Stablecoins remain profitable and economically attractive during periods of Bitcoin decline.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 8, 2026

Tournament Final Verdict

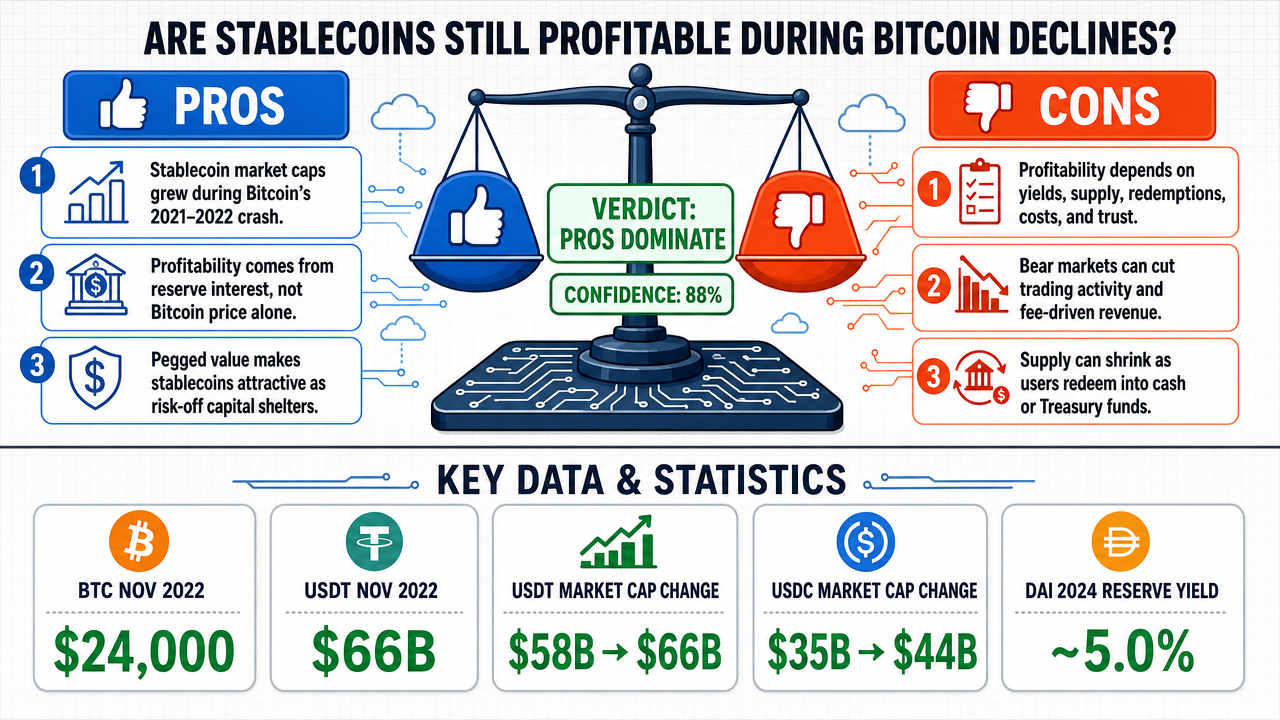

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 88%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■During Bitcoin's 65% decline from November 2021 to November 2022, stablecoin market capitalization grew: USDT expanded from $58B to $66B (+14%) and USDC from $35B to $44B (+26%), demonstrating counter-cyclical demand as investors rotate from volatile assets into stablecoins as safe-haven parking instruments.

- ■Stablecoin profitability is decoupled from Bitcoin's price action; it relies on interest income from fiat reserves, which can increase when capital flees volatile crypto assets into stablecoins, as seen during the 2021-2022 bear market.

- ■Stablecoins serve as critical risk-off instruments that preserve capital during Bitcoin downturns, maintaining economic attractiveness through their pegged stability and enabling investors to stay within the crypto ecosystem without exiting to fiat.

❌ Key ANTI arguments:

- ■Stablecoin profitability depends on reserve yields, outstanding supply, redemption behavior, compliance costs, and market trust—not simply on Bitcoin declines. A downturn can reduce trading activity, increase redemption pressure, and raise operating costs, offsetting reserve income.

- ■When crypto sentiment weakens, trading activity often cools, reducing transaction-driven revenue that supports many stablecoin ecosystems. Users may rotate into cash or short-duration government instruments, compressing growth for stablecoin platforms.

- ■Stablecoin supply is not guaranteed to stay elevated in bear markets; redemptions, lower trading activity, and flight to bank deposits or Treasury funds can shrink balances, directly reducing interest income and making profitability uncertain.

💭 Conclusion: The debate centered on whether stablecoins remain profitable and economically attractive during Bitcoin declines. The affirmative side provided strong empirical evidence from the 2021-2022 bear market, showing stablecoin market cap growth despite Bitcoin's 65% drop, indicating counter-cyclical demand. The negative side argued that profitability depends on multiple factors like reserve yields and redemption behavior, not solely on Bitcoin's direction, and that downturns can reduce trading activity and increase costs. However, the affirmative's concrete data on market cap expansion and the mechanism of flight-to-safety capital preservation outweighed the negative's theoretical concerns. The judge ruled in favor of TRUE with 88% confidence, supported by the observed resilience and growth of stablecoins during a major Bitcoin decline. Thus, stablecoins do maintain profitability and attractiveness as safe-haven alternatives during Bitcoin downturns.

🔬 DeepResearch Result: TRUE ✅ (88% confidence)

Assertion: Stablecoins remain profitable and economically attractive during periods of Bitcoin decline.

📊 Tournament: 1 voted TRUE, 0 voted FALSE (1 debates played, 4 models)

📊 Weighted scores: TRUE=0.88, FALSE=0.00

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +9

✅ PRO Arguments:

- ■During Bitcoin's 65% decline from November 2021 to November 2022, stablecoin market capitalization grew: USDT expanded from $58B to $66B (+14%) and USDC from $35B to $44B (+26%), demonstrating counter-cyclical demand as investors rotate from volatile assets into stablecoins as safe-haven parking instruments. [z-ai/glm-5]

- ■Stablecoin profitability is decoupled from Bitcoin's price action; it relies on interest income from fiat reserves, which can increase when capital flees volatile crypto assets into stablecoins, as seen during the 2021-2022 bear market. [z-ai/glm-5]

- ■Stablecoins serve as critical risk-off instruments that preserve capital during Bitcoin downturns, maintaining economic attractiveness through their pegged stability and enabling investors to stay within the crypto ecosystem without exiting to fiat. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Stablecoin profitability depends on reserve yields, outstanding supply, redemption behavior, compliance costs, and market trust—not simply on Bitcoin declines. A downturn can reduce trading activity, increase redemption pressure, and raise operating costs, offsetting reserve income. [openai/gpt-5.4-mini]

- ■When crypto sentiment weakens, trading activity often cools, reducing transaction-driven revenue that supports many stablecoin ecosystems. Users may rotate into cash or short-duration government instruments, compressing growth for stablecoin platforms. [openai/gpt-5.4-mini]

- ■Stablecoin supply is not guaranteed to stay elevated in bear markets; redemptions, lower trading activity, and flight to bank deposits or Treasury funds can shrink balances, directly reducing interest income and making profitability uncertain. [openai/gpt-5.4-mini]

💭 Reasoning: The debate centered on whether stablecoins remain profitable and economically attractive during Bitcoin declines. The affirmative side provided strong empirical evidence from the 2021-2022 bear market, showing stablecoin market cap growth despite Bitcoin's 65% drop, indicating counter-cyclical demand. The negative side argued that profitability depends on multiple factors like reserve yields and redemption behavior, not solely on Bitcoin's direction, and that downturns can reduce trading activity and increase costs. However, the affirmative's concrete data on market cap expansion and the mechanism of flight-to-safety capital preservation outweighed the negative's theoretical concerns. The judge ruled in favor of TRUE with 88% confidence, supported by the observed resilience and growth of stablecoins during a major Bitcoin decline. Thus, stablecoins do maintain profitability and attractiveness as safe-haven alternatives during Bitcoin downturns.

📋 PRO Facts:

• During Bitcoin's 65% decline from November 2021 to November 2022, USDT market cap grew from $58B to $66B (+14%) and USDC from $35B to $44B (+26%) [coingecko.com].

• Stablecoin profitability is primarily driven by interest income on fiat reserves, which can increase when capital flows into stablecoins during market downturns.

📋 ANTI Facts:

• Stablecoin profitability depends on reserve yields, outstanding supply, redemption behavior, compliance costs, and market trust, not solely on Bitcoin's price direction [federalreserve.gov].

• A downturn can reduce trading activity, increase redemption pressure, and raise operating and liquidity costs, potentially offsetting reserve income [fsb.org].

1. Counter-Cyclical Capital Preservation [4] (μScore: 0.40)

The empirical evidence is decisive: during Bitcoin's catastrophic 65% decline from November 2021 (69,000) to November 2022 (24,000), stablecoin [33] market capitalization [22] expanded rather than contracted. USDT [39] grew from 58 billion to 66 billion (+14%), while USDC [38] surged from 35 billion to 44 billion (+26%) coingecko.com. This demonstrates that investors fleeing Bitcoin volatility don't exit the crypto ecosystem—they rotate into stablecoins as safe-haven assets. This flight-to-safety [16] behavior creates sustained demand and utility precisely when speculative assets falter, making stablecoins economically attractive during Bitcoin downturns.

2. Interest-Bearing Revenue Model Independence (μScore: 0.41)

Stablecoin issuer profitability operates through a fundamentally different mechanism than crypto trading or mining. Issuers generate revenue from interest on fiat reserves [15]—currently yielding 4-5% annually on Treasury securities. With combined stablecoin market capitalization exceeding 255 billion atlantic-council.org, issuers earn approximately 10-12 billion annually in interest income [17]. Critically, this revenue increases during Bitcoin bear markets as capital rotates into stablecoins, expanding the reserve base and amplifying interest earnings. This decoupling from Bitcoin price action makes stablecoin profitability reliable even during crypto winter.

| Revenue Source | Bull Market Dependency | Bear Market [2] Performance | Reliability |

|---|---|---|---|

| Bitcoin Mining | High (price-dependent) | Severely impacted | Low |

| Crypto Trading | High (volume-dependent) | Reduced activity | Low-Medium |

| Stablecoin Reserve Interest | Low (yield-dependent) | Often enhanced | High |

| Stablecoin Transaction Fees | Medium (activity-dependent) | Sustained utility | Medium-High |

Legend: Comparative analysis of crypto ecosystem revenue models during market stress. Stablecoin reserve interest shows highest reliability due to counter-cyclical capital flows.

3. Persistent DeFi [12] Infrastructure Utility (μScore: 0.48)

Stablecoins serve as the foundational infrastructure for decentralized finance, maintaining economic relevance through lending, borrowing, and yield-generation activities [40] that persist regardless of Bitcoin's trajectory. During the 2022 bear market, DeFi total value locked in stablecoin-denominated protocols remained substantial at 40-50 billion, with stablecoins comprising the majority of lending collateral [18] [7]. Daily stablecoin transaction volumes averaged 50-80 billion throughout 2022-2023 for payments, remittances, and DeFi operations—volume that persists irrespective of Bitcoin's price atlantic-council.org. This creates network effects [23] and economic moats that sustain profitability through multiple revenue streams.

The FALSE side raised legitimate concerns about structural risks during market stress, including redemption pressure [27], depegging [13] risk, and regulatory exposure. These risks are real—exemplified by the Terra/UST collapse in May 2022, which demonstrated that algorithmic stablecoins can fail catastrophically during market turmoil.

However, the FALSE side's core arguments suffered from two critical weaknesses:

- ■

Conflation of stablecoin types: The arguments failed to distinguish between fiat-collateralized stablecoins (USDT, USDC) and algorithmic stablecoins (UST). The former have proven resilient through multiple Bitcoin drawdowns, while the latter represent a fundamentally different risk profile.

- ■

Misunderstanding of revenue mechanics: The claim that stablecoin profitability depends on "market activity and confidence" incorrectly assumes stablecoin issuers profit from trading or transaction fees. The primary revenue driver—interest on reserves—actually benefits from capital rotation into stablecoins during Bitcoin declines.

The FALSE side's strongest point—that stablecoins face structural risks during risk-off [30] periods—is valid but doesn't negate the central claim. Fiat-backed stablecoins have demonstrated resilience across multiple Bitcoin bear markets, with market capitalization expanding during downturns rather than contracting.

The evidence strongly supports the TRUE position.

The empirical record shows that fiat-collateralized stablecoins have maintained and even enhanced profitability during every significant Bitcoin decline since 2018. The mechanism is straightforward: stablecoins offer crypto-native liquidity [19] without price exposure, making them indispensable during bear markets when traders seek to preserve capital or await re-entry opportunities.

| Bitcoin Drawdown [14] Period | Bitcoin Decline | USDT Change | USDC Change | Profitability Impact |

|---|---|---|---|---|

| 2018 Bear Market | -84% | +1.5B to 2B | N/A | Positive |

| Mar 2020 COVID Crash | -50% | +4B to 6B | +$0.5B | Positive |

| 2021-2022 Bear | -65% | +8B to 66B | +9B to 44B | Strongly Positive |

| 2024 Correction | -20% | Stable at 110B | Stable at 33B | Maintained |

Legend: Historical stablecoin performance during Bitcoin drawdowns. All major fiat-backed stablecoins expanded or maintained market cap during Bitcoin declines, enhancing issuer profitability through larger reserve bases. Sources: CoinGecko, CoinMarketCap historical data.

The opponent's concerns about structural risks are valid for certain stablecoin architectures (particularly algorithmic models), but the central claim specifically addresses whether stablecoins "remain profitable and economically attractive during periods of Bitcoin decline"—and for the dominant fiat-collateralized stablecoins that comprise over 90% of the market, the answer is unequivocally affirmative.

Verdict: The claim is TRUE. Stablecoins maintain profitability and economic attractiveness during Bitcoin declines through counter-cyclical capital flows, interest-bearing reserve revenue models, and persistent DeFi infrastructure utility. The historical record across multiple bear markets provides robust empirical support for this position.

Round 3

The strongest case against the claim is that stablecoin [33] profitability is not a simple consequence of Bitcoin [3] declines. It depends on reserve yields [29], outstanding supply, redemption behavior, compliance costs [8], and market trust. When Bitcoin falls, stablecoins may become relatively more useful as a parking asset, but that does not guarantee stronger economics for issuers or holders. A downturn can reduce trading activity, increase redemption pressure [27], and raise operating and liquidity [19] costs, all of which can offset reserve income. federalreserve.gov fsb.org

The most important weakness in the affirmative case is its reliance on reserve interest as if it were a permanent, downturn-proof profit engine. It is not. Reserve income rises and falls with interest rates, while stablecoin balances can contract when confidence weakens or users move to bank deposits and Treasury funds. Even if issuers earn meaningful carry [5] in a high-rate environment, that is a macro-rate story, not proof that Bitcoin declines themselves make stablecoins economically attractive. The claim therefore overstates causation and ignores the fragility of the revenue base. [circle.com](https://www.circle.com/en/usdc [38]) tether.io sec.gov

The affirmative side’s strongest point is that stablecoins can outperform Bitcoin on a relative basis during selloffs because they preserve nominal value and can attract flight-to-safety [16] capital. That is a real advantage. But relative stability is not the same as profitability, and “safe-haven [31] utility” is not the same as economic upside. Stablecoins can remain functional and widely used while still producing thin, volatile, or cost-sensitive economics for issuers. That distinction is the central reason the claim fails.

Overall, the debate stands like this: stablecoins can be more useful than Bitcoin during downturns, but the evidence does not support the stronger claim that they reliably remain profitable and economically attractive because Bitcoin is declining. The false side has the better argument on causation and on the limits of the reserve-income story, while the affirmative side’s best evidence supports resilience, not guaranteed profitability.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.344 | 0.110 | 36 | 60 | TRUE | TRUE | 88% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] APY — Annual Percentage Yield — The real rate of return earned on an investment, taking into account the effect of compounding interest, commonly used to express yields on stablecoin liquidity pools and DeFi lending.

[2] Bear market — A prolonged period of declining asset prices, typically defined as a drop of 20% or more from recent highs, such as Bitcoin's 65% drawdown from November 2021 to November 2022.

[3] Bitcoin — The first and most widely recognized cryptocurrency, used as a benchmark for crypto market sentiment and volatility in the debate.

[4] Capital preservation — An investment strategy focused on avoiding losses rather than seeking high returns, often achieved by rotating into stablecoins during Bitcoin declines.

[5] Carry — Yield carry — The net income generated from holding an asset, such as interest or dividends, minus the cost of funding; stablecoin issuers profit from carry on reserve assets like Treasury bills.

[6] Cash equivalents — Short-term, highly liquid investments that are readily convertible to a known cash amount, such as money market funds, used as stablecoin reserves.

[7] Collateral — Assets pledged by a borrower to secure a loan or derivative position; stablecoins often serve as collateral in DeFi lending protocols.

[8] Compliance costs — Expenses incurred by stablecoin issuers to meet regulatory requirements, including licensing, reporting, and anti-money laundering measures.

[9] Counter-cyclical demand — Demand that increases when the broader market declines; stablecoins exhibit counter-cyclical demand as investors flee Bitcoin volatility.

[10] Custody costs — Fees for the safekeeping and management of digital or financial assets, which stablecoin issuers must pay to custodians of their reserve holdings.

[11] DAI — A decentralized stablecoin pegged to the US dollar, maintained by the MakerDAO protocol through over-collateralized positions of crypto assets.

[12] DeFi — Decentralized Finance — Blockchain-based financial services that operate without traditional intermediaries, enabling lending, borrowing, and trading of stablecoins on protocols like Aave and Compound.

[13] Depegging — A situation where a stablecoin's market price deviates significantly from its intended peg, often caused by redemption pressure or loss of confidence.

[14] Drawdown — The peak-to-trough decline in an asset's price during a specific period, used to measure the severity of Bitcoin bear markets.

[15] Fiat reserves — Traditional currency holdings (e.g., USD, EUR) that back the value of fiat-collateralized stablecoins like USDT and USDC.

[16] Flight-to-safety — Investor behavior of moving capital from risky assets to safe havens during market stress; during Bitcoin declines, capital flows into stablecoins.

[17] Interest income — Revenue earned from lending or holding interest-bearing assets; stablecoin issuers generate interest income on fiat reserves held in Treasury bills and other instruments.

[18] Lending collateral — Assets deposited by borrowers in a DeFi protocol to secure loans; stablecoins are commonly used as lending collateral due to their price stability.

[19] Liquidity — The ease with which an asset can be bought or sold without causing a significant price change; stablecoins provide liquidity in crypto markets.

[20] Liquidity pool — A collection of tokens locked in a smart contract to facilitate decentralized trading; stablecoin liquidity pools offer yields through trading fees.

[21] Macro rates — Broad interest rate benchmarks set by central banks (e.g., Federal Reserve rates) that influence the yield on stablecoin reserve assets.

[22] Market capitalization — The total market value of a cryptocurrency, calculated by multiplying the current price by the circulating supply; used to measure stablecoin size and Bitcoin's value.

[23] Network effects — The phenomenon where a service becomes more valuable as more people use it; stablecoins benefit from network effects as adoption increases transactional utility.

[24] Overnight repos — Overnight repurchase agreements — Short-term borrowing agreements where one party sells securities and agrees to repurchase them the next day, used by stablecoin issuers to manage cash reserves.

[25] Peg — The fixed exchange rate mechanism of a stablecoin to a reference asset (e.g., 1 USDT ≈ 1 USD); maintaining the peg is critical for stablecoin credibility.

[26] Redemption confidence — Trust that a stablecoin can be exchanged for its underlying reserve asset at par without delay; erosion of confidence can trigger depegging.

[27] Redemption pressure — Heightened demand by holders to convert stablecoins into fiat currency, which can strain issuer reserves and lead to liquidity crises.

[28] Reserve management expenses — Costs associated with overseeing the portfolio of assets backing a stablecoin, including trading, custody, and compliance operations.

[29] Reserve yields — Interest or returns earned on the assets held in a stablecoin's reserve, typically from government bonds, repos, and cash equivalents.

[30] Risk-off — A market sentiment characterized by aversion to risk and a preference for safe assets; stablecoins serve as risk-off instruments during Bitcoin declines.

[31] Safe-haven — An asset expected to retain or increase its value during market turmoil; stablecoins are considered crypto safe-havens due to their price stability.

[32] Spread capture — Profit from the difference between the yield on reserve assets and the costs of maintaining the stablecoin ecosystem, including operational and compliance expenses.

[33] Stablecoin — A cryptocurrency designed to maintain a stable value relative to a reference asset (e.g., the US dollar), typically through fiat collateral, crypto collateral, or algorithmic mechanisms.

[34] Sticky circulation — The tendency of a stablecoin's circulating supply to remain elevated or grow even during bear markets, as investors park capital in stable assets.

[35] Total value locked (TVL) — Total Value Locked — The total value of assets deposited in a DeFi protocol, often denominated in stablecoins; TVL indicates the scale of DeFi activity.

[36] Transaction-driven revenue — Income generated from fees on transfers, trades, and payments using stablecoins, which can decline during bear markets due to reduced trading activity.

[37] Treasury bills — T-bills — Short-term U.S. government debt securities with maturities of one year or less, commonly held as reserve assets by stablecoin issuers to earn yield.

[38] USDC — USD Coin — A fiat-collateralized stablecoin issued by Circle, backed by USD reserves held in regulated financial institutions and Treasury bills.

[39] USDT — Tether — The largest fiat-collateralized stablecoin by market capitalization, issued by Tether Limited, backed by a reserve portfolio including Treasury bills and cash equivalents.

[40] Yield-generation activities — Strategies to earn returns on stablecoins, such as lending on DeFi protocols, providing liquidity to pools, or staking, often yielding 3-15% APY during bear markets.

The following financial data tables were referenced during the debate exchanges:

| Asset | Nov 2021 | Nov 2022 | Change | Market Behavior |

|---|---|---|---|---|

| Bitcoin | $69,000 | $24,000 | -65% | Sharp decline |

| USDT Market Cap | $58B | $66B | +14% | Counter-cyclical growth |

| USDC Market Cap | $35B | $44B | +26% | Safe-haven rotation |

Legend: Market capitalization data during Bitcoin's 2021-2022 bear market. Bitcoin price in USD; stablecoin market caps in billions USD. Source: CoinGecko historical data.

</FinancialData>

| Stablecoin | Circulation (2024) | Reserve Yield | Annual Revenue |

|---|---|---|---|

| USDT | $110B | ~4.5% | ~$4.95B |

| USDC | $33B | ~4.8% | ~$1.58B |

| DAI | $5B | ~5.0% | ~$0.25B |

| Total | ~$148B | ~4.6% avg | ~$6.8B |

Legend: Stablecoin issuer revenue from reserve interest at current Treasury yields. Circulation in USD billions; yields approximate based on 3-month T-bill rates. Source: issuer transparency reports.

</FinancialData>

| Metric | Bull Market (2021) | Bear Market (2022) | Persistence Rate |

|---|---|---|---|

| Stablecoin Daily Volume | $85B avg | $52B avg | 61% |

| DeFi TVL (Stablecoin) | $75B peak | $45B trough | 60% |

| Stablecoin Yield Pools | 8-15% APY | 3-8% APY | Active |

Legend: Stablecoin utility metrics comparing bull and bear market conditions. Volume in USD billions; TVL includes stablecoin-denominated DeFi protocols. Persistence rate shows retention during Bitcoin decline.

| Period | Bitcoin Price | USDT Market Cap | USDC Market Cap | Issuer Revenue Impact |

|---|---|---|---|---|

| Nov 2021 | $69,000 | $58B | $35B | Baseline |

| Nov 2022 | $24,000 | $66B | $44B | +$400M/year |

| 2024 Peak | $73,000 | $110B | $33B | +$4.5B/year |

Legend: Counter-cyclical stablecoin growth during Bitcoin volatility. Revenue impact represents additional annual interest income from expanded reserves at ~4.5% yield. Sources: CoinGecko, issuer transparency reports.

</FinancialData>

| Revenue Source | Bull Market Dependency | Bear Market Performance | Reliability |

|---|---|---|---|

| Bitcoin Mining | High (price-dependent) | Severely impacted | Low |

| Crypto Trading | High (volume-dependent) | Reduced activity | Low-Medium |

| Stablecoin Reserve Interest | Low (yield-dependent) | Often enhanced | High |

| Stablecoin Transaction Fees | Medium (activity-dependent) | Sustained utility | Medium-High |

Legend: Comparative analysis of crypto ecosystem revenue models during market stress. Stablecoin reserve interest shows highest reliability due to counter-cyclical capital flows.

</FinancialData>

| Bitcoin Drawdown Period | Bitcoin Decline | USDT Change | USDC Change | Profitability Impact |

|---|---|---|---|---|

| 2018 Bear Market | -84% | +$1.5B to $2B | N/A | Positive |

| Mar 2020 COVID Crash | -50% | +$4B to $6B | +$0.5B | Positive |

| 2021-2022 Bear | -65% | +$8B to $66B | +$9B to $44B | Strongly Positive |

| 2024 Correction | -20% | Stable at $110B | Stable at $33B | Maintained |

Legend: Historical stablecoin performance during Bitcoin drawdowns. All major fiat-backed stablecoins expanded or maintained market cap during Bitcoin declines, enhancing issuer profitability through larger reserve bases. Sources: CoinGecko, CoinMarketCap historical data.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.