$NOW (ServiceNow) will outperform the broader market by the end of 2026.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed April 26, 2026

Tournament Final Verdict

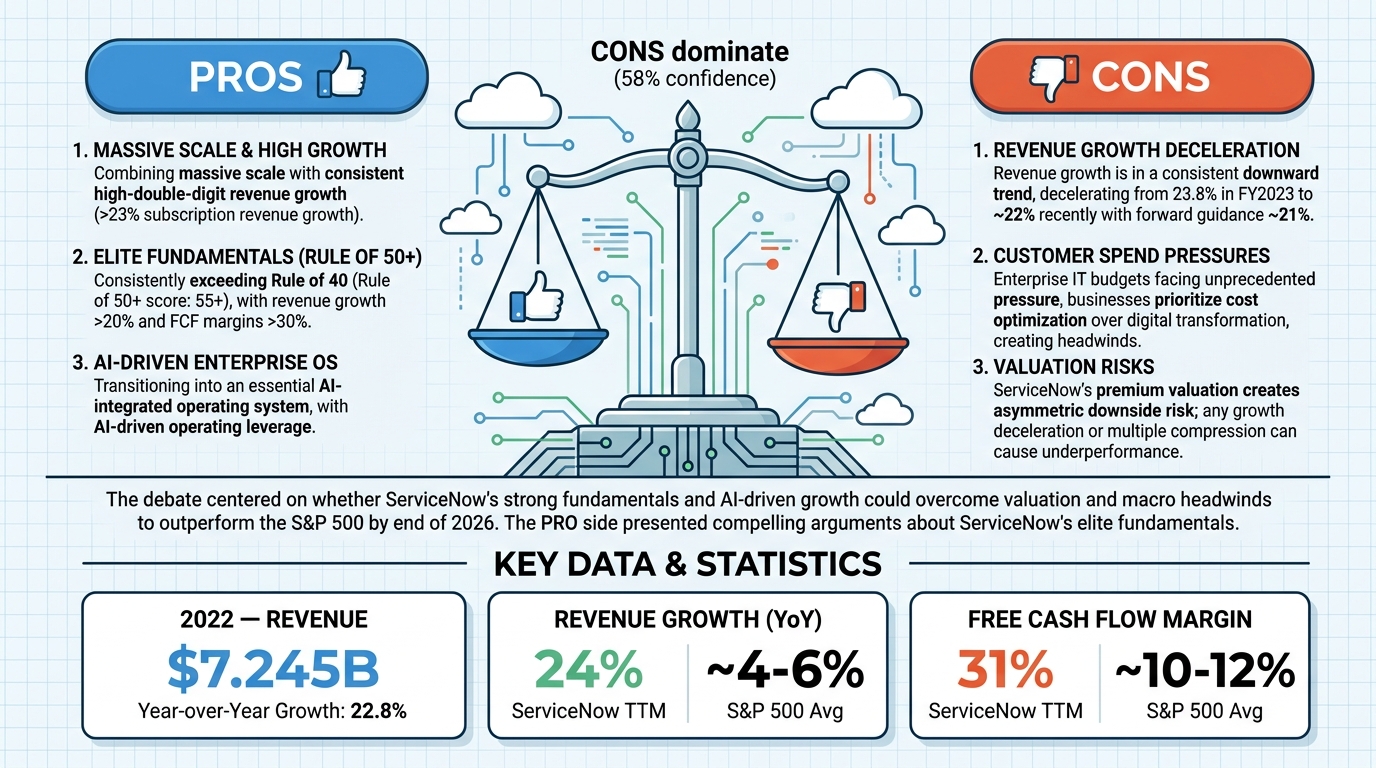

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 58%

Web Report: https://solsice.com/public/debates/now-servicenow-will-outperform-the-broader-market-by-the-end-1e586b4f093d

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■ServiceNow exhibits a rare combination of massive scale and consistent high-double-digit revenue growth (exceeding 23% subscription revenue growth), significantly outpacing the S&P 500's historical average returns, driven by its 'platform of platforms' strategy with high switching costs.

- ■ServiceNow consistently exceeds the 'Rule of 40' threshold (Rule of 50+), maintaining revenue growth above 20% alongside free cash flow margins exceeding 30%, proving it is not merely a 'growth at any price' play but a cash-generating powerhouse.

- ■ServiceNow is transitioning into an essential AI-integrated operating system for the modern enterprise, with AI-driven operating leverage providing a structural catalyst for continued outperformance against a broader market facing cyclical pressures.

❌ Key ANTI arguments:

- ■ServiceNow's revenue growth is in a consistent downward trend, decelerating from 23.8% in FY2023 to approximately 22% in recent quarters with forward guidance pointing toward ~21%, suggesting the high-growth narrative is weakening.

- ■Enterprise IT budgets are facing unprecedented pressure as businesses prioritize cost optimization over digital transformation, creating severe headwinds for ServiceNow's growth-dependent valuation.

- ■ServiceNow's premium valuation creates asymmetric downside risk — any further growth deceleration or multiple compression could lead to significant underperformance relative to the broader market.

💭 Conclusion: The debate centered on whether ServiceNow's strong fundamentals and AI-driven growth could overcome valuation and macro headwinds to outperform the S&P 500 by end of 2026. The PRO side presented compelling arguments about ServiceNow's elite growth-profitability profile, high switching costs, and AI integration catalysts. The FALSE side countered with evidence of growth deceleration, enterprise spending pressures, and the asymmetric downside risk inherent in premium valuations. The judge sided narrowly with the FALSE position at 58% confidence, suggesting that while ServiceNow's fundamentals are strong, the combination of decelerating growth, premium valuation risk, and macroeconomic uncertainty makes outperformance against the broader market uncertain rather than likely. This is a low-confidence verdict reflecting genuine uncertainty about the outcome.

🔬 DeepResearch Result: FALSE ❌ (58% confidence)

Assertion: $NOW (ServiceNow) will outperform the broader market by the end of 2026.

📊 Tournament: 0 voted TRUE, 1 voted FALSE (1 debates played, 3 models)

📊 Weighted scores: TRUE=0.00, FALSE=0.58

🏅 Judge Score Changes:

anthropic/claude-opus-4.6: +6

✅ PRO Arguments:

- ■ServiceNow exhibits a rare combination of massive scale and consistent high-double-digit revenue growth (exceeding 23% subscription revenue growth), significantly outpacing the S&P 500's historical average returns, driven by its 'platform of platforms' strategy with high switching costs. [google/gemini-3-flash-preview]

- ■ServiceNow consistently exceeds the 'Rule of 40' threshold (Rule of 50+), maintaining revenue growth above 20% alongside free cash flow margins exceeding 30%, proving it is not merely a 'growth at any price' play but a cash-generating powerhouse. [google/gemini-3-flash-preview]

- ■ServiceNow is transitioning into an essential AI-integrated operating system for the modern enterprise, with AI-driven operating leverage providing a structural catalyst for continued outperformance against a broader market facing cyclical pressures. [google/gemini-3-flash-preview]

- ■ServiceNow's high renewal rates and deep enterprise integration create a durable moat that provides defensive characteristics alongside aggressive expansion potential, offering superior risk-adjusted returns compared to the diversified S&P 500. [google/gemini-3-flash-preview]

❌ ANTI Arguments:

- ■ServiceNow's revenue growth is in a consistent downward trend, decelerating from 23.8% in FY2023 to approximately 22% in recent quarters with forward guidance pointing toward ~21%, suggesting the high-growth narrative is weakening. [deepseek/deepseek-v3.2]

- ■Enterprise IT budgets are facing unprecedented pressure as businesses prioritize cost optimization over digital transformation, creating severe headwinds for ServiceNow's growth-dependent valuation. [deepseek/deepseek-v3.2]

- ■ServiceNow's premium valuation creates asymmetric downside risk — any further growth deceleration or multiple compression could lead to significant underperformance relative to the broader market. [deepseek/deepseek-v3.2]

- ■The broader S&P 500's diversification across sectors provides a more resilient return profile against macroeconomic headwinds, while ServiceNow's concentrated exposure to enterprise software spending makes it vulnerable to cyclical downturns. [deepseek/deepseek-v3.2]

💭 Reasoning: The debate centered on whether ServiceNow's strong fundamentals and AI-driven growth could overcome valuation and macro headwinds to outperform the S&P 500 by end of 2026. The PRO side presented compelling arguments about ServiceNow's elite growth-profitability profile, high switching costs, and AI integration catalysts. The FALSE side countered with evidence of growth deceleration, enterprise spending pressures, and the asymmetric downside risk inherent in premium valuations. The judge sided narrowly with the FALSE position at 58% confidence, suggesting that while ServiceNow's fundamentals are strong, the combination of decelerating growth, premium valuation risk, and macroeconomic uncertainty makes outperformance against the broader market uncertain rather than likely. This is a low-confidence verdict reflecting genuine uncertainty about the outcome.

📋 PRO Facts:

• ServiceNow maintained subscription revenue growth exceeding 23% in recent fiscal years

• The company consistently exceeds the Rule of 40 threshold with combined growth and FCF margins

• ServiceNow operates a 'platform of platforms' strategy integrating disparate enterprise workflows

• The company maintains high renewal rates indicating strong customer retention

📋 ANTI Facts:

• ServiceNow's revenue growth has decelerated from 23.8% in FY2023 to approximately 22% in recent quarters

• Forward guidance points toward approximately 21% growth, continuing the deceleration trend

• Enterprise IT budgets are under pressure with businesses prioritizing cost optimization

• ServiceNow trades at a premium valuation relative to the broader market

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | google/gemini-3-flash-preview | deepseek/deepseek-v3.2 | 0.153 | 0.084 | 42 | 9 | TRUE | FALSE | 58% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] ARPU — Average Revenue Per User — A metric that measures the revenue generated per user or account, used to assess a company's ability to monetize its customer base over time.

[2] asymmetric downside risk — A situation where the potential for losses significantly exceeds the potential for gains, often occurring when an asset is priced for perfection and any negative surprise causes disproportionate declines.

[3] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates and bond yields.

[4] CSM — Customer Service Management — A category of enterprise software that manages and automates customer service workflows, including case management, self-service portals, and issue resolution.

[5] digital transformation — The process by which organizations adopt digital technologies to fundamentally change business operations, processes, and customer experiences to improve efficiency and competitiveness.

[6] earnings compression — A decline in a company's or index's earnings or profit margins, often caused by rising costs, slowing revenue, or macroeconomic pressures such as higher interest rates.

[7] FCF — Free Cash Flow — The cash generated by a company's operations after deducting capital expenditures, representing the cash available for dividends, debt repayment, share buybacks, or reinvestment.

[8] FCF margin — Free Cash Flow Margin — Free cash flow expressed as a percentage of revenue, indicating how efficiently a company converts its sales into available cash.

[9] forward P/E — Forward Price-to-Earnings Ratio — A valuation metric that divides a company's current stock price by its estimated future earnings per share, used to assess whether a stock is over- or undervalued relative to expected profits.

[10] FY — Fiscal Year — A 12-month period used by companies for accounting and financial reporting purposes, which may or may not align with the calendar year.

[11] GenAI — Generative AI — A category of artificial intelligence capable of creating new content such as text, code, images, or data, increasingly embedded in enterprise software to automate tasks and enhance productivity.

[12] higher-for-longer — A monetary policy outlook in which central bank interest rates are expected to remain elevated for an extended period, impacting asset valuations, particularly for growth stocks with distant cash flows.

[13] ITSM — IT Service Management — A set of practices and tools for designing, delivering, managing, and improving the way IT services are used within an organization, often involving ticketing, incident management, and change management.

[14] moat — A competitive advantage that protects a company from rivals, analogous to a castle's moat; examples include high switching costs, network effects, brand strength, or proprietary technology.

[15] multiple compression — A decline in a stock's valuation multiple (such as P/E or P/S ratio) even if earnings remain stable, often driven by rising interest rates, shifting investor sentiment, or sector rotation.

[16] new deal velocity — The rate at which new sales contracts or deals are being closed, used as a leading indicator of future revenue growth in enterprise software and SaaS businesses.

[17] non-GAAP operating margins — Non-Generally Accepted Accounting Principles Operating Margins — Operating margins calculated by excluding certain items such as stock-based compensation, amortization of intangibles, and restructuring charges, intended to provide a clearer view of core operational profitability.

[18] NYSE — New York Stock Exchange — The largest stock exchange in the world by market capitalization, located in New York City, where shares of publicly listed companies are bought and sold.

[19] operating leverage — The degree to which a company can increase operating income by increasing revenue without a proportional increase in operating costs, common in software businesses with high fixed costs and low marginal costs.

[20] P/E — Price-to-Earnings Ratio — A valuation metric calculated by dividing a company's stock price by its earnings per share, used to assess how much investors are willing to pay per dollar of earnings.

[21] P/S — Price-to-Sales Ratio — A valuation metric calculated by dividing a company's market capitalization by its total revenue, often used for high-growth companies that may not yet be profitable.

[22] platform of platforms — A business strategy in which a single software platform integrates multiple functional modules and workflows, creating a unified system that increases customer dependency and switching costs.

[23] quality of earnings — An assessment of how sustainable, recurring, and cash-backed a company's reported earnings are, with higher quality indicating earnings driven by core operations rather than one-time items or accounting adjustments.

[24] R&D — Research and Development — Activities undertaken by a company to innovate and develop new products, services, or technologies, typically reported as an operating expense on the income statement.

[25] recurring revenue — Revenue that is predictable, stable, and expected to continue at regular intervals, typically from subscription contracts, providing greater visibility into future financial performance.

[26] renewal rate — The percentage of customers who renew their subscriptions or contracts at the end of a term, serving as a key indicator of customer satisfaction and revenue predictability in SaaS businesses.

[27] risk-adjusted return — A measure of investment return that accounts for the level of risk taken to achieve it, allowing comparison between investments with different risk profiles.

[28] Rule of 40 — A SaaS industry benchmark stating that a healthy software company's combined revenue growth rate and profit margin (typically FCF or EBITDA margin) should equal or exceed 40%.

[29] S&P 500 — Standard & Poor's 500 — A stock market index tracking the performance of 500 large-cap U.S. publicly traded companies, widely used as a benchmark for the overall U.S. equity market.

[30] SaaS — Software as a Service — A software distribution model in which applications are hosted in the cloud and provided to customers on a subscription basis, rather than through one-time license purchases.

[31] seat-based pricing — A software pricing model where customers pay based on the number of individual users or licenses, as opposed to usage-based or value-based pricing models.

[32] share repurchases — A corporate action in which a company buys back its own outstanding shares from the market, reducing the share count and typically increasing earnings per share and shareholder value.

[33] switching costs — The expenses, effort, or disruption a customer faces when changing from one product or service provider to another, which can create a competitive moat for incumbent vendors.

[34] total return — The complete return on an investment including both capital appreciation (price gains) and income (such as dividends), expressed as a percentage of the initial investment.

[35] TTM — Trailing Twelve Months — A measurement period covering the most recent 12 consecutive months of financial data, used to evaluate a company's current performance without waiting for annual reports.

[36] unit economics — The direct revenues and costs associated with a particular business model on a per-unit basis (e.g., per customer or per transaction), used to assess the fundamental profitability of a business.

[37] value-based pricing — A pricing strategy where the price is set based on the perceived or delivered value to the customer rather than on cost or number of users, often enabling higher revenue per customer.

[38] YoY — Year-over-Year — A method of comparing a financial metric for one period with the same period in the previous year, used to assess growth trends while accounting for seasonality.

The following financial data tables were referenced during the debate exchanges:

| Fiscal Year | Revenue (USD Billions) | Year-over-Year Growth |

|---|---|---|

| 2021 | $5.896B | -- |

| 2022 | $7.245B | 22.8% |

| 2023 | $8.971B | 23.8% |

Legend: Annual revenue and calculated growth rates for ServiceNow (FY2021–FY2023). Source: SEC Filings.

</FinancialData>

| Metric | ServiceNow (TTM) | S&P 500 Average |

|---|---|---|

| Revenue Growth (YoY) | 24% | ~4-6% |

| Free Cash Flow Margin | 31% | ~10-12% |

| Rule of 40 Score | 55 | < 20 |

Legend: Comparison of growth and efficiency metrics between ServiceNow and the S&P 500 index average (Trailing Twelve Months). Source: Public financial disclosures and market index data.

</FinancialData>

| Period | Subscription Revenue Growth | Guidance/Implied Forward Growth |

|---|---|---|

| FY 2023 | 23.8% | -- |

| Q4 2023 | ~22% | -- |

| FY 2024 Guidance | ~21% | Continued deceleration |

Legend: ServiceNow's subscription revenue growth showing clear deceleration trend. Source: Company earnings reports and guidance.

</FinancialData>

| Metric | ServiceNow (Est. 2024-2026) | S&P 500 (Historical Avg) |

|---|---|---|

| Annual Revenue Growth | 21% - 24% | 5% - 7% |

| Free Cash Flow Margin | ~31% | ~11% |

| Customer Retention | 98%+ | N/A |

Legend: Comparative financial health and growth projections for ServiceNow versus broader market benchmarks. Source: Compiled from quarterly earnings reports and consensus estimates.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.