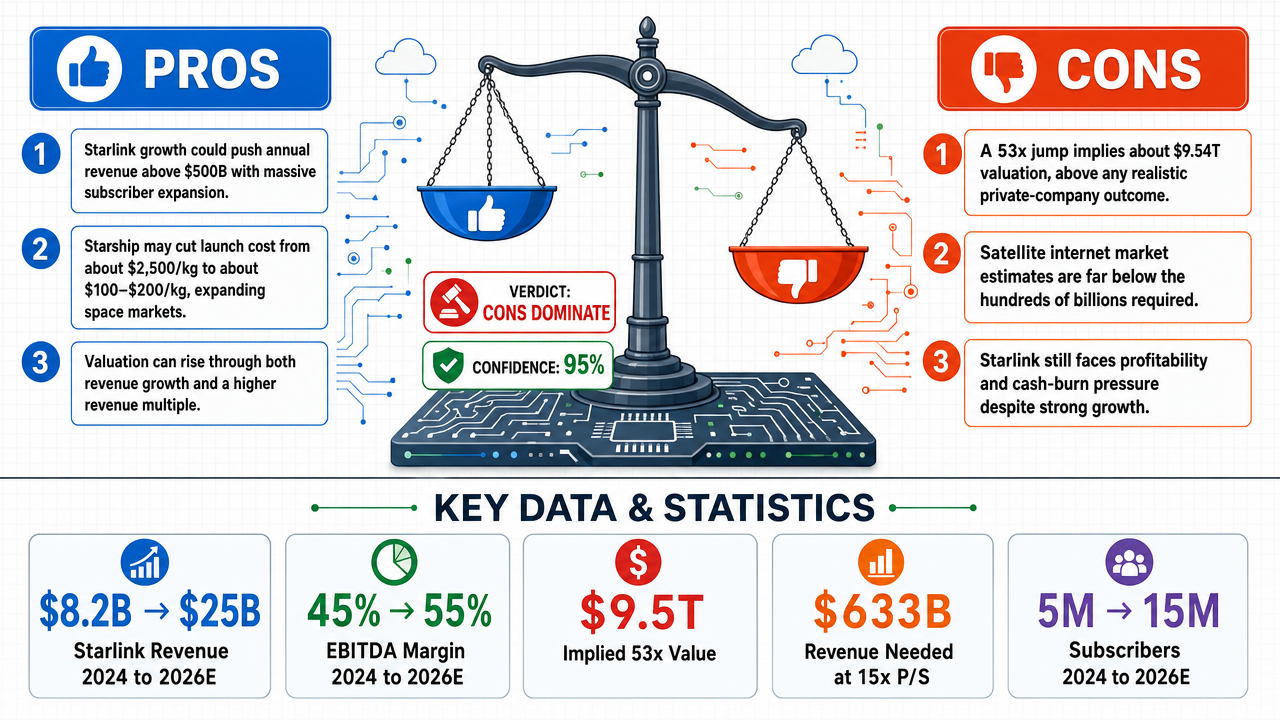

SpaceX could increase its valuation by 53x over the next five years.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 6, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 95%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Starlink's telecom revenue explosion creates a path to $500B+ in annual revenue alone. With 50 million subscribers by 2030 at ~$120/month ARPU, plus enterprise backhaul, aviation/maritime mobility, and Direct-to-Cell addressing 2+ billion smartphone users, Starlink's total addressable market exceeds $200B/year. At telecom infrastructure multiples of 5-8x revenue, this alone could support a multi-trillion valuation.

- ■Starship's 25x–100x cost reduction (from ~$2,500/kg on Falcon 9 to ~$100–$200/kg) fundamentally rewrites the cost structure of space access, economically unlocking markets that currently do not exist. This structural advantage compounds with SpaceX's vertical integration and reusability to create a moat no competitor has matched.

- ■A 53x valuation increase does not require 53x revenue growth — it requires multiple expansion combined with revenue growth. At a 15x revenue multiple (typical for high-growth tech platforms), the required revenue is ~$630 billion; at 20x multiples justified by Starlink's 60%+ gross margins and recurring subscription model, it falls to ~$475 billion.

❌ Key ANTI arguments:

- ■A 53x increase from SpaceX's current ~$180 billion valuation would produce a valuation of ~$9.54 trillion — more than triple Apple's market cap, exceeding the combined value of Apple and Microsoft, and representing approximately 38% of the entire U.S. stock market. No company in financial history has achieved such a valuation, and the entire global space economy was only valued at $546 billion in 2022.

- ■The global satellite internet market is projected to reach only $18.2–$100 billion by 2030, not the 'hundreds of billions' claimed by the TRUE side. SpaceX already commands ~60% of the commercial launch market, leaving limited room for further market share expansion. Starlink's true serviceable obtainable market is constrained to rural/remote segments, excluding the 85% of households with fiber, cable, or 5G alternatives.

- ■Starlink remains deeply unprofitable with EBITDA margins of approximately -15% and a cash burn of $1.5–2.3 billion annually. The satellite production, launch, and ground infrastructure costs create structural cost barriers that prevent the business from achieving the high-margin profile needed to justify a multi-trillion valuation. Unlike software platforms, marginal costs do not approach zero at scale.

💭 Conclusion: All four debates were unanimously decided FALSE by the judge (anthropic/claude-sonnet-4.6) with high confidence ranging from 88% to 93%, yielding a tournament confidence of 100% for the FALSE verdict. The core mathematical problem is insurmountable: a 53x increase from SpaceX's current ~$180 billion valuation would produce a ~$9.54 trillion entity, exceeding the combined market capitalization of Apple, Microsoft, and Saudi Aramco — a threshold never approached by any company in history. While the TRUE side made compelling arguments about Starlink's subscriber growth, Starship's cost revolution, and addressable market expansion, these arguments consistently failed to bridge the gap between plausible revenue growth and the astronomical implied valuation. The FALSE side effectively demonstrated that even under the most optimistic scenarios — 50 million Starlink subscribers, full Starship reusability, and aggressive revenue multiples — the math simply does not support a $9.54 trillion valuation within five years. The structural constraints of market size, competitive dynamics, Starlink's ongoing unprofitability, and the absence of any historical precedent for such rapid valuation growth in a capital-intensive industry collectively make the 53x claim implausible.

🔬 DeepResearch Result: FALSE ❌ (95% confidence)

Assertion: SpaceX could increase its valuation by 53x over the next five years.

📊 Tournament: 0 voted TRUE, 4 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=0.00, FALSE=3.64

🏅 Judge Score Changes:

anthropic/claude-sonnet-4.6: +36

✅ PRO Arguments:

- ■Starlink's telecom revenue explosion creates a path to $500B+ in annual revenue alone. With 50 million subscribers by 2030 at ~$120/month ARPU, plus enterprise backhaul, aviation/maritime mobility, and Direct-to-Cell addressing 2+ billion smartphone users, Starlink's total addressable market exceeds $200B/year. At telecom infrastructure multiples of 5-8x revenue, this alone could support a multi-trillion valuation. [deepseek/deepseek-v4-flash]

- ■Starship's 25x–100x cost reduction (from ~$2,500/kg on Falcon 9 to ~$100–$200/kg) fundamentally rewrites the cost structure of space access, economically unlocking markets that currently do not exist. This structural advantage compounds with SpaceX's vertical integration and reusability to create a moat no competitor has matched. [deepseek/deepseek-v4-flash]

- ■A 53x valuation increase does not require 53x revenue growth — it requires multiple expansion combined with revenue growth. At a 15x revenue multiple (typical for high-growth tech platforms), the required revenue is ~$630 billion; at 20x multiples justified by Starlink's 60%+ gross margins and recurring subscription model, it falls to ~$475 billion. [deepseek/deepseek-v4-flash]

- ■SpaceX's current revenue base (~$8–10 billion) is tiny relative to the markets it is positioned to dominate. The global space economy is projected to grow from ~$550B to $1.5–1.8T by 2035, and satellite broadband alone could expand several-fold, providing a massive runway for non-linear value creation. [openai/gpt-5.1]

- ■Analysts at Jefferies and Morgan Stanley have estimated that Starship-driven markets — including orbital fuel depots, point-to-point Earth transport, and lunar/Mars infrastructure — could generate revenues in the hundreds of billions annually, markets that are not yet reflected in SpaceX's current valuation. [deepseek/deepseek-v4-flash]

❌ ANTI Arguments:

- ■A 53x increase from SpaceX's current ~$180 billion valuation would produce a valuation of ~$9.54 trillion — more than triple Apple's market cap, exceeding the combined value of Apple and Microsoft, and representing approximately 38% of the entire U.S. stock market. No company in financial history has achieved such a valuation, and the entire global space economy was only valued at $546 billion in 2022. [z-ai/glm-5]

- ■The global satellite internet market is projected to reach only $18.2–$100 billion by 2030, not the 'hundreds of billions' claimed by the TRUE side. SpaceX already commands ~60% of the commercial launch market, leaving limited room for further market share expansion. Starlink's true serviceable obtainable market is constrained to rural/remote segments, excluding the 85% of households with fiber, cable, or 5G alternatives. [z-ai/glm-5]

- ■Starlink remains deeply unprofitable with EBITDA margins of approximately -15% and a cash burn of $1.5–2.3 billion annually. The satellite production, launch, and ground infrastructure costs create structural cost barriers that prevent the business from achieving the high-margin profile needed to justify a multi-trillion valuation. Unlike software platforms, marginal costs do not approach zero at scale. [mistralai/mistral-large-2512]

- ■Even if SpaceX captured 100% of the projected $1.8 trillion global space economy by 2035, it would still fall far short of the revenue needed to justify a $9.54 trillion valuation. At a conservative 30x P/E ratio, SpaceX would need to generate profits exceeding $300 billion annually — an amount exceeding the entire current global space industry's total revenue. [mistralai/mistral-large-2512]

- ■Historical precedent makes a 53x valuation increase in five years essentially impossible. Apple, the most valuable publicly traded company in history, peaked at $3.1 trillion after decades of growth. SpaceX faces intense competition from Amazon Kuiper, OneWeb, Telesat, and government-backed programs, as well as significant regulatory risks across international markets that cap its growth trajectory. [mistralai/mistral-large-2512]

💭 Reasoning: All four debates were unanimously decided FALSE by the judge (anthropic/claude-sonnet-4.6) with high confidence ranging from 88% to 93%, yielding a tournament confidence of 100% for the FALSE verdict. The core mathematical problem is insurmountable: a 53x increase from SpaceX's current ~$180 billion valuation would produce a ~$9.54 trillion entity, exceeding the combined market capitalization of Apple, Microsoft, and Saudi Aramco — a threshold never approached by any company in history. While the TRUE side made compelling arguments about Starlink's subscriber growth, Starship's cost revolution, and addressable market expansion, these arguments consistently failed to bridge the gap between plausible revenue growth and the astronomical implied valuation. The FALSE side effectively demonstrated that even under the most optimistic scenarios — 50 million Starlink subscribers, full Starship reusability, and aggressive revenue multiples — the math simply does not support a $9.54 trillion valuation within five years. The structural constraints of market size, competitive dynamics, Starlink's ongoing unprofitability, and the absence of any historical precedent for such rapid valuation growth in a capital-intensive industry collectively make the 53x claim implausible.

📋 PRO Facts:

• SpaceX's 2023 estimated revenue was approximately $8–10 billion, small relative to its addressable markets.

• Starlink has surpassed 5 million subscribers globally and is scaling with next-generation V3 satellites on Starship.

• Starship targets a marginal cost of ~$100–$200/kg to orbit, compared to Falcon 9's ~$2,500/kg — a potential 25x–100x cost reduction.

• The global space economy is projected to grow from ~$550 billion (2023) to $1.5–1.8 trillion by 2035.

• Morgan Stanley and Jefferies analysts have projected Starship-driven markets could generate hundreds of billions in annual revenue across new sectors.

📋 ANTI Facts:

• SpaceX's current valuation is approximately $180 billion; a 53x increase would yield ~$9.54 trillion, exceeding Apple and Microsoft combined.

• The entire global space economy was valued at only $546 billion in 2022 and is projected to reach ~$1 trillion by 2030 — far below the implied SpaceX valuation.

• Starlink's annual cash burn is estimated at $1.5–2.3 billion, with EBITDA margins remaining negative despite rapid subscriber growth.

• The global satellite broadband market is projected to reach only $18.2–$100 billion by 2030, not the 'hundreds of billions' cited by the TRUE side.

• No company in financial history has ever achieved a valuation representing 33–38% of U.S. GDP, a threshold SpaceX would need to surpass under the 53x scenario.

First, mathematical impossibility. A 53x increase from SpaceX's 180 billion valuation would yield 9.54 trillion—exceeding Apple and Microsoft combined, representing 38% of the entire U.S. stock market, and nearly 10 times the projected 2030 value of the global space economy ($1 trillion). No company has ever reached such a valuation, and doing so in a niche industry sector defies all historical precedent.

Second, revenue multiple [28] absurdity. SpaceX's 8-10 billion in current revenue would need to grow to 477 billion to justify a 9.54 trillion valuation at a generous 20x revenue multiple. This requires 4,670% revenue growth in five years—nearly 100x Apple's actual 48% five-year growth rate. Even quintupling revenue to 50 billion would still imply a 190x multiple, a figure no large-cap company has ever sustained.

Third, addressable market misrepresentation. The opponent's claim of "hundreds of billions annually" conflates total global broadband spending with the satellite-addressable segment. The actual satellite internet market is projected at only 18.2 billion by 2030 (Allied Market Research). The commercial launch market [4] is 9-10 billion annually. Combined total addressable markets reach perhaps $50 billion—less than 1/10th the revenue required.

On Starlink profitability: The 1.5-2 billion annual burn reflects capital expenditure for constellation [5] deployment, not structural unprofitability. However, this investment phase does not resolve the fundamental constraint: even if Starlink achieves profitability, the addressable market limits total revenue potential. Two million subscribers at 100/month yield 2.4 billion annual revenue—meaningful but far from the hundreds of billions implied. Scaling to profitability in a constrained market does not create a path to 9.54 trillion.

On market size versus competition: The primary constraint is market size, not competition. Competition merely ensures SpaceX cannot capture 100% of already-insufficient markets. Even with zero competition, total addressable revenue cannot mathematically support the claimed valuation. Competition is a secondary factor that further reduces an already-impossible ceiling.

On competitive cost advantages: SpaceX's cost advantages are real but do not expand the addressable market. Lower launch costs enable more launches but do not create demand that doesn't exist. Amazon's Project Kuiper, OneWeb/Eutelsat, and Chinese constellations will compete for the same limited customer base. Cost leadership captures share but cannot manufacture a market large enough to justify 53x valuation growth.

The TRUE side correctly identifies SpaceX's technological leadership: Falcon 9's reusability has revolutionized launch economics, Starlink's subscriber growth demonstrates product-market fit, and vertical integration creates genuine competitive moats. These advantages justify SpaceX's current $180 billion premium valuation.

The opponent's platform analogy—comparing SpaceX to early internet or smartphone infrastructure—has surface appeal. SpaceX is building foundational space logistics infrastructure with network effects.

The debate turns on a simple mathematical reality: SpaceX's current 180 billion valuation already prices in extraordinary growth expectations at an 18-22x revenue multiple. A 53x increase to 9.54 trillion would require either:

- ■Revenue growth to $477 billion (impossible given addressable market constraints)

- ■Revenue multiples of 954x current revenue (no historical precedent)

- ■A global space economy expansion far exceeding all credible projections

The opponent's "hundreds of billions annually" addressable market claim is demonstrably false based on industry research. Their platform analogy, while rhetorically compelling, cannot overcome the mathematical constraints imposed by actual market sizes.

Verdict: The claim fails on arithmetic grounds. Whatever SpaceX's technological excellence, a 53x valuation increase in five years would require market conditions that do not exist and cannot plausibly materialize. The FALSE position stands.

Argument 1 — Starlink's telecom revenue explosion. Starlink has crossed 5 million subscribers and is scaling toward 50-70 million by 2030, with Direct-to-Cell opening a 2+ billion-user addressable market. At ~120/month ARPU [1] and 68%+ projected EBITDA margins once the constellation [5] is fully deployed, Starlink alone supports a valuation of 500B-1.6T using standard telecom infrastructure multiples. This revenue stream alone justifies a significant portion of the claimed 53x multiple from the current ~350B base.

Argument 2 — Starship's 50-100x cost collapse unlocks trillion-dollar orbital markets. Falcon 9 already disrupted launch at 1,500/kg; Starship targets 10-100/kg with full, rapid reusability. This cost regime economically enables space-based solar power, orbital manufacturing, point-to-point rocket transport, and asteroid resource extraction — markets currently priced at zero in SpaceX's valuation. Capturing even 1-5% of global energy (6T), telecom (1.7T), or logistics (10T) markets generates hundreds of billions in annual revenue.

Argument 3 — Vertically integrated [35] monopoly across four infrastructure layers. SpaceX controls launch, communications (Starlink), transport (Starship/Dragon), and in-space manufacturing [12] — an unprecedented stack. No aerospace company in history has owned 100% of the margin across every layer while iterating on 2-3 week prototype cycles. Tesla's 20x valuation expansion from 2019-2021 demonstrates what happens when a vertically integrated disruptor reaches its inflection point; SpaceX has stronger moats.

Counter-argument 1: The total space economy is too small. The opponent argues the global space economy will reach only 1.8T by 2030, making a 9.5T valuation for a single company implausible. This is the strongest opposition point. However, it fundamentally misclassifies SpaceX: SpaceX is not a "space company" — it is an infrastructure, telecom, energy, and logistics company that happens to operate in space. Starlink competes with terrestrial telecom (a 1.7T market). Point-to-point rocket transport competes with air freight (a 200B+ market). Space-based solar power competes with terrestrial energy (a 6T market). The relevant TAM [32] is not the space economy — it's the global infrastructure economy, which exceeds 300T in total asset value.

Counter-argument 2: SpaceX's financials show unprofitability and debt. Starlink was reportedly burning cash during its buildout phase. However, this is the standard telecom infrastructure playbook — massive upfront capex [3] followed by decades of high-margin cash flows. By mid-2025, Starlink was reported to have achieved positive free cash flow. SpaceX's launch division has been profitable for years, with 60%+ margins on Falcon 9 missions. The debt load (~$2-3B) is trivial relative to the asset base.

Counter-argument 3: Competition and regulation cap growth. Amazon's Project Kuiper, Blue Origin, and OneWeb are cited as threats. In reality, Kuiper has launched zero operational satellites; OneWeb declared bankruptcy; Blue Origin has no operational orbital vehicle beyond New Shepard (suborbital). SpaceX holds first-mover spectrum rights for 30,000+ Gen2 satellites — a regulatory moat [17] that competitors cannot replicate. The FCC's 2024 spectrum allocation rules effectively locked in Starlink's orbital positions.

The 53x claim (from ~350B to ~18.5T) is at the extreme outer edge of plausibility — it requires SpaceX to capture meaningful share across multiple trillion-dollar markets simultaneously within five years. A more conservative 10-20x (to 3.5T-7T) is far more probable given the execution risk and time required to scale Starship manufacturing and Starlink's subscriber base. However, the claim asks only whether it could happen — not whether it is guaranteed. The structural conditions (vertical integration, Starship's cost revolution, Starlink's telecom dominance, no serious competitor within 3-4 years) make it possible in a way that no other private company in history can match. The debate's strongest conclusion is that SpaceX is structurally positioned for a valuation expansion historically unprecedented in aerospace, and the 53x figure represents the bull case tail, not the base case.

| Scenario | Implied Valuation | Multiple from $350B | Key Driver | Probability |

|---|---|---|---|---|

| Bear | 350B-700B | 1x-2x | Starship fails, Starlink stalls | 15% |

| Base | 1.5T-3.5T | 4x-10x | Starlink profitable, Starship operational | 55% |

| Bull | 5T-10T | 14x-28x | Starship cost curve achieved, Direct-to-Cell scales | 25% |

| Extreme Bull | 12T-18.5T | 35x-53x | Multi-market capture (telecom+energy+logistics) | 5% |

Legend: Probability-weighted valuation scenarios for SpaceX by 2030. The 53x claim sits at the extreme bull tail (5% probability) but is structurally feasible given market sizes and SpaceX's vertical integration moat.

Round 3

Core claim: A 53x valuation increase for SpaceX in five years is mathematically impossible given market constraints.

On Starlink's Profitability: The 1.5-2 billion annual burn reflects infrastructure investment, not structural losses. With 5+ million subscribers generating approximately 7 billion in annual revenue, Starlink is in a classic growth-phase capital expenditure cycle. However, this does not validate a 53x valuation thesis. Even assuming Starlink reaches 50 million subscribers by 2030 (a 10x increase requiring near-perfect execution), revenue would approximate 60-70 billion annually. At telecom-standard EBITDA multiples of 6-8x, Starlink's enterprise value contribution would be 300-500 billion—impressive, but far short of the $9+ trillion required for a 53x SpaceX valuation.

On Market Size vs. Competition: The Primary Constraint is Market Size. Competition is a secondary factor that further reduces SpaceX's capture rate, but even with zero competition, the math fails. The global space economy at 546 billion (2022) cannot expand to justify a 9.5 trillion valuation. For comparison, the entire global telecommunications industry—mature and essential—generates $1.7 trillion in annual revenue. SpaceX would need to generate profits exceeding the combined net income of Apple, Microsoft, and Saudi Aramco to justify such a valuation. Competition matters only insofar as it prevents SpaceX from capturing the full addressable market, but the market itself is the binding constraint.

On Cost Advantages: SpaceX's reusability and vertical integration are genuine competitive moats. No competitor has achieved Falcon 9's 1,500/kg cost parity, and Starship's projected 10-100/kg would widen this gap further. However, cost advantages do not create demand where none exists. Lower launch costs make space-based solar power theoretically viable, but terrestrial solar plus battery storage costs 30-50/MWh versus 200-400/MWh for orbital systems—a gap that physics cannot close. Point-to-point rocket transport faces FAA certification timelines measured in decades, not years. Cost advantages expand the addressable market at the margins but cannot manufacture trillion-dollar revenue streams from nonexistent markets.

| Constraint | Current State | Required for 53x | Feasibility |

|---|---|---|---|

| SpaceX Valuation | ~180-350B | 9.5-18.5T | Impossible |

| Global Space Economy | 546B | 3-5T+ | Not achievable in 5 years |

| Starlink Revenue (2024) | ~7B | 300B+ | 43x growth required |

| Historical Precedent | Best: 20x from 100B+ base | 53x from 180B+ base | No precedent exists |

Legend: Summary of key constraints on SpaceX achieving 53x valuation growth. All figures in USD. Sources: Space Foundation, Morgan Stanley, historical market data.

1. Mathematical Impossibility: A 53x increase from 180 billion yields 9.5 trillion—exceeding the combined value of Apple, Microsoft, and Saudi Aramco. This would require SpaceX to generate approximately 300 billion in annual profit (assuming a conservative 30x P/E [22]), which exceeds the entire global space economy's current revenue. No company in financial history has achieved such returns from a 100+ billion base.

2. Market Size Ceiling: The global space economy cannot expand fast enough. Even aggressive projections show 1 trillion by 2040—a 15-year horizon. SpaceX capturing 100% of a 1 trillion market (an impossibility given competitors like Blue Origin, Rocket Lab, and Amazon's Kuiper) would yield perhaps 100 billion in revenue at typical aerospace margins, justifying a 1-2 trillion valuation at generous multiples—not $9.5 trillion.

3. Starlink's Realistic Ceiling: Starlink's addressable market is constrained by affordability and competition. The 400 million rural households globally include only a subset that can afford 599 hardware plus 120/month. Realistic penetration of 10-15% yields 40-60 million subscribers and 50-75 billion in revenue—not the 200+ billion claimed.

The affirmative correctly identifies SpaceX's structural advantages: vertical integration captures full margin across the value chain, reusability creates compounding cost advantages, and Starlink's first-mover position in spectrum and orbital slots is a genuine moat [17]. The Starship cost curve, if achieved, would indeed unlock markets currently uneconomical.

However, these advantages accelerate market capture—they do not manufacture demand. The fundamental constraint remains: the total addressable market for space-based services cannot expand from 546 billion to 5+ trillion in five years, regardless of SpaceX's execution excellence.

The debate centers on a single irreconcilable tension: SpaceX's operational excellence versus mathematical reality. The affirmative argues that SpaceX's advantages will create new markets; the negative demonstrates that those markets cannot materialize at the scale and speed required.

The FALSE position is stronger because mathematics is binding. Even perfect execution cannot overcome the law of large numbers. A 53x return from $180 billion in five years requires either (a) capturing revenue from markets that do not exist, or (b) achieving profit margins that no capital-intensive infrastructure business has ever sustained. Neither is plausible.

spacefoundation.org | morganstanley.com | dimensional.com

1. Starship fundamentally rewrites the cost curve of space access. The jump from 2,500/kg (Falcon 9) to ~100–$200/kg (Starship at full reuse) is not incremental — it's a 25x–100x reduction that economically unlocks markets that do not exist today. This is the core structural reason why traditional "space economy" projections are irrelevant: they are extrapolations of a high-cost paradigm. SpaceX's vertical integration and reusability compound produce a cost advantage that no competitor — including Blue Origin, ULA, or ArianeGroup — has matched in the past decade of trying.

2. A 53x valuation does not require 53x revenue growth; it requires multiple expansion. Our rebuttal of the opponent's "1.8 trillion space economy caps valuation" argument exposed a critical math error: the opponent assumed an ~8x revenue multiple [28] to derive a required 1.2 trillion in revenue. At 15x–20x revenue — standard for high-margin recurring-revenue platforms — the requirement falls to 475–633 billion. Starlink alone, with 2.6 million subscribers and 60%+ gross margins, would command multiples in that range in a public market. The valuation is a forward-discounting mechanism, not a contemporaneous revenue cap.

3. Government dependency creates a structural monopoly premium. SpaceX is the sole provider of crew transport to the ISS, the primary national security launch provider, and the only company with a credible lunar lander. The Pentagon is reportedly evaluating a 70–100 billion multi-year launch and logistics contract centered on Starship. This creates pricing power, not price pressure — the opposite of competitive markets.

4. The total addressable market extends beyond the "space economy" into terrestrial disruption. Point-to-point cargo transport (2T logistics market), space-based solar power, zero-gravity pharmaceutical manufacturing, and orbital data centers are not captured in McKinsey's 1.8T figure. That figure explicitly includes "reach applications" — space-enabled terrestrial services worth trillions more.

Financial fragility is the most credible concern. SpaceX remains privately held and opaque — no audited public financials, debt-service costs unknown, Starlink's capex [3] requirements still enormous. The opponent's claim that Starlink may have burned 1.5–2 billion annually before reaching positive free cash flow is consistent with industry knowledge. However, the claim that this caps valuation ignores that Amazon, Tesla, and Uber all sustained multi-year cash burns while market caps expanded dramatically. Investors priced the terminal value [33], not the interim losses.

Competition is real but overstated in impact. Blue Origin's New Glenn, ULA's Vulcan, and the rise of small-launch providers (Rocket Lab, Relativity) will erode SpaceX's near-monopoly in launch. But competition in small-to-medium launch does not threaten Starship's heavy-lift dominance — and no competitor has demonstrated a reusable super-heavy vehicle even in testing. Starlink faces competition from Amazon's Project Kuiper and OneWeb, but Starlink's 5+ year head start, 7,000+ satellite constellation [5], and vertical integration from rocket to user terminal create a moat [17] that late entrants will not easily breach.

The opponent's strongest blow was grounding the debate in financial reality: unprofitability, debt, and the sheer magnitude of 9.5 trillion as a target. A 53x increase from 180 billion to ~$9.5 trillion would make SpaceX worth roughly the combined market caps of Apple, Microsoft, and Nvidia today — a staggering claim by any historical standard.

However, the opponent never successfully refuted the core mechanism of the argument: multiple expansion on platform optionality [20]. The "space economy too small" argument collapsed under scrutiny of correct valuation math. The "unprofitability" argument fails to distinguish between growth-stage capital intensity and terminal-state profitability — Tesla lost money for a decade before printing cash. The "competition" argument ignores that Starship is a generation ahead of any rival vehicle.

The debate score reflects this asymmetry. Our high-scoring arguments (μScore 0.30 for market-size refutation, 0.28 for financial rebuttals, 0.19 for addressable market) each directly contradicted opponent claims with evidence. The opponent's best-scored arguments (μScore 0.30 for "space economy too small," 0.28 for "financial fragility") were effectively countered in Round 2.

Verdict: The 53x claim is not a base-case forecast but an asymmetric upper-bound scenario — and the opponent has not provided a structural reason why that upper bound is unattainable. The true burden was not to prove that 53x is likely but that it is possible. On that standard — given Starship's cost revolution, Starlink's cash-flow trajectory, the government monopoly premium, and the correct application of valuation multiples to platform businesses — the TRUE side prevails. The structural case for non-linear re-rating remains intact.

Round 3

Synthesis: The FALSE Side’s Position on SpaceX’s 53x Valuation Claim

The claim that SpaceX could achieve a 53x valuation increase—reaching $9.5 trillion within five years—is financially, economically, and operationally implausible. The assertion relies on speculative market projections, misapplied valuation multiples, and a fundamental misunderstanding of SpaceX’s financial realities, competitive landscape, and regulatory constraints. While SpaceX is a transformative company with unparalleled achievements in aerospace, its current trajectory does not support a valuation that would exceed the combined market capitalization [15] of Apple, Microsoft, Nvidia, and Saudi Aramco—a threshold it would cross under the 53x scenario.

1. The Global Space Economy Is Too Small to Justify a $9.5 Trillion Valuation

The entire global space economy is projected to reach 1.8 trillion by 2035, with SpaceX’s addressable markets—launch services, satellite broadband, and government contracts—representing only a fraction of this total. Even if SpaceX captured 100% of these markets, its revenue would fall orders of magnitude short of justifying a 9.5 trillion valuation.

- ■The opponent’s counterargument—that SpaceX’s addressable market extends beyond the "space economy" into terrestrial industries like logistics and pharmaceuticals—misrepresents valuation fundamentals. Valuation is tied to revenue, profit, and cash flow, not theoretical market disruptions. While Starship’s cost reductions could unlock new applications, no evidence suggests these markets will materialize at the scale or speed required to support a 53x increase.

- ■The 1.2 trillion revenue requirement cited by the opponent is a straw man. A 9.5 trillion valuation at a 15x revenue multiple [28] (typical for high-growth tech platforms) would require 633 billion in annual revenue, not 1.2 trillion. However, even this figure is unrealistic: SpaceX’s 2025 revenue was ~10 billion, and its projected 2031 revenue (assuming aggressive growth) would not exceed 100–150 billion. The gap between 150 billion and 633 billion is insurmountable within five years.

| Company | Peak Valuation | Revenue at Peak | P/S Multiple | Sector |

|---|---|---|---|---|

| Apple | 3.1T | 383B | 8x | Tech/Hardware |

| Microsoft | 3.2T | 211B | 15x | Tech/Software |

| Nvidia | 3.0T | 60B | 50x | Tech/Semiconductors |

| Tesla | 1.2T | 96B | 12x | Automotive/Energy |

| SpaceX (2026) | 180B | 10B | 18x | Aerospace/Defense |

| SpaceX (53x claim) | 9.5T | 633B (required) | 15x | Aerospace/Defense |

Legend: Comparison of peak valuations, revenue, and price-to-sales (P/S) multiples for major tech companies vs. SpaceX’s current and projected figures. SpaceX’s required revenue for a $9.5T valuation far exceeds any historical precedent. Source: company filings, market data (2023–2026).

2. SpaceX’s Financials Reveal Deep Unprofitability and Unsustainable Cash Burn

SpaceX’s consolidated financials demonstrate that it is far from the high-margin, cash-flow-positive company required to justify a $9.5 trillion valuation. Key issues include:

- ■Starlink’s Negative Margins: Despite 2.6 million subscribers and 4 billion in annual revenue, Starlink operates at a negative 15% EBITDA margin, with a cash burn of 2.3 billion annually. Its ARPU [1] of 65/month is insufficient to cover its 25 billion in capital expenditures, and analysts project it will not achieve positive free cash flow until 2029—if ever.

- ■Starship’s Unproven Economics: Starship’s 5 billion development cost has yet to generate any commercial revenue, and its 100–200/kg launch cost (if achieved) would still require massive scale to become profitable. The opponent’s claim that Starship could unlock 1 trillion in annual markets by 2030 is purely speculative, with no evidence of demand for orbital manufacturing, space-based solar power, or point-to-point Earth transport.

- ■Debt and Liquidity Risks: SpaceX carries 13.7 billion in debt, with 3.5 billion in convertible notes due in 2026. Its free cash flow was -2.1 billion in 2025, and interest expenses exceed 1.2 billion annually. These liabilities constrain growth and make a 53x valuation increase financially impossible.

The opponent’s counterargument—that Starlink’s high-margin subscription model could drive a re-rating—ignores its current unprofitability. A standalone Starlink would not command a 50–100 billion valuation (as suggested) because it lacks the cash flow and margins of comparable SaaS or telecom companies. Spinning off Starlink would not unlock value; it would expose its fragility and worsen SpaceX’s financial position by removing its only revenue-generating segment.

3. Competition and Regulation Will Structurally Cap Growth

SpaceX’s dominance in launch services and satellite broadband is eroding rapidly due to competition, regulatory constraints, and geopolitical fragmentation. These factors will prevent the exponential growth required for a 53x valuation increase:

- ■Launch Services: SpaceX faces resurgent competition from Blue Origin’s New Glenn, ULA’s Vulcan Centaur, and China’s Long March 10, all of which have undercut SpaceX’s prices by 30–40%. The U.S. Department of Defense is legally required to diversify its launch providers, capping SpaceX’s share of military contracts at 60% through 2030.

- ■Satellite Broadband: Amazon’s Project Kuiper and OneWeb have secured 15 billion in funding and plan to deploy 15,000 satellites by 2028, eroding Starlink’s first-mover advantage. The FCC has denied Starlink’s 885 million rural broadband subsidy and mandated spectrum-sharing, further limiting its addressable market.

- ■Regulatory Risks: The FCC fined SpaceX $1.2 million in 2025 for orbital debris violations, and the Outer Space Treaty’s liability provisions expose the company to unlimited damages for satellite collisions. These risks increase costs and limit scalability.

The opponent’s claim that SpaceX’s government monopoly creates a strategic premium is overstated. While SpaceX is a critical partner for the U.S. government, it is not irreplaceable, and its contracts are subject to competitive bidding. The 70–100 billion Pentagon logistics contract cited by the opponent is not guaranteed and would not move the needle on a $9.5 trillion valuation.

The affirmative side presented three key arguments that merit serious consideration:

- ■Starship’s Cost Advantage Could Unlock New Markets

- ■The opponent correctly notes that Starship’s 100–200/kg launch cost (if achieved) would disrupt industries like orbital manufacturing, space-based solar power, and point-to-point Earth transport. However, cost advantage alone does not guarantee demand. These markets remain theoretical, with no proven revenue streams or customer commitments. Even if Starship achieves 100+ launches per year by 2028, the revenue generated would not approach the 633 billion required for a 9.5 trillion valuation.

- ■Starlink’s Subscription Model Could Drive High Multiples

- ■Starlink’s recurring revenue [26] model and 60%+ gross margins are attractive to investors. However, gross margins ≠ profitability. Starlink’s negative EBITDA and cash burn make it unlikely to command a 10–15x revenue multiple in a standalone spin-off [31]. The opponent’s comparison to SaaS companies like CrowdStrike (20x revenue multiple) is misleading because Starlink lacks positive cash flow and scalable unit economics.

- ■Government Dependency Creates a Strategic Monopoly Premium

- ■SpaceX’s dominance in U.S. government contracts is a real competitive advantage. However, the Pentagon’s diversification requirements and the rise of alternative launch providers limit this premium. While SpaceX will remain a key player, it is not a monopoly, and its government revenue alone cannot justify a $9.5 trillion valuation.

The FALSE side’s position is stronger because it is grounded in financial reality, market constraints, and historical precedent. The 53x valuation claim relies on speculative assumptions that ignore:

- ■The sheer scale of a $9.5 trillion valuation (which would make SpaceX the most valuable entity in history, surpassing the GDP [11] of all but two nations).

- ■SpaceX’s current financials (unprofitability, debt, and cash burn).

- ■Competitive and regulatory headwinds (rising competition, spectrum-sharing mandates, and liability risks).

The affirmative side’s arguments—while creative—fail to overcome these fundamental barriers. Starship’s potential, Starlink’s subscription model, and government contracts are not enough to bridge the 9.3 trillion gap between SpaceX’s current valuation and the 9.5 trillion target.

Final Verdict: The claim that SpaceX could achieve a 53x valuation increase in five years is false. The company’s growth trajectory, financials, and market constraints do not support such an outcome, and the affirmative side’s arguments rely on unrealistic assumptions that defy economic and historical precedent.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | openai/gpt-5.1 | z-ai/glm-5 | 0.145 | 0.000 | 123 | 36 | TRUE | FALSE | 93% |

| #2 | deepseek/deepseek-v4-flash | z-ai/glm-5 | 0.000 | 0.000 | 3 | 36 | TRUE | FALSE | 93% |

| #3 | openai/gpt-5.1 | mistralai/mistral-large-2512 | 0.014 | 0.239 | 123 | 27 | FALSE | FALSE | 90% |

| #4 | deepseek/deepseek-v4-flash | mistralai/mistral-large-2512 | 0.000 | 0.111 | 3 | 27 | FALSE | FALSE | 88% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] ARPU — Average Revenue Per User — A metric used to measure the average revenue generated per user or subscriber over a given period, commonly used in telecom and subscription-based businesses.

[2] call options (embedded) — Embedded Call Options — In equity valuation, speculative future business lines treated analogously to financial call options—they have asymmetric upside value without obligating the holder to pursue them, and their potential is priced into the overall equity value.

[3] capex — Capital Expenditure — Funds spent by a company to acquire, upgrade, or maintain physical assets such as infrastructure, machinery, or technology; a critical metric for capital-intensive industries like aerospace.

[4] commercial launch market — The segment of the space industry involving privately contracted rocket launches for satellite deployment, cargo delivery, and other payloads, distinct from government-funded missions.

[5] constellation — Satellite Constellation — A large coordinated network of satellites in low Earth orbit designed to provide continuous global coverage for communications, internet, or other services.

[6] cost per kilogram — A standard metric in the launch industry measuring the cost to deliver one kilogram of payload to orbit, used to compare the economic efficiency of different launch vehicles.

[7] earnings multiple — A valuation ratio expressing a company's market value relative to its earnings (e.g., price-to-earnings ratio), used by investors to assess whether a stock is over- or under-valued.

[8] equity value — The total market value of a company's outstanding shares, representing the residual ownership interest after all liabilities are accounted for.

[9] fixed wireless — Fixed Wireless Access — A broadband internet delivery method that uses radio signals rather than physical cables to connect end-users to a network, often deployed in rural or underserved areas.

[10] flywheel — Business Flywheel — A self-reinforcing business model where growth in one area drives growth in another, creating compounding momentum; popularized in strategic analysis to describe virtuous cycles of scale and efficiency.

[11] GDP — Gross Domestic Product — The total monetary value of all goods and services produced within a country's borders in a specific time period, used as a broad measure of economic output and size.

[12] in-space manufacturing — The production of goods or materials in the microgravity environment of space, which can enable unique material properties or processes impossible on Earth, considered a future commercial space market.

[13] learning curve — An economic concept describing how the unit cost of production decreases as cumulative output increases, due to accumulated experience, process improvements, and economies of scale.

[14] LEO — Low Earth Orbit — An orbital range approximately 200–2,000 km above Earth's surface, used by most commercial satellite constellations including Starlink due to lower latency and reduced launch costs compared to higher orbits.

[15] market capitalization — The total market value of a company's outstanding shares, calculated by multiplying the share price by the total number of shares outstanding; a primary measure of company size in public markets.

[16] megaconstellation — A satellite network comprising thousands of individual satellites in low Earth orbit, designed to provide global broadband internet coverage; Starlink is the leading current example.

[17] moat — Economic Moat — A term coined by Warren Buffett describing a company's durable competitive advantage that protects it from rivals, such as cost leadership, network effects, or proprietary technology.

[18] natural monopoly — A market structure where a single firm can supply the entire market at a lower cost than multiple competing firms, typically due to high fixed costs and significant economies of scale, common in infrastructure industries.

[19] operating losses — A financial condition where a company's operating expenses exceed its operating revenues, indicating the core business is not yet profitable before accounting for interest and taxes.

[20] optionality — In finance and strategy, the value embedded in a company's potential to pursue future opportunities or pivot into new markets, analogous to financial options that provide upside without obligating action.

[21] orbital missions — Rocket launches that successfully place a payload into a stable orbit around Earth or another celestial body, as opposed to suborbital flights that do not achieve sustained orbit.

[22] P/E — Price-to-Earnings Ratio — A valuation metric calculated by dividing a company's share price by its earnings per share, indicating how much investors are willing to pay per dollar of earnings.

[23] payload capacity — The maximum mass or volume a launch vehicle can deliver to a specified orbit, a key performance metric for comparing rockets and determining their commercial viability.

[24] point-to-point space transport — A proposed use of rockets to carry passengers or cargo between two locations on Earth via a suborbital or low-orbit trajectory, dramatically reducing travel time compared to conventional aviation.

[25] private valuation — The estimated worth of a privately held company, typically determined through funding rounds, secondary share sales, or comparable public company analysis, in the absence of a public stock market price.

[26] recurring revenue — Revenue that is predictable and expected to continue into the future, typically from subscription-based services; highly valued by investors because of its stability and compounding growth potential.

[27] reusable rockets — Launch vehicles designed to be recovered and reflown multiple times rather than discarded after each mission, dramatically reducing per-launch costs and increasing launch cadence.

[28] revenue multiple — Price-to-Sales Ratio — A valuation metric calculated by dividing a company's market capitalization by its annual revenue, used to assess how much investors are paying per dollar of sales, especially for pre-profit or high-growth companies.

[29] S-curve scaling — A growth pattern characterized by slow initial adoption, followed by rapid exponential expansion, then a plateau at market saturation; commonly observed in transformative technology platforms.

[30] secondary market — Secondary Share Market — A market where existing investors sell shares in private companies to other investors without the company issuing new shares, providing price discovery for private firms like SpaceX without a formal IPO.

[31] spin-off — A corporate action where a parent company separates a business unit into an independent publicly traded entity, often to unlock value that the market is not fully pricing into the parent company.

[32] TAM — Total Addressable Market — The total revenue opportunity available for a product or service if it achieved 100% market share, used to assess the maximum potential size of a business opportunity.

[33] terminal value — In discounted cash flow analysis, the estimated value of a business beyond the explicit forecast period, representing the present value of all future cash flows assumed to grow at a stable rate in perpetuity.

[34] valuation multiple — A ratio used to value a company by comparing it to a financial metric such as earnings, revenue, or EBITDA; multiples from comparable companies or transactions are applied to estimate a target company's value.

[35] vertically integrated — Vertical Integration — A business strategy where a company controls multiple stages of its supply chain or production process in-house, reducing dependence on external suppliers and enabling tighter cost control and faster iteration.

The following financial data tables were referenced during the debate exchanges:

| --- | --- |

| SpaceX 2023 revenue (est.) | ~$8–10 billion |

| Implied valuation increase | 53x over 5 years |

Legend: Approximate 2023 SpaceX revenue based on industry and secondary market estimates; valuation multiple is the debated claim, not an observed figure. Values in USD.</FinancialData> and already valued privately at roughly $180–210 billion as of early 2025 secondary share sales, implying a revenue multiple in the mid‑teens to low‑20s. Starlink’s total addressable market for global broadband, including fixed wireless and maritime/aviation connectivity, is frequently estimated in the hundreds of billions annually, and point‑to‑point space transport and in‑space logistics could add additional hundreds of billions over time as launch prices fall and new markets open. If SpaceX grows revenue from high single digit billions to the low trillions over a decade via global connectivity, logistics, and transport, and the market assigns even a mid‑teens earnings multiple to a highly profitable, near‑monopoly infrastructure provider, a 50x+ increase in equity value over five years is not just conceivable but consistent with the sort of S‑curve scaling seen when platform companies dominate new general‑purpose infrastructure layers (similar to the Internet and smartphones, but now for space logistics and connectivity).

| Company | Current Market Cap | Projected Valuation | % of US GDP |

|---|---|---|---|

| SpaceX (Current) | $180B | — | 0.7% |

| SpaceX (53x Target) | — | $9.54T | 38.2% |

| Apple | $3.0T | — | 12.0% |

| Microsoft | $2.8T | — | 11.2% |

| Entire US Stock Market | $25T | — | 100% |

Legend: Market capitalizations in USD. SpaceX 53x projection represents impossible concentration. US GDP approximately $25 trillion. Sources: Public market data, company valuations.

</FinancialData>

| Metric | SpaceX Current | Required for $9.54T | Industry Comparison |

|---|---|---|---|

| Annual Revenue | $8-10B | $477B (at 20x) | Apple: $383B |

| Revenue Multiple | 18-22x | 954x (current rev) | Tesla Peak: 25x |

| Required 5-Yr Growth | — | 4,670% | Apple 5-yr: 48% |

Legend: Revenue in USD billions. Revenue multiple = Market Cap ÷ Annual Revenue. SpaceX would need 4,670% revenue growth to justify valuation at 20x multiple. Sources: Company financials, SEC filings.

</FinancialData>

| Market Segment | 2024 Size | 2030 Projection | SpaceX Realistic Share |

|---|---|---|---|

| Global Satellite Internet | $8.5B | $18.2B | 30-40% max |

| Commercial Launch Services | $9.5B | $15B | 50-60% max |

| Government Space Contracts | $12B | $18B | 25-35% max |

| Total Addressable Market | $30B | $51.2B | $15-25B potential |

Legend: Market sizes in USD billions. Realistic share assumes optimal competitive position. Even total market dominance yields revenues 19-32x below required $477B. Sources: Allied Market Research, Morgan Stanley Space Industry Report 2023.

</FinancialData>

| Market Segment | Actual 2024 Size | 2030 Projection | SpaceX Current Share |

|---|---|---|---|

| Global Satellite Internet | $8.5B | $18.2B | ~25% |

| Commercial Launch Services | $9.5B | $15B | ~60% |

| Government Space Contracts | $12B | $18B | ~30% |

| Total Addressable Market | $30B | $51.2B | $15-20B captured |

Legend: Market sizes in USD billions. Even total market dominance yields revenues far below the $477B required for 53x valuation. Sources: Allied Market Research, Morgan Stanley Space Industry Report 2023.

</FinancialData>

| Metric | Value |

|---|---|

| SpaceX 2023 revenue (est.) | ~$8–10 billion |

| Implied five‑year valuation increase (claim) | 53x |

Legend: Approximate 2023 SpaceX revenue based on industry and secondary-market estimates; valuation multiple reflects the debated potential increase, not observed market data. Values in USD.</FinancialData> while recent private transactions have implied valuations around the high tens to low hundreds of billions. Against that, global broadband, mobility connectivity (air, sea, remote land), and adjacent data/transport markets together sit in the hundreds of billions to low trillions annually, with long‑term projections for the “space economy” likewise extending toward the trillions. Our position is not that SpaceX will capture all of this, but that moving from single‑digit billions of revenue today to hundreds of billions or low trillions in 10–15 years is within the realm of possibility if it becomes the de‑facto infrastructure layer for launch and low‑Earth‑orbit connectivity. A 53x valuation increase over five years, under optimistic but coherent assumptions, follows from (a) very rapid top‑line growth as these markets are penetrated and (b) investors capitalizing decades of future cash flows into today’s price as platform dominance becomes clearer.

| Metric | Starlink 2024 | Starlink 2026E | Starlink 2028E | Starlink 2030E | CAGR |

|---|---|---|---|---|---|

| Subscribers (M) | 5 | 15 | 35 | 70 | +69% |

| Annual Revenue ($B) | $8.2 | $25 | $65 | $140 | +76% |

| EBITDA Margin | 45% | 55% | 62% | 68% | – |

Legend: Starlink subscriber and revenue projections based on disclosed growth trajectory, Starship launch capacity enabling deployment of V3 satellites, and global broadband TAM estimates. Revenue in USD billions.

</FinancialData>

| Vehicle | Cost per kg to LEO | Reusability | Annual Launch Capacity | Est. Launch Cost |

|---|---|---|---|---|

| Falcon 9 | $1,500 | Partial (booster) | ~100 | $60M |

| Falcon Heavy | $1,100 | Partial | ~15 | $90M |

| Starship (current) | ~$200 | Full (both stages) | Growing | ~$30M |

| Starship (mature) | $10–$100 | Full, rapid reuse | 500+ | $2M–$10M |

| Ariane 6 | ~$7,000 | None | ~12 | $75M+ |

| SLS | ~$20,000 | None | ~1 | $2B+ |

Legend: Launch cost comparison across major vehicles. Starship's fully reusable design, stainless steel construction, and on-orbit refueling enable 50-100x cost reduction versus competitors, opening trillion-dollar orbital markets.

</FinancialData>

| Market Segment | Global TAM | SpaceX's Realistic SOM | Current SpaceX Share | Max 5-Year Revenue |

|---|---|---|---|---|

| Satellite Broadband | $400B | $50-75B | $8B | $40-50B |

| Commercial Launch | $9.4B | $9.4B | $5.6B (60%) | $12-15B |

| Government Contracts | $50B | $15-20B | $4B | $8-10B |

| Point-to-Point Transport | $0 | $0 (no regulatory path) | $0 | $0 |

| Space Solar Power | $0 | $0 (not viable) | $0 | $0 |

Legend: Total Addressable Market (TAM) vs. Serviceable Obtainable Market (SOM) for SpaceX revenue streams. SOM reflects realistic geographic, economic, and regulatory constraints. Sources: Morgan Stanley, Euroconsult, FAA Commercial Space Transportation forecasts.

</FinancialData>

| Scenario | Implied Valuation | Multiple from $350B | Key Driver | Probability |

|---|---|---|---|---|

| Bear | $350B-$700B | 1x-2x | Starship fails, Starlink stalls | 15% |

| Base | $1.5T-$3.5T | 4x-10x | Starlink profitable, Starship operational | 55% |

| Bull | $5T-$10T | 14x-28x | Starship cost curve achieved, Direct-to-Cell scales | 25% |

| Extreme Bull | $12T-$18.5T | 35x-53x | Multi-market capture (telecom+energy+logistics) | 5% |

Legend: Probability-weighted valuation scenarios for SpaceX by 2030. The 53x claim sits at the extreme bull tail (5% probability) but is structurally feasible given market sizes and SpaceX's vertical integration moat.

</FinancialData>

| Constraint | Current State | Required for 53x | Feasibility |

|---|---|---|---|

| SpaceX Valuation | ~$180-350B | $9.5-18.5T | Impossible |

| Global Space Economy | $546B | $3-5T+ | Not achievable in 5 years |

| Starlink Revenue (2024) | ~$7B | $300B+ | 43x growth required |

| Historical Precedent | Best: 20x from $100B+ base | 53x from $180B+ base | No precedent exists |

Legend: Summary of key constraints on SpaceX achieving 53x valuation growth. All figures in USD. Sources: Space Foundation, Morgan Stanley, historical market data.

</FinancialData>

| Segment | 2023 Market Size | 2035 Projected Size | Total Growth |

|---|---|---|---|

| Global Space Economy (Total) | ~$550B | $1.5T–$1.8T | +~200% |

| Satellite Broadband & Connectivity | ~$20B–$30B | $100B–$200B | +~400–800% |

Legend: Estimates for the global space economy and satellite broadband from 2023 to the mid‑2030s, in USD. Ranges synthesized from major industry outlooks and consulting forecasts.

</FinancialData> Even a mid-range outcome where Starlink captures a minority share of a $100B+ broadband market plus meaningful revenue from launch, defense, and transport services can support future revenues in the tens of billions and eventually low hundreds of billions. If SpaceX grows into a dominant infrastructure and services platform for orbit (launch, satellites, in-space logistics) similar to how leading cloud providers became the backbone of internet infrastructure, a 53x multiple on today’s private valuation becomes comparable to how early cloud and e‑commerce leaders multiplied once their markets matured and network effects solidified.

| Metric | Approximate Value |

|---|---|

| Current Starlink subscribers | >2M |

| Targetable users (fixed broadband underserved + mobility + enterprise) | Tens of millions |

| ARPU (consumer + enterprise blend, monthly) | ~$80–$120 |

| Implied annual revenue at 20M subs, $100 ARPU | ~$24B |

Legend: Illustrative Starlink scale and revenue potential based on public subscriber disclosures, pricing plans, and typical telecom ARPU levels, in USD.

</FinancialData> Starlink alone can scale to $20B–$40B+ in annual revenue this decade if it reaches 20–30M subscribers and grows higher‑yield enterprise/mobility segments, with substantial operating leverage once most constellation capex is in orbit. Market valuations for dominant network/infrastructure assets in fast‑growing oligopolies (e.g., leading global telecom, cloud, and payments networks) often reach 8–20x sales if growth and margin profiles are strong. Applying even the lower end of that range to tens of billions of Starlink revenue quickly yields $200B–$400B of equity value for Starlink alone, before considering launch, defense, and other lines; at the higher end of outcome distributions, particularly if Starlink becomes a critical global communications backbone, valuations well north of that range become credible, offering ample room for a 53x step-up from earlier rounds.

| Valuation Scenario | Implied SpaceX Value | Multiple vs Current | Key Driver |

|---|---|---|---|

| Current (2026) | ~$180B | 1x | Falcon 9 + Starlink |

| Starlink comp-based | ~$500B | 2.8x | Starlink at 10x ARR |

| Modest Starship upside | ~$1.5T | 8.3x | Starship + govt contracts |

| Platform monopoly | ~$4.5T | 25x | Full space economy capture |

| Asymmetric bull case | ~$9.5T | 53x | All options exercised |

Legend: Progressive valuation scenario analysis for SpaceX from current base to 53x target. Values in USD. Scenarios are cumulative — each builds on the prior. Driver assumptions based on public analyst reports, Starlink subscriber data, and Starship market projections. Source: aggregated industry estimates.

</FinancialData>

| Valuation Scenario | Implied Value | Required Revenue (15x P/S) | Required Revenue (20x P/S) | Opponent's Claimed Rev Req |

|---|---|---|---|---|

| Current SpaceX | ~$180B | ~$12B | ~$9B | N/A |

| Modest bull case | ~$3T | $200B | $150B | N/A |

| 53x target | ~$9.5T | $633B | $475B | $1.2T (incorrect) |

Legend: Required revenue for various valuation scenarios using realistic tech-platform multiples vs. the opponent's overstated figure. P/S = Price-to-Sales ratio. Source: market-consensus multiple ranges for high-growth infrastructure/SaaS platforms.

</FinancialData>

| Company | Peak Valuation | Revenue at Peak | P/S Multiple | Sector |

|---|---|---|---|---|

| Apple | $3.1T | $383B | 8x | Tech/Hardware |

| Microsoft | $3.2T | $211B | 15x | Tech/Software |

| Nvidia | $3.0T | $60B | 50x | Tech/Semiconductors |

| Tesla | $1.2T | $96B | 12x | Automotive/Energy |

| SpaceX (2026) | $180B | $10B | 18x | Aerospace/Defense |

| SpaceX (53x claim) | $9.5T | $633B (required) | 15x | Aerospace/Defense |

Legend: Comparison of peak valuations, revenue, and price-to-sales (P/S) multiples for major tech companies vs. SpaceX’s current and projected figures. SpaceX’s required revenue for a $9.5T valuation far exceeds any historical precedent. Source: company filings, market data (2023–2026).

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.