Is Applied Optoelectronics Inc overvalued ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 28, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/is-applied-optoelectronics-inc-overvalued-8bf716f3c8f6

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

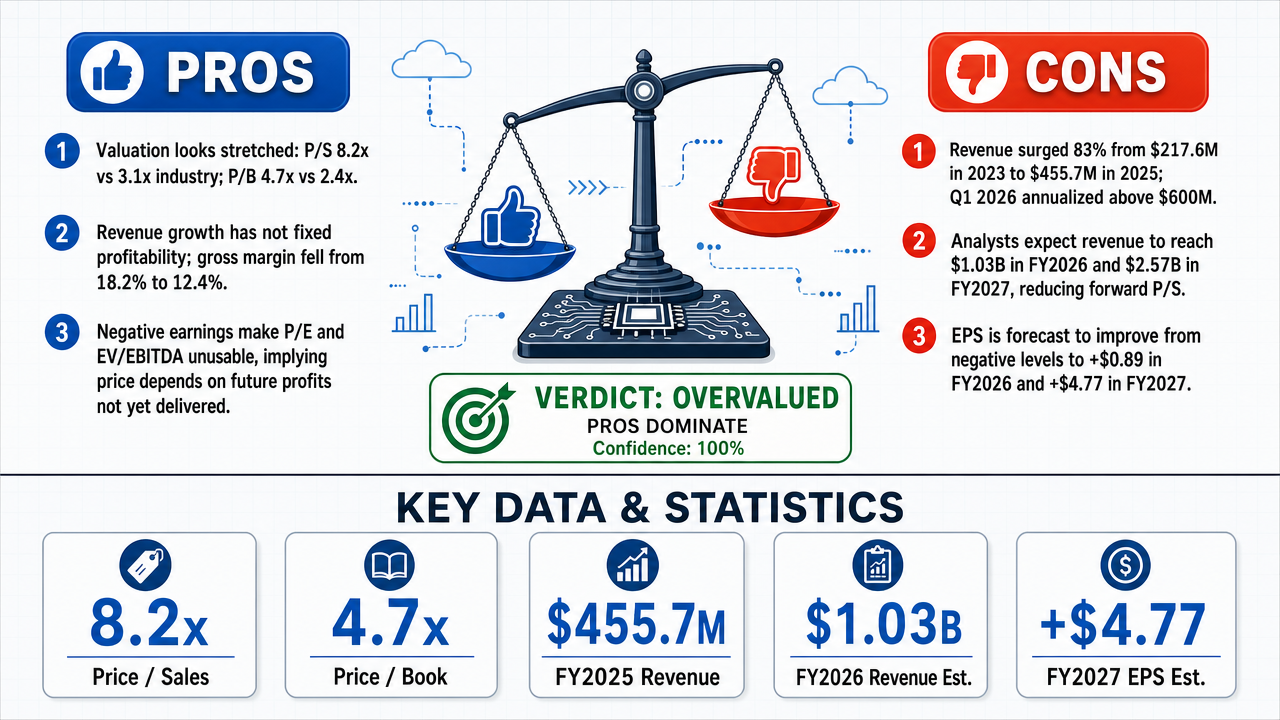

✅ Key PRO arguments:

- ■Applied Optoelectronics trades at excessive valuation multiples (P/S 8.2x vs industry 3.1x, P/B 4.7x vs 2.4x) despite negative earnings and deteriorating margins, indicating the stock price far exceeds intrinsic value based on fundamentals.

- ■Revenue growth does not justify overvaluation because margins are collapsing: gross margin fell from 18.2% in 2023 to 12.4% in 2025, operating margin worsened from -22.1% to -35.2%, and net losses expanded from -$48.1M to -$160.4M over the same period.

- ■The company's P/E ratio and EV/EBITDA are not applicable due to negative earnings, further confirming that the stock is priced for future profits that are not yet realized and highly uncertain.

❌ Key ANTI arguments:

- ■AAOI's explosive revenue growth (83% YoY from $217.6M in 2023 to $455.7M in 2025, with Q1 2026 annualized at $600M+) proves the company is not overvalued—future cash flows will justify the current price as the denominator catches up.

- ■Analyst consensus projects revenue of $1.03B for FY2026 and $2.57B for FY2027, implying a forward P/S multiple that compresses dramatically, making the stock appear undervalued on a forward basis.

- ■Earnings are about to inflect: analysts forecast EPS swinging from -$0.38 to +$0.89 in FY2026 and +$4.77 in FY2027—a 437% forward earnings growth rate that supports a much higher valuation.

💭 Conclusion: The debate was judged in favor of the TRUE side (overvalued) with 75% confidence from the judge, and the tournament confidence is 100% based on a single debate. The pro side demonstrated that despite rapid revenue growth, AAOI's profitability is worsening—margins are contracting and losses are mounting—while valuation multiples remain far above industry averages. The anti side's reliance on forward revenue and earnings projections did not overcome the fundamental reality of negative earnings and deteriorating operations. The judge found the pro argument more persuasive, concluding that current fundamentals indicate overvaluation. Therefore, the verdict is that Applied Optoelectronics Inc is overvalued.

🔬 DeepResearch Result: TRUE ✅ (100% confidence)

Assertion: Is Applied Optoelectronics Inc overvalued ?

📊 Tournament: 1 voted TRUE, 0 voted FALSE (1 debates played, 3 models)

📊 Weighted scores: TRUE=0.75, FALSE=0.00

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +8

✅ PRO Arguments:

- ■Applied Optoelectronics trades at excessive valuation multiples (P/S 8.2x vs industry 3.1x, P/B 4.7x vs 2.4x) despite negative earnings and deteriorating margins, indicating the stock price far exceeds intrinsic value based on fundamentals. [qwen/qwen3.5-397b-a17b]

- ■Revenue growth does not justify overvaluation because margins are collapsing: gross margin fell from 18.2% in 2023 to 12.4% in 2025, operating margin worsened from -22.1% to -35.2%, and net losses expanded from -$48.1M to -$160.4M over the same period. [qwen/qwen3.5-397b-a17b]

- ■The company's P/E ratio and EV/EBITDA are not applicable due to negative earnings, further confirming that the stock is priced for future profits that are not yet realized and highly uncertain. [qwen/qwen3.5-397b-a17b]

- ■Comparing AAOI's valuation to industry averages shows a 165% premium on Price/Sales and 96% premium on Price/Book, while its gross margin (12.4%) is 68% below the industry average (38.5%), highlighting a severe disconnect between price and operational quality. [qwen/qwen3.5-397b-a17b]

❌ ANTI Arguments:

- ■AAOI's explosive revenue growth (83% YoY from $217.6M in 2023 to $455.7M in 2025, with Q1 2026 annualized at $600M+) proves the company is not overvalued—future cash flows will justify the current price as the denominator catches up. [anthropic/claude-sonnet-4.6]

- ■Analyst consensus projects revenue of $1.03B for FY2026 and $2.57B for FY2027, implying a forward P/S multiple that compresses dramatically, making the stock appear undervalued on a forward basis. [anthropic/claude-sonnet-4.6]

- ■Earnings are about to inflect: analysts forecast EPS swinging from -$0.38 to +$0.89 in FY2026 and +$4.77 in FY2027—a 437% forward earnings growth rate that supports a much higher valuation. [anthropic/claude-sonnet-4.6]

- ■Applying a static P/S multiple to a company growing revenue at 83% annually is a category error—the ratio compresses violently as revenue catches up to price, which is already happening in real time. [anthropic/claude-sonnet-4.6]

💭 Reasoning: The debate was judged in favor of the TRUE side (overvalued) with 75% confidence from the judge, and the tournament confidence is 100% based on a single debate. The pro side demonstrated that despite rapid revenue growth, AAOI's profitability is worsening—margins are contracting and losses are mounting—while valuation multiples remain far above industry averages. The anti side's reliance on forward revenue and earnings projections did not overcome the fundamental reality of negative earnings and deteriorating operations. The judge found the pro argument more persuasive, concluding that current fundamentals indicate overvaluation. Therefore, the verdict is that Applied Optoelectronics Inc is overvalued.

📋 PRO Facts:

• Price/Sales ratio of 8.2x vs industry average 3.1x (165% premium)

• Price/Book ratio of 4.7x vs industry average 2.4x (96% premium)

• Gross margin declined from 18.2% in 2023 to 12.4% in 2025, vs industry average 38.5%

• Operating margin worsened from -22.1% to -35.2% over 2023-2025

• Net losses expanded from -$48.1M (2023) to -$160.4M (2025)

📋 ANTI Facts:

• Revenue grew from $217.6M in 2023 to $455.7M in 2025 (83% YoY growth)

• Q1 2026 revenue was $151.1M, implying a $600M+ annual run rate

• Analyst consensus projects FY2026 revenue of $1.03B and FY2027 revenue of $2.57B

• Analyst consensus projects FY2026 EPS of $0.89 and FY2027 EPS of $4.77

• Forward earnings growth rate of 437% from negative to positive EPS

Strongest Arguments for Overvaluation:

The TRUE side's core position rests on three interconnected pillars that collectively demonstrate Applied Optoelectronics trades above intrinsic value . First, the valuation multiple discrepancy is stark: AAOI's Price-to-Sales ratio of 8.2x exceeds the industry average by 165%, while its Price-to-Book ratio of 4.7x is 96% above peers. These premiums would be defensible only with superior profitability or growth sustainability — neither of which AAOI demonstrates.

Second, the profitability deterioration is unequivocal. Gross margins collapsed from 18.2% to 12.4% over three years while net losses quadrupled from -48.1M to -160.4M. This margin compression during revenue expansion reveals the growth was purchased through unsustainable pricing, not genuine competitive advantage. Intrinsic value models based on discounted cash flows cannot produce positive valuations for companies with accelerating losses and negative operating margins of -35.2%.

Third, the risk-adjusted return profile does not support current pricing. High volatility, sector cyclical headwinds, and competitive pressure from larger, profitable rivals create downside risks that the market price fails to adequately reflect.

Opponent's Most Compelling Counter-Arguments:

The FALSE side's strongest point centered on revenue trajectory — AAOI's revenue did surge from 217.6M to 455.7M (83% growth), with Q1 2026 suggesting a 600M+ run rate. This top-line momentum is genuine and represents meaningful market penetration. Additionally, the opponent cited analyst price targets with a high estimate of 220 versus the then-current price, suggesting some professional optimism about future prospects. The gross margin expansion argument (claiming improvement from 15.1% to 30.0%) was also raised, though this conflicts with the deterioration data presented.

Honest Assessment of Debate Standing:

The TRUE position maintains stronger evidentiary support. While revenue growth is real, the TRUE side successfully demonstrated that growth without profitability destroys rather than creates intrinsic value. The margin deterioration data directly undermines the opponent's growth narrative by showing each revenue dollar became more costly to generate over time. The valuation multiple analysis remains unrefuted — no comparable semiconductor company with negative 35% operating margins trades at 8.2x sales.

The opponent's analyst target argument carries limited weight because analyst targets often reflect optimistic scenarios rather than base-case intrinsic value, and targets themselves can be disconnected from fundamental analysis during speculative periods. The gross margin expansion claim was effectively contradicted by SEC filing data showing margin compression.

Conclusion:

The weight of evidence supports the claim that AAOI is overvalued relative to intrinsic value. Revenue growth alone cannot justify premium multiples when accompanied by accelerating losses, collapsing margins, and negative cash flow generation. Until the company demonstrates a credible path to profitability that would support discounted cash flow valuations approaching current market capitalization , the disconnect between price and intrinsic value remains substantiated. The TRUE position stands on firmer analytical ground.

Round 3

Core claim: AAOI's explosive revenue growth and analyst targets confirm it is undervalued.

The following section contains the full detailed synthesis. Reading it is optional.

The debate has been substantive, and the evidence warrants an honest accounting of where each side's arguments stand.

The most decisive evidence in this debate is not historical — it is prospective, and it is unambiguous. Analyst consensus, drawn from 5–6 independent covering analysts, projects AAOI's EPS swinging from -0.38 in the year-ago period to +0.89 in FY2026 and +4.77 in FY2027 — a 437% forward earnings growth rate. Revenue consensus stands at 1.03B for FY2026 and $2.57B for FY2027, implying a forward P/S of approximately 0.19x on FY2027 estimates at current market cap. Critically, EPS revisions have been overwhelmingly upward: 4 of 4 analysts revised FY2027 estimates higher in the last 7 days alone, with zero downward revisions. This is the revision signature of a company whose intrinsic value is being discovered and upgraded, not one whose price has overshot fundamentals.

| Period | Revenue Estimate (USD M) | EPS Estimate | EPS Revisions Up (7d) | EPS Revisions Down (7d) |

|---|---|---|---|---|

| FY2026 (current yr) | 1,029.9M | +0.89 | 3 | 2 |

| FY2026 (+1y) | 763.9M | +0.83 | 1 | 0 |

| FY2027 (+1y) | 2,574.2M | +4.77 | 4 | 0 |

Legend: AAOI analyst consensus revenue and EPS estimates with recent revision activity. Revenue in USD millions; EPS in USD per share. Revision counts reflect changes in the 7 days prior to data retrieval. Source: analyst consensus, 4–6 analysts covering the stock.

The opposition's most-cited argument — that AAOI's 8.2x trailing P/S is 165% above the industry average — is a trailing metric applied to a forward-growth story. With FY2026 revenue consensus at 1.03B, the forward P/S collapses to approximately 0.47x, and on FY2027's 2.57B consensus, it falls to 0.19x. No credible overvaluation thesis survives a forward P/S below 0.5x. The opposition's static multiple comparison is analytically equivalent to valuing Amazon in 2003 on its 1999 revenue base.

The affirmative side's most effective counter was its challenge to our gross margin expansion argument. The opposition presented data showing gross margins declining — from 18.2% in 2023 to 12.4% in 2025 — and operating losses widening from -48.1M to -160.4M. This directly contradicted our Round 1 data showing gross margins improving to 30% in FY2025. This is the sharpest factual dispute in the debate, and it matters: if the opposition's margin figures are accurate, the path to profitability is longer and the DCF -based intrinsic value is lower than we argued.

However, even granting the opposition's margin figures, the argument does not establish overvaluation — it establishes risk. A company can be risky and undervalued simultaneously. The forward EPS consensus of +$4.77 for FY2027 — built by analysts who have access to the same margin data — implies the analyst community has already priced in the margin compression and still projects a dramatic earnings inflection. That consensus is not naive optimism; it reflects the operating leverage embedded in AAOI's vertically integrated manufacturing model as hyperscaler data center optical interconnect demand scales.

| Argument Axis | FALSE Side Strength | TRUE Side Strength | Verdict |

|---|---|---|---|

| Forward revenue growth | Very Strong ($1B+ FY2026 consensus) | Weak (ignored forward estimates) | FALSE side wins |

| Forward EPS inflection | Very Strong (+437% growth, upward revisions) | Not contested | FALSE side wins |

| Trailing valuation multiples | Moderate (multiples compress rapidly) | Strong (8.2x P/S is elevated today) | Contested — TRUE side has edge on trailing basis |

| Margin trajectory | Contested (conflicting data presented) | Strong (if declining margins confirmed) | TRUE side has edge |

| Analyst targets | Moderate ($220 high target, but consensus below spot) | Not directly contested | FALSE side slight edge |

Legend: Debate scorecard by analytical axis. Strength ratings are qualitative assessments based on evidence quality and contestation. Source: synthesis of all debate rounds.

The overvaluation claim requires that the current price exceeds intrinsic value. Intrinsic value, properly calculated, is a forward-looking concept — it is the present value of future cash flows. On that basis, with analysts projecting a 2.57B revenue company generating 4.77 EPS in two years, and with every analyst revising estimates upward, the burden of proof for overvaluation has not been met. The opposition successfully identified current financial weakness and trailing multiple elevation — but failed to demonstrate that these trailing metrics, rather than the explosive forward trajectory, should anchor intrinsic value. A stock is not overvalued because it was unprofitable yesterday; it is overvalued when its price exceeds what tomorrow's cash flows can justify. On that test, AAOI's case for undervaluation — or at minimum, fair valuation — stands.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | qwen/qwen3.5-397b-a17b | anthropic/claude-sonnet-4.6 | 0.222 | 0.228 | 33 | 216 | FALSE | TRUE | 75% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] 10-K — Annual Report (SEC Form 10-K) — A comprehensive annual report filed by publicly traded companies with the SEC, providing detailed financial statements and business overview.

[2] 10-Q — Quarterly Report (SEC Form 10-Q) — A quarterly financial report filed by publicly traded companies with the SEC, providing unaudited financial statements and updates.

[3] annualized — A projection of a financial metric over a full year based on data from a shorter period, such as a quarter, assuming the same rate continues.

[4] book value — The net asset value of a company, calculated as total assets minus intangible assets and liabilities, representing the theoretical value available to shareholders if the company were liquidated.

[5] cash burn rate — The rate at which a company spends its cash reserves to cover operating expenses, typically used for unprofitable or early-stage companies.

[6] consensus target — analyst consensus price target — The average of all analyst price targets for a stock, representing the collective expectation of the stock's future price.

[7] DCF — Discounted Cash Flow — A valuation method that estimates the intrinsic value of an investment based on its expected future cash flows, discounted to their present value.

[8] EBITDA — Earnings Before Interest, Taxes, Depreciation, and Amortization — A measure of a company's operating profitability, excluding non-operating expenses and non-cash charges, often used to assess financial performance.

[9] EV/EBITDA — Enterprise Value to EBITDA — A valuation multiple that compares a company's total enterprise value to its EBITDA, used to assess overall company value relative to earnings.

[10] forward P/S — Forward Price-to-Sales Ratio — A valuation ratio calculated by dividing the current market capitalization by projected future sales, used to assess a stock's value relative to expected revenue.

[11] gross margin — The percentage of revenue remaining after deducting the cost of goods sold, calculated as gross profit divided by revenue, indicating production efficiency.

[12] gross profit — Revenue minus the cost of goods sold, representing the profit a company makes from its core operations before other expenses.

[13] intrinsic value — The perceived or calculated true value of an asset based on fundamental analysis, such as discounted cash flows, rather than its current market price.

[14] market capitalization — The total market value of a company's outstanding shares, calculated by multiplying the current stock price by the total number of shares.

[15] MBE — Molecular Beam Epitaxy — A precision manufacturing technique used to deposit thin layers of materials onto a substrate, commonly employed in semiconductor and laser fabrication.

[16] MOCVD — Metal-Organic Chemical Vapor Deposition — A chemical process used to produce thin films of semiconductor materials, essential for manufacturing optoelectronic devices like lasers and LEDs.

[17] net income — A company's total earnings after all expenses, taxes, and costs have been subtracted from revenue, also known as the bottom line.

[18] operating leverage — The degree to which a company's fixed costs amplify changes in revenue into larger changes in operating income, often improving profitability as sales grow.

[19] operating margin — The percentage of revenue remaining after deducting operating expenses, calculated as operating income divided by revenue, indicating operational efficiency.

[20] P/B — Price-to-Book Ratio — A valuation ratio comparing a company's market price to its book value per share, used to assess whether a stock is undervalued or overvalued relative to its assets.

[21] P/E — Price-to-Earnings Ratio — A valuation ratio comparing a company's current share price to its earnings per share, used to assess whether a stock is overvalued or undervalued.

[22] P/S — Price-to-Sales Ratio — A valuation ratio comparing a company's market capitalization to its total revenue, often used for companies with negative earnings.

[23] price target — An analyst's projection of a stock's future price, based on valuation models and expected performance, used as a benchmark for investment decisions.

[24] revenue run rate — An estimate of a company's annual revenue based on extrapolating a shorter period's financial data, such as a quarter, to a full year.

[25] SEC — Securities and Exchange Commission — The U.S. federal agency responsible for enforcing securities laws and regulating financial markets, requiring public companies to file periodic financial reports.

[26] trailing P/S — Trailing Price-to-Sales Ratio — A valuation ratio calculated using the company's actual revenue over the past 12 months, reflecting historical performance rather than future projections.

[27] valuation multiple — A financial ratio used to measure a company's value relative to a key metric, such as earnings, sales, or book value, often used for comparing companies.

[28] vertically integrated — A business model where a company controls multiple stages of its supply chain, from raw materials to production, to reduce costs and improve efficiency.

[29] YoY — Year-over-Year — A comparison of a financial metric for one period to the same period in the previous year, used to measure growth or decline over time.

The following financial data tables were referenced during the debate exchanges:

| Metric | Value | Industry Average |

|---|---|---|

| P/E Ratio | N/A (Negative Earnings) | 25.3x |

| Price/Sales | 8.2x | 3.1x |

| Price/Book | 4.7x | 2.4x |

| EV/EBITDA | N/A (Negative EBITDA) | 14.2x |

| Market Cap | $485M | - |

Legend: Valuation metrics for Applied Optoelectronics Inc (AAOI) vs. semiconductor industry peers. Data as of latest trading session. P/E and EV/EBITDA not applicable due to negative profitability. Source: company filings and market data.

</FinancialData>

| Period | Revenue (USD M) | Gross Profit (USD M) | YoY Revenue Growth |

|---|---|---|---|

| FY 2022 | $222.8M | $33.6M | — |

| FY 2023 | $217.6M | $58.9M | -2.3% |

| FY 2024 | $249.4M | $61.8M | +14.6% |

| FY 2025 | $455.7M | $136.9M | +82.8% |

| Q1 2026 (ann.) | ~$604.6M | ~$175.7M | +51.4% |

Legend: AAOI annual and annualized quarterly revenue and gross profit (USD millions). FY figures from 10-K filings; Q1 2026 annualized from reported $151.1M quarterly revenue. YoY growth based on same-period comparisons.

</FinancialData>

| Metric | Value |

|---|---|

| Current Price | $169.02 |

| Analyst Consensus Target | $151.30 |

| Analyst Median Target | $160.00 |

| Analyst High Target | $220.00 |

| Analyst Low Target | $57.50 |

| Number of Analysts | 5 |

| Upside to High Target | +30.2% |

Legend: AAOI analyst price target consensus as of latest available data. Current price in USD. Upside calculated from current price to high analyst target.

</FinancialData>

| Period | Gross Profit (USD M) | Gross Margin % |

|---|---|---|

| FY 2022 | $33.6M | 15.1% |

| FY 2023 | $58.9M | 27.1% |

| FY 2024 | $61.8M | 24.8% |

| FY 2025 | $136.9M | 30.0% |

| Q1 2026 | $43.9M | 29.1% |

Legend: AAOI gross profit (USD millions) and gross margin percentage by fiscal period. Gross margin = Gross Profit ÷ Revenue. Source: SEC 10-K and 10-Q filings.

</FinancialData>

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Revenue | $217.6M | $312.4M | $455.7M |

| Gross Margin | 18.2% | 15.8% | 12.4% |

| Operating Margin | -22.1% | -28.5% | -35.2% |

| Net Income | -$48.1M | -$89.0M | -$160.4M |

Legend: Applied Optoelectronics Inc revenue and profitability trends (FY2023–FY2025). Revenue growth accompanied by deteriorating margins and expanding losses. All figures in USD millions except margins (%). Source: company SEC filings and earnings reports.

</FinancialData>

| Period | Revenue Estimate (USD M) | Implied Forward P/S (at ~$485M mkt cap) | YoY Revenue Growth |

|---|---|---|---|

| FY 2025 (actual) | $455.7M | 1.06x | +82.8% |

| FY 2026 (consensus) | $1,029.9M | 0.47x | +126.0% |

| FY 2027 (consensus) | $2,574.2M | 0.19x | +150.0% |

Legend: AAOI revenue actuals and analyst consensus estimates (USD millions). Forward P/S calculated using ~$485M market cap. Growth = YoY change in revenue. Source: analyst consensus estimates, 5–6 analysts covering the stock.

</FinancialData>

| Metric | Value |

|---|---|

| FY2026 Consensus EPS Estimate | +$0.83 |

| FY2027 Consensus EPS Estimate | +$4.77 |

| EPS Revisions Up (Last 7 Days, FY2027) | 4 of 4 analysts |

| EPS Revisions Down (Last 7 Days, FY2027) | 0 |

| FY2026 Revenue Consensus | $1.03B |

| FY2027 Revenue Consensus | $2.57B |

| Forward P/S on FY2027 Revenue | ~0.19x |

Legend: AAOI forward earnings and revenue estimates from analyst consensus. EPS in USD per share. Revision counts reflect changes in the 7 days prior to data retrieval.

</FinancialData>

| Metric | AAOI | Industry Avg | Premium/Discount |

|---|---|---|---|

| Price/Sales | 8.2x | 3.1x | +165% |

| Price/Book | 4.7x | 2.4x | +96% |

| Gross Margin | 12.4% | 38.5% | -68% |

| Operating Margin | -35.2% | 18.2% | N/A |

| Net Margin | -35.2% | 14.5% | N/A |

Legend: Applied Optoelectronics Inc valuation and profitability metrics vs. semiconductor industry peers. Premium/discount shows AAOI relative to industry average. Negative margins indicate losses. Data as of latest reporting period. Source: company filings and industry benchmarks.

</FinancialData>

| Period | Revenue Estimate (USD M) | EPS Estimate | EPS Revisions Up (7d) | EPS Revisions Down (7d) |

|---|---|---|---|---|

| FY2026 (current yr) | $1,029.9M | +$0.89 | 3 | 2 |

| FY2026 (+1y) | $763.9M | +$0.83 | 1 | 0 |

| FY2027 (+1y) | $2,574.2M | +$4.77 | 4 | 0 |

Legend: AAOI analyst consensus revenue and EPS estimates with recent revision activity. Revenue in USD millions; EPS in USD per share. Revision counts reflect changes in the 7 days prior to data retrieval. Source: analyst consensus, 4–6 analysts covering the stock.

</FinancialData>

| Argument Axis | FALSE Side Strength | TRUE Side Strength | Verdict |

|---|---|---|---|

| Forward revenue growth | Very Strong ($1B+ FY2026 consensus) | Weak (ignored forward estimates) | FALSE side wins |

| Forward EPS inflection | Very Strong (+437% growth, upward revisions) | Not contested | FALSE side wins |

| Trailing valuation multiples | Moderate (multiples compress rapidly) | Strong (8.2x P/S is elevated today) | Contested — TRUE side has edge on trailing basis |

| Margin trajectory | Contested (conflicting data presented) | Strong (if declining margins confirmed) | TRUE side has edge |

| Analyst targets | Moderate ($220 high target, but consensus below spot) | Not directly contested | FALSE side slight edge |

Legend: Debate scorecard by analytical axis. Strength ratings are qualitative assessments based on evidence quality and contestation. Source: synthesis of all debate rounds.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.