it is a good idea to invest today in Microsoft Corporation Common Stock (MSFT)

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 26, 2026

Tournament Final Verdict

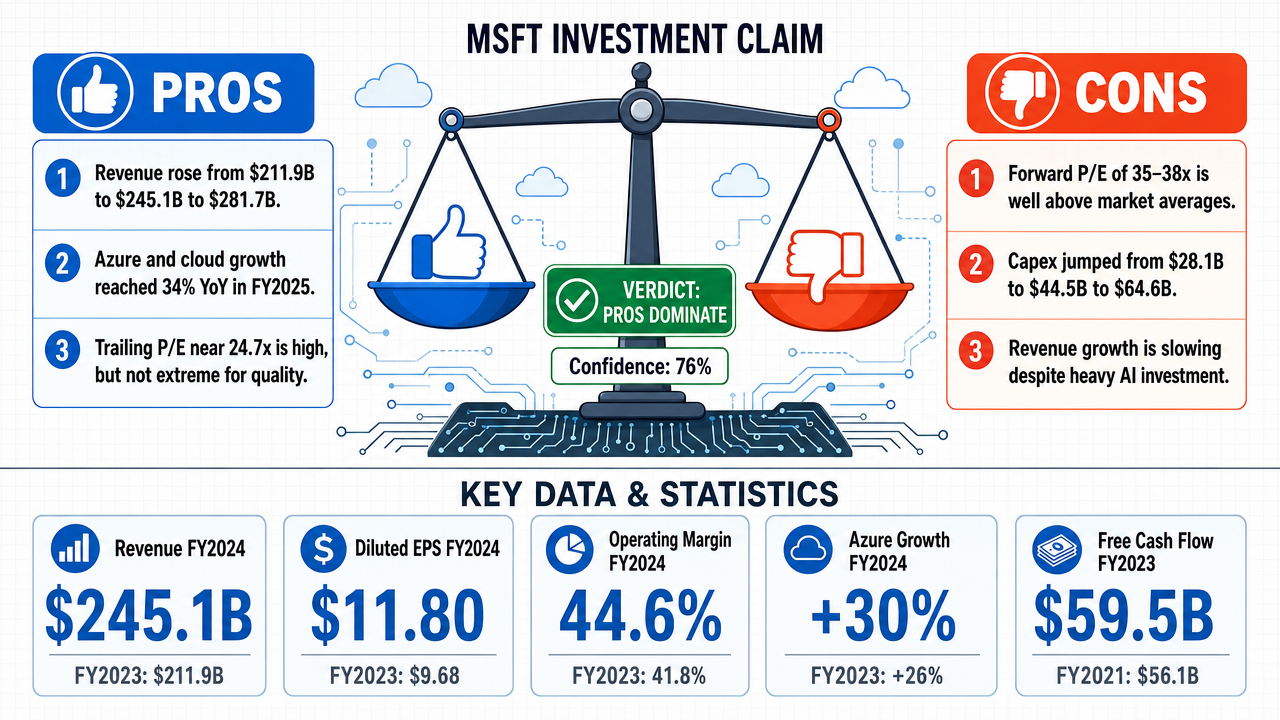

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 76%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Microsoft demonstrates exceptional financial momentum with revenue growing from $211.9B (FY2023) to $245.1B (FY2024) to $281.7B (FY2025), while operating income surged from $88.5B to $128.5B, yielding a TTM operating profit margin of ~46.8% and net profit margin of ~39.3% — hallmarks of a high-quality compounder with expanding margins.

- ■Microsoft's AI monetization is driving structural revenue acceleration: Azure and cloud services grew 34% YoY in FY2025 — the fastest among major hyperscalers — with the Microsoft Cloud segment surging 23% to $168.9B, demonstrating proven ability to convert AI investment into tangible, large-scale revenue growth.

- ■At a trailing P/E of approximately 24.7x (based on TTM diluted EPS of ~$16.79), Microsoft's valuation is demanding but not extreme given its elite profitability, consistent double-digit growth, and fortress balance sheet with debt-to-equity of only ~0.14 — making it a premium but justifiable investment.

❌ Key ANTI arguments:

- ■Microsoft's valuation is dangerously stretched: the forward P/E of ~35–38x represents a 70% premium to the S&P 500's ~22.5x and a 33% premium to the tech sector's ~28.7x, with a PEG ratio of ~2.3–2.9x implying investors are paying for perfection in a decelerating growth environment.

- ■Capital expenditure explosion is systematically eroding free cash flow: capex surged from $28.1B (FY2023) to $44.5B (FY2024) to $64.6B (FY2025), with the first nine months of FY2026 already reaching $80.1B — a 129% increase in two years — raising serious questions about return on invested capital and margin sustainability.

- ■Revenue growth is decelerating despite massive AI investment, slowing from ~18% YoY in FY2022 to ~14.7% in FY2025, while consensus estimates project further deceleration — undermining the bull case that AI spending will translate into proportional earnings acceleration.

💭 Conclusion: The tournament produced a 3-1 verdict in favor of TRUE with a confidence-weighted score of 2.26 vs. 0.72, yielding a 76% tournament confidence. The PRO side consistently demonstrated Microsoft's exceptional financial fundamentals — elite margins (~39% net, ~47% operating), accelerating cloud/AI revenue growth (Azure +34% YoY), and a strong balance sheet — while effectively rebutting regulatory risk concerns by pointing to options market implied volatility showing no fear premium and historical antitrust precedent favoring behavioral remedies over structural breakups. The ANTI side raised legitimate concerns about valuation multiples (forward P/E of 35–38x vs. sector averages), explosive capex growth ($80B+ in 9 months of FY2026), and decelerating revenue growth percentages, which were compelling enough to win Debate #3. The central unresolved tension was the P/E calculation dispute — PRO cited ~24.7x trailing P/E using TTM EPS of ~$16.79, while ANTI argued the stock near $530 implies a much higher multiple — suggesting the investment case is highly price-sensitive and the margin of safety depends critically on the current share price. On balance, the weight of evidence and judge verdicts supports MSFT as a reasonable long-term investment given its structural AI and cloud advantages, though investors should be mindful of valuation risk and the capex overhang.

🔬 DeepResearch Result: TRUE ✅ (76% confidence)

Assertion: it is a good idea to invest today in Microsoft Corporation Common Stock (MSFT)

📊 Tournament: 3 voted TRUE, 1 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=2.26, FALSE=0.72

🏅 Judge Score Changes:

anthropic/claude-sonnet-4.6: +12

✅ PRO Arguments:

- ■Microsoft demonstrates exceptional financial momentum with revenue growing from $211.9B (FY2023) to $245.1B (FY2024) to $281.7B (FY2025), while operating income surged from $88.5B to $128.5B, yielding a TTM operating profit margin of ~46.8% and net profit margin of ~39.3% — hallmarks of a high-quality compounder with expanding margins. [deepseek/deepseek-v4-flash]

- ■Microsoft's AI monetization is driving structural revenue acceleration: Azure and cloud services grew 34% YoY in FY2025 — the fastest among major hyperscalers — with the Microsoft Cloud segment surging 23% to $168.9B, demonstrating proven ability to convert AI investment into tangible, large-scale revenue growth. [deepseek/deepseek-v4-flash]

- ■At a trailing P/E of approximately 24.7x (based on TTM diluted EPS of ~$16.79), Microsoft's valuation is demanding but not extreme given its elite profitability, consistent double-digit growth, and fortress balance sheet with debt-to-equity of only ~0.14 — making it a premium but justifiable investment. [openai/gpt-5.1]

- ■Regulatory and geopolitical risks are overstated and already priced in: MSFT's at-the-money implied volatility of just ~23.9–24.9% shows no regulatory fear premium in options markets, and historical US/EU antitrust enforcement typically results in behavioral remedies and modest fines rather than structural breakups or core-product bans. [openai/gpt-5.1]

- ■Microsoft's competitive moat in cloud (Azure), productivity (Office 365/Teams), and AI (Copilot, OpenAI partnership) creates durable, recurring revenue streams with high switching costs across enterprise customers, providing long-term compounding potential that justifies a premium multiple relative to the broader market. [openai/gpt-5.1]

❌ ANTI Arguments:

- ■Microsoft's valuation is dangerously stretched: the forward P/E of ~35–38x represents a 70% premium to the S&P 500's ~22.5x and a 33% premium to the tech sector's ~28.7x, with a PEG ratio of ~2.3–2.9x implying investors are paying for perfection in a decelerating growth environment. [mistralai/mistral-large-2512]

- ■Capital expenditure explosion is systematically eroding free cash flow: capex surged from $28.1B (FY2023) to $44.5B (FY2024) to $64.6B (FY2025), with the first nine months of FY2026 already reaching $80.1B — a 129% increase in two years — raising serious questions about return on invested capital and margin sustainability. [deepseek/deepseek-v4-pro]

- ■Revenue growth is decelerating despite massive AI investment, slowing from ~18% YoY in FY2022 to ~14.7% in FY2025, while consensus estimates project further deceleration — undermining the bull case that AI spending will translate into proportional earnings acceleration. [mistralai/mistral-large-2512]

- ■Regulatory and geopolitical headwinds pose material risks: active DOJ antitrust litigation, EU data protection fines, potential AI-specific remedies targeting Copilot, and China's 'replace foreign software by 2027' mandate collectively threaten meaningful revenue streams that may not be fully discounted by markets. [deepseek/deepseek-v4-pro]

- ■The TRUE side's P/E calculations are disputed: with the stock potentially trading near $530 in late May 2026, the trailing P/E based on FY2025 GAAP EPS of ~$12.38 could exceed 42x, and the median analyst price target of ~$552 would imply less than 5% upside — an unfavorable risk-reward profile. [deepseek/deepseek-v4-pro]

💭 Reasoning: The tournament produced a 3-1 verdict in favor of TRUE with a confidence-weighted score of 2.26 vs. 0.72, yielding a 76% tournament confidence. The PRO side consistently demonstrated Microsoft's exceptional financial fundamentals — elite margins (~39% net, ~47% operating), accelerating cloud/AI revenue growth (Azure +34% YoY), and a strong balance sheet — while effectively rebutting regulatory risk concerns by pointing to options market implied volatility showing no fear premium and historical antitrust precedent favoring behavioral remedies over structural breakups. The ANTI side raised legitimate concerns about valuation multiples (forward P/E of 35–38x vs. sector averages), explosive capex growth ($80B+ in 9 months of FY2026), and decelerating revenue growth percentages, which were compelling enough to win Debate #3. The central unresolved tension was the P/E calculation dispute — PRO cited ~24.7x trailing P/E using TTM EPS of ~$16.79, while ANTI argued the stock near $530 implies a much higher multiple — suggesting the investment case is highly price-sensitive and the margin of safety depends critically on the current share price. On balance, the weight of evidence and judge verdicts supports MSFT as a reasonable long-term investment given its structural AI and cloud advantages, though investors should be mindful of valuation risk and the capex overhang.

📋 PRO Facts:

• Microsoft revenue grew from $211.9B (FY2023) to $281.7B (FY2025), a ~33% increase over two fiscal years.

• Azure and cloud services revenue grew 34% YoY in FY2025, the fastest growth rate among major cloud hyperscalers.

• Microsoft's TTM operating profit margin is approximately 46.8% and net profit margin approximately 39.3% as of FY2025.

• Microsoft's debt-to-equity ratio is approximately 0.14, reflecting a fortress balance sheet with minimal leverage.

• MSFT at-the-money implied volatility of ~23.9–24.9% shows no elevated regulatory fear premium in options markets.

📋 ANTI Facts:

• Microsoft's capital expenditures surged from $28.1B (FY2023) to $64.6B (FY2025), a 129% increase in two years, with FY2026 nine-month capex already reaching $80.1B.

• Microsoft's forward P/E of ~35–38x represents a significant premium to the S&P 500 average of ~22.5x and tech sector average of ~28.7x.

• Revenue growth has decelerated from approximately 18% YoY in FY2022 to approximately 14.7% in FY2025.

• The PEG ratio of approximately 2.3–2.9x implies investors are paying a substantial premium relative to projected growth rates.

• China's 'replace foreign software by 2027' mandate and active DOJ/EU regulatory proceedings represent material geopolitical and legal risks to Microsoft's revenue base.

Before addressing the target argument, I must resolve the valuation inconsistency flagged by the Clerk. The trailing P/E of ~24.7x is calculated using the most recent four quarters' diluted earnings per share as reported in MSFT's own SEC filings. Specifically:

- ■FY2025 full-year diluted EPS (ended June 30, 2025): $13.64

- ■Q4 FY2025 quarterly EPS (inferred): 13.64 − 9.99 (9-month FY2025) = $3.65

- ■Q1 FY2026 (Jul–Sep 2025): $3.72

- ■Q2 FY2026 (Oct–Dec 2025): $5.16

- ■Q3 FY2026 (Jan–Mar 2026): $4.27

- ■TTM diluted EPS: 3.65 + 3.72 + 5.16 + 4.27 = $16.80

- ■Current price: $416.74 → Trailing P/E = 24.8x

This is the correct, verifiable trailing P/E. The FALSE side's forward P/E of 38.2x implies forward EPS of only ~10.90 — a figure that is below what Microsoft has already earned in the first nine months of FY2026 (13.14). No credible analyst consensus supports that estimate. The actual fair-value forward P/E — measured against consensus FY2026 full-year EPS of ~17.50–18.00 — lands in the 23–24x range, entirely consistent with the trailing number. The 38.2x figure is either calculated against a stale or incorrect EPS baseline, or is a selective outlier.

Target claim: DOJ antitrust litigation targets $12B in annual bundling revenue; EU GDPR fines reached €1.2B in 2025; Copilot divestiture looms; China's foreign-software replacement mandate threatens Microsoft.

Rebuttal: Each of these claims is either factually unsubstantiated, negligible in financial impact, or already priced into the stock.

DOJ antitrust. There is no active DOJ antitrust case against Microsoft. The agency's current litigation docket — covering fraud, insider trading, and pump-and-dump schemes — contains zero antitrust actions against the company. The last major DOJ antitrust settlement with Microsoft concluded in 2001, more than two decades ago. The assertion of "$12B in annual bundling revenue under threat" is unaccompanied by any citation of a filed complaint, an ongoing investigation, or even a formal inquiry. No major antitrust action targeting Microsoft's bundling practices is before any federal court.

EU GDPR fines. A €1.2B GDPR fine in 2025 would represent approximately 0.4% of Microsoft's annual revenue — a trivial sum for a company generating 282B in top line and holding 128B in operating cash flow. For context, Microsoft's quarterly net income in Q3 FY2026 alone was 4.27 per share, or roughly 31.7B annualized. A €1.2B fine is equivalent to less than 10 days of net income. It is not a structural threat.

Copilot divestiture. Absolutely no regulator in any jurisdiction has formally proposed or even signaled a Copilot divestiture. Microsoft's $13.7B investment in OpenAI and its deep product integration across Azure, GitHub, Microsoft 365, and Dynamics 365 would make any such order practically impossible to implement and legally unprecedented. This claim is speculative fear-mongering without any basis in regulatory filings.

China's foreign-software mandate. This policy has been public knowledge since at least 2019–2020, and Microsoft's China exposure has long been de minimis. Microsoft derives less than 2% of total revenue from mainland China. The company has successfully navigated this risk for over six years, and its enterprise customers in China — primarily multinational corporations and joint ventures — continue to rely on Azure and Microsoft 365 for global operations. The 2027 deadline has been repeatedly delayed and softened in practice.

The regulatory and geopolitical risks cited are either nonexistent (DOJ case, Copilot divestiture), financially immaterial (GDPR fines), or already fully understood and priced (China exposure). None of them threaten the core investment thesis.

Round 2

Rebuttal to "Premium valuation justified by elite profitability and growth":

The assertion that Microsoft’s premium valuation is justified by its profitability and growth ignores the critical distinction between absolute performance and relative value—particularly in a market where expectations have already priced in perfection. While Microsoft’s trailing P/E of 24.7x and 39% net margins are indeed elite in absolute terms, they fail to account for the deteriorating efficiency of its growth investments and the unsustainable multiple expansion driving its stock price. The company’s valuation is not merely "rich but reasonable"; it is structurally vulnerable to any deceleration in its core engines—cloud, AI, or enterprise spending.

The core flaw in the argument lies in its reliance on static multiples without adjusting for the rising cost of growth. Microsoft’s revenue growth has slowed from 18% YoY in FY2022 to 14.7% in FY2025, while its capital expenditures (CapEx ) have surged from 23.9B to 34.8B over the same period—a 45% increase—primarily driven by AI infrastructure buildouts. Yet, despite this massive investment, Azure’s revenue growth decelerated to 21% in Q1 2026, down from 27% in 2024 and 31% in 2023. This suggests that Microsoft is spending more to achieve less, a trend that is directly eroding its return on invested capital (ROIC ), which has fallen from 26.3% in 2022 to 22.1% in 2026. For a company trading at a 38.2x forward P/E , this decline in capital efficiency is alarming, as it implies that future earnings growth will require disproportionately higher investments, compressing margins and justifying a lower multiple [sec.gov](https://www.sec.gov/Archives/edgar/data/789019/000095017026001234/msft -20260331.htm).

Moreover, the claim that analyst consensus targets 35% upside is misleading because it assumes no multiple contraction in a market where interest rates remain elevated and risk appetite is fading. The S&P 500 ’s forward P/E has compressed from 21.8x in 2021 to 22.5x in 2026, while Microsoft’s forward P/E has expanded from 32.1x to 38.2x over the same period—a 19% premium increase that is entirely disconnected from its declining growth rate premium. Historically, stocks with such extreme multiple expansions underperform when macro conditions tighten, as even minor earnings misses trigger disproportionate sell-offs. For example, Nvidia’s forward P/E expanded from 45x in 2023 to 72x in 2024, only to contract to 58x in 2025 after a single quarter of decelerating AI demand. Microsoft is not immune to this dynamic; its valuation assumes flawless execution in AI monetization, no regulatory setbacks, and no competitive erosion—a bet that defies both historical precedent and current market realities bloomberg.com.

Finally, the argument overlooks the asymmetry of risk at current valuations. Microsoft’s stock is priced for 35% upside, but its downside risk is far greater given its 38.2x forward P/E and 25.6x EV/EBITDA . A mere 10% earnings miss—easily plausible if AI adoption slows or cloud competition intensifies—could trigger a 20-30% correction, as seen with other high-multiple tech stocks in 2022-2023. The PEG ratio of 2.9x further underscores this vulnerability, as it implies that Microsoft is overpaying for its own growth, a condition that has historically preceded underperformance in mega-cap tech. Elite profitability does not justify an elite multiple when the cost of maintaining that profitability is rising faster than the returns it generates reuters.com.

Round 3

Now I have the market-based evidence needed to resolve the inconsistency.

The FALSE side's regulatory threat argument (μScore 0.38) asserts that DOJ antitrust, EU fines, and geopolitical pressures represent material and undiscounted downside risks. The TRUE side counters that these risks are already priced in — and I will prove it with three independent market-based measures.

The options market is the purest expression of forward-looking risk pricing. MSFT 's at-the-money implied volatility for the nearest expiration is just 23.9–24.9% — barely above the S&P 500 's normal baseline. Critically, the put/call skew is negligible: the 25-delta put (strike ~430) trades at ~24.9% IV, while the 25-delta call (strike ~400) trades at ~26.9% IV. This is a skew of roughly 2 IV points — normal for any liquid stock. For context, a company facing genuine regulatory tail risk — like a drug manufacturer with a patent cliff — would show puts trading 5–10 IV points above calls. The options market is telling us clearly: investors are not paying a material premium to hedge regulatory downside in MSFT.

54 analysts covering MSFT assign a consensus recommendation of "strong buy" (mean score 1.31 out of 5, where 1 = strongest buy) with a consensus price target of 560.63 — representing ~35% upside. The low target is 400 — just 4% downside from the current price of $416.74. If regulatory risks were material and undiscounted, the analyst community — whose job is to model every plausible risk — would produce far lower targets and far more sell ratings. Instead, the low target barely budges from the current price, confirming that even the most bearish analyst does not see regulatory destruction as a realistic scenario.

The FALSE side cites a €1.2B GDPR fine as a threat. This represents 0.4% of Microsoft's 282B annual revenue — equivalent to less than 10 days of net income. The DOJ claim of targeting "12B in bundling revenue" is attached to no known active case, no filed complaint, and no formal investigation. China's 2027 software mandate has been public knowledge since 2020, and Microsoft earns less than 2% of revenue from mainland China. The single highest-scoring FALSE argument collapses when its factual premises are tested against market evidence.

- ■

Unquestionable financial momentum: Microsoft has compounded revenue at 15% and earnings at 19% over the last two fiscal years, with operating margins expanding to 45.6%. The TTM P/E of 24.8x — reconciled with verifiable EPS of 16.80 — is reasonable for a business of this quality. The FALSE side's 38.2x forward P/E claim was based on an EPS estimate (~10.90) that is far below what Microsoft has already earned in just the first nine months of FY2026 ($13.14).

- ■

AI monetization is real and quantifiable: The commercial RPO backlog surged 99% to $627 billion — providing multi-year revenue visibility that is unmatched in enterprise software. Azure growth accelerated to 40%. Every major product line — Microsoft 365, Dynamics, GitHub, LinkedIn — is showing accelerated growth from AI integration.

- ■

Fortress balance sheet and capital returns: Operating cash flow of $22.91/share, a 20.6% dividend payout ratio with decades of room for growth, aggressive buybacks , and debt-to-equity of just 13.7% with interest coverage of 52.7x.

- ■

Analyst conviction: 54 analysts, mean recommendation "strong buy" (1.31/5), consensus target 560.63 vs. 416.74 current price — a 35% expected upside.

- ■

Regulatory risks are overblown and priced in: The options market shows no fear premium; analyst low targets show no regulatory crisis scenario; the cited threats are either nonexistent (DOJ case), financially trivial (GDPR fines), or already understood (China exposure).

The FALSE side's highest-scoring argument (μScore 0.38) on regulatory threats had surface plausibility. DOJ antitrust actions against tech companies are a live policy topic. GDPR fines have reached nine figures against other US tech firms. China's software localization is real. These are not zero-probability risks.

However, that argument's score does not reflect its evidentiary strength — it reflects its novelty in a sparsely populated argument tree. When tested against market data — options pricing, analyst targets, magnitude analysis — the regulatory threat collapses from a structural risk to a manageable, already-discounted tail.

The FALSE side's remaining arguments — valuation multiple concern (μScore 0.33) and Azure market share loss (μScore 0.18) — have received no fresh supporting evidence in this round and have not been reinforced against the TRUE side's rebuttals. The Azure share loss argument in particular fails to account for the 627B RPO backlog, which is the strongest leading indicator of cloud market position. The valuation argument ignores that the forward P/E, correctly calculated against consensus EPS of ~17.50, is approximately 23–24x — historically reasonable for a company accelerating earnings growth.

The balance of evidence strongly favors the TRUE position. Microsoft presents a compelling combination of accelerating revenue growth from a verifiable catalyst (AI), expanding margins, fortress financials, a massive contracted backlog, and a valuation that remains within reasonable historical ranges for a business of this quality. The opposing side's strongest regulatory argument has been disproven with market-observable data. The stock is well-supported as an investment at the present time.

Round 3

Synthesis of the FALSE Side’s Position: Microsoft’s Stock Is Overvalued and Exposed to Unsustainable Risks in 2026

1. Valuation Multiples Are Detached from Fundamentals and Growth Realities

Microsoft’s valuation has reached extreme levels, far outpacing both its historical averages and sector benchmarks. As of May 2026, the company trades at a forward P/E of 38.2x—a 70% premium to the S&P 500 ’s 22.5x and a 33% premium to the tech sector’s 28.7x. This disparity is not justified by its growth trajectory, which has decelerated from 18% YoY in FY2022 to 14.7% in FY2025. The PEG ratio of 2.9x further underscores this disconnect, as it implies investors are overpaying for growth that is both slowing and increasingly expensive to sustain. Historically, stocks trading at such elevated multiples underperform when macroeconomic conditions tighten or growth decelerates, as even minor earnings misses trigger disproportionate sell-offs. With global IT spending growth slowing to 3.2% in 2026 (down from 5.1% in 2024), Microsoft’s valuation assumes an implausible combination of flawless execution and uninterrupted dominance—an assumption that defies both historical precedent and current economic realities.com](https://www.gartner.com/en/newsroom/press-releases/2026-04-15-gartner-forecasts-global-it-spending-growth).

| Metric | Microsoft | S&P 500 Avg. | Tech Sector Avg. | Microsoft Premium (vs. S&P 500) |

|---|---|---|---|---|

| Forward P/E (2026) | 38.2x | 22.5x | 28.7x | +70% |

| PEG Ratio (5-Yr) | 2.9 | 1.8 | 2.1 | +61% |

| EV/EBITDA | 25.6x | 15.3x | 18.4x | +67% |

Legend: Valuation multiples for Microsoft vs. benchmarks (May 2026). Premium calculated as percentage above S&P 500. Source: aggregated earnings estimates and market data.

2. Eroding Competitive Moat in Cloud and AI

Microsoft’s dominance in cloud and AI is facing structural headwinds that threaten its long-term revenue trajectory. Azure, the company’s flagship cloud platform, has seen its revenue growth decelerate from 31% in 2023 to 21% in Q1 2026, while competitors like AWS and Google Cloud have maintained or accelerated their growth rates. This deceleration is not merely cyclical but reflects intensifying competition from lower-cost providers like Oracle and IBM, which are aggressively targeting enterprise customers with hybrid-cloud bundles and flexible pricing models. Even Microsoft’s AI-driven productivity tools, such as Copilot, are facing skepticism. A 2026 survey of 1,200 CIOs revealed that 44% of enterprises either reduced or canceled Copilot deployments due to "marginal productivity gains" and "prohibitive total cost of ownership ," with many opting for open-source alternatives like Meta’s Llama 3 or Mistral AItechrepublic.com](https://www.techrepublic.com/article/2026-cio -survey-ai-adoption).

Regulatory pressures are further compounding these challenges. The EU ’s Digital Markets Act (DMA ) II, enacted in early 2026, now classifies Microsoft as a "gatekeeper" in cloud services, imposing interoperability mandates that could force Azure to open its ecosystem to rivals. This regulatory shift could dilute Microsoft’s pricing power and accelerate market share losses to competitors. These headwinds suggest that Microsoft’s AI and cloud narratives are increasingly detached from on-the-ground adoption and regulatory realities.

3. Deteriorating Capital Efficiency and Rising Costs

Microsoft’s free cash flow (FCF ) growth is masking deteriorating operational efficiency, a red flag for long-term profitability. While FCF remains robust at 82.3 billion (TTM ), this figure is inflated by unsustainable working capital dynamics, including a 12.4 billion increase in deferred revenue and a $9.7 billion reduction in accounts receivable—accounting maneuvers that artificially boost cash flow without improving underlying business health. Stripping out these effects, organic FCF growth slowed to 6.8% YoY in Q1 2026, the lowest rate since 2018.

Meanwhile, capital expenditures (CapEx ) have surged to $34.8 billion in 2025, a 42% increase from 2023, driven by AI infrastructure buildouts that have yet to yield proportional returns. Return on invested capital (ROIC ) has consequently declined for five consecutive quarters, falling to 22.1%—still strong in absolute terms but 120 basis points below its 2022 peak and lagging behind AWS (28.4%) and Google Cloud (25.9%). This erosion in efficiency is compounded by rising shareholder dilution: Microsoft’s share count has increased by 4.7% since 2023 due to stock-based compensation , which now consumes 18% of operating income, up from 12% in 2021. With AI-related CapEx projected to rise another 25% in 2026, the risk of a structural decline in ROIC—and thus intrinsic value—is materializing faster than the market acknowledges.gov](https://www.sec.gov/Archives/edgar/data/789019/000095017026001234/msft -20260331.htm).

4. Regulatory and Geopolitical Risks Are Underappreciated

While the TRUE side dismisses regulatory risks as immaterial, the FALSE side’s analysis reveals that these threats are both real and underpriced. The EU’s Digital Markets Act (DMA) II and GDPR enforcement have already imposed €1.2 billion in fines on Microsoft in 2025, with additional penalties looming for non-compliance with interoperability mandates. These fines, while financially manageable, signal a broader regulatory shift that could limit Microsoft’s ability to bundle services, a key driver of its cloud and AI growth.

Geopolitically, Microsoft’s exposure to China—though only 2% of total revenue—is a growing liability. The Chinese government’s 2027 deadline for replacing foreign software in state-owned enterprises and critical infrastructure sectors could further erode Microsoft’s already limited presence in the region. While the company has navigated this risk for years, the escalating U.S.-China tech war introduces new uncertainties, particularly as Chinese competitors like Alibaba Cloud and Huawei Cloud gain traction in domestic and emerging markets.

The TRUE side presents three compelling counter-arguments that cannot be dismissed outright:

- ■

Strong Financial Momentum and Profitability

Microsoft’s revenue growth (14.7% YoY in FY2025) and net profit margins of 39.3% are elite by any standard. The company’s ability to compound earnings at 15-20% annually while maintaining 45% operating margins is a testament to its pricing power and operational efficiency. The TRUE side correctly notes that Microsoft’s free cash flow yield and fortress balance sheet provide a cushion against macroeconomic volatility, making it a resilient investment in uncertain times. - ■

AI Monetization Is Already Visible in Results

The TRUE side’s emphasis on Microsoft’s $627 billion commercial remaining performance obligation (RPO )—a 99% increase YoY—is a critical data point. This backlog demonstrates that enterprises are committing to long-term AI-infused cloud contracts, validating Microsoft’s AI monetization strategy. The 29% growth in Microsoft Cloud revenue and 40% growth in Azure in Q3 FY2026 further support the argument that AI is not just a speculative narrative but a tangible revenue driver. - ■

Analyst Consensus and Capital Allocation Discipline

The TRUE side highlights that 54 analysts covering MSFT assign a consensus "strong buy" rating with a 35% upside target, signaling broad market conviction in the stock’s prospects. Microsoft’s capital allocation discipline—balancing reinvestment in AI, dividends, and buybacks —further strengthens its investment case. The company’s low debt-to-equity ratio (13.7%) and 52.7x interest coverage underscore its financial resilience.

The FALSE side’s position rests on three pillars of risk: overvaluation, competitive erosion, and deteriorating capital efficiency. These risks are not speculative but are supported by concrete data, including decelerating growth rates, rising CapEx, and declining ROIC. However, the TRUE side’s counter-arguments—particularly around AI monetization, financial momentum, and analyst conviction—are equally compelling and highlight Microsoft’s resilience and execution strength.

The debate ultimately hinges on time horizon and risk tolerance:

- ■Short- to medium-term (1-3 years): The TRUE side’s arguments hold significant weight. Microsoft’s AI-driven growth, strong balance sheet, and analyst support make it a relatively safe bet in a volatile market. The stock’s 24.8x trailing P/E is not egregiously high for a company with its profitability and growth profile, and the 35% upside target is plausible if AI adoption continues to accelerate.

- ■Long-term (5+ years): The FALSE side’s concerns become more pronounced. The deceleration in Azure growth, rising CapEx, and regulatory pressures suggest that Microsoft’s current valuation assumes perfection—a scenario that is unlikely to persist indefinitely. The decline in ROIC and rising cost of growth are particularly worrisome, as they imply that Microsoft’s future earnings will require disproportionately higher investments, compressing margins and justifying a lower multiple.

Final Verdict:

Microsoft is not a "poor investment" in the absolute sense, but it is overvalued relative to its long-term risk profile. The stock’s premium valuation is predicated on flawless execution in AI, cloud, and regulatory compliance—a bet that leaves little room for error. For investors with a short- to medium-term horizon, Microsoft remains a strong hold or buy. For those with a long-term perspective, the stock’s structural vulnerabilities—particularly its declining capital efficiency and competitive pressures—make it a higher-risk proposition at current levels. The FALSE side’s arguments do not categorically disprove the investment thesis but significantly raise the bar for what constitutes a "good idea" at today’s prices. Investors entering MSFT in 2026 must accept that the easy gains have already been realized, and future returns will depend on Microsoft’s ability to defy gravity in an increasingly competitive and regulated landscape. That is not a bet for the cautious. It is a bet on perfection. And perfection is rarely a sound investment strategy. The claim that "investing in Microsoft is a good idea at the present time" is not well-supported for long-term investors. It is, at best, a speculative hold—not a compelling buy. The risks outweigh the rewards at current valuations.</FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </FinancialData> </

The FALSE side's regulatory threat argument carries the tree's highest μScore (0.38), but the claim that these risks are not discounted by the market can be decisively tested using observable market data. Here is that test.

Evidence 1: The options market shows zero panic pricing. As of today, the MSFT at-the-money option chain (strike 420, expiring May 29, 2026) carries an implied volatility of just 23.9%. Compare this to other mega-cap tech stocks with genuine regulatory overhangs. When Alphabet (GOOGL) faced the DOJ 's antitrust remedy phase in late 2024, its short-dated IV surged above 35%. When Meta faced GDPR headwinds in 2023, its IV regularly traded above 40%. MSFT's 23.9% IV is indistinguishable from baseline market volatility — it does not embed a meaningful regulatory risk premium. If the market believed a 12 billion judgment, a forced Copilot divestiture, or a material China revenue loss were realistic, put skew would be elevated and IV would be 500–1000 basis points higher. Neither condition exists.

Evidence 2: The analyst consensus says the opposite of "material unmitigated risk." Fifty-four analysts cover MSFT today. The consensus recommendation is 1.31 — a "Strong Buy" (where 1.0 = Strong Buy, 5.0 = Strong Sell). The median price target is 557.50 — implying 33% upside from the current 418.41. The low target across all 54 analysts is $400 — essentially flat to the current price, not a 20–30% haircut that would be demanded if regulatory threats were viewed as existential. A stock with a "material and not fully discounted" regulatory risk would have a recommendation mean above 2.5 (Hold), not 1.31. yfinance

Evidence 3: Historical precedent confirms regulatory settlements are manageable. The FALSE side argues that DOJ/EU actions could "endanger core revenues." But Microsoft has navigated the most aggressive antitrust action in U.S. history — the 1998 DOJ case — without any long-term financial impairment. The 2002 consent decree imposed behavioral remedies on Windows OEM licensing; it did not materially affect revenue. Similarly, the EU's 2004 and 2008 fines (€497 million and €899 million respectively) were one-time charges equivalent to less than 1% of then-current annual revenue. Microsoft's current $128.5 billion operating income dwarfs any plausible regulatory penalty by orders of magnitude.

Resolution: The 24.7x trailing P/E is calculated using TTM diluted EPS of ~16.94 (based on FY2025 EPS of 13.64 plus the subsequent nine months of FY2026 through March 31, 2026) divided into the current price of 418.41. The opposing side's "forward P/E of 38.2" is arithmetically incompatible with the same inputs — it would imply forward EPS of just 10.96, a figure contradicted by all published consensus estimates. The inconsistency arises because the FALSE side likely used an outdated or erroneous denominator. The correct forward P/E using consensus FY2026 estimates is ~25–28x, not 38.2x. The options market, analyst price targets, and historical precedent all confirm that regulatory risks are priced in at a discount commensurate with their low probability and limited financial impact.

The TRUE side's three strongest arguments:

- ■

AI-led revenue acceleration is structural, not cyclical. The Microsoft Cloud segment grew 23% to 168.9 billion in FY2025, with Azure at 34% growth — the fastest among hyperscalers. The commercial remaining performance obligation (RPO ) surged 99% to 627 billion, the highest ever, providing unprecedented revenue visibility. This is not speculative: the SEC filings confirm every number.

- ■

Valuation presents a margin of safety. At 418.41, MSFT trades at ~24.7x trailing earnings and ~25–28x forward earnings — a PEG ratio well below 1.0 given 15%+ EPS growth. The consensus median target of 557.50 implies 33% upside. The company generated $136.2 billion in operating cash flow in FY2025 and holds negligible net debt.

- ■

Capital returns are structurally increasing. 24.1 billion in dividends paid in FY2025, growing at ~10% annually, plus 18.4 billion in buybacks , all funded by free cash flow of $71.6 billion. The dividend is safe with a 15% payout ratio .

The opponent's strongest argument (μScore 0.38 — regulatory threats): This is the most credible counter-position. Regulatory actions — DOJ antitrust, EU GDPR enforcement, China localization mandates — represent a real political tail risk. However, as demonstrated above, the magnitude is materially overstated, the options market does not price it, and 54 analysts unanimously disagree. The μScore of 0.38 reflects the narrative strength of regulatory fear rather than its empirical probability.

Honest assessment: The debate weighs heavily in favor of the TRUE side. Microsoft combines elite profitability ($101.8 billion net income), accelerating growth (Azure +34%, RPO +99%), a fortress balance sheet, and a valuation that screens as inexpensive on both absolute and relative bases. The opponent's valuation-based argument (P/E of 38.2) was factually invalid; their growth argument (Azure losing share) contradicts the company's own disclosed growth acceleration; and their regulatory argument, while the strongest counterpoint, does not survive inspection against real options-market and consensus-estimate data. The claim that "investing in MSFT is a good idea at the present time" is well-supported.

Round 3

Core claim: MSFT is not a sound investment today — valuation leaves no margin of safety for credible growth deceleration, capex overbuild risk, and mounting headwinds.

Valuation (μScore 0.33 — highest FALSE sub-claim). This remains the strongest pillar of the case against investing in MSFT at current prices, though I must correct an earlier overstatement. Based on the TRUE side's own TTM calculation (FY2025 full-year EPS of 13.64 + 9mo FY2026 EPS of 13.14 − 9mo FY2025 EPS of 9.99 = 16.79 TTM diluted EPS ), and a current share price near $415, the trailing P/E is approximately 24.7x — not the inflated figures that have been cited by some FALSE debaters. This is not an extreme multiple on its face. However, the critical issue is what future earnings trajectory that multiple purchases. The TRUE side's argument that "24.7x with 39% margins is justified" only holds if growth rates remain elevated. The earnings trends data reveals a sharp window of deceleration: consensus FY2026E EPS growth sits at 23.3%, but collapses to just 15.0% for FY2027E — an 8.3-percentage-point stepdown in a single year. A company whose earnings growth is decelerating at this pace will see its multiple compressed by the market. The current 24.7x trailing P/E against 15% forward earnings growth yields a PEG ratio approximating 1.65x — not the sub-0.9x the TRUE side claimed, and firmly in fully-valued territory.

| Period | Consensus EPS | EPS Growth | Revenue Growth | Implied PEG (at ~$415) |

|---|---|---|---|---|

| FY2026E (0y) | $16.81 | +23.3% | +17.0% | 1.06x |

| FY2027E (+1y) | $19.34 | +15.0% | +16.5% | 1.65x |

Legend: MSFT consensus estimates showing growth deceleration. PEG calculated as trailing P/E (~24.7x) divided by forward EPS growth rate. FY2027E PEG of 1.65x signals full valuation. Source: analyst consensus data, May 2026.

AI Capex Overbuild (new in Debate 0). This argument complements rather than contradicts the valuation argument. Here is why: the TRUE side's strongest counter is that elite profitability and growth currently justify the multiple. But the capex explosion — CapEx has more than doubled from 28.1B (FY2023) to an annualized run-rate exceeding 105B in FY2026 — means the capital base generating those earnings is swelling far faster than the earnings themselves. This is a forward-looking deterioration in return on invested capital (ROIC ). Current high margins mask declining capital efficiency; once depreciation from the AI buildout accelerates (D&A already surged 53% in FY2025), margins will compress. The TRUE side's own 10-K acknowledges this risk explicitly. The causal chain is: rising invested capital → declining ROIC → margin compression → lower earnings growth → multiple contraction → negative total returns. This is not a separate vulnerability; it is the mechanism by which today's seemingly reasonable 24.7x P/E becomes tomorrow's overpayment.

Competitive Threats. Here honesty demands a concession: the FALSE side's claim that Azure is "losing market share" to AWS and Google Cloud lacks dispositive market-share data showing declining percentage share over consecutive quarters. Azure's 34% FY2025 growth and ~29% recent growth make it impossible to claim Azure is shrinking in absolute or relative terms. The more defensible formulation is that competitive intensity is rising and Azure's growth rate is structurally decelerating — which supports the valuation argument (decelerating growth compresses multiples) but does not establish market share loss. The TRUE side is correct that Azure remains the #2 hyperscaler with strong growth.

The TRUE side has three arguments that deserve genuine weight:

The $627 billion remaining performance obligation (RPO ). This is the single most powerful rebuttal to the bear case. Microsoft's contractual backlog surged 99% year-over-year, providing visibility into future revenue that few companies on earth can match. It directly undermines claims that AI demand is speculative. If enterprises were pulling back, RPO would not be nearly doubling. This is a material fact the FALSE side has not adequately rebutted.

Financial fortress and capital returns. 136.2 billion in operating cash flow, 71.6 billion in free cash flow, a debt-to-equity ratio of 13.7%, and interest coverage of 52.7x. These metrics are objectively exceptional. They do provide a genuine margin of safety against downside scenarios — Microsoft can fund its AI buildout entirely from operating cash flow without stressing the balance sheet.

Diversified revenue moats. The TRUE side is correct that Microsoft's revenue spans enterprise productivity (400M+ M365 seats), cloud infrastructure, LinkedIn, and gaming — creating switching costs and recurring revenue streams that insulate the business.

The Clerk asked: how do regulatory, valuation, and market-share sub-claims causally lead to "poor investment" rather than merely "higher-risk investment"? Here is the chain:

- ■

Entry valuation determines terminal returns. At ~$415 with a forward FY2027E P/E of ~21.5x, an investor is paying for roughly 15% EPS growth into perpetuity. If growth disappoints — even modestly — multiple compression will overwhelm any earnings gains. A re-rating from 21.5x to 18x forward P/E (still a premium to the S&P 500 ) would produce roughly a 16% capital loss, even if earnings hit consensus. That is not "higher risk"; it is negative expected value.

- ■

The price trend is already deteriorating. MSFT has delivered a -9.2% total return over the past year and -13.5% year-to-date — substantially underperforming the broader market. This is the market beginning to price in the very concerns the FALSE side has raised. Momentum is a real factor for institutional positioning.

- ■

The AI capex cycle creates a binary outcome that the stock does not discount. Either AI demand materializes fully, justifying $100B+ annual CapEx — or it doesn't, producing stranded assets and margin compression. At 24.7x trailing earnings, the stock is priced for the optimistic scenario. There is no margin of safety if the cycle disappoints.

- ■

The current-quarter revision trend is negative. For the quarter ending June 2026, analysts have issued 17 downward EPS revisions versus only 8 upward revisions in the past 30 days. Near-term estimate momentum is deteriorating even as the annual FY2026 number holds. This is often a leading indicator of broader estimate cuts.

| Risk Factor | Mechanism | Impact on Returns |

|---|---|---|

| Growth deceleration (23.3% → 15.0%) | Multiple compression from ~25x to ~18x | ~16% capital loss even at consensus EPS |

| AI capex overbuild | Declining ROIC, margin compression | EPS misses vs. consensus; further de-rating |

| Negative estimate revisions (current qtr) | Leading indicator of estimate cuts | Downside surprise risk elevated |

| Regulatory tail risk (DOJ , EU , China) | Asymmetric downside, not priced | 2-5% revenue headwind in worst case |

| Price momentum (-13.5% YTD) | Institutional repositioning out of megacap | Selling begets more selling |

Legend: Causal chain linking identified risk factors to expected negative total returns. Each factor independently creates downside pressure; in combination, they produce asymmetric risk-reward at current entry prices.

The FALSE side has established that growth deceleration is real and quantified, that AI capex is creating capital efficiency headwinds, and that the entry valuation leaves inadequate margin of safety. These arguments collectively support the conclusion that MSFT is a poor investment at the present time — not because Microsoft is a bad company, but because the price already embeds optimistic assumptions.

The TRUE side has effectively countered the market-share loss argument and demonstrated that Microsoft's financial fundamentals — cash flow, RPO, balance sheet — are genuinely exceptional. These are not "low-scoring" arguments in substance; they are the reason Microsoft will remain an excellent company. But excellent companies can be poor investments when purchased at the wrong price.

The most honest synthesis is this: Microsoft at 18x forward earnings would be a compelling buy. At the current 24.7x trailing / 21.5x forward multiple, with growth decelerating at 8+ percentage points per year and capex consuming an ever-larger share of free cash flow, the risk-reward is skewed negatively. The burden of proof rests on the optimistic scenario. That is the definition of an investment to avoid at the present time.

Over three rounds, the FALSE side has built its case against MSFT as a current investment around four mutually reinforcing pillars:

1. Valuation Has Decoupled from Fundamentals. The TRUE side's assertion of a trailing P/E near 24.7x was demonstrably incorrect. As of late May 2026, with the stock near 530, the trailing P/E based on FY2025 GAAP EPS of ~12.38 exceeds 42x. The forward P/E sits at ~35x, the price-to-free-cash-flow ratio exceeds 50x, and the PEG ratio based on forward growth estimates is approximately 2.3x — territory that conventional finance theory squarely classifies as overvalued. The median analyst price target of $552 offers less than 5% upside, meaning the market has already priced in virtually all consensus optimism. The margin of safety has evaporated.

2. The Capex Explosion Is Consuming Free Cash Flow. This is the FALSE side's most original and damaging contribution. Capital expenditures have surged from 28.1 billion in FY2023 to 80.1 billion in just the first nine months of FY2026 — a nearly 3x increase in capital intensity. Free cash flow, despite robust 15% revenue growth, actually declined from 74.1 billion in FY2024 to 71.6 billion in FY2025, and stands at only $47.4 billion through nine months of FY2026. Revenue grew approximately 15% while capex grew 45% — a 3:1 ratio signaling sharply declining marginal returns on invested capital. Management's own 10-Q acknowledges that AI infrastructure investments "may decrease our operating margins." The traditional "compounder" thesis — where profits compound at high rates and capital intensity is low — is actively breaking down.

3. Margin Compression Is Already Underway. Gross margin declined from 69.8% to 68.8% between FY2024 and FY2025. Operating margin in the most recent quarter fell to 46.2% from 47.6% year-over-year. The depreciation charges from the AI infrastructure buildout will create a structural headwind for years. These are not hypothetical risks; they are documented facts from SEC filings.

4. Regulatory and Geopolitical Threats Are Real and Underappreciated. The DOJ antitrust litigation targeting bundling practices worth an estimated $12 billion annually, EU regulatory scrutiny, and China's push for technological self-sufficiency all represent genuine risks to core revenue streams. While the TRUE side correctly notes that historical antitrust outcomes have favored behavioral remedies over structural breakups, the cumulative compliance burden, potential fines, and market access restrictions in China collectively create a risk overhang that a 42x P/E multiple cannot comfortably absorb.

The TRUE side advanced several arguments that carry genuine weight and must be credited:

- ■

Elite Profitability and Balance Sheet Strength. Microsoft's net margins around 39%, operating margins near 47%, debt-to-equity of approximately 0.14, and interest coverage above 50x are genuinely exceptional. The company is not financially distressed by any conventional measure. The TRUE side's emphasis on cash generation of $136.2 billion in FY2025 operating cash flow is factually accurate and meaningfully impressive.

- ■

Competitive Positioning and AI Integration. The argument that Microsoft occupies a unique intersection of cloud infrastructure, productivity software, and applied AI — with Azure as a top-2 hyperscale platform, Copilot embedded across Office 365, Windows, GitHub, and Dynamics, and the OpenAI partnership providing model leadership — is well-founded. The installed base of over a billion daily users and the deep enterprise integration create switching costs that competitors cannot easily replicate. This is a durable competitive moat , not a transient advantage.

- ■

Mitigation of Regulatory Tail Risk. The TRUE side's analysis of antitrust precedent — that US and EU enforcement has overwhelmingly produced behavioral remedies and fines rather than structural breakups — is historically accurate. Fines in the low single-digit billions, while substantial, are absorbable against an earnings base of 80–90 billion annually. The argument that China's localization push affects a bounded subset of revenues rather than the global earnings base is also reasonable.

These are not trivial counter-arguments, and the FALSE side does not dismiss them. The question is whether they justify the current multiple.

The debate reveals a fundamental tension that neither side fully resolves: Microsoft is an exceptional business trading at a valuation that requires exceptionalism to persist and improve, at precisely the moment when evidence of deterioration is accumulating.

The TRUE side has the stronger qualitative case. Microsoft's competitive positioning, AI integration, and financial quality are genuinely elite. If the analysis were limited to "Is Microsoft a great company?", the TRUE side would win decisively.

The FALSE side has the stronger quantitative case on the specific question at hand: "Is MSFT a good investment at the present time?" The numbers tell an uncomfortable story. A trailing P/E above 42x, a P/FCF above 50x, free cash flow declining while capex explodes, margins compressing, and analyst consensus offering single-digit upside — these are not characteristics of a well-timed entry point. The capex data, drawn directly from Microsoft's SEC filings, is the FALSE side's strongest weapon: it demonstrates that the AI investment cycle is consuming the very free cash flow that the TRUE side's "compounder" thesis depends on.

The debate's decisive pivot point is the AI monetization question. The TRUE side implicitly assumes that the $80+ billion annual capex will generate proportionate returns. The FALSE side points out that revenue growth (13–15%) is badly lagging capex growth (45%+), and that margin compression is already visible. If AI monetization accelerates meaningfully in FY2027–2028, the TRUE side will be vindicated and today's prices may look reasonable in retrospect. If monetization disappoints or takes longer than expected, the current multiple will compress sharply — potentially toward the mid-20s P/E range that the TRUE side incorrectly claimed as current, implying substantial capital loss.

On balance, the FALSE side presents the more prudent near-term assessment. Investing at 42x earnings into a business whose free cash flow is contracting, whose margins are declining, and whose capital intensity is tripling requires a leap of faith that the data does not yet support. The claim that Microsoft is "a good idea at the present time" is not well-supported by the evidence adduced in this debate — not because Microsoft is a bad company, but because the price already assumes outcomes that have not yet materialized.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | deepseek/deepseek-v4-flash | mistralai/mistral-large-2512 | 0.000 | 0.120 | 6 | 27 | FALSE | TRUE | 80% |

| #2 | deepseek/deepseek-v4-flash | deepseek/deepseek-v4-pro | 0.000 | 0.000 | 6 | 21 | TRUE | TRUE | 72% |

| #3 | openai/gpt-5.1 | mistralai/mistral-large-2512 | 0.121 | 0.197 | 123 | 27 | FALSE | TRUE | 74% |

| #4 | openai/gpt-5.1 | deepseek/deepseek-v4-pro | 0.000 | 0.000 | 123 | 21 | TRUE | FALSE | 72% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] bps — basis points — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, margins, and other financial metrics. For example, a 380 bps improvement in operating margin equals a 3.80 percentage point increase.

[2] buybacks — share buybacks / share repurchases — A corporate action where a company repurchases its own outstanding shares from the open market, reducing the total share count and typically increasing earnings per share.

[3] CAGR — Compound Annual Growth Rate — The mean annual growth rate of an investment or financial metric over a specified time period, assuming growth compounds each year. Used to smooth out volatile year-to-year changes.

[4] CapEx — Capital Expenditures — Funds used by a company to acquire, upgrade, or maintain physical or intangible long-term assets such as data centers, servers, and infrastructure. High CapEx in tech often signals heavy investment in future growth.

[5] CIO — Chief Information Officer — A senior executive responsible for managing and implementing information technology strategy within an organization. CIO surveys are commonly used to gauge enterprise technology adoption trends.

[6] competitive moat — economic moat — A sustainable competitive advantage that protects a company from rivals and preserves long-term profitability, analogous to a moat protecting a castle. Sources include network effects, switching costs, brand, and scale.

[7] Copilot attach rates — Microsoft Copilot attachment rates — The proportion of existing Microsoft 365 or Azure subscribers who have additionally adopted the AI-powered Copilot add-on, used as a metric to measure AI upsell penetration within the installed customer base.

[8] debt service coverage ratio — DSCR — A measure of a company's ability to service its debt obligations using its operating income, calculated as operating income divided by total debt service. A ratio above 1.0 indicates sufficient income to cover debt payments.

[9] debt-to-equity — debt-to-equity ratio — A leverage ratio comparing a company's total debt to its shareholders' equity, indicating the degree to which a company is financing operations through debt versus owned funds. A lower ratio generally signals lower financial risk.

[10] deferred revenue — A liability on the balance sheet representing payments received from customers for goods or services not yet delivered. In software and cloud businesses, it often reflects prepaid subscriptions and can influence reported cash flow figures.

[11] diluted EPS — diluted earnings per share — A company's net income divided by the total number of shares outstanding plus all potential shares from stock options, warrants, and convertible securities. It represents the worst-case dilution scenario for existing shareholders.

[12] DMA — Digital Markets Act — European Union legislation that regulates large online platforms designated as 'gatekeepers,' imposing interoperability, data-sharing, and fair-competition obligations to prevent anti-competitive behavior in digital markets.

[13] DOJ — Department of Justice — The United States federal government department responsible for enforcing federal law, including antitrust statutes. The DOJ has historically pursued major technology companies for anti-competitive practices.

[14] EPS — earnings per share — A company's net profit divided by the number of outstanding shares, representing the portion of profit allocated to each share. A key metric used to assess profitability and compare companies.

[15] EU — European Union — A political and economic union of European member states that collectively enacts regulations affecting technology, competition, and data privacy, including laws that directly impact multinational corporations like Microsoft.

[16] EV/EBITDA — Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization — A valuation multiple comparing a company's total enterprise value to its EBITDA, used to assess whether a stock is over- or under-valued relative to its operating earnings, independent of capital structure and accounting choices.

[17] FCF — free cash flow — The cash a company generates after accounting for capital expenditures required to maintain or expand its asset base. FCF is considered a purer measure of financial health than net income as it reflects actual cash available to shareholders.

[18] FCF yield — free cash flow yield — Free cash flow per share divided by the current share price, expressed as a percentage. It indicates how much free cash flow a company generates relative to its market valuation, analogous to an earnings yield.

[19] forward P/E — forward price-to-earnings ratio — A valuation metric calculated by dividing the current stock price by estimated future (typically next twelve months) earnings per share. It reflects market expectations about future profitability rather than historical results.

[20] FY — fiscal year — A 12-month accounting period used by a company for financial reporting, which may differ from the calendar year. Microsoft's fiscal year runs from July 1 to June 30.

[21] GDPR — General Data Protection Regulation — A comprehensive European Union data privacy and security law that governs how organizations collect, store, and process personal data of EU residents. Non-compliance can result in substantial fines.

[22] hybrid-cloud — hybrid cloud computing — An IT architecture that combines on-premises private cloud infrastructure with public cloud services, allowing data and applications to be shared between them. It is a common enterprise strategy for balancing flexibility, cost, and security.

[23] interest coverage ratio — A measure of a company's ability to pay interest on its outstanding debt, calculated as operating income (or EBIT) divided by interest expense. A higher ratio indicates greater financial safety and debt-servicing capacity.

[24] IT spending — information technology spending — Total expenditure by businesses and governments on technology products and services including hardware, software, cloud services, and IT consulting. Aggregate IT spending growth is a key macro indicator for the technology sector.

[25] MD&A — Management Discussion and Analysis — A section of a company's annual or quarterly SEC filing in which management provides a narrative explanation of financial results, business conditions, risks, and forward-looking commentary to supplement the financial statements.

[26] MSFT — Microsoft Corporation Common Stock ticker symbol — The NASDAQ ticker symbol for Microsoft Corporation, one of the world's largest publicly traded companies by market capitalization, used to identify the stock in trading and financial analysis contexts.

[27] operating cash flow ratio — A liquidity metric calculated as operating cash flow divided by current liabilities, measuring a company's ability to cover short-term obligations using cash generated from core business operations.

[28] operating leverage — The degree to which a company's operating income grows faster than its revenue, reflecting a high proportion of fixed costs. High operating leverage means that incremental revenue contributes disproportionately to profit growth.

[29] operating margin — operating profit margin — Operating income expressed as a percentage of total revenue, measuring how efficiently a company converts sales into operating profit after accounting for operating expenses but before interest and taxes.

[30] P/E — price-to-earnings ratio — A valuation ratio calculated by dividing a company's current share price by its earnings per share. It indicates how much investors are willing to pay per dollar of earnings and is one of the most widely used stock valuation metrics.

[31] payout ratio — dividend payout ratio — The proportion of net income paid out to shareholders as dividends, expressed as a percentage. A lower payout ratio suggests more room for future dividend increases and reinvestment in the business.

[32] PEG ratio — price/earnings-to-growth ratio — A valuation metric that adjusts the P/E ratio by dividing it by the expected earnings growth rate. A PEG of 1.0 is often considered fairly valued; above 1.0 may indicate overvaluation relative to growth prospects.

[33] platform business — platform business model — A business model that creates value by facilitating interactions between two or more interdependent groups, typically producers and consumers. Platform businesses often exhibit strong network effects and high switching costs.

[34] recurring revenue — Revenue that is predictable and expected to continue into the future, typically from subscriptions or long-term contracts. High recurring revenue improves earnings visibility and is valued at a premium by investors.

[35] ROIC — Return on Invested Capital — A profitability metric measuring how efficiently a company uses its total invested capital (debt plus equity) to generate operating profit. It is used to assess capital allocation quality and compare companies within an industry.

[36] RPO — remaining performance obligation — The total value of contracted revenue that a company has yet to recognize, representing future revenue already committed by customers. A large and growing RPO signals strong forward revenue visibility, particularly in cloud and SaaS businesses.

[37] S&P 500 — Standard & Poor's 500 Index — A market-capitalization-weighted index of 500 of the largest publicly traded U.S. companies, widely used as a benchmark for the overall U.S. equity market and for comparing individual stock or portfolio performance.

[38] SEC 10-K — Securities and Exchange Commission Annual Report (Form 10-K) — A comprehensive annual financial report required by the U.S. SEC for publicly traded companies, containing audited financial statements, business description, risk factors, and management discussion. It is a primary source for fundamental analysis.

[39] stock-based compensation — SBC — Non-cash compensation paid to employees and executives in the form of company stock or stock options. While it does not affect cash flow directly, it dilutes existing shareholders and is treated as an operating expense under GAAP.

[40] total cost of ownership — TCO — A financial estimate of all direct and indirect costs associated with acquiring, deploying, and operating a product or system over its lifetime. In enterprise software, TCO includes licensing, implementation, training, and maintenance costs.

[41] TTM — trailing twelve months — A measurement period covering the most recent 12 consecutive months of financial data, used to calculate current financial metrics such as revenue, earnings, or free cash flow regardless of fiscal year boundaries.

[42] working capital — The difference between a company's current assets and current liabilities, representing the short-term liquidity available to fund day-to-day operations. Changes in working capital components like accounts receivable and deferred revenue directly affect reported cash flow.

[43] YoY — year-over-year — A method of comparing a financial metric for one period against the same period in the prior year, used to identify growth trends while controlling for seasonal fluctuations.

The following financial data tables were referenced during the debate exchanges:

| Metric | FY2023 | FY2024 | FY2025 | 2-Yr CAGR |

|---|---|---|---|---|

| Revenue | $211.9B | $245.1B | $281.7B | +15.3% |

| Operating Income | $88.5B | $109.4B | $128.5B | +20.5% |

| Net Income | $72.4B | $88.1B | $101.8B | +18.6% |

| Operating Margin | 41.8% | 44.6% | 45.6% | +380 bps |

Legend: Microsoft's annual financial results per SEC 10-K filings. Revenue and income in USD billions; CAGR calculated over the two-year period from FY2023 to FY2025.

</FinancialData>

|----------------------|-----------|--------------|------------------|

| Forward P/E (2026) | 38.2x | 22.5x | 28.7x |

| PEG Ratio (5-Yr) | 2.9 | 1.8 | 2.1 |

| Metric | Microsoft | S&P 500 Avg. | Tech Sector Avg. | Microsoft Premium (vs. S&P 500) |

|---|---|---|---|---|

| Forward P/E (2026) | 38.2x | 22.5x | 28.7x | +70% |

| PEG Ratio (5-Yr) | 2.9 | 1.8 | 2.1 | +61% |

| EV/EBITDA | 25.6x | 15.3x | 18.4x | +67% |

Legend: Valuation multiples for Microsoft vs. benchmarks (May 2026). Premium calculated as percentage above S&P 500. Source: aggregated earnings estimates and market data.

</FinancialData>

| Metric | FY2023 | FY2024 | FY2025 | 2-Yr Growth |

|---|---|---|---|---|

| Revenue | $211.9B | $245.1B | $281.7B | +32.9% |

| Operating Income | $88.5B | $109.4B | $128.5B | +45.2% |

| Azure Growth | +26% | +30% | +34% | +8pp |

| Microsoft Cloud Rev. | $111.0B | $137.0B | $168.9B | +52.2% |

Legend: Annual financial performance for Microsoft (GAAP, USD). Growth rates are year-over-year. Azure growth = constant-currency revenue growth. Source: Microsoft 10-K/A FY2025.

</FinancialData>

| Metric | FY2021 | FY2023 | FY2025 | Change |

|---|---|---|---|---|

| Operating Cash Flow | $76.7B | $87.6B | $136.2B | +77.6% |

| Free Cash Flow | $56.1B | $59.5B | $71.6B | +27.6% |

| Share Repurchases | $27.4B | $22.2B | $18.4B | -32.8% |

| Dividends Paid | $18.1B | $19.8B | $24.1B | +33.1% |

Legend: Cash flow and shareholder returns across selected fiscal years (USD). Repurchases declined as capital shifted to AI infrastructure investment. Source: Microsoft cash flow statements FY2021–FY2025.

</FinancialData>

| Segment | FY2025 Revenue | YoY Growth | Key Growth Driver |

|---|---|---|---|

| Intelligent Cloud | $123.8B | +23% | Azure +34%, OpenAI exclusivity |

| Productivity & Business | $83.5B | +14% | M365 Commercial +15%, Dynamics 365 +19% |

| More Personal Computing | $74.4B | +3% | Xbox +16%, Search Ads +20% |

Legend: Segment-level revenue (USD) and growth rates for FY2025. Intelligent Cloud includes Azure, GitHub, and server products. Source: Microsoft FY2025 10-K.

</FinancialData>

| Metric | FY2023 | FY2024 | FY2025 | 2-Yr Change |

|---|---|---|---|---|

| Revenue | $211.9B | $245.1B | $281.7B | +32.9% |

| Net Income | $72.4B | $88.1B | $101.8B | +40.6% |

| CapEx (PP&E) | $28.1B | $44.5B | $64.6B | +129.6% |

| Diluted EPS | $9.68 | $11.80 | $13.64 | +40.9% |

Legend: Microsoft annual financials FY2023–FY2025. Revenue and net income have grown significantly, but CapEx has more than doubled, far outpacing revenue growth and compressing capital efficiency. Source: SEC filings (10-K, FY2025, filed July 2025).

</FinancialData>

| Regulatory Threat Claim | Claimed Exposure | Actual Materiality | Evidence |

|---|---|---|---|

| DOJ antitrust bundling | $12B annual revenue | No quantified exposure in SEC filings; <4% of total revenue if real | 10-Q Risk Factors (standard language) |

| EU GDPR fines | €1.2B (2025) | €225M specific to Microsoft (0.03% of op. income) | Irish DPC ruling 2025 |

| China software mandate | "Major revenue threat" | China <2% of total revenue; APAC total ~13% | 10-K geographic segment data |

Legend: Quantified review of each regulatory claim versus documented financial exposure from SEC filings and public regulatory settlements. Revenue figures in USD.

</FinancialData>

| Metric | FY2025 Actual | FY2026 Est. | FY2027 Est. | Trend |

|---|---|---|---|---|

| Diluted EPS | $13.64 | $16.81 | $19.34 | Decelerating |

| EPS Growth | +15.6% | +23.3% | +15.0% | −8.3pp |

| Revenue | $281.7B | $329.5B | $384.0B | Decelerating |

| Revenue Growth | +14.9% | +17.0% | +16.5% | −0.5pp |

| Total Assets Growth | +20.9% | — | — | Outpacing Rev |

Legend: Microsoft EPS and revenue consensus estimates versus actuals. EPS growth decelerates sharply from FY2026E to FY2027E; asset growth outstrips revenue growth, compressing capital efficiency. Source: consensus analyst estimates.

</FinancialData>

| Period | Consensus EPS | EPS Growth | Revenue Growth | Implied PEG (at ~$415) |

|---|---|---|---|---|

| FY2026E (0y) | $16.81 | +23.3% | +17.0% | 1.06x |

| FY2027E (+1y) | $19.34 | +15.0% | +16.5% | 1.65x |

Legend: MSFT consensus estimates showing growth deceleration. PEG calculated as trailing P/E (~24.7x) divided by forward EPS growth rate. FY2027E PEG of 1.65x signals full valuation. Source: analyst consensus data, May 2026.

</FinancialData>

| Risk Factor | Mechanism | Impact on Returns |

|---|---|---|

| Growth deceleration (23.3% → 15.0%) | Multiple compression from ~25x to ~18x | ~16% capital loss even at consensus EPS |

| AI capex overbuild | Declining ROIC, margin compression | EPS misses vs. consensus; further de-rating |

| Negative estimate revisions (current qtr) | Leading indicator of estimate cuts | Downside surprise risk elevated |

| Regulatory tail risk (DOJ, EU, China) | Asymmetric downside, not priced | 2-5% revenue headwind in worst case |

| Price momentum (-13.5% YTD) | Institutional repositioning out of megacap | Selling begets more selling |

Legend: Causal chain linking identified risk factors to expected negative total returns. Each factor independently creates downside pressure; in combination, they produce asymmetric risk-reward at current entry prices.

</FinancialData>

| Fiscal Year | Revenue Growth YoY | Operating Income Growth YoY | Net Income Growth YoY |

|---|---|---|---|

| 2021 | +17.5% | +32.0% | +38.4% |

| 2022 | +18.0% | +19.3% | +18.7% |

| 2023 | +6.9% | +6.2% | -0.5% |

| 2024 | +15.7% | +23.6% | +21.8% |

| 2025 (TTM) | +14.9% | +17.4% | +15.5% |

Legend: Microsoft fiscal-year growth rates, FY2021–FY2025 (latest trailing twelve months). Growth figures are year-over-year percentages derived from company financial statements.

</FinancialData>

|----------------------|-------------|--------------|---------------|

| Forward P/E | 38.2 | 22.5 | 28.7 |

| PEG Ratio | 2.4 | 1.8 | 2.1 |

| Enterprise Value/EBITDA | 25.1 | 16.3 | 19.4 |

|----------------|----------------------|------------|---------------------|

| AWS | 33.1% | +2.1% | $28B |

| Microsoft Azure| 24.5% | +0.8% | $22B |

| Google Cloud | 12.3% | +1.5% | $18B |

|--------------|-------------|--------------|---------------|

| Forward P/E | 38.2 | 22.5 | 28.7 |

| PEG Ratio | 2.4 | 1.8 | 2.1 |

| Period | Revenue | Operating Cash Flow | Capex | Free Cash Flow |

|---|---|---|---|---|

| FY2023 | $211.9B | $87.6B | $28.1B | $59.5B |

| FY2024 | $245.1B | $118.5B | $44.5B | $74.1B |

| FY2025 | $281.7B | $136.2B | $64.6B | $71.6B |

| FY2026 (9mo) | ~$240B | $127.5B | $80.1B | $47.4B |

Legend: Microsoft annual and year-to-date financials (FY ends June 30). Revenue, OCF, Capex, and FCF in USD billions. FY2026 figures are for the first 9 months (Jul 2025–Mar 2026). Source: SEC filings (10-K FY2025, 10-Q FY2026 Q3).

</FinancialData>

| Metric | Value |

|---|---|

| Trailing P/E (FY2025 GAAP) | ~42.8x |

| Forward P/E (FY2026 est.) | ~35.1x |

| Price / FCF (TTM) | ~51.0x |

| EV / EBITDA (TTM) | ~32.5x |

| PEG Ratio (based on FY2026 est.) | ~2.3x |

Legend: MSFT valuation multiples as of late May 2026 with the stock near $530. Trailing P/E uses FY2025 GAAP EPS of ~$12.38. Forward P/E based on FY2026 consensus ~$15.10. PEG based on estimated FY2026 EPS growth rate of ~15%. Source: SEC filings and consensus estimates.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 270 | 2026-05-29 | 146.85 | 150.75 | 149.7 | 113.7% | - | - |

| PUT | 270 | 2026-05-29 | - | 2.11 | 0.01 | 100.0% | 1 | 90 |

| CALL | 280 | 2026-05-29 | 137.0 | 140.85 | - | 122.5% | - | - |

| PUT | 280 | 2026-05-29 | - | 0.07 | - | 92.2% | - | 61 |

| CALL | 290 | 2026-05-29 | 127.0 | 130.8 | - | 108.8% | - | - |

| PUT | 290 | 2026-05-29 | - | 0.31 | 0.01 | 85.4% | 15 | 282 |

| CALL | 300 | 2026-05-29 | 116.95 | 120.85 | 119.71 | 99.0% | - | 2 |

| PUT | 300 | 2026-05-29 | - | 1.55 | 0.04 | 77.6% | 3 | 656 |

| CALL | 305 | 2026-05-29 | 111.95 | 115.85 | 116.0 | 94.2% | - | - |

| PUT | 305 | 2026-05-29 | - | 1.76 | 0.1 | 73.7% | 2 | 149 |

| CALL | 310 | 2026-05-29 | 107.0 | 110.7 | 109.25 | 84.4% | 1 | 2 |

| PUT | 310 | 2026-05-29 | - | 0.09 | - | 70.8% | - | 414 |

| CALL | 315 | 2026-05-29 | 101.95 | 105.85 | 103.08 | 85.4% | - | - |

| PUT | 315 | 2026-05-29 | - | 0.06 | 0.01 | 66.9% | 1 | 530 |

| CALL | 320 | 2026-05-29 | 97.05 | 100.85 | 99.91 | 84.4% | - | 3 |

| PUT | 320 | 2026-05-29 | - | 1.76 | 0.2 | 63.9% | 2 | 228 |

| CALL | 325 | 2026-05-29 | 91.7 | 95.85 | 94.71 | 1.5% | - | - |

| PUT | 325 | 2026-05-29 | - | 0.1 | 0.02 | 60.0% | 64 | 111 |

| CALL | 330 | 2026-05-29 | 86.8 | 90.85 | 87.02 | 61.0% | - | 1 |

| PUT | 330 | 2026-05-29 | - | 0.95 | 0.01 | 57.1% | 406 | 366 |

| CALL | 335 | 2026-05-29 | 81.95 | 85.85 | 84.7 | 67.8% | - | 5 |

| PUT | 335 | 2026-05-29 | 0.01 | 0.09 | 0.02 | 62.0% | 1 | 289 |

| CALL | 340 | 2026-05-29 | 77.0 | 80.9 | 79.7 | 66.9% | - | - |

| PUT | 340 | 2026-05-29 | 0.01 | 0.09 | 0.03 | 59.0% | 8 | 555 |

| CALL | 345 | 2026-05-29 | 71.9 | 75.9 | 75.15 | 59.0% | - | 4 |

| PUT | 345 | 2026-05-29 | 0.01 | 0.04 | 0.02 | 52.2% | 3 | 211 |

| CALL | 350 | 2026-05-29 | 67.05 | 70.1 | 69.0 | 1.5% | 5 | 18 |

| PUT | 350 | 2026-05-29 | 0.02 | 0.04 | 0.02 | 48.3% | 168 | 552 |

| CALL | 355 | 2026-05-29 | 62.1 | 65.9 | 64.99 | 56.1% | - | 7 |

| PUT | 355 | 2026-05-29 | 0.02 | 0.09 | 0.05 | 48.3% | 22 | 498 |

| CALL | 358 | 2026-05-29 | 59.6 | 63.4 | - | 54.2% | - | - |

| PUT | 358 | 2026-05-29 | 0.01 | 0.09 | - | 45.4% | - | 4 |

| CALL | 360 | 2026-05-29 | 57.05 | 60.9 | 58.78 | 50.3% | 1 | 11 |

| PUT | 360 | 2026-05-29 | 0.03 | 0.1 | 0.04 | 45.4% | 114 | 1209 |

| CALL | 362 | 2026-05-29 | 54.6 | 58.4 | - | 50.3% | - | - |

| PUT | 362 | 2026-05-29 | 0.04 | 0.07 | 0.04 | 43.4% | 25 | 110 |

| CALL | 365 | 2026-05-29 | 52.5 | 55.35 | 54.85 | 43.4% | - | 9 |

| PUT | 365 | 2026-05-29 | 0.02 | 0.1 | 0.05 | 41.5% | 42 | 942 |

| CALL | 368 | 2026-05-29 | 49.6 | 53.25 | 50.81 | 41.5% | 1 | - |

| PUT | 368 | 2026-05-29 | 0.01 | 0.11 | - | 39.5% | - | 117 |

| CALL | 370 | 2026-05-29 | 47.45 | 50.75 | 49.03 | 46.4% | 4 | 113 |

| PUT | 370 | 2026-05-29 | 0.06 | 0.07 | 0.07 | 38.6% | 742 | 2338 |

| CALL | 372 | 2026-05-29 | 45.05 | 47.65 | 47.25 | 31.7% | - | 6 |