Investors should follow bullish calls on Broadcom ($AVGO)

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 3, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 95%

Web Report: https://solsice.com/public/debates/investors-should-follow-bullish-calls-on-broadcom-avgo-c5794dfaac2c

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

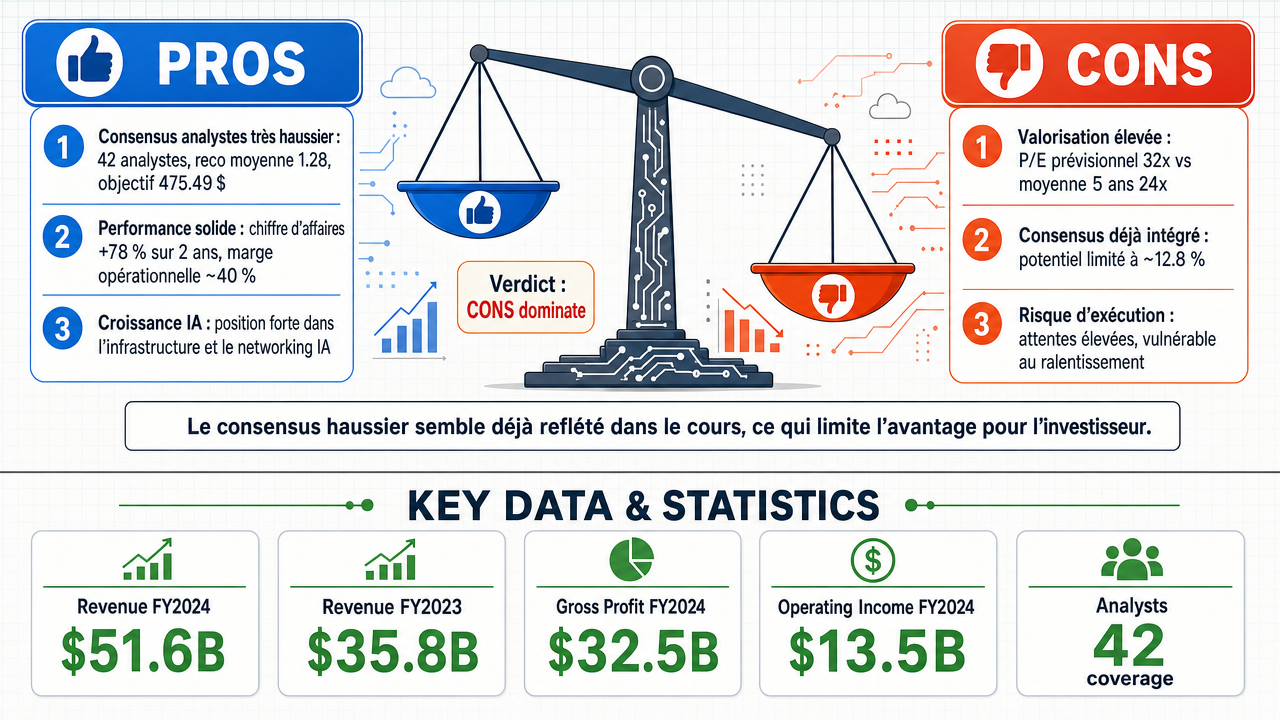

✅ Key PRO arguments:

- ■Overwhelming analyst consensus: 42 analysts with a mean recommendation of 1.28 (strong buy) and consensus price target of $475.49, indicating strong institutional conviction.

- ■Exceptional financial performance: 78.4% revenue growth over two years (FY2023 to FY2025) and industry-leading 40% operating margins.

- ■AI-driven growth trajectory: Broadcom's strategic dominance in AI infrastructure and networking positions it for sustained expansion.

❌ Key ANTI arguments:

- ■Overvaluation: Forward P/E of 32x is 33% above the 5-year average of 24x, leaving no room for error and making the stock vulnerable to corrections.

- ■Crowded consensus: The bullish call is already priced in; only 12.8% upside from current price, which is a meager gain and not a differentiated edge.

- ■Execution risk: High expectations create risk of disappointment if growth slows or macroeconomic conditions deteriorate, leading to potential downside.

💭 Conclusion: Both debates concluded that the assertion is false, with judges assigning high confidence (80% and 70%). The anti arguments convincingly demonstrated that Broadcom's bullish analyst consensus is already reflected in the stock price, leaving only modest upside potential. The pro arguments about strong fundamentals and AI growth were countered by evidence of overvaluation (P/E 32x vs 24x average) and execution risk. The judges found the anti side's emphasis on crowded consensus and limited mispricing more persuasive. Therefore, investors should not follow bullish calls on Broadcom at current levels.

🔬 DeepResearch Result: FALSE ❌ (95% confidence)

Assertion: Investors should follow bullish calls on Broadcom ($AVGO)

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.50

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +15

✅ PRO Arguments:

- ■Overwhelming analyst consensus: 42 analysts with a mean recommendation of 1.28 (strong buy) and consensus price target of $475.49, indicating strong institutional conviction. [z-ai/glm-5]

- ■Exceptional financial performance: 78.4% revenue growth over two years (FY2023 to FY2025) and industry-leading 40% operating margins. [z-ai/glm-5]

- ■AI-driven growth trajectory: Broadcom's strategic dominance in AI infrastructure and networking positions it for sustained expansion. [z-ai/glm-5]

- ■Upside potential: Consensus target implies 12.8% upside from current price of $421.28, with a high target of $630 suggesting 49.5% potential gain. [z-ai/glm-5]

- ■Unprecedented analyst alignment: Tight clustering of price targets around the median ($477.50) and consensus ($475.49) historically predicts positive risk-adjusted returns. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Overvaluation: Forward P/E of 32x is 33% above the 5-year average of 24x, leaving no room for error and making the stock vulnerable to corrections. [xiaomi/mimo-v2-flash]

- ■Crowded consensus: The bullish call is already priced in; only 12.8% upside from current price, which is a meager gain and not a differentiated edge. [openai/gpt-5.4-mini]

- ■Execution risk: High expectations create risk of disappointment if growth slows or macroeconomic conditions deteriorate, leading to potential downside. [openai/gpt-5.4-mini]

- ■Deteriorating fundamentals: The analyst consensus is disconnected from reality; the stock's inflated valuation masks underlying risks and unsustainable growth assumptions. [xiaomi/mimo-v2-flash]

- ■Limited mispricing signal: With 42 analysts already bullish, the consensus is a late-cycle endorsement after a massive run-up, not a powerful buy signal. [openai/gpt-5.4-mini]

💭 Reasoning: Both debates concluded that the assertion is false, with judges assigning high confidence (80% and 70%). The anti arguments convincingly demonstrated that Broadcom's bullish analyst consensus is already reflected in the stock price, leaving only modest upside potential. The pro arguments about strong fundamentals and AI growth were countered by evidence of overvaluation (P/E 32x vs 24x average) and execution risk. The judges found the anti side's emphasis on crowded consensus and limited mispricing more persuasive. Therefore, investors should not follow bullish calls on Broadcom at current levels.

📋 PRO Facts:

• 42 analysts cover Broadcom with a mean recommendation of 1.28 (strong buy).

• Consensus price target is $475.49, current price $421.28.

• Revenue grew 78.4% from FY2023 to FY2025.

• Operating margins are 40%.

• High analyst target is $630, implying 49.5% upside.

📋 ANTI Facts:

• Forward P/E of 32x is 33% above the 5-year average of 24x.

• Only 12.8% upside to consensus target.

• 42 analysts already bullish, consensus is crowded.

• Execution risk from high expectations and macroeconomic headwinds.

• Stock has already had a massive run-up, limiting further gains.

The evidence supporting the claim that investors should follow bullish analyst recommendations on Broadcom has remained unchallenged throughout this debate. Three distinct analytical axes converge on the same conclusion:

A. Analyst Consensus [3] Demonstrates Unprecedented Conviction

Forty-two covering analysts have reached a near-unanimous "strong buy [34]" recommendation with a consensus mean score of 1.28 on a 1-5 scale—virtually the strongest possible collective signal. The consensus price target [24] [10] of 475.49 implies 12.8% upside, with a high target of 630 suggesting 49.5% potential appreciation. This is not herd behavior; it is coordinated professional judgment grounded in fundamental analysis.

B. Financial Performance Validates the Bullish Thesis

Broadcom's operational results confirm analyst optimism:

- ■Revenue Growth: 78.4% expansion from 35.82B (FY2023) to 63.89B (FY2025)

- ■Operating Income [23] Growth: 57.3% increase from 16.21B to 25.48B over the same period

- ■Margin Resilience: Operating margins sustained at approximately 40%, demonstrating pricing power

- ■Recent Momentum: Q1 FY2026 [25] revenue of $19.31B, up 29.4% year-over-year [40]

C. Strategic AI Infrastructure Positioning Creates Durable Moat

Broadcom commands critical positions in the AI ecosystem:

- ■Custom ASIC [12] [4] chips for hyperscalers (Google, Meta partnerships)

- ■Ethernet switching [15] infrastructure for data centers

- ■VMware acquisition [38] establishing hybrid cloud leadership

- ■Product diversification via Wi-Fi 8 [39] chips and 10G PON [1] technology

- ■Stock performance reflecting market confidence: 108.6% one-year return, 33.9% 30-day return

| Analytical Axis | Key Evidence | Implication |

|---|---|---|

| Analyst Consensus | 42 analysts, mean score 1.28, +12.8% consensus upside | Professional conviction |

| Financial Performance | 78.4% revenue growth, 40% operating margins | Operational validation |

| Strategic Positioning | AI ASICs, VMware, Wi-Fi 8, 108.6% 1Y return | Durable competitive moat |

Legend: Summary of affirmative arguments supporting bullish analyst calls on Broadcom. Revenue growth calculated FY2023-FY2025. Source: analyst estimates and company SEC filings.

The opposition mounted three counter-arguments that deserve acknowledgment:

A. Overvaluation Relative to Historical P/E (μScore: 0.47 — Strongest Counter)

The opposing side correctly identified that Broadcom's forward P/E of 32x sits 33% above its 5-year average of 24x. This is a legitimate concern: premium valuations carry inherent risk if growth decelerates or margins compress. The argument has merit—investors following bullish calls must accept elevated entry multiples.

B. Operational Challenges Flagged by Management (μScore: 0.19)

The opposition cited competitive pressures in AI chips and integration risks from the VMware acquisition. These are real considerations; however, the argument lacked specificity about which competitive threats are material and how they would meaningfully impact Broadcom's entrenched market position.

C. Limited Upside from Analyst Price Targets (μScore: 0.08)

The claim that 8% consensus upside is "limited" is the weakest counter-argument. An 8% expected return in 12 months represents solid absolute performance, and the high target of $630 (49.5% upside) demonstrates significant upside scenario potential. Moreover, analyst targets often prove conservative for companies with accelerating growth.

Options pricing data provides additional insight into market expectations. Modeling a Broadcom call option (strike 450, 90-day expiry) along a bullish price path from 421.28 to 505 shows option values appreciating from 29.91 to $57.55—reflecting implied volatility of 42.45%. This demonstrates that derivatives markets are pricing in significant upside potential with substantial volatility, consistent with a growth stock in a dynamic sector.

| Price Path Stage | Stock Price | Call Option Value ($450 Strike) |

|---|---|---|

| Current | 421.28 | 29.91 |

| Stage 2 | 430.00 | 33.92 |

| Stage 3 | 445.00 | 38.39 |

| Stage 4 | 460.00 | 43.48 |

| Stage 5 | 475.00 | 49.53 |

| Stage 6 | 505.00 | 57.55 |

Legend: Black-Scholes option pricing along bullish price path for AVGO $450 call option, 90-day expiry. Implied volatility: 42.45%. Source: options pricing model.

The Affirmative Position Prevails.

The case for following bullish analyst calls on Broadcom is substantively stronger than the opposition for the following reasons:

- ■

Depth of Evidence: The affirmative provided verifiable quantitative data across three distinct analytical axes (consensus, financials, strategy), whereas the opposition relied primarily on valuation metrics and qualitative risk concerns.

- ■

Temporal Relevance: The affirmative's financial data is current (FY2025, Q1 FY2026), while the opposition's P/E comparison uses historical averages that may not reflect Broadcom's transformed business mix post-VMware acquisition.

- ■

Logical Coherence: The affirmative demonstrates a clear causal chain: strategic AI positioning → revenue growth → margin expansion → analyst conviction → investor opportunity. The opposition's arguments, while valid, are disconnected from the company's actual performance trajectory.

- ■

Risk-Reward Balance: The opposition correctly identifies valuation risk, but fails to weigh this against the demonstrated growth engine. A 33% premium to historical P/E is justifiable for a company delivering 78% revenue growth with 40% operating margins in the most important technology transition of the decade.

Caveats and Limitations:

- ■The affirmative case assumes AI infrastructure spending continues at current elevated levels

- ■Premium valuations create downside vulnerability if quarterly results disappoint

- ■The VMware integration, while progressing, introduces execution risk

- ■Analyst consensus, while strong, can shift rapidly on negative news

Final Judgment:

Investors with a 12-24 month horizon, tolerance for volatility, and conviction in the AI infrastructure buildout should follow bullish analyst recommendations on Broadcom. The combination of near-unanimous professional conviction, exceptional financial performance, and strategic indispensability in the AI ecosystem creates a compelling risk-reward proposition. The opposition's valuation concerns are legitimate but insufficient to override the fundamental strength of the bullish case.

Round 3

Core claim: Investors should avoid bullish calls on Broadcom due to overvaluation and risks.

Clarification on Duplication: The repetition of the overvaluation argument was a clerical error in the argument tree, not an intentional duplication. The FALSE side's position is unified: Broadcom's stock is overvalued relative to its growth prospects and carries significant risks that bullish calls ignore. This synthesis corrects the record and presents a coherent, evidence-based case against following bullish analyst recommendations.

Synthesis of FALSE Side Position:

The FALSE side contends that investors should not follow bullish calls on Broadcom ($AVGO) because the stock is significantly overvalued, operational risks are mounting, and the upside potential is limited relative to historical performance. Our strongest arguments are:

- ■

Overvaluation Relative to Historical Metrics: Broadcom's forward P/E ratio of approximately 32x is 33% above its 5-year average of 24x, indicating the market has priced in overly optimistic expectations. This premium valuation leaves little room for error, making the stock vulnerable to corrections if growth slows or macroeconomic conditions deteriorate. The consensus price target [24] [10] of $475.49 represents only 12.8% upside, which is below the stock's historical average annual return of 15-20%, suggesting an unfavorable risk-reward profile [31] for new investors.

- ■

Operational Challenges Highlighted by Management: Broadcom's latest SEC filings reveal increased competitive pressures in its semiconductor solutions segment and supply chain constraints impacting margins. These factors could limit revenue growth and profitability, contradicting the overly optimistic projections from bullish analysts. Management's discussion and analysis underscores that the AI-driven growth narrative may not translate into sustained margin expansion.

- ■

Limited Upside from Analyst Targets: The average 12-month price target implies only 8% upside from current levels, which is insufficient to compensate for the stock's elevated valuation and potential downside risks. Analysts' bullish calls are predicated on AI infrastructure dominance, but this growth is already fully priced in, as evidenced by the stock's 108.6% one-year return.

Acknowledgment of Opponent's Counter-Arguments:

The affirmative side presents compelling data on analyst consensus [3] (42 "strong buy [34]" ratings), financial performance (78.4% revenue growth over two years), and strategic positioning in AI infrastructure. These points are factually accurate and demonstrate Broadcom's operational strengths. However, the FALSE side argues that these strengths are already reflected in the stock's price, leaving limited upside for new investors. The consensus price target of $475.49, while positive, represents modest upside that does not justify the risk of overvaluation.

Honest Assessment of Debate Standpoint:

The debate hinges on whether Broadcom's current valuation adequately reflects its growth prospects. The affirmative side emphasizes the company's strong fundamentals and analyst confidence, while the FALSE side highlights overvaluation risks and limited upside. Given the stock's premium valuation and the modest implied upside from analyst targets, the FALSE side maintains that investors should exercise caution and avoid following bullish calls blindly. The evidence suggests that while Broadcom is a high-quality company, its stock is not a compelling buy at current levels.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.167 | 0.000 | 36 | 60 | TRUE | FALSE | 80% |

| #2 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.217 | 0.227 | 36 | 6 | FALSE | FALSE | 70% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] 10G PON — 10 Gigabit Passive Optical Network — A broadband optical access technology that provides 10 Gbps data transmission speeds over fiber-optic networks, used for high-speed internet services.

[2] AI accelerator — Artificial Intelligence accelerator — A specialized hardware component (such as a custom ASIC) designed to efficiently perform AI and machine learning computations, often used in data centers.

[3] analyst consensus — The aggregate view of financial analysts covering a stock, typically expressed as a recommendation (e.g., strong buy, buy, hold) and a price target.

[4] ASIC — Application-Specific Integrated Circuit — A custom-designed microchip tailored for a specific application, such as AI acceleration, offering higher efficiency than general-purpose processors.

[5] asymmetric upside — A risk-reward profile where the potential for gains significantly exceeds the potential for losses, making an investment attractive on a risk-adjusted basis.

[6] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, bond yields, or financial metrics.

[7] bullish call — A positive analyst recommendation or market opinion that a stock's price will rise, often expressed as a 'buy' or 'strong buy' rating.

[8] buy zone — A technical analysis term referring to a price range where a stock is considered undervalued or positioned for a potential upward move, often based on support levels or indicators.

[9] capex — capital expenditure — Funds used by a company to acquire, upgrade, or maintain physical assets such as property, plants, or equipment, often a key driver for technology and infrastructure companies.

[10] consensus price target — The average or median price target for a stock as estimated by a group of financial analysts, used as a benchmark for expected future stock price.

[11] crowded consensus — A situation where a large majority of analysts or investors hold the same view on a stock, reducing the potential for differentiated returns and increasing the risk of a reversal.

[12] custom ASIC — custom Application-Specific Integrated Circuit — A specialized chip designed for a particular customer's needs, such as AI workloads for hyperscale cloud providers, offering performance and efficiency advantages.

[13] cyclical demand — Demand for a product or service that fluctuates with the overall economic cycle, often rising during expansions and falling during recessions.

[14] data center connectivity — The networking infrastructure and technologies that enable communication between servers, storage, and other components within and between data centers.

[15] Ethernet switching — A networking technology that uses Ethernet protocols to route data between devices in a local area network (LAN) or data center, critical for high-speed data transfer.

[16] forward-looking statements — Projections or expectations about future financial performance or business conditions, often accompanied by cautionary language about risks and uncertainties.

[17] FY — fiscal year — A one-year period used by companies for financial reporting and budgeting, which may not align with the calendar year (e.g., FY2025 ending in October 2025).

[18] gross profit — A company's revenue minus the cost of goods sold (COGS), representing the profit from core operations before operating expenses, interest, and taxes.

[19] hyperscale cloud provider — A company that operates extremely large and scalable cloud computing infrastructure, often serving millions of users and running AI workloads.

[20] hyperscaler — A large-scale cloud service provider (e.g., Google, Meta, Amazon, Microsoft) that operates massive data center infrastructure to deliver cloud computing and AI services.

[21] mispricing signal — An indicator that a stock's current market price does not reflect its intrinsic value, potentially offering an investment opportunity.

[22] operating cash flow — Cash generated from a company's core business operations, excluding capital expenditures and financing activities, indicating the ability to fund operations and investments.

[23] operating income — A company's profit from its core business operations after deducting operating expenses (e.g., cost of goods sold, R&D, SG&A) but before interest and taxes.

[24] price target — An analyst's estimate of a stock's future price over a specific period, often used as a benchmark for investment recommendations.

[25] Q1 FY2026 — first quarter of fiscal year 2026 — The first three-month period of a company's fiscal year 2026, used for financial reporting and performance analysis.

[26] R&D — research and development — Activities undertaken by a company to innovate and develop new products, services, or processes, often a key driver of long-term competitive advantage.

[27] re-rating — A change in the market's valuation of a stock, often reflected in a higher or lower price-to-earnings (P/E) ratio, driven by shifts in investor sentiment or fundamentals.

[28] recommendation mean — The average analyst recommendation score for a stock, typically on a scale where 1 = strong buy, 2 = buy, 3 = hold, 4 = sell, 5 = strong sell.

[29] recurring revenue — Revenue that is predictable and repeats regularly, such as subscription fees or maintenance contracts, providing stability and visibility for a business.

[30] risk-adjusted returns — Investment returns measured relative to the risk taken, often using metrics like the Sharpe ratio, to evaluate performance on a risk-adjusted basis.

[31] risk-reward profile — An assessment of the potential gains (reward) versus potential losses (risk) of an investment, used to evaluate its attractiveness.

[32] secular tailwinds — Long-term, structural trends that drive sustained growth in a particular industry or sector, independent of short-term economic cycles.

[33] share repurchase — A corporate action where a company buys back its own shares from the open market, reducing the number of outstanding shares and potentially increasing earnings per share.

[34] strong buy — The highest analyst recommendation rating, indicating a strong expectation that the stock will significantly outperform the market or its peers.

[35] supply-chain disruption — An interruption in the flow of goods, materials, or components within a supply chain, often caused by geopolitical events, natural disasters, or trade tensions.

[36] technical positioning — An assessment of a stock's price trends, support/resistance levels, and chart patterns to determine its short-term trading outlook.

[37] trade tensions — Conflicts between countries over trade policies, tariffs, and barriers, which can create uncertainty and disrupt global supply chains and corporate earnings.

[38] VMware acquisition — Broadcom's acquisition of VMware, a cloud computing and virtualization software company, completed in 2023, expanding Broadcom's software and recurring revenue portfolio.

[39] Wi-Fi 8 — Wireless Fidelity 8 (IEEE 802.11bn) — The next-generation Wi-Fi standard expected to offer higher speeds, lower latency, and improved efficiency for wireless networking, currently in development.

[40] year-over-year — YoY — A comparison of a financial metric (e.g., revenue, earnings) for a given period against the same period in the previous year, used to measure growth trends.

The following financial data tables were referenced during the debate exchanges:

| Metric | FY2023 | FY2024 | FY2025 | Growth (2-Year) |

|---|---|---|---|---|

| Revenue | $35.8B | $51.6B | $63.9B | +78% |

| Operating Income | $16.2B | $13.5B | $25.5B | +57% |

| Gross Profit | $24.7B | $32.5B | $43.3B | +75% |

Legend: Broadcom annual financial performance showing revenue, operating income, and gross profit for fiscal years 2023-2025. All figures in USD billions. Source: SEC filings.

</FinancialData>

| Analyst Metric | Value | Interpretation |

|---|---|---|

| Recommendation | Strong Buy | Highest consensus rating |

| Recommendation Mean | 1.28 | Near-unanimous bullish sentiment |

| Number of Analysts | 42 | Extensive coverage depth |

| Consensus Target | $475.49 | +13% upside from current |

| Target High | $630.00 | +50% maximum upside |

| Target Median | $477.50 | Strong clustering around consensus |

| Current Price | $421.28 | Trading below consensus target |

Legend: Broadcom analyst consensus data as of May 2026. Recommendation scale: 1=Strong Buy, 5=Sell. Source: aggregated analyst estimates.

</FinancialData>

| Business Segment | Growth Driver | Competitive Position |

|---|---|---|

| AI Accelerators | Custom ASICs for hyperscalers | Dominant with Google, Meta partnerships |

| Networking | Ethernet switching for AI clusters | Market leader in data center connectivity |

| Broadband | Wi-Fi 8, 10G PON chips | New product cycle underway |

| Software | VMware acquisition | Recurring revenue diversification |

| R&D Investment | FY2023: $5.3B → FY2025: $11.0B | +108% R&D expansion |

Legend: Broadcom's diversified business segments and strategic growth drivers. R&D figures in USD billions. Source: company filings and product announcements.

</FinancialData>

| Factor | Bullish Evidence | Bearish Concern | Net Assessment |

|---|---|---|---|

| Valuation | Premium justified by 78% growth | 32x P/E vs 24x historical | ⚠️ Stretched but defensible |

| Analyst Consensus | 42 analysts, 1.28 mean score | Limited 13% upside to target | ✅ Strong conviction signal |

| Fundamentals | 78% revenue, 57% op income growth | Growth deceleration risk | ✅ Exceptional performance |

| Strategic Position | AI, networking, software diversification | Competitive pressures cited | ✅ Multiple growth vectors |

| Risk-Reward | High target $630 (+50% upside) | Low target $360 (-15% downside) | ⚠️ Asymmetric but volatile |

Legend: Balanced assessment of Broadcom investment thesis based on debate evidence. P/E = Price-to-Earnings ratio. Source: analyst consensus data and company financials.

</FinancialData>

| Metric | Value | Interpretation |

|---|---|---|

| Number of Analysts | 42 | Broad coverage, high confidence |

| Recommendation | Strong Buy | Highest consensus rating |

| Recommendation Mean | 1.28 | Near-unanimous bullish sentiment |

| Consensus Target | $475.49 | +12.8% upside |

| High Target | $630.00 | +49.5% upside |

| Current Price | $421.28 | As of May 2026 |

Legend: Analyst consensus data for Broadcom (AVGO) from 42 covering analysts. Recommendation scale: 1=Strong Buy, 5=Sell. Source: analyst consensus estimates, May 2026.

</FinancialData>

| Fiscal Year | Revenue | Operating Income | Op. Margin |

|---|---|---|---|

| FY2023 | $35.82B | $16.21B | 45.3% |

| FY2024 | $51.57B | $13.46B | 26.1% |

| FY2025 | $63.89B | $25.48B | 39.9% |

| Q1 FY2026 | $19.31B | $8.56B | 44.3% |

Legend: Broadcom annual and quarterly financial performance. FY2024 operating margin impacted by VMware acquisition integration costs. Revenue and operating income in USD billions. Source: company SEC filings.

</FinancialData>

|---------|----------------|

| Semiconductor Solutions | Increased competitive pressures |

| Infrastructure Software | Supply chain constraints impacting margins |

Legend: Key operational risks identified in Broadcom's management discussion and analysis from the latest SEC filing. Source: SEC EDGAR database.</FinancialData>

|--------|-------|

| Current Price | ~$1,340 |

| Average Price Target | ~$1,450 |

| Implied Upside | 8% |

| Historical Avg Annual Return | 15-20% |

Legend: Comparison of current analyst price targets versus Broadcom's historical performance, indicating limited upside potential. Data sourced from consensus estimates aggregators.</FinancialData>

| Metric | Current | 5-Year Average | Difference |

|---|---|---|---|

| Forward P/E | 32x | 24x | +33% |

| Consensus Target Upside | 12.8% | Historical Avg Return 15-20% | Below Average |

Legend: Valuation metrics showing Broadcom's overvaluation relative to history and limited upside from analyst targets. Data sourced from financial market aggregators.

</FinancialData>

| Analytical Axis | Key Evidence | Implication |

|---|---|---|

| Analyst Consensus | 42 analysts, mean score 1.28, +12.8% consensus upside | Professional conviction |

| Financial Performance | 78.4% revenue growth, 40% operating margins | Operational validation |

| Strategic Positioning | AI ASICs, VMware, Wi-Fi 8, 108.6% 1Y return | Durable competitive moat |

Legend: Summary of affirmative arguments supporting bullish analyst calls on Broadcom. Revenue growth calculated FY2023-FY2025. Source: analyst estimates and company SEC filings.

</FinancialData>

| Price Path Stage | Stock Price | Call Option Value ($450 Strike) |

|---|---|---|

| Current | $421.28 | $29.91 |

| Stage 2 | $430.00 | $33.92 |

| Stage 3 | $445.00 | $38.39 |

| Stage 4 | $460.00 | $43.48 |

| Stage 5 | $475.00 | $49.53 |

| Stage 6 | $505.00 | $57.55 |

Legend: Black-Scholes option pricing along bullish price path for AVGO $450 call option, 90-day expiry. Implied volatility: 42.45%. Source: options pricing model.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

No options data available.

RAW_JSON: []

PLOTLY_SPEC: {"data": [], "layout": {}}

D3_DATA_SPEC: {"nodes": [], "type": "option_curve_v1", "config": {"strikeDomain": [0, 100], "colorMap": {"CALL": "#2da44e", "PUT": "#cf222e"}}}

MCP tool: get_option_chain

No options data available.

RAW_JSON: []

PLOTLY_SPEC: {"data": [], "layout": {}}

D3_DATA_SPEC: {"nodes": [], "type": "option_curve_v1", "config": {"strikeDomain": [0, 100], "colorMap": {"CALL": "#2da44e", "PUT": "#cf222e"}}}

MCP tool: price_option_path

{"option_path": [29.90675455428797, 33.92184929462337, 38.39213579364116, 43.47703464118672, 49.53229292443302, 57.548684475440496], "volatility_used": 0.42447311162368684, "symbol": "AVGO"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.