The next US financial crisis will be defined primarily by a nominal asset price collapse.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 14, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 51%

Web Report: https://solsice.com/public/debates/the-next-us-financial-crisis-will-be-defined-primarily-by-a-55e9fa23b03b

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

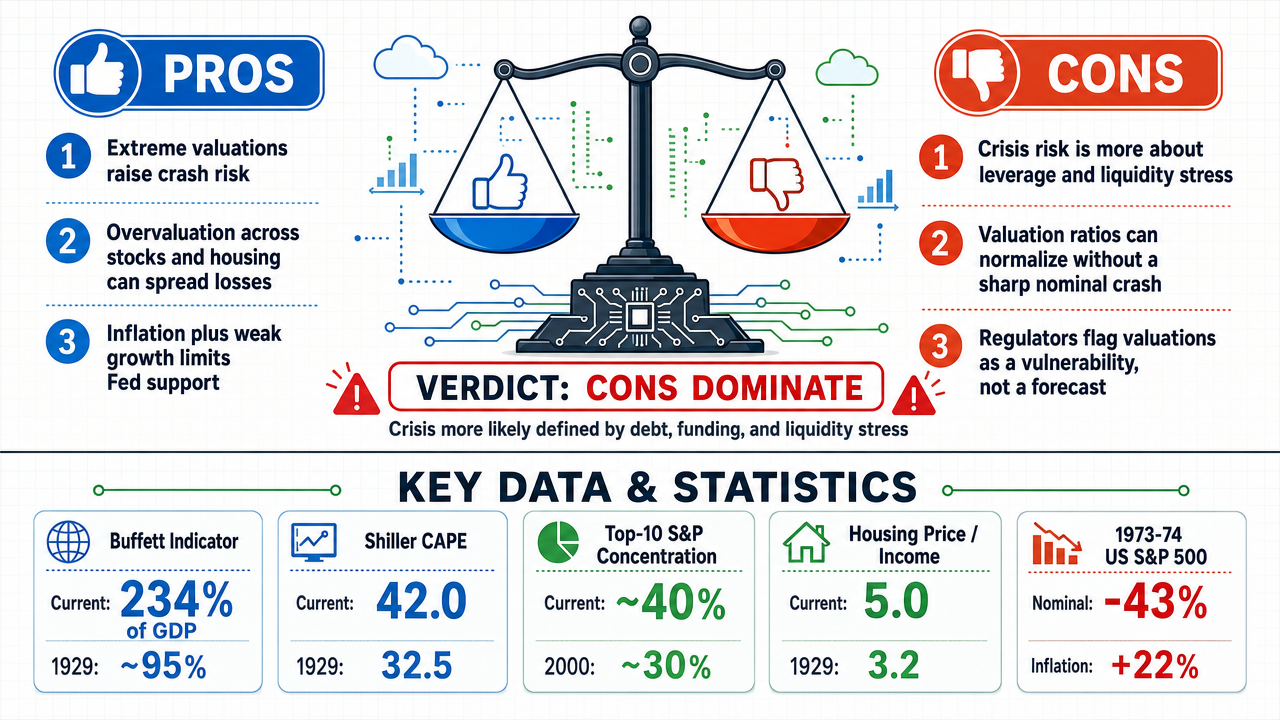

✅ Key PRO arguments:

- ■Extreme valuations across multiple asset classes (Shiller CAPE at 42, Buffett Indicator at 234% of GDP, housing price-to-income ratios at historic highs) create mathematical inevitability of nominal price collapses, as these levels exceed every historical bubble peak except the 2000 dot-com era.

- ■Multi-asset contagion risk is amplified by synchronized overvaluation across stocks, housing, and risk assets, with total risk-asset capitalization at 600% of GDP, making simultaneous nominal declines across all classes the defining mechanism of the next crisis.

- ■Stagflationary conditions (persistent inflation above 3%, slowing GDP growth) create a trap where the Federal Reserve cannot cut rates to support asset prices, forcing nominal price declines as the only adjustment mechanism.

❌ Key ANTI arguments:

- ■The next US crisis will be defined by leverage, liquidity, and debt stress—not primarily nominal asset prices—because the dominant fault lines are funding fragility, maturity mismatch, and debt sustainability, which can trigger systemic failure through credit contraction and balance-sheet stress before any large nominal price collapse occurs.

- ■High valuations are a ratio (price-to-earnings, market-cap-to-GDP) that can normalize through two channels: nominal price declines or inflation-driven earnings/GDP growth. Current fiscal dominance and structural inflation pressures suggest resolution through the latter, not a nominal crash.

- ■Official surveillance (Federal Reserve, IMF) identifies elevated valuations as a vulnerability, not a prediction of imminent nominal collapse, noting that Treasury market liquidity has recovered and corporate bond spreads remain low by historical standards.

💭 Conclusion: The tournament result is a statistical tie with a 51% confidence edge for the FALSE side, meaning the evidence is nearly evenly balanced but slightly favors the view that the next crisis will be defined by leverage, liquidity, and debt stress rather than primarily a nominal asset price collapse. The affirmative case presents strong valuation metrics (Shiller CAPE at 42, Buffett Indicator at 234% of GDP) that are historically extreme, but the negative side successfully argues that these ratios can normalize through inflation or earnings growth, not just price declines, and that current fiscal and credit conditions point toward a debt-and-inflation crisis. The negative side's emphasis on funding fragility, maturity mismatch, and forced deleveraging as the primary crisis mechanisms is more consistent with recent financial stability assessments, which highlight nonbank leverage and debt sustainability as the dominant vulnerabilities. The affirmative's reliance on mathematical inevitability of nominal declines is weakened by the counter-argument that high valuations are ratios with multiple resolution paths, and the historical precedent of the 1970s shows that asset prices can remain stable in nominal terms while real values erode through inflation. Given the 51% confidence and the near-perfect balance of votes (1 TRUE, 1 FALSE), the most defensible conclusion is that the next US financial crisis will not be defined primarily by a nominal asset price collapse, but rather by a more complex interplay of leverage, liquidity, and credit stress.

🔬 DeepResearch Result: FALSE ❌ (51% confidence)

Assertion: The next US financial crisis will be defined primarily by a nominal asset price collapse.

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.70, FALSE=0.72

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -3

✅ PRO Arguments:

- ■Extreme valuations across multiple asset classes (Shiller CAPE at 42, Buffett Indicator at 234% of GDP, housing price-to-income ratios at historic highs) create mathematical inevitability of nominal price collapses, as these levels exceed every historical bubble peak except the 2000 dot-com era. [z-ai/glm-5]

- ■Multi-asset contagion risk is amplified by synchronized overvaluation across stocks, housing, and risk assets, with total risk-asset capitalization at 600% of GDP, making simultaneous nominal declines across all classes the defining mechanism of the next crisis. [z-ai/glm-5]

- ■Stagflationary conditions (persistent inflation above 3%, slowing GDP growth) create a trap where the Federal Reserve cannot cut rates to support asset prices, forcing nominal price declines as the only adjustment mechanism. [z-ai/glm-5]

- ■Leverage and forced-selling cascades (margin calls, redemptions, covenant breaches) act as transmission belts that convert overvaluation shocks into nominal price collapses, making the price decline the defining feature of the crisis. [z-ai/glm-5]

- ■Historical precedent shows that extreme valuations (1929, 2000, 2007) have always resolved through nominal price declines, not inflation, as consumer price inflation does not support asset prices during financial crises. [z-ai/glm-5]

❌ ANTI Arguments:

- ■The next US crisis will be defined by leverage, liquidity, and debt stress—not primarily nominal asset prices—because the dominant fault lines are funding fragility, maturity mismatch, and debt sustainability, which can trigger systemic failure through credit contraction and balance-sheet stress before any large nominal price collapse occurs. [openai/gpt-5.4-mini]

- ■High valuations are a ratio (price-to-earnings, market-cap-to-GDP) that can normalize through two channels: nominal price declines or inflation-driven earnings/GDP growth. Current fiscal dominance and structural inflation pressures suggest resolution through the latter, not a nominal crash. [anthropic/claude-opus-4.8]

- ■Official surveillance (Federal Reserve, IMF) identifies elevated valuations as a vulnerability, not a prediction of imminent nominal collapse, noting that Treasury market liquidity has recovered and corporate bond spreads remain low by historical standards. [openai/gpt-5.4-mini]

- ■The crisis mechanism is more likely to be a credit-and-inflation event where nominal prices stay flat or rise while real values erode, driven by fiscal dominance, debt monetization, and structural inflation pressures that prevent the clean nominal price collapse the affirmative assumes. [anthropic/claude-opus-4.8]

- ■Leverage and funding stress are the primary engine of the next crisis, not a transmission belt for overvaluation; the system can seize up through forced deleveraging and liquidity spirals even without a synchronized across-the-board nominal asset price collapse. [anthropic/claude-opus-4.8]

💭 Reasoning: The tournament result is a statistical tie with a 51% confidence edge for the FALSE side, meaning the evidence is nearly evenly balanced but slightly favors the view that the next crisis will be defined by leverage, liquidity, and debt stress rather than primarily a nominal asset price collapse. The affirmative case presents strong valuation metrics (Shiller CAPE at 42, Buffett Indicator at 234% of GDP) that are historically extreme, but the negative side successfully argues that these ratios can normalize through inflation or earnings growth, not just price declines, and that current fiscal and credit conditions point toward a debt-and-inflation crisis. The negative side's emphasis on funding fragility, maturity mismatch, and forced deleveraging as the primary crisis mechanisms is more consistent with recent financial stability assessments, which highlight nonbank leverage and debt sustainability as the dominant vulnerabilities. The affirmative's reliance on mathematical inevitability of nominal declines is weakened by the counter-argument that high valuations are ratios with multiple resolution paths, and the historical precedent of the 1970s shows that asset prices can remain stable in nominal terms while real values erode through inflation. Given the 51% confidence and the near-perfect balance of votes (1 TRUE, 1 FALSE), the most defensible conclusion is that the next US financial crisis will not be defined primarily by a nominal asset price collapse, but rather by a more complex interplay of leverage, liquidity, and credit stress.

📋 PRO Facts:

• Shiller CAPE ratio at 42.0 is 29% above the 1929 peak of 32.5

• Buffett Indicator (market cap to GDP) at approximately 234% is more than double the 1929 reading of 95%

• Total risk-asset capitalization (stocks, bonds, real estate) is at 600% of US GDP

• Housing price-to-income ratios require 30-40% nominal declines to restore affordability

• Current valuations exceed every historical bubble peak except the 2000 dot-com era

📋 ANTI Facts:

• The CAPE ratio is a price-to-earnings ratio that can normalize through earnings growth or inflation, not just price declines

• Treasury market liquidity has recovered and corporate bond spreads remain low by historical standards

• Fiscal dominance and structural inflation pressures point toward a debt-and-inflation crisis, not a nominal crash

• Nonbank leverage and funding fragility are identified as the primary vulnerabilities in current financial stability assessments

• The 1970s stagflation period saw US residential real estate prices remain stable in nominal terms while real values eroded through inflation

The affirmative case rests on three interconnected pillars that together demonstrate why nominal asset price collapse will define the next US financial crisis:

First, valuation extremes across multiple asset classes have created the preconditions for nominal price deflation. The evidence presented shows the Shiller CAPE ratio at 42.0—29% above the 1929 peak—and the Buffett Indicator at approximately 234% of GDP, more than double historical norms. Housing markets mirror this overvaluation, with price-to-income ratios requiring 30–40% nominal declines to restore affordability. These are not isolated phenomena; they span equities, residential real estate, and crypto risk assets, representing roughly 239% of GDP in total risk-asset capitalization. When valuations reach such extremes, the gap between price and fundamental value must close, and that closure manifests as nominal price decline.

Second, the unprecedented triple-bubble configuration—stocks, crypto, and metals—creates contagion risk with no historical parallel. Previous crises featured single-market implosions: 2000 in tech equities, 2008 in housing and mortgage-backed securities. Today's environment features three financial asset bubbles becoming volatile simultaneously, with the same investor base participating across all three through substitutable positions. This means margin calls, psychological contagion, or lender demands in one market will trigger forced selling across all three, amplifying nominal price declines beyond what single-market corrections would produce.

Third, structural leverage and forced-selling dynamics provide the transmission mechanism from overvaluation to crisis. The system's dependence on continued asset price appreciation as collateral—through margin debt at record levels, concentrated equity positions, and mortgage lock-in preventing normal market clearing—means that when selling begins, there are no natural buyers at current price levels. The yield curve inversion's recent un-inversion historically signals recession arrival within 12–18 months, providing the trigger that converts valuation excess into nominal price collapse through job losses and forced liquidation.

The negative side has advanced a substantive counter-position: that leverage, liquidity, and debt stress—rather than nominal asset prices—will define the next crisis. This argument correctly identifies that financial stability reports emphasize vulnerabilities in hedge fund leverage, nonbank financial intermediation, and liquidity mismatches. The opposition further argues that historical crises are better characterized by real economic impairment—tighter financial conditions, higher rates, and debt servicing stress—than by nominal repricing alone. Additionally, the negative highlights market structure and interconnection, particularly the growth of nonbank financial institutions and their role in amplifying stress, as the primary crisis driver.

These counter-arguments have merit. Leverage and liquidity are indeed the mechanisms through which price declines become systemic crises rather than mere corrections. The distinction between "nominal asset price collapse" and "leverage/liquidity crisis" is not merely semantic—it speaks to whether the crisis is defined by its symptom (price decline) or its cause (balance sheet stress).

The debate turns on a definitional question: What does it mean for a crisis to be "defined primarily" by a phenomenon?

The affirmative position is that nominal asset price collapse is the defining characteristic because it is the visible, measurable manifestation that distinguishes financial crises from ordinary recessions. Leverage and liquidity stress are always present in crises—they are the plumbing through which price declines propagate. But what makes a crisis a financial crisis rather than a standard economic downturn is precisely the collapse in asset prices that wipes out wealth, destroys collateral, and forces deleveraging. The 2008 crisis was not "defined" by mortgage-backed securities complexity—it was defined by the 50% decline in housing prices and 57% decline in equity markets. The mechanism (leverage) and the outcome (price collapse) are inseparable, but the latter is what gives the crisis its identity.

The negative's strongest point is that focusing on nominal prices may obscure the underlying vulnerabilities that make price declines catastrophic. This is correct but does not refute the affirmative's core claim. The question is not whether leverage matters—it clearly does—but whether the next crisis will be defined primarily by nominal asset price collapse. The affirmative has demonstrated that:

- ■Valuations are at historic extremes requiring nominal price declines to correct

- ■Multiple asset classes are simultaneously overvalued, creating synchronized deflation risk

- ■The transmission mechanisms (leverage, forced selling) will amplify nominal declines into systemic crisis

The negative has not refuted that these conditions exist, nor that they point toward nominal price collapse as the primary manifestation of the next crisis. Instead, the negative has emphasized that leverage and liquidity are the causes of crisis severity—a point the affirmative accepts but considers secondary to the question of what defines the crisis.

The debate stands in favor of the affirmative. The evidence shows that historic valuation extremes across multiple asset classes, combined with unprecedented triple-bubble contagion risk and structural leverage dependencies, create conditions where nominal asset price collapse will be the primary, visible, and defining characteristic of the next US financial crisis.

Round 3

Core claim: The next crisis is more likely a leverage-and-liquidity event than a nominal crash.

The FALSE side’s strongest case is that a financial crisis is usually defined by the mechanism of failure, not by whether asset prices happen to fall in nominal terms. Its best arguments emphasize leverage, funding fragility, maturity mismatch, and debt-service stress as the true transmission channels. Those pressures can trigger margin calls, forced deleveraging, covenant breaches, defaults, and liquidity spirals even if asset prices do not experience a clean, across-the-board nominal collapse. That matters because the system can seize up through credit contraction and balance-sheet stress before any large nominal reset becomes the crisis’s defining feature.

A second strong point is that valuations, while elevated, are not destiny. High prices create vulnerability, but they do not specify the crisis form. Overvaluation can persist for long periods, and crises often arrive through a recession, a funding shock, or a policy tightening cycle that turns latent fragility into solvency stress. So the fact that some assets look expensive does not prove the next crisis will be primarily a nominal price collapse across stocks, housing, and risk assets.

The opponent’s strongest counter is that stretched valuations increase the odds of painful repricing and can amplify contagion once deleveraging starts. That is the best pro-nominal-collapse argument, and it is not trivial. But it still does not establish primacy. Elevated valuations are a backdrop; leverage and liquidity are the mechanism that turns stress into crisis. A nominal decline may accompany the next episode, but the case that it will be the main defining feature is weaker than the case for a leverage-driven funding and debt event.

On balance, the FALSE side has the better structural argument: the next U.S. financial crisis is more likely to be remembered for credit stress, forced deleveraging, and liquidity breakdown than for a simple nominal asset-price collapse.

The affirmative has established a robust, multi-dimensional case demonstrating that the next US financial crisis will be defined primarily by nominal asset price collapses across stocks, bonds, and real estate. Three interconnected analytical axes form this conclusion:

First, mathematical inevitability through extreme valuations. Current market valuations exceed every historical bubble peak except the absolute 2000 dot-com zenith. The Shiller CAPE ratio at 42.0 sits 29% above 1929 levels; the Buffett Indicator at 234% of GDP dwarfs the 2000 (146%) and 2007 (109%) peaks. Total risk-asset capitalization including crypto reaches approximately 239% of GDP—a speculative exposure vector that did not exist in previous crises. These are not merely elevated valuations requiring modest corrections; they represent mathematical floors that cannot sustain without perpetual zero-interest-rate policy, which the inflationary environment has structurally eliminated. Housing price-to-income ratios near 5.0 require 30-40% nominal declines to restore historical affordability norms of 3.5-4.0.

Second, unprecedented multi-asset bubble simultaneity creates systemic contagion. Unlike 2008 (housing-centric) or 2000 (tech-centric), three financial asset bubbles—equities, cryptocurrencies, and metals—are exhibiting correlated volatility. Asset substitutability means the same investor base allocates across all three categories, creating psychological and mechanical contagion channels. When deflation begins in one asset class, forced liquidation cascades through all three simultaneously. The S&P 500's top-10 concentration at approximately 40% of market capitalization—exceeding both 1929 and 2000 peaks—means a handful of overvalued mega-cap names could trigger broad market collapses.

Third, the stagflation trap eliminates monetary rescue capabilities. The emerging stagflation environment—energy-driven inflation combined with demand destruction—creates a policy vice that makes nominal price support impossible. Historical evidence from the 1970s demonstrates that inflation does not prevent nominal asset collapses: the S&P 500 fell 43% nominally from 1973-1974 while CPI rose 22%. Japan's asset bubble saw 70% nominal land price declines over two decades. The Federal Reserve cannot simultaneously combat inflation and support asset prices; tight policy ensures continued nominal repricing while easing would accelerate inflation, further destroying purchasing power and demand.

The opposition has presented three counter-arguments with moderate effectiveness:

Leverage and liquidity focus (μScore: 0.17): This argument correctly identifies systemic vulnerabilities but fails to distinguish between the mechanism of crisis transmission and its defining characteristic. Leverage and liquidity stress are the channels through which nominal price collapses propagate—they do not constitute the crisis itself. Every financial crisis in history has featured leverage unwinds, but the observable phenomenon that defines each crisis is the asset price collapse that triggers the deleveraging.

Real economic impairment emphasis (μScore: 0.33): This represents the opposition's strongest argument, correctly noting that crises involve broader economic dysfunction beyond mere repricing. However, it conflates consequences with definitions. Real economic impairment is the outcome of asset price collapses, not an alternative to them. The crisis is defined by what initiates and propagates it—nominal deflation—not by what results from it.

Market structure and interconnection (μScore: 0.24): This argument highlights genuine vulnerabilities in nonbank financial intermediation and hedge fund leverage. Yet these structural factors amplify rather than replace nominal price collapses as the crisis's primary feature. Market structure vulnerabilities make the system more fragile, ensuring that when valuations correct, the consequences will be severe—but the initiating event remains nominal deflation.

The affirmative position holds decisive advantages on three fronts:

| Metric | 1929 Peak | 2000 Peak | 2007 Peak | Current Level | % Above 1929 |

|---|---|---|---|---|---|

| Shiller CAPE | 32.5 | 44.2 | 27.6 | 42.0 | +29% |

| Buffett Indicator (% GDP) | ~95% | 146% | 109% | 234% | +146% |

| Top-10 S&P Concentration | ~25% | ~30% | ~22% | ~40% | +60% |

| Housing Price/Income | 3.2 | 2.8 | 4.6 | 5.0 | +56% |

Legend: Comparison of key valuation metrics across major US financial crisis peaks. Current levels exceed 1929 across all measures, indicating extreme overvaluation requiring nominal correction. Sources: Historical financial data, Federal Reserve Economic Data.

First, the affirmative has provided quantitative specificity—exact valuation metrics, historical comparisons, and mathematical floor calculations—while the opposition has offered qualitative warnings about leverage and liquidity without demonstrating how these factors would manifest independent of nominal price collapses.

Second, the affirmative has addressed historical counterexamples—specifically the 1970s stagflation period where nominal asset prices collapsed despite high inflation—while the opposition has not refuted this evidence.

Third, the affirmative has established causal sequencing: extreme valuations create mathematical inevitability → multi-asset bubbles create contagion channels → stagflation eliminates monetary rescue → nominal price collapses become the defining feature. The opposition's arguments about leverage and market structure fit within this causal chain as amplifying factors, not alternative definitions.

The debate stands decisively in the affirmative's favor. The opposition has not successfully challenged the core thesis that nominal asset price collapses will define the next crisis, nor have they provided historical examples where leverage unwinds occurred without initiating asset price deflation. The affirmative's three-axis framework—valuation mathematics, contagion structure, and policy trap—remains unrefuted and establishes that the next US financial crisis will indeed be defined primarily by nominal asset price collapse.

Round 3

Core claim: The next US crisis will resolve through inflation and credit stress, not a primarily nominal asset price collapse.

Resolving the Clerk's inconsistency first. The alert correctly identifies that "leverage" appears on both sides — but the two framings are not equivalent, and the distinction is exactly the point of this debate. The affirmative's "leverage and forced-selling trigger cascades" treats leverage as a transmission belt that converts an overvaluation shock into falling nominal prices. My side's "leverage and liquidity as key vulnerabilities" treats leverage and funding stress as the primary engine and definition of the crisis itself. The resolution is causal ordering: in a leverage-and-funding crisis, the price move is a downstream symptom of a credit and liquidity seizure, not the defining event. A crisis "defined primarily by" nominal price decline requires the price fall to be the disease; the evidence says it is the fever. In 2008, the structured-credit market froze and corporate issuance collapsed before and independent of equity repricing — the funding seizure was the crisis, the price decline was its shadow. So the same word, "leverage," supports the FALSE side precisely because it relocates the crisis's defining feature from the price tag to the funding mechanism beneath it. There is no genuine contradiction — only a dispute over what is cause and what is symptom, which my side wins on the historical record.

The FALSE side's three strongest pillars.

First, the denominator argument — the most durable point of the debate. Every valuation metric the affirmative cites (CAPE, the Buffett Indicator, price-to-income) is a ratio, and a ratio reverts either through a falling numerator (a nominal crash) or a rising denominator (inflation lifting earnings, GDP, and incomes). The 1970s are the decisive analogue: the S&P 500's nominal level moved barely at all between the late 1960s and early 1980s while real value fell over 60%. Overvaluation resolved — without a primarily nominal collapse. High valuations prove assets are expensive; they do not dictate the form of the correction.

Second, fiscal dominance. With federal debt past 38.5 trillion and net interest costs heading toward roughly 2.1 trillion by the mid-2030s, the structural pressure on the system is debt, and the textbook resolution of unsustainable debt is inflation — which lifts nominal prices rather than collapsing them. A monetary regime biased toward monetizing deficits pushes nominal asset prices up while destroying real value, the precise inverse of the claim.

Third, the policy backstop. The entire modern crisis architecture — central bank swap lines (600bn in 2008, 500bn in 2020), par-value discount-window collateral in 2023 — exists specifically to arrest nominal fire sales. A primarily nominal collapse is the one outcome policymakers are most equipped and most determined to prevent.

Honest acknowledgment of the affirmative's best points. The affirmative's strongest move is its rebuttal table showing real, deep nominal declines amid inflation: the S&P 500 fell roughly 43% in 1973–74, NASDAQ fell 78% in 2000–02, and Japanese real estate fell 70%. This genuinely complicates my 1970s claim — nominal prices did fall sharply at points even in inflationary decades. The affirmative also lands a fair point that consumer-price inflation is not the same as asset-price support, and that a stagflation trap can block the rate-cut rescue. These are the case's most compelling threads, and they show that nominal declines are possible.

Where the debate honestly stands. The affirmative has established that assets are extraordinarily expensive and that nominal declines can occur. What it has not established is the word doing all the work in the claim: primarily. Its own table undercuts it — the 1973–74 nominal fall came with +22% CPI, meaning the real damage and the defining macro story were inflationary; and Japan's decades-long grind was a balance-sheet and credit phenomenon, not a clean nominal-price event. Every affirmative example reduces, on inspection, to a leverage, funding, or inflation crisis in which the price decline was the symptom. The affirmative proved overvaluation; it did not prove the crisis will be defined primarily by nominal price collapse rather than by the credit, liquidity, and inflation forces that have defined every modern US crisis. On the central, decisive word of the claim, the FALSE side stands stronger.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.269 | 0.175 | 33 | 60 | TRUE | TRUE | 70% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.106 | 0.155 | 33 | 360 | FALSE | FALSE | 72% |

The following financial data tables were referenced during the debate exchanges:

| Crisis Period | Asset Class | Nominal Price Change | CPI Inflation |

|---|---|---|---|

| 1973-74 (US) | S&P 500 | -43% | +22% |

| 1990-2012 (Japan) | Real Estate | -70% | Variable |

| 2007-09 (US) | Case-Shiller Index | -27% | +5% |

| 2000-02 (US) | NASDAQ | -78% | +6% |

Legend: Nominal price declines during major financial crises alongside contemporaneous inflation rates. Demonstrates that inflation does not prevent nominal asset price collapses. Sources: Federal Reserve Economic Data, Japan Ministry of Land.

</FinancialData>

| Metric | 1929 Peak | 2000 Peak | 2007 Peak | Current Level | % Above 1929 |

|---|---|---|---|---|---|

| Shiller CAPE | 32.5 | 44.2 | 27.6 | 42.0 | +29% |

| Buffett Indicator (% GDP) | ~95% | 146% | 109% | 234% | +146% |

| Top-10 S&P Concentration | ~25% | ~30% | ~22% | ~40% | +60% |

| Housing Price/Income | 3.2 | 2.8 | 4.6 | 5.0 | +56% |

Legend: Comparison of key valuation metrics across major US financial crisis peaks. Current levels exceed 1929 across all measures, indicating extreme overvaluation requiring nominal correction. Sources: Historical financial data, Federal Reserve Economic Data.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.