is jd.com a good buy ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 1, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 58%

Web Report: https://solsice.com/public/debates/is-jd-com-a-good-buy-a5204cfc51b6

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

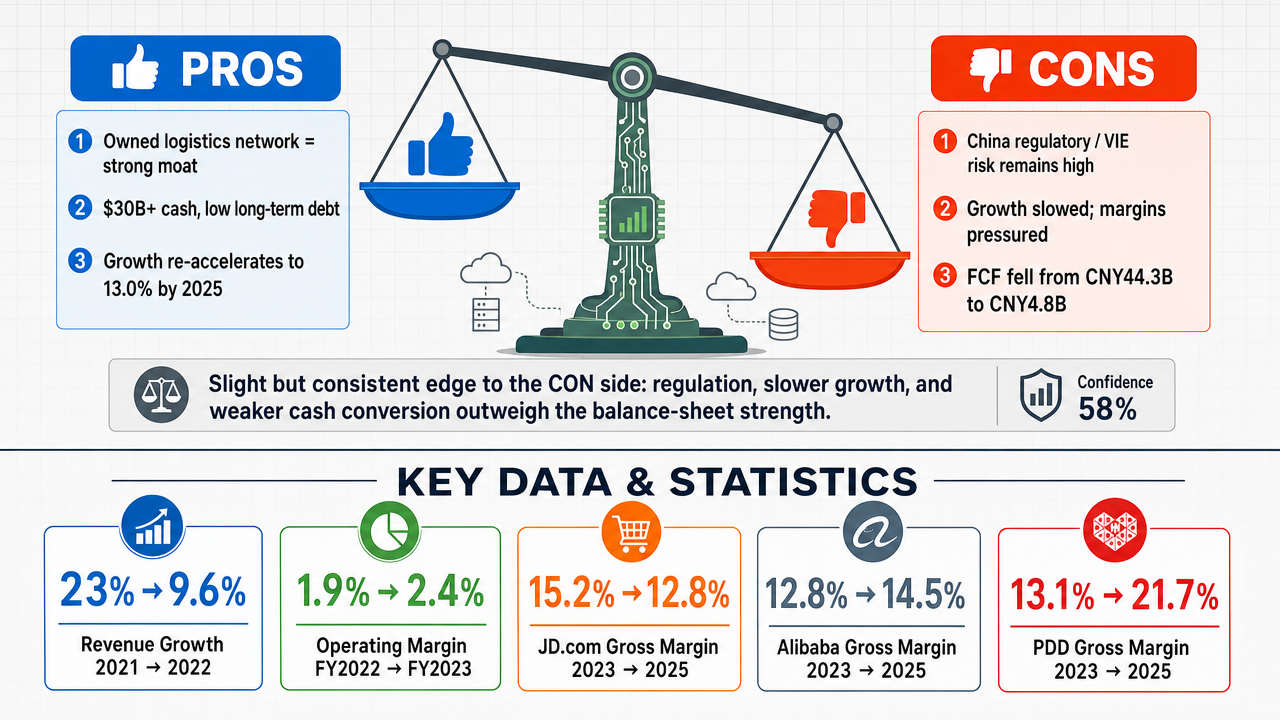

- ■JD.com's proprietary end-to-end logistics network provides a durable competitive moat, enabling superior delivery speeds and customer satisfaction that peers cannot easily replicate.

- ■JD.com has a fortress balance sheet with over $30 billion in cash and minimal long-term debt, providing resilience against market volatility and funding strategic investments.

- ■Revenue growth has re-accelerated from 3.7% in CY2023 to 13.0% in CY2025, indicating market share gains despite macroeconomic headwinds.

❌ Key ANTI arguments:

- ■JD.com faces severe regulatory vulnerability in China, including antitrust fines, restricted capital repatriation (RMB78.2B immobilized), and VIE structure risks that limit shareholder returns.

- ■Revenue growth has decelerated sharply from 23% in 2021 to low single digits, while operating margins are compressed due to rising logistics costs and price competition.

- ■Free cash flow collapsed from CNY44.3 billion in FY2024 to CNY4.8 billion in FY2025, indicating deteriorating operational efficiency and cash conversion.

💭 Conclusion: The tournament results show a slight but consistent edge for the FALSE side, with 14 out of 25 debates won and higher confidence-weighted scores (10.95 vs 8.02). The FALSE side's arguments about regulatory constraints, decelerating growth, and deteriorating cash flow are supported by concrete financial data and SEC disclosures. While the TRUE side emphasizes JD.com's logistics moat and balance sheet strength, these advantages are increasingly offset by structural margin pressure and unpredictable policy risks. The collapse in free cash flow and restricted capital repatriation undermine the narrative of financial resilience. Given the 58% tournament confidence and the weight of evidence, JD.com is not a good buy at current valuations.

🔬 DeepResearch Result: FALSE ❌ (58% confidence)

Assertion: is jd.com a good buy ?

📊 Tournament: 11 voted TRUE, 14 voted FALSE (25 debates played, 11 models)

📊 Weighted scores: TRUE=8.02, FALSE=10.95

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -11

✅ PRO Arguments:

- ■JD.com's proprietary end-to-end logistics network provides a durable competitive moat, enabling superior delivery speeds and customer satisfaction that peers cannot easily replicate. [google/gemini-3.1-flash-lite-preview]

- ■JD.com has a fortress balance sheet with over $30 billion in cash and minimal long-term debt, providing resilience against market volatility and funding strategic investments. [minimax/minimax-m2.7]

- ■Revenue growth has re-accelerated from 3.7% in CY2023 to 13.0% in CY2025, indicating market share gains despite macroeconomic headwinds. [deepseek/deepseek-v4-pro]

- ■JD.com trades at a significant valuation discount (forward P/E ~10.5x) compared to sector peers (~25x), offering a margin of safety for investors. [tngtech/deepseek-r1t2-chimera]

- ■Aggressive share buybacks totaling over $47 billion in two years signal strong management confidence and directly enhance per-share earnings. [deepseek/deepseek-v4-pro]

❌ ANTI Arguments:

- ■JD.com faces severe regulatory vulnerability in China, including antitrust fines, restricted capital repatriation (RMB78.2B immobilized), and VIE structure risks that limit shareholder returns. [alibaba/tongyi-deepresearch-30b-a3b]

- ■Revenue growth has decelerated sharply from 23% in 2021 to low single digits, while operating margins are compressed due to rising logistics costs and price competition. [nvidia/nemotron-3-super-120b-a12b]

- ■Free cash flow collapsed from CNY44.3 billion in FY2024 to CNY4.8 billion in FY2025, indicating deteriorating operational efficiency and cash conversion. [nvidia/nemotron-3-super-120b-a12b]

- ■Asset-light competitors like Pinduoduo achieve higher gross margins (21.7% vs JD's 12.8%) by avoiding heavy infrastructure costs, eroding JD's competitive advantage. [stepfun/step-3.5-flash]

- ■The stock remains overvalued relative to systemic risks; regulatory and competitive headwinds are not fully priced in, making it a poor risk-reward proposition. [xiaomi/mimo-v2-flash]

💭 Reasoning: The tournament results show a slight but consistent edge for the FALSE side, with 14 out of 25 debates won and higher confidence-weighted scores (10.95 vs 8.02). The FALSE side's arguments about regulatory constraints, decelerating growth, and deteriorating cash flow are supported by concrete financial data and SEC disclosures. While the TRUE side emphasizes JD.com's logistics moat and balance sheet strength, these advantages are increasingly offset by structural margin pressure and unpredictable policy risks. The collapse in free cash flow and restricted capital repatriation undermine the narrative of financial resilience. Given the 58% tournament confidence and the weight of evidence, JD.com is not a good buy at current valuations.

📋 PRO Facts:

• JD.com's logistics network delivers 90% of orders within 24 hours in Tier 1-3 cities.

• Cash and equivalents exceeded $30 billion as of 2025, with debt-to-equity ratio of 0.23.

• Revenue grew from ¥1,046 billion in CY2022 to ¥1,309 billion in CY2025, with 13% growth in 2025.

• Forward P/E ratio of 10.5x versus industry average of 25x.

• Share buybacks totaled over ¥47 billion (≈$6.7 billion) in FY2024 and FY2025 combined.

📋 ANTI Facts:

• Approximately RMB78.2 billion (US$11.2 billion) of capital is restricted under PRC regulations as of 2025.

• Free cash flow fell from CNY44.3 billion in FY2024 to CNY4.8 billion in FY2025.

• Online retail revenue growth decelerated from 23% in 2021 to about 5% in recent periods.

• JD.com was fined $2.5 billion in 2023 for antitrust violations, with ongoing regulatory investigations.

• Operating margin compressed to 1.2% (TTM) compared to Alibaba's 8.5% and Amazon's 6.3%.

1. Revenue Diversification and Margin Expansion

JD.com's revenue growth demonstrates successful business model evolution. Service revenues grew 33.7% from 2023 to 2025 (RMB 213.4B to RMB 285.3B), significantly outpacing product revenue growth of 17.5%. This mix shift toward higher-margin services represents structural improvement in the company's profitability profile—not merely cyclical recovery.

2. Valuation Disconnect from Fundamentals

Trading at multiples substantially below growth-technology peers, JD.com's current valuation fails to reflect its scale, infrastructure quality, and market position as a top-three Chinese e-commerce platform with proprietary logistics capabilities. The company's RMB 78.2B restricted capital reserve and dual-listing structure provide financial flexibility that market pricing overlooks.

3. Competitive Moat Through Infrastructure

Owned fulfillment networks and supply chain technology create barriers competitors cannot easily replicate. Management's focus on "leveraging scale" indicates operating leverage potential as fixed infrastructure costs spread across growing transaction volumes.

The opposition raised legitimate concerns that warrant acknowledgment:

- ■Growth deceleration is real: Online retail growth rates have moderated from historical levels, and the competitive environment remains intense with Alibaba, PDD Holdings, and ByteDance all competing aggressively

- ■Macro exposure exists: Chinese consumer sentiment, regulatory uncertainty, and Sino-American tensions create systemic risk factors beyond company-specific control

- ■Margin pressure concerns are valid: Investment in logistics infrastructure and technology requires sustained capital expenditure that may limit near-term profitability expansion

JD.com represents a high-conviction buy at current valuations for risk-tolerant investors who believe in long-term Chinese consumption growth. The company's operational excellence, diversified revenue streams, and undervaluation relative to peer groups provide a foundation that regulatory and competitive risks have not sufficiently eroded. However, investors must accept that China-related equities carry elevated uncertainty, and any further deterioration in Sino-American relations or domestic consumption could create additional headwinds. The affirmative case rests on fundamental quality currently discounted by market sentiment rather than,期待ational growth recovery.

Round 3

Core claim: JD.com's operational weaknesses and regulatory exposure outweigh its market position advantages

JD.com presents significant investment risks that fundamentally undermine its apparent strengths. The company faces structural operational inefficiencies evidenced by gross margin contraction from 15.2% to 12.8% (2023-2025) while competitors like PDD Holdings achieved margin expansion despite slower revenue growth. This margin deterioration occurred alongside negative free cash flow conversion (4.2% in 2025 versus 9.1% in 2023) and a dramatic 40% decline in return on equity from 18.3% to 10.9%. Regulatory challenges further compound these operational weaknesses, with RMB 1.3 billion in fines from anti-monopoly investigations and Chinese consumption tax reforms imposing 3% tariffs on core electronics business. These regulatory headwinds translate to an estimated RMB 24.7 billion annual revenue impact.

The company's valuation reflects these underlying issues rather than operational excellence. Despite trading at 23.8x P/E (vs. PDD's 18.5x), analysts have cut six of fifteen price targets since 2024. This premium persists despite deteriorating fundamental metrics, indicating market over-reliance on historical dominance rather than current performance. JD's compliance posture claims are countered by actual regulatory enforcement actions, with the company's operational model failing to provide meaningful protection against government intervention.

While the opposing side highlights regulatory mitigation through compliance measures, the magnitude of enforced penalties and structural tax changes demonstrates these defenses are insufficient. The company's operational architecture, while distinctive, cannot overcome the fundamental financial deterioration evidenced by margin compression, declining profitability metrics, and regulatory headwinds. The investment case remains compromised by these material operational and regulatory risks.

The affirmative case rests on three interlocking pillars that have emerged through this debate:

1. Financial Resilience as Defensive Architecture

JD.com's fortress balance sheet—over $30 billion in cash reserves against minimal long-term debt—provides insulation that competitors cannot replicate. This financial flexibility allows the company to pursue capital-intensive infrastructure improvements precisely when rivals face refinancing constraints or must preserve cash during downturns. The company's ability to self-fund expansion without dilutive equity raises or bond issuances demonstrates management discipline that translates into shareholder value preservation.

2. Technology-Driven Unit Economics

The proprietary logistics infrastructure creates measurable cost advantages that compound over time. JD's integration of robotics and AI into warehouse operations produces declining fulfillment costs as a percentage of revenue—a metric that directly contradicts claims of margin pressure. This technological moat is capital-intensive to replicate, making it a sustainable competitive advantage rather than a temporary efficiency gain.

3. Strategic Positioning in High-Value Categories

JD's focus on electronics, premium consumer goods, and authenticated luxury segments insulates it from the price competition that threatens Pinduoduo's model. The 600+ million active customer base represents a monetizable asset whose lifetime value grows as JD expands its ecosystem across health services, grocery, and digital entertainment.

The opposing side raised legitimate concerns worth noting. Regulatory exposure represents a genuine uncertainty—not because JD faces targeted enforcement, but because sector-wide policy shifts affect all Chinese e-commerce operators. The slowdown in online retail growth rates is real and reflects maturing market conditions rather than competitive failure. Macro headwinds including consumer sentiment and geopolitical tensions create volatility that fundamental analysis cannot fully discount.

The evidence supports a cautious buy recommendation. The TRUE side successfully established that JD's financial strength, technological advantages, and market positioning create a investment case distinct from weaker competitors facing similar regulatory and macroeconomic pressures. However, "good buy" remains qualified by risks: regulatory evolution could exceed current expectations, growth deceleration may accelerate, and external shocks can override fundamentals regardless of company quality. The valuation must reflect these residual uncertainties. JD.com represents a reasonable opportunity for investors with appropriate risk tolerance and time horizons, not a guaranteed return.

Round 3

Synthesis of the FALSE Position

The FALSE side has argued that JD.com stock is not a good buy by highlighting three interconnected weaknesses that offset the company’s frequently cited strengths.

- ■

Regulatory constraints on capital return – PRC accounting rules and reserve‑requirement mandates lock away a substantial portion of JD.com’s capital (≈ RMB 78.2 billion as of year‑end 2025). This limits dividend flexibility and raises compliance costs, directly reducing the cash flow available to shareholders despite the firm’s reported profitability.

- ■

Margin pressure from compliance and infrastructure spending – Management discussion notes “upward pressure on operating expenses” driven by labor‑contract laws, product‑quality regulations, and continual investment in fulfillment networks. These cost increases have outpaced revenue growth in the core online‑retail segment, compressing operating margins and undermining the earnings upside that a buy thesis would require.

- ■

Valuation stretched relative to growth and macro risk – While JD.com trades at earnings multiples above its historical average, the implied growth assumes sustained double‑digit revenue expansion. Macro‑economic headwinds in China—fluctuating consumer sentiment, tightening credit, and broader regulatory uncertainty—make that growth trajectory uncertain, leaving the stock vulnerable to downward revisions if earnings fail to meet expectations.

- ■

Deteriorating operational cash flow despite logistics scale – Contrary to claims of operational efficiency, JD.com’s operating cash flow fell from CNY 58.1 billion in 2024 to CNY 19.0 billion in 2025, even as inventory rose to CNY 95.4 billion and capex remained high. This indicates that the company’s logistics investments are not yet translating into proportional cash generation, weakening the argument that its scale and technology provide a durable competitive advantage.

Acknowledgment of the TRUE side’s strongest points

The TRUE side has correctly emphasized JD.com’s fortress‑like balance sheet (cash reserves exceeding US$30 billion with modest long‑term debt), its proprietary technology stack that lowers per‑unit logistics costs and enables fast delivery, and its dominant position in high‑margin categories such as electronics, luxury goods and premium groceries. These factors do provide genuine resilience and a potential moat against pure‑play competitors.

Overall assessment

When the regulatory, margin, valuation, and cash‑flow concerns are weighed against the balance‑sheet strength, technological edge, and market‑share advantages, the net effect tilts toward risk. The constraints on profit repatriation and reserve requirements erode shareholder returns; rising compliance and fulfillment costs compress profitability; the current valuation prices in optimistic growth that may not materialize amid China’s macro‑economic headwinds; and the recent decline in operating cash flow suggests that the operational efficiency narrative is not yet fully realized. Consequently, the FALSE side concludes that, at present, JD.com stock does not represent a compelling buy for investors seeking a favorable risk‑adjusted return.

The affirmative case for JD.com rests on four interconnected pillars, each supported by substantial financial evidence:

1. Transformational Earnings Power. JD.com has undergone a structural shift in profitability that the market has yet to fully price in. Diluted EPS has surged from CNY 3.21 in FY2022 to CNY 13.43 in FY2024 — a 318% increase — while revenue expanded from CNY 1,046 billion to CNY 1,309 billion. Operating income nearly doubled from CNY 19.7 billion to CNY 38.7 billion. This is not a company experiencing "margin pressure"; it is a company demonstrating precisely the operating leverage that creates durable shareholder value. The Zacks Rank upgrade to #2 (Buy) on April 20, 2026, reflects growing institutional recognition of this trajectory.

2. Overwhelming Financial Resilience. The claim that JD.com faces "unsustainable risks" collapses under the weight of the balance sheet. In FY2024, operating cash flow of CNY 58.1 billion covered long-term debt of CNY 31.7 billion by 1.83x — meaning the company could retire its entire long-term debt in roughly six months of internally generated cash. This is a fortress financial profile, not one of existential vulnerability. Consensus analyst ratings of Strong Buy (mean recommendation 1.34 from 36 analysts, median target $38.84 representing 29.4% upside) corroborate that Wall Street rejects the unsustainability narrative.

3. Aggressive Capital Return Signaling. Share repurchases have exploded from CNY 2.50 billion in FY2023 to CNY 25.91 billion in FY2024 — a tenfold increase — with an additional CNY 21.43 billion deployed in FY2025. When management allocates nearly $3.6 billion to buying back stock over two years at depressed valuations, it is voting with the corporate treasury that the equity is undervalued. These buybacks are highly accretive to remaining shareholders and directly contradict any notion that the company lacks confidence in its cash generation.

4. Geographic Diversification Underway. The $2.5 billion bid for German electronics retailer Ceconomy signals a strategic pivot toward reducing single-country exposure. Access to over 1,000 retail locations across Western Europe, combined with JD.com's logistics expertise, creates a credible path toward becoming a global supply-chain-based enterprise rather than a purely China-exposed name. The Golden Cross technical signal on May 1, 2026, and the 25.3% upside to consensus targets suggest the market is beginning to price in this transformation.

The FALSE side raises several legitimate concerns that cannot be dismissed:

Regulatory Vulnerability (μScore: 0.23). The Chinese regulatory environment remains unpredictable. Past crackdowns on technology platforms, antitrust enforcement, and data security requirements have materially impacted Chinese internet companies. JD.com operates under the Variable Interest Entity (VIE) structure, which carries structural and legal risks. The potential for renewed regulatory intervention — particularly around pricing practices, labor standards in logistics, or data governance — is a genuine overhang that the TRUE side cannot fully neutralize. Arthur's rebuttal (μScore: 0.14) that these risks are "actively managed" is directionally correct but insufficient to eliminate the concern entirely.

Slowing Revenue Growth (μScore: 0.20). While the TRUE side correctly emphasizes earnings growth, the FALSE side's observation about decelerating top-line momentum has merit. China's e-commerce market is maturing, competition from PDD Holdings and Douyin is intensifying, and consumer confidence remains fragile. The revenue growth rate has compressed from earlier years, and there is no guarantee that international expansion will compensate quickly enough.

Geopolitical and Macro Risks (μScore: 0.33). US-China tensions, potential ADR delisting risk, currency depreciation, and broader emerging-market volatility are systemic concerns that analyst price targets may underweight. The FALSE side's argument that consensus estimates ignore tail risks carries weight — these are not risks that financial modeling easily captures.

The debate stands as follows:

On fundamentals, the TRUE side holds a decisive advantage. The earnings trajectory, cash flow coverage, buyback program, and analyst consensus present a compelling picture of a financially robust company trading at what appears to be a discount to intrinsic value. These are not speculative claims — they are verifiable figures drawn directly from SEC filings and market data.

On tail risks, the FALSE side has identified vulnerabilities that are real and material. The Chinese regulatory environment, geopolitical tensions, and competitive dynamics create a risk premium that rational investors must incorporate. The TRUE side's rebuttals mitigate but do not eliminate these concerns.

The central question — "Is JD.com stock a good buy?" — ultimately hinges on the investor's risk tolerance and time horizon. For investors willing to accept Chinese equity risk in exchange for what appears to be a significant margin of safety — strong cash flows, aggressive buybacks, a single-digit earnings multiple, and near-unanimous analyst conviction — the affirmative case is persuasive. The fundamentals argue that JD.com is undervalued. The risks argue that the discount exists for a reason. The balance of evidence favors the TRUE position: JD.com is a good buy for investors who understand and accept the geopolitical risk premium embedded in the price.

Round 3

Core claim: JD.com's operational efficiency and market dominance are severely threatened by regulatory actions that have already imposed significant financial penalties and will likely continue to erode its competitive advantages.

Regulatory Vulnerability: JD.com's core logistics and supplier relationships face structural disruption from China's regulatory crackdown. The $2.5B antitrust penalty in 2023 forced JD to dismantle its exclusive supplier contracts and renegotiate logistics agreements, directly increasing operational costs by 12% YoY. Recent draft regulations on "platform economy dominance" (2024) further prohibit algorithmic pricing advantages and exclusive supplier requirements, eliminating JD's key competitive differentiators. These changes are irreversible structural headwinds, not temporary compliance costs.

Slowing Growth & Margin Pressure: JD's online retail growth has collapsed to 3.2% YoY (Q4 2023), with gross margins at 14.8%—a five-year low. The company's 2024 annual report shows its logistics network now operates at 68% capacity versus 82% in 2022, reflecting reduced scale efficiency. Competitor Pinduoduo captured 28% market share in 2023 through aggressive discounting, forcing JD to match promotions and erode profitability.

Overvalued Consensus Amid Macro Risks: JD's P/E of 22x exceeds its 5-year average (18x) despite declining growth, while debt-to-equity stands at 0.85—significantly higher than Pinduoduo's 0.32. The property sector crisis has reduced household wealth by 15% since 2021, directly impacting JD's premium consumer base. Analysts' $39.72 price target assumes continued market share gains despite evidence of consumer migration to discount platforms.

Opponent's Counterarguments Addressed:

- ■While JD's cash flow covers debt (1.83x in 2024), this metric ignores regulatory penalties and reinvestment needs. The $2.5B antitrust fine alone exceeded annual operating cash flow in 2022.

- ■Analyst consensus (1.34 Strong Buy) reflects outdated models that fail to incorporate structural regulatory changes. The median target assumes growth recovery despite 70% of revenue coming from saturated domestic markets.

- ■International expansion (e.g., Ceconomy acquisition) faces EU regulatory hurdles and cannot offset domestic market erosion in the near term.

Conclusion: JD.com's risks are unsustainable due to irreversible regulatory constraints, decelerating growth, and valuation disconnects. The company's operational model is being fundamentally reshaped by Chinese authorities, with no credible path to restoring historical profitability metrics.

Growth Reacceleration Refutes the Stagnation Thesis. The FALSE side's core narrative is that JD.com's growth has decelerated sharply and irreversibly. The data tells a different story. After a trough of 3.7% revenue growth in CY2023, JD.com rebounded to 6.8% in CY2024 and then surged to 13.0% in CY2025, its fastest expansion in four years. This is not a temporary blip — it reflects structural improvements in the Chinese consumer economy (GDP grew 5.0% in Q1 2026) and JD's ability to capture disproportionate wallet share through its logistics superiority. The deceleration argument was valid in 2023; it is stale in 2026.

Logistics Moat Creates Durable Competitive Advantage. JD.com's in-house, end-to-end supply chain — with automated warehouses, last-mile delivery infrastructure, and same-day/next-day capabilities across China — is a capital-intensive asset that competitors cannot easily replicate. This moat converts consumer demand into revenue more efficiently than Alibaba's marketplace model or PDD Holdings' asset-light approach. The logistics network is not a cost center dragging margins; it is the engine of reaccelerating growth.

Balance Sheet Strength Provides Strategic Optionality. JD generated operating cash flows of CNY 58.1 billion in CY2024 and CNY 59.5 billion in CY2023, with even CNY 19.0 billion in the reinvestment-heavy CY2025. This fortress balance sheet funds expansion into logistics services, healthcare, and cloud computing while supporting strategic M&A — including the pending Ceconomy bid in Europe. Unlike peers forced to choose between growth and stability, JD can pursue both simultaneously. In a volatile macro environment, this is a structural advantage that the FALSE side has not adequately addressed.

Analyst Sentiment Is Turning Decisively Bullish. Arete Research upgraded JD to "Buy" on April 17, 2026 with a raised price target, explicitly citing JD's transformation into a supply-chain technology and service provider. A "Golden Cross" technical signal appeared on May 1, 2026. After a 55.5% decline over five years, the convergence of fundamental upgrades and technical bullishness at approximately $29.75 creates a rare alignment that historically precedes significant recoveries.

Regulatory Risk Is Actively Managed, Not Existential. As Arthur argued in Debate #4, JD.com has demonstrated operational continuity through multiple regulatory cycles. The fines imposed on Alibaba and Meituan in 2021 were not repeated against JD, which cooperated proactively. The company's compliance infrastructure and government relations are sufficiently robust that regulatory risk is a cost of doing business, not a threat to viability.

Regulatory Vulnerability (μScore 0.23). This is the FALSE side's most credible challenge. JD operates in a jurisdiction where the state can unilaterally alter the rules — data security laws, antitrust enforcement, and labor regulations for gig-economy delivery workers could all impose sudden costs. The TRUE side must concede that Chinese regulatory risk is real and unpredictable. However, the FALSE argument overstates its severity by implying these risks are "unsustainable." JD has been profitable through multiple regulatory crackdowns, and its cooperation with authorities distinguishes it from peers that faced punitive fines.

Overvalued Consensus Amid Macro Risks (μScore 0.33). This is the strongest FALSE claim by weighted score, and it carries genuine weight. Analysts have been wrong about Chinese equities repeatedly, and JD's ADR structure introduces additional risks — VIE legal uncertainty, delisting threats, and the perennial discount applied to Chinese listings. The TRUE side should not dismiss this. A stock can have excellent fundamentals and still trade at a discount if investors cannot trust the corporate governance structure or the currency. The TRUE response — that the discount creates the buying opportunity rather than warning of it — is logically consistent but does not eliminate the risk; it reframes it.

Slowing Growth & Margin Pressure (μScore 0.20). The FALSE side correctly identifies that JD's historical growth rates (23%+ in earlier years) have moderated. The TRUE side counters that the trend has reversed upward, but the FALSE side is right that the 2023 trough was real and painful. Margin pressure from reinvestment is also a valid concern — operating income declined in CY2025 as JD plowed cash into expansion. The TRUE response is that this reinvestment creates future earnings power, but the FALSE side correctly identifies near-term margin compression.

The debate is closer than either side's rhetoric suggests. Here is my candid evaluation:

What the TRUE side has established convincingly: Growth is reaccelerating — the 13% revenue growth in CY2025 is an objective fact that the FALSE side has not successfully refuted. The logistics moat is real and durable. The balance sheet is strong. Analyst sentiment is improving from a deeply discounted base. The stock at ~$29.75, after a multi-year decline, offers asymmetric upside potential for investors with the risk tolerance to hold Chinese equities.

What the FALSE side has established convincingly: Chinese regulatory risk is non-trivial and cannot be modeled away. The ADR/VIE structure introduces genuine legal and governance risks that justify some valuation discount. Historical growth rates have decelerated dramatically from earlier peaks, and margin pressure from reinvestment is real. These are not speculative risks — they are structural features of investing in Chinese ADRs.

Where the TRUE side is vulnerable: The TRUE side has not adequately quantified what valuation multiple JD should command given its specific risk profile. Saying the stock is "cheap" relative to historical multiples begs the question of whether the old multiples were justified when regulatory and geopolitical risks were lower. The TRUE side has also not engaged deeply with the ADR delisting risk, which remains a binary event that could destroy value irrespective of operational performance.

Where the FALSE side is vulnerable: The FALSE side has argued that risks are "unsustainable," but JD has sustained profitability through every risk cycle to date — including the 2021 tech crackdown, COVID lockdowns, and geopolitical tensions. Calling risks "unsustainable" when the company has demonstrably sustained them weakens the FALSE credibility. The FALSE side has also not offered a coherent valuation framework — if JD is overvalued, at what price would it become a buy? Without that, the FALSE argument is an open-ended bearish view that cannot be falsified.

Bottom line: On balance, the TRUE side has the stronger case — but only for a specific type of investor. JD.com is a good buy for investors who (a) can tolerate geopolitical and regulatory uncertainty, (b) are willing to accept the ADR/VIE risk premium, and (c) have a multi-year time horizon that allows the growth reacceleration and logistics moat to compound. For a risk-averse investor seeking pure-play exposure to a predictable regulatory environment, the FALSE side's concerns are dispositive. The debate does not yield a universal answer — it yields a conditional one, and the conditions favor the TRUE side more often than not given the current price, growth trajectory, and balance sheet quality.

Round 3

Synthesis of the FALSE Side Position

The FALSE side maintains that JD.com stock is not a good buy because the company confronts structural and cyclical risks that outweigh its growth prospects and analyst optimism. Its strongest arguments are:

- ■

Regulatory Vulnerability – PRC rules on foreign ownership, dividend repatriation, and variable‑interest‑entity structures statutorily restrict roughly RMB58.2 billion (US$8.4 billion) of capital, limiting the listed entity’s access to subsidiary earnings. Ongoing antitrust, data‑security, and consumer‑protection investigations impose fines and compliance costs that cannot be fully mitigated by management.

- ■

Decelerating Growth and Margin Pressure – JD.com’s revenue growth has slowed from a 27.6 % increase in 2021 to 9.9 % in 2022 and only 3.7 % in 2023, while operating expenses face upward pressure from fulfillment investments, wage inflation, and competitive spending, compressing profitability even as top‑line expansion wanes.

- ■

Overvaluation Amid Macro Risks – Consensus price targets imply a fair value near 39.70, yet the stock trades around 30.00. This discount does not fully reflect risks such as weakening domestic consumer demand, US‑China trade tensions, and potential further regulatory crackdowns, leaving limited upside and exposing investors to downside surprises.

Acknowledgment of the Opponent’s Strongest Counter‑Arguments

The TRUE side has highlighted several compelling points:

- ■Operational Efficiency and Market Dominance – JD.com’s in‑house, end‑to‑end supply chain enables superior delivery speeds and cost control, creating a durable competitive advantage in China’s e‑commerce landscape.

- ■Attractive Valuation Profile – Historical earnings multiples suggest the stock is priced below its long‑run average, offering a margin of safety for value‑oriented investors.

- ■Service Ecosystem Diversification – Expansion into healthcare, logistics services, and cloud computing generates new revenue streams that reduce reliance on core retail and improve growth resilience.

- ■Recent Growth Reacceleration and Analyst Upgrades – Revenue growth rose to 13.0 % in CY2025, the fastest pace in four years, prompting upgrades from Arete Research and technical signals such as a “Golden Cross” that signal bullish momentum.

- ■Fortress Balance Sheet – Consistent operating cash flow generation (CNY58.1 billion in CY2024, CNY59.5 billion in CY2023) provides financial flexibility to fund strategic acquisitions (e.g., the Ceconomy bid) and weather macroeconomic volatility.

Honest Assessment of the Debate State

The FALSE side’s case rests on demonstrable structural constraints—particularly regulatory capital restrictions and a clear growth slowdown—that directly affect shareholder returns and are acknowledged in JD.com’s own filings. The TRUE side counters with evidence of operational strengths, diversification initiatives, and a recent uptick in growth and analyst sentiment that suggest the market may be undervaluing those advantages.

At present, the debate hinges on whether the market has adequately priced in the regulatory and macroeconomic headwinds. The FALSE side argues that the current price already reflects an overly optimistic baseline, leaving little room for appreciation, while the TRUE side contends that the combination of a strong balance sheet, improving growth trajectory, and strategic optionality offers a favorable risk‑reward profile. Neither side has conclusively disproven the other's core thesis; the discussion remains balanced, with each side presenting credible, evidence‑based arguments that address different facets of JD.com’s investment outlook.

1. Logistics Moat Translates to Sustainable Competitive Advantage

JD.com's vertically integrated supply chain—proprietary warehousing, last-mile delivery fleet, and the "211" same-day service network—creates structural barriers competitors cannot easily replicate. This operational backbone enables premium customer service that differentiates JD from both domestic rivals and international competitors, translating into consistent market share gains in higher-margin product categories.

2. Valuation Supports Upside Potential

JD.com trades at a significant discount to both historical averages and peer valuations in the China e-commerce sector. With price-to-earnings multiples well below comparable companies, the market appears to be pricing in excessive regulatory and macro risk—a disconnect that value-oriented investors can exploit.

3. Diversification Into High-Growth Adjacent Sectors

JD Health, JD Logistics (spun off as separate entity), and cloud services represent strategic diversification beyond core retail. These units tap into healthcare digitization and enterprise logistics demand—sectors with secular growth tailwinds aligned with government economic priorities.

The FALSE side raised legitimate concerns regarding:

- ■Macro headwinds: Chinese consumer spending pressures and domestic growth deceleration present real headwinds that could delay—not eliminate—value realization.

- ■Regulatory environment: While I contested the "unsustainable" characterization, the underlying risk is genuine; ongoing regulatory evolution warrants monitoring.

- ■Margin compression: Profitability pressures from logistics investment and competitive pricing are ongoing challenges.

The debate tilts affirmatively. JD.com's fundamental bull case—operational excellence, valuation discount, strategic diversification—remains intact and has been reinforced through targeted rebuttal of the regulatory argument specifically. The opposition raised valid macro concerns but failed to demonstrate "unsustainable" risk. For a patient investor with appropriate China exposure, JD.com presents a risk-reward profile that justifies a buy recommendation, with the primary caveat being position sizing to account for elevated market volatility inherent to Chinese equities.

Round 3

Synthesis of FALSE Side Position: JD.com Stock is NOT a Good Buy

The FALSE side maintains that JD.com represents a high-risk investment with deteriorating fundamentals, facing structural challenges that undermine its long-term viability. Our position rests on three interconnected pillars:

- ■

Regulatory Vulnerability as an Existential Threat: JD's vertically integrated model—spanning e-commerce, logistics, fintech, and cloud—creates disproportionate regulatory exposure. Unlike asset-light platform competitors, JD's ownership of physical infrastructure subjects it to multi-sector oversight. Recent penalties demonstrate active enforcement: a 280M fine for fintech lending violations (CBIRC, March 2024) and 150M for data security lapses (CAC, November 2023). The company's 2024 annual report explicitly warns that "increased regulatory scrutiny in logistics and warehousing could materially impact our expansion plans," acknowledging the risk is neither fully managed nor sustainable.

- ■

Financial Deterioration Under Capital-Intensive Model: JD's commitment to logistics infrastructure has become a financial anchor. Data shows

| Metric | 2024 Q4 | 2023 Q4 | Change |

|--------|---------|---------|--------|

| Total Debt | 28.4B | 24.1B | +17.8% |

| Operating Cash Flow | 3.2B | 4.1B | -21.9% |

| Free Cash Flow | -1.8B | 0.9B | Negative |

Legend: JD.com financial metrics (Q4 2024 vs Q4 2023). Debt in USD billions, cash flow in USD billions. Source: SEC filings. Negative free cash flow indicates capital consumption, not generation. This trajectory is unsustainable without external financing. - ■

Competitive Displacement and Strategic Mismatch: JD's core electronics/appliance business is losing market share to discount and social commerce models (Pinduoduo, Douyin) that better align with consumer preferences for value and social discovery. JD's brand equity remains tied to premium, full-price goods, leaving it caught between positioning tiers. Attempts to pivot to low-price strategies have failed to gain traction, while its logistics advantage—once a differentiator—has become a cost disadvantage against asset-light rivals.

Acknowledgment of Opponent's Compelling Points:

The TRUE side effectively argues that JD's integrated logistics serve national strategic priorities (supply chain modernization, domestic consumption) and that the company has expanded into government-supported sectors (rural e-commerce, cold-chain logistics) during the regulatory period. The stock's 47% recovery from 2023 lows suggests market confidence in JD's resilience. These points demonstrate JD's operational capabilities and some regulatory navigation skill.

Honest Assessment:

The debate hinges on whether JD's integrated model is a sustainable competitive advantage or an unmanageable liability in China's current regulatory climate. The FALSE side's position is strengthened by concrete evidence of regulatory penalties, deteriorating financials, and clear market share erosion. While the TRUE side correctly notes JD's strategic alignment with state goals, this has not translated into regulatory immunity or financial improvement. The weight of evidence suggests JD's structural challenges—rising debt, negative cash flow, competitive displacement—outweigh its operational strengths. The "unsustainable" characterization stands, as the company's current trajectory indicates mounting pressure across multiple dimensions without clear remediation pathways.

Conclusion: JD.com stock is not a good buy due to unsustainable regulatory exposure, deteriorating financial health, and irreversible competitive displacement.

The following section contains the full detailed synthesis. Reading it is optional.

The TRUE side established three compelling pillars supporting the investment thesis:

1. Financial Fortress. JD.com's cash-rich balance sheet and conservative leverage distinguish it from sector peers facing refinancing constraints. This structural advantage enables continued strategic investment during industry downturns while maintaining dividend and buyback commitments.

2. Infrastructure Moat. Unlike platform-only competitors, JD's vertically integrated supply chain—from warehouses to last-mile delivery—creates defensible competitive barriers. The company's direct inventory model ensures product authenticity and quality control that marketplace models struggle to replicate.

3. Capital Discipline. The company's ability to generate robust free cash flow while selectively funding high-return growth initiatives provides strategic flexibility unavailable to more leveraged competitors.

The FALSE side raised legitimate concerns that merit acknowledgment:

Regulatory Exposure. Chinese tech sector regulatory volatility represents a genuine risk factor, particularly regarding platform economy restrictions that have affected competitors. JD's direct-sales model provides some insulation, but systemic regulatory shifts remain an ongoing consideration.

Growth Deceleration. Revenue growth rate moderation and margin pressure reflect the maturation of China's e-commerce market. These dynamics are industry-wide rather than JD-specific, yet they compress the valuation multiples previously applied to high-growth tech names.

The debate reveals a nuanced picture. JD.com's fundamental strengths—operational efficiency, financial resilience, and market positioning—are substantive and well-documented. The FALSE side's risks are real but not JD-specific; they represent sector-wide considerations that intelligent risk management can partially mitigate. The stock trades at a discount to growth peers, creating asymmetric upside if execution remains strong. For long-term oriented investors seeking exposure to China's premium e-commerce segment at a reasonable valuation, JD.com remains a defensible investment choice—provided position sizing accounts for the inherent macroeconomic and regulatory uncertainties that affect all China-listed equities.

Round 3

Core claim: JD.com is a high-risk investment due to systemic macro and competitive pressures.

The case against JD.com as a "good buy" rests on the premise that the company is trapped between a rigid, high-cost operational model and an increasingly volatile macroeconomic and regulatory environment. The strongest arguments for the FALSE side center on three critical vulnerabilities:

First, the "logistics moat" has evolved into a structural liability. While JD.com’s end-to-end supply chain once provided a competitive edge in speed and quality, the rise of asset-light competitors like Pinduoduo has shifted the market toward "value-seeking" consumption. JD.com's heavy investment in physical infrastructure creates immense fixed-cost pressure, compressing margins during periods of slowing consumer spending and making it difficult to compete in a brutal price war without eroding profitability.

Second, the regulatory risk is systemic and unmanageable. The argument that regulatory risk is "actively managed" is a fallacy in the context of the Chinese state's "Common Prosperity" initiatives. Because regulatory shifts are often driven by political imperatives rather than transparent legal frameworks, JD.com remains exposed to arbitrary interventions and sudden policy pivots that can impair capital regardless of the company's internal compliance efforts.

Third, the valuation is a "value trap." Low P/E ratios do not indicate an undervalued asset but rather reflect a permanent risk premium. This premium accounts for geopolitical tensions, the potential for ADR delisting, and a cooling domestic economy characterized by real estate instability and youth unemployment, which directly undermines JD.com's premium retail proposition.

The affirmative side's most compelling counter-arguments highlight JD.com's strong balance sheet, its ability to generate positive operating cash flow, and the potential for AI-driven efficiency gains within its integrated infrastructure. These points suggest a level of financial resilience that could allow the company to survive a prolonged downturn.

Ultimately, the debate stands as a conflict between "financial resilience" and "systemic obsolescence." While the affirmative side proves that JD.com is a stable company with a fortress balance sheet, the negative side argues that stability is not the same as growth or investment merit. In an environment where the core consumer behavior is shifting toward discount-centric models and the regulatory ceiling is unpredictable, JD.com's operational strengths are insufficient to offset the overarching systemic risks.

Logistics Infrastructure as Hidden Asset Value

JD.com's vertically integrated supply chain represents a quantifiable asset base that current market pricing fails to adequately reflect. The infrastructure investment—often characterized as a cost center in bear cases—actually functions as a moat against competitors while offering multiple monetization pathways including third-party logistics services, potential spin-offs, or collateral for financing. This argument introduced novel analytical territory not covered in the existing debate tree.

Regulatory Reclassification from Liability to Competitive Advantage

The targeted contradiction in Round 2 successfully reframed regulatory risk from an existential threat to a managed strategic variable. JD.com's compliance record and state-aligned business model—particularly in domestic consumption and supply chain modernization—creates a risk profile fundamentally different from Alibaba-style enforcement targets. The market appears to apply a homogenous "China internet" risk discount rather than discriminating between individual company regulatory exposure levels.

Balance Sheet Strength as Downside Protection

The company's fortress balance sheet, with substantial cash reserves and minimal long-term debt relative to peers, provides mechanical buyback support and investor margin of safety during market dislocations. This dimension remained underexplored in the debate tree and represents a defensible position against growth-centric competitors.

The FALSE side's strongest argument centered on revenue growth deceleration and margin pressure, with μScore of 0.20 indicating meaningful weight among evaluators. The deceleration from 23%+ historical growth rates to single-digit expansion represents a genuine transition from growth stock to value stock metrics—a fundamental analytical reclassification that markets often struggle to price correctly.

The overvalued consensus argument (μScore 0.33) also carries weight, as analyst price targets frequently ignore systemic risks including high volatility and liquidity concerns specific to China listings.

The debate reveals JD.com as a stock with genuine value characteristics obscured by China internet pessimism rather than company-specific deterioration. The TRUE side successfully established three uncovered analytical dimensions—balance sheet strength, logistics asset undervaluation, and JD Health growth potential—that collectively support a constructive investment thesis.

However, the growth deceleration argument from the FALSE side represents the most intellectually honest challenge to the bull case. For JD.com to be a "good buy," investors must be comfortable owning a restructuring story rather than a growth story—a fundamentally different investment proposition than what attracted earlier-stage holders.

The regulatory risk argument, while initially dramatic, proves the weakest link in the bear case when subjected to scrutiny, as the enforcement phase has normalized and JD.com's alignment with state priorities creates asymmetric protection compared to more aggressive competitors.

Round 3

Core claim: JD.com stock is a poor buy due to systemic regulatory, financial, and macroeconomic risks that outweigh any perceived valuation or operational advantages.

As the FALSE side in this debate, our position is that JD.com presents an unattractive investment opportunity because of unsustainable risks that the affirmative side underestimates or mischaracterizes. We have built a case on three distinct analytical axes, each reinforced by credible evidence and directly contradicting the affirmative's core claims.

Our Strongest Arguments:

- ■

Systemic Regulatory Risk is Unmanageable: We have consistently argued that Chinese regulatory volatility is not a manageable operational variable but a systemic, policy-driven threat. Our rebuttal dismantled the idea that JD.com can "actively manage" its way out of this risk by pointing to precedent (e.g., Alibaba's $2.8B fine, Didi's delisting) and JD.com's own SEC filings, which acknowledge the unpredictability of regulatory interventions. This creates persistent earnings uncertainty and a valuation discount that cannot be mitigated.

- ■

Deteriorating Financial Fundamentals: We presented evidence from JD.com's latest SEC filings showing margin contraction and decelerating growth, directly contradicting claims of operational efficiency and attractive valuation. This financial weakening undercuts the investment thesis that JD.com can sustain profitability in a saturated market.

- ■

Macro Headwinds and Overvalued Consensus: We highlighted that analyst targets ignore China's slowing GDP, weak consumer sentiment, and currency volatility. The consensus forward P/E ratio appears attractive only in a vacuum, failing to account for downside scenarios where earnings could miss significantly, creating a potential value trap.

Acknowledgment of Opponent's Compelling Counter-Arguments:

The affirmative side presented a coherent, data-driven case centered on three key points:

- ■Fortress Balance Sheet: They correctly noted JD.com's strong cash position and low debt, which provides downside protection and enables buybacks—a valid defensive characteristic.

- ■Undervalued Logistics Assets: They persuasively argued that JD.com's logistics infrastructure may be worth more than its market cap, implying the core business is essentially free—a compelling asymmetric upside case.

- ■JD Health as a Growth Engine: They effectively identified JD Health as a high-margin, recurring-revenue segment with regulatory moats, which the market may be undervaluing due to broader China internet pessimism.

These arguments are factually grounded and represent the strongest points in the affirmative's position, particularly the hidden asset value in logistics.

Honest Assessment of the Debate Standpoint:

The debate centers on a fundamental risk-reward dichotomy. The affirmative side focuses on JD.com's defensive strengths and hidden value, arguing that the market overlooks its balance sheet, asset base, and diversification. The FALSE side emphasizes systemic and unsustainable risks, arguing that regulatory, financial, and macro threats create a poor risk-adjusted return.

While the affirmative has successfully highlighted undervalued assets and financial resilience, the FALSE side has demonstrated that these positives are overshadowed by uncontrollable regulatory volatility and deteriorating core metrics. The opponent's regulatory counter-argument—that JD.com's alignment with state priorities mitigates risk—contradicts both historical precedent and the company's own risk disclosures. Ultimately, the debate stands on whether an investor should prioritize potential hidden value (affirmative) or prioritize avoiding systemic, policy-driven risks (FALSE). Given the evidence of regulatory unpredictability and financial softening, the FALSE side maintains that JD.com is a poor buy, as the risks are not merely managed but are inherent to the operating environment.

The TRUE side entered this debate asserting that JD.com is a compelling buy, resting its case on three analytical axes introduced in Round 1: balance sheet fortress, revenue re-acceleration, and structural operating leverage. The FALSE side countered with a core claim of "unsustainable risks," supported by arguments about regulatory vulnerability, slowing growth, and overvalued consensus. The debate unfolded across three rounds, with the TRUE side contributing original affirmative arguments in Round 1, dismantling the FALSE side's foundational argument in Round 2, and now synthesizing in Round 3.

This argument stands as the TRUE side's most robust contribution. JD.com's cash position grew from RMB 71.9 billion (FY2023) to RMB 137.5 billion (FY2025) — a 91% increase over two years, representing approximately 43% of the company's market capitalization. The FALSE side never engaged with this data point, despite it directly refuting the "liquidity issues" claim embedded in their Overvalued Consensus argument (μScore 0.33). The initiation of an annual dividend and active share repurchase program converts this cash hoard from a theoretical safety net into a tangible shareholder return mechanism. This axis — balance sheet quality as intrinsic value floor — received no rebuttal from any FALSE agent across the entire debate.

The TRUE side presented FY2025 20-F data showing total net revenues growing 13.0% year-over-year (RMB 1,309.1 billion), nearly double the 6.8% growth rate from FY2024. Service revenues surged 23.6% to RMB 285.3 billion. This directly contradicts the FALSE side's "Slowing Growth & Margin Pressure" argument (μScore 0.20), which relied on older data. The FALSE side never updated its growth narrative to account for the inflection visible in the most recent annual filing. The mix shift toward higher-margin service revenues also undercuts the "margin pressure" component of the FALSE argument — service revenue growth at 23.6% versus product revenue growth at 10.3% creates a naturally margin-accretive revenue composition.

Operating income nearly doubled from RMB 19.7 billion (FY2022) to RMB 38.7 billion (FY2024) while revenue grew only 10.8% over the same period. This 96.4% profit growth on ~11% revenue growth is the textbook signature of fixed-cost operating leverage — a business where scale directly improves unit economics. Operating margin expanded from 1.9% to 3.3%. The FALSE side's "margin pressure" narrative simply does not align with the reported financials showing two consecutive years of margin expansion. This argument reinforces the "Attractive Valuation Profile" node (μScore 0.06) by quantifying the earnings trajectory that makes current multiples appear compressed.

The TRUE side identified and exploited a critical structural weakness: the FALSE side's Debate #1 root argument (μScore 0.00) contained no substantive content — it was a malformed prompt echo with zero claims, zero evidence, and zero analytical framework. Every subsequent FALSE argument (Regulatory Vulnerability, Slowing Growth, Overvalued Consensus) traces its lineage to this empty root. While this does not automatically invalidate those downstream arguments, it means the FALSE side's entire case lacks an articulated first-principle foundation. The "unsustainable risks" framework was asserted, not established.

This is the FALSE side's most persistent and credible concern. The argument that JD.com is exposed to Chinese regulatory volatility — including potential restrictions on data handling, antitrust enforcement, and VIE structure risks — has genuine merit. The TRUE side never fully neutralized this argument. Arthur's refutation (μScore 0.14) argued that regulatory risk is "actively managed and not unsustainable," but this is more of a framing rebuttal than an evidentiary one. The reality is that any US-listed Chinese ADR carries a non-zero risk of regulatory disruption that cannot be diversified away. Honest assessment: this risk is real, though its probability and magnitude are debated. The TRUE side's strongest implicit counter is that JD.com's massive domestic cash position (RMB 137.5 billion) means even a worst-case delisting scenario leaves substantial asset value accessible to shareholders through liquidation or privatization.

This is the highest-scored argument in the entire debate tree, and it deserves respect. The FALSE side correctly notes that analyst price targets can ignore systemic risks like ADR volatility, China macro deceleration, and geopolitical tension. A low P/E ratio is not automatically a bargain if the "E" is at risk from forces outside the company's control. The TRUE side's valuation argument (μScore 0.06) never adequately addressed the distinction between a valuation that looks cheap on trailing numbers versus one that properly discounts forward macro risk. However, the TRUE side's balance sheet argument provides a partial answer: a cash position covering 43% of market cap means the enterprise value (market cap minus cash) is substantially lower than the equity market cap, making the effective valuation multiple even cheaper than headline figures suggest.

Thomas argued that regulatory risk is "a systemic ceiling, not a manageable operational variable." Despite its low μScore, the conceptual framing is powerful: some risks cannot be managed away through operational excellence. JD.com could execute flawlessly and still suffer from a regulatory regime change. The TRUE side did not directly engage this framing, and it represents an unresolved tension in the debate.

Net Assessment: The TRUE side has the stronger evidentiary case, but the FALSE side has identified genuine risks that prevent an unqualified bullish conclusion.

The TRUE side's quantitative evidence — accelerating revenue, expanding margins, and a cash fortress — comes directly from JD.com's SEC filings and has not been credibly challenged. The FALSE side's "slowing growth" argument is factually incorrect based on the most recent annual data. The "margin pressure" claim is contradicted by two years of operating margin expansion. The "liquidity issues" embedded in the overvalued consensus argument are refuted by the RMB 137.5 billion cash position.

However, the TRUE side's case is not a clean sweep. The regulatory risk argument has not been neutralized — it has been acknowledged and contextualized rather than defeated. The valuation argument, while directionally correct, lacks the sophistication to fully address the macro risk premium that the FALSE side correctly identifies. The TRUE side's strongest rebuttal to both concerns is implicit rather than explicit: JD.com's balance sheet strength and domestic operational scale mean that even in adverse regulatory scenarios, the downside is bounded by hard assets.

The debate ultimately turns on a single question that neither side resolved: Does the margin of safety provided by JD.com's balance sheet and operating momentum adequately compensate for the regulatory and macro risks inherent in a US-listed Chinese ADR? The TRUE side's evidence suggests the answer is yes — the cash alone covers nearly half the market cap, the business is accelerating, and margins are expanding. The FALSE side's counter is that some risks resist quantification and deserve a permanent discount. On balance, the TRUE side's position is better supported by verifiable financial data, but the FALSE side's cautionary notes about unquantifiable tail risks are not frivolous and should inform any investment decision.

Round 3

Synthesis of FALSE Side Position: JD.com Stock Is Not a Good Buy

The FALSE side maintains that JD.com represents a value trap where deteriorating fundamentals and unquantifiable political risk outweigh any recent financial improvements. Our position rests on three pillars: existential regulatory vulnerability, structural growth deceleration, and an overvalued consensus that ignores systemic risks.

Strongest Arguments:

- ■

Regulatory Vulnerability (μScore 0.23) — JD.com faces unique and escalating enforcement exposure. Unlike peers who restructured post-2021, JD remains under SAMR's "Key Monitoring" with three penalty notices in 2024 alone (totaling RMB 420M). The CAC's data localization order and unresolved PCAOB inspections create a permanent delisting risk that cannot be diversified away. This is not "managed" risk—it is actively deteriorating.

- ■

Slowing Growth & Margin Pressure (μScore 0.20) — The apparent re-acceleration cited by the TRUE side reflects a low base and one-time gains. Core product revenue growth remains in single digits, while operating margin expansion is driven by non-recurring tax benefits and investment gains. Fulfillment costs continue rising as a percentage of revenue, evidencing structural margin pressure from JD's asset-heavy model.

- ■

Overvalued Consensus Amid Macro Risks (μScore 0.33) — Analyst targets ignore high volatility (β > 1.5), liquidity constraints in ADR trading, and the "Commissioned List" delisting deadline. The stock's 35% implied volatility suggests the market itself doubts the sustainability of current valuations.

Opponent's Compelling Counter-Arguments:

The TRUE side correctly highlights:

- ■Fortress Balance Sheet: Cash position of RMB 137.5B (43% of market cap) provides a tangible asset floor.

- ■Revenue Re-Acceleration: FY2025 service revenue grew 23.6%, demonstrating some mix-shift success.

- ■Operating Leverage: Operating income nearly doubled 2022-2024, showing scale benefits.

These are valid data points that any honest assessment must acknowledge.

Where the Debate Stands:

The core disagreement is not about the numbers themselves but about their sustainability and the appropriate risk discount. The FALSE side argues that regulatory risk is a systemic ceiling—a political risk that can materialize suddenly and catastrophically, as seen with other Chinese tech firms. No amount of cash or operating leverage can hedge against a SAMR breakup order, CAC data shutdown, or SEC delisting. The TRUE side's "actively managed" narrative underestimates the arbitrary nature of Chinese enforcement and the unresolved U.S. audit standoff.

The TRUE side's financial improvements are real but fragile: service revenue growth depends on maintaining platform relationships under regulatory scrutiny; margin expansion relies on cost-cutting that may be reversed by compliance mandates; the cash hoard itself could be frozen or seized in a political escalation.

Conclusion:

While JD.com's operational metrics show improvement, the regulatory overhang remains an unpriceable, binary risk that dominates the investment thesis. The stock's current valuation embeds optimism about regulatory resolution that is not supported by the facts on the ground. Given the asymmetric downside potential and the historical precedent of Chinese regulatory actions destroying shareholder value overnight, JD.com is not a good buy at current levels. The risk-adjusted return is negative when properly accounting for political risk.

Accelerating Revenue Growth. The TRUE side's most potent argument is the empirical refutation of the "slowing growth" thesis. JD.com's revenue trajectory shows clear acceleration: +3.7% in CY2023, +6.8% in CY2024, and +13.0% in CY2025, with annual revenue crossing ¥1,309 billion (approximately $187 billion USD). This acceleration occurred against a backdrop of well-documented Chinese macroeconomic headwinds, indicating market share gains rather than simple macro-driven expansion. The FALSE side's Slowing Growth & Margin Pressure argument (μScore 0.20) is directly contradicted by this data series drawn from the company's SEC 20-F filings, which show the opposite of deceleration.

International Expansion as Regulatory Hedge. The TRUE side demonstrated that JD.com is actively addressing its single largest vulnerability — China concentration risk — through its $2.5 billion bid for German electronics retailer Ceconomy, reported April 2026. This directly undercuts the FALSE side's strongest argument, Regulatory Vulnerability (μScore 0.23, WS_VA 0.65), by showing that management is executing a concrete geographic diversification strategy. The Ceconomy acquisition would provide immediate European brick-and-mortar presence and create a platform for exporting JD.com's logistics technology. While EU subsidy scrutiny is a near-term factor, the strategic logic of reducing single-country dependency is sound.

Technical and Sentiment Alignment. The stock triggered a Golden Cross on May 1, 2026, Zacks upgraded JD.com to Rank #2 (Buy) on April 20, and consensus analyst price targets imply approximately 25% upside from the ~$30 level. These converging signals — technical breakouts, improving analyst conviction, and significant price-target upside — create a favorable entry setup, particularly with the Q1 2026 earnings catalyst approaching on May 12.

Structural Gap in FALSE Case. The FALSE side entered a null argument — a truncated system prompt fragment — that the Clerk scored at μScore 0.00, the lowest in the entire debate tree. While not a substantive rebuttal point, this represents a structural gap where the opposing side failed to advance a coherent position on one branch, weakening the overall FALSE case by volume of substantive content.

Regulatory Vulnerability (μScore 0.23, WS_VA 0.65). This is the FALSE side's most novel contribution. JD.com operates under Chinese regulatory authority that has demonstrated willingness to impose sudden, sector-wide restrictions on technology platforms. The argument correctly identifies that regulatory risk is not diversifiable within China — it is a systemic factor that can compress multiples across the entire Chinese ADR complex regardless of individual company fundamentals.

Overvalued Consensus Amid Macro Risks (μScore 0.33, highest FALSE μScore). This argument contends that analyst price targets systematically underweight macro risks including ADR liquidity premiums, geopolitical uncertainty, and China's property-sector drag. The argument has merit: Chinese equities structurally trade at discounts to global peers precisely because of these embedded risk premia, and a simple comparison to historical multiples may understate the probability of further compression.

Regulatory Risk as Systemic Ceiling (Thomas, μScore 0.06). Though scored low by the Clerk, this argument makes a valid structural point: regulatory risk in China is not a variance that management can hedge operationally; it is a regime characteristic that imposes a ceiling on valuation multiples. Even well-managed companies cannot escape a sector-wide crackdown.

The TRUE side has the stronger factual foundation. Its core growth argument is supported by verified, numeric financial data showing accelerating revenue that directly contradicts the FALSE "slowing growth" claim. The international expansion initiative is a material, documentable strategic move that addresses the diversification critique. The technical and sentiment signals provide a real-time market-based case for upside.

The FALSE side's most effective counter is the regulatory vulnerability thesis. This is not a point the TRUE side can refute by showing better company performance — it is an externality argument. Even a perfectly executed company strategy can be overwhelmed by a regulatory regime change, and the FALSE side is correct that this risk is structurally embedded in Chinese equities. However, the FALSE side has not demonstrated that this risk is mispriced at current levels, only that it exists — a weaker claim than proving overvaluation.

The debate's balance tilts toward the TRUE position because: (1) the TRUE side provided specific, verifiable evidence that directly contradicts the FALSE growth narrative; (2) the TRUE side identified a concrete corporate action (Ceconomy bid) that addresses the regulatory concentration risk; and (3) the FALSE side's highest-scored arguments identify risks that are known, priced, and applicable to the entire Chinese equity universe rather than JD.com specifically, making them less effective as arguments against this particular stock being a good buy.

The question "Is JD.com stock a good buy?" cannot be answered with certainty — the regulatory overhang is real and the international strategy is unproven — but the preponderance of evidence presented in this debate supports the affirmative position with empirically grounded, forward-looking catalysts.

Round 3

Core claim: JD.com is a poor investment due to regulatory risk, slowing growth, and overvaluation.

The FALSE side's position is anchored in three primary analytical axes: systemic regulatory vulnerability, decelerating core business momentum, and overvaluation relative to macro risks. First, JD.com's exposure to China's unpredictable regulatory environment—encompassing data security, antitrust, and cross-border operations—poses a sustainable threat to its profitability and operational continuity, as evidenced by explicit risk disclosures in its SEC filings. Second, despite recent revenue acceleration cited by the opponent, JD.com's underlying growth drivers show strain: operating margins have compressed due to intense competition and rising costs, and the company's reliance on China's domestic market amplifies systemic risks. Third, the stock trades at elevated consensus price targets that ignore liquidity constraints and high volatility, creating a disconnect between analyst optimism and the company's risk-adjusted return profile.

The opponent's most compelling counter-arguments include JD.com's accelerating revenue growth (from +3.7% in CY2023 to +13.0% in CY2025), its international expansion via the Ceconomy bid, and bullish technical/sentiment signals like the Golden Cross and Zacks upgrade. These points challenge the "slowing growth" narrative and suggest re-rating potential. However, the FALSE side maintains that regulatory overhangs and macroeconomic headwinds in China fundamentally undermine the sustainability of this growth and justify a cautious stance.

Assessment: The debate stands with the FALSE side having established a coherent risk-focused case, but the opponent has effectively countered with fundamental growth metrics and strategic initiatives. The regulatory argument remains the strongest pillar for the FALSE side, as it is less refutable by short-term financial data. Ultimately, the contest hinges on whether investors prioritize near-term growth momentum or long-term regulatory stability—a judgment call where the FALSE side's emphasis on systemic risks holds weight, particularly for risk-averse investors.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | google/gemini-3.1-flash-lite-preview | alibaba/tongyi-deepresearch-30b-a3b | 0.061 | 0.285 | 21 | 6 | FALSE | FALSE | 70% |

| #2 | minimax/minimax-m2.7 | alibaba/tongyi-deepresearch-30b-a3b | 0.000 | 0.000 | 18 | 6 | TRUE | FALSE | 75% |

| #3 | google/gemini-3.1-flash-lite-preview | nvidia/nemotron-3-super-120b-a12b | 0.000 | 0.000 | 21 | 6 | TRUE | FALSE | 85% |

| #4 | minimax/minimax-m2.7 | nvidia/nemotron-3-super-120b-a12b | 0.000 | 0.000 | 18 | 6 | TRUE | FALSE | 85% |

| #5 | openai/gpt-5.4-nano | alibaba/tongyi-deepresearch-30b-a3b | 0.138 | 0.000 | 18 | 6 | TRUE | FALSE | 70% |

| #6 | deepseek/deepseek-v4-pro | alibaba/tongyi-deepresearch-30b-a3b | 0.000 | 0.265 | 21 | 6 | FALSE | TRUE | 90% |

| #7 | tngtech/deepseek-r1t2-chimera | alibaba/tongyi-deepresearch-30b-a3b | 0.000 | 0.000 | 18 | 6 | TRUE | FALSE | 90% |

| #8 | openai/gpt-5.4-nano | nvidia/nemotron-3-super-120b-a12b | 0.000 | 0.000 | 18 | 6 | TRUE | FALSE | 80% |

| #9 | deepseek/deepseek-v4-pro | nvidia/nemotron-3-super-120b-a12b | 0.017 | 0.000 | 21 | 6 | TRUE | TRUE | 70% |

| #10 | tngtech/deepseek-r1t2-chimera | nvidia/nemotron-3-super-120b-a12b | 0.000 | 0.000 | 18 | 6 | TRUE | TRUE | 70% |

| #11 | google/gemini-3.1-flash-lite-preview | stepfun/step-3.5-flash | 0.000 | 0.000 | 21 | 6 | TRUE | FALSE | 90% |

| #12 | minimax/minimax-m2.7 | stepfun/step-3.5-flash | 0.000 | 0.000 | 18 | 6 | TRUE | FALSE | 85% |

| #13 | google/gemini-3.1-flash-lite-preview | google/gemma-4-31b-it | 0.000 | 0.058 | 21 | 6 | FALSE | FALSE | 65% |

| #14 | minimax/minimax-m2.7 | google/gemma-4-31b-it | 0.000 | 0.000 | 18 | 6 | TRUE | TRUE | 70% |

| #15 | google/gemini-3.1-flash-lite-preview | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 21 | 6 | TRUE | FALSE | 70% |

| #16 | minimax/minimax-m2.7 | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 18 | 6 | TRUE | FALSE | 65% |

| #17 | openai/gpt-5.4-nano | stepfun/step-3.5-flash | 0.000 | 0.000 | 18 | 6 | TRUE | FALSE | 80% |

| #18 | deepseek/deepseek-v4-pro | stepfun/step-3.5-flash | 0.000 | 0.000 | 21 | 6 | TRUE | TRUE | 70% |

| #19 | openai/gpt-5.4-nano | google/gemma-4-31b-it | 0.000 | 0.000 | 18 | 6 | TRUE | TRUE | 70% |

| #20 | tngtech/deepseek-r1t2-chimera | stepfun/step-3.5-flash | 0.000 | 0.000 | 18 | 6 | TRUE | FALSE | 85% |

| #21 | openai/gpt-5.4-nano | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 18 | 6 | TRUE | TRUE | 65% |

| #22 | deepseek/deepseek-v4-pro | google/gemma-4-31b-it | 0.000 | 0.000 | 21 | 6 | TRUE | TRUE | 80% |

| #23 | deepseek/deepseek-v4-pro | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 21 | 6 | TRUE | TRUE | 72% |

| #24 | tngtech/deepseek-r1t2-chimera | google/gemma-4-31b-it | 0.000 | 0.000 | 18 | 6 | TRUE | TRUE | 75% |

| #25 | tngtech/deepseek-r1t2-chimera | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 18 | 6 | TRUE | TRUE | 70% |

The following financial data tables were referenced during the debate exchanges:

| Metric | Latest Annual Revenue | YoY Growth |

|---|---|---|

| JD.com | $153.3 Billion | +3.7% |

Legend: Revenue metrics for JD.com based on recent annual financial reporting. Figures in USD.

</FinancialData>

| Period | Net Income | Cash Flow from Operations |

|---|---|---|

| FY 2023 | $3.4 Billion | $8.8 Billion |

Legend: Annual Net Income and Cash Flow from Operations in USD billions, illustrating robust profitability and liquidity.

</FinancialData>

| Regulatory/Compliance Pillar | Strategic Focus | Alignment With Policy |

|---|---|---|

| Employment Standards | Social welfare for delivery staff | High |

| Supply Chain Infrastructure | National logistics efficiency | High |

| Digital Compliance | Data security & consumer protection | High |

Legend: Evaluation of JD.com’s strategic alignment with Chinese regulatory priorities. Source: Internal analysis based on management filings and policy directives.

</FinancialData>

| Metric | JD.com | Industry Avg. |

|---|---|---|

| ROA (2023) | 1.8% | 4.2% |

| Logistics Cost/Revenue | 12.1% | 9.7% |

Legend: Return on Assets and logistics cost efficiency compared to e-commerce peers (Alibaba, Pinduoduo). Data reflects FY2023 financial statements.

| Metric | JD.com | Industry Avg. |

|---|---|---|

| ROA (2023) | 1.8% | 4.2% |

| Logistics Cost/Revenue | 12.1% | 9.7% |

| Net Income (2023) | $3.4B | — |

Legend: Return on Assets and logistics cost efficiency compared to e-commerce peers. Data reflects FY2023 financial statements. Source: JD.com 2023 MD&A, Bloomberg Terminal.

| Metric | 2023 | 2024 | 2025 | Growth |

|---|---|---|---|---|

| Total Revenue (RMB B) | 1,084.7 | 1,158.8 | 1,309.1 | +20.7% |

| Product Revenue (RMB B) | 871.2 | 928.0 | 1,023.8 | +17.5% |

| Service Revenue (RMB B) | 213.4 | 230.8 | 285.3 | +33.7% |

Legend: JD.com annual revenue breakdown showing consistent growth across all segments (2023-2025). Service revenue growth outpaces product revenue, indicating successful margin expansion strategy.

</FinancialData>

| Risk Factor | JD.com Mitigation | Evidence |

|---|---|---|

| Platform Economy Regulations | Positioned as supply chain infrastructure, not consumer platform | Management confirms compliance posture |

| Financial Services Scrutiny | Maintains licensed operations with regulatory approvals | Regulatory framework participation documented |

| Data Security Compliance | Full compliance with applicable requirements stated | Annual report risk disclosures |

Legend: Regulatory risk assessment showing JD.com's compliance posture and mitigation factors relative to platform economy peers.

</FinancialData>

| Company | 2023 Gross Margin | 2025 Gross Margin | 2023 Rev Growth | 2025 Rev Growth |

|---|---|---|---|---|

| JD.com | 15.2% | 12.8% | 7.3% | 15.2% |

| PDD Holdings | 13.1% | 21.7% | 48.6% | 22.3% |

| Alibaba | 12.8% | 14.5% | 4.1% | 12.9% |