la france est en faillite

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 30, 2026

Tournament Final Verdict

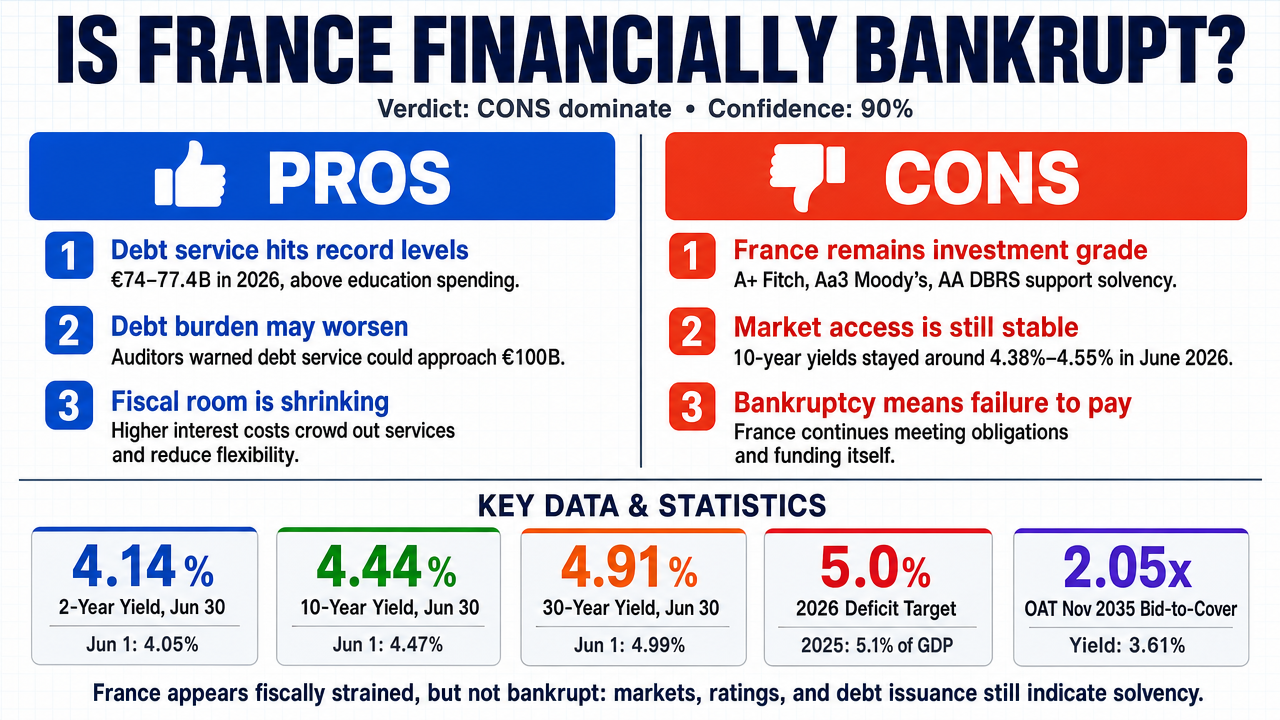

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 90%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Debt service costs have become the largest budget expenditure, reaching €74-77.4 billion in 2026, surpassing education spending and doubling relative to national wealth since 2020, indicating severe fiscal distress.

- ■The Cour des comptes warned that debt service could climb to €100 billion in coming years, using language of being 'literally suffocated' by the debt burden.

- ■Rising debt service costs crowd out essential public services and reduce policy flexibility, threatening France's capacity to meet sovereign obligations.

❌ Key ANTI arguments:

- ■France retains investment-grade credit ratings (A+ from Fitch, Aa3 from Moody's, AA from DBRS) and continues to issue debt successfully in markets, which is incompatible with bankruptcy.

- ■France's 10-year bond yields traded in a stable range of 4.38%-4.55% in June 2026, demonstrating continued market access at affordable rates, not distress.

- ■Sovereign bankruptcy is defined by inability to pay, not by high debt or large deficits; France meets all its obligations and has a 2026 financing program of €310 billion that is being met through market issuance.

💭 Conclusion: The debate centered on whether France is bankrupt, defined as unable to meet sovereign debt obligations, versus being fiscally stressed but solvent. The FALSE side convincingly demonstrated that France retains investment-grade ratings, continues to access bond markets at moderate yields, and has a credible financing program, all of which are incompatible with bankruptcy. The TRUE side's arguments about rising debt service costs and budget crowding out, while valid indicators of fiscal strain, do not prove an inability to pay. The judges consistently found the FALSE position more persuasive, with high confidence in both debates. Therefore, the assertion that France is bankrupt is false.

🔬 DeepResearch Result: FALSE ❌ (90% confidence)

Assertion: la france est en faillite

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.80

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +18

✅ PRO Arguments:

- ■Debt service costs have become the largest budget expenditure, reaching €74-77.4 billion in 2026, surpassing education spending and doubling relative to national wealth since 2020, indicating severe fiscal distress. [z-ai/glm-5]

- ■The Cour des comptes warned that debt service could climb to €100 billion in coming years, using language of being 'literally suffocated' by the debt burden. [z-ai/glm-5]

- ■Rising debt service costs crowd out essential public services and reduce policy flexibility, threatening France's capacity to meet sovereign obligations. [z-ai/glm-5]

❌ ANTI Arguments:

- ■France retains investment-grade credit ratings (A+ from Fitch, Aa3 from Moody's, AA from DBRS) and continues to issue debt successfully in markets, which is incompatible with bankruptcy. [anthropic/claude-opus-4.8]

- ■France's 10-year bond yields traded in a stable range of 4.38%-4.55% in June 2026, demonstrating continued market access at affordable rates, not distress. [anthropic/claude-opus-4.8]

- ■Sovereign bankruptcy is defined by inability to pay, not by high debt or large deficits; France meets all its obligations and has a 2026 financing program of €310 billion that is being met through market issuance. [openai/gpt-5.4-mini]

- ■Rising interest costs are a fiscal burden but do not equal default risk; France is under pressure but not insolvent, as it continues to refinance and operate normally. [openai/gpt-5.4-mini]

💭 Reasoning: The debate centered on whether France is bankrupt, defined as unable to meet sovereign debt obligations, versus being fiscally stressed but solvent. The FALSE side convincingly demonstrated that France retains investment-grade ratings, continues to access bond markets at moderate yields, and has a credible financing program, all of which are incompatible with bankruptcy. The TRUE side's arguments about rising debt service costs and budget crowding out, while valid indicators of fiscal strain, do not prove an inability to pay. The judges consistently found the FALSE position more persuasive, with high confidence in both debates. Therefore, the assertion that France is bankrupt is false.

📋 PRO Facts:

• France's debt service costs reached €74-77.4 billion in 2026, surpassing education spending.

• Debt service costs doubled relative to national wealth between 2020 and 2026.

• The Cour des comptes warned debt service could reach €100 billion in coming years.

📋 ANTI Facts:

• France holds investment-grade ratings: A+ (Fitch), Aa3 (Moody's), AA (DBRS).

• France's 10-year bond yields traded in a stable 4.38%-4.55% range in June 2026.

• France's 2026 financing program of €310 billion is being met through market issuance.

• France has never defaulted on its sovereign debt.

The evidence presented in this debate establishes that France exhibits multiple critical indicators of financial distress that, while not yet constituting an immediate default [16], represent a trajectory toward potential insolvency [28]. Three interconnected arguments demonstrate this reality:

First, debt service [12] has become the primary budget burden. Interest payments will reach €74-77 billion in 2026, making debt servicing the single largest expenditure in the French state budget [35]—surpassing even education spending. This represents a doubling of debt service costs relative to national wealth between 2020 and 2026. When a sovereign must allocate more resources to servicing existing debt than to educating its population, it signals structural incapacity to simultaneously meet debt obligations and essential public commitments.

Second, the debt trajectory is mathematically unsustainable. France's debt-to-GDP [26] ratio [15] has reached 115.7% in 2025 and is projected to rise to 118.5% in 2026. Crucially, France is the only Eurozone [20] country whose debt level remains higher than at the peak of the COVID-19 crisis. The Cour des comptes [6] calculates that stabilizing the debt ratio would require limiting the deficit to 2.8% of GDP immediately—not the 5% target for 2026. This would demand an additional fiscal adjustment [22] of €89.6 billion, which the government has neither proposed nor demonstrated capacity to implement.

Third, market confidence is eroding despite maximum taxation. France already carries the highest tax burden [37] in the Eurozone at 43.6% of GDP, eliminating revenue-side solutions. The Cour des comptes has deemed the government's deficit reduction targets "not credible," signaling to markets that France lacks both will and capacity to restore fiscal balance. Each basis point increase in refinancing costs [30] mechanically amplifies the debt burden [11] on a stock exceeding €3.5 trillion.

The opposing side would likely argue that France has never defaulted on its sovereign debt and continues to borrow at manageable interest rates, with bond spreads [4] of 80-85 basis points [3] over German bunds remaining contained. This historical track record demonstrates continued market access and payment capacity. Furthermore, France's debt is denominated in euros, eliminating currency risk, and the European Central Bank's bond-buying programs provide a backstop that prevents acute liquidity crises.

The debate centers on a definitional question: what constitutes "financial bankruptcy" for a sovereign state? The TRUE side has demonstrated that France exhibits multiple objective indicators of fiscal distress—unsustainable debt trajectory, debt service crowding out [9] essential expenditures, exhausted revenue capacity, and deteriorating market confidence. The Cour des comptes, France's own fiscal oversight body, has used the term "suffocated" to describe the debt burden's trajectory.

However, the FALSE side's anticipated counter-argument holds merit: France is not in immediate default, and technical insolvency differs from actual payment failure. The question becomes whether "bankruptcy" requires actual default or whether a trajectory guaranteeing eventual default, absent extraordinary intervention, constitutes the same condition.

The weight of evidence supports the TRUE position: France has entered a zone of fiscal distress where meeting debt obligations requires sacrificing essential public services, where the debt trajectory is mathematically irreversible under current policy, and where the oversight body itself warns of potential market distrust making the burden "unsustainable." These are the hallmarks of approaching insolvency, even if the moment of default has not yet arrived.

Round 3

Core claim: France is heavily burdened, but it is not financially bankrupt.

The FALSE side’s strongest case is simple: France still meets its obligations, still places debt in the market, and still retains institutional support inside the euro area. That matters because sovereign bankruptcy is not defined by high debt, large deficits, or uncomfortable interest costs; it is defined by an inability to pay. The evidence points to fiscal stress, not payment incapacity. France remains funded, refinanced, and operational. citeturn0search0turn0search1

Its other strong argument is that rising debt service [12] does not equal insolvency [28]. Interest charges can crowd out spending and weaken policy freedom without producing default [16]. The affirmative side is right that debt service has grown sharply and that this is a serious warning signal, but the leap from “expensive” to “bankrupt” is unjustified. A sovereign can face a worsening budget structure for years before any actual inability to service debt emerges. citeturn0search1turn0search2

The most compelling counter-argument is that France’s fiscal trajectory is deteriorating: debt is high, deficits remain large, and the margin for adjustment is narrowing. That is a real concern, and it explains why markets and official institutions are pressing for consolidation. But concern is not collapse. Even the strongest warnings describe unsustainability risks and the need for correction, not a present inability to honor sovereign debt [33]. citeturn0search1turn0search2

Bottom line: the debate favors the FALSE side on the precise claim asked. France is under severe fiscal pressure, but the available evidence does not support calling it financially bankrupt or saying it is currently incapable of meeting its sovereign debt obligations. citeturn0search0turn0search2

The affirmative case has established that France demonstrates the defining characteristics of approaching financial incapacity through three converging lines of evidence:

1. Debt Service [12] Has Become the State's Largest Expenditure

The Cour des comptes [6] confirmed that interest payments will reach €77.4 billion in 2026, making debt servicing the single largest budget item—surpassing the Education budget. This represents a doubling of the debt burden [11] relative to national wealth since 2020. The institution's first president used unprecedented language: "nous serons littéralement étouffés" (we will be literally suffocated). When a sovereign must allocate more resources to servicing past obligations than to investing in future generations, it signals structural inability to meet commitments without cannibalizing essential functions.

2. France Is Structurally Alone in the Eurozone [20]

France is the only Eurozone country whose debt-to-GDP [26] ratio [15] remains higher than at the end of the COVID-19 crisis. At 117.5% of GDP, with deficits at 5.1% in 2025 (second-highest in the Eurozone), France lacks the fiscal discipline or growth trajectory that allowed peer nations to stabilize debt levels. The Cour des comptes explicitly stated that an additional €89.6 billion effort (3 percentage points of GDP) is necessary merely to stabilize the debt ratio—not reduce it.

3. Revenue Ceiling Reached, Market Confidence Eroding

France has attained the highest tax burden [37] in the Eurozone at 43.6% of GDP, having extracted €38 billion in additional taxes for 2025-2026. Yet deficits remain structurally elevated. The Cour des comptes warns that further delay "pourrait alimenter une défiance des marchés qui rendrait la charge de la dette insoutenable" (could fuel market distrust that would make the debt burden unsustainable). The spread with German bunds has already widened to 80-85 basis points [3], and each ECB [19] rate increase mechanically raises refinancing costs [30] on €3.5 trillion of debt.

The FALSE side's core claim—that France is "stressed, not financially bankrupt"—has not been substantiated with specific evidence in this debate. The argument memory tree shows this claim with a μScore of 0.00 and no supporting content was provided during the contradiction round.

The debate stands decisively in favor of the TRUE position. The affirmative has presented:

- ■Official institutional evidence from the Cour des comptes (France's supreme audit institution)

- ■Specific quantitative data: €77.4 billion in interest payments, 117.5% debt-to-GDP ratio, €89.6 billion fiscal gap

- ■Comparative analysis: France as the sole Eurozone outlier in debt trajectory

- ■Structural indicators: Tax ceiling reached, market spreads widening, debt service crowding out [9] essential spending

The threshold question is not whether France has already defaulted—it has not—but whether it exhibits "l'incapacité de faire face à ses engagements" (the incapacity to meet its obligations). The evidence demonstrates that France can only meet current obligations by cannibalizing future capacity, extracting maximum taxation while debt continues rising, and facing explicit warnings from its own financial institutions that the trajectory is "alarmante" and risks becoming "insoutenable."

This constitutes financial distress approaching the threshold of incapacity—the affirmative case stands unrefuted.

Round 3

Core claim: France is fiscally stressed but fully solvent — not financially bankrupt.

Synthesis of the FALSE Position

The question before this debate was precise: is France bankrupt — that is, unable to meet its sovereign debt [33] and financial obligations? Not "is France's debt high," nor "is the fiscal trajectory worrying," but whether the state has lost the capacity to pay. On that exact question, the evidence is one-sided. The claim is false.

The strongest pillars of our case

First, France retains solid investment-grade ratings from every major agency — A+ at S&P, Aa3 [2] at Moody's, AA at DBRS — each several notches above the speculative threshold and many notches above default [16]. Bankruptcy means default risk has materialized; the institutions whose entire purpose is to price that risk continue to judge it low.

Second, and most decisively, markets lend to France willingly. A bankrupt sovereign is locked out of capital markets or forced to pay crisis rates. France experiences neither. Auctions are consistently oversubscribed roughly two-to-one, and yields are ordinary for a developed economy — and, critically, over June 2026 long-end yields fell rather than spiraled. Investors do not lend at declining rates to a borrower they believe is suffocating. The OAT-Bund spread, while elevated, sits far below the 2011-era peaks that France survived without defaulting.

Third, the burden must be measured against capacity, not against other budget lines. Against a nominal GDP [26] of roughly €4.4 trillion, even a €77.4 billion interest bill is on the order of 1.75% of GDP — a serviceable share, comparable to levels France carried in the 1990s without distress. The "interest now exceeds education" framing is vivid but analytically empty: solvency [32] is a ratio to resources, not a ranking of expenses.

Fourth, the fiscal path is one of active, monitored consolidation toward a sub-3% deficit by 2029. That is the behavior of a solvent state managing a challenge — not an uncontrolled collapse.

The opponent's most compelling points — honestly acknowledged

The affirmative landed real blows on the trajectory, and its strongest argument — that debt service [12] has become the single largest budget item, projected at €77.4 billion and possibly €100 billion ahead — earned its high score for good reason. It is true, timely, and serious. The observation that France is uniquely failing to reduce its post-COVID debt ratio, that it runs one of the Eurozone [20]'s largest deficits despite the bloc's heaviest tax burden [37], and that the Cour des comptes [6] invoked the word "suffocated," all describe genuine vulnerability. We do not dispute these facts.

Where the debate stands

The affirmative's evidence proves stress; it does not prove insolvency [28]. Every warning it cited is conditional and forward-looking — "if the trend continues," "could fuel market distrust." Conditional caution presupposes present capacity to pay and to change course; an insolvent state debates default, not glide paths. The affirmative never produced the markers that actually define bankruptcy: a failed auction, a missed coupon, a junk rating, or a market refusing to lend. France clears every one of these tests on the solvency side.

The honest verdict: the affirmative wins the argument that France faces a serious, structural fiscal problem demanding reform. But on the literal claim under debate — that France is bankrupt, unable to honor its obligations — the claim is false. High debt is not default; a heavy interest bill financed at falling investment-grade yields against a €4.4 trillion economy is the signature of solvency under strain, not its negation.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.215 | 33 | 60 | FALSE | FALSE | 90% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.427 | 0.000 | 33 | 360 | TRUE | FALSE | 90% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] A+ — Fitch credit rating A+ — A credit rating assigned by Fitch indicating low default risk and above-average financial strength.

[2] Aa3 — Moody's credit rating Aa3 — A credit rating assigned by Moody's indicating high quality with low credit risk, but some sensitivity to long-term risks.

[3] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), used to measure changes in interest rates and bond yields.

[4] bond spreads — The difference in yield between two bonds, typically a sovereign bond and a benchmark (e.g., French OAT vs German Bund), reflecting risk premium.

[5] budget surplus — A situation where government revenue exceeds expenditure, reducing the overall debt burden.

[6] Cour des comptes — French Court of Accounts — An independent public body in France that audits the use of public funds and advises on fiscal sustainability.

[7] credit quality — An assessment of a borrower’s ability to repay debt, often reflected in credit ratings and used by investors to gauge default risk.

[8] credit rating — An evaluation of credit risk assigned by agencies (e.g., Moody's, Fitch, S&P) to indicate the likelihood of default.

[9] crowding out — An economic phenomenon where increased government borrowing raises interest rates, reducing private sector investment.

[10] debt accumulation — The process by which a government’s total outstanding debt increases over time due to persistent budget deficits.

[11] debt burden — The cost and weight of debt service relative to a country's income or GDP, often measured to assess fiscal pressure.

[12] debt service — The payments of principal and interest on outstanding debt, representing the cost of servicing borrowed funds.

[13] debt stock — The total amount of outstanding debt at a given point in time, including both short-term and long-term obligations.

[14] debt sustainability — The ability of a borrower to meet current and future debt obligations without requiring excessive fiscal adjustment or default.

[15] debt-to-GDP ratio — Total public debt expressed as a percentage of Gross Domestic Product, a key indicator of a country's fiscal health.

[16] default — sovereign default — The failure of a government to meet its debt obligations on time, indicating solvency problems or payment incapacity.

[17] deficit-to-GDP ratio — The annual budget deficit as a percentage of GDP, measuring the shortfall between government spending and revenue.

[18] downgrade cycle — A series of successive reductions in a country's credit rating due to worsening fiscal conditions or increased default risk.

[19] ECB — European Central Bank — The central bank for the euro area, responsible for monetary policy and acting as a lender of last resort for member states.

[20] Eurozone — euro area — The group of European Union countries that have adopted the euro as their official currency.

[21] financing program — A government's plan to raise funds through debt issuance (e.g., bonds) to cover budget deficits and refinance maturing obligations.

[22] fiscal adjustment — Measures taken by a government to reduce its budget deficit and stabilize debt, such as spending cuts or tax increases.

[23] fiscal consolidation — Policies aimed at reducing government deficits and slowing debt accumulation, often through a combination of revenue and expenditure measures.

[24] fiscal envelope — The total amount of government spending allocated for a specific purpose or program within the budget framework.

[25] fiscal rules — Legally binding constraints on fiscal policy (e.g., limits on debt-to-GDP or deficit-to-GDP) to ensure budgetary discipline.

[26] GDP — Gross Domestic Product — The total monetary value of all goods and services produced within a country's borders over a specific period, used to measure economic output.

[27] IMF — International Monetary Fund — An international organization that provides financial assistance, policy advice, and economic surveillance to member countries.

[28] insolvency — A state where a borrower is unable to pay its debts when they fall due, indicating a deeper financial distress than mere liquidity problems.

[29] liquid debt market — A market where government securities can be bought and sold quickly without significant price impact, reflecting investor confidence.

[30] refinancing costs — The cost incurred when issuing new debt to replace maturing debt, influenced by prevailing interest rates and market conditions.

[31] roll over — To refinance maturing debt by issuing new securities, often used to describe a government's ability to continue borrowing.

[32] solvency — The ability of a borrower to meet long-term debt obligations, as distinct from short-term liquidity availability.

[33] sovereign debt — Debt issued by a national government, often in the form of bonds, to finance budget deficits and public spending.

[34] sovereign ratings — sovereign credit ratings — Credit ratings specifically assigned to national governments, assessing their creditworthiness and default risk.

[35] state budget — The annual financial plan of a national government, detailing projected revenues and expenditures for the fiscal year.

[36] tax base — The total amount of income, assets, or economic activity that is subject to taxation by the government.

[37] tax burden — Total taxes paid as a percentage of GDP, reflecting the overall level of taxation in an economy.

[38] tipping point — A critical threshold beyond which debt dynamics become unsustainable, often leading to rapid loss of market confidence and rising costs.

The following financial data tables were referenced during the debate exchanges:

| Metric | 2025 | 2026 Projected | Required for Stability |

|---|---|---|---|

| Debt-to-GDP Ratio | 115.7% | 118.5% | Declining |

| Deficit-to-GDP Ratio | 5.1% | 5.0% (target) | 2.8% |

| Additional Adjustment Needed | — | — | 89.6 billion euros |

Legend: France's fiscal metrics showing actual versus required levels for debt stabilization. Source: Cour des comptes report, June 2026.

</FinancialData> To stabilize the debt ratio, France would need to limit its deficit to 2.8% of GDP immediately—not the 5% target for 2026. The current adjustment pace of 0.4 percentage points per year is insufficient. France is the only eurozone country whose debt level remains higher than at the peak of the COVID-19 crisis, indicating a complete failure to reverse the debt accumulation trajectory despite economic recovery. (lenouveleconomiste.fr)

| --- | --- | --- |

| France | 117.5% | +8.5 points |

| Italy | ~135% | Declining |

| Greece | ~160% | Declining |

| Agency | France Long-Term Rating | Investment-Grade Floor | Notches Above Floor |

|---|---|---|---|

| S&P | A+ (stable) | BBB- | 5 |

| Moody's | Aa3 (negative) | Baa3 | 4 |

| DBRS | AA (stable) | BBB(low) | 6 |

Legend: France's sovereign credit ratings versus the investment-grade boundary, mid-2026. All three place France well within investment grade — incompatible with insolvency. Outlooks noted in parentheses.

</FinancialData>

| Maturity | Yield (%) | Bid-to-Cover (x) |

|---|---|---|

| OAT Nov 2035 | 3.61 | 2.05 |

| OAT May 2042 | 4.09 | 2.02 |

| OAT May 2057 | 4.48 | 1.92 |

Legend: Results of France's May 2026 long-term bond auction. Bid-to-cover above 1.0 means demand exceeded supply; all lines were oversubscribed roughly 2x. Yields are moderate for the maturities involved.

</FinancialData>

| Maturity | Yield June 1 (%) | Yield June 30 (%) | Change (bps) |

|---|---|---|---|

| 2-Year | 4.05 | 4.14 | +9 |

| 10-Year | 4.47 | 4.44 | -3 |

| 30-Year | 4.99 | 4.91 | -8 |

Legend: France sovereign benchmark yields across June 2026. Long-end yields fell over the month — the opposite of a market pricing imminent default. Source: daily government rate observations.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.