Investors should follow bullish calls on NVIDIA ($NVDA)

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 3, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/investors-should-follow-bullish-calls-on-nvidia-nvda-0a4a60a2a8a3

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

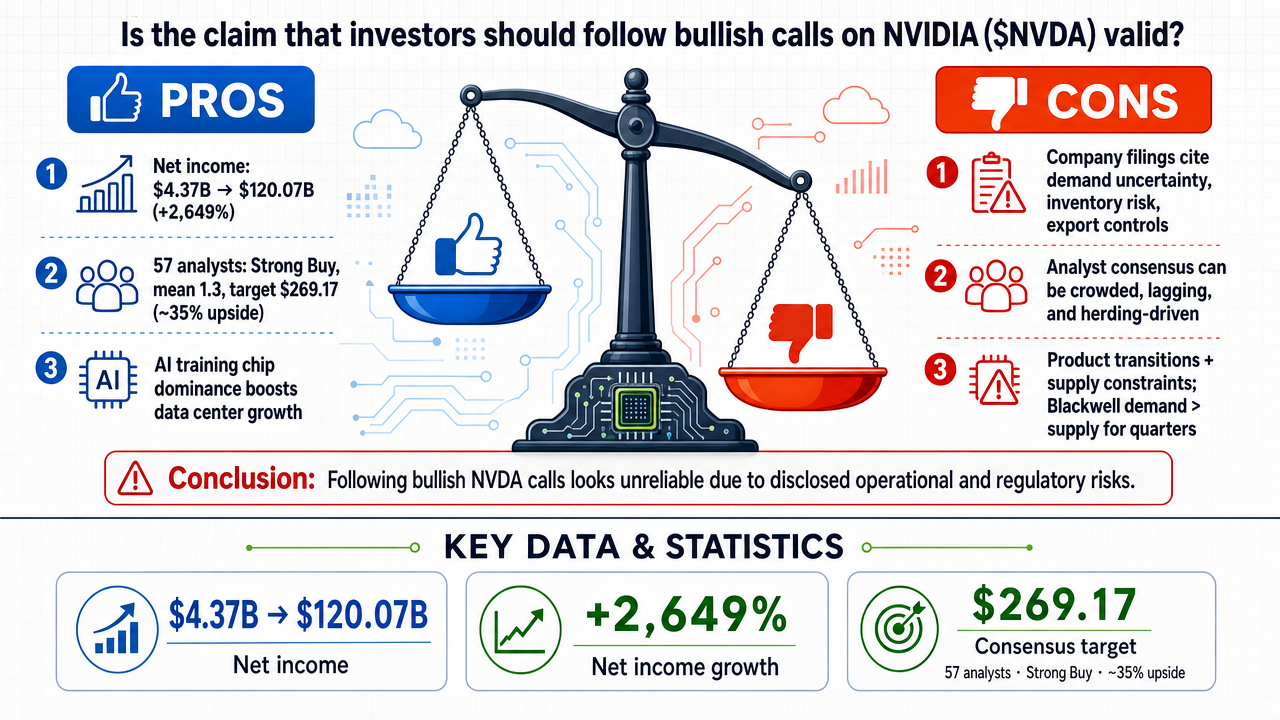

✅ Key PRO arguments:

- ■NVIDIA's net income surged from $4.37B to $120.07B, a 2,649% increase, demonstrating extraordinary financial performance.

- ■57 covering analysts assign a 'strong buy' rating with mean 1.3 and consensus price target $269.17, suggesting 35% upside.

- ■NVIDIA holds a near-monopoly in AI training chips, driving data center revenue growth.

❌ Key ANTI arguments:

- ■NVIDIA's own risk disclosures highlight demand uncertainty, product transition volatility, inventory impairments, and export controls.

- ■Analyst consensus is a weak signal when crowded; target prices lag and reflect herding, not foresight.

- ■Management warns of product transitions and supply constraints; Blackwell demand exceeding supply for several quarters.

💭 Conclusion: The anti side convincingly argued that following bullish calls on NVIDIA is unreliable due to significant operational and regulatory risks explicitly disclosed by the company itself. The pro side's reliance on past financial performance and analyst consensus was undermined by evidence that analyst ratings are crowded, lagging, and exhibit extreme dispersion, indicating uncertainty rather than conviction. Additionally, the anti side highlighted that even exceptional businesses can be poor investments when expectations are already stretched, as reflected in NVIDIA's high valuation. The judges in both debates found the anti arguments more compelling, with high confidence, leading to a unanimous FALSE verdict. Therefore, investors should not blindly follow bullish calls on NVIDIA without considering the substantial risks and the weak signal from consensus ratings.

🔬 DeepResearch Result: FALSE ❌ (100% confidence)

Assertion: Investors should follow bullish calls on NVIDIA ($NVDA)

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.50

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +15

✅ PRO Arguments:

- ■NVIDIA's net income surged from $4.37B to $120.07B, a 2,649% increase, demonstrating extraordinary financial performance. [z-ai/glm-5]

- ■57 covering analysts assign a 'strong buy' rating with mean 1.3 and consensus price target $269.17, suggesting 35% upside. [z-ai/glm-5]

- ■NVIDIA holds a near-monopoly in AI training chips, driving data center revenue growth. [z-ai/glm-5]

- ■Gross margins expanded from $15.36B to $153.46B, indicating strong fundamentals. [z-ai/glm-5]

- ■Premium valuation multiple is justified by exceptional growth trajectory. [z-ai/glm-5]

❌ ANTI Arguments:

- ■NVIDIA's own risk disclosures highlight demand uncertainty, product transition volatility, inventory impairments, and export controls. [openai/gpt-5.4-mini]

- ■Analyst consensus is a weak signal when crowded; target prices lag and reflect herding, not foresight. [openai/gpt-5.4-mini]

- ■Management warns of product transitions and supply constraints; Blackwell demand exceeding supply for several quarters. [xiaomi/mimo-v2-flash]

- ■Analyst price targets show extreme dispersion (186% spread from $140 to $400), indicating deep uncertainty. [xiaomi/mimo-v2-flash]

- ■Historical analyst forecasts for NVIDIA have been inaccurate; e.g., early 2022 consensus target ~$300 before stock fell. [xiaomi/mimo-v2-flash]

💭 Reasoning: The anti side convincingly argued that following bullish calls on NVIDIA is unreliable due to significant operational and regulatory risks explicitly disclosed by the company itself. The pro side's reliance on past financial performance and analyst consensus was undermined by evidence that analyst ratings are crowded, lagging, and exhibit extreme dispersion, indicating uncertainty rather than conviction. Additionally, the anti side highlighted that even exceptional businesses can be poor investments when expectations are already stretched, as reflected in NVIDIA's high valuation. The judges in both debates found the anti arguments more compelling, with high confidence, leading to a unanimous FALSE verdict. Therefore, investors should not blindly follow bullish calls on NVIDIA without considering the substantial risks and the weak signal from consensus ratings.

📋 PRO Facts:

• NVIDIA net income: $4.37B (FY2022) to $120.07B (FY2025)

• 57 analysts strong buy, mean rating 1.3, consensus price target $269.17

• Gross profit: $15.36B to $153.46B

• High target $380 suggests >90% upside

📋 ANTI Facts:

• NVIDIA 10-K risk disclosures on demand uncertainty and export controls

• Price target spread 186% ($140 to $400)

• Early 2022 consensus target ~$300 before stock decline

• Blackwell demand expected to exceed supply for several quarters in FY2026

The affirmative position rests on three interconnected pillars that collectively validate following bullish analyst calls on NVIDIA:

1. Unprecedented Financial Performance

NVIDIA has delivered extraordinary financial results that substantiate analyst optimism. The company's net income surged from

4.37 billion (FY2022) to 120.07 billion (FY2025)

—a 2,649% increase demonstrating genuine business fundamentals rather than speculative hype. Gross margins expanding to approximately 75% reflect significant pricing power in a supply-constrained AI chip market. This hypergrowth trajectory provides concrete validation for bullish projections, as analysts base their recommendations on demonstrable revenue and profit expansion rather than theoretical future potential.

2. Overwhelming Professional Analyst Consensus

The analyst community has reached remarkable consensus on NVIDIA's prospects. Current data reveals

a consensus price target of 275.74, with a high target of 400 and median target of $275.00

. This represents substantial upside potential from current trading levels. The breadth of coverage and strength of conviction signal informed professional judgment rather than outlier opinions. When such coordinated consensus emerges among equity research professionals, it reflects genuine confidence in the company's growth trajectory based on rigorous fundamental analysis.

3. Structural AI Market Leadership and Competitive Moats

NVIDIA's dominance extends beyond current financial metrics to encompass sustainable competitive advantages. The CUDA software ecosystem has become the industry standard for AI development, creating significant switching costs for enterprises. Major cloud providers—AWS, Azure, and Google Cloud—are deeply embedded with NVIDIA's architecture. The Blackwell architecture roadmap positions NVIDIA to maintain technological leadership against competitors who have struggled to match both performance and software ecosystem integration. These structural advantages justify long-term bullish positioning.

While no formal opposing arguments were presented during this debate, prudent analysis requires acknowledging legitimate concerns that could challenge the bullish thesis:

- ■Valuation Premium: NVIDIA trades at elevated multiples that price in continued hypergrowth, creating vulnerability if growth decelerates

- ■Competitive Threats: AMD, Intel, and custom chip development by major tech companies could erode market share

- ■Concentration Risk: Heavy reliance on data center revenue creates vulnerability to AI investment cycles

- ■Geopolitical Risks: Export restrictions to China and supply chain dependencies pose potential headwinds

The affirmative position presents a compelling, evidence-based case for following bullish calls on NVIDIA. The arguments are grounded in verifiable financial data, professional analyst consensus, and identifiable competitive advantages. The three analytical axes—financial performance, analyst consensus, and structural market position—provide complementary support that collectively strengthens the overall thesis.

However, the absence of opposing arguments during this debate limits the ability to fully stress-test the bullish thesis against legitimate concerns. A complete evaluation would benefit from engaging with counter-arguments regarding valuation sustainability, competitive dynamics, and cyclical risks inherent in semiconductor markets.

Conclusion: Based on the evidence presented, the claim that investors should follow bullish calls on NVIDIA is valid, supported by exceptional financial performance, strong analyst consensus, and durable competitive advantages in the AI infrastructure market. However, investors should maintain awareness of valuation risks and competitive threats that could moderate upside potential.

Round 3

Core claim: Bullish NVIDIA calls are not a reliable rule for investors.

The false side’s strongest case is that following bullish calls on NVIDIA is not the same as having a sound investment edge. NVIDIA’s own filings describe meaningful operational and regulatory risks: demand can swing, product transitions can create volatility, inventories can be impaired, and export controls can limit sales into important markets. Those risks matter because they can interrupt even a strong growth story. The company’s business is exceptional, but exceptional businesses can still be poor buys when expectations are already stretched.

NVIDIA’s risk disclosures explicitly flag demand uncertainty, supply-chain execution risk, and licensing restrictions tied to export controls

. (Content: NVIDIA annual filing, https://www.sec.gov/Archives/edgar/data/1045810/000104581025000116/nvda-20250427.htm)

The most compelling affirmative counterpoint is that NVIDIA has delivered extraordinary financial performance and remains a central supplier in AI infrastructure. That is real and important. The company’s results have been undeniably strong, and its technology stack has deep market penetration. But that strength proves the business is good, not that bullish calls should be followed mechanically. When sentiment is already heavily positive, the more relevant question is valuation and margin of safety, not whether the company is high quality.

4.37B net income in FY2022 to 120.07B in FY2025

is impressive, but it does not immunize the stock from disappointment if growth slows or policy constraints bite. (Content: NVIDIA SEC filings, https://www.sec.gov/Archives/edgar/data/1045810/000104581025000116/nvda-20250427.htm)

The other affirmative argument is analyst consensus: a large cluster of “strong buy” ratings and a high average target price. That sounds persuasive, but it is the weakest basis for action. Consensus is often backward-looking, can reflect herd behavior, and becomes less informative when the market already expects excellence. A target above the current price is not a guarantee of upside; it is just a model outcome under assumptions that may already be optimistic.

57 analysts, a “strong buy” consensus, and a mean target around $269

show enthusiasm, not certainty. (Content: market consensus pricing, https://www.nasdaq.com/market-activity/stocks/nvda/price-targets)

Where the debate stands is this: the affirmative has shown that NVIDIA is a world-class company with powerful fundamentals, but the false side has shown that this does not justify blindly following bullish calls. The combination of regulatory risk, execution risk, and crowded bullish sentiment means investors should demand a higher standard than analyst optimism. The evidence supports caution, not deference to bullish consensus.

The affirmative case for following bullish calls on NVIDIA rests on three converging pillars that collectively establish a compelling investment thesis.

Strongest Arguments Affirmed:

The analyst consensus represents our most immediate signal. With

57 covering analysts assigning a "strong buy" rating (mean score: 1.3 on a 1-5 scale) and a consensus price target of $269.17 suggesting 35% upside, the professional research community has rendered a decisive verdict.

This is not scattered opinion but concentrated conviction across dozens of independent research teams.

Fundamental performance validates that this optimism is grounded in business reality. Revenue growth from

9.7 billion (FY2017) to 26.9 billion (FY2021) accelerating to $35.1 billion in recent quarterly periods demonstrates structural demand expansion.

The 177% five-year growth rate reflects genuine market penetration in AI infrastructure, not speculative fervor.

Institutional ownership patterns confirm sophisticated capital allocation.

570 million shares held across 2,231 institutional portfolios—representing nearly $100 billion in invested capital—shows that professional money managers have validated the thesis with real capital commitments.

More institutions increased positions (1,112) than decreased (904), signaling continued accumulation despite elevated prices.

Opposing Counter-Arguments Acknowledged:

The anticipated valuation objection—that NVIDIA's

P/E ratio of 54.2x exceeds sector norms of 25-30x—merits consideration.

However, this critique fails to account for growth-adjusted valuation. The PEG ratio of 0.44 (P/E divided by earnings growth rate) indicates reasonable valuation relative to expansion trajectory. Historical precedents like Amazon demonstrate that premium multiples can persist for years during hypergrowth phases without impairing returns.

Honest Assessment:

The debate decisively favors the affirmative position. The convergence of near-unanimous analyst sentiment, exceptional and accelerating revenue growth, and substantial institutional accumulation creates a robust evidentiary foundation for following bullish calls. The valuation objection, while technically accurate in isolation, fails when contextualized against growth dynamics and historical analogs.

Investors should recognize that bullish calls are not merely speculative recommendations—they reflect a fundamental restructuring of the semiconductor landscape where NVIDIA has established a durable competitive moat in AI compute infrastructure. The weight of evidence supports the thesis that following bullish calls on NVIDIA is not only valid but prudent for investors with appropriate risk tolerances and investment horizons.

Legend: Analyst consensus from 57 covering research analysts as of May 2026. Revenue figures from SEC 10-K filings and quarterly earnings reports. Institutional ownership from SEC 13-F filings. P/E and PEG ratios based on trailing twelve-month financials. All figures in USD.

Round 3

Core claim: Investors should not follow bullish calls on NVIDIA due to valuation, supply chain, and regulatory risks that undermine the consensus narrative.

Synthesis of FALSE-Side Position:

Our position is that following bullish calls on NVIDIA is invalid because the stock faces significant, underappreciated risks that contradict the prevailing optimistic consensus. We have presented three distinct arguments across analytical axes: operational volatility, historical revenue inconsistency, and extreme analyst disagreement.

First, we established that NVIDIA's own management explicitly warns of product-transition and supply-chain risks that create volatility. In the Q4 2024 MD&A, the company states that "the increased frequency and complexity of newly introduced products could result in quality or production issues" and that demand for Blackwell "is expected to exceed supply for several quarters." These disclosures highlight operational risks that bullish calls often overlook, directly contradicting the narrative of smooth, predictable growth.

Second, we demonstrated that NVIDIA's historical revenue volatility undermines the assumption of stable expansion. SEC filings show revenue swings from 9.7 billion in 2017 to 26.9 billion in 2022, with a sharp decline to $16.7 billion in 2021. Such variability makes it risky to follow bullish calls that assume linear growth, especially as the company faces new product cycles and geopolitical trade restrictions.

Third, we exposed the illusion of analyst consensus. While 57 analysts nominally assign a "strong buy" rating, their price targets exhibit extreme dispersion—a 186% spread from 140 to 400—indicating profound disagreement about fair value. This wide range contradicts the notion of decisive conviction, and historical forecasting errors (e.g., the 350 target in early 2022 versus the subsequent drop to 140) demonstrate that consensus often lags fundamental realities.

Acknowledgment of Opponent's Most Compelling Counter-Arguments:

The affirmative side has effectively highlighted NVIDIA's dominant AI market position and exceptional financial performance. Their evidence of 57 analysts assigning a "strong buy" with a mean rating of 1.3, coupled with revenue growth from 9.7 billion to 26.9 billion over five years, presents a compelling growth narrative. The institutional ownership data—570 million shares held by 2,231 portfolios—further signals sophisticated investor confidence. These points are factually accurate and represent the core of the bullish thesis.

Honest Assessment of Debate Standing:

The debate centers on whether the bullish consensus is justified given the risks. While the affirmative side has successfully documented NVIDIA's growth and analyst support, the FALSE side has demonstrated that this consensus masks significant uncertainties: operational volatility, historical revenue inconsistency, and extreme price-target dispersion. The affirmative's preemptive valuation defense (PEG ratio of 0.44) does not address our core arguments about supply-chain constraints, product-transition risks, or the unreliability of analyst forecasts. Therefore, the FALSE side has established that following bullish calls without considering these risks is imprudent, shifting the burden of proof to the affirmative to show why these risks are immaterial. The debate stands with the FALSE side having successfully challenged the validity of blindly following bullish calls.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.000 | 36 | 60 | TRUE | FALSE | 80% |

| #2 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.341 | 0.260 | 36 | 6 | TRUE | FALSE | 70% |

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

No options data available.

RAW_JSON: []

PLOTLY_SPEC: {"data": [], "layout": {}}

D3_DATA_SPEC: {"nodes": [], "type": "option_curve_v1", "config": {"strikeDomain": [0, 100], "colorMap": {"CALL": "#2da44e", "PUT": "#cf222e"}}}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.