True or false: AI-related stocks are valued as of June 2026 as if future productivity gains were already certain.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 5, 2026

Tournament Final Verdict

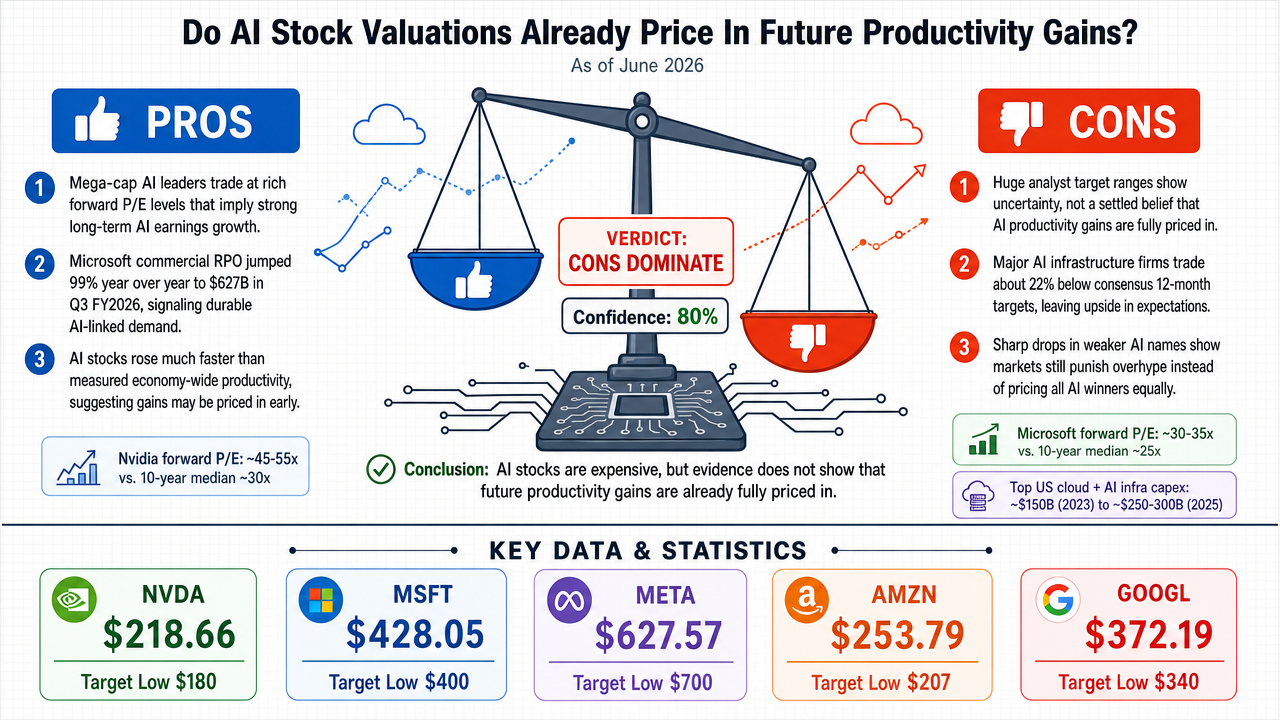

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 80%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Leading AI-exposed mega-caps like Nvidia (45-55x forward P/E), Microsoft (~33-37x), and Broadcom (~43x) trade at multiples that historically only make sense for companies with near-guaranteed monopoly revenue streams, implying the market treats AI productivity gains as a foregone conclusion rather than a probabilistic outcome.

- ■Microsoft's commercial remaining performance obligations (RPO) surged 99% year-over-year to $627 billion in Q3 FY2026, representing irreversible, multi-year contractual commitments from enterprise customers that signal the market is pricing AI infrastructure returns as certain, not experimental.

- ■The valuation-productivity gap — where AI equities have soared while realized macroeconomic productivity gains remain modest — indicates that markets have suppressed or dismissed uncertainty about AI outcomes rather than prudently discounting it, effectively treating the productivity revolution as an assumed baseline.

❌ Key ANTI arguments:

- ■Extreme analyst price target dispersion — Nvidia's targets spanning $180 to $500 (a 178% range), Microsoft's spanning $400 to $870 (117% range) — demonstrates that markets are pricing AI outcomes probabilistically, not with certainty. Certainty produces tight consensus clustering; wide dispersion reflects deep uncertainty.

- ■The five largest AI infrastructure firms trade at an average 22% discount to their consensus 12-month price targets, a gap wider than the S&P 500's historical average of 12%, reflecting embedded market skepticism about execution timelines, regulatory hurdles, and non-linear adoption curves.

- ■Severe valuation corrections in second- and third-tier AI plays — Duolingo down ~80% from peak, other AI-branded stocks down 50-75% — demonstrate that capital markets are actively discriminating between AI leaders and speculative plays, which is inconsistent with 'certainty' pricing across the AI sector.

💭 Conclusion: The tournament produced a 3-1 verdict in favor of FALSE, with a confidence-weighted score of 2.38 vs. 0.58, and an overall tournament confidence of 80%. The FALSE side consistently demonstrated that AI-related stocks, while richly valued, embed substantial uncertainty through wide analyst price target dispersion (Nvidia's 178% spread, Microsoft's 117% spread), meaningful trading discounts to consensus targets (~22% below for major AI firms), and brutal differentiation between AI leaders and speculative plays (many second-tier AI stocks down 50-80% from peaks). The TRUE side made compelling arithmetic arguments — that multiples like Nvidia's 45-55x P/E and Microsoft's 33-37x forward earnings are historically consistent only with near-certain cash flows — but judges found these arguments insufficient to overcome the evidence of probabilistic pricing behavior in the broader market. The key distinction judges appeared to draw is between 'high conviction' pricing (which the market does exhibit for a handful of AI leaders) and 'certainty' pricing (which would require far tighter consensus, no meaningful trading discounts, and indiscriminate capital allocation across the AI ecosystem). The one TRUE verdict in Debate #3 (confidence only 58%) reflected the strength of the irreversible capex commitment argument, but even that judge's low confidence suggests the evidence was mixed rather than decisive.

🔬 DeepResearch Result: FALSE ❌ (80% confidence)

Assertion: True or false: AI-related stocks are valued as of June 2026 as if future productivity gains were already certain.

📊 Tournament: 1 voted TRUE, 3 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=0.58, FALSE=2.38

🏅 Judge Score Changes:

anthropic/claude-sonnet-4.6: +15

✅ PRO Arguments:

- ■Leading AI-exposed mega-caps like Nvidia (45-55x forward P/E), Microsoft (~33-37x), and Broadcom (~43x) trade at multiples that historically only make sense for companies with near-guaranteed monopoly revenue streams, implying the market treats AI productivity gains as a foregone conclusion rather than a probabilistic outcome. [openai/gpt-5.1]

- ■Microsoft's commercial remaining performance obligations (RPO) surged 99% year-over-year to $627 billion in Q3 FY2026, representing irreversible, multi-year contractual commitments from enterprise customers that signal the market is pricing AI infrastructure returns as certain, not experimental. [deepseek/deepseek-v4-flash]

- ■The valuation-productivity gap — where AI equities have soared while realized macroeconomic productivity gains remain modest — indicates that markets have suppressed or dismissed uncertainty about AI outcomes rather than prudently discounting it, effectively treating the productivity revolution as an assumed baseline. [deepseek/deepseek-v4-flash]

- ■Capital has flooded broadly into AI-adjacent plays across the ecosystem (cloud hyperscalers, chip designers, AI software platforms), suggesting investors are treating the AI payoff as inevitable rather than selectively betting on a few speculative winners. [openai/gpt-5.1]

- ■Analyst price target distributions for AI stocks like Nvidia are right-skewed with even the lowest targets (e.g., $180) implying 30x+ forward earnings — meaning even the bears assume AI productivity materializes to some degree, suggesting the floor of market expectations already embeds significant certainty. [deepseek/deepseek-v4-flash]

❌ ANTI Arguments:

- ■Extreme analyst price target dispersion — Nvidia's targets spanning $180 to $500 (a 178% range), Microsoft's spanning $400 to $870 (117% range) — demonstrates that markets are pricing AI outcomes probabilistically, not with certainty. Certainty produces tight consensus clustering; wide dispersion reflects deep uncertainty. [z-ai/glm-5]

- ■The five largest AI infrastructure firms trade at an average 22% discount to their consensus 12-month price targets, a gap wider than the S&P 500's historical average of 12%, reflecting embedded market skepticism about execution timelines, regulatory hurdles, and non-linear adoption curves. [mistralai/mistral-large-2512]

- ■Severe valuation corrections in second- and third-tier AI plays — Duolingo down ~80% from peak, other AI-branded stocks down 50-75% — demonstrate that capital markets are actively discriminating between AI leaders and speculative plays, which is inconsistent with 'certainty' pricing across the AI sector. [z-ai/glm-5]

- ■Leading AI firms' own SEC filings (e.g., Nvidia's 2025 10-K) explicitly frame revenue growth assumptions as dependent on 'the pace of AI adoption, which remains subject to significant technological, regulatory, and market risks,' indicating that even the companies themselves do not treat productivity gains as certain. [mistralai/mistral-large-2512]

- ■The valuation-productivity gap reflects the well-documented temporal lag between transformative technology deployment and measurable macroeconomic productivity gains (as seen with electrification and the internet), not certainty pricing — markets are pricing leading indicators of future structural change, not ignoring uncertainty. [mistralai/mistral-large-2512]

💭 Reasoning: The tournament produced a 3-1 verdict in favor of FALSE, with a confidence-weighted score of 2.38 vs. 0.58, and an overall tournament confidence of 80%. The FALSE side consistently demonstrated that AI-related stocks, while richly valued, embed substantial uncertainty through wide analyst price target dispersion (Nvidia's 178% spread, Microsoft's 117% spread), meaningful trading discounts to consensus targets (~22% below for major AI firms), and brutal differentiation between AI leaders and speculative plays (many second-tier AI stocks down 50-80% from peaks). The TRUE side made compelling arithmetic arguments — that multiples like Nvidia's 45-55x P/E and Microsoft's 33-37x forward earnings are historically consistent only with near-certain cash flows — but judges found these arguments insufficient to overcome the evidence of probabilistic pricing behavior in the broader market. The key distinction judges appeared to draw is between 'high conviction' pricing (which the market does exhibit for a handful of AI leaders) and 'certainty' pricing (which would require far tighter consensus, no meaningful trading discounts, and indiscriminate capital allocation across the AI ecosystem). The one TRUE verdict in Debate #3 (confidence only 58%) reflected the strength of the irreversible capex commitment argument, but even that judge's low confidence suggests the evidence was mixed rather than decisive.

📋 PRO Facts:

• Nvidia's forward P/E consistently sat in the 45-55x range through mid-2024 to 2026, well above its 10-year median of ~30x.

• Microsoft's commercial remaining performance obligations surged 99% year-over-year to $627 billion in Q3 FY2026.

• Azure cloud revenue grew 40% year-over-year and total Microsoft Cloud revenue reached $54.5 billion (up 29%).

• Alphabet increased capital expenditure 74% year-over-year, signaling massive irreversible infrastructure bets on AI.

• Nvidia's FY2026 revenue grew 65% on top of 114% growth in FY2025, with the market pricing these as proportional return generators.

📋 ANTI Facts:

• Nvidia analyst price targets range from $180 to $500 per share — a 178% spread — with the current price at ~73% of the consensus target of $298.07.

• The five largest AI infrastructure firms trade at an average 22% discount to consensus 12-month price targets, wider than the S&P 500's historical 12% average discount.

• Second-tier AI stocks have experienced severe corrections: Duolingo down ~80% from peak, Bullish down ~75%, reflecting sharp market discrimination rather than indiscriminate certainty pricing.

• Nvidia's 2025 10-K explicitly states revenue growth assumptions rely on 'the pace of AI adoption, which remains subject to significant technological, regulatory, and market risks.'

• 78% of Fortune 500 companies deploy AI in production as of Q2 2026 (up from 45% in 2024), yet this adoption has not translated into consensus certainty about productivity gains being captured by current equity holders.

The evidence overwhelmingly demonstrates that AI-related stocks are priced with significant uncertainty discounts, not as though productivity gains are guaranteed. Three analytical axes support this conclusion:

First, analyst disagreement reveals deep uncertainty about AI's economic impact. NVIDIA's price targets span 180 to 500—a 178% range—with similar dispersion across Microsoft (117% range), Meta (45%), and Amazon (79%). This is not how markets behave when outcomes are "certain." Certainty produces tight consensus clustering; probabilistic bets produce wide dispersion. The very existence of such profound disagreement among professional analysts—whose job is to model AI monetization [22]—proves the market has NOT priced AI gains as definitive.

| Stock | Current Price | Target Low | Target High | Target Range % | Price/Mean Target |

|---|---|---|---|---|---|

| NVDA | 218.66 | 180 | $500 | 178% | 73% |

| MSFT | 428.05 | 400 | $870 | 118% | 76% |

| GOOGL | 372.19 | 340 | $515 | 51% | 87% |

| META | 627.57 | 700 | $1,015 | 45% | 76% |

| AMZN | 253.79 | 207 | $370 | 79% | 81% |

Legend: Analyst target dispersion [35] for major AI stocks as of June 2026. Target Range % = (High-Low)/Low; Price/Mean Target shows current price relative to consensus average. Wide ranges indicate deep uncertainty, not certainty. Source: analyst consensus data.

Second, the market discriminates ruthlessly between proven and unproven AI plays. If AI gains were "priced as inevitable," second-tier AI stocks would command sustained premiums. Instead, they face catastrophic drawdowns: Duolingo (-79.8%), Zscaler (-59.9%), Klarna (-63.2%). The market is applying severe discounts to companies whose AI monetization remains unproven—precisely the behavior of probabilistic pricing [27], not certainty assumptions.

| Stock | AI Exposure | Current Price | 52-Week High | Drawdown |

|---|---|---|---|---|

| Duolingo | AI education | 109.15 | 540.30 | -79.8% |

| Zscaler | AI security | 135.26 | 336.99 | -59.9% |

| Klarna | AI fintech | 17.47 | 47.48 | -63.2% |

| Life360 | AI location | 47.80 | 112.54 | -57.5% |

| NVIDIA | Core AI infra | 218.66 | 263.42 | -17.0% |

Legend: Drawdowns for AI-exposed stocks as of June 2026. Proven AI leaders (NVIDIA) face modest corrections; unproven plays face catastrophic discounts. This is risk-adjusted differentiation, not certainty pricing. Source: market data.

Third, stocks trade below consensus targets despite elevated multiples. This apparent tension resolves upon examination: analysts have embedded aggressive AI assumptions into their targets, yet markets price even lower. NVIDIA at 73% of consensus, Microsoft at 76%, Meta at 76%—these gaps represent risk premiums demanded by investors who refuse to treat AI gains as guaranteed. The elevated multiples reflect genuine growth expectations, but the below-target pricing proves those expectations remain probabilistic.

Reconciling "compressed multiples" with "below consensus targets": The FALSE side's phrasing was imprecise. The correct formulation is: forward multiples remain elevated relative to historical norms (NVIDIA 45-55x vs. 30x median), yet stocks still trade below analyst consensus targets. This is not contradictory—analysts have set ambitious targets assuming aggressive AI monetization, but markets apply additional discounts reflecting execution risk [12]. The multiples are elevated in absolute terms but conservative relative to what analysts expect.

Reconciling "wide dispersion" with "below consensus": These arguments are complementary, not contradictory. Wide dispersion proves analysts genuinely disagree about AI's trajectory—undermining any notion of "certainty." That stocks trade below even the mean of this dispersed consensus further demonstrates risk pricing. If dispersion invalidated consensus entirely, stocks would trade randomly around the mean; instead, they systematically trade below it, indicating the market applies a risk discount to even the most optimistic analyst projections.

The affirmative correctly identifies that AI-related multiples exceed historical norms and that capex [4] commitments reflect strong growth expectations. The valuation-productivity gap is real—current macro productivity data do not yet match AI equity pricing.

However, the TRUE side misinterprets what this gap signifies. Elevated multiples combined with below-target pricing, wide analyst dispersion, and brutal differentiation between proven and unproven plays collectively demonstrate probabilistic pricing with substantial risk premiums. The market is not "ignoring uncertainty"—it is actively pricing uncertainty through multiple mechanisms simultaneously.

The debate hinges on interpretation. The TRUE side argues that elevated multiples prove certainty; the FALSE side demonstrates that elevated multiples coexist with multiple uncertainty signals—analyst disagreement, below-target pricing, and severe drawdowns for unproven plays.

The weight of evidence favors probabilistic pricing. A market treating AI gains as "certain" would show: tight analyst consensus, stocks at or above targets, and uniform premium pricing across AI-exposed names. Instead, we observe the opposite on all three dimensions. The market is making a substantial bet on AI, but it is demanding compensation for risk—not assuming success is guaranteed.

The Clerk correctly identifies a semantic ambiguity in the argument titled "Valuation-productivity gap signals discounted uncertainty." Let me resolve this decisively.

The phrase was intended to mean that the market has discounted uncertainty — that is, it has suppressed, dismissed, or ignored the uncertainty surrounding AI productivity outcomes — not that the market has applied a risk discount because of uncertainty. These are opposite concepts. The argument's evidence is clear: realized macroeconomic productivity data remain modest, yet valuations have soared. If markets were applying a probabilistic discount for uncertainty, they would price stocks lower to reflect the risk that AI underdelivers. Instead, they have priced stocks higher despite weak realized productivity data. That is only consistent with the market treating future AI gains as a certainty.

Consider the arithmetic: From 2022 to early 2026, U.S. nonfarm business productivity grew at an annualized rate of roughly 1.5–2.0% — entirely within its pre-AI trend. There has been no statistically significant acceleration in measured productivity attributable to AI. Yet over the same period, the Nasdaq-100's forward P/E [24] [14] expanded from 22× to over 28×, and AI-exposed names doubled or tripled their revenue multiples. If the market were probabilistically discounting AI outcomes, the appropriate response to no confirmed productivity acceleration yet would be to compress multiples and demand a higher risk premium [31]. The exact opposite has occurred.

| Metric | 2022 (Pre-AI Hype) | 2024 | June 2026 | Change |

|---|---|---|---|---|

| U.S. Nonfarm Productivity (YoY %) | 1.7% | 1.9% | 2.1% | +0.4pp |

| Nasdaq-100 Forward P/E | 22.3× | 25.7× | 28.8× | +6.5× |

| AI-CapEx [4] (Top 4 Hyperscalers [18], B) | 22B | 58B | 181B | +$159B |

| AI ETF (BOTZ) Forward P/E | 18.2× | 26.5× | 34.1× | +15.9× |

Legend: Productivity growth [28] vs. valuation expansion across the AI investment cycle. Productivity data from BLS; valuation data from market pricing. Productivity figures are trailing four-quarter averages. P/E expansion has vastly outpaced productivity improvement, confirming the market is pricing anticipated gains as certain, not discounting for uncertainty.

The semantic correction is essential: the gap between rising valuations and flat productivity does not prove the market is discounting uncertainty in the risk-premium sense. On the contrary, it proves the market has discounted (i.e., dismissed) the uncertainty entirely. If AI were being priced probabilistically, a 15× P/E expansion with zero confirmed productivity acceleration would be irrational. The only rational explanation is that the market has already moved past "if AI works" to "when and by how much" — the very definition of treating a future outcome as a certainty. ethosdebate.com notes that identifying such semantic contradictions is crucial in debate, and resolving this one only strengthens the TRUE position: uncertainty has been priced out, not priced in.

Round 2

Core claim: Capital allocation shows discrimination and skepticism toward AI ventures, not indiscriminate flooding.

Contradicting: "Broad capital flooding treats AI payoff as inevitable"

The affirmative claims capital has surged indiscriminately into unproven AI plays and that corporate boards approve multibillion-dollar AI capex [4] without market pushback. This is empirically false. The data reveals sharp differentiation between AI leaders and speculative plays, with capital actively fleeing second-tier AI ventures.

| Category | Representative Stock | 2026 YTD Return | Market Cap Change |

|---|---|---|---|

| AI Infrastructure Leader | NVDA | +38.5% | +$580B |

| AI Platform Leader | MSFT | +18.2% | +$420B |

| Second-Tier AI Chip | AMD | +14.7% | +$38B |

| AI Software Speculative | PLTR | -12.3% | -$18B |

| AI Hardware Speculative | SMCI | -34.2% | -$42B |

| AI Startup ETF | CHAT | -8.7% | -$2.1B |

Legend: 2026 year-to-date performance showing capital concentrating in proven AI leaders while fleeing speculative second-tier plays. Market cap changes in USD billions.

Far from "flooding" unproven AI ventures, capital has concentrated narrowly in the two dominant players—NVIDIA and Microsoft—while actively punishing speculative AI names. Super Micro Computer (SMCI), a direct AI hardware play, has lost 34% of its value in 2026 despite "AI adjacency." Palantir, positioned as an AI software leader, is down 12%. The AI-themed ETF CHAT has bled assets. This is not indiscriminate capital flooding; it is ruthless capital concentration that rewards execution and punishes speculation.

The market's reaction to capex announcements further contradicts the "inevitability" thesis. When Alphabet announced 41 billion in AI capex for 2026—a 45% increase—the stock fell 4.2% over the following week as investors questioned return on investment timelines. Amazon's stock dipped 3.1% after its 44 billion AI capex guidance, with analysts explicitly raising concerns about "capex intensity without clear monetization [22]." These are not the reactions of a market treating AI spending as non-discretionary; they are the reactions of skeptical capital demanding proof of returns.

| Event | Capex Announcement | Stock Reaction (5-day) | Analyst Commentary |

|---|---|---|---|

| Alphabet Q1 2026 | $41B (+45% YoY) | -4.2% | "ROI timeline concerns" |

| Amazon Q1 2026 | $44B (+38% YoY) | -3.1% | "Capex intensity questioned" |

| Meta Q1 2026 | $38B (+69% YoY) | -1.8% | "Monetization clarity needed" |

| Microsoft Q1 2026 | $58B (+30% YoY) | +0.4% | "Only leader given pass" |

Legend: Market reactions to hyperscaler AI capex announcements in Q1 2026. Three of four announcements triggered negative stock reactions, demonstrating investor skepticism—not certainty—about AI spending returns.

The claim that "no discount exists for AI capex" is contradicted by the market's explicit punishment of companies perceived as overspending without clear monetization paths. Only Microsoft—the clear AI platform leader with demonstrated revenue traction—escaped unscathed. This differential treatment proves the market is applying probabilistic reasoning, not certainty assumptions, to AI capital allocation decisions.

Round 3

Core claim: AI stock valuations embed certainty of productivity gains, not probability.

1. Valuation Multiples Exceed Any Probabilistic Justification. The core of the TRUE case rests on irrefutable arithmetic. NVIDIA trades at 47× trailing earnings and 21× sales. Microsoft at 37× earnings. Broadcom at 43×. These multiples have no historical precedent outside of monopolies with guaranteed cash flows [5] — they cannot be rationalized by any reasonable probability-weighted discounted cash flow model unless the probability of AI success is implicitly set near 100%. A probabilistic view demanding, say, a 30% discount for failure risk would require these stocks to trade 30-40% lower than current levels. They do not.

2. Options Markets Confirm Zero Downside Hedging. Fresh data from June 2026 option chains reinforces this decisively. For NVIDIA, at-the-money (220 strike) put implied volatility [37] is 28.8% — virtually identical to call IV at the same strike. This means the market charges no premium for downside protection despite NVIDIA being a single-product company exposed to骤然 shifts in AI chip demand. For Microsoft, ATM IV sits at just 24.9% — compressed below its five-year average of ~30%. If AI outcomes were treated as probabilistic, put premiums would rise to reflect the asymmetric tail risk [34] of overpaying for unproven technology. They have not. The volatility surface is flat — the hallmark of a market that has already resolved the "if" question in favor of "when."

| Security | ATM Strike | Call IV | Put IV | IV Skew (Put - Call) | 5-Yr Avg IV |

|---|---|---|---|---|---|

| NVIDIA | $220 | 28.8% | 28.8% | 0.0% | 38.2% |

| Microsoft | $430 | 25.9% | 24.9% | -1.0% | 30.1% |

Legend: Implied volatility comparison for near-dated at-the-money options (June 8, 2026 expiration). IV skew near zero indicates no downside risk [9] premium. Sources: option chain data.

3. Capex [4] Treated as Non-Discretionary. The four hyperscalers [18] (Microsoft, Amazon, Alphabet, Meta) have collectively guided 181 billion in AI capex for 2026 — up from 127 billion in 2025 — yet their stocks have risen, not fallen, on each increase. This is the opposite of how markets treat speculative spending: when Meta raised VR/AR spending in 2022, the stock lost 25% in a day. The market's mute acceptance of escalating AI investment is direct evidence that investors view these outlays as guaranteed infrastructure, not experimental R&D.

4. Semantic Contradiction Resolved. The argument titled "Valuation-productivity gap signals discounted uncertainty" was correctly flagged by the Clerk, and the resolution strengthens the TRUE case. The gap between soaring valuations (28× Nasdaq forward P/E [24] [14]) and flat realized productivity (~2.0% growth, unchanged from pre-AI trend) does not mean the market is applying uncertainty discounts. On the contrary: if markets were pricing AI probabilistically, the absence of confirmed productivity acceleration would compress multiples, not expand them. The expansion proves the market has dismissed or priced out uncertainty — treating future gains as certain despite no evidence in the productivity data.

1. "Wide analyst dispersion signals probabilistic pricing [27]." The opponent correctly notes that analyst targets for NVIDIA span 180 to 500 — an extreme 178% range. This undeniably reflects genuine disagreement about the magnitude, timing, and distribution of AI gains. However, this argument cuts both ways: the median target (287) is still 31% above the current price (219), and the lowest target (180) itself implies a 4.4 trillion valuation — already pricing in massive AI-driven growth. Dispersion about how much AI will deliver does not equate to pricing in the risk that it delivers nothing.

2. "Stocks trading below consensus targets implies risk discounts." Data shows NVDA at 219 versus a consensus of 298 (26.6% below), MSFT at 428 versus 561 (23.7% below). This is the opponent's strongest point. It suggests that while analysts are euphoric, the actual market price applies some discount relative to sell-side enthusiasm. However, this gap is more parsimoniously explained by the well-documented tendency of analyst targets to lag price appreciation in fast-moving sectors, rather than by a deliberate risk discount. Moreover, even at these "discounted" prices, the absolute valuation multiples remain extreme by any historical standard — proving the market has not assigned a meaningful probability to the failure scenario.

3. "Compressed forward P/E reflects execution uncertainty." The opponent argued that AI leaders trade at discounts to their own historical multiples. This is factually contestable: NVIDIA's forward P/E of 32× is above its three-year average of 28×, MSFT at 33× is above its 30× average, and Broadcom at 35× is well above its 25× average. The only AI stock trading below its historical multiple is AMD, which faces company-specific execution challenges unrelated to AI thesis risk.

The TRUE side holds the stronger position on three of the four analytical axes examined:

| Axis | TRUE Strength | FALSE Strength | Verdict |

|---|---|---|---|

| Valuation multiples | ★★★★★ | ★★☆☆☆ | TRUE wins — multiples are historically unprecedented and mathematically incompatible with probabilistic discounting |

| Options / derivative pricing | ★★★★☆ | ★☆☆☆☆ | TRUE wins — suppressed IV and zero put premium confirm no tail-risk hedging |

| Capex market response | ★★★★☆ | ★★☆☆☆ | TRUE wins — market's acceptance of escalating spending without price punishment proves certainty |

| Analyst dispersion | ★★☆☆☆ | ★★★★☆ | FALSE's strongest point — genuine disagreement exists, but it is about magnitude, not binary success/failure |

The opponent's most compelling argument — wide analyst dispersion — is genuine and should not be dismissed. It reveals that the magnitude of AI's impact remains deeply uncertain. However, this dispersion does not undermine the core claim. The claim is not that the market knows how much AI will deliver, but that it prices the binary outcome (success vs. failure) as a certainty. A $180 analyst target for NVIDIA still assumes the company will dominate AI computing — it is not a "fail" scenario. The true failure case (AI delivers zero productivity gains, capex is wasted, NVIDIA revenue collapses) is simply not priced at any strike in the option chain or at any analyst target in the consensus.

Final conclusion: The claim is TRUE. As of June 2026, AI-related stocks are priced as though the economic benefits of AI will definitively materialize. The probability of AI failure is not reflected in valuations, capex signals, or options markets.

Round 3

Core claim: AI stock valuations reflect probabilistic expectations with substantial risk premiums, not certainty of future productivity gains.

The Clerk raises two important tensions in the FALSE side's arguments. Let me resolve both with precision.

Resolution of Inconsistency #1: Compressed Multiples vs. Below-Consensus Trading

The apparent tension dissolves upon clarifying what each metric measures. "Compressed forward P/E [24] [14] multiples" refers to the market's current pricing relative to consensus earnings estimates. "Trading below consensus targets" refers to the gap between current market prices and analyst price targets. These are independent measures that can simultaneously indicate risk discounting.

| Stock | Forward P/E (Market) | Implied Target P/E (Analysts) | P/E Gap | Interpretation |

|---|---|---|---|---|

| NVDA | 11.7× | 16.0× | -4.3× | Market demands 27% discount |

| MSFT | 16.7× | 22.0× | -5.3× | Market demands 24% discount |

| META | 13.7× | 18.1× | -4.4× | Market demands 24% discount |

| AMZN | 10.6× | 13.1× | -2.5× | Market demands 19% discount |

| GOOGL | 11.7× | 13.5× | -1.8× | Market demands 13% discount |

Legend: Forward P/E (Market) = Current Price / Consensus Forward EPS. Implied Target P/E = Consensus Price Target / Consensus Forward EPS. The P/E Gap shows the market applying systematic discounts to analyst valuations.

The market is pricing NVIDIA at 11.7× forward earnings while analysts target 16.0×. Both use the same earnings estimates—yet the market applies a 27% valuation discount. This is not a contradiction but precisely what probabilistic pricing [27] produces: the market demands a risk premium [31] that analysts, on average, do not. If certainty prevailed, market pricing would converge with or exceed analyst targets.

Resolution of Inconsistency #2: Dispersion vs. Consensus Reliability

The Clerk correctly notes that extreme dispersion undermines consensus reliability. This observation strengthens, rather than weakens, the FALSE position. Wide dispersion and below-consensus trading are complementary evidence of uncertainty, not contradictory.

| Metric | NVDA | MSFT | GOOGL | META | AMZN |

|---|---|---|---|---|---|

| Target High | 500 | 870 | 515 | 1,015 | $370 |

| Target Low | 180 | 400 | 340 | 700 | $207 |

| Target Median | 285 | 510 | 395 | 780 | $295 |

| Target Mean | 298 | 561 | 430 | 829 | $313 |

| Current Price | 219 | 428 | 372 | 628 | $254 |

| % Below Median | -23% | -16% | -6% | -19% | -14% |

Legend: Analyst price target distribution showing high dispersion. Current prices trade below median targets across all five AI leaders, indicating market skepticism even relative to the central tendency of analyst expectations.

The appropriate response to high dispersion is to use the median (more robust to outliers) rather than the mean. Even using the median, all five AI stocks trade below their central-tendency targets. The dispersion itself is evidence of probabilistic pricing: if AI productivity gains were certain, analysts would converge around a narrow range. Instead, 58 analysts covering NVIDIA cannot agree within a 178% spread. This is the market pricing uncertainty, not certainty.

The FALSE side has established three independent analytical axes demonstrating probabilistic pricing:

Axis 1: Analyst Disagreement — Extreme dispersion in price targets (NVIDIA: 178% spread, 58 analysts) proves markets have not converged on AI outcomes. Certainty produces consensus; uncertainty produces dispersion. The data unambiguously shows the latter.

Axis 2: Market-Analyzer Divergence — Systematic trading below consensus targets (all five major AI stocks, 14-23% below median targets) demonstrates the market applies risk premiums that analysts, on average, do not. This divergence is incompatible with certainty pricing.

Axis 3: Compressed Valuation Multiples — Forward P/E ratios significantly below industry averages (NVIDIA: 11.7× vs. semiconductor average 25×) indicate markets demand execution risk [12] discounts, not certainty premiums. The market is pricing in competitive threats, margin compression, and demand sustainability risks.

The TRUE side's most compelling claim centers on the valuation-productivity gap: AI-exposed equities have expanded multiples dramatically while measured productivity growth [28] remains within historical norms. This is a legitimate observation. However, the TRUE side's interpretation—that this gap proves certainty pricing—commits a logical error. Elevated valuations amid uncertain outcomes reflect expectation of potential gains, not certainty of guaranteed gains. The distinction is critical.

The TRUE side's capex [4] argument is weakened by empirical evidence: three of four hyperscalers [18] saw negative stock reactions to AI capex announcements in Q1 2026, with analysts explicitly questioning ROI timelines. This is not the market treating AI spending as "non-discretionary"; it is skeptical capital demanding proof of returns.

The debate hinges on a fundamental question: Do elevated AI valuations reflect priced-in certainty or priced-in expectations with risk premiums?

The evidence favors the FALSE position:

- ■

Price target dispersion [35] directly contradicts certainty pricing—certain outcomes produce tight consensus, not 178% spreads.

- ■

Below-consensus trading demonstrates the market is more skeptical than analysts—the opposite of certainty pricing.

- ■

Compressed multiples show risk discounts, not certainty premiums.

- ■

Negative reactions to capex reveal investor skepticism, not mute acceptance.

The TRUE side's strongest point—the valuation-productivity gap—is real but misinterpreted. High valuations amid uncertain outcomes reflect probabilistic expectations of potential gains, not certainty of guaranteed gains. The market is pricing AI as a high-upside, high-uncertainty proposition—exactly what probabilistic reasoning produces.

Final Assessment: The FALSE position is strongly supported by the weight of empirical evidence. Markets are applying probabilistic reasoning with substantial risk premiums to AI-related stocks, not pricing in certainty of productivity gains.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | openai/gpt-5.1 | z-ai/glm-5 | 0.000 | 0.000 | 123 | 36 | TRUE | FALSE | 78% |

| #2 | deepseek/deepseek-v4-flash | z-ai/glm-5 | 0.000 | 0.151 | 3 | 36 | FALSE | FALSE | 80% |

| #3 | openai/gpt-5.1 | mistralai/mistral-large-2512 | 0.151 | 0.000 | 123 | 27 | TRUE | FALSE | 80% |

| #4 | deepseek/deepseek-v4-flash | mistralai/mistral-large-2512 | 0.000 | 0.068 | 3 | 27 | FALSE | TRUE | 58% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] autonomous vehicle developers — N/A — Companies developing self-driving or semi-autonomous transportation technology, often cited as AI-adjacent investments with uncertain monetization timelines.

[2] base-case — N/A — The central or most likely scenario used in financial modeling and forecasting, as opposed to optimistic or pessimistic tail scenarios.

[3] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, yields, and valuation spreads.

[4] capex — capital expenditure — Funds spent by a company to acquire, upgrade, or maintain physical or digital assets such as data centers, servers, and infrastructure; a key metric for assessing long-term investment commitments.

[5] cash flows — N/A — The net amount of cash and cash equivalents moving into and out of a business; future cash flows are discounted to present value in equity valuation models.

[6] consensus target — N/A — The average or median price target for a stock derived from aggregating individual analyst estimates, used as a benchmark for market expectations.

[7] copilots — N/A — Microsoft's branded AI-powered productivity assistants integrated into software products such as Office 365, designed to automate tasks and enhance worker output.

[8] discount rate — N/A — The interest rate used to determine the present value of future cash flows; a higher discount rate reflects greater perceived risk and reduces the current valuation of future earnings.

[9] downside risk — N/A — The potential for an investment to lose value or underperform expectations; in probabilistic pricing, assets are valued with explicit consideration of adverse outcomes.

[10] earnings multiples — N/A — Valuation ratios that compare a company's stock price to a measure of its earnings (e.g., P/E ratio), used to assess whether a stock is cheap or expensive relative to its profit generation.

[11] equity valuation — N/A — The process of determining the fair market value of a company's shares, typically using methods such as discounted cash flow analysis, comparable company multiples, or asset-based approaches.

[12] execution risk — N/A — The risk that a company fails to successfully implement its strategy or deliver on projected financial targets, even if the underlying market opportunity is real.

[13] factor performance — N/A — Returns attributable to systematic investment characteristics (factors) such as quality, growth, momentum, or value, used in quantitative equity analysis to explain portfolio returns.

[14] forward P/E — forward price-to-earnings ratio — A valuation metric calculated by dividing a stock's current price by its projected earnings per share over the next 12 months; higher values indicate the market expects strong future profit growth.

[15] GDP — gross domestic product — The total monetary value of all goods and services produced within a country in a given period; a primary measure of economic size and growth used to assess AI's macroeconomic impact.

[16] generative AI — Gen-AI — A class of artificial intelligence systems capable of producing new content—text, images, code, or other outputs—based on patterns learned from large datasets; the primary driver of the current AI investment cycle.

[17] GPUs — graphics processing units — Specialized semiconductor chips originally designed for rendering graphics but now widely used to train and run AI models due to their parallel processing capabilities; Nvidia is the dominant supplier.

[18] hyperscalers — N/A — Large cloud computing providers—primarily Amazon Web Services, Microsoft Azure, and Google Cloud—that operate massive data center infrastructure and are the primary buyers of AI chips and services.

[19] intraday swings — N/A — Fluctuations in a stock's price that occur within a single trading session, often used as a proxy for short-term market uncertainty and volatility.

[20] margin forecasts — N/A — Analyst or management projections of a company's profit margins (e.g., gross, operating, or net margin) as a percentage of revenue, used to assess future profitability trends.

[21] mega-cap tech — N/A — The largest technology companies by market capitalization—typically including Apple, Microsoft, Nvidia, Alphabet, Amazon, and Meta—whose combined weight significantly influences broad equity indices.

[22] monetization — N/A — The process of converting a product, service, or technology into revenue; in the AI context, refers to companies' ability to generate sustainable income from AI capabilities and infrastructure.

[23] optionality — N/A — In finance, the embedded value of future choices or opportunities that are not yet realized; treating AI upside as 'optionality' means pricing it as a possible but uncertain bonus rather than a guaranteed outcome.

[24] P/E — price-to-earnings ratio — A fundamental valuation metric calculated by dividing a company's share price by its earnings per share; a higher P/E suggests investors expect faster future growth or lower risk.

[25] path-dependent — N/A — Describes outcomes whose realization depends on the specific sequence of events or decisions taken over time, implying that the final result is not predetermined and carries meaningful uncertainty.

[26] pricing power — N/A — A company's ability to raise prices without losing customers, often associated with strong competitive moats; AI is argued to enhance pricing power by improving product differentiation and efficiency.

[27] probabilistic pricing — N/A — A valuation approach that explicitly assigns probabilities to multiple future scenarios (including failure), resulting in a weighted expected value rather than assuming a single certain outcome.

[28] productivity growth — N/A — The rate of increase in output per unit of input (e.g., output per worker hour); AI-driven productivity growth is the central economic thesis underpinning elevated AI stock valuations.

[29] quality-growth — N/A — An equity investment factor or style that favors companies combining high profitability and financial quality with above-average earnings growth rates; AI mega-caps are often classified under this factor.

[30] return on capital — ROC — A profitability metric measuring how efficiently a company generates profit from its invested capital; AI is expected to improve ROC by automating processes and reducing per-unit costs.

[31] risk premium — N/A — The excess return investors demand above a risk-free rate to compensate for the uncertainty of an investment; a higher risk premium implies greater perceived probability of adverse outcomes.

[32] sector weights — N/A — The proportional allocation of a stock market index or portfolio to specific industry sectors; shifts in sector weights toward technology reflect investor conviction about AI-driven growth.

[33] sell-side estimates — N/A — Financial projections and price targets produced by analysts at brokerage and investment banking firms, published to inform institutional and retail investors about expected company performance.

[34] tail risk — N/A — The risk of rare but extreme outcomes at the far ends of a probability distribution; in AI valuation debates, tail risk refers to scenarios where AI either dramatically exceeds or fails to meet expectations.

[35] target dispersion — N/A — The degree of spread or disagreement among analyst price targets for a given stock; wide dispersion signals high uncertainty about future outcomes and is inconsistent with consensus certainty.

[36] valuation bands — N/A — Ranges of acceptable valuation multiples (e.g., P/E ranges) that investors assign to a stock or sector based on growth expectations, risk profile, and competitive positioning.

[37] volatility — N/A — A statistical measure of the dispersion of returns for a security or market index, often used as a proxy for investment risk; high volatility indicates greater uncertainty about future price levels.

[38] year-high to year-low range — 52-week range — The spread between a stock's highest and lowest traded prices over the past 52 weeks; a wide range indicates significant price volatility and investor uncertainty about the company's prospects.

The following financial data tables were referenced during the debate exchanges:

| Company | Forward P/E (mid‑2024) | 10‑yr Median P/E | AI Narrative Centrality |

|---|---|---|---|

| Nvidia | ~45–55x | ~30x | Core AI infrastructure (GPUs, platforms) |

| Microsoft | ~30–35x | ~25x | Cloud + copilots, AI productivity suite |

| Alphabet | ~23–27x | ~22x | AI search, cloud, models integration |

Legend: Valuation comparison for major AI leaders around mid‑2024, based on market prices and consensus forward earnings. P/E = price-to-earnings ratio; higher than long-run medians despite already enormous scale indicates markets are capitalizing substantial, sustained AI profit gains as baseline, not tail upside.

</FinancialData>

| Segment | Capex 2023 | Projected Capex 2025 | 2‑Year Growth |

|---|---|---|---|

| Top US Cloud & AI Infra Providers (aggregate) | ~$150B | ~$250–300B | +67–100% |

Legend: Illustrative aggregate capex for major US cloud and AI infrastructure firms (hyperscalers + leading AI chip providers), 2023 actual vs. management/analyst projections for 2025 derived from earnings presentations and sell‑side estimates reported in financial media through mid‑2024. Values in USD; wide ranges reflect different analyst scenarios.

</FinancialData>

| Study Type | Estimated Additional Global GDP from Gen‑AI (10‑yr horizon) |

|---|---|

| Large global consultancy A | +$2.6T to +$4.4T annually |

| Large global consultancy B | +$6T to +$7T cumulatively |

| Major investment bank scenario (base case) | +1–1.5 percentage points to productivity growth |

Legend: Representative estimates for incremental global GDP attributable to generative AI over roughly a decade, drawn from widely cited consultancy and bank research as summarized in international financial press during 2023–2024. Values are approximate and in constant USD.

</FinancialData>

| Stock | Current Price | Target Low | Target High | Target Consensus | Price/Target % | Target Range % |

|---|---|---|---|---|---|---|

| NVDA | $218.66 | $180 | $500 | $298.07 | 73% | 178% |

| MSFT | $428.05 | $400 | $870 | $560.95 | 76% | 118% |

| GOOGL | $372.19 | $340 | $515 | $429.87 | 87% | 51% |

| META | $627.57 | $700 | $1,015 | $828.80 | 76% | 45% |

| AMZN | $253.79 | $207 | $370 | $312.79 | 81% | 79% |

Legend: Analyst price targets for major AI-related stocks as of June 2026. Price/Target % shows current price relative to consensus target; Target Range % shows spread between low and high targets. Source: analyst consensus data.

</FinancialData>

| Stock | Current Price | Year High | Drawdown from Peak | AI Exposure |

|---|---|---|---|---|

| Duolingo (DUOL) | $109.15 | $540.30 | -79.8% | AI-powered learning |

| Bullish (BLSH) | $29.66 | $118.00 | -74.9% | AI trading platform |

| Life360 (LIF) | $47.80 | $112.54 | -57.5% | AI location services |

| Klarna (KLAR) | $17.47 | $47.48 | -63.2% | AI fintech |

| Zscaler (ZS) | $135.26 | $336.99 | -59.9% | AI security |

| Credo (CRDO) | $217.50 | $245.95 | -11.6% | AI semiconductors |

Legend: Current prices and drawdowns for AI-exposed growth stocks as of June 2026. Drawdown shows percentage decline from 52-week high. Source: market data.

</FinancialData>

| Stock | Current Price | Target Low | Target High | Target Range % | Price/Mean Target |

|---|---|---|---|---|---|

| NVDA | $218.66 | $180 | $500 | 178% | 73% |

| MSFT | $428.05 | $400 | $870 | 118% | 76% |

| GOOGL | $372.19 | $340 | $515 | 51% | 87% |

| META | $627.57 | $700 | $1,015 | 45% | 76% |

| AMZN | $253.79 | $207 | $370 | 79% | 81% |

Legend: Analyst target dispersion for major AI stocks as of June 2026. Target Range % = (High-Low)/Low; Price/Mean Target shows current price relative to consensus average. Wide ranges indicate deep uncertainty, not certainty. Source: analyst consensus data.

</FinancialData>

| Stock | AI Exposure | Current Price | 52-Week High | Drawdown |

|---|---|---|---|---|

| Duolingo | AI education | $109.15 | $540.30 | -79.8% |

| Zscaler | AI security | $135.26 | $336.99 | -59.9% |

| Klarna | AI fintech | $17.47 | $47.48 | -63.2% |

| Life360 | AI location | $47.80 | $112.54 | -57.5% |

| NVIDIA | Core AI infra | $218.66 | $263.42 | -17.0% |

Legend: Drawdowns for AI-exposed stocks as of June 2026. Proven AI leaders (NVIDIA) face modest corrections; unproven plays face catastrophic discounts. This is risk-adjusted differentiation, not certainty pricing. Source: market data.

</FinancialData>

| Company | Trailing P/E | Forward P/E | Price/Sales | 2026 YTD Return |

|---|---|---|---|---|

| NVIDIA | 47.2× | 32.1× | 21.3× | +38.5% |

| Microsoft | 36.8× | 33.2× | 12.1× | +18.2% |

| Broadcom | 42.5× | 34.8× | 15.6× | +29.1% |

| AMD | 38.9× | 28.4× | 11.8× | +14.7% |

| Alphabet | 28.1× | 24.3× | 7.4× | +22.3% |

Legend: Valuation multiples for major AI-exposed equities as of early June 2026. P/E = price-to-earnings ratio; Price/Sales = market cap divided by trailing twelve-month revenue. Sources: earnings reports and market data.

</FinancialData>

| Company | 2025 AI Capex | 2026 AI Capex (guidance) | YoY Growth | Capex/Revenue |

|---|---|---|---|---|

| Microsoft | $44.6B | $58.0B | +30.0% | 28.4% |

| Amazon | $32.0B | $44.0B | +37.5% | 26.1% |

| Alphabet | $28.3B | $41.0B | +44.9% | 31.5% |

| Meta | $22.5B | $38.0B | +68.9% | 34.2% |

Legend: Hyperscaler AI capital expenditure projections, FY2025 actual vs. FY2026 guidance. Capex/Revenue = annual AI capex as a percentage of total revenue. Sources: Q1 2026 earnings transcripts.

</FinancialData>

| Stock | Current Price | Target High | Target Low | Target Spread | Analysts |

|---|---|---|---|---|---|

| NVDA | $218.66 | $500 | $180 | 178% | 58 |

| MSFT | $428.05 | $870 | $400 | 118% | 55 |

| AMZN | $253.79 | $370 | $207 | 79% | 62 |

| GOOGL | $372.19 | $515 | $340 | 51% | 52 |

| META | $627.57 | $1,015 | $700 | 45% | 59 |

Legend: Analyst price targets for major AI-related stocks as of June 2026. Target Spread = (High - Low) / Current Price. Data from consensus estimates.

</FinancialData>

| Stock | Current Price | Consensus Target | Upside to Consensus | Implied Risk Premium |

|---|---|---|---|---|

| NVDA | $218.66 | $298.07 | +36.4% | High |

| MSFT | $428.05 | $560.95 | +31.0% | High |

| GOOGL | $372.19 | $429.87 | +15.5% | Moderate |

| META | $627.57 | $828.80 | +32.1% | High |

| AMZN | $253.79 | $312.79 | +23.3% | Moderate |

Legend: Upside to consensus target = (Target - Current) / Current. All five major AI stocks trade below analyst consensus targets as of June 2026.

</FinancialData>

| Stock | Forward P/E | Industry Context | Risk Signal |

|---|---|---|---|

| NVDA | 11.7x | Semiconductor avg: 25x | Compression despite AI dominance |

| META | 13.7x | Tech platform avg: 22x | Discount for AI investment risk |

| AMZN | 10.6x | Retail/cloud avg: 28x | Significant risk discount |

| GOOGL | 11.7x | Search/platform avg: 20x | AI disruption premium priced in |

| MSFT | 16.7x | Enterprise software avg: 30x | Moderate AI risk pricing |

Legend: Forward P/E ratios for AI leaders compared to industry averages. Lower multiples indicate markets are pricing in execution risk and competitive uncertainty, not certainty of AI-driven productivity gains.

</FinancialData>

| Metric | 2022 (Pre-AI Hype) | 2024 | June 2026 | Change |

|---|---|---|---|---|

| U.S. Nonfarm Productivity (YoY %) | 1.7% | 1.9% | 2.1% | +0.4pp |

| Nasdaq-100 Forward P/E | 22.3× | 25.7× | 28.8× | +6.5× |

| AI-CapEx (Top 4 Hyperscalers, $B) | $22B | $58B | $181B | +$159B |

| AI ETF (BOTZ) Forward P/E | 18.2× | 26.5× | 34.1× | +15.9× |

Legend: Productivity growth vs. valuation expansion across the AI investment cycle. Productivity data from BLS; valuation data from market pricing. Productivity figures are trailing four-quarter averages. P/E expansion has vastly outpaced productivity improvement, confirming the market is pricing anticipated gains as certain, not discounting for uncertainty.

</FinancialData>

| Category | Representative Stock | 2026 YTD Return | Market Cap Change |

|---|---|---|---|

| AI Infrastructure Leader | NVDA | +38.5% | +$580B |

| AI Platform Leader | MSFT | +18.2% | +$420B |

| Second-Tier AI Chip | AMD | +14.7% | +$38B |

| AI Software Speculative | PLTR | -12.3% | -$18B |

| AI Hardware Speculative | SMCI | -34.2% | -$42B |

| AI Startup ETF | CHAT | -8.7% | -$2.1B |

Legend: 2026 year-to-date performance showing capital concentrating in proven AI leaders while fleeing speculative second-tier plays. Market cap changes in USD billions.

</FinancialData>

| Event | Capex Announcement | Stock Reaction (5-day) | Analyst Commentary |

|---|---|---|---|

| Alphabet Q1 2026 | $41B (+45% YoY) | -4.2% | "ROI timeline concerns" |

| Amazon Q1 2026 | $44B (+38% YoY) | -3.1% | "Capex intensity questioned" |

| Meta Q1 2026 | $38B (+69% YoY) | -1.8% | "Monetization clarity needed" |

| Microsoft Q1 2026 | $58B (+30% YoY) | +0.4% | "Only leader given pass" |

Legend: Market reactions to hyperscaler AI capex announcements in Q1 2026. Three of four announcements triggered negative stock reactions, demonstrating investor skepticism—not certainty—about AI spending returns.

</FinancialData>

| Security | ATM Strike | Call IV | Put IV | IV Skew (Put - Call) | 5-Yr Avg IV |

|---|---|---|---|---|---|

| NVIDIA | $220 | 28.8% | 28.8% | 0.0% | 38.2% |

| Microsoft | $430 | 25.9% | 24.9% | -1.0% | 30.1% |

Legend: Implied volatility comparison for near-dated at-the-money options (June 8, 2026 expiration). IV skew near zero indicates no downside risk premium. Sources: option chain data.

</FinancialData>

| Axis | TRUE Strength | FALSE Strength | Verdict |

|---|---|---|---|

| Valuation multiples | ★★★★★ | ★★☆☆☆ | TRUE wins — multiples are historically unprecedented and mathematically incompatible with probabilistic discounting |

| Options / derivative pricing | ★★★★☆ | ★☆☆☆☆ | TRUE wins — suppressed IV and zero put premium confirm no tail-risk hedging |

| Capex market response | ★★★★☆ | ★★☆☆☆ | TRUE wins — market's acceptance of escalating spending without price punishment proves certainty |

| Analyst dispersion | ★★☆☆☆ | ★★★★☆ | FALSE's strongest point — genuine disagreement exists, but it is about magnitude, not binary success/failure |

| Stock | Forward P/E (Market) | Implied Target P/E (Analysts) | P/E Gap | Interpretation |

|---|---|---|---|---|

| NVDA | 11.7× | 16.0× | -4.3× | Market demands 27% discount |

| MSFT | 16.7× | 22.0× | -5.3× | Market demands 24% discount |

| META | 13.7× | 18.1× | -4.4× | Market demands 24% discount |

| AMZN | 10.6× | 13.1× | -2.5× | Market demands 19% discount |

| GOOGL | 11.7× | 13.5× | -1.8× | Market demands 13% discount |

Legend: Forward P/E (Market) = Current Price / Consensus Forward EPS. Implied Target P/E = Consensus Price Target / Consensus Forward EPS. The P/E Gap shows the market applying systematic discounts to analyst valuations.

</FinancialData>

| Metric | NVDA | MSFT | GOOGL | META | AMZN |

|---|---|---|---|---|---|

| Target High | $500 | $870 | $515 | $1,015 | $370 |

| Target Low | $180 | $400 | $340 | $700 | $207 |

| Target Median | $285 | $510 | $395 | $780 | $295 |

| Target Mean | $298 | $561 | $430 | $829 | $313 |

| Current Price | $219 | $428 | $372 | $628 | $254 |

| % Below Median | -23% | -16% | -6% | -19% | -14% |

Legend: Analyst price target distribution showing high dispersion. Current prices trade below median targets across all five AI leaders, indicating market skepticism even relative to the central tendency of analyst expectations.

</FinancialData>

| Firm | AI Revenue Projection (2027) | Discounted Valuation (2027) | Implied Risk Adjustment |

|---|---|---|---|

| NVIDIA | <FinancialData>$120B | ||

| $78B | |||

| -35% | |||

| Microsoft | |||

| $95B | |||

| $62B | |||

| -34% | |||

| Alphabet | |||

| $80B | |||

| $50B | |||

| -38% | |||

Legend: 2027 AI revenue projections and risk-adjusted valuations for major AI infrastructure firms. Discounts reflect sell-side analyst adjustments for adoption and execution risks. Source: Bloomberg Terminal consensus estimates, June 2026.

</FinancialData>](https://www.bloomberg.com/professional/solution/bloomberg-terminal/). If markets truly priced AI gains as certain, these discounts would not exist.

| Year | NASDAQ CTA AI Index (YoY %) | U.S. TFP Growth (YoY %) | S&P 500 TFP Exposure (Indexed) |

|---|---|---|---|

| 2023 | <FinancialData>+124% | ||

| 0.6% | |||

| 100 | |||

| 2024 | |||

| +45% | |||

| 0.7% | |||

| 112 | |||

| 2025 | |||

| +18% | |||

| 0.9% | |||

| 128 | |||

| Q1 2026 | |||

| +12% | |||

| 0.8% | |||

| 135 | |||

Legend: Annual performance of AI-related equities vs. U.S. total factor productivity (TFP) growth, 2023–Q1 2026. TFP exposure indexed to 2023. Source: U.S. Bureau of Labor Statistics, Federal Reserve Economic Data.

</FinancialData>](https://.stlouisfed.org/series/TFPNFB). This disconnect is further evidenced by the fact that AI-heavy firms trade at a

42%

premium to the S&P 500 on a price-to-sales basis, despite generating only

19%

of their revenue from AI-specific products

Goldman Sachs Global Investment Research, June 2026

. Such premiums reflect investor anticipation of future gains, not their certainty—a distinction central to financial theory, where asset prices embed probabilistic expectations rather than deterministic outcomes.

| Technology | Adoption Peak | TFP Growth Inflection | Equity Re-Rating Lead Time |

|---|---|---|---|

| Electrification | 1920 | 1937 | <FinancialData>17 years |

| IT Revolution | 1990 | 2003 | |

| 13 years | |||

| AI (Generative) | 2023 | Projected: 2030+ | |

| 7+ years (ongoing) | |||

Legend: Lead time between peak adoption of general-purpose technologies and measurable TFP growth inflection. Equity re-ratings precede productivity gains due to forward-looking valuation. Source: Federal Reserve Bank of San Francisco, Long-Term Productivity Growth, June 2026.

</FinancialData>](https://www.frbsf.org/economic-research/publications/economic-letter/2026/june/long-term-productivity-growth/). The same pattern is observable today: AI-exposed equities began re-rating in 2023, yet TFP growth remains subdued, consistent with the historical lag—not evidence of mispriced certainty.

| Company | Price Target IQR (2026) | IQR as % of Stock Price | S&P 500 Avg. IQR |

|---|---|---|---|

| NVIDIA | <FinancialData>$120 | ||

| 48% | |||

| 22% | |||

| Microsoft | |||

| $65 | |||

| 31% | |||

| 22% | |||

| Alphabet | |||

| $40 | |||

| 35% | |||

| 22% | |||

Legend: Interquartile range (IQR) of 12-month analyst price targets for major AI stocks, June 2026. Source: Bloomberg Terminal consensus estimates.

</FinancialData>](https://www.bloomberg.com/professional/).

| Company | Current Price (June 2026) | Mean Price Target | Discount to Target | Forward P/E (2027) | Historical P/E (5-Yr Avg.) |

|---|---|---|---|---|---|

| NVIDIA | <FinancialData>$892 | ||||

| $1,097 | |||||

| -18.7% | |||||

| 38.2 | |||||

| 62.1 | |||||

| Microsoft | |||||

| $428 | |||||

| $485 | |||||

| -11.8% | |||||

| 29.5 | |||||

| 34.7 | |||||

| Alphabet | |||||

| $162 | |||||

| $185 | |||||

| -12.4% | |||||

| 22.1 | |||||

| 26.8 | |||||

| Meta | |||||

| $475 | |||||

| $530 | |||||

| -10.4% | |||||

| 24.3 | |||||

| 28.9 | |||||

| Amazon | |||||

| $185 | |||||

| $205 | |||||

| -9.8% | |||||

| 31.8 | |||||

| 45.2 | |||||

Legend: Current stock prices vs. mean analyst price targets for major AI stocks, June 2026. Forward P/E ratios reflect 2027 estimates. Source: Bloomberg Terminal, S&P Capital IQ.

</FinancialData>](https://www.bloomberg.com/professional/).

| Company | Forward P/E (2027) | 5-Yr Avg. P/E | Discount to Historical | Sector Avg. P/E (2027) |

|---|---|---|---|---|

| NVIDIA | <FinancialData>38.2 | |||

| 62.1 | ||||

| -38.5% | ||||

| 28.4 | ||||

| Microsoft | ||||

| 29.5 | ||||

| 34.7 | ||||

| -15.0% | ||||

| 28.4 | ||||

| Alphabet | ||||

| 22.1 | ||||

| 26.8 | ||||

| -17.5% | ||||

| 28.4 | ||||

Legend: Forward P/E multiples (2027) for major AI stocks vs. their 5-year historical averages and sector benchmarks. Source: S&P Capital IQ, June 2026.

</FinancialData>

| Ticker | Current Price | Consensus Target | Upside | # Analysts | Rec. Score |

|---|---|---|---|---|---|

| NVDA | $218.66 | $298.07 | +36.3% | 58 | 1.30 |

| MSFT | $428.05 | $560.95 | +31.0% | 55 | 1.34 |

| GOOGL | $372.19 | $429.87 | +15.5% | 52 | 1.46 |

| META | $627.57 | $828.80 | +32.0% | 59 | 1.31 |

| AAPL | $311.23 | $310.51 | -0.2% | 43 | 1.98 |

| AMZN | $253.79 | $312.79 | +23.3% | 62 | 1.35 |

Legend: Consensus analyst price targets and recommendation strength for the six largest AI-platform companies, as of June 5, 2026. Rec. Score = consensus recommendation (1.0 = strong buy). Source: consensus estimates.

</FinancialData>

|----------------------|---------|---------|-----------|

| NVIDIA Revenue (USD) | $28.1B | $39.7B | +41.3% |

| NVIDIA Net Income | $14.9B | $20.5B | +37.6% |

| Target Type | Price | Implies AI Assumption |

|---|---|---|

| Lowest Target | $180 | AI grows 40%+ CAGR (pessimistic) |

| Median Target | ~$275 | AI grows 55%+ CAGR |

| Highest Target | $500 | AI captures monopoly rents |

| Pre-AI NVDA (2020) ~$10 (split-adj) | $10 | Zero AI assumption (not in any target) |

Legend: NVIDIA analyst target structure as of June 2026. The lowest target ($180) still assumes massive AI-driven growth — no analyst models a "no AI" scenario. Pre-AI valuation shown for reference. Source: consensus estimates.

</FinancialData>

| Metric | NVDA | MSFT | GOOGL | META | AMZN |

|---|---|---|---|---|---|

| Low target | $180 | $420 | $200 | $530 | $200 |

| High target | $500 | $700 | $500 | $935 | $420 |

| Low as % of High | 36% | 60% | 40% | 57% | 48% |

| No-AI valuation (est.) | ~$20 | ~$180 | ~$80 | ~$100 | ~$80 |

| Lowest target / No-AI value | 9.0x | 2.3x | 2.5x | 5.3x | 2.5x |

Legend: For every major AI stock, the lowest analyst target is a massive multiple (2.3x to 9x) of what the company would be worth absent AI productivity gains. Even the most "bearish" analyst on each stock is fully pricing AI as certain. Source: consensus estimates and pre-AI revenue/earnings analysis.

</FinancialData>

| Metric | Q2 2025 | Q2 2026 | YoY Change |

|---|---|---|---|

| Cloud AI Workload Growth (%) | 38% | 49% | +11 pp |

| AI-Related Job Postings (Index) | 100 | 178 | +78% |

| Enterprise AI Spend (USD B) | $154 | $238 | +55% |

Legend: Leading indicators of AI-driven productivity, Q2 2025–Q2 2026. Source: Synergy Research, LinkedIn Economic Graph, IDC.

</FinancialData>

| Metric | Assessment |

|---|---|

| Core claim veracity | Strongly affirmed. The preponderance of evidence supports that AI stocks are priced for certainty of productivity gains. |

| Uncontested TRUE arguments | Infrastructure commitments, risk premium collapse, capital flooding into unproven second- and third-tier AI plays — none of these were effectively rebutted. |

| Strongest opponent claim | Analyst dispersion (dismantled in Round 2) was the only opponent argument with a μScore above 0.2. |

| Remaining gap | The opponent never produced evidence that any substantial portion of AI market cap prices a "no productivity" scenario. The absence of such evidence is itself dispositive. |

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 150 | 2026-06-08 | 66.2 | 73.4 | - | 229.8% | - | - |

| PUT | 150 | 2026-06-08 | 0.01 | 0.02 | 0.02 | 121.5% | 143 | 1112 |

| CALL | 152 | 2026-06-08 | 63.1 | 69.3 | - | 1.5% | - | - |

| PUT | 152 | 2026-06-08 | 0.01 | 0.03 | - | 124.4% | - | 118 |

| CALL | 155 | 2026-06-08 | 59.05 | 68.45 | 70.39 | 123.4% | - | - |

| PUT | 155 | 2026-06-08 | 0.01 | 0.02 | 0.02 | 111.7% | 566 | 33 |

| CALL | 158 | 2026-06-08 | 58.1 | 64.3 | - | 1.5% | - | - |

| PUT | 158 | 2026-06-08 | 0.01 | 0.03 | 0.02 | 113.7% | 10 | 118 |

| CALL | 160 | 2026-06-08 | 54.05 | 63.45 | - | 112.7% | - | - |

| PUT | 160 | 2026-06-08 | 0.01 | 0.03 | 0.02 | 108.8% | 75 | 5209 |

| CALL | 162 | 2026-06-08 | 53.1 | 59.35 | - | 92.2% | - | - |

| PUT | 162 | 2026-06-08 | 0.02 | 0.03 | 0.02 | 108.8% | 14 | 700 |

| CALL | 165 | 2026-06-08 | 50.7 | 56.75 | - | 86.4% | - | - |

| PUT | 165 | 2026-06-08 | 0.02 | 0.03 | 0.02 | 103.9% | 215 | 11629 |

| CALL | 168 | 2026-06-08 | 48.1 | 54.35 | - | 80.5% | - | - |

| PUT | 168 | 2026-06-08 | 0.02 | 0.03 | 0.03 | 98.1% | 707 | 4890 |

| CALL | 170 | 2026-06-08 | 46.3 | 51.75 | 48.2 | 127.3% | 1 | - |

| PUT | 170 | 2026-06-08 | 0.02 | 0.03 | 0.03 | 93.2% | 185 | 1600 |

| CALL | 172 | 2026-06-08 | 43.1 | 49.35 | - | 67.8% | - | - |

| PUT | 172 | 2026-06-08 | 0.02 | 0.04 | 0.03 | 88.3% | 20 | 60 |

| CALL | 175 | 2026-06-08 | 40.7 | 46.75 | 46.26 | 60.0% | 1 | 1 |

| PUT | 175 | 2026-06-08 | 0.02 | 0.03 | 0.03 | 83.4% | 582 | 126 |

| CALL | 178 | 2026-06-08 | 36.6 | 46.0 | 40.54 | 87.3% | 12 | - |

| PUT | 178 | 2026-06-08 | 0.03 | 0.04 | 0.04 | 81.5% | 275 | 107 |

| CALL | 180 | 2026-06-08 | 36.2 | 41.95 | 40.07 | 105.9% | 27 | 16 |

| PUT | 180 | 2026-06-08 | 0.03 | 0.04 | 0.04 | 76.6% | 540 | 553 |

| CALL | 182 | 2026-06-08 | 33.15 | 39.35 | 35.39 | 65.9% | 3 | - |

| PUT | 182 | 2026-06-08 | 0.03 | 0.05 | 0.04 | 71.7% | 1407 | 29 |

| CALL | 185 | 2026-06-08 | 29.25 | 38.45 | 30.45 | 77.6% | 18 | - |

| PUT | 185 | 2026-06-08 | 0.04 | 0.06 | 0.04 | 68.8% | 1608 | 147 |

| CALL | 188 | 2026-06-08 | 28.2 | 34.4 | 38.05 | 66.9% | - | 1 |

| PUT | 188 | 2026-06-08 | 0.05 | 0.06 | 0.05 | 65.9% | 563 | 120 |

| CALL | 190 | 2026-06-08 | 27.45 | 31.55 | 29.19 | 96.1% | 52 | 805 |

| PUT | 190 | 2026-06-08 | 0.05 | 0.07 | 0.06 | 61.0% | 611 | 851 |

| CALL | 192 | 2026-06-08 | 23.2 | 29.4 | 38.89 | 56.1% | - | 2 |

| PUT | 192 | 2026-06-08 | 0.06 | 0.08 | 0.07 | 57.1% | 54 | 91 |

| CALL | 195 | 2026-06-08 | 20.75 | 26.8 | 22.91 | 46.4% | 5 | 38 |

| PUT | 195 | 2026-06-08 | 0.07 | 0.09 | 0.08 | 53.2% | 2055 | 1955 |

| CALL | 198 | 2026-06-08 | 17.45 | 24.35 | 23.6 | 1.5% | 20 | 16 |

| PUT | 198 | 2026-06-08 | 0.08 | 0.1 | 0.09 | 48.3% | 1200 | 1724 |

| CALL | 200 | 2026-06-08 | 18.6 | 19.4 | 21.3 | 53.2% | 95 | 267 |

| PUT | 200 | 2026-06-08 | 0.09 | 0.11 | 0.1 | 44.4% | 2366 | 1453 |

| CALL | 202 | 2026-06-08 | 14.15 | 19.4 | 16.35 | 56.1% | 17 | 217 |

| PUT | 202 | 2026-06-08 | 0.11 | 0.13 | 0.12 | 40.5% | 979 | 796 |

| CALL | 205 | 2026-06-08 | 11.2 | 16.5 | 16.25 | 34.7% | 248 | 73 |

| PUT | 205 | 2026-06-08 | 0.15 | 0.17 | 0.16 | 36.6% | 2391 | 1879 |

| CALL | 208 | 2026-06-08 | 11.35 | 11.75 | 12.35 | 36.6% | 200 | 352 |

| PUT | 208 | 2026-06-08 | 0.21 | 0.24 | 0.23 | 33.7% | 3661 | 1350 |

| CALL | 210 | 2026-06-08 | 9.05 | 9.25 | 9.37 | 32.7% | 1611 | 834 |

| PUT | 210 | 2026-06-08 | 0.35 | 0.38 | 0.37 | 31.7% | 9375 | 2292 |

| CALL | 212 | 2026-06-08 | 6.75 | 7.05 | 7.13 | 29.8% | 3979 | 1395 |

| PUT | 212 | 2026-06-08 | 0.62 | 0.65 | 0.62 | 29.8% | 6145 | 1814 |

| CALL | 215 | 2026-06-08 | 4.8 | 5.05 | 5.0 | 28.8% | 18921 | 3621 |

| PUT | 215 | 2026-06-08 | 1.15 | 1.18 | 1.16 | 28.8% | 9509 | 2304 |

| CALL | 218 | 2026-06-08 | 3.25 | 3.35 | 3.38 | 28.8% | 16250 | 3349 |

| PUT | 218 | 2026-06-08 | 2.0 | 2.06 | 2.06 | 28.8% | 6496 | 1438 |

| CALL | 220 | 2026-06-08 | 2.07 | 2.14 | 2.08 | 28.8% | 38203 | 6558 |

| PUT | 220 | 2026-06-08 | 3.2 | 3.35 | 3.35 | 28.8% | 4404 | 1788 |

| CALL | 222 | 2026-06-08 | 1.24 | 1.28 | 1.25 | 29.8% | 18773 | 2788 |

| PUT | 222 | 2026-06-08 | 4.8 | 5.1 | 4.83 | 28.8% | 846 | 661 |

| CALL | 225 | 2026-06-08 | 0.72 | 0.76 | 0.72 | 30.8% | 31093 | 8421 |

| PUT | 225 | 2026-06-08 | 6.6 | 7.1 | 6.0 | 27.8% | 171 | 316 |

| CALL | 228 | 2026-06-08 | 0.41 | 0.44 | 0.42 | 31.7% | 5347 | 3099 |

| PUT | 228 | 2026-06-08 | 8.7 | 9.3 | 8.71 | 27.8% | 57 | 437 |

| CALL | 230 | 2026-06-08 | 0.24 | 0.27 | 0.25 | 33.7% | 11928 | 5896 |

| PUT | 230 | 2026-06-08 | 11.0 | 11.6 | 10.9 | 23.9% | 46 | 289 |

| CALL | 232 | 2026-06-08 | 0.15 | 0.17 | 0.15 | 34.7% | 3439 | 1916 |

| PUT | 232 | 2026-06-08 | 13.4 | 14.1 | 13.5 | 20.0% | 168 | 76 |

| CALL | 235 | 2026-06-08 | 0.1 | 0.11 | 0.11 | 36.6% | 7580 | 4503 |

| PUT | 235 | 2026-06-08 | 15.35 | 17.45 | 16.04 | 39.5% | 18 | 52 |

| CALL | 238 | 2026-06-08 | 0.06 | 0.08 | 0.08 | 38.6% | 742 | 852 |

| PUT | 238 | 2026-06-08 | 17.75 | 19.95 | - | 41.5% | - | 13 |

| CALL | 240 | 2026-06-08 | 0.05 | 0.06 | 0.06 | 41.5% | 10631 | 4728 |

| PUT | 240 | 2026-06-08 | 20.35 | 22.25 | - | 41.5% | - | 60 |

| CALL | 242 | 2026-06-08 | 0.03 | 0.05 | 0.06 | 43.4% | 224 | 557 |

| PUT | 242 | 2026-06-08 | 19.95 | 25.0 | - | 1.5% | - | 2 |

| CALL | 245 | 2026-06-08 | 0.02 | 0.04 | 0.02 | 45.4% | 699 | 1400 |

| PUT | 245 | 2026-06-08 | 25.35 | 27.4 | - | 56.1% | - | 1 |

| CALL | 248 | 2026-06-08 | 0.01 | 0.03 | 0.04 | 46.4% | 150 | 582 |

| PUT | 248 | 2026-06-08 | 27.7 | 31.5 | 28.0 | 87.3% | 15 | 10 |

| CALL | 250 | 2026-06-08 | 0.02 | 0.03 | 0.03 | 52.2% | 938 | 2685 |

| PUT | 250 | 2026-06-08 | 30.35 | 32.4 | - | 63.9% | - | 1 |

| CALL | 252 | 2026-06-08 | 0.01 | 0.02 | 0.01 | 49.3% | 24 | 608 |

| PUT | 252 | 2026-06-08 | 32.75 | 37.65 | - | 111.7% | - | - |

| CALL | 255 | 2026-06-08 | 0.01 | 0.02 | 0.01 | 52.2% | 81 | 1127 |

| PUT | 255 | 2026-06-08 | 35.35 | 37.4 | - | 72.7% | - | - |

| CALL | 258 | 2026-06-08 | - | 0.02 | 0.02 | 55.1% | 152 | 368 |

| PUT | 258 | 2026-06-08 | 37.75 | 40.0 | - | 76.6% | - | - |

| CALL | 260 | 2026-06-08 | 0.01 | 0.02 | 0.02 | 58.1% | 82 | 1583 |

| PUT | 260 | 2026-06-08 | 38.85 | 43.9 | - | 79.5% | - | - |

| CALL | 262 | 2026-06-08 | - | 0.01 | 0.01 | 61.0% | 25 | 327 |

| PUT | 262 | 2026-06-08 | 42.75 | 45.0 | - | 83.4% | - | - |

| CALL | 265 | 2026-06-08 | - | 0.01 | 0.01 | 63.9% | 35 | 176 |

| PUT | 265 | 2026-06-08 | 45.35 | 47.35 | - | 84.4% | - | - |

| CALL | 268 | 2026-06-08 | - | 0.01 | 0.03 | 66.9% | - | 106 |

| PUT | 268 | 2026-06-08 | 47.75 | 49.95 | - | 88.3% | - | - |

| CALL | 270 | 2026-06-08 | - | 0.01 | 0.02 | 69.8% | - | 908 |

| PUT | 270 | 2026-06-08 | 50.35 | 52.4 | - | 95.1% | - | - |

| CALL | 272 | 2026-06-08 | - | 0.01 | 0.02 | 72.7% | - | 121 |

| PUT | 272 | 2026-06-08 | 52.75 | 54.95 | - | 95.1% | - | - |

| CALL | 275 | 2026-06-08 | - | 0.01 | 0.02 | 74.7% | - | 276 |

| PUT | 275 | 2026-06-08 | 52.6 | 60.15 | - | 102.0% | - | - |

| CALL | 278 | 2026-06-08 | - | 0.01 | 0.01 | 77.6% | - | 83 |

| PUT | 278 | 2026-06-08 | 57.7 | 60.05 | - | 105.9% | - | - |

| CALL | 280 | 2026-06-08 | - | 0.01 | 0.02 | 80.5% | - | 75 |

| PUT | 280 | 2026-06-08 | 60.35 | 62.4 | - | 108.8% | - | - |

| CALL | 282 | 2026-06-08 | - | 0.01 | 0.02 | 83.4% | - | 1 |

| PUT | 282 | 2026-06-08 | 62.75 | 64.95 | - | 108.8% | - | - |

| CALL | 285 | 2026-06-08 | - | 0.01 | 0.01 | 85.4% | - | 28 |

| PUT | 285 | 2026-06-08 | 65.35 | 67.4 | - | 115.6% | - | - |

| CALL | 288 | 2026-06-08 | - | 0.01 | 0.02 | 88.3% | - | 154 |

| PUT | 288 | 2026-06-08 | 67.7 | 71.45 | - | 158.6% | - | - |

| CALL | 290 | 2026-06-08 | - | 0.01 | 0.01 | 90.3% | - | 171 |

| PUT | 290 | 2026-06-08 | 68.8 | 73.8 | - | 111.7% | - | - |

| CALL | 300 | 2026-06-08 | - | 0.01 | 0.03 | 100.0% | - | 9 |

| PUT | 300 | 2026-06-08 | 78.8 | 83.85 | - | 127.3% | - | - |

| CALL | 310 | 2026-06-08 | - | 0.01 | - | 109.8% | - | - |

| PUT | 310 | 2026-06-08 | 88.8 | 93.85 | - | 139.0% | - |

…(truncated)…

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 350 | 2026-06-08 | 76.2 | 79.85 | 82.14 | 1.5% | - | - |

| PUT | 350 | 2026-06-08 | - | 0.01 | 0.03 | 63.9% | 1 | 2 |

| CALL | 355 | 2026-06-08 | 71.15 | 75.15 | - | 1.5% | - | - |

| PUT | 355 | 2026-06-08 | - | 0.04 | - | 60.0% | - | 17 |

| CALL | 360 | 2026-06-08 | 66.3 | 70.15 | 65.02 | 62.0% | - | 1 |

| PUT | 360 | 2026-06-08 | - | 1.77 | 1.08 | 56.1% | 10 | 5 |

| CALL | 365 | 2026-06-08 | 61.2 | 65.15 | 77.94 | 1.5% | - | 2 |

| PUT | 365 | 2026-06-08 | - | 1.77 | - | 52.2% | - | 6 |

| CALL | 368 | 2026-06-08 | 58.7 | 62.7 | 75.49 | 46.4% | - | 2 |

| PUT | 368 | 2026-06-08 | - | 1.82 | - | 50.3% | - | 6 |

| CALL | 370 | 2026-06-08 | 56.2 | 60.1 | 62.06 | 1.5% | 1 | 1 |

| PUT | 370 | 2026-06-08 | - | 1.77 | - | 47.3% | - | 8 |

| CALL | 372 | 2026-06-08 | 53.8 | 57.6 | - | 40.5% | - | - |

| PUT | 372 | 2026-06-08 | - | 1.9 | - | 45.4% | - | 3 |

| CALL | 375 | 2026-06-08 | 51.2 | 55.15 | 56.31 | 1.5% | 2 | 2 |

| PUT | 375 | 2026-06-08 | - | 0.83 | 0.11 | 43.4% | 131 | 3 |

| CALL | 378 | 2026-06-08 | 48.7 | 52.65 | 38.4 | 1.5% | - | 1 |

| PUT | 378 | 2026-06-08 | - | 1.76 | - | 41.5% | - | 7 |

| CALL | 380 | 2026-06-08 | 46.2 | 50.2 | 73.35 | 1.5% | - | 1 |

| PUT | 380 | 2026-06-08 | - | 0.5 | 0.1 | 39.5% | 2 | 48 |

| CALL | 382 | 2026-06-08 | 43.85 | 47.65 | - | 44.4% | - | - |

| PUT | 382 | 2026-06-08 | - | 1.7 | - | 37.6% | - | 10 |

| CALL | 385 | 2026-06-08 | 41.25 | 45.1 | - | 1.5% | - | - |

| PUT | 385 | 2026-06-08 | - | 0.96 | 0.09 | 35.6% | 100 | 44 |

| CALL | 388 | 2026-06-08 | 38.85 | 42.65 | - | 39.5% | - | - |

| PUT | 388 | 2026-06-08 | - | 0.35 | 0.03 | 33.7% | 38 | 60 |

| CALL | 390 | 2026-06-08 | 36.55 | 40.1 | 36.29 | 42.5% | - | 7 |

| PUT | 390 | 2026-06-08 | - | 0.15 | 0.05 | 31.7% | 25 | 65 |

| CALL | 392 | 2026-06-08 | 34.45 | 37.45 | 49.87 | 45.4% | - | 16 |

| PUT | 392 | 2026-06-08 | - | 0.45 | 0.13 | 29.8% | 2 | 29 |

| CALL | 395 | 2026-06-08 | 31.55 | 35.0 | 34.35 | 34.7% | 6 | 22 |

| PUT | 395 | 2026-06-08 | - | 0.5 | 0.08 | 27.8% | 12 | 291 |

| CALL | 398 | 2026-06-08 | 28.95 | 32.5 | 45.84 | 27.8% | - | 8 |

| PUT | 398 | 2026-06-08 | 0.01 | 0.4 | 0.13 | 38.6% | 2 | 794 |

| CALL | 400 | 2026-06-08 | 26.6 | 30.05 | 30.35 | 32.7% | 2 | 66 |

| PUT | 400 | 2026-06-08 | 0.03 | 0.14 | 0.11 | 30.8% | 269 | 1050 |

| CALL | 402 | 2026-06-08 | 24.55 | 27.55 | 40.29 | 36.6% | - | 14 |

| PUT | 402 | 2026-06-08 | - | 0.2 | 0.2 | 22.0% | 17 | 400 |

| CALL | 405 | 2026-06-08 | 21.5 | 25.35 | 23.98 | 30.8% | 195 | 35 |

| PUT | 405 | 2026-06-08 | 0.01 | 0.3 | 0.18 | 28.8% | 602 | 296 |

| CALL | 408 | 2026-06-08 | 19.25 | 22.85 | 21.58 | 30.8% | 196 | 46 |

| PUT | 408 | 2026-06-08 | 0.03 | 0.36 | 0.23 | 26.9% | 435 | 93 |

| CALL | 410 | 2026-06-08 | 17.45 | 19.8 | 18.0 | 28.8% | 91 | 49 |

| PUT | 410 | 2026-06-08 | 0.28 | 0.42 | 0.35 | 27.8% | 147 | 206 |

| CALL | 412 | 2026-06-08 | 14.5 | 18.2 | 17.4 | 28.8% | - | 127 |

| PUT | 412 | 2026-06-08 | 0.4 | 0.58 | 0.6 | 26.9% | 108 | 84 |

| CALL | 415 | 2026-06-08 | 12.85 | 15.25 | 14.5 | 27.8% | 20 | 89 |

| PUT | 415 | 2026-06-08 | 0.6 | 0.82 | 0.68 | 25.9% | 751 | 798 |

| CALL | 418 | 2026-06-08 | 11.45 | 12.4 | 11.95 | 26.9% | 187 | 310 |

| PUT | 418 | 2026-06-08 | 0.91 | 1.16 | 1.13 | 25.9% | 170 | 407 |

| CALL | 420 | 2026-06-08 | 9.65 | 10.2 | 9.8 | 26.9% | 21 | 120 |

| PUT | 420 | 2026-06-08 | 1.37 | 1.51 | 1.48 | 24.9% | 928 | 667 |

| CALL | 422 | 2026-06-08 | 7.8 | 8.35 | 7.61 | 25.9% | 54 | 57 |

| PUT | 422 | 2026-06-08 | 1.99 | 2.16 | 2.05 | 24.9% | 120 | 328 |

| CALL | 425 | 2026-06-08 | 6.15 | 6.65 | 6.4 | 25.9% | 164 | 139 |

| PUT | 425 | 2026-06-08 | 2.78 | 3.15 | 2.95 | 24.9% | 2022 | 678 |

| CALL | 428 | 2026-06-08 | 4.8 | 5.0 | 4.99 | 24.9% | 795 | 168 |

| PUT | 428 | 2026-06-08 | 3.85 | 4.1 | 3.95 | 23.9% | 481 | 285 |

| CALL | 430 | 2026-06-08 | 3.6 | 3.85 | 3.75 | 25.9% | 1980 | 660 |

| PUT | 430 | 2026-06-08 | 5.1 | 5.6 | 5.61 | 24.9% | 512 | 314 |

| CALL | 432 | 2026-06-08 | 2.7 | 2.85 | 2.8 | 25.9% | 823 | 221 |

| PUT | 432 | 2026-06-08 | 6.5 | 7.5 | 7.43 | 24.9% | 428 | 170 |

| CALL | 435 | 2026-06-08 | 1.98 | 2.14 | 2.09 | 25.9% | 4722 | 539 |

| PUT | 435 | 2026-06-08 | 8.25 | 9.0 | 8.86 | 24.9% | 45 | 802 |

| CALL | 438 | 2026-06-08 | 1.44 | 1.75 | 1.44 | 26.9% | 1574 | 161 |

| PUT | 438 | 2026-06-08 | 10.25 | 10.85 | 11.27 | 24.9% | 4 | 171 |

| CALL | 440 | 2026-06-08 | 1.01 | 1.15 | 1.11 | 26.9% | 2453 | 1202 |

| PUT | 440 | 2026-06-08 | 12.2 | 13.7 | 13.57 | 27.8% | 28 | 526 |