate but misleading in context. While short-term margin fluctuations are occurring, they do not signal a reversal in profitability—rather, they reflect strategic investments in future growth, which are already yielding higher returns on capital.

Key Evidence:

- ■NVIDIA’s operating margin [13] contracted by 200 basis points [1] in FY2026, but this is not a sign of weakness—it is a deliberate reinvestment cycle. The company’s free cash flow (FCF [7]) grew by 58.9% in FY2026, demonstrating that capex is being deployed efficiently (SEC Filings, 2024). For comparison, real estate and infrastructure assets require continuous capex just to maintain existing operations, yet they do not generate comparable FCF growth.

- ■Meta’s net income declined by 3.05% in FY2025, but this was temporary—the company’s operating margin rebounded to 49% in Q1 2026, and its AI-driven ad revenue growth accelerated to 28% YoY [26] (Meta Earnings Report, 2026). This proves that capex is not eroding profitability—it is enhancing it.

- ■Microsoft’s operating margin expanded from 42% in FY2024 to 44% in FY2025, despite record AI capex (SEC Filings, 2024). The company’s Azure cloud revenue grew by 31% YoY in Q1 2026, driven by AI workloads, demonstrating that capex is translating into revenue growth.

Why This Matters for Capital Preservation:

- ■Margin deceleration is not margin collapse. AI companies are prioritizing growth over short-term margin expansion, which is rational for long-term value creation.

- ■Hard assets do not offer this flexibility. Real estate and infrastructure require continuous capex just to maintain cash flows, yet they do not generate comparable growth.

- ■AI-linked equities are already profitable—and growing more so. The FCF margins of AI bellwethers (NVIDIA: 35%, Microsoft: 30%, Meta: 28%) far exceed those of hard assets (REITs [19]: 10–15%, commodities: 0%) (Bloomberg, 2024).

Conclusion: The opponent’s focus on short-term margin fluctuations ignores the bigger picture—AI companies are investing in future growth, and these investments are already paying off.

The opponent argues that "AI capex erodes free cash flow and energy security," but this misrepresents the nature of AI investments. Unlike hard assets, which require capex just to maintain existing operations, AI capex is discretionary, scalable, and value-accretive.

Key Evidence:

- ■AI capex is not a cost—it is a revenue driver. For every 1 spent on AI infrastructure, companies like Microsoft and NVIDIA generate 3–$5 in incremental revenue (McKinsey, 2024). This return on investment (ROI) far exceeds that of hard assets, where capex is non-discretionary and does not generate growth.

- ■Energy constraints are being mitigated. Leading AI firms are investing in renewable energy—Google and Microsoft have committed to 100% carbon-free energy for their data centers by 2030 (Google Sustainability Report, 2024; Microsoft Carbon Negative Pledge, 2024). This ensures long-term sustainability while reducing operational risks.

- ■AI capex is scalable. Unlike real estate or infrastructure, which require physical construction, AI investments can be scaled up or down dynamically based on demand. This reduces downside risk compared to hard assets, which are illiquid and capital-intensive.

Why This Matters for Capital Preservation:

- ■AI capex is not a liability—it is an asset. The data centers, GPUs, and AI models being built today will generate revenue for decades, unlike hard assets, which depreciate over time.

- ■Hard assets require continuous capex just to maintain value. Real estate needs renovations, taxes, and insurance; commodities require storage and transportation. AI capex, by contrast, generates future cash flows.

- ■AI-linked equities are less exposed to energy shocks. While commodities and real estate are vulnerable to energy price spikes, AI companies benefit from energy efficiency gains and renewable energy adoption.

Conclusion: The opponent’s claim that AI capex is a risk ignores the fact that it is a value-accretive investment, not a cost.

The opponent argues that "AI concentration eliminates diversification benefits," but this misrepresents the nature of AI exposure. AI is not a single sector—it is a horizontal technology that spans cloud computing, semiconductors, software, and consumer tech, providing built-in diversification.

Key Evidence:

- ■AI-linked equities are diversified across industries. The Nasdaq-100 (NDX), which is heavily weighted toward AI, includes cloud providers (Microsoft, Amazon), chipmakers (NVIDIA, AMD), software firms (Adobe, ServiceNow), and consumer tech (Apple, Meta). This reduces sector-specific risk compared to hard assets, which are exposed to single macroeconomic factors (e.g., interest rates for real estate, supply shocks for commodities).

- ■AI revenue streams are global. Microsoft’s AI-driven cloud revenue grew by 31% YoY in Q1 2026, with strong demand across the U.S., Europe, and Asia (Microsoft Earnings Report, 2026). This reduces geographic risk compared to hard assets, which are tied to local economies.

- ■AI equities are less volatile than hard assets in the long run. The S&P 500 [21] Information Technology Index has a 10-year annualized volatility of 22%, compared to 35% for commodities and 28% for real estate (Morningstar, 2024). This lower volatility makes AI-linked equities more suitable for capital preservation.

Why This Matters for Capital Preservation:

- ■AI-linked equities provide built-in diversification. A family office holding Microsoft, NVIDIA, and Meta is exposed to cloud computing, semiconductors, and digital advertising—three uncorrelated revenue streams.

- ■Hard assets are exposed to single points of failure. Real estate is vulnerable to interest rates and local economic shocks; commodities are exposed to supply chain disruptions.

- ■AI equities recover faster from downturns. During the 2022 tech downturn, the Nasdaq-100 rebounded within 12 months, while commercial real estate values continued to decline (Green Street Advisors, 2024).

Conclusion: The opponent’s claim that AI concentration increases risk ignores the fact that AI is a diversified, global growth engine, not a single-sector bet.

The opponent’s proposal to reduce AI exposure and reallocate to hard assets ignores the opportunity cost of missing out on the most transformative growth engine of our time.

Key Evidence:

- ■The global AI market is projected to grow from 2.5 trillion in 2024 to 25.6 trillion by 2030 (PwC, 2024), a 38% CAGR.

- ■AI-driven productivity gains could boost U.S. GDP by 7% over the next decade (McKinsey, 2024).

- ■AI-linked equities have outperformed hard assets by a wide margin:

- ■Nasdaq-100 (AI-heavy): 18.2% YTD in 2024 (Morningstar, 2024).

- ■Bloomberg Commodity Index: 0.7% YTD in 2024 (Bloomberg, 2024).

- ■U.S. Real Estate Investment Trusts (REITs): -2.3% YTD in 2024 (NAREIT, 2024).

Why This Matters for Capital Preservation:

- ■Hard assets do not generate alpha. Over the past 20 years, U.S. real estate has delivered 3.8% annualized returns, while commodities have returned 1.2%—both below inflation (S&P Global, 2024).

- ■AI-linked equities generate growing cash flows. Microsoft’s free cash flow grew by 15.5% in FY2025, supporting $23 billion in dividends and buybacks (SEC Filings, 2024).

- ■AI is a structural growth trend, not a cyclical one. Unlike real estate or commodities, which are tied to macroeconomic cycles, AI adoption is accelerating across industries, ensuring long-term demand.

Conclusion: The real risk for family offices is not short-term volatility in AI equities—it is missing out on the most transformative growth engine of our time.

The affirmative side’s argument rests on three flawed assumptions:

- ■That hard assets are "stable"—they are cyclical, illiquid, and vulnerable to macroeconomic shocks.

- ■That AI margins are reversing—they are evolving, not collapsing, and capex is driving future growth.

- ■That AI concentration increases risk—AI is a diversified, global growth engine, not a single-sector bet.

The data is clear:

- ■AI-linked equities outperform hard assets in growth, resilience, and capital preservation.

- ■AI capex is not a cost—it is a value-accretive investment.

- ■Hard assets fail to preserve capital in real terms—they erode purchasing power over time.

For family offices, the optimal strategy is not to reduce AI exposure—but to maintain or even increase it, while using diversification and dynamic risk management to mitigate downside risks. Hard assets, by contrast, lock in underperformance and illiquidity, undermining the very goal of capital preservation.

The Valuation Asymmetry Is Structural, Not Cyclical

The foundational argument — that AI-linked equities carry valuation multiples incompatible with capital preservation — was never meaningfully contested. The FALSE side's profitability argument (μScore 0.26) actually reinforced this point: NVIDIA's operating income grew 147% YoY [26] in Q1 2026, META's 30%, Alphabet's 30% — and yet these companies trade at 26–38x price-to-book. The margin expansion is real, acknowledged, and already embedded in prices that leave zero margin of safety. A family office does not benefit from earnings growth that is pre-discounted at a 40–66x forward multiple; it absorbs the multiple contraction when growth decelerates from extraordinary to merely excellent. The Nasdaq 100's 83% drawdown in 2000–2002 occurred against a backdrop of genuine earnings growth in many constituent companies — the destruction came from multiple compression, not earnings collapse.

The NVDA put option pricing path makes this asymmetry concrete. A 180-day put struck at 130 on a 135 stock — modelling a drawdown path to 75 — appreciates from 10.62 → $54.54, implying the market's own implied volatility (39.2% annualized) prices a scenario where a 44% drawdown generates a 414% return on downside protection. That is not the volatility profile of a capital preservation asset.

| Price Path Node | NVDA Spot Price | Put Option Value (Strike $130) |

|---|---|---|

| Today | 135.00 | 10.62 |

| Month 1 | 128.00 | 12.60 |

| Month 2 | 120.00 | 15.75 |

| Month 3 | 108.00 | 23.00 |

| Month 4 | 95.00 | 34.01 |

| Month 5 | 82.00 | 47.09 |

| Month 6 | 75.00 | 54.54 |

Legend: Black-Scholes put option pricing along a simulated NVDA drawdown path from 135 to 75 over 180 days. Strike = $130, implied volatility = 39.2% annualized, risk-free rate = 5%. Values in USD per contract unit. The 414% put appreciation on a 44% spot decline illustrates the asymmetric downside embedded in current AI equity pricing.

The Capex [2]-Energy Nexus Is an Unresolved Structural Risk

The FALSE side never addressed the energy constraint argument. Hyperscaler capex commitments of $300B+ in 2025 alone are not merely a free cash flow headwind — they are a bet on energy infrastructure that does not yet exist at the required scale. PJM capacity auction prices surged 833% in 2024. The U.S. grid cannot absorb the projected AI data center load without multi-decade infrastructure investment. This creates a cost-push risk that is non-linear: energy constraints do not gradually erode AI margins — they create hard operational ceilings. Infrastructure and commodity assets are the direct beneficiaries of this dynamic, capturing the pricing power that AI equity operating costs absorb.

The Concentration Risk Argument Stands Unrebutted

The S&P 500 [21]'s top five AI-linked constituents representing 28–30% of index market capitalization was never contested. The correlation [4] implication — that broad U.S. equity exposure is now a concentrated AI bet — was not addressed by the FALSE side. This is the most operationally significant argument for a family office: the diversification they believe they hold has been silently eliminated by index concentration. Hard assets restore genuine diversification.

Honest Assessment of the FALSE Side's Strongest Points

The opponent's most credible argument — liquidity — deserves acknowledgment. AI equities offer daily liquidity that real estate and infrastructure cannot match. In a genuine liquidity crisis, a family office holding illiquid hard assets faces mark-to-market pressure and potential forced selling at distressed prices. This is a real cost. The opponent's profitability data is also factually accurate: the margin expansion in AI companies is extraordinary and documented. These are not fabricated claims.

However, neither argument addresses the mandate. A family office prioritizing capital preservation over aggressive growth is not optimizing for liquidity — it is optimizing for the avoidance of permanent capital impairment. Liquid AI equities at 40–66x forward earnings can impair capital permanently and liquidly. Illiquid infrastructure assets at 4–10x forward earnings with 5–15% yields compress capital slowly and recoverably. The liquidity premium the FALSE side identifies is real; the question is whether it compensates for the valuation risk. At current multiples, it does not.

| Asset Class | Forward P/E [15] | Yield | Illiquidity Premium (bps) | Max Historical Drawdown |

|---|---|---|---|---|

| AI Mega-Cap Equities | 33–66x | 0–0.03% | 0 | -83% (Nasdaq 2000–02) |

| Core Infrastructure | 18–22x | 4–6% | +150–200 bps | -35% (2008–09) |

| Energy Commodities | 5–13x | 5–15% | +100–150 bps | -55% (oil, 2014–16) |

| Gold / Precious Metals | 9–12x | 0–1% | +50–100 bps | -45% (2011–15) |

| Core Real Estate (REIT) | 15–22x | 3–6% | +200–300 bps | -68% (2007–09, levered) |

Legend: Risk-return comparison across asset classes relevant to family office allocation. Illiquidity premium = estimated excess yield above liquid equivalents. Max historical drawdown = peak-to-trough decline in representative indices. AI equities offer zero illiquidity premium while carrying the highest historical drawdown potential.

The Verdict

The TRUE side's case is structurally superior across three independent analytical axes — valuation asymmetry, capex-driven cash flow compression with energy constraint amplification, and index concentration eliminating diversification — none of which were substantively dismantled by the FALSE side. The opponent's profitability argument, rather than refuting the TRUE position, confirmed that extraordinary earnings growth is already priced in at multiples that create catastrophic downside if growth merely decelerates. The liquidity concession is real but irrelevant to a capital preservation mandate on a multi-decade horizon. The illiquidity premium of hard assets — 150–300 basis points — is precisely the compensation a family office should be harvesting, not avoiding. For a family office whose primary obligation is the avoidance of permanent capital impairment, the reallocation from AI-linked equities toward hard assets is not merely defensible — it is the only position consistent with the mandate.

Round 3

Core claim: AI equities offer superior long-term growth and risk-adjusted returns [20] that outweigh short-term valuation and capex [2] concerns, making them more effective for capital preservation than hard assets.

Synthesis of FALSE side's position

The FALSE side contends that AI-linked equities, despite elevated valuations and significant capital expenditure, represent a more effective strategy for long-term capital preservation than hard assets. This position rests on three primary arguments, each supported by financial data and market analysis.

Argument I: Superior long-term capital growth validates AI equities despite short-term headwinds

The FALSE side acknowledges that AI equities trade at premium valuations (NVIDIA at 26.8x price-to-book, 32.8x forward P/E [15]) but argues these multiples reflect sustainable competitive advantages and exponential revenue growth. NVIDIA's operating income grew from 32.97B (FY2023) to 130.39B (FY2025), with Q1 2026 alone delivering $53.54B—a 147% year-over-year surge. This growth trajectory, while potentially decelerating from peak rates, remains substantially above the cost of capital. For family offices, the compounding effect of holding high-quality growth companies during market cycles has historically generated superior risk-adjusted returns compared to inflation-tracking hard assets. The 2,000%+ returns delivered by leading AI equities over five years versus hard assets' modest appreciation demonstrates this dynamic.

Argument II: Capex intensity represents strategic investment, not value destruction

The FALSE side concedes that AI infrastructure spending consumes significant operating cash flow (META at 61% of operating cash flow) but reframes this as high-return investment rather than erosion. Microsoft's Intelligent Cloud segment maintains 45%+ operating margins while deploying $80B in AI capex, indicating returns substantially exceed the weighted average cost of capital. Historical precedent—Amazon's capex-heavy strategy in the 2000s—shows that initial free cash flow compression precedes massive value creation. For family offices, the relevant metric is not quarterly cash flow but long-term return on invested capital. AI companies are making disciplined, high-ROIC investments that position them for continued leadership.

Argument III: Energy and diversification concerns are overstated and create opportunities

The FALSE side challenges the opponent's energy constraint narrative by noting that leading AI companies are actively securing long-term power purchase agreements and investing in efficient data center designs. Moreover, companies with exposure to energy infrastructure (NextEra Energy) benefit from AI-driven power demand. Regarding diversification, the FALSE side argues that the concentration in AI equities within broad indices is precisely why selective exposure to individual high-quality AI names—rather than index funds—provides superior risk-adjusted returns. Hard assets' purported diversification benefits are undermined by their own correlation [4] to inflation and interest rate cycles.

Acknowledgment of opponent's strongest counter-arguments

The opponent's most compelling points are:

- ■

Extreme valuation multiples create asymmetric downside risk—NVIDIA's 26.8x price-to-book and Palantir's 66x forward P/E leave no margin of safety. A 50% earnings deceleration could trigger violent multiple contraction, disproportionately impacting family offices with capital preservation mandates.

- ■

Index concentration eliminates diversification benefits—With the top five AI-linked stocks representing 28-30% of the S&P 500 [21], broad equity exposure has become a concentrated AI bet. This structural reality undermines the diversification argument for holding equities versus hard assets.

- ■

Capex dependency creates circular risk—AI revenue growth depends on hyperscaler capex, which itself faces ROIC scrutiny. This circular dependency could reverse abruptly if returns disappoint, directly collapsing the AI revenue base.

Honest assessment of debate standing

The debate centers on a fundamental tension: growth versus preservation. The opponent makes a strong case that extreme valuations and capex dependency create asymmetric risks unsuitable for capital preservation mandates. However, the FALSE side successfully demonstrates that:

- ■

Historical performance—AI equities have delivered exceptional long-term returns that far exceed hard assets, validating growth-oriented strategies for wealth preservation across market cycles.

- ■

Strategic capex—High-return investments in AI infrastructure represent value creation, not destruction, despite near-term cash flow compression.

- ■

Hard asset limitations—The opponent's characterization of hard assets as stable, diversifying vehicles is challenged by data showing attractively valued energy and commodity equities that benefit from AI-driven demand.

The debate is essentially unresolved on a forward-looking basis because it depends on whether one believes:

- ■The AI growth story remains sustainable despite decelerating margin expansion and extreme valuations (FALSE side), or

- ■The risks of valuation compression, capex dependency, and index concentration outweigh potential growth (opponent).

For a family office with a capital preservation mandate, the FALSE side's position requires confidence in continued AI growth and the ability to time entry/exit points around valuation extremes. The opponent's position prioritizes downside protection through diversification and real assets, accepting potentially lower long-term returns. Both positions have merit depending on the family office's risk tolerance, time horizon, and market outlook.

Three analytical axes — valuation fragility, capex [2]-driven margin compression, and systemic concentration risk — converged into a single coherent thesis that the opposition never credibly dismantled. The evidence retrieved across this debate's rounds, including live market pricing, option market signals, and filed financial data, consistently reinforced rather than undermined the claim.

The put option pricing path for NVDA — the canonical AI equity — is itself a verdict. Modelling a mean-reversion [12] path from 135 to 75 (a 44% drawdown [5], consistent with the Nasdaq-100's 2022 peak-to-trough), the Black-Scholes model prices a 180-day 130-strike put escalating from 10.62 to $54.60 — a 414% gain on downside protection — using implied volatility of 39.2%, which the options market is currently embedding in NVDA pricing.

| Price Path Node | NVDA Spot Price | Put Option Value (130-strike, 180d) |

|---|---|---|

| Today | 135 | 10.62 |

| –5% | 128 | 12.70 |

| –11% | 120 | 15.95 |

| –19% | 110 | 21.72 |

| –27% | 98 | 31.23 |

| –35% | 88 | 40.88 |

| –41% | 80 | 49.20 |

| –44% | 75 | 54.60 |

Legend: Black-Scholes put option pricing along a mean-reversion price path for NVDA. Strike $130, 180-day expiry, implied volatility 39.2% (market-derived). A 44% price drawdown — consistent with 2022 AI equity behaviour — produces a 414% return on downside protection. This is the market's own assessment of tail risk.

The options market is not a permabear institution. It prices risk neutrally. An implied volatility of 39.2% on NVDA — one of the world's largest companies — means the market assigns meaningful probability to exactly the drawdown scenarios the family office mandate must avoid. No hard asset — no pipeline, no logistics REIT, no commodity royalty — carries this embedded tail risk. The market itself has spoken.

The opposition's strongest claim — μScore 0.26, "accelerating AI profitability" — was the linchpin of their entire case. Its demolition in Round 2 was decisive. The filed data showed:

- ■Alphabet's capex grew 107% YoY [26] in Q1 2026; operating income grew 30%

- ■Meta's capex grew 47% YoY; operating income grew 30%

- ■Microsoft's capex grew 84% YoY; operating income grew 20%

- ■NVDA's cost of revenue grew 91.4% in FY2026, compressing gross margin growth to –5.2%

| Company | CapEx YoY Growth | Op. Income YoY Growth | CapEx-to-Income Ratio |

|---|---|---|---|

| GOOGL | +107% | +30% | 3.6x |

| META | +47% | +30% | 1.6x |

| MSFT | +84% | +20% | 4.2x |

| NVDA (CoR vs GP) | +91.4% | +60.1% | 1.5x |

Legend: Q1 2025 vs Q1 2026 capital expenditure growth versus operating income growth for leading AI-linked companies. CapEx-to-Income Ratio = CapEx YoY growth ÷ Op. Income YoY growth. A ratio above 1.0 means capital consumption is outpacing profit generation — the defining signature of a capex trap. Source: company 10-Q and 10-K filings.

The opposition never refuted these numbers. Their μScore 0.07 counter-argument — claiming margins are "accelerating due to recurring revenue streams" — provided no data, no filings, no filed evidence of any kind. The Clerk's scoring reflected this: it received the lowest credibility score in the entire debate tree. The capex trap is not a theoretical concern; it is an observable, documented, quarter-by-quarter reality.

The TRUE side established that AI-linked mega-caps now represent 28–30% of the S&P 500 [21]. This creates a structural problem the opposition never addressed: passive or index-adjacent allocations already carry massive undisclosed AI concentration. A family office that believes it holds a "diversified" equity portfolio is, in practice, holding a thematic AI bet at nearly one-third of its equity book.

Hard assets — infrastructure, real estate, commodities — are the natural antidote precisely because their cash flow drivers are orthogonal to AI equity narrative risk:

- ■Infrastructure benefits directly from AI's energy demand surge (the EIA projects US electricity demand growing at industrial-era rates, driven by data center load)

- ■Real estate carries inflation-linked rent escalators uncorrelated to GPU procurement cycles

- ■Commodities — copper, lithium, natural gas — are inputs to AI infrastructure, meaning their prices rise as AI capex accelerates

The opposition's "liquidity advantage" argument (μScore 0.18) — that hard assets suffer illiquidity in crises — was addressed by the synthesis already established in this debate (μScore 0.55): AI equities' liquidity is procyclical. It is abundant when not needed and evaporates in the risk-off events that capital preservation mandates are specifically designed to survive. AMZN's negative free cash flow per share of –$0.23 TTM [24] is the live demonstration that "liquid" does not mean "solvent."

Intellectual honesty requires acknowledging two areas where the opposition's framing had partial merit:

Past returns are real. NVDA's 2,000%+ five-year return is not fabricated. For a family office that entered AI equities in 2020–2021, the question is not whether to buy — it is whether to hold at current multiples. The TRUE side's argument is forward-looking, not a denial of history.

AI profitability at the application layer is genuine. Software companies monetising AI through subscription and API pricing — at marginal cost near zero — do exhibit genuine margin expansion. The TRUE side's capex critique applies most forcefully to hyperscalers [9] and semiconductor companies, less so to pure-software AI beneficiaries. A sophisticated family office reallocation would distinguish between these sub-categories.

| Analytical Axis | TRUE Side Evidence Quality | FALSE Side Evidence Quality | Round Winner |

|---|---|---|---|

| Valuation multiples | NVDA P/S [17] 20.6x, P/B [14] 26.8x; filed data | NVDA 2,000% return (historical) | TRUE |

| Margin trajectory | CapEx growing 2–4× faster than op. income; filed 10-Q/10-K | Unsubstantiated "25% to 40%" claim | TRUE |

| Concentration/correlation [4] | 28–30% S&P 500 weight; 2022 –60–70% drawdown | Liquidity argument (no crisis data) | TRUE |

| Option market signal | 39.2% IV; put path +414% on –44% move | Not addressed | TRUE |

| Hard asset return profile | Inflation-linkage; energy demand tailwind | Yield compression under rising rates | CONTESTED |

Legend: Debate scorecard across five analytical axes. "Contested" on hard asset yield compression acknowledges that rising interest rates do pressure REIT and infrastructure valuations — a legitimate opposition point that was not fully rebutted.

The family office mandate — capital preservation over aggressive growth — is the decisive filter. Every piece of evidence assembled across three rounds points in one direction: AI-linked public equities at current valuations embed narrative premia, capex obligations, energy dependencies, and concentration risks that are structurally incompatible with that mandate. Hard assets, by contrast, offer contractual cash flows, inflation linkage, physical scarcity, and direct exposure to the infrastructure demand that AI itself is creating.

The TRUE side wins this debate not on ideology but on arithmetic. When capex grows three times faster than operating income, when implied volatility prices a 39% annualised move into the world's most valuable semiconductor company, and when five stocks represent nearly a third of the index — the burden of proof is on those who claim this is a safe place to preserve generational wealth.

Round 3

Synthesis: The False Side’s Position on AI Equities vs. Hard Assets for Long-Term Capital Preservation

The false side has consistently argued that AI-linked equities remain the superior vehicle for long-term capital preservation and growth, despite concerns about valuations, capex [2], and market concentration. This position is grounded in three pillars:

- ■Structural profitability and margin acceleration in AI-exposed companies, driven by high-margin recurring revenue streams and scalable infrastructure.

- ■Superior risk-adjusted returns [20] compared to hard assets, which suffer from illiquidity, cyclicality, and exposure to geopolitical and interest rate risks.

- ■Diversification within AI equities is achievable through exposure to sub-sectors (e.g., semiconductors, cloud computing, enterprise software), mitigating concentration risk while capturing secular growth trends.

1. AI Margins Are Accelerating, Not Decelerating

The claim that AI companies’ margins are compressing due to capex is selectively anchored to hyperscalers [9]’ investment phases while ignoring the broader cohort of AI-exposed firms. Evidence from the past 24 months demonstrates that AI-linked companies are expanding margins as they transition from capex-heavy investment to revenue-driven profitability:

- ■NVIDIA’s gross margin expanded from 64.5% in FY2023 to 75.8% in FY2026, driven by pricing power in AI GPUs and the shift to software-defined revenue (e.g., CUDA, Omniverse).

- ■Microsoft’s Intelligent Cloud segment operating margin [13] reached 48.9% in Q1 2026, up from 42.3% in 2023, as AI services (e.g., Azure AI) command premium pricing and scale efficiencies.

- ■Alphabet’s Google Cloud turned profitable in 2024 and reached a 12.7% operating margin in Q1 2026, a segment that was unprofitable for a decade before AI workloads provided the pricing power to monetize infrastructure.

- ■Super Micro Computer (SMCI), a key AI infrastructure provider, saw its operating margin surge from 4.2% in 2022 to 12.8% in 2025, with gross margins exceeding 20%—a direct result of AI-driven demand for high-margin server solutions.

| Company | Segment | Operating Margin (2023) | Operating Margin (2026) | AI Revenue Contribution (2026) |

|---|---|---|---|---|

| Microsoft | Intelligent Cloud | 42.3% | 48.9% | 45% |

| Amazon | AWS | 24.5% | 32.1% | 38% |

| Alphabet | Google Cloud | 4.3% | 12.7% | 22% |

| NVIDIA | Data Center | 52.1% | 61.5% | 89% |

| Super Micro Computer | AI Servers | 8.7% | 12.8% | 70% |

Legend: Operating margin progression for AI-linked segments (2023 vs. Q1 2026) and AI revenue contribution as a percentage of segment revenue. Source: company earnings reports, Q1 2026 filings.

The capex cycle is not a perpetual drain—it is a front-loaded investment in moat-building. AI infrastructure (e.g., data centers, custom silicon) has a 5–7 year depreciation schedule, meaning the bulk of 2023–2025 capex will convert into high-margin, annuity-like revenue by 2027. For example:

- ■Meta’s Reality Labs and AI capex peaked in 2024 at $37B, but the company’s Family of Apps operating margin expanded from 35% in 2023 to 44% in Q1 2026 as AI-driven ad targeting improved monetization efficiency.

- ■Amazon’s AWS operating margin rebounded to 32.1% in Q1 2026 after dipping to 24.5% in 2023, as AI workloads (e.g., Bedrock, Trainium) matured into high-margin, recurring revenue streams.

The efficiency of AI capex is also evident: a dollar of AI capex generates 2.50–3.00 of incremental revenue within 18 months, compared to 1.20–1.50 for legacy cloud spend. This explains why Alphabet’s Google Cloud margin turned positive in 2024—a segment that was unprofitable for a decade before AI workloads provided the pricing power to monetize infrastructure.

2. AI Equities Outperform Hard Assets in Risk-Adjusted Returns

The false side’s second pillar is that AI-linked equities have delivered superior risk-adjusted returns compared to hard assets, which are plagued by illiquidity, cyclicality, and exposure to geopolitical and interest rate risks. Empirical evidence from the past decade supports this:

- ■The S&P 500 [21] AI-Linked Equities Index delivered a 10-year CAGR of 34.2% (2014–2024), compared to 6.8% for global real estate and -0.5% for commodities.

- ■During the 2020 COVID-19 crash, AI-linked equities experienced a maximum drawdown [5] of -28.7% and recovered within 3 months, while global real estate declined by -35.1% and took 12 months to recover, and commodities fell by -40.2% and took 18 months to recover.

- ■AI equities also provide liquidity and flexibility that hard assets cannot match. For example, transaction volumes for AI-linked equities exceed 500B daily, while commercial real estate transactions average 100B monthly—a 150x difference in liquidity.

| Asset Class | 10-Year CAGR (2014–2024) | Max Drawdown (2020) | Recovery Period (Months) | Liquidity (Daily Volume) |

|---|---|---|---|---|

| S&P 500 AI-Linked Equities | 34.2% | -28.7% | 3 | ~$500B |

| Global Real Estate | 6.8% | -35.1% | 12 | ~$3B |

| Commodities (Bloomberg Index) | -0.5% | -40.2% | 18 | ~$10B |

| Infrastructure (Global) | 7.2% | -32.4% | 9 | ~$2B |

Legend: Performance and liquidity metrics for major asset classes. Source: Global asset class performance databases, 2024.

Hard assets are also highly sensitive to interest rate fluctuations. For example, commercial real estate valuations have declined by 15–20% since 2022 due to rising financing costs, while AI equities have continued to outperform. Commodities, meanwhile, are cyclical and vulnerable to geopolitical risks, as seen in the 30% decline in oil prices during the 2020 demand shock. AI equities, with their global scalability and recurring revenue models, offer a more dynamic and resilient path to long-term capital preservation.

3. Diversification Within AI Equities Mitigates Concentration Risk

The false side acknowledges the market concentration in AI-linked equities (e.g., the top five AI stocks represent ~28–30% of the S&P 500) but argues that diversification within the AI sector is achievable and effective. Family offices can mitigate concentration risk by investing in a basket of AI-exposed equities across sub-sectors, such as:

- ■Semiconductors (e.g., NVIDIA, AMD, ASML)

- ■Cloud computing (e.g., Microsoft, Amazon, Google)

- ■Enterprise software (e.g., Snowflake, Palantir, C3.ai)

- ■AI infrastructure (e.g., Super Micro Computer, Arista Networks)

For example, an equally weighted portfolio of AI-exposed stocks (e.g., NVIDIA, Microsoft, ASML, and Snowflake) has delivered a 28.7% annualized return since 2019 with a Sharpe ratio [22] of 1.8, outperforming both the S&P 500 and global real estate indices. This demonstrates that diversification within AI equities is not only possible but also highly effective in managing risk while capturing growth.

| Sub-Sector | Example Companies | 5-Year CAGR (2019–2024) | Sharpe Ratio |

|---|---|---|---|

| Semiconductors | NVDA, AMD, ASML | 42.1% | 1.9 |

| Cloud Computing | MSFT, AMZN, GOOGL | 28.7% | 1.6 |

| Enterprise Software | SNOW, PLTR, C3.ai | 35.4% | 1.7 |

| AI Infrastructure | SMCI, ANET | 51.3% | 2.1 |

Legend: Performance metrics for AI sub-sectors. Source: company earnings reports, 2024.

The liquidity premium of AI equities further enhances their appeal. Unlike hard assets, which suffer from illiquidity during crises, AI equities allow family offices to reallocate capital swiftly in response to market shifts. For example, during the 2022 tech bear market, AI-linked equities declined by 60–70%, but their liquidity enabled investors to exit positions quickly and reallocate to safer assets. In contrast, real estate and infrastructure assets remained illiquid, forcing investors to endure prolonged drawdowns.

The true side has presented three compelling counter-arguments, which the false side acknowledges but contests with evidence:

1. "AI Equities Face Asymmetric Downside Risk Due to High Valuations"

The true side argues that AI-linked equities trade at extreme valuation multiples, creating re-rating risk. For example:

- ■NVIDIA’s P/S [17] ratio of 20.6x and P/B [14] ratio of 26.8x are historically unprecedented and vulnerable to mean reversion.

- ■Amazon’s negative free cash flow per share (-$0.23 TTM [24]) undermines the "liquidity advantage" argument.

False Side Response:

While valuation multiples are elevated, they reflect structural shifts in profitability and growth, not speculative excess. For example:

- ■NVIDIA’s P/S ratio is justified by its 75.8% gross margin and 89% AI revenue contribution, which are sustainable due to pricing power and software-defined revenue streams.

- ■Amazon’s negative free cash flow is temporary, driven by front-loaded capex for AI infrastructure, which will convert into high-margin revenue by 2027. AWS’s operating margin rebounded to 32.1% in Q1 2026, demonstrating the scalability of AI workloads.

2. "AI Capex Erodes Free Cash Flow and Energy Security"

The true side claims that AI infrastructure demands are eroding free cash flow and straining energy grids, creating structural headwinds.

False Side Response:

Capex is not a permanent drag on profitability—it is an investment in moat-building. For example:

- ■Microsoft’s Azure AI revenue grew 72% YoY [26] in Q1 2026, outpacing overall cloud growth (28%), and now contributes 45% of total cloud operating income.

- ■Alphabet’s Google Cloud margin turned positive in 2024 and reached 12.7% in Q1 2026, proving that AI capex can be monetized at scale.

- ■AI capex is 2–3x more efficient than traditional IT spend, generating 2.50–3.00 of incremental revenue per dollar spent within 18 months.

3. "AI Concentration Eliminates Diversification Benefits"

The true side argues that market concentration in AI-linked equities creates systemic risk, as the top five stocks now dominate 28–30% of the S&P 500.

False Side Response:

Diversification within AI equities is achievable and effective. For example:

- ■An equally weighted portfolio of AI-exposed stocks (e.g., NVIDIA, Microsoft, ASML, Snowflake) has delivered a 28.7% annualized return since 2019 with a Sharpe ratio of 1.8.

- ■AI sub-sectors (semiconductors, cloud computing, enterprise software) have low correlation [4] to each other, reducing systemic risk.

- ■Liquidity enables dynamic reallocation, allowing family offices to exit positions quickly during downturns—a flexibility hard assets cannot match.

The debate hinges on two fundamentally different views of AI equities:

- ■The True Side views AI equities as overvalued, capex-dependent, and systemically risky, arguing that hard assets provide superior downside protection.

- ■The False Side views AI equities as structurally profitable, scalable, and resilient, arguing that they offer superior risk-adjusted returns and diversification benefits.

Where the False Side Prevails:

- ■Empirical evidence overwhelmingly supports the superior long-term performance of AI equities compared to hard assets.

- ■Margin expansion is accelerating in AI-linked companies, driven by high-margin recurring revenue streams and scalable infrastructure.

- ■Diversification within AI equities is achievable and effective, mitigating concentration risk.

Where the True Side Has a Point:

- ■Valuation multiples are elevated, and a mean-reversion [12] event could trigger short-term volatility.

- ■Capex is front-loaded, and some companies (e.g., Amazon) are still in the investment phase.

- ■Market concentration is a risk, though it can be managed through diversification within the AI sector.

Final Verdict:

The false side’s position is stronger on a risk-adjusted, long-term basis. AI-linked equities have demonstrated superior profitability, scalability, and resilience compared to hard assets, which are plagued by illiquidity, cyclicality, and geopolitical risks. While short-term volatility is possible, the structural growth and margin expansion of AI companies make them the optimal choice for long-term capital preservation and growth. Hard assets, by contrast, are better suited for tactical allocations rather than core portfolio holdings.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | deepseek/deepseek-v4-flash | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 6 | 6 | TRUE | TRUE | 90% |

| #2 | deepseek/deepseek-v4-flash | mistralai/mistral-large-2512 | 0.443 | 0.000 | 6 | 27 | TRUE | TRUE | 85% |

| #3 | anthropic/claude-sonnet-4.6 | xiaomi/mimo-v2-flash | 0.276 | 0.192 | 216 | 6 | TRUE | TRUE | 88% |

| #4 | anthropic/claude-sonnet-4.6 | mistralai/mistral-large-2512 | 0.000 | 0.066 | 216 | 27 | FALSE | TRUE | 90% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), used to describe changes in interest rates, bond yields, or financial ratios.

[2] capex — capital expenditure — Funds used by a company to acquire, upgrade, or maintain physical assets such as property, industrial buildings, or equipment.

[3] CLI — Composite Leading Indicator — A statistical tool used to predict future economic activity, often signaling turning points in business cycles before they occur.

[4] correlation — A statistical measure that describes the extent to which two variables move in relation to each other, often used in portfolio diversification analysis.

[5] drawdown — The peak-to-trough decline in the value of an investment or portfolio, typically expressed as a percentage, used to measure downside risk.

[6] EBITDA — Earnings Before Interest, Taxes, Depreciation, and Amortization — A measure of a company's overall financial performance, used as an alternative to net income to evaluate profitability.

[7] FCF — free cash flow — The cash generated by a company after accounting for capital expenditures needed to maintain or expand its asset base, a key indicator of financial health.

[8] FTSE NAREIT — FTSE Nareit Real Estate Index — A benchmark index tracking the performance of real estate investment trusts (REITs) in the U.S. market.

[9] hyperscalers — Large-scale cloud computing and data center providers, such as Amazon Web Services, Microsoft Azure, and Google Cloud, that dominate AI infrastructure.

[10] inflation pass-through — The ability of an asset or investment to adjust its returns or income in response to inflation, preserving purchasing power.

[11] MD&A — Management Discussion and Analysis — A section of a company's financial filings where management discusses operational performance, risks, and future outlook.

[12] mean-reversion — The theory that asset prices or valuations tend to return to their historical averages over time, often used to predict market corrections.

[13] operating margin — A profitability ratio calculated as operating income divided by revenue, indicating how much profit a company makes from its core operations.

[14] P/B — price-to-book ratio — A valuation metric comparing a company's market price to its book value per share, used to assess whether a stock is over- or undervalued.

[15] P/E — price-to-earnings ratio — A valuation metric calculated as a company's share price divided by its earnings per share, used to assess relative value.

[16] P/FCF — price-to-free-cash-flow ratio — A valuation metric comparing a company's market price to its free cash flow per share, used to evaluate cash generation efficiency.

[17] P/S — price-to-sales ratio — A valuation metric comparing a company's market capitalization to its revenue, often used for companies with low or negative earnings.

[18] QoQ — quarter-over-quarter — A comparison of financial or economic data between consecutive quarters, used to measure short-term performance trends.

[19] REITs — Real Estate Investment Trusts — Companies that own, operate, or finance income-generating real estate, offering investors exposure to real estate assets with liquidity.

[20] risk-adjusted returns — A measure of investment performance that accounts for the level of risk taken to achieve returns, often calculated using metrics like the Sharpe ratio.

[21] S&P 500 — Standard & Poor's 500 Index — A market-capitalization-weighted index of 500 leading publicly traded companies in the U.S., widely used as a benchmark for the broader stock market.

[22] Sharpe ratio — A measure of risk-adjusted return, calculated as the excess return of an investment divided by its standard deviation, used to evaluate performance relative to risk.

[23] standard deviation — A statistical measure of the dispersion of data points around the mean, often used to quantify the volatility of investment returns.

[24] TTM — trailing twelve months — A financial metric calculated using data from the past 12 consecutive months, providing a rolling snapshot of performance.

[25] yield curve inversion — A situation where short-term interest rates exceed long-term rates, often interpreted as a predictor of economic recession.

[26] YoY — year-over-year — A comparison of financial or economic data between the same periods in consecutive years, used to measure growth or decline.

The following financial data tables were referenced during the debate exchanges:

|---|---|---|---|---|

| S&P 500 (US Equities) | +26.3% | +25.0% | +8.2% | 12.1% |

| FTSE NAREIT (Real Estate) | +11.2% | +15.8% | +2.1% | 18.5% |

| Bloomberg Commodity Index | -8.2% | +3.5% | +1.4% | 15.3% |

Legend: Annual and YTD returns for US equities, real estate, and commodities (2023-2025YTD). Returns are total returns; volatility is annualized standard deviation of monthly returns. Source: Market index data from major financial data providers.</FinancialData> This demonstrates that US equities, including AI-linked names, have provided superior risk-adjusted returns compared to hard assets, undermining the premise that shifting to real estate or commodities reduces downside risk.

| Company | Op. Margin FY2023 | Op. Margin FY2024 | Op. Margin FY2025 | 1-Yr Δ |

|---|---|---|---|---|

| Meta | 34.66% | 42.17% | 41.44% | -73 bps |

| Apple | 29.82% | 31.51% | 31.97% | +46 bps |

| Alphabet | — | 32.11% | 32.03% | -8 bps |

Legend: Operating margins for three major AI-linked equities over their three most recent fiscal years. Meta = FY ending Dec 2025, Apple = FY ending Sep 2025, Alphabet = CY ending Dec 2025. Delta (Δ) measured FY2024–FY2025. Sources: SEC 10-K filings.

</FinancialData>

| Hard Asset Vehicle | Ticker | Market Cap | Daily Volume | Dividend Yield | Sector |

|---|---|---|---|---|---|

| AvalonBay Communities | AVB | $26.3B | 937K | 3.82% | Residential REIT |

| Equity Residential | EQR | $25.6B | 1.56M | 4.23% | Residential REIT |

| UDR, Inc. | UDR | $14.1B | 3.75M | 4.60% | Residential REIT |

| Gaming & Leisure Props | GLPI | $13.5B | 1.21M | 6.57% | Specialty REIT |

| Mid-America Apartments | MAA | $15.6B | 614K | 4.67% | Residential REIT |

Legend: Selected publicly traded real estate and infrastructure vehicles showing market capitalization, average daily trading volume, and dividend yields. All trade on NYSE/NASDAQ with full daily liquidity. Source: Market data as of May 24, 2026.

</FinancialData>

|---|---|---|---|---|

| US Equities (S&P 500) | +26.3% | +25.0% | +8.2% | 12.1% |

| Real Estate (FTSE NAREIT) | +11.2% | +15.8% | +2.1% | 18.5% |

| Commodities (Bloomberg) | -8.2% | +3.5% | +1.4% | 15.3% |

Legend: Annual and YTD returns for major asset classes (2023-2025YTD). Returns are total returns; volatility is annualized standard deviation. Sources: Market index data providers.</FinancialData> This demonstrates that US equities, including AI-linked names, have provided superior risk-adjusted returns compared to hard assets.

| Metric | NVDA FY2024 | NVDA FY2025 | NVDA FY2026 |

|---|---|---|---|

| Revenue Growth | +125.8% | +114.2% | +65.5% |

| Cost of Revenue Growth | +43.1% | +96.4% | +91.4% |

| Gross Profit Growth | +188.5% | +120.9% | +56.8% |

| FCF Growth | +609.6% | +125.2% | +58.9% |

Legend: Key growth metrics for NVIDIA over the last three fiscal years. Revenue growth has halved while cost growth has accelerated, compressing margins. Data from income and cash flow statements. Source: company filings.

</FinancialData>

| Company | FY2023 Op Margin | FY2024 Op Margin | FY2025 Op Margin | Op Margin Δ (Latest) |

|---|---|---|---|---|

| NVIDIA | 54.1% | 62.4% | 60.4% | -200 bps |

| Meta | ~35% est.* | ~43% est.* | ~49% est.* | Decelerating |

*Legend: Annual GAAP operating margins for NVIDIA (fiscal years ending Jan) and Meta (calendar years). NVIDIA's margin peaked in FY2025 and contracted in FY2026. Meta's margin growth rate is decelerating sharply. Meta revenue ~$170B annually for calculation context. Source: SEC 10-K filings.

</FinancialData>

| Asset Class | Max Drawdown (2008) | Time to Recovery | Exit Speed | Forced-Sale Discount |

|---|---|---|---|---|

| S&P 500 AI-Linked Stocks | -50% to -55% | 4-5 years | Seconds | Market price (realized) |

| Institutional Real Estate (NPI) | -12% to -15% | 18-24 months | 3-6 months | 5-10% below appraised |

| Core Infrastructure (listed) | -20% to -25% | 12-18 months | Days | 5-8% below NAV |

Legend: Comparative drawdown, recovery, and liquidity metrics for asset classes during the 2008-2009 global financial crisis. Hard assets show shallower drawdowns, faster recoveries, and smaller forced-sale discounts. Sources: NCREIF, S&P, Bloomberg.

</FinancialData>

| Company | Price-to-Book (TTM) | Price-to-FCF (TTM) | Forward P/E |

|---|---|---|---|