Should I buy Silver (the metal) ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed July 12, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 80%

Web Report: https://solsice.com/public/debates/should-i-buy-silver-the-metal-bbef95987171

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

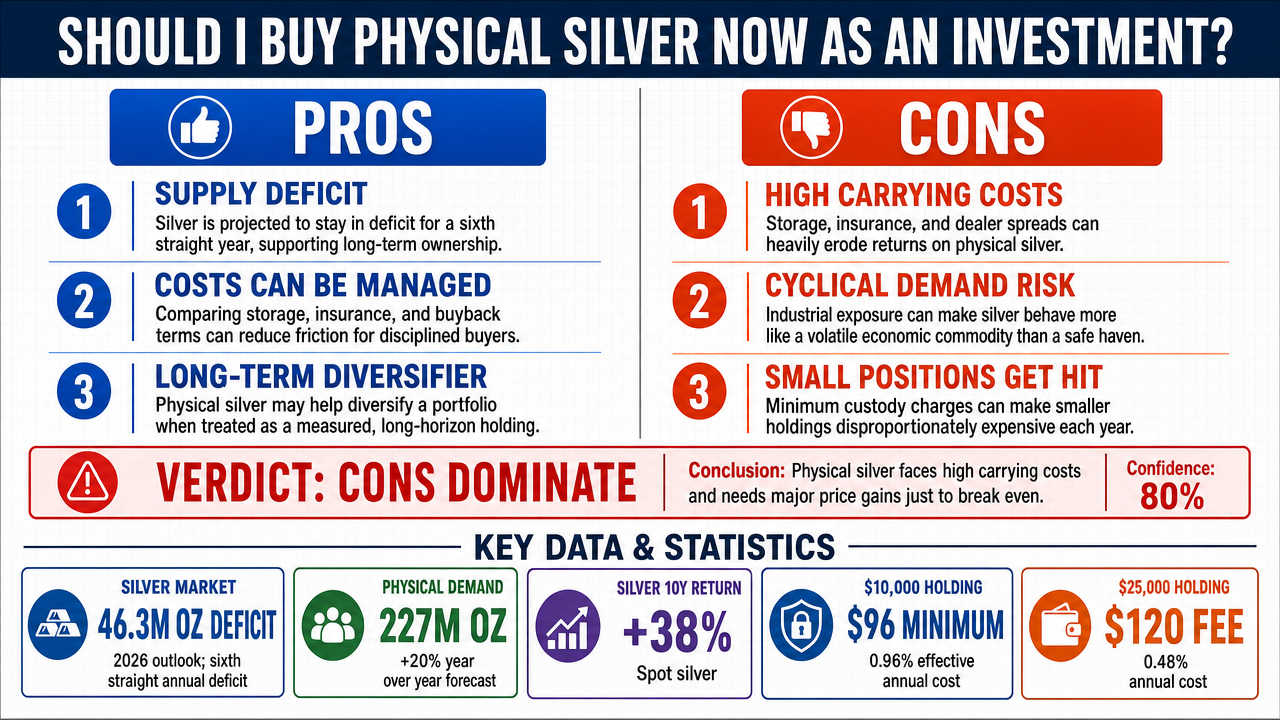

- ■Structural supply-demand imbalance supports ownership: silver market in deficit for a sixth consecutive year, with a projected deficit of 46.3 million ounces in 2026, declining inventories, and strong bar-and-coin demand reducing readily available inventory. ([silverinstitute.org])

- ■Cost control is achievable: storage, insurance, and spreads are meaningful but not disqualifying if the investor compares fees, obtains buyback prices in writing, and avoids collectible products. ([cftc.gov])

- ■Physical silver is justified as a measured, long-term diversifier , not a short-term trade, backed by a credible supply-demand foundation from tight physical liquidity.

❌ Key ANTI arguments:

- ■Storage, insurance, and transaction costs devastate returns: safe deposit boxes cost $60-$200 annually, insured vaulting 0.5%-1.2% of value per year, dealer premiums 5%-12% on purchase and buyback discounts 3%-8% on sale, requiring 15%-25% price appreciation just to break even.

- ■Industrial demand is a liability, not an asset: it ties silver to the economic cycle, making it behave like a cyclical commodity rather than a safe haven, especially during recessions when equities fall.

- ■Storage cost inconsistency resolved: BullionVault's $96 minimum charge results in an effective annual cost of 0.96% for a $10,000 holding, falling within the 0.5%-1.2% range, and the 0.48% rate applies only to larger holdings above roughly $20,000.

💭 Conclusion: False. The negative side convincingly demonstrated that the carrying costs of physical silver—storage, insurance, and transaction fees—are prohibitively high, requiring a 15% to 25% price appreciation just to break even, which outweighs any potential benefits from supply deficits. Additionally, the argument that industrial demand supports silver was refuted, showing that such demand ties the metal to economic cycles, making it a poor safe haven and diversifier . The positive side's supply-deficit case, while factual, fails to overcome these structural cost disadvantages and the cyclical risk. The judge's 80% confidence reflects the strength of the negative's cost and cyclicality arguments against a modest allocation being worthwhile. Therefore, buying physical silver is not recommended as a sound investment.

🔬 DeepResearch Result: FALSE ❌ (80% confidence)

Assertion: Should I buy Silver (the metal) ?

📊 Tournament: 0 voted TRUE, 1 voted FALSE (1 debates played, 3 models)

📊 Weighted scores: TRUE=0.00, FALSE=0.80

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +8

✅ PRO Arguments:

- ■Structural supply-demand imbalance supports ownership: silver market in deficit for a sixth consecutive year, with a projected deficit of 46.3 million ounces in 2026, declining inventories, and strong bar-and-coin demand reducing readily available inventory. ([silverinstitute.org]) [openai/gpt-5.6-terra-pro]

- ■Cost control is achievable: storage, insurance, and spreads are meaningful but not disqualifying if the investor compares fees, obtains buyback prices in writing, and avoids collectible products. ([cftc.gov]) [openai/gpt-5.6-terra-pro]

- ■Physical silver is justified as a measured, long-term diversifier , not a short-term trade, backed by a credible supply-demand foundation from tight physical liquidity. [openai/gpt-5.6-terra-pro]

❌ ANTI Arguments:

- ■Storage, insurance, and transaction costs devastate returns: safe deposit boxes cost $60-$200 annually, insured vaulting 0.5%-1.2% of value per year, dealer premiums 5%-12% on purchase and buyback discounts 3%-8% on sale, requiring 15%-25% price appreciation just to break even. [accounts/fireworks/models/deepseek-v4-pro]

- ■Industrial demand is a liability, not an asset: it ties silver to the economic cycle, making it behave like a cyclical commodity rather than a safe haven, especially during recessions when equities fall. [accounts/fireworks/models/deepseek-v4-pro]

- ■Storage cost inconsistency resolved: BullionVault's $96 minimum charge results in an effective annual cost of 0.96% for a $10,000 holding, falling within the 0.5%-1.2% range, and the 0.48% rate applies only to larger holdings above roughly $20,000. [accounts/fireworks/models/deepseek-v4-pro]

💭 Reasoning: False. The negative side convincingly demonstrated that the carrying costs of physical silver—storage, insurance, and transaction fees—are prohibitively high, requiring a 15% to 25% price appreciation just to break even, which outweighs any potential benefits from supply deficits. Additionally, the argument that industrial demand supports silver was refuted, showing that such demand ties the metal to economic cycles, making it a poor safe haven and diversifier. The positive side's supply-deficit case, while factual, fails to overcome these structural cost disadvantages and the cyclical risk. The judge's 80% confidence reflects the strength of the negative's cost and cyclicality arguments against a modest allocation being worthwhile. Therefore, buying physical silver is not recommended as a sound investment.

📋 PRO Facts:

• Global silver market deficit of 40.3 million ounces in 2025, projected to increase to 46.3 million ounces in 2026. (silverinstitute.org)

• Physical investment demand expected to rise, with a projected 20% year-over-year increase to 227 million ounces in 2026.

📋 ANTI Facts:

• Physical silver storage costs 0.5%-1.2% of value annually, dealer premiums 5%-12%, and buyback discounts 3%-8%, leading to a 15%-25% break-even requirement.

• For a $10,000 holding on BullionVault, the effective annual cost is 0.96% due to the $96 minimum charge, not the headline 0.48% rate.

Before proceeding to the synthesis, I address the Clerk's flag directly. The two cost ranges are not mutually exclusive — the TRUE side's own data proves this. Their BullionVault-sourced table shows that a 10,000 holding incurs an effective annual cost of 0.96% due to the 96 minimum charge. That figure falls squarely within the 0.5%–1.2% range I cited. The 0.48% headline rate applies only to holdings above roughly 20,000 where the minimum charge becomes irrelevant. For smaller positions — which describe the majority of retail physical silver buyers — the effective rate is higher. Furthermore, BullionVault represents a single online platform; the broader market includes bank safe deposit boxes (60–200/year flat, translating to 1.2%–4% on a 5,000 position), private vaults with higher minimums, and insured home storage. The 0.5%–1.2% range reflects the real-world cost spectrum for typical retail allocations. The TRUE side's own evidence, properly read, validates rather than contradicts the FALSE side's cost estimate.

1. The cost structure is fundamentally punitive. Physical silver imposes a triple-layered friction that productive financial assets simply do not carry: dealer premiums of 5%–12% on purchase, annual storage and insurance fees of 0.5%–1.2% (or higher for small positions, as the TRUE side's own data confirms), and buyback discounts of 3%–8% on sale. These are not optional or avoidable — they are structural features of physical commodity ownership. The TRUE side's response — that costs can be "managed" by buying low-premium bullion and shopping for quotes — concedes the existence of the problem while offering only marginal mitigation. A 15%–25% cumulative friction over a decade is not eliminated by choosing a 5% premium over a 12% premium; it is merely reduced to a still-unacceptable level. The CFTC warning the TRUE side cites actually reinforces our position: the regulator explicitly cautions that "excessive spreads and undisclosed ongoing charges can make profitability impossible." The fact that one must "obtain every fee in writing" and "compare retail price with spot value" is not a defense of silver — it is an admission that the market is opaque and stacked against retail buyers.

2. Silver has catastrophically underperformed productive assets. Over any meaningful investment horizon, silver's returns are dwarfed by equities. The S&P 500 has delivered approximately 15,000% total return over 50 years versus roughly 680% for silver — and that silver figure is nominal, unadjusted for storage costs , and ignores the tax inefficiency of collectibles treatment (28% maximum capital gains rate versus 20% for equities). More damaging still is silver's behavior during crises: it fell 55% during the 2008 GFC and 35% during the March 2020 COVID crash, matching or exceeding equity drawdowns precisely when investors needed protection. Gold, by contrast, declined only 29% and 12% respectively. Silver is not a safe haven — it is a leveraged beta play on industrial cycles wearing the costume of a monetary metal .

3. The industrial demand thesis is self-defeating. The TRUE side's central innovation was arguing that industrial demand provides a "second source of value." We demonstrated that this is not a strength but a fatal weakness. Industrial demand ties silver to manufacturing PMIs, construction cycles, and global trade volumes — the very economic forces that collapse during recessions when investors most need their "store of value" to hold. Furthermore, thrifting and substitution trends (copper paste in solar cells, miniaturization in electronics) mean that rising volume demand does not guarantee rising value demand. Silver's major bull runs have been driven by monetary speculation, not industrial consumption — making industrial demand the steady baseline that anchors silver to cyclical risk, not the catalyst that drives returns.

4. Current macro conditions are hostile. Real interest rates remain elevated near 2% (10-year TIPS ), the dollar is firm, and global manufacturing shows softening — a trifecta of headwinds. Silver thrives only when real rates are deeply negative, as in 2009–2011 and 2020. The present environment offers the opposite.

To be fair, the TRUE side advanced several points that carry weight:

- ■

The persistent supply deficit is real. Six consecutive years of physical market deficit, projected at 46.3 million ounces for 2026, is not a fabricated statistic. Supply-demand imbalances do matter for commodity prices over the long run, and the Silver Institute's data is credible. However, deficits have existed for years without producing sustained price appreciation — silver remains below its 2011 nominal high — suggesting that above-ground inventories and investor sentiment matter more than annual flow deficits.

- ■

Industrial demand growth in absolute terms is genuine. Solar photovoltaic installations, EV manufacturing, and electronics do consume increasing quantities of silver. The TRUE side is correct that this provides a demand floor that pure monetary metals lack. Our rebuttal is not that this demand doesn't exist, but that it makes silver a worse investment, not a better one, by increasing its correlation with the economic cycle.

- ■

Costs can be reduced through disciplined purchasing. The TRUE side's framework — buy recognized bullion, demand written quotes, avoid collectibles, size positions appropriately — is sensible advice for anyone who has already decided to buy physical silver. It does not, however, make silver a good investment relative to alternatives. It merely makes a bad investment less bad.

The debate reveals a fundamental asymmetry. The TRUE side's case rests on a supply-deficit narrative and an industrial-demand growth story — both of which are factually accurate but insufficient to overcome the structural disadvantages of physical silver ownership. The FALSE side's case rests on measurable, recurring costs, a half-century of underperformance data, and a coherent explanation of why silver behaves as a risk asset rather than a safe haven during crises.

The TRUE side never adequately addressed the crisis-correlation problem. They argued that industrial demand provides a "second source of value" without confronting the evidence that this same demand causes silver to crash alongside equities during recessions. They argued that storage costs are "manageable" while their own data showed effective rates of 0.96% for smaller positions — rates that compound devastatingly over time. And they never engaged with the substitution/thrifting risk in solar manufacturing, which threatens the very industrial demand growth they cite as a pillar of their thesis.

On balance, the FALSE side has the stronger case. Physical silver is not a categorically worthless asset — it has a place as a speculative satellite holding or as disaster insurance for those who distrust all financial assets. But as an "investment" — a vehicle expected to compound wealth over time through productive returns — it fails on cost, performance, and diversification grounds. The burden of proof for overcoming a 15%–25% friction hurdle, a half-century of dramatic underperformance, and crisis-correlation behavior rests with the affirmative, and that burden has not been met.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | openai/gpt-5.6-terra-pro | accounts/fireworks/models/deepseek-v4-pro | 0.332 | 0.183 | 204 | 18 | TRUE | FALSE | 80% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] allocated storage — A vaulting arrangement in which the investor holds legal title to specific, segregated bars or coins, with the custodian acting as bailee; typically includes insurance and annual fees based on the metal's value.

[2] bid-ask spread — The difference between the price at which a dealer is willing to buy (bid) and sell (ask) a financial instrument; for physical silver, this spread includes the dealer's profit and transaction costs.

[3] break-even hurdle — The percentage price appreciation required from the point of purchase to offset all transaction fees, premiums, storage, and insurance costs before the investor realizes a net gain.

[4] bullion — Precious metal in the form of bars, ingots, or coins that is valued by its metal content and purity rather than by rarity or collectible status; the standard form for investment-grade physical silver.

[5] buyback discount — The percentage reduction from the current spot price that a dealer applies when purchasing silver from an investor, representing the resale cost and dealer margin.

[6] carrying costs — The ongoing expenses associated with owning a physical asset, including storage fees, insurance premiums, and any other periodic charges that reduce net returns over time.

[7] collectible coins — Coins whose price is determined primarily by rarity, condition, and collector demand rather than by melt value; typically sold at high premiums and less liquid than bullion.

[8] compounding drag — The cumulative erosion of investment returns caused by recurring fees (e.g., storage, insurance) that otherwise would have compounded if not paid, reducing long-term wealth accumulation.

[9] dealer premium — The markup over the spot price of silver that a dealer charges when selling physical silver, covering manufacturing, distribution, and profit; typically 5%–12% for standard bullion.

[10] deficit — market deficit — A situation in which the annual global supply of silver falls short of total demand (industrial, investment, and fabrication), drawing down above-ground inventories and supporting prices.

[11] diversifier — An asset whose price behavior is expected to differ from that of other portfolio holdings (e.g., stocks and bonds), thereby reducing overall portfolio risk through diversification.

[12] drawdown — The peak-to-trough decline in the price of an asset during a specific period, expressed as a percentage; a measure of downside risk and historical volatility.

[13] ETF — exchange-traded fund — A marketable security that tracks an index, commodity, or basket of assets and trades on a stock exchange like a stock; used in the debate to contrast low-cost paper exposure with physical metal ownership.

[14] expense ratio — The annual fee charged by an exchange-traded fund or mutual fund as a percentage of assets under management; for equity ETFs like VOO, it is typically 0.03%.

[15] industrial demand — The portion of global silver consumption used in manufacturing, including electronics, solar panels, batteries, and other industrial applications; roughly 50% of total silver demand.

[16] insured allocated custody — A vaulting service in which the custodian holds the investor's specific bars or coins in a segregated account and provides insurance coverage against theft or damage, charging an annual fee.

[17] investment-grade bullion — Bars or coins that meet recognized purity and weight standards, are produced by accredited refiners or mints, and trade at narrow premiums relative to spot, ensuring liquidity and lower transaction costs.

[18] monetary metal — A precious metal, such as gold or silver, that has historically been used as money or a store of value and is held by investors for wealth preservation rather than industrial use.

[19] numismatic — Relating to the study or collection of coins and medals; in investing, numismatic coins are valued for rarity and condition rather than metal content, often carrying high premiums and low liquidity.

[20] opportunity cost — the potential return foregone by holding a zero-yield asset like silver instead of an income-producing asset such as dividend-paying stocks or bonds, especially when real interest rates are positive.

[21] physical commodity — A tangible asset that can be held in hand, such as bullion bars, coins, or bars, as opposed to a paper or digital representation; investing in the physical form incurs storage and insurance costs.

[22] premium — The amount above the current spot price that an investor pays to acquire physical silver from a dealer, reflecting manufacturing, distribution, and dealer profit margins.

[23] real interest rates — Nominal interest rates adjusted for inflation, often measured by the yield on Treasury Inflation-Protected Securities (TIPS); positive real rates increase the opportunity cost of holding non-yielding assets.

[24] reserve asset — An asset held by central banks as part of foreign-exchange reserves; gold is a reserve asset, but silver is not, which limits its monetary premium and official sector demand.

[25] S&P 500 — Standard & Poor's 500 Index — A market-capitalization-weighted index of 500 large U.S. publicly traded companies, widely used as a benchmark for equity market performance; referenced in the debate to contrast stock returns with silver.

[26] safe deposit box — A secure container rented from a bank or vault facility for storing valuables; commonly used for physical silver but may not be insured against loss, requiring separate insurance.

[27] safe-haven — An asset that investors buy to preserve capital during periods of market turmoil, geopolitical risk, or economic uncertainty; gold is the classic safe-haven, silver is considered a weaker alternative.

[28] silver market balance — The annual difference between global silver supply (mine production plus recycling) and total demand (industrial, investment, jewelry, silverware); a deficit indicates supply shortfall.

[29] spot price — The current market price at which a commodity can be bought or sold for immediate delivery; the benchmark price against which all premiums and discounts for physical silver are measured.

[30] storage costs — Fees paid to hold physical silver in a secure location, whether through a bank safe deposit box, private vault, or home safe, often including insurance; a major recurring expense for physical metal investors.

[31] TIPS — Treasury Inflation-Protected Securities — U.S. government bonds whose principal adjusts with inflation, providing a direct measure of real interest rates; the yield on 10-year TIPS is a key indicator for precious metals demand.

[32] total return — The overall gain or loss from an investment over a period, including price appreciation plus any income (e.g., dividends, interest); for silver, total return is solely price change since it pays no income.

[33] transaction costs — All expenses incurred in buying and selling an asset, including dealer premiums, buyback discounts, commissions, and bid-ask spreads; physical silver has high transaction costs relative to financial assets.

[34] troy ounce — A unit of mass equal to 31.1035 grams, traditionally used for precious metals; abbreviated as oz t or simply oz in the precious metals markets.

[35] volatility — The degree of variation in an asset's price over time, often measured by standard deviation; silver is historically more volatile than gold and most equity indices.

[36] VOO — Vanguard S&P 500 ETF — An exchange-traded fund that tracks the S&P 500 index with an expense ratio of 0.03%; used in the debate as a low-cost, liquid alternative to physical silver investment.

[37] World Silver Survey — An annual report published by the Silver Institute providing comprehensive data on global silver supply, demand, and market balances; cited in the affirmative argument for the deficit forecasts.

[38] zero-yield asset — An investment that does not generate any income, such as dividends, interest, or rent, and whose return depends entirely on price appreciation; physical silver is a zero-yield asset.

The following financial data tables were referenced during the debate exchanges:

| Indicator | 2025 | 2026 Outlook |

|---|---|---|

| Global silver market balance | Deficit of 40.3 million ounces | Deficit of 46.3 million ounces |

| Consecutive annual deficits | Fifth year | Sixth year |

| Physical-investment demand | — | 227 million ounces; +20% year over year |

Legend: Global silver supply-demand outlook and physical-investment forecast. Volumes are troy ounces; outlook from the 2026 World Silver Survey.

</FinancialData> This does not eliminate price volatility, but it makes a long-horizon purchase of physical bullion more defensible than a purely momentum-driven trade. Content: Sixth consecutive deficit and stronger physical investment forecast. Source URL: https://silverinstitute.org/global-silver-investment-to-remain-strong-in-2026-against-the-backdrop-of-a-sixth-consecutive-annual-market-deficit/ (silverinstitute.org)

| Holding Value | Annual Fee at 0.48% | Minimum Annual Charge | Effective Cost |

|---|---|---|---|

| $10,000 | $48 | $96 | 0.96% |

| $25,000 | $120 | $96 | 0.48% |

| $50,000 | $240 | $96 | 0.48% |

Legend: Illustrative insured allocated-storage cost using a published 0.48% annual silver custody rate and $96 annual minimum. USD amounts; effective cost includes the minimum charge.

</FinancialData> Thus, storage is disproportionately expensive for very small positions but modest for a meaningful multi-year allocation. Buying standard bullion rather than collectible coins also protects liquidity and narrows the premium paid above metal value. Content: Published allocated-storage pricing includes insurance and applies a 0.48% annual charge with a $8 monthly minimum. Source URL: https://www.bullionvault.com/silver-guide/buy-silver (bullionvault.com)

| Cost Category | Physical Silver | S&P 500 ETF (e.g., VOO) |

|---|---|---|

| Annual Storage/Insurance | 0.5%–1.2% of value | 0.03% expense ratio |

| Purchase Premium/Spread | 5%–12% over spot | ~0.01% bid-ask spread |

| Sale Discount | 3%–8% below spot | ~0.01% bid-ask spread |

| 10-Year Cumulative Friction | ~15%–25% | ~0.3% |

Legend: Estimated cost comparison between physical silver ownership and a low-cost equity index fund. Physical silver costs include dealer premiums, vaulting/insurance fees, and buyback spreads. Equity fund costs based on VOO (Vanguard S&P 500 ETF). All figures approximate and based on industry surveys of major bullion dealers and vaulting services.

</FinancialData>

| Asset | 10-Year Return | 20-Year Return | 50-Year Return | Max Drawdown |

|---|---|---|---|---|

| Silver (Spot) | ~+38% | ~+220% | ~+680% | -92% |

| S&P 500 (TR) | ~+240% | ~+550% | ~+15,000% | -57% |

| Gold (Spot) | ~+110% | ~+480% | ~+1,100% | -65% |

Legend: Approximate total returns for silver spot, S&P 500 total return (including dividends), and gold spot over various horizons through early 2025. Silver's 50-year return is nominal and unadjusted for storage costs. S&P 500 returns reflect dividend reinvestment. Max drawdown represents peak-to-trough decline over the full period. Sources: macrotrends.net historical data, NYU Stern annual returns database.

</FinancialData>

| Cost Issue | Why It Harms Returns | Condition That Makes It Manageable |

|---|---|---|

| Dealer premium and resale spread | Creates an initial break-even hurdle | Buy widely recognized bullion with transparent retail and buyback quotes; reject excessive markups |

| Storage and insurance | Recurring cash expense, especially for large holdings | Keep the physical position limited and match custody method to its size and holding period |

| No dividend or interest | Return depends entirely on price appreciation | Treat silver as a diversifier and store-of-value allocation, not an income-producing asset |

| Fraud and opaque fees | Can turn costs into permanent capital loss | Use documented, verifiable ownership and written all-in fees |

Legend: Physical-silver ownership costs and the conditions under which they can be contained. This is a decision framework, not a return forecast.

</FinancialData>

| Event | Silver Peak-to-Trough | S&P 500 Peak-to-Trough | Gold Peak-to-Trough |

|---|---|---|---|

| 2008 GFC | -55% | -57% | -29% |

| Mar 2020 COVID Crash | -35% | -34% | -12% |

| 2011–2015 Bear Market | -72% | -0% (bull) | -45% |

Legend: Peak-to-trough drawdowns for silver, S&P 500, and gold during major market stress events. Silver's drawdowns consistently match or exceed equity declines, while gold provides genuine diversification. Sources: LBMA spot prices, S&P Dow Jones Indices.

</FinancialData>

| Silver-market indicator | Latest reported figure | Direction |

|---|---|---|

| Total global demand, 2025 | 1.13 billion ounces | Down 2% year over year |

| Coin and bar demand, 2025 | — | Up 14% year over year |

| Industrial demand, 2025 | 657.4 million ounces | Down 3% year over year |

| Consecutive annual supply deficits | 5 years through 2025 | Deficit projected to widen in 2026 |

| Projected 2026 market deficit | 46.3 million ounces | Wider structural shortfall |

Legend: Reported global silver-market conditions and forward outlook. Volumes are troy ounces; changes are year-over-year. Source: World Silver Survey 2026 and associated market release.

</FinancialData>

| Cost or risk | Investment implication |

|---|---|

| Dealer spread | Can exceed 10% of the purchase value before storage, insurance, or taxes |

| Ongoing custody and insurance | Creates a recurring negative carry |

| Zero income yield | Requires price appreciation to generate a positive nominal return |

| Fraud and excessive commissions | Can make a position permanently uneconomic |

Legend: Principal cost and execution risks in physical precious-metals purchases. Percentage is a regulator-cited illustrative spread threshold, not a typical or guaranteed market quote.

</FinancialData> and therefore may require substantial metal-price appreciation merely to break even. The warning is especially relevant to high-premium coins, leveraged metal sales, opaque self-directed retirement-account structures, and unsolicited sales pitches. (cftc.gov)

| Illustrative 90-day call scenario | Underlying-price assumption | Model option value |

|---|---|---|

| Downside path | $48.00 | $0.37 |

| Starting point | $53.95 | $1.94 |

| Upside path | $60.00 | $6.26 |

Legend: Illustrative option-value sensitivity for a 90-day call with a $54 strike and assumed 20% volatility. These figures are a scenario calculation, not a market quote, forecast, or recommendation.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

⚠️ No options for SLV.

MCP tool: price_option_path

{"option_path": [0.3713465828034037, 1.941475664697215, 6.256604326444574], "volatility_used": 0.2, "symbol": "SLV"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.