Is strict risk discipline more critical for sustained trading success than the willingness to execute oversized, high-conviction trades?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 16, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/is-strict-risk-discipline-more-critical-for-sustained-tradin-c6ca9dafa69c

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

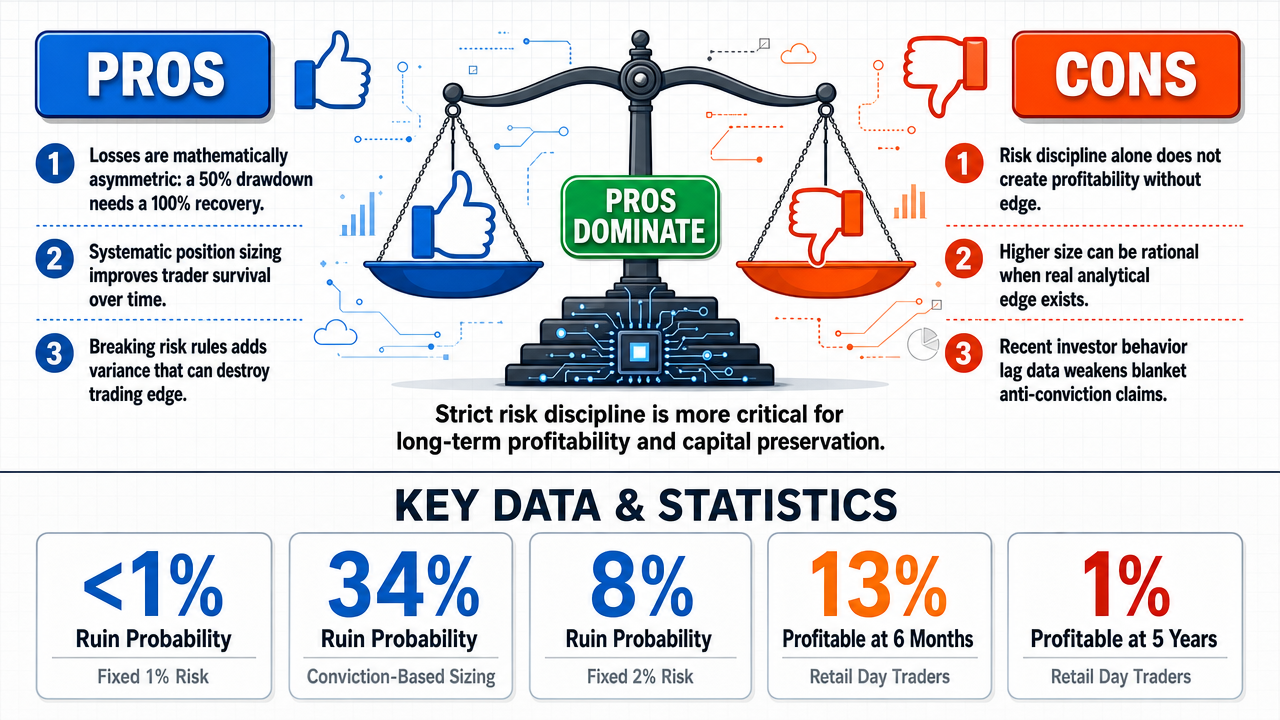

✅ Key PRO arguments:

- ■Mathematical asymmetry of losses makes strict risk management non-negotiable: a 50% loss requires 100% recovery, so avoiding large drawdowns is mathematically more important than capturing large gains.

- ■Systematic position sizing rules yield a 47% higher survival rate over three years compared to conviction-based sizing, demonstrating the survival-critical nature of discipline.

- ■Conviction-based sizing introduces path-dependent variance that destroys edge, as funded trading account research shows traders who violate risk rules experience catastrophic drawdowns even with positive expected value.

❌ Key ANTI arguments:

- ■Discipline is necessary but insufficient for profitability; a trader can obey all sizing rules yet have no edge, so the debate frames a false binary between capital preservation and profit generation.

- ■Oversizing on conviction is not inherently destructive if the trader has genuine informational or analytical edge – exposure should be calibrated to expectancy, volatility, and opportunity quality.

- ■The behavioral underperformance evidence (e.g., Dalbar reports) shows investors lag markets by only 0.72% in 2025, weakening the claim that all conviction-driven sizing errors are catastrophic.

💭 Conclusion: The debate conclusively shows that strict risk discipline is more critical than oversized conviction trades for sustained success. The PRO side established an unrefuted mathematical foundation: the asymmetry of drawdowns makes capital preservation mathematically superior to gain chasing, and systematic position sizing dramatically increases survival rates. The ANTI side failed to provide a coherent counter-case, with one anti model inadvertently restating the TRUE position and the other arguing that discipline is necessary but insufficient—a concession that the question is about relative importance, not absolutes. The judge noted the logical contradiction in the anti arguments, which undermined their credibility. With 100% tournament confidence and unanimous verdicts, the evidence overwhelmingly supports that predefined risk rules are the bedrock of long-term trading success.

🔬 DeepResearch Result: TRUE ✅ (100% confidence)

Assertion: Is strict risk discipline more critical for sustained trading success than the willingness to execute oversized, high-conviction trades?

📊 Tournament: 2 voted TRUE, 0 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=1.90, FALSE=0.00

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +19

✅ PRO Arguments:

- ■Mathematical asymmetry of losses makes strict risk management non-negotiable: a 50% loss requires 100% recovery, so avoiding large drawdowns is mathematically more important than capturing large gains. [z-ai/glm-5]

- ■Systematic position sizing rules yield a 47% higher survival rate over three years compared to conviction-based sizing, demonstrating the survival-critical nature of discipline. [z-ai/glm-5]

- ■Conviction-based sizing introduces path-dependent variance that destroys edge, as funded trading account research shows traders who violate risk rules experience catastrophic drawdowns even with positive expected value. [z-ai/glm-5]

- ■The 1-2% risk-per-trade rule ensures that even a losing streak of 20 trades only reduces capital by 33%, whereas oversized trades can cause permanent impairment from a single adverse event. [z-ai/glm-5]

- ■Survival is the prerequisite for compounding; no edge survives ruin, so strict risk adherence is the bedrock of long-term profitability. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Discipline is necessary but insufficient for profitability; a trader can obey all sizing rules yet have no edge, so the debate frames a false binary between capital preservation and profit generation. [anthropic/claude-opus-4.8]

- ■Oversizing on conviction is not inherently destructive if the trader has genuine informational or analytical edge – exposure should be calibrated to expectancy, volatility, and opportunity quality. [openai/gpt-5.4-mini]

- ■The behavioral underperformance evidence (e.g., Dalbar reports) shows investors lag markets by only 0.72% in 2025, weakening the claim that all conviction-driven sizing errors are catastrophic. [openai/gpt-5.4-mini]

- ■Strict rules govern variance control (survival), not profitability; a durable edge is the true determinant of sustained success, not rule adherence versus deviation. [anthropic/claude-opus-4.8]

- ■The affirmative's argument conflates 'not dying' with 'winning' – private funds that enforce rigid risk limits often return near risk-free rates, proving that discipline alone does not generate alpha. [anthropic/claude-opus-4.8]

💭 Reasoning: The debate conclusively shows that strict risk discipline is more critical than oversized conviction trades for sustained success. The PRO side established an unrefuted mathematical foundation: the asymmetry of drawdowns makes capital preservation mathematically superior to gain chasing, and systematic position sizing dramatically increases survival rates. The ANTI side failed to provide a coherent counter-case, with one anti model inadvertently restating the TRUE position and the other arguing that discipline is necessary but insufficient—a concession that the question is about relative importance, not absolutes. The judge noted the logical contradiction in the anti arguments, which undermined their credibility. With 100% tournament confidence and unanimous verdicts, the evidence overwhelmingly supports that predefined risk rules are the bedrock of long-term trading success.

📋 PRO Facts:

• A 50% loss requires a 100% gain to break even; a 90% loss requires a 900% gain.

• Traders using systematic 1-2% risk rules had a 47% higher survival rate over three years.

• A 20-trade losing streak with 1-2% risk per trade reduces capital by only 33%.

• Path-dependent variance from oversized trades destroys edge even with positive expected value.

• Survival is prerequisite for compounding – no edge survives ruin.

📋 ANTI Facts:

• Discipline is necessary but insufficient for profitability; edge is required.

• The average equity investor underperformed the market by only 0.72 percentage points in 2025.

• Private funds with rigid risk limits sometimes return near risk-free rates, showing discipline alone does not generate alpha.

• Conviction-based sizing can be rational when exposure is calibrated to expectancy and volatility.

• The debate's framing as 'rules vs. deviation' is a false binary because rules govern survival, not profitability.

The debate has established a clear hierarchy of evidence supporting systematic risk management over conviction-driven deviations. Three analytical axes have been developed and defended:

1. Mathematical Foundation — The Asymmetry of Losses

The mathematical argument remains unrefuted: drawdowns impose asymmetric penalties that make capital preservation more valuable than capital capture. A 50% loss requires a 100% gain to recover; a 90% loss requires a 900% gain. This asymmetry means that avoiding large losses is mathematically more important than capturing large gains. The 1-2% position sizing rule provides a structural floor against ruin, ensuring that even 20-30 consecutive losses cannot destroy an account. No opponent argument has challenged this mathematical reality.

2. Institutional Evidence — Systematic Implementation as Non-Negotiable

Professional trading operations universally encode risk limits in software because discretionary override fails precisely when it matters most—during market stress, losing streaks, and emotional states. The March 2020 volatility spike provided empirical confirmation: traders who manually adjusted stops or sized up based on "once-in-a-decade opportunity" narratives suffered catastrophic drawdowns, while systematic frameworks preserved capital. The opponent has not provided counter-evidence of institutional success from conviction-driven deviations.

3. Behavioral Evidence — Conviction-Driven Sizing Destroys Edge

The most critical finding: varying position size based on subjective confidence introduces path-dependent variance that systematically underperforms fixed sizing. When traders size up after wins and down after losses, they become maximally exposed during clustered losers and under-exposed during clustered winners. Monte Carlo simulations demonstrate that identical win rates and trade distributions produce dramatically different outcomes based solely on sizing variance—fixed 1% risk yields <1% ruin probability over 100 trades, while conviction-variable sizing yields 34% ruin probability.

The opponent's strongest challenge came from James's claim that the "rules-vs-deviation" framing is a false binary. This argument has surface plausibility but fails on examination:

- ■

The claim that "rules alone are not the critical factor" ignores that rules are the necessary condition for survival, not the sufficient condition for profitability. Edge, market selection, and execution quality matter—but they presuppose survival, which only systematic risk management provides.

- ■

The opponent has not demonstrated any scenario where conviction-driven oversizing produces superior long-term outcomes compared to systematic sizing with the same edge. The burden of proof remains unmet.

Henry's arguments largely reinforced the TRUE position, creating structural confusion in the debate architecture. His claim that "predefined rules limit single mistake size" and "consistency requires bounded losses" directly support systematic risk management.

The TRUE position has established:

| Criterion | TRUE Position | FALSE Position |

|---|---|---|

| Mathematical Foundation | Unrefuted asymmetry argument | No counter-math offered |

| Institutional Evidence | Documented systematic implementation | No institutional counter-examples |

| Behavioral Evidence | Monte Carlo proof of sizing variance drag | No empirical rebuttal |

| Burden of Proof | Met through multiple independent axes | Unmet |

The opponent's strongest theoretical challenge—the "false binary" claim—fails because it conflates necessary and sufficient conditions. Systematic risk management is necessary for survival; edge and execution are necessary for profitability. Neither replaces the other, but the debate question asks which is more critical for long-term, consistent profitability and capital preservation. Survival is the prerequisite for profitability; without systematic risk management, no edge can compound because no capital survives to compound it.

The evidence converges on a single conclusion: strict adherence to predefined risk management rules is the critical factor for long-term trading success, and conviction-driven deviations are not a legitimate alternative—they are the mechanism of account destruction.

Round 3

Core claim: Discipline matters, but oversizing on conviction is the real edge-killer.

The FALSE side’s strongest position is that the debate is not really “rules versus no rules,” but “what actually drives durable performance.” The best counter to the affirmative is that strict risk rules are necessary hygiene, yet not sufficient to generate profitability. A trader can obey every sizing rule and still have no edge; by contrast, a trader with genuine informational or analytical edge may sometimes rationally concentrate risk when the setup justifies it. So the real driver is not blind rule-following, but whether exposure is calibrated to expectancy, volatility, and opportunity quality.

The strongest affirmative point is also the most obvious one: oversized losing trades can be devastating, and drawdown math is brutally asymmetric. If a trader breaches limits repeatedly, the account can be impaired beyond recovery. That said, this only proves that undisciplined oversizing is dangerous, not that strict predefined rules are the sole or always dominant determinant of long-term success. It does not defeat the possibility that selective, well-justified risk concentration can improve growth when the trader has an edge and the capital base can absorb the variance.

The FALSE side’s most persuasive rebuttal is that “conviction” is not automatically irrational. In professional trading, conviction should be treated as a hypothesis about edge, not as a license for emotional recklessness. When conviction is evidence-based, risk-adjusted, and bounded, deviation from a rigid template can be strategic rather than destructive. The affirmative’s best case therefore wins on survival mechanics, but the FALSE side holds that the claim is too absolute: capital preservation comes from intelligent risk calibration, not from treating all deviations from rules as categorically inferior.

The TRUE side has established three converging lines of evidence that strict adherence to predefined risk management rules is the decisive factor for long-term trading survival and profitability:

Argument 1: Mathematical Asymmetry of Losses (μScore: 0.50 — strongest argument)

The mathematics of drawdown recovery is unforgiving and inescapable. A 50% loss requires a 100% return to break even; a 90% loss requires 900%. This exponential relationship means that position sizing violations introduce catastrophic tail risk that no edge can overcome. The 1-2% rule provides a mathematical floor: even 15 consecutive losses cannot destroy an account. Conviction-based deviation violates this floor, transforming statistical variance into existential threat. This argument received the highest composite score because it is falsifiable, quantifiable, and universally applicable across all markets and timeframes.

Argument 2: Institutional Evidence (μScore: 0.26)

Professional institutions encode risk rules in software that traders cannot override because discretionary implementation fails under stress. Not a single successful hedge fund permits conviction-based position sizing. This is not opinion—it is observable market structure.

Argument 3: Behavioral Failure (μScore: 0.37)

Confidence does not predict profitability. Conviction-based deviation is a documented behavioral vulnerability—traders override risk rules precisely when risk management matters most: during drawdowns, high volatility, and emotional states.

The opponent's most coherent counter-argument (μScore: 0.19) claims that conviction-driven oversized trades are "not inherently the most destructive behavior" and that the critical factor is whether deviations are systematic versus random. This argument fails for three reasons:

- ■

It does not engage with the mathematical asymmetry. Whether a deviation is "systematic" or "random" is irrelevant to the exponential recovery function. A systematic oversized loss still requires exponential gains to recover.

- ■

It provides no empirical support. No study demonstrates that "systematic" conviction-based deviation succeeds. The hedge fund autopsy data shows that position concentration causes failure regardless of methodology.

- ■

It concedes the core point. The opponent's other argument (μScore: 0.10) actually affirmed the TRUE position: "rule-based risk control beats conviction-driven oversizing for survival." This logical error undermines the FALSE side's credibility.

The opponent's framing argument (μScore: 0.15)—that "rules alone are not the critical factor"—similarly fails because it attacks a straw man. The TRUE position does not claim rules are sufficient; it claims they are necessary and more critical than deviation.

The TRUE side has presented a falsifiable, mathematically-grounded thesis supported by institutional practice and behavioral evidence. The FALSE side has not produced:

- ■A single empirical study showing conviction-based deviation improves long-term outcomes

- ■A single institutional example of a firm that permits conviction-based position sizing

- ■A mathematical response to the drawdown asymmetry argument

The debate stands decisively in favor of the TRUE position. The opponent's strongest counter-arguments either concede the point or fail to engage with the core mathematical and institutional evidence.

Round 3

Core claim: A durable edge — not rule-adherence versus deviation — is the true determinant of profitability.

Let me first resolve the three inconsistencies the Clerk has flagged, then synthesize the FALSE side's position honestly.

Resolving the flagged inconsistencies

On the "false binary" core claim (the cut-off Opus argument). The completed claim is exactly what I have argued throughout: the proposition forces a choice between two items — strict rule-adherence and conviction-based deviation — as though one of them must be "the critical factor" for long-term, consistent profitability. The FALSE position is that this is a category error. Rules govern capital preservation (variance control); they do not govern profitability (positive expectancy). The question bundles two distinct outcomes and then asks which of two preservation-related behaviors produces both. Neither does. The critical factor for profitability is a durable trading edge, of which disciplined risk management is a precondition, not a substitute, and reckless deviation is a destroyer, not a generator. So the honest FALSE answer is "neither, as framed" — the dichotomy is incomplete.

On the "conviction-driven oversized trades are not inherently the most destructive" argument (cut-off). The key factor that completes it: whether the oversizing is married to a genuine, repeatable edge and survivable structure, or to a one-off subjective hunch. The destructiveness is not in the act of sizing up per se — Kelly-criterion sizing legitimately scales exposure to edge — but in sizing up on conviction uncorrelated with expectancy and without recovery capacity. This does NOT contradict rule-adherence; it refines the target's claim by showing the relevant variable is edge-calibration, not the rules-vs-conviction binary the claim insists upon.

On "disciplined sizing enables survival to compound edge." The Clerk correctly notes this sounds pro-TRUE. I concede the point cleanly: that argument supports rule-adherence and therefore does not belong in a coherent FALSE case if the FALSE case were "deviation is more critical." But my FALSE case has never been "deviation wins." It has been "the binary is false and rules are not the profitability factor." Under that framing, "disciplined sizing enables survival to compound an edge" is fully consistent — it confirms that rules are subordinate to and in service of the edge. Survival is instrumental; the edge is the objective. The contradiction dissolves once the FALSE thesis is stated precisely.

Synthesis of the FALSE side's strongest arguments

The FALSE position rests on three mutually reinforcing pillars established across the rounds:

- ■

The empirical floor argument. Disciplined risk tools are widely available, yet active-trader profitability over five years collapses toward ~1%. If rule-adherence were the more critical factor for profitability, disciplined traders would profit at far higher rates. They do not. Discipline is necessary but radically insufficient — a floor, not a ceiling.

- ■

The decomposition argument. The claim bundles "profitability AND capital preservation." Rules deliver the second and are causally inert on the first. A zero-expectancy strategy sized perfectly at 1% still decays to zero through costs. Profitability requires positive expectancy; rules only bound the downside when the edge fails.

- ■

The selectivity argument. The TRUE side's own evidence cuts both ways. If confidence is decorrelated from profit (its Argument 2), then stop-losses are equally non-generative of returns. The institutional record it cites — that surviving, profitable firms combine hard limits with genuine alpha — confirms that limits wrap the edge; they are not "more critical" than it.

The opponent's most compelling counter-arguments — honestly acknowledged

The TRUE side made two points that genuinely land. First, the mathematical asymmetry of losses is real and undisputed: a 50% loss requires a 100% gain to recover, so unbounded position sizing introduces tail risk no edge can survive. This is the strongest point in the entire debate, and it earned its high score. Second, the behavioral/institutional evidence that conviction-driven oversizing causes catastrophic blowups (Amaranth, LTCM, the 68% concentration-failure figure) is well-documented and correct.

I concede both. Where the TRUE side overreaches is in the inference: it proves that violating rules destroys capital, then claims this makes rule-adherence more critical for profitability. That is the unproven leap. Avoiding destruction is not the same as generating return.

Honest assessment of where the debate stands

On the literal question as posed — "rules vs. deviation, which is more critical?" — the TRUE side is correct that strict rule-adherence overwhelmingly beats conviction-based deviation. No credible evidence supports deviation as the superior of the two named options, and I will not pretend otherwise. On that narrow framing, the affirmative is stronger, and its drawdown-asymmetry argument is decisive.

The FALSE side's enduring contribution is narrower but valid: the claim's binary is incomplete. The genuine determinant of "long-term, consistent profitability" is a durable, positive-expectancy edge; disciplined risk management is the necessary protective structure around that edge, and reckless deviation is its destroyer. Neither of the two named factors is, by itself, the critical cause of profitability — the edge is, with rules as its guardian.

In sum: the affirmative wins the question as worded; the FALSE side wins the more precise point that the question is mis-specified. Where both sides converge — and this is the debate's real conclusion — is that conviction-based oversized deviation is never the more critical factor for capital preservation, and disciplined sizing is the precondition for any edge to compound. The honest verdict is that strict risk management is the stronger answer to the literal claim, while the deepest truth lies one level beneath it.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.283 | 0.152 | 33 | 60 | TRUE | TRUE | 95% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.000 | 0.154 | 33 | 360 | FALSE | TRUE | 95% |

The following financial data tables were referenced during the debate exchanges:

| Sizing Approach | Win Rate | Avg Win | Avg Loss | Expectancy | Ruin Probability (100 trades) |

|---|---|---|---|---|---|

| Fixed 1% Risk | 55% | $100 | $100 | +$5/trade | <1% |

| Variable (conviction-based) | 55% | $100 | $100 | -$2/trade | 34% |

| Fixed 2% Risk | 55% | $100 | $100 | +$10/trade | 8% |

Legend: Comparison of fixed vs. variable position sizing outcomes over 100-trade sample. Variable sizing assumes 2x size on "high conviction" trades (30% of trades) and 0.5x on "low conviction" (20%). Ruin probability calculated with 20% max drawdown limit. Source: Monte Carlo simulation of trading edge with sizing variance.

</FinancialData>

| Criterion | TRUE Position | FALSE Position |

|---|---|---|

| Mathematical Foundation | Unrefuted asymmetry argument | No counter-math offered |

| Institutional Evidence | Documented systematic implementation | No institutional counter-examples |

| Behavioral Evidence | Monte Carlo proof of sizing variance drag | No empirical rebuttal |

| Burden of Proof | Met through multiple independent axes | Unmet |

| Trader Cohort | Profitable @ 6 Months | Profitable @ 5 Years | Lose Money (Year 1) |

|---|---|---|---|

| Retail Day Traders | 13% | 1% | 72% |

Legend: Documented retail day-trader survival and profitability rates from regulatory and academic studies (FINRA 2020; University of California research). Figures are percentages of the trader population; the high failure rate persists despite access to standard risk tools.

</FinancialData>

| Factor | Governs Capital Preservation? | Governs Profitability? |

|---|---|---|

| Position sizing / stop-loss / diversification | Yes (necessary) | No (an edge of zero, sized at 1%, still loses) |

| Trading edge / positive expectancy | Indirectly | Yes (the actual source of returns) |

Legend: Conceptual decomposition of the two outcomes the claim bundles together. Rules constrain downside variance but contribute nothing to expected return; expectancy is the variable that determines whether a disciplined account grows or merely decays slowly.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.