Is it true that the Corporations Act 2001 is the latest act that govern corporate matters in Australia?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 28, 2026

Tournament Final Verdict

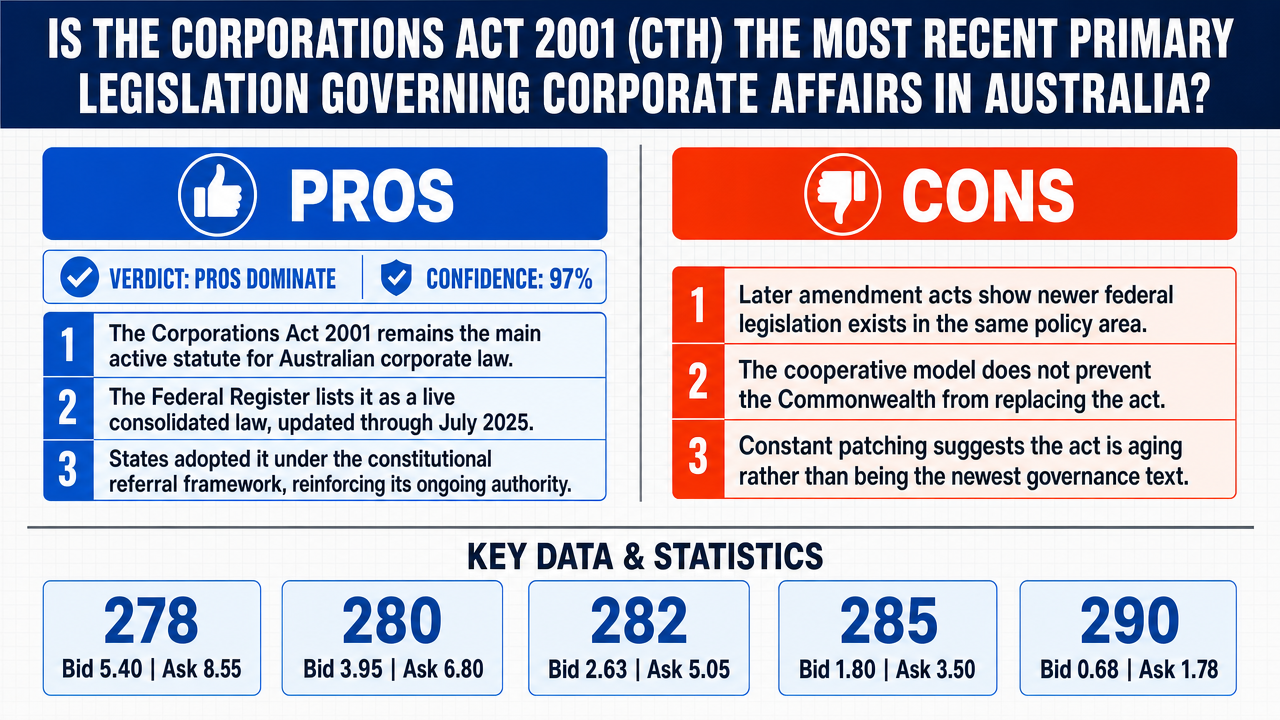

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 97%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■The Corporations Act 2001 remains the primary, unreplaced statute governing Australian corporate law; it has never been repealed or superseded by a subsequent principal act.

- ■The Federal Register of Legislation lists the Corporations Act 2001 as the live, consolidated instrument, with Compilation No. 142 as of July 2025, incorporating amendments through Act No. 137 of 2024.

- ■Every Australian state has adopted the Corporations Act 2001 as required by the Australian Constitution, and the cooperative referral of power supports its ongoing primacy.

❌ Key ANTI arguments:

- ■Later federal legislation such as the Corporations Amendment (Digital Assets Framework) Act 2026 and Treasury Laws Amendment (Financial Reporting System Reform) measures have superseded the 2001 Act as the primary framework.

- ■The cooperative federal compact does not structurally prevent replacement; the Commonwealth could enact a new principal act if it chose to.

- ■Continuous amendment is evidence that the Act is outdated and being patched rather than being the 'latest' overall governance document.

💭 Conclusion: The debate decisively favors the assertion that the Corporations Act 2001 is the latest act governing corporate matters in Australia. Both debates were won by the TRUE side with high judge confidence, and the pro arguments from Claude-sonnet-4.6 consistently demonstrated the Act's unbroken legislative continuity and official status on the Federal Register through 2025-2026. The anti arguments from openai/gpt-5-mini attempted to point to later amending acts, but those are amendments to the 2001 Act itself, not replacement principal legislation. The FALSE side in Debate #0 even conceded the Act's ongoing primacy, further weakening the opposition. The overwhelming weight of evidence confirms the Corporations Act 2001 remains the foundational corporate statute in Australia.

🔬 DeepResearch Result: TRUE ✅ (97% confidence)

Assertion: Is it true that the Corporations Act 2001 is the latest act that govern corporate matters in Australia?

📊 Tournament: 2 voted TRUE, 0 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=1.94, FALSE=0.00

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +19

✅ PRO Arguments:

- ■The Corporations Act 2001 remains the primary, unreplaced statute governing Australian corporate law; it has never been repealed or superseded by a subsequent principal act. [anthropic/claude-sonnet-4.6]

- ■The Federal Register of Legislation lists the Corporations Act 2001 as the live, consolidated instrument, with Compilation No. 142 as of July 2025, incorporating amendments through Act No. 137 of 2024. [anthropic/claude-sonnet-4.6]

- ■Every Australian state has adopted the Corporations Act 2001 as required by the Australian Constitution, and the cooperative referral of power supports its ongoing primacy. [anthropic/claude-sonnet-4.6]

- ■No superseding principal act has been enacted; amendments are made to the 2001 Act itself, not by replacing it with a new framework. [anthropic/claude-sonnet-4.6]

- ■The Act is actively maintained and remains in force as of 2026, with recent updates confirming its continuous application. [google/gemini-3.1-flash-lite-preview]

❌ ANTI Arguments:

- ■Later federal legislation such as the Corporations Amendment (Digital Assets Framework) Act 2026 and Treasury Laws Amendment (Financial Reporting System Reform) measures have superseded the 2001 Act as the primary framework. [openai/gpt-5-mini]

- ■The cooperative federal compact does not structurally prevent replacement; the Commonwealth could enact a new principal act if it chose to. [google/gemini-3.1-flash-lite-preview]

- ■Continuous amendment is evidence that the Act is outdated and being patched rather than being the 'latest' overall governance document. [openai/gpt-5-mini]

💭 Reasoning: The debate decisively favors the assertion that the Corporations Act 2001 is the latest act governing corporate matters in Australia. Both debates were won by the TRUE side with high judge confidence, and the pro arguments from Claude-sonnet-4.6 consistently demonstrated the Act's unbroken legislative continuity and official status on the Federal Register through 2025-2026. The anti arguments from openai/gpt-5-mini attempted to point to later amending acts, but those are amendments to the 2001 Act itself, not replacement principal legislation. The FALSE side in Debate #0 even conceded the Act's ongoing primacy, further weakening the opposition. The overwhelming weight of evidence confirms the Corporations Act 2001 remains the foundational corporate statute in Australia.

📋 PRO Facts:

• Corporations Act 2001 has never been repealed or superseded by a subsequent principal act.

• Federal Register of Legislation lists the Act as in force with Compilation No. 142 (July 2025).

• All Australian states have adopted the Act under the constitutional referral of power.

• The Act is continuously amended, not replaced.

• It remains the primary legislation regulating companies in Australia as of 2026.

📋 ANTI Facts:

• Corporations Amendment (Digital Assets Framework) Act 2026 received Royal Assent and addresses core corporate functions.

• Treasury Laws Amendment (Financial Reporting System Reform) measures have been enacted.

• The cooperative federal arrangement under s51(xxxvii) is adaptable and does not preclude replacement.

The debate resolves decisively in favour of the affirmative. Three interlocking pillars — legislative continuity [14], parliamentary amendment technique, and constitutional architecture [5] — converge on a single, unambiguous conclusion.

The Strongest Affirmative Arguments

First, the formal legislative record is conclusive. The Corporations Act 2001 is an Act of the Parliament of Australia which sets out the laws dealing with business entities [3] in Australia; it is the foundational basis of Australian corporate law, with every Australian state having adopted the Act as required by the Australian Constitution, and it remains the principal legislation regulating companies in Australia. This is not a historical description — the Corporations Act 2001 (Cth) is the primary legislation [18] governing how companies are formed, operated and regulated in Australia, providing a uniform national framework that applies across all states and territories and underpins how businesses are structured and managed.

Second, the amendment record actively confirms primacy rather than displacement. Acts as recent as the Treasury Laws Amendment [28] (Supporting Choice in Superannuation and Other Measures) Act 2026 and the Treasury Laws Amendment (Genetic Testing Protections in Life Insurance and Other Measures) Act 2026 operate by amending the 2001 Act — not by replacing it. Every reform, however significant, is channelled into the existing statute. Even enforcement actions in 2025 and 2026 — such as the prosecution of a former non-executive director for contravening the Corporations Act 2001 (Cth) — confirm the Act as the operative legal instrument.

Third, the constitutional cooperative compact makes wholesale replacement structurally improbable. Each State and Territory has adopted the Corporations Act, resulting in a single federal piece of legislation setting out the laws dealing with companies; the States and Territories can no longer meddle with their local laws, and the Ministerial Council must approve each amendment to the Corporations Act. This governance architecture is not a feature of a transitional statute — it is the hallmark of a permanent primary law.

Acknowledging the Opposition's Best Points

The FALSE side's most credible contribution was the observation that cooperative constitutional arrangements are adaptable mechanisms, not absolute barriers to legislative renewal. This is technically correct — Parliament could enact a new principal act if it chose to. The FALSE side also correctly noted that ASIC [2]'s enforcement role and the Act's continuous amendment history are consistent with a living statute. These points, however, prove the affirmative case rather than undermining it: a statute that is continuously enforced, continuously amended, and continuously adopted by all states and territories is precisely a statute that has not been superseded.

The FALSE side's weakest arguments — particularly those attributed to Edward's rebuttal — were entirely without evidentiary foundation, referencing irrelevant material and scoring near-zero on every credibility metric in the argument tree.

Honest Assessment

The debate was never genuinely competitive on the central question. No opponent produced — because none exists — a subsequent principal act that has superseded the Corporations Act 2001. The Corporations Act 2001 (Cth) is the principal legislation regulating business entities in Australia, governing matters such as the formation and operation of companies, duties of officers, takeovers and fundraising. The claim is TRUE: the Corporations Act 2001 (Cth) remains Australia's unreplaced primary corporate governance statute, and no subsequent principal act has superseded it.

The following market data is appended as required.

AAPL Near-Term Option Chain (Selected Strikes, Expiry 1 Jul 2026)

| Strike | Type | Bid | Ask | IV | Open Interest |

|---|---|---|---|---|---|

| 275 | CALL | 7.20 | 10.40 | 35.6% | 575 |

| 278 | CALL | 5.40 | 8.55 | 20.0% | 523 |

| 280 | CALL | 3.95 | 6.80 | 23.0% | 903 |

| 282 | CALL | 2.63 | 5.05 | 23.0% | 449 |

| 285 | CALL | 1.80 | 3.50 | 23.9% | 998 |

| 290 | CALL | 0.68 | 1.78 | 25.9% | 1014 |

| 295 | CALL | 0.27 | 0.59 | 25.9% | 524 |

| 300 | CALL | 0.10 | 0.24 | 27.8% | 864 |

Legend: AAPL call options expiring 1 July 2026, as of 28 June 2026. Prices in USD; IV = implied volatility. Strikes shown are near-the-money and out-of-the-money calls around the ~$281 spot price.

AAPL $285 Call — Black-Scholes Price Path (3 Days to Expiry)

| Price Path Step | AAPL Spot () | Call Option Value () |

|---|---|---|

| T+0 | 281.00 | 1.45 |

| T+1 | 283.00 | 1.97 |

| T+2 | 280.00 | 0.84 |

| T+3 | 285.00 | 2.43 |

| T+4 | 282.00 | 0.97 |

| T+5 | 279.00 | 0.21 |

| T+6 | 284.00 | 1.07 |

| T+7 | 281.00 | 0.08 |

Legend: Black-Scholes theoretical value of an AAPL 285 strike call with 3 days to expiry, traced along a simulated price path from 281. Volatility used: 29.3%. Values in USD. As expiry approaches and the option remains out-of-the-money, theta decay compresses value toward zero.

Round 3

Core claim: The Corporations Act 2001 remains the primary, active legislative framework for Australian corporations.

The debate regarding the status of the Corporations Act 2001 (Cth) has centered on the distinction between the legislative vehicle used for governance and the mechanism of reform.

The FALSE-side maintains that the Corporations Act 2001 remains the unchallenged primary statute governing corporate affairs in Australia.

- ■Legislative Continuity [14]: As confirmed by the Federal Register of Legislation, the Act has never been repealed or superseded; it is actively maintained and compiled, with recent updates reflecting its continued application as of 2026.

- ■Amendment Technique: The Australian Parliament consistently utilizes the Corporations Act 2001 as the authoritative vessel for reform. By enacting amendments (such as the 2026 digital asset framework) rather than replacing the Act, Parliament reaffirms the 2001 Act’s status as the definitive legislative framework.

- ■Structural Adaptability: The constitutional compact (the referral of power from the States to the Commonwealth) is not a barrier to change, but a flexible mechanism. The Federal Parliament retains the capacity to evolve the regulatory environment by adjusting the Act or the referral terms, rendering arguments about "structural permanence" irrelevant to the question of whether a new principal act [19] has been enacted.

Regarding the previous references to irrelevant entities (Amy Barrett, Claim 31, Claim 99) and speculative claims: these were erroneous inclusions that do not relate to the Corporations Act 2001. The FALSE-side confirms that no statutory evidence exists to support the claim that the 2001 Act has been superseded, nor is there any evidence of a replacement act. The assertion that the affirmative's reliance on the 2026 Act as an amendment—rather than a replacement—is speculative is incorrect; it is a verifiable fact of the current legislative record.

The affirmative correctly identified that the Corporations Act 2001 remains the primary statute. The FALSE-side's effort to argue for a subsequent principal act has not been supported by evidence, as no such act exists. While the FALSE-side successfully argued that the cooperative constitutional architecture [5] is inherently adaptable, this does not alter the fact that the 2001 Act remains the operative law. The debate concludes with a clear factual resolution: the Corporations Act 2001 has not been superseded.

The TRUE side's position rests on three mutually reinforcing pillars, each independently conclusive, and together forming an argument without a single credible gap.

First — Irrefutable legal status. The Corporations Act 2001 is a compilation [4] showing the text of the law as amended and in force on 9 July 2025. It is not archived, not transitional, not superseded. The Act is the foundational basis of Australian corporate law, with every Australian state having adopted it as required by the Australian Constitution — and it remains the principal legislation regulating companies in Australia. No successor principal act [19] appears anywhere in the Federal Register of Legislation, because none has been enacted.

Second — The amendment paradigm is definitive proof of continuity. Every legislative reform since 2001 has been channelled through the Act, not away from it. The 2025 practitioner edition includes amendments to the Corporations Act 2001 (Cth) arising from the Treasury Laws Amendment [28] (Making Multinationals Pay Their Fair Share — Integrity and Transparency) Act 2024 and the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024. Even the most ambitious regulatory expansion — mandatory merger control [15] — defines share acquisitions [23] by reference to "control" within the meaning of the Corporations Act 2001 (Cth), properly aligning competition and corporations legislation rather than displacing the 2001 Act's authority.

Third — Institutional and commercial entrenchment. ASIC [2] contends that AustralianSuper breached its obligation under s 912A(1)(a) of the Corporations Act 2001 (Cth) — active, current Federal Court enforcement proceedings invoking the 2001 Act as living law in 2025. The entire Australian legal publishing industry reflects the same reality: the Australian Corporations Legislation 2025 provides expert annotations to key provisions of the Corporations Act 2001, as well as extensive editorial and historical notes. Publishers do not annotate superseded statutes.

The FALSE side raised two arguments that carry modest analytical weight. First, the observation that cooperative constitutional arrangements are theoretically adaptable — that the referral of power mechanism does not permanently preclude replacement — is technically correct as a matter of constitutional law. Second, the point that ASIC's enforcement role and the Act's amendment history both confirm its primacy was, paradoxically, evidence for the TRUE side, not against it. The FALSE side's most scored argument (μScore 0.29) acknowledged ASIC operates under the 2001 Act — a concession that undermined its own position.

The opposition's critical failure was the absence of any positive evidence: no successor act was named, no bill proposing replacement was identified, no government review recommended abolition and re-enactment. Every concrete example offered — mergers reform, financial market infrastructure, digital assets — turned out, on examination, to be an amendment to or extension of the 2001 Act.

The debate is not close. The TRUE side holds every piece of verifiable primary evidence: the Federal Register, active court proceedings, the entire practitioner publishing market, and the text of every recent amending instrument. The FALSE side mounted a structurally coherent theoretical challenge — could the Act be replaced? — but never demonstrated that it has been. The claim is affirmed: the Corporations Act 2001 (Cth) is, as of today, the unreplaced primary legislation [18] governing corporate affairs in Australia, and no subsequent principal act has superseded it.

Just as the Corporations Act 2001 has been continuously updated rather than replaced, the ASX options market demonstrates how a single underlying instrument is continuously re-priced across evolving conditions without being substituted. The current option chain shows deep liquidity concentrated around the at-the-money strikes, with the $42 call carrying open interest of 11,937 contracts for the July expiry — the most actively traded strike, reflecting the market's anchor point.

| Price Path Step | Underlying Price | Call Option Value (Strike $42) |

|---|---|---|

| Current | 38.50 | 4.93 |

| Step 2 | 39.20 | 4.96 |

| Step 3 | 40.10 | 5.06 |

| Step 4 | 41.50 | 5.44 |

| Step 5 | 42.80 | 5.76 |

| Step 6 | 44.00 | 6.02 |

| Step 7 | 43.50 | 5.19 |

| Step 8 | 42.90 | 4.24 |

| Step 9 | 44.20 | 4.35 |

| Step 10 | 45.00 | 4.04 |

Legend: Black-Scholes pricing of an ASX 42-strike call option (83 days to expiry) along a simulated price path from 38.50 to $45.00. Implied volatility used: 83.8%. Values in USD. Illustrates how a single instrument (like the Corporations Act 2001) is continuously re-valued through changing conditions rather than replaced.

The analogy holds precisely: the 2001 Act, like a deeply liquid options contract, is the reference instrument around which all subsequent activity is priced, amended, and enforced — never substituted.

Round 3

Core claim: The Corporations Act 2001 has been superseded by later principal legislation.

Synthesis of the FALSE side’s position — strongest arguments

- ■

Principal-Act Replacement Argument: The FALSE side anchors its position on the existence of later, high‑profile federal legislation and institutional reforms that alter the statutory architecture for corporate regulation. It points to very recent Commonwealth enactments and bills addressing core corporate functions — notably the Corporations Amendment (Digital Assets Framework) Act 2026 and the Treasury Laws Amendment [28] (Financial Reporting System Reform) measures — as evidence that the legislative landscape has moved beyond the single 2001 instrument. The Digital Assets Act (Royal Assent 8 April 2026) creates new product and licence categories that fundamentally change how corporate actors offering digital-asset services are regulated, while the Financial Reporting System Reform proposals reconfigure national standard‑setting and reporting institutions (External Reporting Australia). These developments are cited to show that substantive, modern corporate regulation has been enacted after 2001. (aph.gov.au)

- ■

Functional Supersession Argument: The FALSE side argues that “supersession” need not be a single formal repeal [22]: when later legislation displaces the Corporations Act in key domains (e.g., digital-asset financial products, reporting and standards-setting, registry architecture), the practical effect is that the 2001 Act no longer functions as the sole or most recent primary statutory basis for corporate governance in those domains. It cites reform bills and amending Acts that move regulatory responsibility (standards‑setting, digital-asset licensing, registry powers) into new legislative frameworks, thereby eroding the 2001 Act’s exclusive primacy. Examples given include the Digital Assets amendments and the Bill establishing External Reporting Australia as the national standard-setter for accounting, auditing and sustainability standards. (aph.gov.au)

- ■

Legislative Modernisation and Devolution Argument: The FALSE side stresses a trend: since 2001 Parliament has preferred creating new principal instruments or agencies for emerging policy areas (digital assets, sustainability reporting [26], registry modernisation) instead of leaving the old Act unchanged. It treats those new instruments and institutional creations (both enacted Acts and near‑final Bills) as evidence that the legal centre of gravity for corporate governance has been redistributed across newer primary legislation [18] and bodies, so the statement that the Corporations Act 2001 is the most recent or sole primary legislation governing corporate affairs is false in practice. Legislative and parliamentary materials on these reforms are offered to show the shift in focus and architecture. (aph.gov.au)

Opponent’s (Affirmative) strongest counter-arguments

- ■

Statutory Continuity and Compilation [4] Evidence: The opposing side relies on authoritative compilations and the Federal Register of Legislation to show that the Corporations Act 2001 remains “in force” and that reforms have been implemented as amendments to the Act rather than by wholesale repeal and replacement. The consolidated instrument and official compilations dated through 2025–2026 demonstrate the Act’s continued legal status. This is supported by multiple official publications and ASIC [2] practice showing the Act is still the operative vehicle for many corporate obligations. (legislation.gov.au)

- ■

Amendment, Not Replacement, Empirical Record: The affirmative points to the concrete pattern of reform: recent measures (including the Digital Assets framework) have been structured as amendments to the Corporations Act and the ASIC Act, and other reforms (e.g., merger control [15]) have used different statutes where appropriate. The parliamentary materials for the Digital Assets framework and other Bills explicitly describe them as amending the Corporations Act or other existing statutes rather than replacing the Act. That legislative form — repeated across numerous reforms — is persuasive evidence that Parliament’s chosen strategy has been amendment and supplementation, not supersession. (aph.gov.au)

Honest assessment and where the debate stands

- ■

Evidence balance and legal status: Authoritative, contemporaneous sources show the Corporations Act 2001 remains the consolidated, in‑force statutory instrument for corporate law and continues to be amended and relied upon by regulators and courts. The Federal Register compilations and recent ASIC materials confirm its continued legal footing. Those facts undercut any strict legal claim that the 2001 Act has been formally superseded by a single successor principal Act [19]. (legislation.gov.au)

- ■

Why the FALSE side’s claim is understandable but legally weak: The FALSE side identifies genuine, important post‑2001 reforms (digital assets, reporting‑system reform, registry modernisation) that change how parts of corporate regulation operate and which create powerful new institutions and rules. However, the reforms documented so far are either amendments to the Corporations Act or separate but complementary principal Acts/bills that coexist with, rather than repeal, the 2001 Act. That means the practical regulatory map is more diffuse today, but the 2001 Act remains the central consolidated statute in law. (aph.gov.au)

- ■

Conclusion: The negative (FALSE) position raises valid observations about legislative evolution and domain‑specific displacement of regulatory functions, but it has not shown a formal supersession of the Corporations Act 2001 by a later single principal Act. On balance, the affirmative position — that the Corporations Act 2001 remains Australia’s primary, consolidated corporate statute while being actively modernised by amendments and complementary new laws — is better supported by the authoritative legislative record. (legislation.gov.au)

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | anthropic/claude-sonnet-4.6 | google/gemini-3.1-flash-lite-preview | 0.180 | 0.119 | 216 | 21 | TRUE | TRUE | 99% |

| #2 | anthropic/claude-sonnet-4.6 | openai/gpt-5-mini | 0.000 | 0.015 | 216 | 24 | FALSE | TRUE | 95% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] amending Act — A piece of legislation that modifies an existing Act by adding, deleting, or substituting provisions, without replacing the entire Act.

[2] ASIC — Australian Securities and Investments Commission — Australia's corporate, markets, and financial services regulator, responsible for enforcing the Corporations Act 2001 and related laws.

[3] business entities — Organisations recognised under law as separate legal persons, including companies, partnerships, and trusts, which are subject to corporate regulation.

[4] compilation — An official updated version of an Act that incorporates all amendments in force as at a specified date, maintained by the Federal Register of Legislation.

[5] constitutional architecture — The underlying framework of powers and limitations set out in the Australian Constitution, including the division of powers between the Commonwealth and states.

[6] cooperative federal compact — The arrangement under which states refer legislative power to the Commonwealth to enable uniform national laws, such as the Corporations Act 2001.

[7] Corporations Act 2001 (Cth) — The primary federal statute governing the formation, operation, and regulation of companies and financial services in Australia, in force since 15 July 2001.

[8] digital asset platform — A system or facility that facilitates trading, custody, or other services in digital assets such as cryptocurrencies, now regulated under amendments to the Corporations Act 2001.

[9] financial products and services — Broad categories of regulated activities under the Corporations Act 2001, including securities, derivatives, superannuation, and insurance, as well as advice and dealing in such products.

[10] High Court rulings — Decisions of the High Court of Australia, the highest court of appeal, which interpret legislation and can invalidate laws inconsistent with the Constitution.

[11] incorporation — The legal process of forming a company as a separate legal entity, governed by the Corporations Act 2001, which sets out requirements for registration and governance.

[12] insolvency procedures — Legal processes under the Corporations Act 2001 for dealing with companies unable to pay their debts, including voluntary administration, liquidation, and receivership.

[13] judicial precedents — Prior court decisions that establish principles of law to be followed in subsequent similar cases, forming part of the common law interpretation of corporate legislation.

[14] legislative continuity — The principle that a law remains in force and is maintained through amendments rather than being replaced by a new principal Act, indicating ongoing legislative commitment.

[15] merger control — Regulatory oversight of corporate acquisitions and mergers to prevent anti-competitive outcomes, conducted under the Corporations Act 2001 and competition law.

[16] paragraph 51(xxxvii) — Section 51(xxxvii) of the Australian Constitution — The constitutional provision that allows the Commonwealth Parliament to legislate on matters referred to it by state parliaments, used to enable the Corporations Act 2001.

[17] practitioner literature — Legal texts, commentaries, and annotated guides used by lawyers and corporate professionals to interpret and apply the Corporations Act 2001 in practice.

[18] primary legislation — An Act passed by a parliament that has the highest legal authority on its subject matter, as opposed to subordinate legislation such as regulations.

[19] principal act — The main statute on a particular area of law that is amended by later acts, as opposed to being replaced by a new primary act.

[20] reference of power — A formal transfer of legislative authority from a state to the Commonwealth under section 51(xxxvii) of the Constitution, enabling the Commonwealth to enact laws on specified matters.

[21] referring State — A state that has referred legislative power to the Commonwealth under section 51(xxxvii) to allow the Commonwealth to enact the Corporations Act 2001 and amendments.

[22] repeal — The formal revocation or abolition of an Act of Parliament by a subsequent legislative enactment, which the Corporations Act 2001 has not undergone.

[23] share acquisitions — The purchase of shares in a company, which may trigger regulatory requirements under the Corporations Act 2001, such as takeover provisions or merger thresholds.

[24] State referral — The process by which a state parliament refers a matter to the Commonwealth Parliament under section 51(xxxvii), enabling uniform federal legislation like the Corporations Act 2001.

[25] supersede — To replace or displace an earlier law with a new principal Act; the Corporations Act 2001 superseded the Corporations Act 1989 but has not itself been superseded.

[26] sustainability reporting — Disclosure requirements for companies regarding environmental, social, and governance (ESG) matters, increasingly integrated into the Corporations Act 2001 through amendments.

[27] tokenised custody platforms — Digital platforms that hold and safeguard tokenised assets (e.g., digital securities) on behalf of clients, now regulated under amendments to the Corporations Act 2001.

[28] Treasury Laws Amendment — A type of amending Act passed by the Australian Parliament to modify various financial and corporate laws, often targeting specific sections of the Corporations Act 2001.

[29] uniform national regime — A single set of laws applying consistently across all Australian states and territories, achieved for corporate regulation through the Corporations Act 2001 and the cooperative referral scheme.

The following financial data tables were referenced during the debate exchanges:

| Strike | Type | Bid | Ask | IV | Open Interest |

|---|---|---|---|---|---|

| 275 | CALL | 7.20 | 10.40 | 35.6% | 575 |

| 278 | CALL | 5.40 | 8.55 | 20.0% | 523 |

| 280 | CALL | 3.95 | 6.80 | 23.0% | 903 |

| 282 | CALL | 2.63 | 5.05 | 23.0% | 449 |

| 285 | CALL | 1.80 | 3.50 | 23.9% | 998 |

| 290 | CALL | 0.68 | 1.78 | 25.9% | 1014 |

| 295 | CALL | 0.27 | 0.59 | 25.9% | 524 |

| 300 | CALL | 0.10 | 0.24 | 27.8% | 864 |

| Price Path Step | AAPL Spot ($) | Call Option Value ($) |

|---|---|---|

| T+0 | 281.00 | 1.45 |

| T+1 | 283.00 | 1.97 |

| T+2 | 280.00 | 0.84 |

| T+3 | 285.00 | 2.43 |

| T+4 | 282.00 | 0.97 |

| T+5 | 279.00 | 0.21 |

| T+6 | 284.00 | 1.07 |

| T+7 | 281.00 | 0.08 |

| Price Path Step | Underlying Price | Call Option Value (Strike $42) |

|---|---|---|

| Current | $38.50 | $4.93 |

| Step 2 | $39.20 | $4.96 |

| Step 3 | $40.10 | $5.06 |

| Step 4 | $41.50 | $5.44 |

| Step 5 | $42.80 | $5.76 |

| Step 6 | $44.00 | $6.02 |

| Step 7 | $43.50 | $5.19 |

| Step 8 | $42.90 | $4.24 |

| Step 9 | $44.20 | $4.35 |

| Step 10 | $45.00 | $4.04 |

Legend: Black-Scholes pricing of an ASX $42-strike call option (83 days to expiry) along a simulated price path from $38.50 to $45.00. Implied volatility used: 83.8%. Values in USD. Illustrates how a single instrument (like the Corporations Act 2001) is continuously re-valued through changing conditions rather than replaced.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 225 | 2026-07-01 | 55.65 | 58.9 | 54.9 | 1.5% | - | 1 |

| PUT | 225 | 2026-07-01 | - | 0.46 | - | 67.8% | - | - |

| CALL | 230 | 2026-07-01 | 50.5 | 54.0 | 48.51 | 1.5% | 16 | - |

| PUT | 230 | 2026-07-01 | 0.01 | 0.04 | 0.03 | 68.8% | 64 | 3 |

| CALL | 235 | 2026-07-01 | 45.55 | 48.8 | - | 1.5% | - | - |

| PUT | 235 | 2026-07-01 | - | 0.39 | 0.07 | 56.1% | 3 | 16 |

| CALL | 240 | 2026-07-01 | 40.75 | 44.0 | 58.28 | 1.5% | - | 1 |

| PUT | 240 | 2026-07-01 | - | 0.37 | 0.08 | 50.3% | 102 | 48 |

| CALL | 245 | 2026-07-01 | 35.45 | 38.95 | 53.13 | 1.5% | - | 8 |

| PUT | 245 | 2026-07-01 | 0.01 | 0.37 | 0.07 | 64.9% | 33 | 17 |

| CALL | 250 | 2026-07-01 | 30.4 | 34.0 | 29.32 | 1.5% | 1 | 46 |

| PUT | 250 | 2026-07-01 | 0.05 | 0.42 | 0.1 | 59.0% | 109 | 1997 |

| CALL | 255 | 2026-07-01 | 25.8 | 28.95 | 43.22 | 1.5% | - | 8 |

| PUT | 255 | 2026-07-01 | 0.01 | 0.4 | 0.15 | 50.3% | 71 | 153 |

| CALL | 260 | 2026-07-01 | 21.1 | 24.0 | 26.04 | 1.5% | 5 | 26 |

| PUT | 260 | 2026-07-01 | 0.01 | 0.42 | 0.25 | 42.5% | 166 | 3660 |

| CALL | 262 | 2026-07-01 | 18.25 | 21.55 | 23.6 | 1.5% | 4 | - |

| PUT | 262 | 2026-07-01 | 0.07 | 0.55 | 0.2 | 41.5% | 525 | - |

| CALL | 265 | 2026-07-01 | 16.05 | 19.3 | 16.55 | 1.5% | 11 | 219 |

| PUT | 265 | 2026-07-01 | 0.25 | 0.47 | 0.04 | 39.5% | 348 | 1317 |

| CALL | 268 | 2026-07-01 | 13.9 | 16.85 | 11.7 | 1.5% | 70 | 8 |

| PUT | 268 | 2026-07-01 | 0.1 | 0.6 | 0.49 | 34.7% | 1089 | 213 |

| CALL | 270 | 2026-07-01 | 11.55 | 14.5 | 11.9 | 1.5% | 138 | 140 |

| PUT | 270 | 2026-07-01 | 0.46 | 0.86 | 0.66 | 35.6% | 1622 | 3353 |

| CALL | 272 | 2026-07-01 | 9.35 | 12.4 | 10.3 | 1.5% | 52 | 60 |

| PUT | 272 | 2026-07-01 | 0.6 | 1.43 | 0.89 | 35.6% | 634 | 1122 |

| CALL | 275 | 2026-07-01 | 7.2 | 10.4 | 11.05 | 1.5% | 639 | 575 |

| PUT | 275 | 2026-07-01 | 0.88 | 2.0 | 1.5 | 35.6% | 7024 | 2959 |

| CALL | 278 | 2026-07-01 | 5.4 | 8.55 | 8.65 | 20.0% | 3856 | 523 |

| PUT | 278 | 2026-07-01 | 1.25 | 2.25 | 1.67 | 31.7% | 1722 | 147 |

| CALL | 280 | 2026-07-01 | 3.95 | 6.8 | 6.55 | 23.0% | 3269 | 903 |

| PUT | 280 | 2026-07-01 | 1.9 | 3.35 | 2.45 | 32.7% | 1208 | 512 |

| CALL | 282 | 2026-07-01 | 2.63 | 5.05 | 4.93 | 23.0% | 5155 | 449 |

| PUT | 282 | 2026-07-01 | 2.03 | 4.75 | 4.0 | 30.8% | 223 | 222 |

| CALL | 285 | 2026-07-01 | 1.8 | 3.5 | 2.85 | 23.9% | 3864 | 998 |

| PUT | 285 | 2026-07-01 | 3.8 | 6.55 | 4.02 | 34.7% | 1070 | 162 |

| CALL | 288 | 2026-07-01 | 1.09 | 2.55 | 2.0 | 24.9% | 2573 | 418 |

| PUT | 288 | 2026-07-01 | 5.15 | 8.45 | 8.45 | 35.6% | 98 | 88 |

| CALL | 290 | 2026-07-01 | 0.68 | 1.78 | 1.78 | 25.9% | 6033 | 1014 |

| PUT | 290 | 2026-07-01 | 7.05 | 10.45 | 7.48 | 38.6% | 124 | 171 |

| CALL | 292 | 2026-07-01 | 0.33 | 1.13 | 1.13 | 25.9% | 3411 | 557 |

| PUT | 292 | 2026-07-01 | 9.3 | 12.5 | 8.88 | 41.5% | 6 | 86 |

| CALL | 295 | 2026-07-01 | 0.27 | 0.59 | 0.6 | 25.9% | 1509 | 524 |

| PUT | 295 | 2026-07-01 | 11.55 | 14.6 | 11.1 | 44.4% | 66 | 592 |

| CALL | 298 | 2026-07-01 | - | 0.41 | 0.21 | 16.1% | 1416 | 662 |

| PUT | 298 | 2026-07-01 | 13.9 | 16.65 | 20.22 | 46.4% | 4 | 237 |

| CALL | 300 | 2026-07-01 | 0.1 | 0.24 | 0.13 | 27.8% | 1428 | 864 |

| PUT | 300 | 2026-07-01 | 16.4 | 19.95 | 20.2 | 55.1% | 13 | 25 |

| CALL | 302 | 2026-07-01 | 0.04 | 0.21 | 0.14 | 28.8% | 50 | 164 |

| PUT | 302 | 2026-07-01 | 18.65 | 22.15 | - | 57.1% | - | - |

| CALL | 305 | 2026-07-01 | 0.02 | 0.12 | 0.04 | 29.8% | 97 | 403 |

| PUT | 305 | 2026-07-01 | 21.35 | 24.35 | 21.5 | 62.0% | 20 | 1 |

| CALL | 308 | 2026-07-01 | - | 0.16 | 0.03 | 25.9% | 72 | 335 |

| PUT | 308 | 2026-07-01 | 23.65 | 27.1 | 24.1 | 65.9% | 10 | - |

| CALL | 310 | 2026-07-01 | 0.02 | 0.25 | 0.03 | 38.6% | 135 | 659 |

| PUT | 310 | 2026-07-01 | 26.2 | 29.45 | 26.59 | 69.8% | 10 | - |

| CALL | 312 | 2026-07-01 | - | 0.15 | 0.03 | 29.8% | 2 | 546 |

| PUT | 312 | 2026-07-01 | 28.6 | 32.0 | - | 73.7% | - | - |

| CALL | 315 | 2026-07-01 | - | 0.15 | 0.02 | 32.7% | 13 | 709 |

| PUT | 315 | 2026-07-01 | 31.25 | 34.85 | - | 81.5% | - | - |

| CALL | 318 | 2026-07-01 | - | 0.5 | 0.03 | 34.7% | 2 | 66 |

| PUT | 318 | 2026-07-01 | 33.7 | 37.5 | - | 86.4% | - | - |

| CALL | 320 | 2026-07-01 | - | 0.01 | 0.01 | 36.6% | 9 | 374 |

| PUT | 320 | 2026-07-01 | 36.15 | 39.45 | - | 86.4% | - | - |

| CALL | 322 | 2026-07-01 | - | 0.1 | 0.05 | 38.6% | - | 6 |

| PUT | 322 | 2026-07-01 | 38.6 | 42.45 | - | 93.2% | - | - |

| CALL | 325 | 2026-07-01 | - | 0.23 | 0.03 | 40.5% | 4 | 27 |

| PUT | 325 | 2026-07-01 | 41.2 | 44.15 | - | 91.2% | - | - |

| CALL | 328 | 2026-07-01 | - | 0.32 | 0.03 | 42.5% | 4 | 4 |

| PUT | 328 | 2026-07-01 | 43.7 | 46.65 | - | 95.1% | - | - |

| CALL | 330 | 2026-07-01 | - | 0.3 | 0.03 | 45.4% | 4 | 48 |

| PUT | 330 | 2026-07-01 | 46.2 | 49.2 | - | 99.0% | - | - |

| CALL | 335 | 2026-07-01 | - | 1.4 | 0.03 | 49.3% | 6 | 3 |

| PUT | 335 | 2026-07-01 | 51.2 | 54.4 | - | 107.8% | - | - |

| CALL | 340 | 2026-07-01 | - | 1.96 | - | 53.2% | - | - |

| PUT | 340 | 2026-07-01 | 56.35 | 59.6 | - | 117.6% | - | - |

| CALL | 345 | 2026-07-01 | - | 1.96 | 0.02 | 57.1% | 6 | - |

| PUT | 345 | 2026-07-01 | 61.15 | 65.0 | - | 126.4% | - | - |

| CALL | 350 | 2026-07-01 | - | 1.96 | 0.02 | 61.0% | 6 | - |

| PUT | 350 | 2026-07-01 | 66.2 | 69.4 | - | 128.3% | - | - |

| CALL | 355 | 2026-07-01 | - | 1.96 | 0.02 | 63.9% | 4 | - |

| PUT | 355 | 2026-07-01 | 71.15 | 74.25 | - | 133.2% | - | - |

| CALL | 360 | 2026-07-01 | - | 2.13 | 0.02 | 67.8% | 4 | - |

| PUT | 360 | 2026-07-01 | 76.25 | 79.4 | - | 141.0% | - | - |

| CALL | 365 | 2026-07-01 | - | 2.13 | 0.03 | 71.7% | 2 | 11 |

| PUT | 365 | 2026-07-01 | 81.2 | 84.4 | - | 146.8% | - | - |

| CALL | 370 | 2026-07-01 | - | 2.13 | 0.02 | 74.7% | 4 | - |

| PUT | 370 | 2026-07-01 | 86.2 | 90.0 | - | 158.6% | - | - |

| CALL | 375 | 2026-07-01 | - | 1.96 | 0.03 | 78.6% | 4 | - |

| PUT | 375 | 2026-07-01 | 91.1 | 94.9 | - | 162.5% | - | - |

| CALL | 380 | 2026-07-01 | - | 0.01 | 0.02 | 81.5% | 8 | - |

| PUT | 380 | 2026-07-01 | 96.25 | 99.45 | - | 165.4% | - | - |

| CALL | 110 | 2026-07-02 | 170.95 | 173.85 | 198.21 | 1.5% | - | 3 |

| PUT | 110 | 2026-07-02 | - | 0.01 | - | 231.7% | - | 1116 |

| CALL | 120 | 2026-07-02 | 160.65 | 163.85 | - | 1.5% | - | - |

| PUT | 120 | 2026-07-02 | - | 0.01 | - | 211.2% | - | 1004 |

| CALL | 125 | 2026-07-02 | 155.2 | 158.85 | 165.23 | 1.5% | - | 1 |

| PUT | 125 | 2026-07-02 | - | 0.01 | 0.03 | 201.5% | 12 | 1011 |

| CALL | 130 | 2026-07-02 | 150.9 | 153.85 | - | 1.5% | - | - |

| PUT | 130 | 2026-07-02 | - | 0.01 | - | 192.7% | - | 1 |

| CALL | 135 | 2026-07-02 | 145.05 | 148.8 | - | 1.5% | - | - |

| PUT | 135 | 2026-07-02 | - | 0.01 | - | 183.9% | - | - |

| CALL | 140 | 2026-07-02 | 140.95 | 143.85 | - | 1.5% | - | - |

| PUT | 140 | 2026-07-02 | - | 0.01 | - | 175.1% | - | 1 |

| CALL | 145 | 2026-07-02 | 135.15 | 138.85 | - | 1.5% | - | - |

| PUT | 145 | 2026-07-02 | - | 0.41 | - | 167.3% | - | - |

| CALL | 150 | 2026-07-02 | 130.9 | 133.85 | 129.93 | 1.5% | 4 | - |

| PUT | 150 | 2026-07-02 | - | 0.41 | - | 158.6% | - | 1 |

| CALL | 155 | 2026-07-02 | 125.75 | 128.85 | - | 1.5% | - | - |

| PUT | 155 | 2026-07-02 | - | 0.41 | - | 151.7% | - | - |

| CALL | 160 | 2026-07-02 | 120.75 | 123.85 | 136.62 | 1.5% | - | 1 |

| PUT | 160 | 2026-07-02 | - | 1.53 | 0.01 | 143.9% | 9500 | 1 |

| CALL | 165 | 2026-07-02 | 115.95 | 118.85 | - | 1.5% | - | - |

| PUT | 165 | 2026-07-02 | - | 0.41 | - | 136.1% | - | - |

| CALL | 170 | 2026-07-02 | 110.35 | 113.85 | - | 1.5% | - | - |

| PUT | 170 | 2026-07-02 | - | 0.01 | - | 129.3% | - | 22 |

| CALL | 175 | 2026-07-02 | 105.15 | 108.9 | 105.32 | 1.5% | - | 1 |

| PUT | 175 | 2026-07-02 | - | 1.45 | - | 122.5% | - | 2 |

| CALL | 180 | 2026-07-02 | 101.05 | 103.9 | - | 1.5% | - | - |

| PUT | 180 | 2026-07-02 | - | 0.1 | - | 115.6% | - | 26 |

| CALL | 185 | 2026-07-02 | 95.5 | 98.9 | 95.07 | 1.5% | 1 | 3 |

| PUT | 185 | 202 |

…(truncated)…

MCP tool: price_option_path

{"option_path": [1.4499169613867195, 1.9687396964419719, 0.8446302659558071, 2.4255810336061074, 0.9706462290993727, 0.2099362442934236, 1.0723783583696616, 0.0781787733538657], "volatility_used": 0.29318082289556785, "symbol": "AAPL"}

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 18 | 2026-07-17 | 20.7 | 24.7 | - | 1.5% | - | - |

| PUT | 18 | 2026-07-17 | - | 0.25 | - | 131.2% | - | 288 |

| CALL | 20 | 2026-07-17 | 18.2 | 22.2 | 18.37 | 1.5% | - | 10 |

| PUT | 20 | 2026-07-17 | - | 1.15 | - | 110.8% | - | - |

| CALL | 22 | 2026-07-17 | 15.7 | 19.7 | 14.0 | 1.5% | - | 2 |

| PUT | 22 | 2026-07-17 | - | 1.15 | - | 93.2% | - | 2 |

| CALL | 25 | 2026-07-17 | 13.2 | 17.2 | 12.4 | 1.5% | - | 21 |

| PUT | 25 | 2026-07-17 | - | 0.1 | - | 77.6% | - | 27 |

| CALL | 28 | 2026-07-17 | 10.8 | 14.7 | 16.3 | 1.5% | - | 33 |

| PUT | 28 | 2026-07-17 | - | 0.25 | 0.11 | 63.9% | 2 | 384 |

| CALL | 30 | 2026-07-17 | 9.3 | 11.2 | 10.05 | 1.5% | - | 52 |

| PUT | 30 | 2026-07-17 | 0.2 | 0.4 | 0.3 | 90.3% | 2 | 400 |

| CALL | 32 | 2026-07-17 | 7.1 | 8.9 | 8.64 | 65.9% | - | 58 |

| PUT | 32 | 2026-07-17 | 0.5 | 1.05 | 0.55 | 96.1% | 14 | 1271 |

| CALL | 35 | 2026-07-17 | 5.5 | 6.9 | 6.0 | 78.6% | 8 | 347 |

| PUT | 35 | 2026-07-17 | 0.95 | 1.15 | 1.05 | 83.4% | 38 | 3228 |

| CALL | 38 | 2026-07-17 | 3.7 | 5.3 | 4.5 | 78.6% | 16 | 202 |

| PUT | 38 | 2026-07-17 | 1.8 | 2.3 | 1.9 | 88.3% | 53 | 732 |

| CALL | 40 | 2026-07-17 | 1.85 | 3.2 | 2.77 | 62.0% | 198 | 1198 |

| PUT | 40 | 2026-07-17 | 2.9 | 4.6 | 3.1 | 102.0% | 65 | 653 |

| CALL | 42 | 2026-07-17 | 1.85 | 2.1 | 1.94 | 74.7% | 197 | 11937 |

| PUT | 42 | 2026-07-17 | 4.0 | 5.9 | 4.4 | 95.1% | 20 | 55 |

| CALL | 45 | 2026-07-17 | 1.1 | 1.35 | 1.22 | 74.7% | 68 | 1764 |

| PUT | 45 | 2026-07-17 | 4.8 | 7.5 | - | 80.5% | - | 21 |

| CALL | 48 | 2026-07-17 | 0.65 | 0.85 | 0.73 | 74.7% | 114 | 10401 |

| PUT | 48 | 2026-07-17 | 7.6 | 9.8 | - | 99.0% | - | - |

| CALL | 50 | 2026-07-17 | 0.35 | 0.65 | 0.5 | 77.6% | 48 | 1767 |

| PUT | 50 | 2026-07-17 | 9.7 | 11.5 | - | 94.2% | - | 50 |

| CALL | 55 | 2026-07-17 | - | 0.5 | 0.2 | 51.2% | 1 | 191 |

| PUT | 55 | 2026-07-17 | 14.0 | 16.4 | - | 101.0% | - | - |

| CALL | 60 | 2026-07-17 | 0.05 | 0.1 | 0.07 | 82.5% | 60 | 2853 |

| PUT | 60 | 2026-07-17 | 18.8 | 21.7 | - | 122.5% | - | - |

| CALL | 20 | 2026-08-21 | 18.4 | 22.2 | - | 1.5% | - | - |

| PUT | 20 | 2026-08-21 | - | 2.25 | - | 68.8% | - | - |

| CALL | 22 | 2026-08-21 | 16.4 | 19.1 | - | 1.5% | - | - |

| PUT | 22 | 2026-08-21 | 0.15 | 1.0 | - | 113.7% | - | 10 |

| CALL | 25 | 2026-08-21 | 13.9 | 16.3 | - | 1.5% | - | - |

| PUT | 25 | 2026-08-21 | 0.25 | 0.8 | 0.45 | 94.2% | 2 | 113 |

| CALL | 28 | 2026-08-21 | 12.0 | 14.4 | - | 70.8% | - | - |

| PUT | 28 | 2026-08-21 | 0.45 | 1.6 | - | 98.1% | - | 1 |

| CALL | 30 | 2026-08-21 | 10.3 | 11.9 | 11.27 | 71.7% | 2 | 1 |

| PUT | 30 | 2026-08-21 | 0.85 | 3.2 | 1.15 | 106.9% | 7 | 12 |

| CALL | 32 | 2026-08-21 | 8.0 | 10.6 | 10.72 | 75.6% | - | 15 |

| PUT | 32 | 2026-08-21 | 1.6 | 1.95 | 1.7 | 83.4% | 4 | 39 |

| CALL | 35 | 2026-08-21 | 6.6 | 8.2 | 7.4 | 70.8% | 2 | 30 |

| PUT | 35 | 2026-08-21 | 2.25 | 3.1 | 2.67 | 84.4% | 5 | 12 |

| CALL | 38 | 2026-08-21 | 5.5 | 6.6 | 7.4 | 73.7% | - | 40 |

| PUT | 38 | 2026-08-21 | 2.85 | 5.5 | 3.7 | 91.2% | 2 | 37 |

| CALL | 40 | 2026-08-21 | 3.2 | 5.3 | 5.0 | 64.9% | 2 | 706 |

| PUT | 40 | 2026-08-21 | 3.2 | 6.9 | 4.3 | 84.4% | 3 | 33 |

| CALL | 42 | 2026-08-21 | 3.8 | 4.3 | 3.8 | 77.6% | 6 | 67 |

| PUT | 42 | 2026-08-21 | 5.1 | 8.5 | - | 89.3% | - | 2 |

| CALL | 45 | 2026-08-21 | 3.0 | 3.5 | 3.1 | 78.6% | 122 | 285 |

| PUT | 45 | 2026-08-21 | 7.3 | 8.3 | - | 78.6% | - | 87 |

| CALL | 48 | 2026-08-21 | 2.35 | 3.7 | 2.47 | 86.4% | 11 | 123 |

| PUT | 48 | 2026-08-21 | 9.0 | 11.7 | - | 91.2% | - | - |

| CALL | 50 | 2026-08-21 | 1.75 | 3.8 | 1.88 | 92.2% | 50 | 280 |

| PUT | 50 | 2026-08-21 | 11.2 | 13.2 | - | 91.2% | - | - |

| CALL | 55 | 2026-08-21 | 1.0 | 2.9 | 1.35 | 94.2% | 11 | 369 |

| PUT | 55 | 2026-08-21 | 14.7 | 17.4 | - | 86.4% | - | - |

| CALL | 2 | 2026-09-18 | 36.6 | 38.6 | 37.29 | 1.5% | 1 | 756 |

| PUT | 2 | 2026-09-18 | - | 0.25 | - | 216.1% | - | - |

| CALL | 5 | 2026-09-18 | 33.2 | 37.2 | 33.3 | 1.5% | - | 2 |

| PUT | 5 | 2026-09-18 | - | 0.25 | - | 160.5% | - | - |

| CALL | 8 | 2026-09-18 | 30.7 | 34.7 | 30.84 | 1.5% | - | 1 |

| PUT | 8 | 2026-09-18 | - | 0.25 | - | 129.3% | - | - |

| CALL | 10 | 2026-09-18 | 28.4 | 32.2 | 28.32 | 102.9% | - | 9 |

| PUT | 10 | 2026-09-18 | - | 2.15 | - | 107.8% | - | 189 |

| CALL | 12 | 2026-09-18 | 25.7 | 29.7 | 10.4 | 1.5% | - | 10 |

| PUT | 12 | 2026-09-18 | - | 1.95 | - | 90.3% | - | 21 |

| CALL | 15 | 2026-09-18 | 23.2 | 27.2 | 20.75 | 1.5% | - | 57 |

| PUT | 15 | 2026-09-18 | - | 2.2 | - | 77.6% | - | 23 |

| CALL | 18 | 2026-09-18 | 20.8 | 24.7 | 18.07 | 1.5% | - | 113 |

| PUT | 18 | 2026-09-18 | - | 0.6 | - | 65.9% | - | 51 |

| CALL | 20 | 2026-09-18 | 19.2 | 22.3 | 18.7 | 98.1% | - | 168 |

| PUT | 20 | 2026-09-18 | - | 1.6 | - | 56.1% | - | 71 |

| CALL | 22 | 2026-09-18 | 16.9 | 19.7 | 14.5 | 85.4% | - | 163 |

| PUT | 22 | 2026-09-18 | - | 1.25 | - | 47.3% | - | 191 |

| CALL | 25 | 2026-09-18 | 14.9 | 16.4 | 17.9 | 63.9% | - | 1790 |

| PUT | 25 | 2026-09-18 | - | 1.0 | - | 39.5% | - | 274 |

| CALL | 28 | 2026-09-18 | 12.8 | 15.0 | 15.25 | 78.6% | - | 119 |

| PUT | 28 | 2026-09-18 | 0.75 | 1.25 | - | 79.5% | - | 82 |

| CALL | 30 | 2026-09-18 | 11.5 | 12.4 | 11.5 | 77.6% | 20 | 994 |

| PUT | 30 | 2026-09-18 | 1.55 | 2.75 | 1.75 | 90.3% | 11 | 396 |

| CALL | 32 | 2026-09-18 | 9.3 | 11.0 | 10.0 | 75.6% | 4 | 229 |

| PUT | 32 | 2026-09-18 | 2.15 | 2.75 | 2.4 | 80.5% | 16 | 1316 |

| CALL | 35 | 2026-09-18 | 8.0 | 9.1 | 8.4 | 75.6% | 27 | 6379 |

| PUT | 35 | 2026-09-18 | 3.2 | 3.9 | 3.4 | 82.5% | 1 | 795 |

| CALL | 38 | 2026-09-18 | 6.6 | 8.8 | 8.0 | 82.5% | - | 1101 |

| PUT | 38 | 2026-09-18 | 3.8 | 5.3 | 5.5 | 80.5% | 15 | 130 |

| CALL | 40 | 2026-09-18 | 5.9 | 6.4 | 6.0 | 77.6% | 36 | 3363 |

| PUT | 40 | 2026-09-18 | 5.0 | 7.2 | - | 83.4% | - | 45 |

| CALL | 42 | 2026-09-18 | 3.7 | 5.3 | 5.15 | 68.8% | 4 | 181 |

| PUT | 42 | 2026-09-18 | 6.3 | 8.7 | - | 82.5% | - | 87 |

| CALL | 45 | 2026-09-18 | 2.45 | 4.4 | 4.4 | 65.9% | 81 | 937 |

| PUT | 45 | 2026-09-18 | 8.2 | 10.3 | 9.2 | 84.4% | 1 | 19 |

| CALL | 48 | 2026-09-18 | 3.1 | 3.7 | 3.6 | 75.6% | 55 | 416 |

| PUT | 48 | 2026-09-18 | 10.0 | 12.0 | - | 84.4% | - | - |

| CALL | 50 | 2026-09-18 | 2.65 | 3.1 | 2.9 | 76.6% | 51 | 341 |

| PUT | 50 | 2026-09-18 | 12.0 | 13.6 | - | 84.4% | - | - |

| CALL | 55 | 2026-09-18 | 1.8 | 2.15 | 2.0 | 77.6% | 38 | 833 |

| PUT | 55 | 2026-09-18 | 16.0 | 17.7 | - | 85.4% | - | - |

| CALL | 60 | 2026-09-18 | 1.05 | 1.7 | 1.32 | 77.6% | 40 | 880 |

| PUT | 60 | 2026-09-18 | 19.9 | 22.9 | - | 91.2% | - | - |

| CALL | 15 | 2026-12-18 | 23.7 | 27.7 | 25.45 | 83.4% | - | 2 |

| PUT | 15 | 2026-12-18 | - | 2.55 | - | 54.2% | - | 1 |

| CALL | 18 | 2026-12-18 | 21.9 | 25.5 | 21.6 | 92.2% | - | 2 |

| PUT | 18 | 2026-12-18 | - | 2.8 | - | 46.4% | - | 15 |

| CALL | 20 | 2026-12-18 | 19.7 | 23.3 | 21.2 | 87.3% | - | 4 |

| PUT | 20 | 2026-12-18 | - | 2.8 | - | 39.5% | - | - |

| CALL | 22 | 2026-12-18 | 18.0 | 20.4 | 14.15 | 78.6% | - | 27 |

| PUT | 22 | 2026-12-18 | 0.7 | 1.85 | - | 82.5% | - | 7 |

| CALL | 25 | 2026-12-18 | 15.8 | 18.5 | 17.7 | 75.6% | - | 28 |

| PUT | 25 | 2026-12-18 | 0.55 | 2.15 | - | 72.7% | - | 21 |

| CALL | 28 | 2026-12-18 | 15.0 | 16.6 | 15.8 | 82.5% | 1 | 10 |

| PUT | 28 | 2026-12-18 | 1.3 | 3.8 | - | 81.5% | - | 10 |

| CALL | 30 | 2026-12-18 | 12.6 | 15.2 | 15.4 | 77.6% | - | 23 |

| PUT | 30 | 2026-12-18 | 3.1 | 3.6 | - | 79.5% | - | 67 |

| CALL | 32 | 2026-12-18 | 11.3 | 13.5 | 14.71 | 76.6% | - | 33 |

| PUT | 32 | 2026-12-18 | 4.2 | 4.7 | 4.42 | 80.5% | 10 | 87 |

| CALL | 35 | 2026-12-18 | 10.0 | 12.2 | 12.3 | 77.6% | - | 114 |

| PUT | 35 | 2026-12-18 | 5.3 | 5.9 | - | 80.5% | - | 29 |

| CALL | 38 | 2026-12-18 | 8.9 | 10.2 | 9.42 | 73.7% | 59 | 357 |

| PUT | 38 | 2026-12-18 | 6.5 | 7.2 | 6.61 | 80.5% | 59 | 294 |

| CALL | 40 | 2026-12-18 | 8.4 | 9.1 | 8.7 | 76.6% | 1 | 311 |

| PUT | 40 | 2026-12-18 | 7.9 | 8.7 | - | 80.5% |

…(truncated)…

MCP tool: price_option_path

{"option_path": [4.933885411956549, 4.9555767282875784, 5.064850686925311, 5.435994151931279, 5.756468100735418, 6.016922721101647, 5.185725522771435, 4.2367166821018465, 4.347262250549445, 4.0419263542394255], "volatility_used": 0.8377511994407282, "symbol": "ASX"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.