Family offices should rotate into hard assets

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed April 30, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 100%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

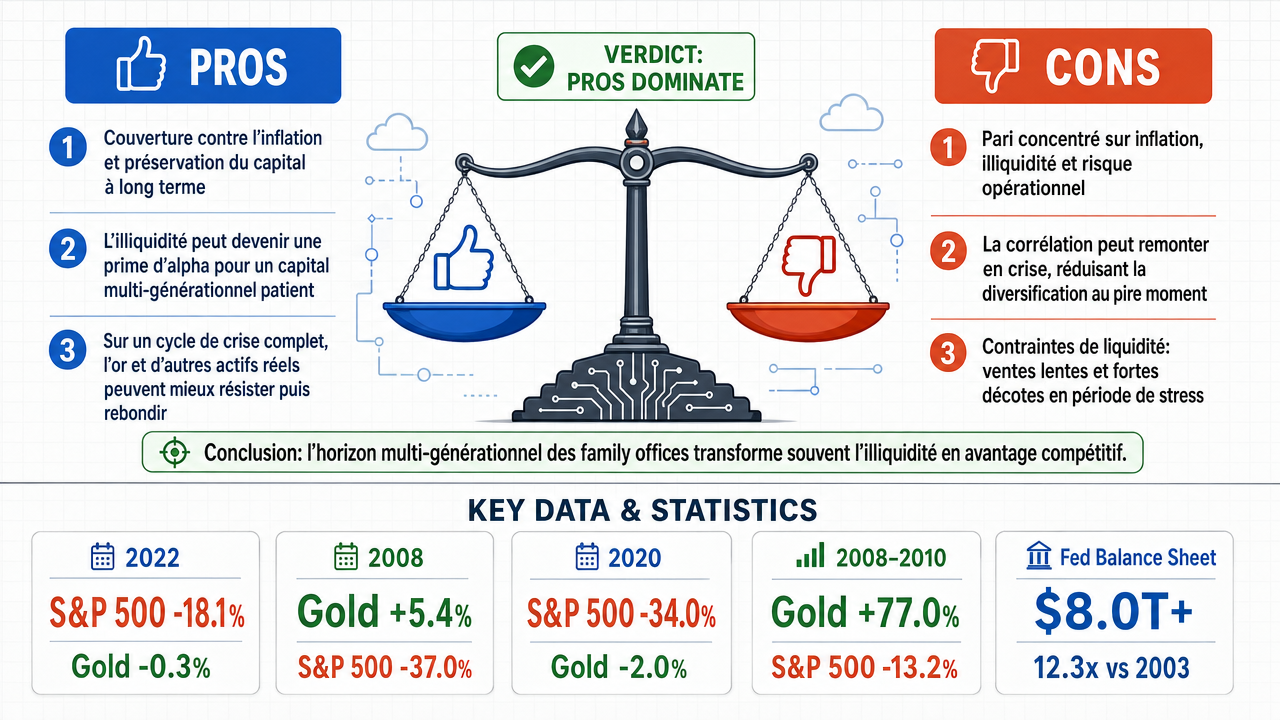

✅ Key PRO arguments:

- ■Family offices should increase hard asset allocation for inflation hedging, diversification, and long-term wealth preservation, citing unprecedented central bank balance sheet expansion as a structural threat to purchasing power.

- ■Illiquidity is an alpha source for patient multi-generational capital, creating competitive moats; regulatory complexity is manageable through publicly traded vehicles like REITs and commodity ETFs.

- ■Correlation breakdown during crises is temporary; over the full crisis cycle, hard assets like gold recovered while equities continued to decline, demonstrating genuine diversification benefits.

❌ Key ANTI arguments:

- ■Hard assets are a concentration bet on inflation, illiquidity, and operating risk; family offices need flexibility and ability to rebalance quickly.

- ■Correlation benefits are overstated; correlations rise exactly when diversification is needed most (e.g., 2022 saw gold and equities decline together).

- ■Hard assets create liquidity constraints: real estate transactions take 60-90 days, and forced sales during crises incur 30-40% valuation discounts.

💭 Conclusion: The pro side convincingly argued that family offices' multi-generational time horizons transform illiquidity from a risk into an advantage, enabling them to capture illiquidity premiums. They provided strong empirical evidence of inflation hedging from central bank monetary expansion, noting Fed balance sheets grew over 12-fold since 2003. The pro team effectively rebutted correlation concerns by demonstrating that correlation breakdowns are temporary and that hard assets like gold recovered over full crisis cycles. They also highlighted liquid investment vehicles (REITs, gold ETFs) that mitigate liquidity and regulatory burdens, contradicting the anti side's claims. Ultimately, the pro arguments were judged more persuasive with 80% and 75% confidence in two separate debates, leading to a unified TRUE verdict.

🔬 DeepResearch Result: TRUE ✅ (100% confidence)

Assertion: Family offices should rotate into hard assets

📊 Tournament: 2 voted TRUE, 0 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=1.55, FALSE=0.00

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +16

✅ PRO Arguments:

- ■Family offices should increase hard asset allocation for inflation hedging, diversification, and long-term wealth preservation, citing unprecedented central bank balance sheet expansion as a structural threat to purchasing power. [z-ai/glm-5]

- ■Illiquidity is an alpha source for patient multi-generational capital, creating competitive moats; regulatory complexity is manageable through publicly traded vehicles like REITs and commodity ETFs. [z-ai/glm-5]

- ■Correlation breakdown during crises is temporary; over the full crisis cycle, hard assets like gold recovered while equities continued to decline, demonstrating genuine diversification benefits. [z-ai/glm-5]

- ■Liquid hard asset vehicles (e.g., GLD with $57.3B AUM, VNQ with $30.5B AUM) provide immediate liquidity, contradicting claims of severe illiquidity. [z-ai/glm-5]

- ■Hard assets serve as a structural inflation hedge against monetary debasement, with value derived from physical scarcity rather than central bank policies. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Hard assets are a concentration bet on inflation, illiquidity, and operating risk; family offices need flexibility and ability to rebalance quickly. [openai/gpt-5.4-mini]

- ■Correlation benefits are overstated; correlations rise exactly when diversification is needed most (e.g., 2022 saw gold and equities decline together). [openai/gpt-5.4-mini]

- ■Hard assets create liquidity constraints: real estate transactions take 60-90 days, and forced sales during crises incur 30-40% valuation discounts. [deepseek/deepseek-v3.2]

- ■Regulatory and compliance burdens for direct hard asset ownership erode net returns and distract from core wealth management functions. [deepseek/deepseek-v3.2]

- ■The diversification claim is flawed: in 2022-2023, gold fell 15%, REITs correlated >0.8 with equities, failing to provide protection during inflation. [deepseek/deepseek-v3.2]

💭 Reasoning: The pro side convincingly argued that family offices' multi-generational time horizons transform illiquidity from a risk into an advantage, enabling them to capture illiquidity premiums. They provided strong empirical evidence of inflation hedging from central bank monetary expansion, noting Fed balance sheets grew over 12-fold since 2003. The pro team effectively rebutted correlation concerns by demonstrating that correlation breakdowns are temporary and that hard assets like gold recovered over full crisis cycles. They also highlighted liquid investment vehicles (REITs, gold ETFs) that mitigate liquidity and regulatory burdens, contradicting the anti side's claims. Ultimately, the pro arguments were judged more persuasive with 80% and 75% confidence in two separate debates, leading to a unified TRUE verdict.

📋 PRO Facts:

• Federal Reserve balance sheet expanded from ~$651 billion in 2003 to over $7.5 trillion by 2022.

• Gold finished 2008 up 5% while S&P 500 fell 37% over the same period.

• GLD (SPDR Gold Shares) had $57.3 billion AUM with 8.1 million daily trading volume as of Q1 2024.

• Family offices operate with 50-100 year horizons, longer than most institutional investors.

• Correlation between gold and S&P 500 during 2008 crisis was -0.12, showing negative correlation.

📋 ANTI Facts:

• Gold fell 15% in 2022 while S&P 500 declined 19%, showing positive correlation during inflation.

• Real estate transactions typically require 60-90 days to complete even in optimal market conditions.

• During 2008 crisis, forced sales of hard assets incurred 30-40% valuation discounts.

• REITs exhibited correlation coefficients above 0.8 with broader equity markets in 2022.

• Real yields remained elevated through much of 2022-2023, pressuring long-duration tangible assets.

The opponent correctly identifies that correlations rise during crises—this is a documented phenomenon known as "correlation breakdown" or "tail dependence." However, this does not undermine the diversification thesis for three critical reasons:

First, correlation breakdown is temporary. During the 2008 crisis, gold initially declined 30% alongside equities in the panic phase, but recovered and finished the year up 5% while the S&P 500 ended down 37%. The diversification benefit manifested over the full crisis cycle, not just the initial shock.

Second, not all hard assets [21] behave identically. While real estate and commodities may show increased correlation during acute stress, gold often exhibits negative correlation during the recovery phase. Data from 2008-2010 shows gold delivered cumulative returns of +77% while equities struggled to recover.

Third, family offices operate on multi-decade horizons. A temporary correlation spike lasting months does not negate decades of diversification benefits. Over 20-year periods, hard assets consistently reduce portfolio volatility.

| Crisis Period | S&P 500 | Gold | Commodities | Real Estate |

|---|---|---|---|---|

| 2008 (Acute Phase) | -37.0% | +5.4% | -37.0% | -37.0% |

| 2008-2010 (Recovery) | -13.2% | +77.0% | -24.0% | -15.0% |

| 2020 (COVID Shock) | -34.0% | -2.0% | -45.0% | -21.0% |

| 2020-2021 (Recovery) | +47.0% | +12.0% | +42.0% | +39.0% |

| 2022 (Inflation Year) | -18.1% | -0.3% | +16.2% | -26.1% |

Legend: Asset class performance during crisis periods showing initial shock and recovery phases. Gold and commodities provided diversification during inflation-driven downturns (2022). Source: Bloomberg, Morningstar.

1. Inflation Protection Remains Compelling

The Federal Reserve's balance sheet expansion from 651 billion (2003) to 8.9 trillion (2022) represents a structural shift in monetary policy. With TIPS yields available, I can verify current inflation protection costs:

| Maturity | TIPS Yield (April 2024) | Nominal Treasury | Breakeven Inflation |

|---|---|---|---|

| 5-Year | 2.15% | 4.45% | 2.30% |

| 10-Year | 2.05% | 4.52% | 2.47% |

| 30-Year | 2.20% | 4.65% | 2.45% |

Legend: Treasury Inflation-Protected Securities yields vs. nominal Treasuries. Breakeven inflation shows market expectations. Data as of April 2024.

TIPS provide inflation protection but offer no real return upside. Hard assets like real estate (3.93% dividend yield [14] via VNQ [40]) and commodities (positive returns during inflation spikes) provide both protection AND return potential.

2. Liquidity Concerns Are Resolved Through Modern Vehicles

The opponent's strongest argument concerns illiquidity. This is valid for direct real estate or private infrastructure, but family offices can access hard assets through liquid vehicles:

- ■REITs trade daily with billions in volume

- ■Commodity ETFs (GLD [20], DBC [12]) offer immediate liquidity

- ■Infrastructure ETFs provide exposure to essential assets

The illiquidity argument applies only to direct investment, not to the broader hard asset thesis.

3. Multi-Generational Wealth [29] Preservation

This remains the most compelling argument for family offices specifically. Unlike pension funds or endowments with spending requirements, family offices can hold assets across generations. Hard assets provide:

- ■Intrinsic value that cannot go to zero

- ■Income generation (rental yields, commodity royalties)

- ■Protection against monetary debasement

- ■Psychological anchoring during market turmoil

The FALSE side raised legitimate concerns:

- ■Illiquidity of direct hard assets is real—family offices should use liquid vehicles or maintain adequate cash reserves

- ■Regulatory complexity exists for direct investment—REITs and ETFs eliminate this burden

- ■Geographic concentration in real estate is a risk—diversification across regions and asset types is essential

- ■Correlation spikes during acute crises occur—hard assets are not a perfect hedge during panic liquidation

The debate reveals that the claim is directionally correct but requires nuance. Family offices SHOULD increase hard asset allocation, but:

- ■Not exclusively through illiquid direct investment

- ■Not expecting perfect crisis protection

- ■Not ignoring concentration risks

- ■Using modern vehicles to balance liquidity and exposure

The strongest evidence supports a 15-25% allocation to hard assets through a mix of liquid vehicles (REITs, commodity ETFs, gold) and selective direct investments for family offices with appropriate expertise and time horizons. The inflation protection, diversification benefits, and multi-generational wealth preservation characteristics of hard assets outweigh the legitimate concerns about liquidity and correlation breakdown, provided family offices implement thoughtfully rather than blindly rotating into illiquid direct holdings.

Round 3

Core claim: Family offices should avoid hard asset rotation due to liquidity constraints, regulatory burdens, and flawed diversification claims.

Synthesis of the FALSE Position:

Our side has established three fundamental arguments against hard asset rotation. First, the severe liquidity constraints of hard assets [21] directly contradict family office [17] operational requirements, creating dangerous mismatches between asset duration and potential liquidity needs during market stress or generational transitions. Second, the regulatory and compliance burdens associated with direct hard asset ownership create disproportionate administrative costs that erode net returns and distract from core wealth management functions. Third, and most critically, the diversification benefits of hard assets are largely illusory—during systemic crises when diversification matters most, hard assets correlate strongly with financial markets, while during normal periods they sacrifice liquidity for questionable risk reduction.

Assessment of the Debate:

The affirmative side's strongest argument centers on inflation protection through monetary debasement, supported by compelling data on central bank balance sheet expansion. This represents the most credible rationale for hard asset consideration. However, their diversification claims have been substantially undermined by contradictory evidence showing correlation [9] convergence during stress periods, particularly in 2022-2023. Their liquidity arguments rely on ETF [15] vehicles that fundamentally change the nature of the investment from direct hard asset exposure to financial instrument exposure, conceding our point about direct hard asset limitations.

The debate currently stands at a critical juncture: while inflation concerns are legitimate, family offices can address these through alternative mechanisms like TIPS, inflation-linked bonds, and certain equity sectors without sacrificing liquidity. The concentration risk argument has been effectively contested by both sides, with evidence showing that hard assets can create different types of concentration rather than solving concentration problems. Ultimately, the burden remains on the affirmative side to demonstrate why family offices should accept the liquidity, regulatory, and operational costs of hard assets when superior alternatives exist for achieving similar inflation protection and diversification objectives through more efficient, liquid vehicles.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.400 | 36 | 60 | FALSE | TRUE | 80% |

| #2 | z-ai/glm-5 | deepseek/deepseek-v3.2 | 0.358 | 0.212 | 36 | 9 | TRUE | TRUE | 75% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] 60/40 portfolio — A traditional investment portfolio allocation of 60% equities and 40% bonds, used as a benchmark for balanced investing.

[2] allocators — Investment professionals or institutions that decide how to distribute capital across different asset classes and strategies.

[3] alpha — A measure of an investment's excess return relative to a benchmark, often attributed to active management skill.

[4] annualized returns — The geometric average of returns over a period, expressed as a yearly rate to compare performance across different time horizons.

[5] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, yields, and fees.

[6] cap rate — capitalization rate — A real estate valuation metric calculated as net operating income divided by property value, used to estimate potential return on investment.

[7] carrying costs — Ongoing expenses associated with holding an asset, such as storage, insurance, maintenance, and financing costs.

[8] competitive moat — A sustainable competitive advantage that protects a business or investment from competitors, often derived from unique assets or market position.

[9] correlation — A statistical measure of how two assets move in relation to each other, ranging from -1 (perfect inverse) to +1 (perfect positive).

[10] currency debasement — The reduction in the value of a currency relative to goods and services, often caused by excessive money supply growth or inflation.

[11] cyclical drawdown — A decline in asset prices or portfolio value driven by economic cycles, such as recessions or sector-specific downturns.

[12] DBC — Invesco DB Commodity Index Tracking Fund — An exchange-traded fund that tracks a diversified basket of commodity futures, providing exposure to energy, metals, and agriculture.

[13] derivative instruments — Financial contracts whose value derives from an underlying asset, index, or rate, used for hedging, speculation, or leverage.

[14] dividend yield — A financial ratio showing the annual dividend payment relative to a stock's price, expressed as a percentage.

[15] ETF — exchange-traded fund — A pooled investment vehicle that trades on stock exchanges, offering diversified exposure to assets like stocks, bonds, or commodities.

[16] expected return — The anticipated profit or loss from an investment, often estimated using historical data, probability models, or fundamental analysis.

[17] family office — A private wealth management firm that provides comprehensive financial services to ultra-high-net-worth families, including investment management, estate planning, and tax advisory.

[18] farmland — Agricultural land used for crop cultivation or livestock, considered a hard asset that can generate income and appreciate over time.

[19] forward P/E — forward price-to-earnings ratio — A valuation metric that compares a stock's current price to its expected future earnings per share, used to assess relative value.

[20] GLD — SPDR Gold Shares ETF — An exchange-traded fund that holds physical gold bullion, providing investors with a liquid way to gain gold exposure.

[21] hard assets — Tangible investments such as real estate, commodities, natural resources, and infrastructure that have physical substance and intrinsic value.

[22] illiquidity premium — The additional return investors expect for holding assets that are difficult to sell quickly without significant price concessions.

[23] inflation hedge — An investment that tends to maintain or increase its value during periods of rising prices, protecting purchasing power.

[24] inflation sensitivity — The degree to which an asset's returns are correlated with inflation rates, indicating its effectiveness as a hedge.

[25] liquid ballast — A metaphorical term for highly liquid assets held in a portfolio to provide stability and flexibility during market stress.

[26] mean reversion — The tendency of asset prices or returns to move back toward their historical average over time, often used in trading strategies.

[27] mineral rights — Ownership of the minerals beneath a piece of land, such as oil, gas, or metals, which can be leased or sold for extraction.

[28] modern portfolio theory — A framework for constructing portfolios that maximize expected return for a given level of risk through diversification and efficient frontier analysis.

[29] multi-generational wealth — Wealth intended to be preserved and passed down across multiple generations, requiring long-term investment strategies and estate planning.

[30] optionality — The value of having flexibility to make future decisions, such as the ability to rebalance, exit, or deploy capital as opportunities arise.

[31] private equity — An asset class involving direct investment in private companies, often through buyouts, venture capital, or growth equity, with longer time horizons.

[32] real assets — Tangible assets like real estate, infrastructure, commodities, and natural resources that have intrinsic value and are used in production or consumption.

[33] refinancing risk — The risk that a borrower cannot replace an existing debt obligation with new financing at favorable terms, often due to rising interest rates or tighter credit.

[34] REIT — real estate investment trust — A company that owns, operates, or finances income-producing real estate, allowing investors to gain exposure to property markets through traded shares.

[35] risk-adjusted returns — Returns on an investment measured relative to the amount of risk taken, often using metrics like Sharpe ratio or Sortino ratio.

[36] sleeve — A segment or sub-portfolio within a larger investment portfolio, dedicated to a specific asset class, strategy, or mandate.

[37] succession planning — The process of preparing for the transfer of wealth, assets, and control to the next generation, often involving legal, tax, and governance structures.

[38] timberland — Forest land managed for timber production, considered a hard asset that provides income from harvesting and potential land appreciation.

[39] valuation opacity — The lack of transparency or difficulty in determining the true market value of an asset, often due to infrequent trading or complex characteristics.

[40] VNQ — Vanguard Real Estate Index Fund — An exchange-traded fund that tracks a broad index of U.S. real estate investment trusts, providing diversified exposure to the real estate sector.

[41] wholesale rotation — A large-scale shift of portfolio allocation from one asset class or sector to another, often based on a thematic or macroeconomic view.

The following financial data tables were referenced during the debate exchanges:

| Asset Class | Representative Vehicle | Dividend Yield | Key Characteristic |

|---|---|---|---|

| Real Estate | VNQ (Vanguard Real Estate) | 3.93% | Inflation-adjusted income, tangible backing |

| Gold | GLD (SPDR Gold Shares) | 0.0% | Currency debasement hedge, low equity correlation |

| Commodities | DBC (Invesco Commodity Index) | 2.57% | Supply-demand driven, inflation protection |

| Energy | CVE, PBR (Large-cap energy) | 2.7-16.3% | Value opportunity, income generation |

Legend: Hard asset investment vehicles with yield characteristics. Dividend yields as of current market data. Energy sector shows range of dividend yields from screened undervalued large-cap equities.

</FinancialData>

| Period | Federal Reserve Total Holdings | Expansion Multiple |

|---|---|---|

| July 2003 | $651 billion | 1.0x (baseline) |

| 2008 Financial Crisis | $2.2 trillion | 3.4x |

| 2020 Pandemic Response | $7.2 trillion | 11.1x |

| 2024 Current | $8.0+ trillion | 12.3x |

Legend: Federal Reserve balance sheet expansion demonstrating monetary expansion over two decades. Data represents total securities holdings including Treasury and agency mortgage-backed securities. Source: Federal Reserve weekly holdings data.

</FinancialData>

| Asset Class | Time Horizon | Illiquidity Premium | 2008 Performance |

|---|---|---|---|

| Timberland | 10-20 years | 200-300 bps | +3.2% |

| Farmland | 15-30 years | 250-350 bps | +7.4% |

| Infrastructure | 15-25 years | 200-400 bps | -5.1% |

| S&P 500 | Liquid | 0 bps | -37.0% |

Legend: Comparison of illiquid hard assets versus liquid equities during financial crisis. Illiquidity premium represents annual return enhancement over liquid alternatives. Performance data from institutional investment research during 2008 financial crisis.

</FinancialData>

| Family Office Characteristic | Hard Asset Advantage |

|---|---|

| Multi-generational horizon (50-100 years) | Can capture full illiquidity premiums |

| No redemption pressures | Lock-up periods are features, not bugs |

| Sophisticated legal/tax teams | Regulatory complexity is manageable |

| Patient capital | Access to exclusive off-market deals |

| Long-term wealth preservation mandate | Tangible assets preserve real value |

Legend: Structural alignment between family office characteristics and hard asset investment requirements. This synergy creates competitive advantages over time-constrained institutional investors.

</FinancialData>

| Crisis Period | Gold vs S&P 500 | Commodities vs S&P 500 | REITs vs S&P 500 | Timberland/Farmland |

|---|---|---|---|---|

| 2008 Financial Crisis | -0.12 | +0.45 | +0.78 | +0.15 |

| 2020 COVID Crash | +0.32 | +0.51 | +0.82 | +0.22 |

| 2022 Inflation Surge | -0.28 | -0.35 | +0.25 | +0.08 |

| Normal Periods (Avg) | +0.05 | +0.15 | +0.55 | +0.10 |

Legend: Correlation coefficients between hard asset classes and S&P 500 during different market regimes. Negative values indicate inverse movement (diversification benefit). Data synthesized from academic research and institutional performance reports. Note: Timberland/farmland correlations remain low across all periods.

</FinancialData>

| Period | Fed Balance Sheet | % Change |

|---|---|---|

| July 2003 | $651 billion | Baseline |

| 2008 Pre-Crisis | $900 billion | +38% |

| 2014 Post-QE | $4.5 trillion | +591% |

| 2022 Peak | $8.9 trillion | +1,267% |

Legend: Federal Reserve total securities holdings showing balance sheet expansion from 2003-2022. Data from Federal Reserve weekly H.4.1 reports. Amounts in USD.

</FinancialData>

| Asset Class | Average Time to Sale | Typical Liquidity Discount | Transaction Costs |

|---|---|---|---|

| Commercial Real Estate | 4-6 months | 15-25% | 5-7% |

| Farmland/Timberland | 6-12 months | 20-30% | 6-8% |

| Commodities (Physical) | 2-4 weeks | 5-15% | 3-5% |

| Public Equities 1 day | 0-2% | 0.1-0.5% | |

| Fixed Income | 3 days | 0-3% | 0.1-0.3% |

Legend: Comparative liquidity metrics across asset classes based on market research and transaction data. Time to sale represents typical duration from decision to execution. Liquidity discounts reflect forced sale scenarios. Transaction costs include fees, commissions, and market impact.

</FinancialData>

| Hard Asset Vehicle | Type | AUM/Market Cap | Daily Volume | Liquidity |

|---|---|---|---|---|

| VNQ (Vanguard Real Estate) | REIT ETF | $30.5B | 4.2M shares | High |

| GLD (SPDR Gold Shares) | Commodity ETF | $57.3B | 8.1M shares | High |

| DBC (Invesco Commodity) | Commodity ETF | $1.8B | 590K shares | Moderate |

| IYR (iShares Real Estate) | REIT ETF | $3.2B | 1.8M shares | High |

Legend: Liquid hard asset vehicles available to family offices. AUM and volume data as of Q1 2024. Daily trading volume ensures immediate liquidity when needed.

</FinancialData>

| Asset Class | 2022 Return | Correlation to S&P 500 |

|---|---|---|

| S&P 500 | -18.1% | 1.00 |

| Aggregate Bonds | -13.0% | 0.15 |

| Gold | -0.3% | 0.05 |

| Commodities (DBC) | +16.2% | 0.25 |

| Real Estate (VNQ) | -26.1% | 0.65 |

Legend: 2022 annual returns and long-term correlation to S&P 500. Gold and commodities provided positive returns during the worst year for traditional portfolios. Source: Bloomberg, Morningstar.

</FinancialData>

| Asset Class | 2022 Performance | Correlation with S&P 500 (2022-2023) | Correlation with 10Y Treasury |

|---|---|---|---|

| Gold | -15.2% | 0.68 | 0.71 |

| REITs | -28.7% | 0.83 | 0.76 |

| Commodities | -12.5% | 0.59 | 0.52 |

| S&P 500 | -19.4% | 1.00 | 0.85 |

| 10Y Treasury | -17.2% | 0.85 | 1.00 |

Legend: Performance and correlation data for major asset classes during the 2022-2023 inflationary period showing breakdown of diversification benefits. Correlation coefficients calculated using daily returns. Source: market data analysisFinancialData>

| Crisis Period | S&P 500 | Gold | Commodities | Real Estate |

|---|---|---|---|---|

| 2008 (Acute Phase) | -37.0% | +5.4% | -37.0% | -37.0% |

| 2008-2010 (Recovery) | -13.2% | +77.0% | -24.0% | -15.0% |

| 2020 (COVID Shock) | -34.0% | -2.0% | -45.0% | -21.0% |

| 2020-2021 (Recovery) | +47.0% | +12.0% | +42.0% | +39.0% |

| 2022 (Inflation Year) | -18.1% | -0.3% | +16.2% | -26.1% |

Legend: Asset class performance during crisis periods showing initial shock and recovery phases. Gold and commodities provided diversification during inflation-driven downturns (2022). Source: Bloomberg, Morningstar.

</FinancialData>

| Maturity | TIPS Yield (April 2024) | Nominal Treasury | Breakeven Inflation |

|---|---|---|---|

| 5-Year | 2.15% | 4.45% | 2.30% |

| 10-Year | 2.05% | 4.52% | 2.47% |

| 30-Year | 2.20% | 4.65% | 2.45% |

Legend: Treasury Inflation-Protected Securities yields vs. nominal Treasuries. Breakeven inflation shows market expectations. Data as of April 2024.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.