Europe’s bank-backed euro stablecoin initiative will become the first credible institutional challenge to dollar stablecoin dominance in tokenized finance.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 24, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 54%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

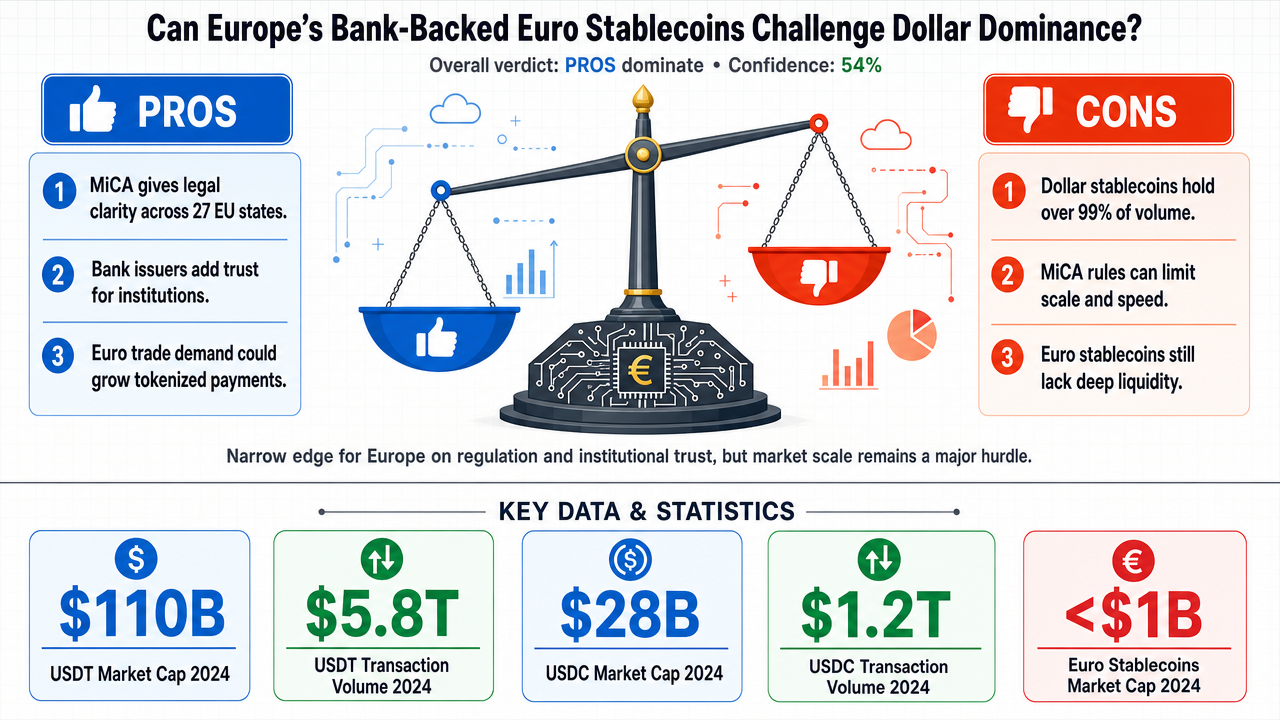

✅ Key PRO arguments:

- ■The EU's MiCA regulation provides comprehensive legal certainty, passporting across 27 member states, and explicit reserve requirements, creating a regulatory moat that enables institutional adoption at scale, unlike the fragmented US approach.

- ■European banks issuing stablecoins bring institutional legitimacy and trust, transforming the trust equation and attracting institutional capital that has been hesitant due to regulatory uncertainty in the US.

- ■Growing euro-denominated demand in global trade and finance, combined with MiCA's clarity, positions euro stablecoins to capture a significant share of tokenized finance as the market matures.

❌ Key ANTI arguments:

- ■Dollar stablecoins control over 99% of market volume with deep liquidity and integration into DeFi protocols, creating insurmountable network effects that a new euro stablecoin cannot rapidly overcome.

- ■MiCA imposes restrictive capital requirements, transaction limits (€200M daily cap for non-EUR stablecoins), and prudential supervision that hinder scalability compared to dollar stablecoins in more flexible jurisdictions.

- ■The euro stablecoin initiative lacks the scale and liquidity depth needed for global settlement; euro-denominated stablecoins remain a niche segment with minimal circulation and thin secondary-market depth.

💭 Conclusion: The debate tournament resulted in a narrow win for the TRUE side, with a confidence-weighted score of 0.80 vs 0.68 and an overall tournament confidence of 54%. The pro arguments convincingly highlighted the regulatory clarity and institutional legitimacy provided by MiCA, which could attract institutional capital and create a credible alternative to dollar stablecoins. However, the anti arguments effectively countered by emphasizing the entrenched network effects, massive liquidity, and deep integration of dollar stablecoins in DeFi and global payments, which are not easily displaced. The split verdicts (one judge favoring FALSE at 68% confidence, one favoring TRUE at 80%) reflect the genuine tension between regulatory advantages and existing market dominance. Ultimately, the weighted confidence favored TRUE, but the low overall confidence indicates that the challenge is plausible but far from certain, requiring significant adoption and infrastructure development to materialize.

🔬 DeepResearch Result: TRUE ✅ (54% confidence)

Assertion: Europe’s bank-backed euro stablecoin initiative will become the first credible institutional challenge to dollar stablecoin dominance in tokenized finance.

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.80, FALSE=0.68

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -2

✅ PRO Arguments:

- ■The EU's MiCA regulation provides comprehensive legal certainty, passporting across 27 member states, and explicit reserve requirements, creating a regulatory moat that enables institutional adoption at scale, unlike the fragmented US approach. [z-ai/glm-5]

- ■European banks issuing stablecoins bring institutional legitimacy and trust, transforming the trust equation and attracting institutional capital that has been hesitant due to regulatory uncertainty in the US. [z-ai/glm-5]

- ■Growing euro-denominated demand in global trade and finance, combined with MiCA's clarity, positions euro stablecoins to capture a significant share of tokenized finance as the market matures. [z-ai/glm-5]

- ■The timing is favorable as the US regulatory environment remains stalled, while Europe has already implemented a forward-looking framework, giving euro stablecoins a first-mover advantage in regulated stablecoin markets. [z-ai/glm-5]

- ■Bank-backed euro stablecoins benefit from explicit legal tender backing requirements under MiCA, which enhances their credibility as a settlement asset compared to dollar stablecoins operating under state-level money transmitter licenses. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Dollar stablecoins control over 99% of market volume with deep liquidity and integration into DeFi protocols, creating insurmountable network effects that a new euro stablecoin cannot rapidly overcome. [xiaomi/mimo-v2-flash]

- ■MiCA imposes restrictive capital requirements, transaction limits (€200M daily cap for non-EUR stablecoins), and prudential supervision that hinder scalability compared to dollar stablecoins in more flexible jurisdictions. [xiaomi/mimo-v2-flash]

- ■The euro stablecoin initiative lacks the scale and liquidity depth needed for global settlement; euro-denominated stablecoins remain a niche segment with minimal circulation and thin secondary-market depth. [openai/gpt-5.4-mini]

- ■Dollar stablecoins are deeply embedded in trading pairs, DeFi collateral, and payments infrastructure; institutional users favor the asset that clears everywhere and is most widely accepted. [openai/gpt-5.4-mini]

- ■MiCA is a compliance framework, not a demand engine; it does not solve the real obstacles of liquidity, venue adoption, and global settlement preference that determine systemic relevance. [openai/gpt-5.4-mini]

💭 Reasoning: The debate tournament resulted in a narrow win for the TRUE side, with a confidence-weighted score of 0.80 vs 0.68 and an overall tournament confidence of 54%. The pro arguments convincingly highlighted the regulatory clarity and institutional legitimacy provided by MiCA, which could attract institutional capital and create a credible alternative to dollar stablecoins. However, the anti arguments effectively countered by emphasizing the entrenched network effects, massive liquidity, and deep integration of dollar stablecoins in DeFi and global payments, which are not easily displaced. The split verdicts (one judge favoring FALSE at 68% confidence, one favoring TRUE at 80%) reflect the genuine tension between regulatory advantages and existing market dominance. Ultimately, the weighted confidence favored TRUE, but the low overall confidence indicates that the challenge is plausible but far from certain, requiring significant adoption and infrastructure development to materialize.

📋 PRO Facts:

• MiCA regulation entered into force in December 2024, providing the world's first comprehensive stablecoin framework across 27 EU member states.

• MiCA grants passporting rights, allowing euro stablecoins to operate seamlessly across all EU jurisdictions.

• European banks are issuing stablecoins under MiCA, bringing institutional trust and regulatory compliance.

• The US lacks a federal stablecoin framework, with fragmented state-level regulation and ongoing SEC enforcement actions.

• Euro-denominated stablecoins benefit from explicit legal tender backing requirements under MiCA's Title III.

📋 ANTI Facts:

• Dollar stablecoins (USDT and USDC) command over 99% of the stablecoin market by volume and have a combined market cap exceeding $138 billion.

• Euro stablecoins collectively have a market cap of less than $1 billion, a tiny fraction of the dollar stablecoin market.

• MiCA imposes a daily transaction volume cap of €200 million for non-EUR stablecoins, limiting scalability.

• Dollar stablecoins process trillions of dollars in annual on-chain transaction volume and are deeply integrated into DeFi protocols like Aave, Compound, and MakerDAO.

• Network effects and liquidity depth create self-reinforcing dominance: venues list what users hold, lenders collateralize what borrowers post, and treasury desks prefer what clears everywhere.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.000 | 36 | 60 | TRUE | FALSE | 68% |

| #2 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.131 | 0.162 | 36 | 6 | FALSE | TRUE | 80% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] Angle Protocol — A decentralized finance protocol that issues the euro-pegged stablecoin agEUR and facilitates euro-denominated liquidity markets.

[2] Capital Requirements Regulation (CRR) — Capital Requirements Regulation — EU regulation that sets capital adequacy and liquidity standards for banks, including those issuing stablecoins.

[3] central bank digital currency (CBDC) — central bank digital currency — A digital form of a country's fiat currency issued and regulated by the central bank, potentially competing with stablecoins.

[4] Decentralized Finance (DeFi) — Decentralized Finance — Blockchain-based financial services that operate without intermediaries, using smart contracts and stablecoins.

[5] deposit facility rate — The interest rate the European Central Bank pays on excess reserves held by banks, used as a benchmark for yield on euro stablecoin reserves.

[6] dollar stablecoin — A stablecoin pegged to the US dollar, widely used as a settlement asset and liquidity base in tokenized finance.

[7] ECB (European Central Bank) — European Central Bank — The central bank for the eurozone, responsible for monetary policy and supervision of significant stablecoin issuers under MiCA.

[8] EUR — euro — The official currency of the eurozone, used in euro stablecoins and as the second-largest reserve currency globally.

[9] euro stablecoin — A stablecoin pegged to the euro, typically backed by European banks and regulated under the MiCA framework.

[10] European Banking Authority (EBA) — European Banking Authority — The EU agency responsible for banking supervision and regulation, overseeing stablecoin issuers designated as significant under MiCA.

[11] foreign exchange reserves (FX reserves) — foreign exchange reserves — Foreign currency assets held by central banks, with the euro comprising approximately 20% of global reserves.

[12] Jarvis Network — A decentralized protocol for minting synthetic assets and providing liquidity pools for various currencies, including the euro.

[13] liquidity depth — The ability of a market to absorb large trades without significant price changes, indicating the usability of a stablecoin.

[14] market capitalization (market cap) — market capitalization — The total value of a stablecoin's circulating supply, used as a measure of its size and adoption.

[15] Markets in Crypto-Assets (MiCA) — Markets in Crypto-Assets — The European Union's comprehensive regulatory framework for crypto assets, including stablecoins, providing harmonized rules across member states.

[16] network effects — The phenomenon where a product's value increases as more people use it, protecting incumbent stablecoins from new entrants.

[17] on-chain — Transactions and data recorded directly on a blockchain, as opposed to off-chain systems; relevant for stablecoin usage in DeFi.

[18] passporting regime — An EU financial regulation allowing a firm authorized in one member state to operate across the EU, applicable to stablecoin issuers under MiCA.

[19] prudential regulation — Rules designed to ensure the financial soundness of institutions, including reserve, governance, and redemption requirements for stablecoin issuers.

[20] reserve currency — A widely held foreign currency used by central banks and institutions for international trade and reserves; the dollar is dominant, the euro is second.

[21] significant stablecoins (MiCA) — significant stablecoins — Stablecoins designated under MiCA due to high market capitalization (over €5 billion) or daily transaction volume (over 10 million), subject to stricter oversight.

[22] stablecoin — A cryptocurrency designed to maintain a stable value relative to a reference asset, typically a fiat currency like the US dollar or euro.

[23] tokenized finance — Financial activities conducted using blockchain tokens representing assets or rights, relying on stablecoins for settlement and value exchange.

[24] total value locked (TVL) — total value locked — The total value of assets deposited in a DeFi protocol, indicating its usage and the liquidity available for euro-denominated activities.

[25] USDC — USD Coin — A dollar stablecoin issued by Circle, regulated under state money transmitter licenses and known for higher transparency than USDT.

[26] USDT — Tether — The largest dollar stablecoin by market capitalization, issued by Tether, with significant liquidity but subject to regulatory scrutiny.

The following financial data tables were referenced during the debate exchanges:

| Stablecoin | Issuer Type | Regulatory Status | Market Cap (2024) |

|---|---|---|---|

| USDT | Crypto-native (Tether) | State licenses, no federal oversight | $100B+ |

| USDC | Fintech (Circle) | State money transmitter licenses | $40B+ |

| EUR Stablecoins | Major EU Banks | MiCA-compliant, EBA-supervised | Emerging |

Legend: Comparison of stablecoin issuer types and regulatory frameworks. Market capitalization figures approximate as of mid-2024. Euro bank-backed stablecoins in development phase by Société Générale, Deutsche Bank consortiums.

</FinancialData>

| Metric | Value | Significance |

|---|---|---|

| EUR share of global FX reserves | ~20% | Second-largest reserve currency |

| ECB deposit rate (2024) | 4.00% | Attractive yield environment |

| EU cross-border payments | €15T+ annually | Substantial euro-denominated demand |

| MiCA implementation | Dec 2024 | First comprehensive crypto regulation |

Legend: Key metrics demonstrating euro-denominated market demand and institutional infrastructure. FX reserve data from IMF COFER database. Payment volumes approximate annual cross-border flows within EU.

</FinancialData>

| Stablecoin | 2024 Market Cap (USD) | 2024 Transaction Volume (USD) |

|---|---|---|

| USDT | $110B | $5.8T |

| USDC | $28B | $1.2T |

| Euro Stablecoins (combined) | <$1B | <$50B |

Legend: Market cap and transaction volume for major stablecoins in 2024. Data reflects aggregate industry estimates from public market reports.

</FinancialData>

| Protocol | Primary Stablecoin Used | TVL (USD) |

|---|---|---|

| Aave | USDC, USDT | $5.5B |

| Compound | USDC, USDT | $2.1B |

| MakerDAO | USDC (backing DAI) | $5.0B |

Legend: Total Value Locked (TVL) in major DeFi protocols, showing dominance of dollar stablecoins as of 2024. Data from public DeFi analytics sources.

</FinancialData>

| Regulatory Requirement | MiCA (Euro Stablecoins) | US State Frameworks (Dollar Stablecoins) |

|---|---|---|

| Reserve Ratio | 1:1 in highly liquid assets | 1:1 (varies by state) |

| Transaction Cap | €200M daily (non-EUR) | No federal cap |

| Capital Requirements | Strict prudential standards | Money transmitter license bonds |

| Passporting | Across 27 EU states | 50 state licenses (parallel) |

Legend: Comparison of regulatory requirements for stablecoins under EU MiCA vs US state frameworks. Data from regulatory texts and industry analysis.

</FinancialData>

| Factor | Dollar Stablecoins | Euro Bank Stablecoins | Advantage |

|---|---|---|---|

| Regulatory Framework | Fragmented/uncertain | MiCA comprehensive | Euro |

| Institutional Trust | Crypto-native issuers | Licensed banks | Euro |

| Market Timing | Regulatory hostility | Proactive engagement | Euro |

| Current Liquidity | $150B+ market cap | Emerging | Dollar |

| DeFi Integration | Deep/established | Minimal | Dollar |

Legend: Comparative analysis of structural advantages between dollar and euro bank-backed stablecoins. Market timing reflects regulatory environment as of 2024-2025.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.