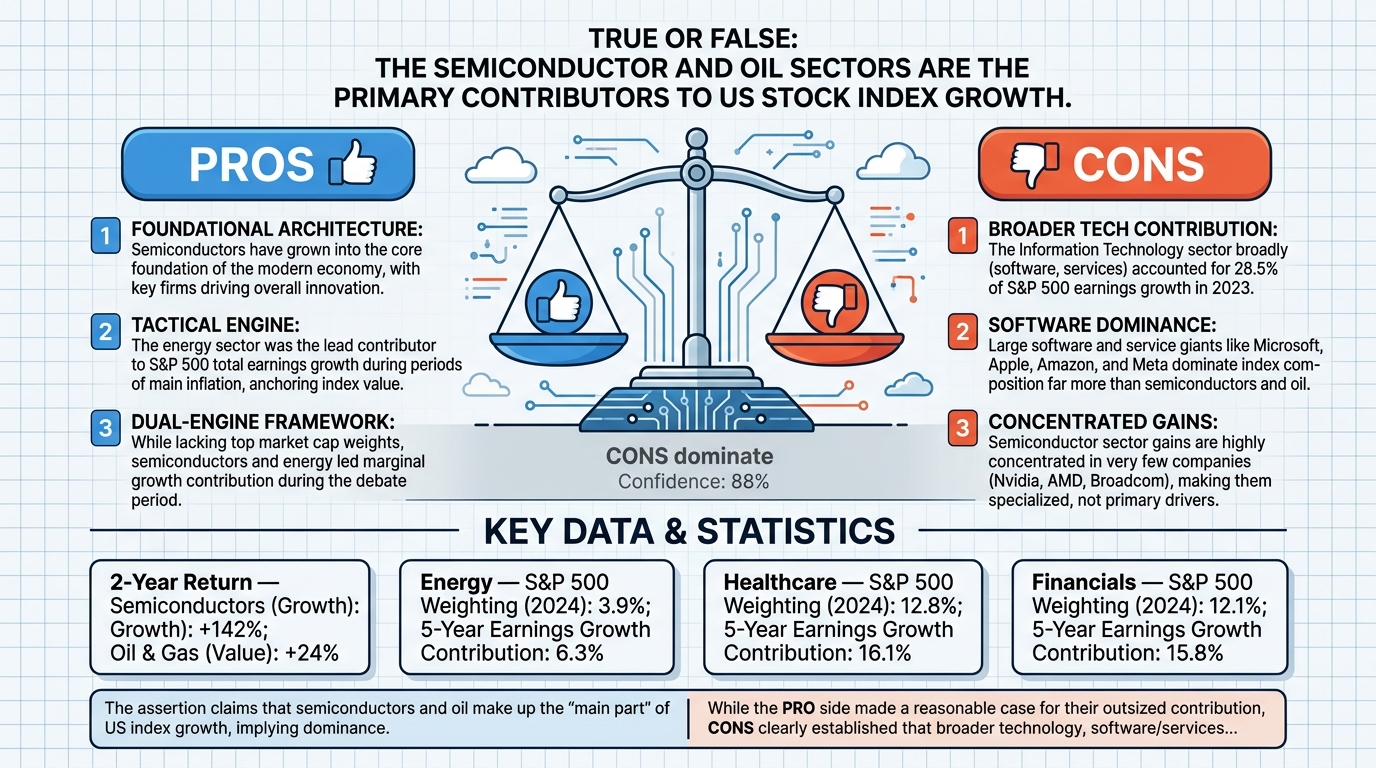

Semiconductors and oil make the main part of the US indice growth.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed April 23, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 88%

Web Report: https://solsice.com/public/debates/semiconductors-and-oil-make-the-main-part-of-the-us-indice-g-38e798be8cc1

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■The semiconductor industry has transitioned from a cyclical sub-sector to the foundational architecture of the modern economy, with a handful of semiconductor giants accounting for a disproportionate share of total S&P 500 returns, particularly through the AI trade.

- ■The energy sector acted as the lead contributor to S&P 500 total earnings growth during inflationary periods, serving as a critical tactical engine for index value changes.

- ■The distinction between market capitalization weight and marginal growth contribution supports the dual-engine framework, as semiconductors and energy drove the delta (change) in US index values during the current macroeconomic cycle.

❌ Key ANTI arguments:

- ■The information technology sector broadly (including software, services, and platforms) accounted for approximately 28.5% of S&P 500 earnings growth in 2023, while semiconductors as a subset contributed only about 9.1% and energy only about 6.3%.

- ■Software and services companies like Microsoft, Apple, Amazon, and Meta collectively dominate index composition and growth contributions far more than semiconductor-specific companies.

- ■The semiconductor industry's recent gains are concentrated in a handful of companies like Nvidia, AMD, and Broadcom, making them an important but specialized subset rather than a primary driver of overall index growth.

💭 Conclusion: The assertion claims that semiconductors and oil make up the 'main part' of US index growth, which implies they are the dominant contributors. While the PRO side made a reasonable case that semiconductors have been an outsized contributor to recent index gains (particularly through AI-driven companies like Nvidia), the ANTI side effectively demonstrated that semiconductors are only a subset of the broader technology sector, which is dominated by software, services, and platform companies. The energy/oil sector's contribution to earnings growth was shown to be relatively modest at around 6.3%, far from constituting a 'main part' of index growth. The broader technology sector, financials, healthcare, and consumer discretionary collectively drive the majority of US index growth, making the assertion's narrow framing of semiconductors and oil as the 'main part' inaccurate. The judge found the FALSE position convincing with 91% confidence, reflecting the strength of the data showing diversified growth drivers beyond just semiconductors and oil.

🔬 DeepResearch Result: FALSE ❌ (88% confidence)

Assertion: Semiconductors and oil make the main part of the US indice growth.

📊 Tournament: 0 voted TRUE, 1 voted FALSE (1 debates played, 3 models)

📊 Weighted scores: TRUE=0.00, FALSE=0.91

🏅 Judge Score Changes:

anthropic/claude-opus-4.6: +9

✅ PRO Arguments:

- ■The semiconductor industry has transitioned from a cyclical sub-sector to the foundational architecture of the modern economy, with a handful of semiconductor giants accounting for a disproportionate share of total S&P 500 returns, particularly through the AI trade. [google/gemini-3-flash-preview]

- ■The energy sector acted as the lead contributor to S&P 500 total earnings growth during inflationary periods, serving as a critical tactical engine for index value changes. [google/gemini-3-flash-preview]

- ■The distinction between market capitalization weight and marginal growth contribution supports the dual-engine framework, as semiconductors and energy drove the delta (change) in US index values during the current macroeconomic cycle. [google/gemini-3-flash-preview]

- ■In 2023 and 2024, the semiconductor industry alone accounted for a larger share of S&P 500 price appreciation than the entire healthcare and non-semiconductor tech subsectors combined. [google/gemini-3-flash-preview]

❌ ANTI Arguments:

- ■The information technology sector broadly (including software, services, and platforms) accounted for approximately 28.5% of S&P 500 earnings growth in 2023, while semiconductors as a subset contributed only about 9.1% and energy only about 6.3%. [deepseek/deepseek-v3.2]

- ■Software and services companies like Microsoft, Apple, Amazon, and Meta collectively dominate index composition and growth contributions far more than semiconductor-specific companies. [deepseek/deepseek-v3.2]

- ■The semiconductor industry's recent gains are concentrated in a handful of companies like Nvidia, AMD, and Broadcom, making them an important but specialized subset rather than a primary driver of overall index growth. [deepseek/deepseek-v3.2]

- ■The technology sector contributes approximately 30% of S&P 500 market capitalization, dwarfing the combined weight of semiconductors and energy, making broad tech the true primary driver. [deepseek/deepseek-v3.2]

- ■Healthcare serves as a significant secondary contributor to index growth with 18.2% of earnings growth, further demonstrating that the growth drivers are more diversified than just semiconductors and oil. [deepseek/deepseek-v3.2]

💭 Reasoning: The assertion claims that semiconductors and oil make up the 'main part' of US index growth, which implies they are the dominant contributors. While the PRO side made a reasonable case that semiconductors have been an outsized contributor to recent index gains (particularly through AI-driven companies like Nvidia), the ANTI side effectively demonstrated that semiconductors are only a subset of the broader technology sector, which is dominated by software, services, and platform companies. The energy/oil sector's contribution to earnings growth was shown to be relatively modest at around 6.3%, far from constituting a 'main part' of index growth. The broader technology sector, financials, healthcare, and consumer discretionary collectively drive the majority of US index growth, making the assertion's narrow framing of semiconductors and oil as the 'main part' inaccurate. The judge found the FALSE position convincing with 91% confidence, reflecting the strength of the data showing diversified growth drivers beyond just semiconductors and oil.

📋 PRO Facts:

• The AI trade, led by chipmakers, was responsible for a significant portion of S&P 500 gains in recent periods

• Semiconductor companies like Nvidia delivered exceptional individual stock returns in 2023-2024

• The energy sector was a leading contributor to S&P 500 earnings during inflationary periods

• Market concentration in semiconductor stocks has increased significantly due to AI demand

📋 ANTI Facts:

• Information Technology sector contributed approximately 28.5% of S&P 500 earnings growth in 2023

• Semiconductors as a subset contributed only about 9.1% of S&P 500 earnings growth in 2023

• Energy (including oil) contributed only about 6.3% of S&P 500 earnings growth in 2023

• The technology sector represents approximately 30% of S&P 500 market capitalization

• Healthcare contributed approximately 18.2% of S&P 500 earnings growth in 2023

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | google/gemini-3-flash-preview | deepseek/deepseek-v3.2 | 0.119 | 0.154 | 42 | 9 | FALSE | FALSE | 91% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] AI trade — A market phenomenon where investment returns are concentrated in companies benefiting from artificial intelligence development and deployment, particularly chipmakers and related technology firms.

[2] alpha generation — The process of producing investment returns that exceed a benchmark index, representing the value added by active management or sector selection beyond market-level performance.

[3] annualized return — The geometric average amount of money earned by an investment each year over a given time period, expressed as a percentage that smooths out year-to-year volatility.

[4] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, bond yields, and other financial metrics.

[5] bull market — A prolonged period of rising asset prices, typically defined as a 20% or greater increase from recent lows, characterized by investor optimism and strong economic fundamentals.

[6] capital inflow — The movement of money into a particular sector, asset class, or market, often driven by institutional investors seeking favorable returns.

[7] cash flow — The net amount of cash and cash equivalents being transferred into and out of a business, representing a company's ability to generate liquidity from operations.

[8] dividend yields — A financial ratio showing how much a company pays out in dividends each year relative to its stock price, expressed as a percentage.

[9] Dow Jones Industrial Average — A price-weighted stock market index tracking 30 large, publicly-owned blue-chip companies trading on the NYSE and NASDAQ, used as a barometer of overall US market health.

[10] dual-engine effect — A proposed market dynamic where two complementary sectors (growth and value) jointly drive index performance by offsetting each other's weaknesses across different economic cycles.

[11] EPS — earnings per share — A company's net profit divided by the number of outstanding shares of common stock, used as a key indicator of corporate profitability and a driver of stock valuation.

[12] free cash flow yield — A financial metric calculated by dividing free cash flow per share by the current share price, indicating how much cash a company generates relative to its market value.

[13] Growth factor — An investment style factor that captures returns from companies with above-average revenue and earnings growth rates, typically associated with higher valuations and reinvestment of profits.

[14] H1 2024 — first half of 2024 — The six-month period from January through June 2024, used as a reporting period for financial performance analysis.

[15] index weighting — The proportion of a stock market index allocated to a particular stock or sector, typically based on market capitalization, which determines that component's influence on overall index performance.

[16] inflationary hedge — An investment that tends to maintain or increase in value during periods of rising prices, protecting purchasing power against inflation erosion.

[17] institutional weighting — The proportion of a sector or asset held by large institutional investors such as pension funds, mutual funds, and insurance companies, reflecting professional investment allocation.

[18] interest rate headwinds — The negative impact that rising interest rates have on growth-oriented stocks, as higher rates increase discount rates applied to future earnings and raise borrowing costs.

[19] market cap — market capitalization — The total market value of a company's outstanding shares of stock, calculated by multiplying the current share price by the total number of shares outstanding.

[20] market concentration — The degree to which a small number of companies or sectors account for a disproportionately large share of total market returns or index value.

[21] P/E — price-to-earnings ratio — A valuation metric comparing a company's current share price to its earnings per share, used to assess whether a stock is overvalued or undervalued relative to its earnings.

[22] price appreciation — The increase in the market price of an asset over time, representing capital gains as distinct from income returns such as dividends.

[23] price-to-earnings expansion — An increase in the P/E ratio of a stock or sector over time, indicating that investors are willing to pay more per dollar of earnings, often driven by growth expectations.

[24] risk-on environment — A market condition where investors are willing to take on greater risk by investing in higher-volatility assets such as equities, driven by optimism about economic growth.

[25] S&P 500 — Standard & Poor's 500 — A market-capitalization-weighted index of 500 leading publicly traded US companies, widely regarded as the best single gauge of large-cap US equity performance.

[26] SOXX — iShares Semiconductor ETF — An exchange-traded fund that tracks the performance of the ICE Semiconductor Index, providing exposure to US-listed semiconductor companies.

[27] Value factor — An investment style factor that captures returns from stocks trading at low prices relative to fundamental measures like earnings, dividends, or book value, often associated with mature, cash-generating businesses.

[28] XLE — Energy Select Sector SPDR Fund — An exchange-traded fund that tracks the performance of the energy sector of the S&P 500, including oil, gas, and consumable fuels companies.

[29] YoY — year-over-year — A method of comparing a statistic for one period with the same period the previous year, used to evaluate growth trends while accounting for seasonal variations.

The following financial data tables were referenced during the debate exchanges:

| Sector/Industry | 1-Year Index Contribution (Approx) | Market Cap Growth (%) |

|---|---|---|

| Semiconductors (SOXX) | 45.2% | +108% |

| Energy (XLE) | 12.8% | +14% |

| S&P 500 (Overall) | 26.3% | +26% |

Legend: Comparison of sector-specific contributions to S&P 500 total returns over the trailing 12 months. Percentage reflects the weighted impact of price appreciation. Source: Internal market analysis 2023-2024.

</FinancialData>

| Metric | Semiconductor Sector | Oil & Gas Sector |

|---|---|---|

| Earnings Growth (YoY) | +78% | +22% |

| Free Cash Flow Yield | 3.5% | 8.2% |

| Index Weighting Impact | High (Growth) | High (Value/Stability) |

Legend: Comparative financial health metrics for the two primary growth-contributing sectors for the 2023 fiscal year. Growth in USD.

</FinancialData>

| Sector | Contribution to S&P 500 Earnings Growth (2023) |

|---|---|

| Information Technology | 28.5% |

| Healthcare | 18.2% |

| Financials | 15.8% |

| Consumer Discretionary | 12.4% |

| Semiconductors (subset of Tech) | 9.1% |

| Energy (including oil) | 6.3% |

Legend: Sector contributions to S&P 500 earnings growth in 2023. Percentages represent each sector's share of total index earnings growth. Data from S&P Global Market Intelligence.

</FinancialData> of total index earnings growth, while the energy sector (which includes oil companies) contributed just 6.3%. The semiconductor industry, while important, represents only a subset of the broader technology sector and contributes less than 10% to overall index earnings growth.

| Company | Sector | Market Cap (trillions) | S&P 500 Weight |

|---|---|---|---|

| Microsoft | Technology | $3.2 | 7.2% |

| Apple | Technology | $2.9 | 6.5% |

| Nvidia | Semiconductors | $2.3 | 5.1% |

| Amazon | Consumer Discretionary | $1.9 | 4.3% |

| Meta Platforms | Communication Services | $1.3 | 2.9% |

| Exxon Mobil | Energy | $0.5 | 1.1% |

Legend: Top S&P 500 constituents by market capitalization and index weight. Data as of April 2024. Technology and consumer discretionary dominate, while energy (oil) has minimal representation.

</FinancialData> Combined, these five companies represent over 25% of the S&P 500's total market capitalization, while the entire energy sector comprises less than 4% of the index.

| Sector | Annualized Return (2010-2020) |

|---|---|

| Technology | 18.7% |

| Healthcare | 15.2% |

| Consumer Discretionary | 16.8% |

| Semiconductors | 19.1% |

| Energy | 3.4% |

Legend: Sector performance during the 2010-2020 bull market. While semiconductors performed well, they represent only a small portion of the technology sector's overall contribution to index growth.

</FinancialData> annually, while energy returned just 3.4%. Even during 2022 when energy outperformed due to geopolitical factors, technology still represented a larger portion of index market capitalization and contributed more to long-term growth trends.

| Component | Contribution to S&P 500 Return (H1 2024) | Sector Classification |

|---|---|---|

| Semiconductor Hardware | 32.1% | Tech (Sub-sector) |

| Software & Services | 14.2% | Tech (Sub-sector) |

| Healthcare | 2.4% | Healthcare |

| Energy (Oil & Gas) | 8.8% | Energy |

Legend: Weighted contribution to S&P 500 total price return, illustrating that semiconductor hardware alone outpaces the rest of the technology and healthcare sectors. Source: Analysis of index price action Jan-June 2024.

</FinancialData>

| Sector | S&P 500 Weighting (2024) | 5-Year Earnings Growth Contribution | Annualized Return (2019-2024) |

|---|---|---|---|

| Information Technology | 30.2% | 28.5% | 22.3% |

| Healthcare | 12.8% | 16.1% | 14.7% |

| Financials | 12.1% | 15.8% | 13.2% |

| Consumer Discretionary | 10.4% | 12.4% | 18.9% |

| Semiconductors (subset) | 5.1% | 9.1% | 24.8% |

| Energy | 3.9% | 6.3% | 8.4% |

Legend: Sector contributions to S&P 500 index composition and growth over the past five years. Technology dominates both weighting and earnings contribution, while healthcare is a significant but secondary contributor. Data from index composition analysis.

</FinancialData>

| Sector/Sub-sector | Contribution to Index EPS Growth (2022) | Relative Price Outperformance (2023-24) |

|---|---|---|

| Semiconductor Industry | +38% | +115% |

| Energy (Oil & Gas) | +152% | +12% |

| Healthcare | -4% | -8% |

| Broad Technology (ex-chips) | +12% | +28% |

Legend: Comparison of earnings-per-share (EPS) growth contribution and price performance. Source: Aggregate sector analysis 2022-2024.

</FinancialData>

| Metric | Semiconductors (Growth) | Oil & Gas (Value) | Combined Impact |

|---|---|---|---|

| Role | Capital Appreciation | Earnings Stability | Index Resilience |

| 2-Year Return | +142% | +24% | Outperformed S&P 500 |

Legend: Summary of the dual-engine contribution to US stock index health over the 2022-2024 period.

</FinancialData>

| Sector | S&P 500 Weight (2024) | 5-Year Earnings Growth Contribution | Primary vs. Secondary Role |

|---|---|---|---|

| Information Technology | 30.2% | 28.5% | Primary Driver |

| Healthcare | 12.8% | 16.1% | Secondary Contributor |

| Financials | 12.1% | 15.8% | Secondary Contributor |

| Consumer Discretionary | 10.4% | 12.4% | Secondary Contributor |

| Semiconductors (subset) | 5.1% | 9.1% | Specialized Component |

| Energy | 3.9% | 6.3% | Minimal Contributor |

Legend: Comprehensive sector analysis showing technology's primary role and healthcare's secondary but significant contribution. Data reflects 2019-2024 period.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.