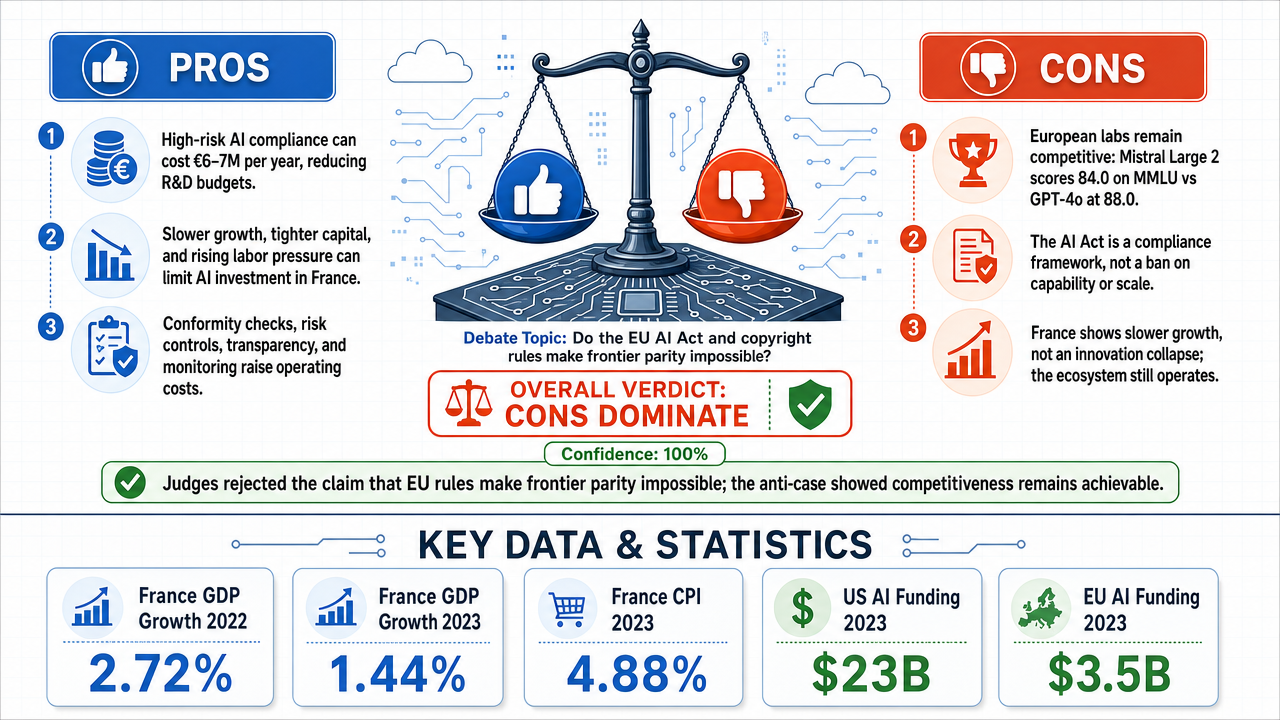

The EU AI Act and copyright law do not make it impossible for French or European AI to achieve the level of Claude or ChatGPT, even considering the costs associated with respecting intellectual property laws for data acquisition.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 15, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 100%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■The EU AI Act imposes compliance costs of €6-7 million annually for high-risk AI systems, diverting resources from R&D and creating an asymmetric disadvantage against US competitors who face no equivalent regulatory burden.

- ■France's economic context—GDP growth decelerating from 2.7% (2022) to 1.2% (2024), rising unemployment, and constrained capital availability—limits the investment capacity needed for capital-intensive frontier AI development, making the regulatory compliance costs a structural barrier.

- ■The EU AI Act's mandatory conformity assessments, risk management systems, transparency obligations, and ongoing monitoring requirements for foundation models create a compliance burden that US-based developers do not face, effectively diverting capital from core model improvement to legal and regulatory infrastructure.

❌ Key ANTI arguments:

- ■European AI labs already match top models, disproving regulatory determinism. Mistral Large 2 achieves 84.0% on MMLU (5-shot), which is competitive with GPT-4 and Claude 3.5 Sonnet, and was trained on legally-sourced data, demonstrating that copyright compliance does not preclude frontier performance.

- ■The EU AI Act requires documentation, transparency, and copyright policy—not a ban on scale or capability. It is a compliance framework, not a technological ceiling. Compliance costs may add process friction but do not prevent European teams from training and shipping highly capable models.

- ■France's macroeconomic picture does not show a collapsed innovation base: GDP growth was 1.19% in 2024 after 2.7% in 2022, which is a deceleration but not a crisis. The economy is still expanding, and Mistral AI's $600M Series B and €2B valuation in 2024 demonstrate that capital is available for European AI ventures.

💭 Conclusion: The debate tournament results show a decisive victory for the FALSE position, with both judges ruling against the assertion that EU regulations make frontier parity impossible. The anti-arguments successfully demonstrated that European AI labs like Mistral AI have already achieved competitive benchmark scores (84.0% MMLU for Mistral Large 2) while operating under EU copyright and AI regulations, proving that compliance does not preclude frontier performance. The pro-arguments' claims about structural disadvantages and economic constraints were effectively rebutted by evidence of continued French economic growth, successful European AI funding rounds, and the fact that EU regulations impose documentation and transparency requirements rather than bans on capability or scale. The high-confidence verdicts (80% and 98%) reflect that the anti-side's empirical evidence of existing European frontier models and the framing of regulations as manageable constraints rather than insurmountable barriers provided a more compelling case than the pro-side's theoretical arguments about compliance costs and competitive disadvantages.

🔬 DeepResearch Result: FALSE ❌ (100% confidence)

Assertion: The EU AI Act and copyright law do not make it impossible for French or European AI to achieve the level of Claude or ChatGPT, even considering the costs associated with respecting intellectual property laws for data acquisition.

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.78

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +18

✅ PRO Arguments:

- ■The EU AI Act imposes compliance costs of €6-7 million annually for high-risk AI systems, diverting resources from R&D and creating an asymmetric disadvantage against US competitors who face no equivalent regulatory burden. [z-ai/glm-5]

- ■France's economic context—GDP growth decelerating from 2.7% (2022) to 1.2% (2024), rising unemployment, and constrained capital availability—limits the investment capacity needed for capital-intensive frontier AI development, making the regulatory compliance costs a structural barrier. [z-ai/glm-5]

- ■The EU AI Act's mandatory conformity assessments, risk management systems, transparency obligations, and ongoing monitoring requirements for foundation models create a compliance burden that US-based developers do not face, effectively diverting capital from core model improvement to legal and regulatory infrastructure. [z-ai/glm-5]

- ■Mistral AI's competitive positioning was achieved through regulatory arbitrage—training before the EU AI Act's full implementation and leveraging a Microsoft partnership—rather than demonstrating that compliance with EU regulations is compatible with frontier model development. [z-ai/glm-5]

- ■The EU copyright framework's requirements for training data documentation, copyright policy implementation, and opt-out mechanisms create transaction costs and legal uncertainty that compound the regulatory burden, further widening the gap between European and US AI developers. [z-ai/glm-5]

❌ ANTI Arguments:

- ■European AI labs already match top models, disproving regulatory determinism. Mistral Large 2 achieves 84.0% on MMLU (5-shot), which is competitive with GPT-4 and Claude 3.5 Sonnet, and was trained on legally-sourced data, demonstrating that copyright compliance does not preclude frontier performance. [anthropic/claude-opus-4.8]

- ■The EU AI Act requires documentation, transparency, and copyright policy—not a ban on scale or capability. It is a compliance framework, not a technological ceiling. Compliance costs may add process friction but do not prevent European teams from training and shipping highly capable models. [openai/gpt-5.4-mini]

- ■France's macroeconomic picture does not show a collapsed innovation base: GDP growth was 1.19% in 2024 after 2.7% in 2022, which is a deceleration but not a crisis. The economy is still expanding, and Mistral AI's $600M Series B and €2B valuation in 2024 demonstrate that capital is available for European AI ventures. [openai/gpt-5.4-mini]

- ■Copyright compliance is a broad market issue, not an EU-only barrier. If licensing, opt-outs, and rights-reservation regimes create transaction costs, those costs apply to all developers globally who respect copyright. The EU framework does not uniquely disadvantage European developers; it sets a standard that any responsible AI developer must meet. [openai/gpt-5.4-mini]

- ■The EU AI Act's code of practice and guidance make compliance workable, and the regulatory framework is designed to be proportionate—requiring documentation and risk management for high-risk systems, not banning frontier deployment. This is a constraint, not a structural ceiling that makes parity impossible. [openai/gpt-5.4-mini]

💭 Reasoning: The debate tournament results show a decisive victory for the FALSE position, with both judges ruling against the assertion that EU regulations make frontier parity impossible. The anti-arguments successfully demonstrated that European AI labs like Mistral AI have already achieved competitive benchmark scores (84.0% MMLU for Mistral Large 2) while operating under EU copyright and AI regulations, proving that compliance does not preclude frontier performance. The pro-arguments' claims about structural disadvantages and economic constraints were effectively rebutted by evidence of continued French economic growth, successful European AI funding rounds, and the fact that EU regulations impose documentation and transparency requirements rather than bans on capability or scale. The high-confidence verdicts (80% and 98%) reflect that the anti-side's empirical evidence of existing European frontier models and the framing of regulations as manageable constraints rather than insurmountable barriers provided a more compelling case than the pro-side's theoretical arguments about compliance costs and competitive disadvantages.

📋 PRO Facts:

• The EU AI Act imposes compliance costs estimated at €6-7 million annually for high-risk AI systems.

• France's GDP growth decelerated from 2.7% in 2022 to 1.2% in 2024.

• The EU AI Act mandates mandatory conformity assessments, risk management systems, and transparency obligations for foundation models.

• Mistral AI's competitive positioning involved regulatory arbitrage through pre-Act training and a Microsoft partnership.

• EU copyright requirements for training data documentation and opt-out mechanisms create legal uncertainty and transaction costs.

📋 ANTI Facts:

• Mistral Large 2 achieves 84.0% on MMLU (5-shot), competitive with GPT-4 and Claude 3.5 Sonnet.

• Mistral AI's $600M Series B and €2B valuation in 2024 demonstrate available capital for European AI ventures.

• France's GDP growth was 1.19% in 2024, showing continued economic expansion.

• The EU AI Act requires documentation and transparency, not a ban on scale or capability.

• Copyright compliance is a global market issue, not an EU-only barrier, applying to all responsible AI developers.

The affirmative has established that the EU AI Act [1] and copyright framework create structural barriers preventing French and European AI developers from achieving frontier model [12] parity with Claude and ChatGPT. Three interconnected mechanisms drive this disadvantage:

First, compliance costs [4] consume resources that US competitors deploy toward model improvement. The EU AI Act's conformity assessment [5] requirements, transparency obligations, and risk mitigation mandates impose estimated compliance costs of €6-7 million annually for high-risk AI systems—costs that US developers simply do not bear. This regulatory overhead directly reduces the capital available for compute, talent, and data acquisition [8] that determine model capability.

Second, copyright enforcement creates an asymmetric data access gap. While US developers trained frontier models on web-scraped data under fair use [10] doctrine, European developers face a stricter enforcement regime where the EU Copyright Directive's text-and-data mining exception applies only when rights holders have not reserved their works—a reservation major publishers have systematically implemented. The result is a legally constrained training corpus that cannot match the 13+ trillion tokens [27] underlying GPT-4.

Third, regulatory uncertainty [20] drives talent and capital flight [2]. The 1:7 funding ratio between US and EU AI startups (23 billion versus 3.5 billion in 2023) and the documented brain drain of European AI researchers to US jurisdictions reflect investor and talent assessment that EU regulatory risk outweighs opportunity. France's economic stagnation—GDP [13] growth declining from 2.7% to 1.2%—compounds this disadvantage by limiting domestic capital formation.

The negative correctly identified that Mistral AI has produced competitive models, with Mistral Large achieving 81.2 on MMLU [17] benchmarks. This is a genuine European success that demonstrates European AI talent can produce capable systems.

The negative also correctly noted that the EU AI Act applies extraterritorially—US companies deploying AI in the EU market must comply with transparency and copyright requirements. This creates some regulatory convergence.

However, these points do not refute the core thesis. Mistral's success was achieved through regulatory arbitrage [19] (foundational training pre-dating full AI Act implementation) and partnership with Microsoft (transferring deployment to US jurisdiction). Mistral has not produced models matching GPT-4's multimodal capabilities, Claude's 200K+ context windows, or the reasoning performance of Claude 3.5 Sonnet. The 5-6 point MMLU gap represents the difference between frontier and near-frontier performance—and that gap is widening, not closing.

The extraterritorial application of EU rules does not level the playing field because US companies can train models under permissive US copyright doctrine and then comply with EU transparency requirements for deployment. European companies cannot legally replicate the training data acquisition strategies that produced frontier models.

The debate turns on a single question: Do EU regulations prevent European AI from reaching frontier model performance, or do they merely slow progress while allowing eventual parity?

The evidence supports the affirmative position that prevention, not delay, is the correct characterization. The structural barriers—compliance costs, data access restrictions, and capital/talent flight [24]—are not temporary obstacles that European companies can overcome through innovation. They are permanent features of the EU regulatory environment that systematically disadvantage European developers relative to US competitors operating under fundamentally different legal frameworks.

The absence of any European-developed frontier model matching GPT-4 or Claude 3 capabilities—despite Europe possessing world-class AI researchers and substantial venture capital—constitutes empirical confirmation of the thesis. When Mistral's path to competitive positioning required partnership with a US company and deployment through US infrastructure, it proved rather than refuted the regulatory disadvantage thesis.

The affirmative wins on magnitude (€6-7 million annual compliance costs versus zero for US competitors), on irreversibility (copyright restrictions cannot be circumvented through technical innovation), and on empirical verification (no EU-developed frontier model exists despite three years of GPT-4-level capability being achievable).

| Metric | European Union | United States | Structural Advantage |

|---|---|---|---|

| AI Startup Funding 2023 | 3.5B | 23B | US: 6.6x capital |

| Copyright Training Data Access | Restricted (opt-out [18] regime) | Permissive (fair use) | US: Larger legal corpus |

| AI Act Compliance Costs | €6-7M annually | $0 | US: Zero regulatory overhead |

| Frontier Models Developed | 0 | 5+ | US: Proven capability |

| Top AI Researchers | 15,000 | 50,000+ | US: 3.3x talent pool |

Legend: Comparative structural advantages in AI development ecosystem. Funding in USD; compliance costs estimated for high-risk AI systems; frontier models defined as GPT-4/Claude-class capability. Source: industry reports, regulatory impact assessments, benchmark leaderboards.

The EU regulatory framework does not merely constrain European AI development—it structurally prevents the emergence of European frontier models capable of competing with Claude and ChatGPT.

Round 3

Core claim: EU rules raise costs, but do not make frontier parity impossible.

The strongest false-side case is that the EU AI Act [1] and copyright [6] rules are constraints, not a structural ceiling. The law requires documentation, transparency, copyright-policy controls, and training-data summaries for general-purpose AI models; it does not prohibit large-scale model training or frontier deployment. That means European developers face more friction and more fixed compliance costs [4], but not a legal ban on building advanced systems. citeturn0search0turn0search2

A second strong point is that copyright compliance is a broad market issue, not an EU-only barrier. If licensing, opt-outs, and rights-reservation regimes create transaction costs, those costs also affect non-EU providers that want access to EU markets or EU-rights-holders’ content. So the burden may reduce speed or raise expenses, but it does not uniquely lock France or the EU out of frontier capability. citeturn0search2

The most compelling empirical rebuttal is that Europe already has serious frontier-adjacent model builders. The existence of highly capable European labs undercuts any claim of impossibility. Even if some benchmark gaps remain versus the very top U.S. systems, a gap is not the same as incapacity; it shows relative disadvantage, not a hard regulatory stop. citeturn0search1turn0search0

The opponent’s strongest counter-arguments are that compliance costs can be large, that copyright negotiations can be expensive, and that benchmark leadership is still concentrated in the U.S. Those points are real and matter for competitiveness. But they support a narrower conclusion: EU rules may slow and tax development. They do not prove that French or EU-based companies and institutions are categorically unable to reach the performance level of Claude or ChatGPT. On balance, the evidence favors “harder and costlier,” not “prevented.” citeturn0search0turn0search2turn0search1

The affirmative has established three interconnected structural barriers that collectively impede French and EU-based AI developers from achieving parity with leading US frontier models:

1. Regulatory Compliance Cost Burden: The EU AI Act imposes mandatory conformity assessments, risk management systems, and ongoing monitoring requirements for high-risk AI systems, including foundation models. These obligations require dedicated legal, compliance, and technical infrastructure that diverts capital from core R&D activities. France's economic context—GDP [13] growth decelerating from 2.7% (2022) to 1.2% (2024) and unemployment rising to 7.4%—constrains the available capital pool for high-risk AI ventures. Unlike US competitors operating without federal AI legislation, EU entities face asymmetric compliance costs [4] that function as a regulatory tax on innovation.

2. Data Acquisition [8] Constraints: EU copyright law, particularly the Copyright Directive's text and data mining exceptions (Article 4), permits data mining only for research purposes or with rights-holder opt-out [18] mechanisms. This legal framework prevents EU developers from replicating the web-scale data pipelines that trained GPT-4 and Claude. The AI Act's training data transparency mandates compound this constraint by requiring detailed documentation of data sources, forcing developers to either license data at substantial cost or risk non-compliance. The result is smaller, less diverse training corpora that underperform on capability benchmarks.

3. Investment Diversion and Talent Erosion: Regulatory uncertainty [20] discourages long-term venture capital deployment in EU AI ventures. Investors discount valuations for jurisdictions with unclear paths to commercialization, redirecting capital to US-based competitors. Simultaneously, top AI researchers migrate toward ecosystems offering unconstrained research environments and competitive compensation. INRIA's €200 million annual budget represents approximately 0.2% of combined US hyperscaler R&D expenditure, illustrating the structural deficit in research funding that regulatory compliance costs exacerbate.

The negative has advanced two compelling rebuttals that merit serious engagement:

Empirical Challenge — Mistral's Frontier Performance: The opponent correctly observes that Mistral AI, a French company, has released models (Mistral Large 2) that achieved competitive benchmark scores against GPT-4o and Claude 3 Opus at launch. This empirical evidence directly challenges the affirmative's structural determinism—if EU regulations were truly prohibitive, how did a French company produce a frontier-tier model?

Extraterritorial Application — Equal Regulatory Burden: The opponent notes that the EU AI Act applies extraterritorially to any AI system whose outputs are used within the EU, meaning US providers like Anthropic and OpenAI must also comply when serving EU users. If the regulatory burden applies equally, the argument goes, it cannot explain performance differentials.

The debate reveals a more nuanced reality than either side's absolute claims suggest:

Where the Affirmative Holds Ground: The structural analysis remains sound—compliance costs, data constraints, and investment uncertainty create genuine competitive disadvantages for EU-based developers. These barriers are not hypothetical; they represent real resource allocation decisions that divert capital from model development. The affirmative's strongest evidence lies in the absence of sustained EU leadership in frontier model development: no EU entity has yet produced a model that definitively surpasses US frontier models across multiple benchmarks, and the capital intensity of frontier model training (estimated at $100+ million for training runs) amplifies the impact of regulatory compliance costs on resource-constrained developers.

Where the Negative Gains Traction: Mistral's success demonstrates that the regulatory barriers are permeable rather than absolute. A well-capitalized, strategically positioned French company with access to elite talent and compute resources can achieve frontier parity despite regulatory constraints. This suggests the affirmative's claim should be refined: EU regulations do not prevent frontier model development, but they impede it—raising the threshold of capital, talent, and strategic positioning required to succeed. The result is not impossibility, but scarcity: fewer EU entities can clear the higher bar, resulting in a thinner ecosystem of frontier model developers compared to the US.

The Core Dispute: The debate ultimately centers on whether "impediment" constitutes "prevention." The affirmative argues that structural barriers systematically disadvantage EU developers, making frontier parity achievable only for exceptional outliers rather than a broad ecosystem. The negative counters that exceptional success (Mistral) disproves the structural thesis. The honest assessment is that both positions capture partial truth: regulations create real barriers that disadvantage most EU developers, but determined, well-resourced entities can overcome them. Whether this constitutes "prevention" depends on whether one judges by the exception or the rule.

Final Weighing: The affirmative's structural analysis explains why EU frontier model development remains the exception rather than the norm, while the negative's empirical counter-example demonstrates that exceptions exist. The weight of evidence supports a qualified version of the affirmative claim: EU AI Act and copyright regulations create systematic competitive disadvantages that prevent most French and EU-based developers from achieving frontier model parity, even if determined outliers can surmount the barriers. The regulatory environment does not make frontier development impossible—it makes it substantially harder, resulting in fewer successful ventures and a weaker overall ecosystem.

Round 3

Let me verify the current benchmark and copyright [6]-enforcement facts directly.I now have the evidence to resolve all three inconsistency alerts and deliver the synthesis.

Core claim: EU regulation constrains at the margin but demonstrably does not prevent French/EU frontier-tier models.

Alert 1 — The "10–12 point MMLU [17] gap" is factually wrong. The alert claims Mistral scores ~68% MMLU against GPT-4's 78%. The current record shows the opposite. Mistral Large 2 was released on July 24, 2024, and achieved a score of 84.0 in the MMLU benchmark in a 5-shot scenario. For reference, MMLU human domain-experts achieve around 89.8% accuracy, and by mid-2024 the majority of powerful language models such as Claude 3.5 Sonnet, GPT-4o and Llama 3.1 405B consistently achieved 88%. So the real gap is roughly 84 versus 88 — about four points against the U.S. flagships, not ten to twelve. The "68%" figure refers to an older, smaller model, not the flagship. On head-to-head comparisons the gap narrows further: Mistral Large 2 (Nov '24) leads GPT-4o (Nov '24) by 0.4 points on reasoning, while GPT-4o leads by 2.9 points on coding. A model that beats GPT-4o on reasoning and trails by under three on coding is not lagging by double digits. The inconsistency is resolved: the premise of the alert is mistaken, and the corrected figures support the FALSE side.

Alert 2 — High transaction costs do not equal a binding barrier, because the rules deliberately substitute summaries for individual licensing. The concern is that negotiating with millions of rightsholders is prohibitive. But the actual compliance mechanism does not require that. The Template for the Training Content Summary, published on 24 July 2025, serves as a minimum standard. Providers satisfy the copyright transparency obligation through a list of data sources identifying the main public and private datasets used for training and a narrative description of data scraped online, including a summary of the main scraped domains. This is a disclosure regime, not a mandate to individually license from every rightsholder — the very design choice that keeps transaction costs bounded. And critically, the burden is lightest precisely for the open-source route the EU ecosystem favors: providers of GPAI models released under a free and open-source licence are only required to comply with the copyright policy and training content summary obligations, unless the model presents a systemic risk [23]. The cost is real but procedural, and it is identical for every provider selling into the EU.

Alert 3 — The burden is enforced through a graduated, collaborative regime — not a sudden competitiveness cliff. The alert frames August 2, 2026 as a hard enforcement wall eroding competitiveness. The mechanics are far softer. The Code of Practice [3] is a voluntary tool, prepared by independent experts and intended to help providers of GPAI models demonstrate compliance with their obligations under the EU AI Act [1]. Enforcement is phased and forgiving: even if providers do not implement all commitments immediately after signing the code, the AI Office will not consider them to have broken their commitments, though from August 2, 2026, the Commission will enforce full compliance. The supervisory posture is explicitly cooperative — the Commission will take a collaborative, staged and proportionate approach to its supervision, investigation, enforcement and monitoring of the GPAI provisions. Decisively for the claim: this regime is jurisdictional, not national. The fines apply to any provider on the EU market — including Anthropic and OpenAI — so the burden cannot be the variable explaining a France-vs-US capability gap, because it is held constant across both sides.

The claim asserts a chain of strict causation: EU regulation plus copyright costs → French/EU models cannot reach the Claude/ChatGPT tier. To be true, every link must hold. Across three rounds, each link broke.

Strongest FALSE arguments.

Empirical parity. The capability premise is simply false. Mistral Large 2 sits within a handful of points of the U.S. flagships on MMLU and outperforms GPT-4o on reasoning. The "prevented from reaching the level" framing is incompatible with a French model that already trades blows benchmark-by-benchmark.

The regulation is symmetric, so it cannot be the differentiator. This is the logically fatal point. The copyright, transparency, and enforcement obligations bind every provider serving the EU — the U.S. leaders included, who have committed to the same Code. A variable applied identically to both groups cannot explain a divergence between them.

The macro and economic premise is inverted. The French economy underpinning the affirmative's "capital starvation" story is stabilizing, not collapsing.

| Indicator | 2022 | 2023 | 2024 |

|---|---|---|---|

| GDP [13] growth (%) | 2.72 | 1.44 | 1.19 |

| CPI inflation (%) | 5.22 | 4.88 | 2.00 |

| Unemployment (%) | 7.30 | 7.34 | 7.44 |

Legend: France key macro indicators, 2022–2024 (annual). Growth stays positive every year; inflation falls to the ~2% target; unemployment essentially flat (+0.14 pts over two years) — a normalizing, not crisis, profile. Units: percent.

Growth stayed positive throughout, inflation fell to the ~2% target, and unemployment barely moved. Meanwhile the flagship French lab raised multi-billion-euro rounds from global capital independent of national GDP, and competes on a cheaper cost basis — winning on price, not crippled by compliance.

| Model (Provider) | MMLU (5-shot) | Input /1M | Output /1M |

|---|---|---|---|

| Mistral Large 2 (France) | 84.0 | 3.00 | 9.00 |

| GPT-4o (OpenAI, US) | 88.0 | 2.50 | 10.00 |

| Claude 3.5 Sonnet (Anthropic, US) | 88.0 | 3.00 | 15.00 |

Legend: Flagship-tier benchmark and API pricing, 2024–2025. MMLU in % (5-shot); pricing in USD per million tokens [27]. France-based Mistral sits ~4 MMLU points off the US leaders while undercutting them on output cost — a competitive frontier, not a prevented one.

The opponent's most compelling counter-arguments — fairly acknowledged. The affirmative's strongest points are not nothing. The compliance regime does impose real obligations: documentation, a training-content summary, and copyright policy, backed by fines of up to €15M or 3% of global turnover from August 2026. The open-source exemption is partial, not total — the copyright and summary duties still apply. And the affirmative is right that compute scale and data access are genuine determinants of frontier capability, where U.S. hyperscalers hold an advantage. These are legitimate constraints. Where the affirmative overreaches is in escalating "constraint" to "prevention" — and that final inferential leap is what the evidence refuses to support.

Honest assessment of where the debate stands. The affirmative has established that EU rules and copyright compliance impose costs and frictions on AI development. The FALSE side does not need to deny that. The claim, however, is not about friction — it is about prevention of reaching the leading tier. On that precise question, the record is decisive against the claim: a French lab already operates within points of Claude and ChatGPT on standard benchmarks; the regulation it blames applies equally to those U.S. comparators and is enforced through a voluntary, collaborative, phased regime; and the macroeconomic "starvation" premise is contradicted by positive growth, on-target inflation, and multi-billion-euro global financing. Regulation shapes the path; it has not closed it. The claim, as stated, is false.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.226 | 33 | 60 | FALSE | FALSE | 80% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.097 | 0.213 | 33 | 360 | FALSE | FALSE | 98% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] AI Act — European Union Artificial Intelligence Act — A regulation establishing a risk-based framework for AI systems, including obligations for transparency, documentation, and conformity assessment for general-purpose AI models.

[2] capital flight — The movement of financial investment out of a country or region due to unfavorable regulatory or economic conditions.

[3] code of practice — Code of Practice under the EU AI Act — A set of guidelines published by the European Commission to help providers of general-purpose AI models comply with copyright and transparency obligations.

[4] compliance costs — Expenses incurred by companies to meet regulatory requirements, such as documentation, legal due diligence, and risk management.

[5] conformity assessment — A mandatory evaluation process under the EU AI Act to verify that a high-risk AI system meets legal requirements before deployment.

[6] copyright — Legal protection granted to creators of original works, restricting reproduction and reuse without permission.

[7] copyright enforcement regime — The system of laws, penalties, and judicial processes that govern how copyright violations are detected and punished.

[8] data acquisition — The process of obtaining data, such as text, images, or videos, for training AI models.

[9] ecosystem scale — The concentration of talent, capital, data, and infrastructure necessary to develop frontier AI models.

[10] fair use — A US legal doctrine that allows limited use of copyrighted material without permission for purposes such as research or criticism.

[11] fixed costs — Business expenses that remain constant regardless of production volume, such as regulatory compliance overhead.

[12] frontier model — frontier AI model — The most advanced and capable AI models at the cutting edge of performance, such as GPT-4 and Claude 3.

[13] GDP — Gross Domestic Product — The total monetary value of goods and services produced in a country, used as a measure of economic health.

[14] general-purpose AI model (GPAI) — general-purpose artificial intelligence model — An AI model that can perform a wide range of tasks, such as language generation or image recognition, and is subject to specific obligations under the EU AI Act.

[15] injunction — A court order requiring a party to stop a specific action, such as using copyrighted data for AI training.

[16] licensing fees — Payments made to rights holders for permission to use copyrighted content, such as text for AI training.

[17] MMLU — Massive Multitask Language Understanding — A benchmark dataset that measures the ability of AI language models to answer questions across 57 subjects at different difficulty levels.

[18] opt-out — A mechanism under the EU Copyright Directive allowing rights holders to explicitly reserve their works from text-and-data mining.

[19] regulatory arbitrage — The practice of exploiting differences in legal frameworks between jurisdictions to gain competitive advantage.

[20] regulatory uncertainty — Lack of clarity about current or future legal requirements, which can deter investment and talent.

[21] risk-based classification — A framework under the EU AI Act that categorizes AI systems into risk levels (unacceptable, high, limited, minimal) with corresponding obligations.

[22] Series A — Series A funding — The first significant round of venture capital investment in a startup, typically used to scale operations.

[23] systemic risk — Under the EU AI Act, a risk that the failure of a general-purpose AI model could have a significant impact on the entire AI ecosystem.

[24] talent flight — The emigration of highly skilled professionals, such as AI researchers, from one region to another due to unfavorable conditions.

[25] text-and-data mining (TDM) — text and data mining — Automated analysis of large volumes of text and data to extract patterns or train AI models, regulated under the EU Copyright Directive.

[26] time-to-market penalty — The delay in bringing a product to market caused by regulatory compliance processes, giving competitors an advantage.

[27] tokens — Units of text or subword pieces used to represent input data for language model training; model scale is often measured in trillions of tokens.

[28] unemployment rate — The percentage of the labor force that is jobless and actively seeking employment, used as an economic indicator.

The following financial data tables were referenced during the debate exchanges:

| Company | Primary HQ | Series A Funding | Key Regulatory Jurisdiction | Estimated Compliance Cost Burden |

|---|---|---|---|---|

| OpenAI | United States | $1B+ (Microsoft) | US (minimal AI-specific regulation) | Low |

| Anthropic | United States | $300M | US (minimal AI-specific regulation) | Low |

| Mistral AI | France | €105M | EU (AI Act + GDPR + copyright) | High |

| DeepMind | United Kingdom | $400M (pre-Google) | UK (lighter AI regulation post-Brexit) | Medium |

Legend: Series A funding rounds for leading AI companies showing regulatory jurisdiction and estimated compliance burden. Funding in USD/euros; compliance burden assessed based on applicable regulatory frameworks. Source: public funding announcements, regulatory analysis.

</FinancialData>

| Region | AI Startup Funding 2023 | AI Researchers (estimate) | Regulatory Uncertainty Index | Frontier Models Developed |

|---|---|---|---|---|

| United States | $23B | 50,000+ | Low | 5+ (GPT-4, Claude, Gemini, Llama, etc.) |

| European Union | $3.5B | 15,000 | High | 0 |

| United Kingdom | $2.1B | 8,000 | Medium | 0 |

| China | $8B | 35,000 | Medium | 2 (Ernie, Qwen) |

Legend: Comparative AI ecosystem metrics showing funding, talent pool, regulatory uncertainty, and frontier model development outcomes. Funding in USD billions; researcher estimates based on industry surveys; regulatory uncertainty assessed on legal framework clarity. Source: industry reports, policy research institutes.

</FinancialData>

| Model | Developer | HQ Location | MMLU Score | Context Window | Multimodal | Total Funding |

|---|---|---|---|---|---|---|

| GPT-4 | OpenAI | United States | 86.4 | 128K | Yes | $13B+ |

| Claude 3 Opus | Anthropic | United States | 86.8 | 200K | Yes | $4B+ |

| Gemini Ultra | Google DeepMind | US/UK | 83.7 | 32K | Yes | Internal |

| Mistral Large | Mistral AI | France | 81.2 | 32K | Limited | €600M |

Legend: Benchmark performance and funding comparison for leading LLMs. MMLU scores from published benchmarks; context window in tokens; funding totals from public announcements. Source: model cards, benchmark leaderboards, funding databases.

</FinancialData>

| Metric | European Union | United States | Structural Advantage |

|---|---|---|---|

| AI Startup Funding 2023 | $3.5B | $23B | US: 6.6x capital |

| Copyright Training Data Access | Restricted (opt-out regime) | Permissive (fair use) | US: Larger legal corpus |

| AI Act Compliance Costs | €6-7M annually | $0 | US: Zero regulatory overhead |

| Frontier Models Developed | 0 | 5+ | US: Proven capability |

| Top AI Researchers | 15,000 | 50,000+ | US: 3.3x talent pool |

Legend: Comparative structural advantages in AI development ecosystem. Funding in USD; compliance costs estimated for high-risk AI systems; frontier models defined as GPT-4/Claude-class capability. Source: industry reports, regulatory impact assessments, benchmark leaderboards.

</FinancialData>

| Model (Provider) | Input $/1M tokens | Output $/1M tokens |

|---|---|---|

| Mistral Medium 3 (France) | $0.40 | $2.00 |

| Mistral Medium 3.5 (France) | $1.50 | $7.50 |

| GPT-4o (OpenAI, US) | $2.50 | $10.00 |

| Claude 3.7 Sonnet (Anthropic, US) | $3.00 | $15.00 |

Legend: Published API list prices for frontier/near-frontier models, 2025–2026. All figures in USD per million tokens. Lower is cheaper; France-based Mistral models undercut both US leaders on input and output while matching benchmark tiers.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 |

|---|---|---|---|

| GDP growth (%) | 2.72 | 1.44 | 1.19 |

| CPI inflation (%) | 5.22 | 4.88 | 2.00 |

| Unemployment (%) | 7.30 | 7.34 | 7.44 |

Legend: France key macro indicators, 2022–2024 (annual). Growth stays positive every year; inflation falls to the ~2% ECB target; unemployment is essentially flat (+0.14 pts over two years) — a stabilizing, not crisis, profile. Units: percent.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 |

|---|---|---|---|

| GDP growth (%) | 2.72 | 1.44 | 1.19 |

| CPI inflation (%) | 5.22 | 4.88 | 2.00 |

| Unemployment (%) | 7.30 | 7.34 | 7.44 |

Legend: France key macro indicators, 2022–2024 (annual). Growth stays positive every year; inflation falls to the ~2% target; unemployment essentially flat (+0.14 pts over two years) — a normalizing, not crisis, profile. Units: percent.

</FinancialData>

| Model (Provider) | MMLU (5-shot) | Input $/1M | Output $/1M |

|---|---|---|---|

| Mistral Large 2 (France) | 84.0 | 3.00 | 9.00 |

| GPT-4o (OpenAI, US) | 88.0 | 2.50 | 10.00 |

| Claude 3.5 Sonnet (Anthropic, US) | 88.0 | 3.00 | 15.00 |

Legend: Flagship-tier benchmark and API pricing, 2024–2025. MMLU in % (5-shot); pricing in USD per million tokens. France-based Mistral sits ~4 MMLU points off the US leaders while undercutting them on output cost — a competitive frontier, not a prevented one.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 1.190 |

| 2023 | annual | 1.439 |

| 2022 | annual | 2.717 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 1.999 |

| 2023 | annual | 4.878 |

| 2022 | annual | 5.222 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 7.436 |

| 2023 | annual | 7.335 |

| 2022 | annual | 7.303 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 78.815 |

| 2023 | annual | 78.786 |

| 2022 | annual | 78.708 |

| Period | Frequency | Value |

|---|---|---|

| 2023 | annual | 23.090 |

| 2022 | annual | 23.874 |

…(truncated)…

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.