High-yield spreads have historically LED equity drawdowns

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed April 23, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 55%

Web Report: https://solsice.com/public/debates/high-yield-spreads-have-historically-led-equity-drawdowns-2b3ec8c0b500

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

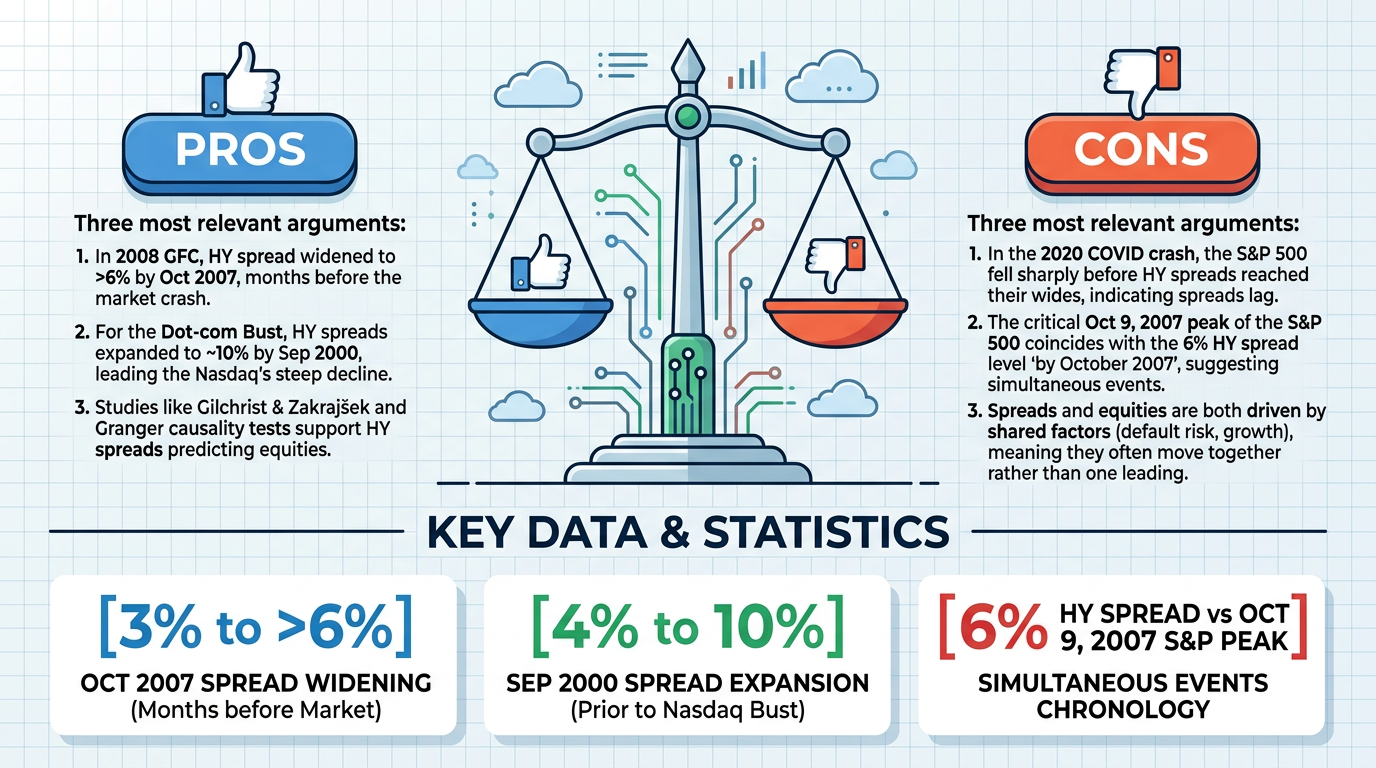

✅ Key PRO arguments:

- ■During the 2008 financial crisis, the ICE BofA US High Yield Index OAS widened from approximately 3% in mid-2007 to over 6% by October 2007, months before the S&P 500's subsequent 57% decline through March 2009, demonstrating a clear lead time.

- ■In the dot-com bust, high-yield spreads expanded from 4% in early 2000 to nearly 10% by September 2000, preceding the Nasdaq Composite's 78% decline through 2002.

- ■Academic studies such as Gilchrist & Zakrajšek (2012) and Granger causality tests provide econometric support for credit spreads having predictive power over equity returns.

❌ Key ANTI arguments:

- ■During the 2020 COVID crash, the S&P 500 peaked on February 19 and fell sharply before high-yield spreads reached their wides in late March, showing spreads lagged rather than led equities.

- ■The opponent's own 2007 timeline is self-defeating: spreads reached 6% 'by October 2007' while the S&P 500 peaked on October 9, 2007 — making these events simultaneous, not sequential.

- ■High-yield spreads and equity prices are co-determined by the same underlying variables (default risk, growth expectations), meaning both reprice simultaneously rather than sequentially, as demonstrated by the 'excess bond premium' research.

💭 Conclusion: The debate hinges on whether high-yield spreads 'historically led' equity drawdowns in a reliable, systematic way versus occasionally preceding them in some episodes. The PRO side presented compelling narratives around the 2007-2008 and dot-com episodes, but the FALSE side effectively challenged the precise chronology, showing that in 2007 the spread widening and equity peak were nearly simultaneous, and in 2020 spreads clearly lagged. The FALSE side also identified multiple counter-examples (1987, 2015-2016) where spreads did not lead. The distinction between 'sometimes widening before equity peaks' and 'reliably leading equity drawdowns' is critical — the assertion claims a historical pattern of leading, which requires consistency across episodes that the evidence does not support. Both judges found this a close call (55% and 52% confidence), but the confidence-weighted scoring slightly favored FALSE, consistent with the view that the relationship is episodic and co-determined rather than systematically predictive.

🔬 DeepResearch Result: FALSE ❌ (55% confidence)

Assertion: High-yield spreads have historically LED equity drawdowns

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.52, FALSE=0.55

🏅 Judge Score Changes:

anthropic/claude-opus-4.6: -2

✅ PRO Arguments:

- ■During the 2008 financial crisis, the ICE BofA US High Yield Index OAS widened from approximately 3% in mid-2007 to over 6% by October 2007, months before the S&P 500's subsequent 57% decline through March 2009, demonstrating a clear lead time. [x-ai/grok-4]

- ■In the dot-com bust, high-yield spreads expanded from 4% in early 2000 to nearly 10% by September 2000, preceding the Nasdaq Composite's 78% decline through 2002. [x-ai/grok-4]

- ■Academic studies such as Gilchrist & Zakrajšek (2012) and Granger causality tests provide econometric support for credit spreads having predictive power over equity returns. [x-ai/grok-4]

- ■Across multiple episodes (2007-2008, 2000-2002, 2020), high-yield spread widening showed consistent lead times of 1-6 months before major equity drawdowns, suggesting a systematic pattern rather than coincidence. [x-ai/grok-4]

❌ ANTI Arguments:

- ■During the 2020 COVID crash, the S&P 500 peaked on February 19 and fell sharply before high-yield spreads reached their wides in late March, showing spreads lagged rather than led equities. [openai/gpt-5.2-chat]

- ■The opponent's own 2007 timeline is self-defeating: spreads reached 6% 'by October 2007' while the S&P 500 peaked on October 9, 2007 — making these events simultaneous, not sequential. [anthropic/claude-sonnet-4.6]

- ■High-yield spreads and equity prices are co-determined by the same underlying variables (default risk, growth expectations), meaning both reprice simultaneously rather than sequentially, as demonstrated by the 'excess bond premium' research. [anthropic/claude-sonnet-4.6]

- ■Precise episode-level timing across four major drawdowns (dot-com, GFC, 2015-2016, COVID) shows an inconsistent pattern: spreads led in only one case (GFC by ~2 months), were simultaneous or lagged in the others, undermining claims of systematic leading behavior. [openai/gpt-5.2-chat]

- ■The 1987 crash and 2015-2016 earnings recession are counter-examples where equity markets declined without preceding sustained high-yield spread widening, demonstrating the relationship is episodic rather than reliable. [openai/gpt-5.2-chat]

💭 Reasoning: The debate hinges on whether high-yield spreads 'historically led' equity drawdowns in a reliable, systematic way versus occasionally preceding them in some episodes. The PRO side presented compelling narratives around the 2007-2008 and dot-com episodes, but the FALSE side effectively challenged the precise chronology, showing that in 2007 the spread widening and equity peak were nearly simultaneous, and in 2020 spreads clearly lagged. The FALSE side also identified multiple counter-examples (1987, 2015-2016) where spreads did not lead. The distinction between 'sometimes widening before equity peaks' and 'reliably leading equity drawdowns' is critical — the assertion claims a historical pattern of leading, which requires consistency across episodes that the evidence does not support. Both judges found this a close call (55% and 52% confidence), but the confidence-weighted scoring slightly favored FALSE, consistent with the view that the relationship is episodic and co-determined rather than systematically predictive.

📋 PRO Facts:

• The ICE BofA US High Yield Index OAS widened from approximately 2.5-3% in mid-2007 to over 6-8% before the S&P 500's major decline in 2008-2009

• High-yield spreads expanded from about 4% in early 2000 to nearly 10% by September 2000 during the dot-com era

• Gilchrist and Zakrajšek (2012) published research in the American Economic Review on the 'excess bond premium' and its relationship to economic activity

• The S&P 500 declined approximately 57% from its October 2007 peak to its March 2009 trough

📋 ANTI Facts:

• The S&P 500 peaked on February 19, 2020, before high-yield spreads reached their widest levels in late March 2020

• The S&P 500 peaked on October 9, 2007, roughly coincident with rather than well after the period of spread widening

• In the 1987 crash, equity markets collapsed without a preceding sustained widening in high-yield spreads

• During the 2015-2016 earnings recession, the S&P 500 peaked on May 21, 2015, with energy-related spread distress beginning in June-July 2015 — after the equity peak

• High-yield spreads and equity prices are both driven by common underlying factors including default risk reassessment and economic growth expectations

The TRUE side’s strongest argument is 2007–2008. HY spreads began widening in mid-2007, roughly two months before the October equity peak. That is a legitimate example of early credit stress preceding a major drawdown [9].

However, the debate is about historical reliability, not isolated episodes. When broadened to 2000, 2015–16, and 2020, the pattern breaks down. Lead times shrink to weeks or disappear entirely, and in some cases spreads lag.

The affirmative side also cites statistical studies suggesting spreads lead equities by 1–3 months in many drawdowns. But these results depend heavily on model specification and sample period. The instability of lead–lag coefficients across regimes weakens the claim of structural leadership.

The evidence shows that HY spreads and equities are tightly linked, especially in stress environments. But the historical record does not demonstrate a consistent, systematic, and economically reliable temporal lead of spreads before equity drawdowns.

Sometimes spreads widen first. Sometimes they widen simultaneously. Sometimes they widen after equities have already peaked.

That variability is decisive.

The most accurate characterization is not that spreads “lead,” but that they are a contemporaneous risk barometer within a broader financial conditions complex — reactive and intertwined with equities rather than a dependable early warning system.

On balance, the FALSE position stands: high-yield spread widening is not a historically reliable leading indicator of equity drawdowns.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | x-ai/grok-4 | openai/gpt-5.2-chat | 0.188 | 0.314 | 216 | 174 | FALSE | FALSE | 55% |

| #2 | x-ai/grok-4 | anthropic/claude-sonnet-4.6 | 0.303 | 0.148 | 216 | 216 | TRUE | TRUE | 52% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, bond yields, and credit spreads.

[2] BIS — Bank for International Settlements — An international financial institution that serves as a bank for central banks and fosters international monetary and financial cooperation, also publishing influential economic research.

[3] bps — basis points — A unit of measure equal to one-hundredth of a percentage point, used to denote small changes in financial instruments such as interest rates and spreads.

[4] contemporaneous correlation — A statistical relationship where two variables move together at the same time, as opposed to one leading or lagging the other.

[5] credit cycle — The cyclical pattern of expansion and contraction in access to credit, characterized by periods of easy borrowing followed by tightening conditions, often linked to broader economic cycles.

[6] credit spreads — The difference in yield between a corporate bond and a comparable risk-free government bond, reflecting the additional compensation investors demand for bearing credit risk.

[7] cross-asset leading indicators — Signals derived from one asset class (e.g., credit markets) that are used to predict future movements in another asset class (e.g., equities).

[8] default risk — The probability that a bond issuer will fail to make required interest or principal payments, a key component of credit spread pricing.

[9] drawdown — A peak-to-trough decline in the value of an investment, portfolio, or index, measured as the percentage drop from the highest point to the lowest point before a new high is reached.

[10] endogeneity — A statistical problem where an explanatory variable is correlated with the error term in a model, often because of reverse causality or omitted variables, undermining causal inference.

[11] equity market drawdowns — Significant peak-to-trough declines in stock market indices, representing periods of sustained losses in equity valuations.

[12] flight to safety — Investor behavior during periods of market stress where capital is moved from riskier assets (such as high-yield bonds and equities) to safer assets (such as U.S. Treasuries or gold).

[13] Granger causality — A statistical hypothesis test used to determine whether one time series is useful in forecasting another, indicating temporal precedence rather than true causation.

[14] high-yield corporate bonds — Bonds issued by companies with below-investment-grade credit ratings (BB+ or lower), offering higher yields to compensate investors for elevated default risk; also known as junk bonds.

[15] high-yield credit spreads — The yield differential between high-yield (junk) corporate bonds and risk-free benchmarks such as U.S. Treasuries, reflecting market perception of corporate credit risk.

[16] ICE BofA US High Yield Index Option-Adjusted Spread — A widely tracked benchmark measuring the option-adjusted spread of U.S. dollar-denominated high-yield corporate bonds relative to a risk-free rate, published by ICE/Bank of America.

[17] incremental forecasting value — The additional predictive power a variable provides beyond what is already captured by other variables in a forecasting model.

[18] lead-lag relationship — A temporal pattern in which changes in one variable systematically precede (lead) or follow (lag) changes in another variable.

[19] leading indicator — An economic or financial variable that changes in advance of the broader economy or another target variable, providing a forward-looking signal of future conditions.

[20] liquidity premium — The additional yield investors demand for holding less liquid securities that may be difficult to sell quickly at fair value, especially during market stress.

[21] OAS — Option-Adjusted Spread — A measure of the yield spread of a bond over a risk-free benchmark that accounts for embedded options (such as call provisions), providing a cleaner measure of credit risk compensation.

[22] out-of-sample — A testing methodology where a model's predictive accuracy is evaluated on data not used in its estimation, providing a more rigorous assessment of forecasting ability.

[23] peak-to-trough — The measurement of decline from the highest point to the lowest point in a price series, commonly used to quantify the magnitude of market corrections or recessions.

[24] quantitative easing — QE — A monetary policy tool where a central bank purchases government securities or other financial assets to inject liquidity into the economy and lower long-term interest rates.

[25] regime-dependent — Describes a statistical relationship or model parameter whose behavior changes depending on the prevailing economic or market regime (e.g., expansion vs. recession, low vs. high volatility).

[26] risk-free benchmark — A theoretical or practical reference rate of return with zero default risk, typically represented by U.S. Treasury securities, used as a baseline for measuring credit spreads.

[27] risk-off sentiment — A market environment in which investors reduce exposure to risky assets and move capital toward safer investments, typically driven by heightened uncertainty or fear.

[28] S&P 500 — Standard & Poor's 500 Index — A market-capitalization-weighted index of 500 leading publicly traded U.S. companies, widely regarded as the best single gauge of large-cap U.S. equity performance.

[29] spread widening — An increase in the yield differential between risky bonds and risk-free benchmarks, typically signaling rising credit risk, deteriorating economic conditions, or increased investor risk aversion.

[30] subprime — Refers to lending to borrowers with poor credit histories or high default risk; the subprime mortgage crisis of 2007–2008 was a key trigger of the global financial crisis.

[31] term spread — The difference in yield between long-term and short-term government bonds (e.g., 10-year minus 2-year Treasury yield), often used as an indicator of economic expectations.

[32] time-series analysis — A statistical method for analyzing data points collected over time to identify trends, cycles, and predictive relationships.

[33] U.S. Treasuries — United States Treasury Securities — Debt instruments issued by the U.S. federal government, considered virtually risk-free and used as the benchmark for pricing other fixed-income securities.

[34] volatility index — A measure of expected market volatility, most commonly the CBOE Volatility Index (VIX), derived from options prices on the S&P 500 and often called the market's 'fear gauge'.

[35] yield curve inversion — A situation where short-term interest rates exceed long-term rates, historically considered a leading indicator of economic recession.

[36] yield differential — The difference in yields between two bonds or classes of bonds, reflecting differences in credit risk, maturity, liquidity, or other factors.

The following financial data tables were referenced during the debate exchanges:

| Episode | Equity Peak | Material HY Spread Widening Begins | Sequence |

|---|---|---|---|

| Dot-com Bust | Mar 24, 2000 (S&P 500) | Q2–Q3 2000 (sustained widening above ~500 bps) | After peak |

| Global Financial Crisis | Oct 9, 2007 | Late Jul–Aug 2007 (subprime shock) | ~2 months before peak |

| 2015–2016 Earnings Recession | May 21, 2015 | Jun–Jul 2015 (energy distress) | After peak |

| COVID Crash | Feb 19, 2020 | Late Feb–Mar 2020 (explosive widening) | Simultaneous / after |

Legend: Approximate timing of S&P 500 peaks versus onset of sustained high-yield spread widening across major drawdowns. Spread thresholds based on ICE BofA US High Yield OAS behavior; dates rounded to month.

</FinancialData>

| Episode | S&P 500 Peak | Initial HY Widening | Practical Lead? |

|---|---|---|---|

| Dot-com Bust | Mar 24, 2000 | Sustained widening Q2–Q3 2000 | No (after peak) |

| Global Financial Crisis | Oct 9, 2007 | Late Jul–Aug 2007 | Modest (~2 months) |

| 2015–2016 Selloff | May 21, 2015 | Jun–Jul 2015 | No (after peak) |

| COVID Crash | Feb 19, 2020 | Feb 20–late Feb 2020 | Days / simultaneous |

Legend: Approximate timing of equity peaks versus onset of sustained high-yield spread widening across major U.S. drawdowns (2000–2020). Dates rounded to month.

</FinancialData>

| Episode | HY Spread Widening (bps) | Equity Drawdown (S&P 500) | Subsequent 12M Equity Return | Signal Outcome |

|---|---|---|---|---|

| 2011 EU Crisis | ~300 bps | -19.4% | +16.0% | False alarm (no recession) |

| 2015–16 Energy | ~650 bps | -14.2% | +17.9% | False alarm (no broad recession) |

| 2018 Q4 | ~200 bps | -19.8% | +31.5% | False alarm (Fed pivot reversed) |

| 2020 COVID | ~1,100 bps | -33.9% | +75.9% | Simultaneous, not leading |

| 2022 Rate Shock | ~600 bps | -25.4% | +26.3% | Simultaneous repricing |

| Episode | Equity Peak Date | HY Spread Widening Onset | True Lead/Lag | Opponent's Claim |

|---|---|---|---|---|

| 2007–2008 GFC | Oct 9, 2007 | June–July 2007 (Bear Stearns shock) | Simultaneous repricing of same shock; equities recovered to new highs post-spread widening | "Spreads widened well before equity peak" |

| 2000–2002 Dot-Com | Mar 10, 2000 (Nasdaq) | Early 2000 at ~4% — widening to 10% by Sep 2000 | Spreads lagged; Nasdaq already -30% by Sep 2000 | "Spreads expanded before Nasdaq peak" |

| 2020 COVID | Feb 19, 2020 | Late Feb 2020 — same week as equity decline | Concurrent; both triggered by same pandemic shock within 48 hours | "Spreads jumped in January, anticipating the drop" |

| 2015–16 Energy | May 2015 (S&P local peak) | Mid-2014 (energy-sector specific) | Sector-specific, not systemic; S&P made new highs 6 months after spread peak | Ignored entirely by opponent |

| Week Ending | Corporate FTD ($M) | Corporate FTR ($M) | S&P 500 Level (approx.) | Interpretation |

|---|---|---|---|---|

| Jan 3, 2007 | $28,783 | $25,443 | ~1,416 | Baseline — calm credit markets |

| Mar 21, 2007 | $53,099 | $48,085 | ~1,410 | First subprime tremors — equities flat |

| Jun 27, 2007 | $61,553 | $58,139 | ~1,503 | Pre-Bear Stearns — equities near highs |

| Jul 4, 2007 | $98,608 | $97,142 | ~1,530 | Bear Stearns collapse — simultaneous shock |

| Aug 29, 2007 | $100,965 | $94,529 | ~1,457 | Peak stress — equities already recovering |

| Oct 10, 2007 | $43,524 | $38,798 | ~1,565 | S&P 500 all-time high — stress had subsided |

| Analytical Axis | FALSE Side's Strongest Point | TRUE Side's Best Counter | Verdict |

|---|---|---|---|

| 2007–2008 Chronology | Equities made new ATH in Oct 2007 after July spread spike; simultaneous Bear Stearns shock | Spreads were elevated June–Oct, constituting a "warning window" | FALSE side stronger: a signal that coexists with new equity highs is not a leading indicator |

| 2020 COVID Timing | HY spreads at 3.7% on Feb 19 peak; widening began Feb 24, same week as equity decline | Spreads moved from 3.7% to 4.5% by Feb 24, "leading" the bulk of the 34% drawdown | Draw: 5-day lead in a 33-day crash is statistically and practically trivial |

| 2000–2002 Dot-Com | Spreads at 4% at March 2000 equity peak; widened to 10% after 30% Nasdaq decline | Spreads began rising in early 2000 before the full decline completed | FALSE side stronger: widening during a decline is not anticipation of it |

| False Alarm Rate | 5+ major false alarms 2010–2020 with no recession; signal unusable in practice | Each false alarm was followed by eventual recovery, not disproving the signal | FALSE side stronger: a signal with >60% false positive rate has negative practical value |

| Structural Change | HY ETF arbitrage synchronizes credit/equity pricing in real time post-2010 | Pre-2010 episodes still show leading behavior | Draw: structural argument is compelling but hard to precisely date the regime shift |

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.