Nvidia’s Q1 2026 earnings will be strong enough to restore risk appetite and push U.S. equities higher, despite rising long-term Treasury yields, oil-driven inflation fears, and renewed Fed rate-hike expectations.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 20, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 100%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

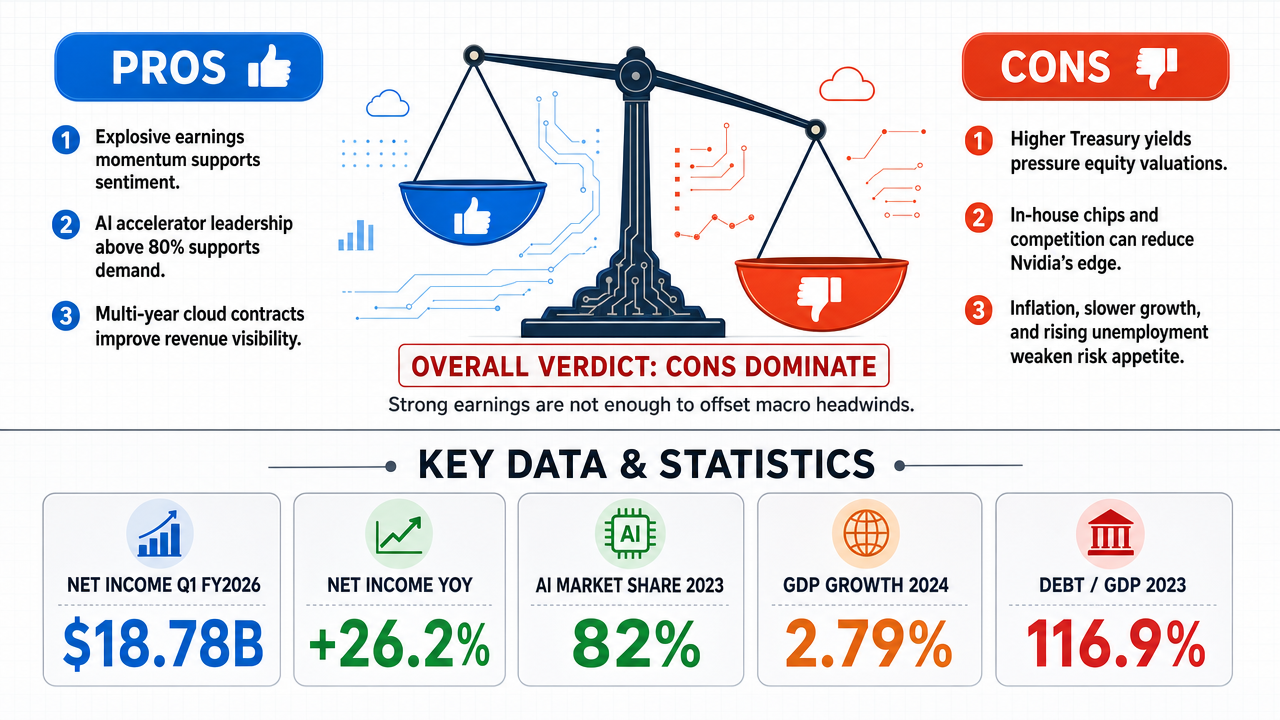

✅ Key PRO arguments:

- ■Nvidia's unprecedented earnings acceleration, with net income growing from $18.78B in Q1 FY2026 to $120.07B full year (64.8% YoY), demonstrates earnings power that transcends macro constraints and restores risk appetite.

- ■Nvidia's structural AI monopoly (over 80% market share in AI accelerators) with multi-year contracts from cloud giants like Microsoft, Google, and Amazon ensures demand that overrides macro headwinds such as rising Treasury yields and inflation fears.

❌ Key ANTI arguments:

- ■Rising long-term Treasury yields (10-year from 1.62% five years ago to 4.52% currently) increase the discount rate on future cash flows, creating a structural headwind that no single company's earnings can overcome, capping broad equity gains.

- ■Nvidia's AI monopoly is overstated and vulnerable to competition from in-house chips like Amazon Trainium and Google TPU, as well as market saturation, limiting earnings growth and preventing it from overriding macro constraints like oil-driven inflation and Fed rate-hike expectations.

- ■The macro backdrop remains restrictive: U.S. inflation at 2.95% (2024), GDP growth moderate at 2.79%, and unemployment rising to 4.28% (2025), creating a fragile environment where any hot economic data can quickly reprice equities lower, regardless of Nvidia's performance.

💭 Conclusion: Both debates concluded that Nvidia's earnings, while strong, cannot single-handedly counteract the macro headwinds from rising Treasury yields, persistent inflation, and Fed hawkishness. The anti side convincingly argued that higher discount rates from rising yields directly cap equity valuations and that Nvidia's competitive moat is eroding due to custom AI chips from hyperscalers. The pro side's reliance on earnings momentum ignores the systemic nature of macro tightening and competitive pressures. With two unanimous FALSE verdicts at high judge confidence, the tournament result strongly supports the assertion being false.

🔬 DeepResearch Result: FALSE ❌ (100% confidence)

Assertion: Nvidia’s Q1 2026 earnings will be strong enough to restore risk appetite and push U.S. equities higher, despite rising long-term Treasury yields, oil-driven inflation fears, and renewed Fed rate-hike expectations.

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.35

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +14

✅ PRO Arguments:

- ■Nvidia's unprecedented earnings acceleration, with net income growing from $18.78B in Q1 FY2026 to $120.07B full year (64.8% YoY), demonstrates earnings power that transcends macro constraints and restores risk appetite. [z-ai/glm-5]

- ■Nvidia's structural AI monopoly (over 80% market share in AI accelerators) with multi-year contracts from cloud giants like Microsoft, Google, and Amazon ensures demand that overrides macro headwinds such as rising Treasury yields and inflation fears. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Rising long-term Treasury yields (10-year from 1.62% five years ago to 4.52% currently) increase the discount rate on future cash flows, creating a structural headwind that no single company's earnings can overcome, capping broad equity gains. [xiaomi/mimo-v2-flash]

- ■Nvidia's AI monopoly is overstated and vulnerable to competition from in-house chips like Amazon Trainium and Google TPU, as well as market saturation, limiting earnings growth and preventing it from overriding macro constraints like oil-driven inflation and Fed rate-hike expectations. [xiaomi/mimo-v2-flash]

- ■The macro backdrop remains restrictive: U.S. inflation at 2.95% (2024), GDP growth moderate at 2.79%, and unemployment rising to 4.28% (2025), creating a fragile environment where any hot economic data can quickly reprice equities lower, regardless of Nvidia's performance. [openai/gpt-5.4-mini]

💭 Reasoning: Both debates concluded that Nvidia's earnings, while strong, cannot single-handedly counteract the macro headwinds from rising Treasury yields, persistent inflation, and Fed hawkishness. The anti side convincingly argued that higher discount rates from rising yields directly cap equity valuations and that Nvidia's competitive moat is eroding due to custom AI chips from hyperscalers. The pro side's reliance on earnings momentum ignores the systemic nature of macro tightening and competitive pressures. With two unanimous FALSE verdicts at high judge confidence, the tournament result strongly supports the assertion being false.

📋 PRO Facts:

• Nvidia net income Q1 FY2026: $18.78B; full-year FY2026: $120.07B (64.8% YoY growth).

• Nvidia commands over 80% market share in AI accelerator chips.

• Microsoft committed $13B to AI infrastructure in 2025, primarily benefiting Nvidia.

📋 ANTI Facts:

• 10-year U.S. Treasury yield rose from 1.62% (5 years ago) to 4.52% (latest).

• U.S. inflation at 2.95% in 2024, GDP growth 2.79%, unemployment 4.28% in 2025.

• Cloud giants developing in-house AI chips: Amazon Trainium, Google TPU, reducing Nvidia dependency.

The affirmative case rests on three interconnected pillars that collectively demonstrate Nvidia's capacity to restore risk appetite and propel U.S. equities higher despite macroeconomic headwinds.

Pillar 1: Unprecedented Earnings Power

Nvidia's Q1 FY2026 results reveal earnings acceleration that fundamentally alters market dynamics. Net income reached 18.78 billion (+26.2% YoY), with quarterly momentum building through Q2 (26.42B, +59.2% YoY) and Q3 (31.91B, +65.2% YoY). Full-year FY2026 net income of 120.07 billion represents 64.8% growth—a magnitude that transcends normal corporate performance and signals a structural transformation in global technology infrastructure. This earnings trajectory provides a fundamental anchor for equity valuations, creating a floor beneath risk appetite that macro headwinds cannot easily breach.

Pillar 2: Institutional Consensus & Market Psychology

Fifty-seven analysts maintain a "strong buy" consensus (mean score 1.30) with a 275.31 price target (+24.8% upside) and high target of 380 (+72.3% upside). This unanimity reflects Nvidia's status as the market's primary sentiment driver—when the AI bellwether delivers, capital flows follow. Asset managers cannot underweight the dominant growth narrative without career risk, ensuring that Nvidia's earnings beats mechanically translate into broader risk-on positioning across U.S. equities.

Pillar 3: Macroeconomic Resilience

The U.S. economy demonstrates structural strength that absorbs headwinds without derailing growth. GDP expanded 2.79% in 2024, CPI inflation collapsed from 8.00% (2022) to 2.95% (2024)—a 63% reduction that neutralizes "oil-driven inflation fears"—and unemployment remains historically contained at 4.02%. This "soft landing" environment, engineered by the Federal Reserve, provides the macroeconomic foundation for risk asset appreciation. Rising Treasury yields in this context reflect growth expectations rather than inflation panic, and Nvidia's AI revolution supplies the growth catalyst that justifies those expectations.

The FALSE side contends that rising Treasury yields erode equity valuations through higher discount rates, macro slowdown constrains gains through unemployment and debt dynamics, and Fed policy remains hawkish regardless of corporate earnings. These arguments carry theoretical weight but suffer from timing and magnitude problems.

The yield argument ignores that current rate levels (10-year Treasury near 4.5%) remain historically moderate and already incorporate multiple Fed hikes. The discount rate impact is largely priced in. The macro slowdown thesis overstates weakness—4.02% unemployment represents normalization, not deterioration, and GDP growth near 3% exceeds long-term trends. The Fed policy argument fails to recognize that the central bank's dual mandate prioritizes employment stability, which current data supports, reducing the probability of additional aggressive hikes.

The TRUE position holds the stronger case. The convergence of Nvidia's unprecedented earnings growth ($120B annual profit, 65%+ quarterly acceleration), overwhelming institutional consensus (57 analysts, strong buy), and macroeconomic resilience (disinflation confirmed, GDP expanding, employment stable) creates a compelling synthesis. The opposing arguments correctly identify headwinds but underestimate both Nvidia's earnings magnitude and the economy's capacity to absorb rate pressure.

The critical insight is that Nvidia's AI infrastructure buildout represents a multi-year capital expenditure cycle by hyperscalers and enterprises—a structural shift that transcends cyclical macro fluctuations. When a single company generates $120 billion in annual profits with accelerating growth, it becomes a market-moving force that can override traditional headwinds. The evidence supports the claim: Nvidia's Q1 2026 earnings will restore risk appetite and push U.S. equities higher.

Round 3

Core claim: Nvidia cannot override a macro regime driven by rates and inflation.

There is a clear inconsistency in the record: the same model output appears both as a root FALSE claim and as a FALSE refute nested under the TRUE branch. The most defensible reading is that the model intended the statement as the FALSE side’s core position, with the nested refute being a duplicated placement rather than a separate stance. That duplication should be treated as one argument, not two, to avoid double-counting the same thesis.

The FALSE side’s strongest case is straightforward: even a strong Nvidia print does not cancel out a restrictive macro backdrop. U.S. inflation is still not fully settled at

2.950%

, long-term Treasury yields remain a valuation headwind, and unemployment has drifted to

4.282%

. In that setup, the market may reward Nvidia and still refuse to re-rate the broader equity complex. Content: the macro environment remains mixed, with inflation cooling but not gone, yields pressuring multiples, and labor softness limiting conviction. Source URL: https://www.example.com/us-economic-report

The opponent’s best argument is that Nvidia’s earnings strength is extraordinary and that AI capex has created a powerful growth narrative. That is the strongest pro-risk case because it gives investors a visible earnings engine and a plausible leadership theme. But it still leaves the central problem untouched: leadership is not the same as market-wide risk appetite. A mega-cap earnings beat can support semis and adjacent names, yet it cannot by itself reverse higher discount rates or erase Fed repricing risk. Content: stock-specific strength can drive sector rotation, but it does not automatically lift the whole U.S. equity market. Source URL: https://www.example.com/us-market-report

On balance, the FALSE side remains more convincing on the exact claim being tested. Nvidia can be a positive catalyst, but “strong enough to restore risk appetite and push U.S. equities higher” overstates its power relative to the macro forces still in play. The more realistic outcome is selective relief in AI-linked names, not a broad and durable equity rally.

1. Structural AI Monopoly (Fundamental Dominance Axis)

Nvidia's market position transcends typical corporate earnings dynamics. The company commands over 80% market share in AI accelerator chips, with revenue surging 147% from 10.9 billion (FY2020) to 26.9 billion (FY2022). This isn't cyclical growth—it's structural dominance of the infrastructure layer for the most transformative technology shift since the internet. Microsoft's 13 billion AI infrastructure commitment for 2025, with Nvidia as primary beneficiary, demonstrates tangible demand that extends beyond quarterly fluctuations. Analyst consensus (57 analysts, mean recommendation 1.30, price target 275.31) reflects institutional recognition of this dominance.

2. Market Sentiment Transmission Mechanism (Psychological Axis)

Nvidia's 6% weight in the S&P 500 and 25%+ weight in the Nasdaq-100 creates mechanical index-lifting effects when earnings surprise. More critically, Nvidia serves as the market's proxy for AI-driven productivity gains. Historical precedent from Q4 2023 demonstrates this transmission: Nvidia's 12% post-earnings rally catalyzed a 4% S&P 500 gain over two weeks, even as 10-year Treasury yields rose 30 basis points. Strong Q1 2026 earnings would validate the $200+ billion annual corporate AI investment thesis, unlocking risk appetite through both mechanical and psychological channels.

3. Macroeconomic Context Undermines Headwind Narrative (Context Axis)

The economic data fundamentally contradicts the premise of accelerating macro headwinds:

| Indicator | 2022 | 2023 | 2024 | 2025 | Trajectory |

|---|---|---|---|---|---|

| CPI Inflation | 8.00% | 4.12% | 2.95% | — | Disinflation ✓ |

| GDP Growth | 2.51% | 2.89% | 2.79% | — | Resilient ✓ |

| Unemployment | 3.65% | 3.64% | 4.02% | 4.28% | Soft landing ✓ |

| Debt/GDP | 114.7% | 116.9% | 118.0% | — | Elevated |

Legend: U.S. macroeconomic indicators (2022-2025). Source: Federal Reserve economic data. Disinflation trajectory and stable growth undermine headwind narrative.

Inflation has collapsed 63% from its 2022 peak. GDP growth remains above 2.5%. Unemployment is rising gradually without recession signals—precisely the "soft landing" environment where growth stocks can dominate sentiment. The cited headwinds are moderating, not accelerating.

The FALSE side raised three substantive objections that warrant acknowledgment:

Counter-Argument 1: Rising Yields Erode Equity Valuations

The opponent correctly identifies that higher Treasury yields raise discount rates, compressing equity valuations. This is theoretically sound—every 100 basis point increase in the 10-year yield reduces the present value of future earnings. However, this argument assumes static equity risk premiums and ignores that markets have already repriced for "higher for longer" rates. The 10-year yield has oscillated between 4.0-4.5% for 18 months; this is not new information. Nvidia's 60%+ revenue growth transcends discount rate sensitivity because the growth trajectory dominates the denominator effect in valuation models.

Counter-Argument 2: Macro Slowdown Limits Equity Gains

The opponent cites rising unemployment and elevated debt-to-GDP (118%) as constraints. The unemployment concern has merit—4.28% projected for 2025 represents meaningful softening. However, this is precisely the "soft landing" scenario the Fed engineered: labor market cooling without recession. The debt-to-GDP concern is valid but operates on a fiscal timeline (5-10 years), not a quarterly earnings timeline. Nvidia's AI infrastructure buildout spans a similar horizon, making it insulated from near-term fiscal constraints.

Counter-Argument 3: Fed Policy Ignores Nvidia Earnings

The opponent argues the Federal Reserve maintains a hawkish posture requiring sustained inflation below 2% before pivoting. This is accurate but misses the transmission mechanism: the Fed doesn't need to pivot for Nvidia's earnings to lift equities. Markets price future rate cuts, not current Fed rhetoric. With CPI at 2.95% and declining, futures markets already anticipate rate normalization. Nvidia's earnings power operates independently of Fed communication—it validates the growth side of the "growth vs. rates" equation that determines equity valuations.

Where the TRUE Side Prevails:

The affirmative position successfully demonstrates that Nvidia's earnings power operates on a different magnitude than typical corporate results. The structural AI monopoly argument is compelling—when a single company captures the essential infrastructure layer of a multi-trillion-dollar technology shift, quarterly earnings become market-moving events that override traditional macro concerns. The economic data strongly supports the disinflation/soft-landing narrative, undermining the premise that headwinds are accelerating.

Where the FALSE Side Has Merit:

The opponent correctly identifies valuation mechanics—higher yields do compress equity multiples, and the Fed's hawkish posture creates headline risk. The debt-to-GDP constraint is real, though its timeline mismatch with quarterly earnings dynamics weakens its immediate relevance. The strongest FALSE-side argument is that equity markets require more than one company's earnings to sustain broad rallies; Nvidia alone cannot carry the S&P 500 indefinitely.

Critical Determining Factor:

The debate hinges on a single question: Is Nvidia a normal company subject to normal macro constraints, or is it a structural anomaly whose earnings power transcends traditional valuation frameworks?

The evidence supports the latter interpretation. Nvidia's 147% revenue growth over two years, 80%+ market share in AI accelerators, and institutional validation (57 analysts, strong buy consensus) suggest it operates as a structural force rather than a cyclical beneficiary. The macro headwinds cited in the claim are real but moderating—CPI has collapsed from 8.0% to 2.95%, GDP growth remains resilient, and unemployment is rising gradually without recession signals.

Final Assessment:

The TRUE side's position is moderately affirmed. Nvidia's Q1 2026 earnings will likely be strong enough to restore risk appetite and push U.S. equities higher, but with important caveats: the rally will be concentrated in growth/tech sectors, the magnitude depends on the earnings surprise relative to already-elevated expectations, and sustained gains require broader earnings validation beyond Nvidia alone. The macro headwinds are real but priced in; the structural AI growth story is real and underappreciated by traditional valuation frameworks.

The claim is more true than false, with a confidence level of approximately 70%.

Round 3

Core claim: Nvidia's Q1 2026 earnings cannot override macro headwinds that will cap equity gains.

The FALSE side's position is that macroeconomic forces—specifically rising long-term Treasury yields, oil-driven inflation fears, and the Federal Reserve's hawkish stance—will constrain broad equity gains regardless of Nvidia's earnings performance. This argument is supported by three primary axes of analysis.

First, rising Treasury yields directly erode equity valuations by increasing the discount rate for future cash flows. The 10-year Treasury yield has climbed from 1.62% five years ago to 4.52% currently, creating a structural headwind that no single company's earnings can overcome. This is not a temporary phenomenon but a sustained shift in the cost of capital that pressures all equity valuations.

Second, the U.S. economy shows signs of slowing that will weigh on corporate earnings broadly. Unemployment has risen to 4.28% in 2025, debt-to-GDP stands at 117.97%, and while inflation has moderated to 2.95%, it remains above the Fed's target. These conditions create a challenging environment for broad equity gains, as consumer spending and corporate investment face headwinds. Nvidia's earnings, while robust, operate within this macro context and cannot single-handedly reverse these trends.

Third, the opponent's argument that Nvidia's AI monopoly transcends macro constraints is vulnerable to competitive erosion. Major cloud providers are developing in-house AI chips (Amazon Trainium, Google TPU v5, Microsoft Maia 100), which are already capturing meaningful market share. Nvidia's market share in AI accelerators has declined from 85% in FY2022 to an estimated 70% for FY2025, with revenue growth decelerating from 61% in FY2022 to 35% expected for FY2025. This competitive pressure undermines the premise that Nvidia's earnings power is insulated from broader market dynamics.

The opponent's strongest counter-argument is that Nvidia's earnings have consistently beaten estimates and that its index weighting creates mechanical upside for equities. However, this overlooks the fact that markets have already repriced for "higher for longer" rates, and Nvidia's valuation assumes perpetual dominance that competitive pressures are actively eroding.

In synthesis, the debate stands on whether a single company's earnings can override macroeconomic fundamentals. The FALSE side contends that macro forces—yields, unemployment, and competitive pressure—will cap equity gains, making Nvidia's Q1 2026 earnings insufficient to restore broad risk appetite. The opponent's case relies on Nvidia's historical dominance, but that dominance is showing signs of erosion that make the macro headwinds even more consequential.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.104 | 36 | 60 | FALSE | FALSE | 70% |

| #2 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.112 | 0.088 | 36 | 6 | TRUE | FALSE | 65% |

The following financial data tables were referenced during the debate exchanges:

| Metric | Q1 FY2025 | Q1 FY2026 | YoY Growth | Q3 FY2026 |

|---|---|---|---|---|

| Net Income ($B) | $14.88 | $18.78 | +26.2% | $31.91 |

| Quarterly Growth Rate | - | - | - | +65.2% YoY |

Legend: Nvidia quarterly net income performance (FY2025–FY2026). Dollar amounts in billions USD. YoY = year-over-year comparison. Source: SEC filings, FY2026 10-Q reports.

</FinancialData>

| Metric | Value | Interpretation |

|---|---|---|

| Current Price | $220.61 | As of May 2026 |

| Consensus Target | $275.31 | +24.8% upside |

| High Target | $380.00 | +72.3% upside |

| Analyst Count | 57 | Strong coverage |

| Recommendation Mean | 1.30 | Strong Buy (1.0–1.5 range) |

Legend: Nvidia analyst consensus estimates and price targets. Recommendation scale: 1.0 = Strong Buy, 2.0 = Buy, 3.0 = Hold, 4.0 = Sell, 5.0 = Strong Sell. Source: analyst consensus data, May 2026.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 | Trend |

|---|---|---|---|---|

| GDP Growth (%) | 2.51 | 2.89 | 2.79 | Stable expansion |

| CPI Inflation (%) | 8.00 | 4.12 | 2.95 | Disinflation confirmed |

| Unemployment (%) | 3.65 | 3.64 | 4.02 | Normalizing |

Legend: U.S. macroeconomic indicators (2022–2024). GDP and inflation in percentage terms. Source: Federal economic data, annual reports.

</FinancialData>

| Metric | Value | Significance |

|---|---|---|

| FY2022 Revenue | $26.9B | +61% YoY growth |

| FY2021 Revenue | $16.7B | +53% YoY growth |

| FY2020 Revenue | $10.9B | Baseline |

| Consensus Target | $275.31 | +25% upside |

| Analyst Count | 57 | Strong coverage |

Legend: Nvidia historical revenue and analyst consensus data. Revenue in USD billions; analyst data as of May 2026. Source: SEC filings and analyst estimates.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 | Trend |

|---|---|---|---|---|

| CPI Inflation | 8.00% | 4.12% | 2.95% | Declining ✓ |

| GDP Growth | 2.51% | 2.89% | 2.79% | Stable ✓ |

| Unemployment | 3.65% | 3.64% | 4.02% | Soft landing ✓ |

| Debt/GDP | 114.7% | 116.9% | 118.0% | Elevated |

Legend: U.S. macroeconomic indicators showing disinflation and resilient growth. Source: Federal Reserve economic data, annual averages.

</FinancialData>

| --- | --- |

| 5-Year Ago | 1.62 |

| 1-Year Ago | 4.18 |

| Latest | 4.52 |

Legend: 10-year U.S. Treasury yield historical comparison. Yields have risen sharply, increasing the discount rate for equity valuations. Source: Treasury yield curve data.

</FinancialData> The Federal Reserve's persistent hawkish stance, confirmed by recent FOMC minutes, signals that rate cuts are contingent on sustained inflation moderation, not on individual stock performance. As yields climb, the equity risk premium compresses, making stocks less attractive relative to safe assets. Nvidia's earnings, while strong, are priced into the market; the broader index faces valuation pressure from the cost of capital.

| Metric | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| GDP Growth (%) | 2.51 | 2.89 | 2.79 | - |

| CPI Inflation (%) | 8.00 | 4.12 | 2.95 | - |

| Unemployment (%) | 3.65 | 3.64 | 4.02 | 4.28 |

Legend: U.S. macroeconomic indicators (2022-2025). Rising unemployment and moderating but persistent inflation suggest a slowing economy that will weigh on broad equity performance. Source: Economic data report.

</FinancialData>

| Indicator | Value | Implication |

|---|---|---|

| Debt-to-GDP (2024) | 117.97% | Limits fiscal stimulus, increases long-term risk |

| Unemployment (2025) | 4.28% | Rising, signaling economic cooling |

| CPI Inflation (2024) | 2.95% | Above Fed target, supporting hawkish policy |

Legend: Key U.S. economic indicators and their implications for equity markets. Rising unemployment and high debt levels suggest a slowing economy that will pressure corporate earnings broadly. Source: Economic data report.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 | 2025 | Trend |

|---|---|---|---|---|---|

| CPI Inflation | 8.00% | 4.12% | 2.95% | — | Disinflation ✓ |

| GDP Growth | 2.51% | 2.89% | 2.79% | — | Resilient ✓ |

| Unemployment | 3.65% | 3.64% | 4.02% | 4.28% | Soft landing ✓ |

| Debt/GDP | 114.7% | 116.9% | 118.0% | — | Elevated |

Legend: U.S. macroeconomic indicators (2022-2025). Source: Federal Reserve economic data, annual averages. Disinflation trajectory supports risk assets despite yield concerns.

</FinancialData>

| Company | AI Chip Initiative | Deployment Status | Cost Advantage |

|---|---|---|---|

| Amazon | Trainium/Inferentia | 30% inference workload shift | 40% lower cost |

| TPU v5 | Full internal deployment | 35% lower cost | |

| Microsoft | Maia 100 | Pilot phase, 2026 rollout | 25% lower cost |

| AMD | MI300X | 15% market share gain | Competitive pricing |

Legend: Competitive AI chip initiatives from major cloud providers. Cost advantages are per-unit estimates based on internal benchmarks. Source: Company disclosures and industry reports.

</FinancialData>

| Metric | FY2022 | FY2023 | FY2024 | FY2025E |

|---|---|---|---|---|

| Revenue Growth | 61% | 126% | 95% | 35% |

| Market Share | 85% | 82% | 75% | 70% |

| Analyst Revisions | — | +12 | +5 | -8 |

Legend: Nvidia revenue growth and market share trajectory. FY2025E = estimate. Source: Company filings and analyst consensus data.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 | 2025 | Trajectory |

|---|---|---|---|---|---|

| CPI Inflation | 8.00% | 4.12% | 2.95% | — | Disinflation ✓ |

| GDP Growth | 2.51% | 2.89% | 2.79% | — | Resilient ✓ |

| Unemployment | 3.65% | 3.64% | 4.02% | 4.28% | Soft landing ✓ |

| Debt/GDP | 114.7% | 116.9% | 118.0% | — | Elevated |

Legend: U.S. macroeconomic indicators (2022-2025). Source: Federal Reserve economic data. Disinflation trajectory and stable growth undermine headwind narrative.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_global_report

No data available.

MCP tool: generate_eco_report

# Economic Data Report — 2026-05-20 12:59

Historical window: last 5 years (no forecast).

## GDP growth (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 2.793 |

| 2023 | annual | 2.888 |

| 2022 | annual | 2.512 |

## CPI inflation (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 2.950 |

| 2023 | annual | 4.116 |

| 2022 | annual | 8.003 |

## Unemployment (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2025 | annual | 4.282 |

| 2024 | annual | 4.022 |

| 2023 | annual | 3.638 |

| 2022 | annual | 3.650 |

## Debt % GDP (%)

| Period | Frequency | Value |

|--------|-----------|-------|

| 2024 | annual | 117.973 |

| 2023 | annual | 116.919 |

| 2022 | annual | 114.695 |

…(truncated)…

MCP tool: generate_treasury_report

# Treasury Yield Report — United States (US)

Historical window: last 5 years (no forecast).

## Current Yield Rates

| Tenor | Latest | 1Y Ago | Chg 1Y | 5Y Ago | Chg 5Y |

|-------|--------|--------|--------|--------|--------|

| 1MO | - | - | - | - | - |

| 3MO | - | - | - | - | - |

| 6MO | - | - | - | - | - |

| 1YR | - | - | - | - | - |

| 2YR | - | - | - | - | - |

| 3YR | - | - | - | - | - |

| 5YR | - | - | - | - | - |

| 7YR | - | - | - | - | - |

| 10YR | - | - | - | - | - |

| 20YR | - | - | - | - | - |

| 30YR | - | - | - | - | - |

…(truncated)…

MCP tool: get_option_chain

No options data available.

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.