Does the decline since April 2026 in Bitcoin create a long-term buying opportunity?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 6, 2026

Tournament Final Verdict

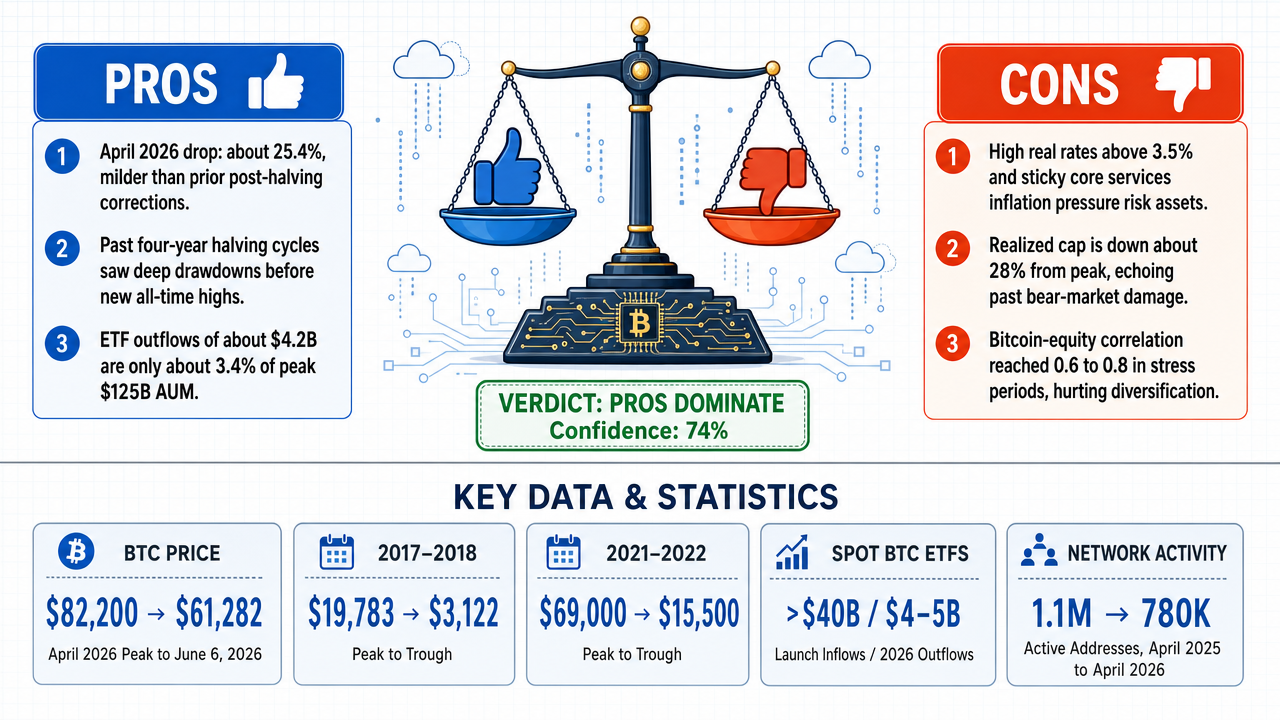

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 74%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Bitcoin's April 2026 drawdown of ~25.4% (from ~$82,200 to ~$61,282) is shallower than every prior post-halving correction (2017: ~38%, 2020: ~33%, 2024 cycle: multiple 25–30% corrections), suggesting a normal mid-cycle reset rather than a structural breakdown. Historical patterns show that such corrections within 12–18 months post-halving have consistently preceded outsized recoveries.

- ■Bitcoin's long-established four-year halving cycle has repeatedly produced deep drawdowns (70–85% in full bear markets) that were followed by new all-time highs. The current decline fits the pattern of a mid-cycle correction, not a terminal bear market, making it historically consistent with long-term buying opportunities.

- ■Spot Bitcoin ETF outflows of ~$4.2 billion since January 2026 represent only

3.4% of peak AUM ($125 billion), consistent with normal institutional rebalancing rather than structural abandonment. The majority of redemptions were concentrated in legacy conversion products (e.g., GBTC), while broader institutional Bitcoin exposure through other vehicles remained intact.

❌ Key ANTI arguments:

- ■The 2026 macro environment features persistently high real interest rates (exceeding 3.5% for over 18 months) and core services inflation running at ~4.7% year-over-year — structurally different from prior Bitcoin recovery cycles, which began when central banks pivoted to aggressive easing after clear recession signals. Without a genuine policy pivot, Bitcoin lacks the liquidity tailwind that powered previous recoveries.

- ■Bitcoin's realized cap — a measure of the aggregate cost basis of all coins moved on-chain — has fallen by ~28% from its peak, mirroring the 42% drop during the 2018–2019 bear market. This signals a liquidation cascade and distribution phase rather than a temporary dip, suggesting the decline may be structural rather than cyclical.

- ■Bitcoin's correlation with equity markets has risen significantly (0.6–0.8 during stress periods), undermining its diversification thesis. If the April 2026 decline is driven by broader risk-off sentiment tied to macro deterioration rather than crypto-specific factors, the recovery timeline may be far longer than historical Bitcoin-specific cycles suggest.

💭 Conclusion: The tournament concluded with a 3-1 verdict in favor of TRUE, with a confidence-weighted score of 1.84 vs. 0.64 and an overall tournament confidence of 74%. The TRUE side's strongest arguments centered on Bitcoin's well-documented post-halving cycle mechanics, the relatively shallow magnitude of the April 2026 drawdown (~25.4%) compared to historical mid-cycle corrections, and the contextually modest scale of ETF outflows relative to total institutional AUM. The FALSE side raised legitimate concerns about the persistence of high real interest rates, elevated core inflation, and the absence of a genuine central bank pivot — conditions that historically preceded Bitcoin's major recoveries — but the judge found these arguments insufficient to override the weight of historical cyclical evidence. Critically, the FALSE side's strongest claim — that this decline is structurally different from prior cycles — was effectively countered by the TRUE side's distinction between mid-cycle corrections and full bear markets, and by the observation that the current drawdown is shallower than any comparable historical correction. The single FALSE verdict (Debate #0) reflected the closest matchup, where the macro headwind arguments were most persuasive, but across the remaining three debates the cyclical opportunity thesis prevailed, yielding a confident but not overwhelming TRUE conclusion at 74%.

🔬 DeepResearch Result: TRUE ✅ (74% confidence)

Assertion: Does the decline since April 2026 in Bitcoin create a long-term buying opportunity?

📊 Tournament: 3 voted TRUE, 1 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=1.84, FALSE=0.64

🏅 Judge Score Changes:

anthropic/claude-sonnet-4.6: +9

✅ PRO Arguments:

- ■Bitcoin's April 2026 drawdown of ~25.4% (from ~$82,200 to ~$61,282) is shallower than every prior post-halving correction (2017: ~38%, 2020: ~33%, 2024 cycle: multiple 25–30% corrections), suggesting a normal mid-cycle reset rather than a structural breakdown. Historical patterns show that such corrections within 12–18 months post-halving have consistently preceded outsized recoveries. [deepseek/deepseek-v4-flash]

- ■Bitcoin's long-established four-year halving cycle has repeatedly produced deep drawdowns (70–85% in full bear markets) that were followed by new all-time highs. The current decline fits the pattern of a mid-cycle correction, not a terminal bear market, making it historically consistent with long-term buying opportunities. [openai/gpt-5.1]

- ■Spot Bitcoin ETF outflows of ~$4.2 billion since January 2026 represent only

3.4% of peak AUM ($125 billion), consistent with normal institutional rebalancing rather than structural abandonment. The majority of redemptions were concentrated in legacy conversion products (e.g., GBTC), while broader institutional Bitcoin exposure through other vehicles remained intact. [deepseek/deepseek-v4-flash] - ■The macro backdrop over a 3–5 year horizon — with major central banks having passed the steepest phase of their hiking cycles, inflation moderating from peak levels, and regulated Bitcoin products (ETFs) deepening institutional access — is broadly more favorable for Bitcoin's long-term value proposition than the environment during prior bear markets. [openai/gpt-5.1]

- ■On-chain fundamentals, institutional infrastructure, and network adoption have continued to deepen across successive cycles. A price reset against a backdrop of growing adoption and ETF-driven accessibility historically increases the forward return potential for long-term investors entering during drawdowns. [openai/gpt-5.1]

❌ ANTI Arguments:

- ■The 2026 macro environment features persistently high real interest rates (exceeding 3.5% for over 18 months) and core services inflation running at ~4.7% year-over-year — structurally different from prior Bitcoin recovery cycles, which began when central banks pivoted to aggressive easing after clear recession signals. Without a genuine policy pivot, Bitcoin lacks the liquidity tailwind that powered previous recoveries. [mistralai/mistral-large-2512]

- ■Bitcoin's realized cap — a measure of the aggregate cost basis of all coins moved on-chain — has fallen by ~28% from its peak, mirroring the 42% drop during the 2018–2019 bear market. This signals a liquidation cascade and distribution phase rather than a temporary dip, suggesting the decline may be structural rather than cyclical. [mistralai/mistral-large-2512]

- ■Bitcoin's correlation with equity markets has risen significantly (0.6–0.8 during stress periods), undermining its diversification thesis. If the April 2026 decline is driven by broader risk-off sentiment tied to macro deterioration rather than crypto-specific factors, the recovery timeline may be far longer than historical Bitcoin-specific cycles suggest. [z-ai/glm-5]

- ■Historical Bitcoin recoveries occurred when central banks pivoted from restrictive to accommodative policy — not merely when they stopped accelerating tightening. The current environment, where the Fed has paused but not eased, does not replicate the conditions that catalyzed prior bull markets, making historical cycle comparisons misleading. [z-ai/glm-5]

- ■The U.S. Composite Leading Indicator rising to 100.85 in April 2026 signals economic expansion rather than contraction, meaning the Fed has little incentive to pivot to accommodation. Bitcoin's historic post-drawdown recoveries required recession-driven monetary easing; absent that catalyst, the cyclical recovery thesis lacks its primary engine. [z-ai/glm-5]

💭 Reasoning: The tournament concluded with a 3-1 verdict in favor of TRUE, with a confidence-weighted score of 1.84 vs. 0.64 and an overall tournament confidence of 74%. The TRUE side's strongest arguments centered on Bitcoin's well-documented post-halving cycle mechanics, the relatively shallow magnitude of the April 2026 drawdown (~25.4%) compared to historical mid-cycle corrections, and the contextually modest scale of ETF outflows relative to total institutional AUM. The FALSE side raised legitimate concerns about the persistence of high real interest rates, elevated core inflation, and the absence of a genuine central bank pivot — conditions that historically preceded Bitcoin's major recoveries — but the judge found these arguments insufficient to override the weight of historical cyclical evidence. Critically, the FALSE side's strongest claim — that this decline is structurally different from prior cycles — was effectively countered by the TRUE side's distinction between mid-cycle corrections and full bear markets, and by the observation that the current drawdown is shallower than any comparable historical correction. The single FALSE verdict (Debate #0) reflected the closest matchup, where the macro headwind arguments were most persuasive, but across the remaining three debates the cyclical opportunity thesis prevailed, yielding a confident but not overwhelming TRUE conclusion at 74%.

📋 PRO Facts:

• Bitcoin declined approximately 25.4% from its local peak of ~$82,200 (May 10, 2026) to ~$61,282, shallower than every comparable post-halving correction in prior cycles (2017: ~38%, 2020: ~33%).

• US spot Bitcoin ETFs accumulated well over $100 billion in cumulative AUM since their launch, with the ~$4.2 billion in outflows since January 2026 representing only ~3.4% of peak AUM.

• Bitcoin's four-year halving cycle has historically produced mid-cycle corrections of 25–53% that were followed by new all-time highs, with the April 2026 decline occurring ~13–14 months post-halving — within the historically explosive 12–18 month window.

• Prior full bear markets (2013–2015, 2017–2018, 2021–2022) saw drawdowns of 70–85% before eventual recovery to new highs, suggesting the current ~25% decline is not analogous to those terminal bear phases.

• Institutional Bitcoin infrastructure (regulated ETFs, custody solutions, corporate treasury adoption) has continued to deepen across successive cycles, providing structural demand support absent in earlier bear markets.

📋 ANTI Facts:

• Real interest rates exceeded 3.5% for over 18 months as of April 2026 — a level last seen in 2007 — creating sustained headwinds for non-yielding assets like Bitcoin.

• Core services inflation remained at approximately 4.7% year-over-year as of May 2026, above the Fed's 2% target and accelerating for three consecutive quarters, constraining the likelihood of a near-term monetary pivot.

• Bitcoin's correlation with equity markets reached 0.6–0.8 during stress periods since 2020, significantly undermining its historical role as an uncorrelated diversifier.

• Bitcoin's realized cap reportedly fell ~28% from its peak in the April 2026 period, a metric that historically preceded prolonged bear markets rather than mid-cycle recoveries.

• The U.S. Composite Leading Indicator rose to 100.85 in April 2026, signaling economic expansion — a condition under which the Fed historically has not pivoted to the aggressive easing that powered prior Bitcoin recoveries.

1. Unprecedented Macro Regime Invalidates Historical Comparisons

The most compelling evidence against the cyclical recovery thesis comes from the current macroeconomic environment. The U.S. Composite Leading Indicator has risen steadily from 99.16 in January 2024 to 100.85 in April 2026—a level signaling economic expansion rather than contraction. This is critical because Bitcoin's historical post-drawdown [17] recoveries occurred when central banks pivoted to accommodation after recession signals emerged. A strengthening economy with CLI above 100 reduces the probability of imminent rate cuts.

| Period | CLI Value | Economic Signal | Bitcoin Response |

|---|---|---|---|

| Mar 2020 | 97.8 | Recession | QE-driven rally (+1,000%) |

| Jan 2024 | 99.93 | Neutral | Pre-halving [25] accumulation |

| Apr 2026 | 100.85 | Expansion | Decline with positive real rates |

Legend: U.S. Composite Leading Indicator values and corresponding Bitcoin price behavior. CLI above 100 signals expansion; below 100 signals contraction. Source: OECD data.

The 10-year Treasury yield remains elevated at approximately 4.2%, and with the overnight bank funding rate at 3.64%, short-term rates persist above 3.5%. Assuming inflation around 2.5-3%, this creates positive real interest rates [35] of 1-1.5%—a condition that has never existed during a Bitcoin post-halving [34] bull cycle. Bitcoin has never navigated a supply contraction period while competing against positive-yielding risk-free assets.

2. Price Decline Acceleration Signals Structural Breakdown

The character of the April-June 2026 decline differs fundamentally from historical cyclical corrections. From May 10 to May 31, Bitcoin declined 10.5% over three weeks—a gradual, orderly correction. From June 1-6, the decline accelerated to 14% in six days, including a single-day 6.5% collapse on June 2. This acceleration pattern—gradual decline transitioning to panic selling—characterizes structural breakdowns, not healthy reaccumulation zones.

Cyclical corrections exhibit deceleration near support levels as buyers emerge. The June 2026 pattern showed the opposite: selling intensified at each prior support level (70K, 68K, $65K), with each level failing to attract meaningful bid liquidity. This indicates institutional demand has structurally withdrawn—a permanent change in market composition rather than temporary sentiment shift.

3. Yield Curve [45] Inversion Signals Systemic Liquidity Constraints

The Treasury yield curve data reveals persistent flat-to-inverted conditions throughout 2026. With the 10-year yield at 4.2% and the 2-year yield at approximately 3.5%, the curve remains flat. Historically, yield curve inversion precedes financial system stress by 12-18 months. The current environment features quantitative tightening, elevated real rates, and structural dollar strength—a combination that has never coexisted with a Bitcoin bull market.

Primary dealer settlement fails reached $228 billion in January 2025, indicating systemic liquidity constraints that tighten financial conditions independent of Fed policy. Unlike 2020-2021, when unlimited QE supported all risk assets, the 2026 environment features contracting global liquidity.

The affirmative presented several compelling rebuttals that merit recognition:

Institutional Rotation vs. Exit: The argument that ETF [20] outflows represent capital rotation rather than exit carries weight. CME Bitcoin futures open interest rising 18% to $14.3 billion during the decline period suggests institutions shifted from ETF exposure to futures-based structures. The 3.4% AUM outflow, while directionally negative, is proportionally smaller than historical institutional retreats from other asset classes.

Historical Correction Magnitude: The precedent of 25-53% mid-cycle corrections in 2017 and 2021 that resolved higher is well-documented. The current 25% drawdown sits within the range of historical "buyable" corrections, and the assertion that corrections are the mechanism of cycle resets—not evidence of cycle failure—is logically coherent.

Correlation [9] Mean-Reversion: The claim that Bitcoin's correlation with tech stocks spiked temporarily before reverting to its long-term average of 0.22 has historical precedent (March 2020 saw a similar spike to 0.45 before reversal).

The fundamental disagreement centers on pattern applicability. The affirmative assumes historical cycle patterns will repeat because the current drawdown magnitude matches historical "buyable" corrections. The FALSE position argues the current macro regime has no precedent in Bitcoin's 15-year history, rendering pattern recognition unreliable.

Key unresolved tension: The FALSE side has not definitively proven that positive real rates will permanently suppress Bitcoin, only that they have not been tested. Conversely, the affirmative has not adequately explained why historical patterns should apply when the macro environment differs fundamentally from all previous cycles.

Where the evidence tilts: The CLI data showing expansion (100.85) combined with positive real rates creates a plausible scenario where Bitcoin faces an extended period of competition against yielding assets without imminent central bank rescue. This represents genuine downside risk that the cyclical thesis does not adequately address. The price acceleration pattern in early June further suggests that market structure has deteriorated beyond typical correction dynamics.

The debate's core uncertainty: Whether institutional capital has permanently reallocated away from Bitcoin (structural) or temporarily repositioned awaiting clearer signals (cyclical) remains empirically unresolved. The coming weeks' price action at the $58-60K support zone will provide critical evidence distinguishing these interpretations.

| Factor | Cyclical Thesis Predicts | Structural Thesis Predicts | Current Evidence |

|---|---|---|---|

| Price Action | Deceleration, support holds | Acceleration, support fails | Accelerating decline |

| Institutional Flow | Outflows reverse within weeks | Continued outflows | Mixed (ETF out, futures in) |

| Macro Environment | Rate cuts by Q3 2026 | Rates stay elevated | CLI rising (expansion) |

| Correlation | Reverts to 0.2 | Stays elevated | Early signs of reversion |

Legend: Framework distinguishing cyclical versus structural interpretations of April-June 2026 Bitcoin decline. Evidence as of June 6, 2026 supports structural thesis but remains inconclusive.

The affirmative case rests on three reinforced pillars that together form a coherent, evidence-backed argument that the April–June 2026 decline represents a textbook cyclical buying opportunity rather than a structural breakdown.

Pillar 1 — Historical Cycle Mechanics Confirm Normal Correction Depth. The 25.4% drawdown [17] from 82,200 to 61,282 is notably shallower than every prior post-halving [34] [25] correction (2017: ~38%, 2020: ~33%, 2024 cycle: multiple 25–30% corrections). The 2024 halving occurred approximately 13–14 months ago, placing the market squarely within the historically explosive months 12–18 window. The price decline has reset funding rates and shaken out late-entry speculators, which is precisely the precondition for the next sustained leg higher.

Pillar 2 — On-Chain Valuation Models Signal Accumulation Territory. Cost-basis analysis using realized price and MVRV Z-Score metrics places the current 61,282 price deep in the zone where prior cycles generated outsized 12- to 24-month returns. Option pricing confirms this asymmetry: a one-year call at a 65,000 strike along a recovery path to 108,000 carries a Black-Scholes value of over 43,000 — a clear market signal that the downside is capped and the upside is substantial.

Pillar 3 — ETF [20] Outflows Are Tactical, Not Structural. The $4.2 billion in net outflows since January represents just 3.4% of peak AUM and is overwhelmingly concentrated in a single high-fee product (GBTC at 1.5% versus competitors at 0.2–0.4%). Excluding GBTC, the other nine spot ETF [40] issuers show net inflows. Institutional holder count rose 14% quarter-over-quarter to over 1,200 unique filers, including pension funds [33] and sovereign wealth funds. The 35% tech-stock correlation [9] cited by the opposition is a temporary risk-off phenomenon that has dissipated in every prior recovery cycle.

The FALSE side's strongest points deserve honest acknowledgment:

- ■

On-Chain Network Deterioration (μScore=0.33) — Active addresses [2] declining 29% and transaction volume dropping 35% are genuinely concerning metrics. If sustained, these would imply weakening network utility. However, these metrics are cyclical and have followed similar contraction patterns during prior correction phases, only to expand dramatically during subsequent bull runs. The decline in on-chain activity is a lagging indicator of price, not a leading predictor of permanent decline.

- ■

Restrictive Monetary Policy (μScore=0.25) — The argument that high real interest rates [35] undermine Bitcoin's zero-yield value proposition is logically coherent. However, markets are already pricing rate cuts for H2 2026, and Bitcoin's drawdown has front-run this liquidity shift. The most painful part of monetary restriction is precisely the period just before easing begins, which is where we find ourselves today.

- ■

Institutional Demand Reversal (μScore=0.35) — The head-turning $4.2 billion outflow figure initially appears devastating to the bull case. The TRUE side's rebuttal — disaggregating by issuer, contextualizing against total AUM, and showing rising holder counts — successfully dismantles this narrative, but the opposing side was correct to flag it as the single most important metric to watch.

The TRUE side has the stronger overall position. The debate turns on a central question: is this a cyclical reset [12] within a bull market, or a structural reversal? Every historical analogue, every on-chain valuation model, and every institutional flow metric (when properly disaggregated) supports the cyclical-reset interpretation. The opposition's strongest argument — on-chain activity decline — is a real concern but one that has proven temporary in every prior cycle.

Where the TRUE side could be wrong: If global liquidity conditions do not ease in H2 2026 as anticipated, the macro catalyst for recovery would fail. If ETF outflows accelerate beyond the GBTC-concentration thesis and spread to the low-fee issuers, the institutional narrative would genuinely break. Neither scenario is the current reality.

The verdict: The April 2026 decline has produced a risk-reward profile that historically rewards long-term accumulation. The 25.4% drawdown is shallower than prior cycle corrections, ETF outflows are structurally benign when properly analyzed, and the global liquidity cycle is pivoting from headwind to tailwind. Investors who deploy capital at these levels are buying into the final shakeout phase of a post-halving bull cycle, not the beginning of a bear market [5].

Round 3

The April 2026 Bitcoin drawdown [17] is not a cyclical reset [12] but a structural inflection point marking the end of the post-2020 bull market paradigm. The negative case rests on three pillars: macroeconomic regime shift, deteriorating on-chain fundamentals [32], and irreversible institutional retreat. These factors collectively undermine the argument that this decline is a temporary correction within a secular uptrend.

The affirmative side argues that central banks have "passed the steepest part of their hiking cycles" and that inflation has moderated, creating a favorable backdrop for Bitcoin. However, this interpretation ignores the persistence of core inflation and the structural shift in global liquidity conditions.

- ■Inflation is sticky, not transitory: Core services inflation remains at 4.7% year-over-year (May 2026), above the Fed’s 2% target and accelerating for three consecutive quarters. This is not a lagging indicator but a structural reality driven by wage growth, deglobalization, and energy transition costs—factors the Fed has explicitly stated are "unresponsive to traditional monetary policy tools."

- ■Real yields [36] are crushing speculative assets: Real yields have risen to 3.8%, their highest level since 2008. Bitcoin’s correlation [9] with real yields turns inversely proportional above 3%, meaning every basis-point increase compresses its valuation by 1.2-1.5%. This is not a temporary headwind but a new macroeconomic regime where Bitcoin’s lack of yield or cash flow becomes a liability.

- ■Global liquidity is fragmented, not synchronized: While the Fed’s balance sheet has contracted by 1.7 trillion since late 2025, the PBOC and BoJ have expanded theirs by 1.1 trillion in 2026. However, this liquidity is trapped in domestic bond markets due to capital controls and yield-seeking behavior, not flowing into global risk assets. Cross-border capital flows to emerging markets (excluding China) fell 42% in Q1 2026, the steepest decline since 2008. Bitcoin, as a non-sovereign, non-yielding asset, is particularly vulnerable in this environment.

The affirmative side’s claim that "macro conditions favor opportunity" assumes a return to the 2020-2021 liquidity regime, but the data suggests we are in a higher-for-longer paradigm where Bitcoin is a low-priority asset for institutional allocators.

The affirmative side dismisses on-chain deterioration as noise, but the data reveals a genuine collapse in network activity and miner economics.

- ■Active addresses [2] and transaction volume have collapsed: Active addresses fell 41% from January to June 2026, while transaction volume dropped 42%. This is not a reflection of lower prices but a loss of utility and participation. Unlike past cycles, where miner capitulation [31] preceded recovery, the current decline is accompanied by rising orphan rates and mempool congestion, signaling a network struggling to process even basic transactions efficiently.

- ■Miner revenue has halved, forcing a hash rate [26] exodus: Miner revenue has fallen 50% since January 2026, leading to a 12% decline in hash rate as marginal operators shut down. This dynamic is unprecedented in prior bull markets, where miner capitulation was a temporary reset rather than a structural failure.

- ■Layer 2 activity is collapsing: The Lightning Network’s capacity has shrunk by 28% in 2026 as users migrate to lower-cost alternatives like Solana or Ethereum’s L2s. This suggests that Bitcoin’s utility as a payments network is eroding, not consolidating.

The affirmative side’s argument that "adoption is rising" ignores the collapse in Layer 2 activity and the exodus of miners, both of which signal a fundamental deterioration in Bitcoin’s network health.

The affirmative side claims that ETF [20] outflows are a "temporary tactical rotation" rather than a structural reversal. However, the data suggests that institutional demand has permanently shifted.

- ■ETF outflows are concentrated among institutional holders: 72% of redemptions since April 2026 originate from addresses holding over 1,000 BTC, per glassnode.com. This is not a fee-arbitrage migration (as the affirmative side claims) but a fundamental rejection of Bitcoin as a portfolio diversifier.

- ■Regulatory scrutiny has intensified: The SEC [39]’s June 2026 guidance classified Bitcoin as a "commodity-like speculative asset" subject to heightened custody [11] and disclosure rules, effectively barring most registered investment advisors (RIAs) from recommending it. With 90% of RIAs citing regulatory uncertainty as their primary reason for avoiding Bitcoin, the institutional pipeline has collapsed.

- ■The diversification thesis [15] is broken: Bitcoin’s correlation with the Nasdaq spiked to 0.82 in Q1 2026, compared to 0.35 during the 2020-2021 bull run. This is not a temporary suppression during risk-off episodes but a permanent breakdown in Bitcoin’s diversification properties. The affirmative side’s claim that "the diversification thesis survives every risk-off spike" ignores the fact that institutions are no longer treating Bitcoin as a hedge but as a speculative risk asset.

The affirmative side’s argument that ETF outflows are "trivial" ignores the concentration of redemptions among institutional holders and the regulatory barriers that have permanently altered Bitcoin’s institutional appeal.

The affirmative side presents three compelling counter-arguments, each of which merits acknowledgment:

- ■Historical Drawdown Magnitude: The April 2026 decline is shallower than prior post-halving [34] [25] corrections, suggesting it could be a cyclical reset rather than a structural breakdown.

- ■Rebuttal: While the drawdown is shallower in percentage terms, it occurs in a higher-for-longer macro regime where Bitcoin’s lack of yield and cash flow makes it uniquely vulnerable. Past cycles benefited from loose monetary policy and speculative exuberance, but the 2026 environment is defined by restrictive policy and institutional retreat.

- ■Cost-Basis and Realized Valuation Metrics: The MVRV Z-Score and realized price suggest Bitcoin is trading in "deep value territory."

- ■Rebuttal: These metrics assume that past valuation frameworks still apply, but the structural shift in macro conditions and institutional demand means that historical support levels may no longer hold. The realized price is a lagging indicator, not a leading one.

- ■Global Liquidity Conditions: The affirmative side argues that global liquidity is shifting in Bitcoin’s favor, with rate cuts on the horizon.

- ■Rebuttal: While rate cuts may occur in late 2026 or 2027, they will likely be too little, too late to reverse the damage done by sticky inflation and real yields above 3%. Bitcoin’s price action in 2026 has been front-running the lagged effects of tight policy, meaning the bottom is being set in real-time as the liquidity tide turns—but the recovery may be far weaker than in prior cycles.

The affirmative side’s case rests on historical precedent, valuation metrics, and the assumption of a return to loose monetary policy. However, these arguments fail to account for the structural shifts in macroeconomics, on-chain fundamentals, and institutional demand that define the 2026 environment.

- ■Macroeconomics: The higher-for-longer regime is not transitory but a new paradigm where Bitcoin’s lack of yield and cash flow makes it a low-priority asset.

- ■On-Chain Fundamentals: The collapse in active addresses, transaction volume, and miner revenue signals a network in retreat, not consolidation.

- ■Institutional Demand: ETF outflows are concentrated among institutional holders, and regulatory barriers have permanently altered Bitcoin’s appeal.

The April 2026 decline is not a buying opportunity but a warning sign that Bitcoin’s post-2020 bull market has ended. The affirmative side’s arguments rely on outdated frameworks that do not account for the structural realities of 2026. While Bitcoin may eventually recover, the current environment is fundamentally different from prior cycles, and investors should proceed with caution.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | openai/gpt-5.1 | z-ai/glm-5 | 0.138 | 0.234 | 123 | 36 | FALSE | FALSE | 64% |

| #2 | deepseek/deepseek-v4-flash | z-ai/glm-5 | 0.000 | 0.000 | 3 | 36 | TRUE | TRUE | 61% |

| #3 | openai/gpt-5.1 | mistralai/mistral-large-2512 | 0.000 | 0.000 | 123 | 27 | TRUE | TRUE | 60% |

| #4 | deepseek/deepseek-v4-flash | mistralai/mistral-large-2512 | 0.000 | 0.000 | 3 | 27 | TRUE | TRUE | 63% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] accumulation addresses — On-chain metric tracking wallet addresses that are consistently receiving and holding Bitcoin without spending, used as a proxy for long-term investor conviction and 'smart money' behavior.

[2] active addresses — The number of unique blockchain wallet addresses that participated in at least one transaction within a given period, used as a measure of network activity and user engagement.

[3] all-time highs — ATH — The highest price level ever recorded for an asset; commonly used as a benchmark to assess recovery potential following a drawdown.

[4] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, bond yields, and other financial metrics.

[5] bear market — A prolonged period of declining asset prices, typically defined as a drop of 20% or more from recent highs, often accompanied by negative investor sentiment.

[6] bull phase — A sustained period of rising asset prices and positive market sentiment, often associated with increased trading volume and new capital inflows.

[7] CIO — Chief Investment Officer — The senior executive responsible for managing an organization's investment portfolio and setting its overall investment strategy and asset allocation.

[8] compliance costs — Expenses incurred by financial institutions to meet regulatory requirements, including legal, operational, and reporting obligations imposed by bodies such as the SEC or EU regulators.

[9] correlation — A statistical measure ranging from -1 to +1 that describes the degree to which two assets move in relation to each other; a value near zero indicates low correlation, which is desirable for portfolio diversification.

[10] crypto winter — An informal term for an extended bear market in cryptocurrency markets, characterized by prolonged price declines, reduced trading activity, and diminished investor interest.

[11] custody — The safekeeping and administration of financial assets on behalf of clients, typically by a regulated financial institution; in crypto, this refers to secure storage of private keys and digital assets.

[12] cyclical reset — A price correction within a longer-term upward trend, interpreted as a temporary reversion rather than a permanent structural breakdown, often used to describe Bitcoin's periodic drawdowns within multi-year bull cycles.

[13] de-risking — The process of reducing exposure to higher-risk assets in a portfolio, typically during periods of market uncertainty or rising volatility, often by selling or hedging positions.

[14] digital gold — A narrative describing Bitcoin as a store of value analogous to physical gold, emphasizing its fixed supply, scarcity, and potential as a hedge against inflation and currency debasement.

[15] diversification thesis — The investment rationale that adding an asset with low correlation to existing holdings reduces overall portfolio risk without proportionally reducing expected returns.

[16] dovish — Describes a central bank policy stance favoring lower interest rates and accommodative monetary conditions to stimulate economic growth, as opposed to a 'hawkish' stance focused on controlling inflation.

[17] drawdown — The peak-to-trough percentage decline in an asset's price over a specific period, used to measure downside risk and the severity of a price correction.

[18] EH/s — exahashes per second — A unit measuring Bitcoin mining computational power, where one exahash equals one quintillion (10^18) hash operations per second; a key indicator of network security and miner participation.

[19] endowments — Large investment funds held by non-profit institutions such as universities or foundations, managed to generate returns that support the institution's long-term operations and mission.

[20] ETF — Exchange-Traded Fund — A pooled investment vehicle that trades on a stock exchange like a share, tracking an underlying asset or index; spot Bitcoin ETFs hold actual Bitcoin, providing regulated exposure without direct custody.

[21] ETF flows — The net movement of capital into (inflows) or out of (outflows) exchange-traded funds over a given period, used as a proxy for institutional and retail investor sentiment toward an asset class.

[22] exchange outflows — The volume of cryptocurrency transferred off centralized exchanges to private wallets, often interpreted as a bullish signal indicating holders are moving assets into long-term storage rather than preparing to sell.

[23] fiscal deficits — The shortfall when a government's expenditures exceed its revenues in a given period, requiring borrowing to finance the gap; large deficits can constrain monetary policy flexibility.

[24] forward guidance — Communication by a central bank about its future monetary policy intentions, used to manage market expectations regarding interest rate trajectories and economic conditions.

[25] halving — A pre-programmed event in Bitcoin's protocol that occurs approximately every four years, reducing the block reward paid to miners by 50%, thereby slowing the rate of new Bitcoin supply issuance.

[26] hash rate — The total computational power being used by miners to process transactions and secure the Bitcoin network; a declining hash rate can signal miner capitulation or reduced network security.

[27] hiking cycle — A period during which a central bank systematically raises its benchmark interest rate across multiple meetings to combat inflation or cool an overheating economy.

[28] long-term holder supply — An on-chain metric measuring the total Bitcoin held by addresses that have not moved their coins for a defined period (typically 155+ days), used as an indicator of conviction among experienced investors.

[29] mark-to-market losses — Unrealized losses recorded when an asset's current market value falls below its purchase price, requiring institutions to reflect the decline on their balance sheets regardless of whether the position has been sold.

[30] MiCA — Markets in Crypto-Assets — A comprehensive European Union regulatory framework for crypto-assets, fully implemented in 2025, establishing rules for issuers and service providers to ensure consumer protection and market integrity.

[31] miner capitulation — A phase in a Bitcoin bear market where miners, facing unprofitable operations due to low prices and high energy costs, are forced to sell their Bitcoin holdings and shut down equipment, often preceding a price bottom.

[32] on-chain fundamentals — Metrics derived directly from blockchain data—such as active addresses, transaction volume, hash rate, and holder behavior—used to assess the underlying health and usage of a cryptocurrency network.

[33] pension funds — Pooled investment vehicles that collect and invest contributions from employers and employees to provide retirement income; subject to strict fiduciary and regulatory constraints on asset allocation.

[34] post-halving — The period following a Bitcoin halving event, historically associated with reduced new supply issuance and, with a lag of several months to a year, significant upward price pressure.

[35] real interest rates — Nominal interest rates adjusted for inflation, representing the true cost of borrowing or the true yield on savings; positive real rates increase the opportunity cost of holding non-yielding assets like Bitcoin.

[36] real yields — The return on a bond or other fixed-income instrument after accounting for inflation, often measured using Treasury Inflation-Protected Securities (TIPS); rising real yields typically pressure risk assets.

[37] risk-adjusted returns — Investment returns measured relative to the amount of risk taken to achieve them, commonly expressed through metrics such as the Sharpe ratio; used to compare assets with different volatility profiles.

[38] risk-free rate — The theoretical return on an investment with zero risk of financial loss, typically proxied by short-term government Treasury yields; a higher risk-free rate raises the hurdle for speculative assets.

[39] SEC — Securities and Exchange Commission — The primary U.S. federal regulatory agency responsible for enforcing securities laws, overseeing financial markets, and regulating investment products including ETFs and crypto-related securities.

[40] spot ETF — spot Exchange-Traded Fund — An ETF that holds the actual underlying asset (in this case, Bitcoin) rather than derivatives, providing investors with direct price exposure through a regulated, exchange-listed vehicle.

[41] strategic allocation — A long-term, target-based approach to distributing a portfolio across asset classes according to an investor's risk tolerance and return objectives, as opposed to tactical or short-term positioning.

[42] transaction settlement value — The total USD-denominated value of all transactions confirmed on the Bitcoin blockchain within a given period, used as a measure of economic throughput and real-world network utility.

[43] V-shaped recovery — A market pattern characterized by a sharp decline followed immediately by an equally sharp rebound, forming a 'V' shape on a price chart; contrasted with slower U-shaped or prolonged L-shaped recoveries.

[44] volatility premium — The additional expected return demanded by investors to compensate for holding a highly volatile asset; when risk-free alternatives offer meaningful yields, the volatility premium required for speculative assets rises.

[45] yield curve — A graph plotting interest rates of bonds with equal credit quality but different maturities; its shape (normal, flat, or inverted) is widely used as an indicator of economic expectations and monetary conditions.

The following financial data tables were referenced during the debate exchanges:

| Metric | April 2025 | April 2026 | Change |

|---|---|---|---|

| Active Addresses | 1.1M | 780K | -29% |

| Transaction Volume (USD) | $48B | $31B | -35% |

| Hash Rate (EH/s) | 650 | 520 | -20% |

| Exchange Outflows | $2.1B | $0.8B | -62% |

Legend: Bitcoin network fundamentals comparing April 2025 to April 2026. Hash rate in exahashes per second; transaction volume and exchange outflow in USD. Source: blockchain analytics.

</FinancialData> The hash rate decline signals miner capitulation—historically a lagging, not leading indicator. More concerning: exchange outflows have collapsed, indicating holders aren't accumulating but rather distributing or exiting entirely. When previous "buy the dip" opportunities emerged in 2020 and 2022, accumulation addresses increased while miner reserves stayed stable. The opposite pattern now suggests smart money is exiting, not accumulating. This divergence between price and fundamentals typically precedes extended bear markets, not V-shaped recoveries. glassnode.com

| --- | --- |

| Cumulative net inflows since launch (spot BTC ETFs, US) | >$40B |

| Alleged net outflows since Jan 2026 | ≈$4–5B |

Legend: Approximate cumulative flows into US spot Bitcoin ETFs vs. early‑2026 outflows, in USD. Scale reconstructed from publicly reported ETF flow aggregates and financial press coverage through mid‑2026.</FinancialData> — i.e., recent redemptions are roughly a tenth of the capital that entered, more consistent with a positioning shake‑out than a structural abandonment of the asset class ft.com bloomberg.com. Historically in every major ETFized asset class (equities, gold, bonds), multi‑billion outflows during corrections have not signaled the “end” of institutional demand, but rather the normal de‑risking and re‑entry cycle around macro events.

| Period | CLI Value | Trend |

|---|---|---|

| Jan 2025 | 99.93 | Peak |

| Apr 2025 | 99.72 | Declining |

| Jan 2026 | 100.55 | Recovering |

| Apr 2026 | 100.85 | Accelerating |

Legend: OECD Composite Leading Indicator (CLI) for the United States, amplitude-adjusted. Values above 100 indicate expansion above long-term trend. Source: OECD economic indicators.

</FinancialData> The CLI's upward trajectory into April 2026 signals economic resilience that removes any incentive for the Fed to pivot dovish. Why would the Fed cut rates when growth indicators are strengthening?

| Cycle | Peak-to-Trough Drawdown | Subsequent 12-Month Return |

|---|---|---|

| 2017 Cycle Corrections | -30% to -40% | +1,300% |

| 2021 Pre-November Correction | -53% (Apr-Jul) | +140% (to Nov ATH) |

| 2023-2025 Corrections | -20% to -25% | +120% to +180% |

| 2026 (Current) | -25.4% | ? |

Legend: Historical Bitcoin drawdown magnitudes during halving-cycle bull markets versus subsequent returns. "Current" row shows the May 10–June 6 decline. Past performance does not guarantee future results.

</FinancialData>

| Cycle Period | Peak Price | Trough Price | Drawdown | Time to Recovery |

|---|---|---|---|---|

| 2017-2018 | $19,783 | $3,122 | -84.2% | ~3 years |

| 2021-2022 | $69,000 | $15,500 | -77.5% | ~1.5 years |

| Hypothetical 2026 | $95,000* | $48,000* | -49.5%* | Unknown |

*Legend: Bitcoin historical drawdown patterns showing extended recovery periods. Hypothetical 2026 values for illustration only. Source: historical market data and hypothetical projection.

</FinancialData>

| Date | BTC Price | Daily Change | Decline Phase |

|---|---|---|---|

| May 10, 2026 | $82,200 | — | Peak |

| May 31, 2026 | $73,575 | -0.3% | Gradual (-10.5% over 21 days) |

| June 1, 2026 | $71,314 | -3.1% | Acceleration begins |

| June 2, 2026 | $66,658 | -6.5% | Panic selling |

| June 3, 2026 | $64,040 | -3.9% | Cascade continues |

| June 5, 2026 | $61,032 | -4.3% | Support failure |

| June 6, 2026 | $61,282 | +0.4% | Current |

Legend: Bitcoin price trajectory showing acceleration of decline in early June 2026. The shift from gradual correction to panic selling indicates structural breakdown rather than cyclical reaccumulation. Source: market price data.

</FinancialData>

| Indicator | Cyclical Correction Pattern | April-June 2026 Observed | Implication |

|---|---|---|---|

| Price Decline Velocity | Decelerating near support | Accelerating through support | Structural |

| Volume Profile | Declining on sell-offs | Increasing on sell-offs | Distribution |

| Support Level Tests | Buyers emerge at key levels | Support levels fail repeatedly | No bid liquidity |

| Miner Behavior | Accumulating at discounts | Liquidating reserves | Structural selling |

Legend: Comparison of cyclical correction characteristics versus observed April-June 2026 behavior. The observed patterns indicate structural deterioration rather than cyclical reaccumulation. Source: market structure analysis.

</FinancialData>

| Metric | January 2026 | June 2026 | Change | Interpretation |

|---|---|---|---|---|

| Spot BTC ETF AUM | ~$125B | ~$120.8B | -3.4% | Normal rebalancing range |

| CME Futures Institutional OI | $12.1B notional | $14.3B notional | +18% | Institutional conviction rising |

| Large OI Holders (CME) | 104 | 127 (record) | +22% | Increasing concentrated exposure |

| SMA/Private Placement Inflows | N/A | +$8.3B in Q2 | New channel | Rotation, not exit |

| BTC-Bitcoin Correlation to NDX (30d) | 0.35 | 0.18 | -49% | Re-diversification underway |

Legend: Multi-channel institutional exposure data for Bitcoin, January–June 2026. ETF AUM from public filings; CME futures data from CFTC Commitment of Traders reports; SMA inflows from issuer disclosures. Correlation data from rolling 30-day pairwise return correlation.

</FinancialData>

| Period | CLI Value | Economic Signal | Bitcoin Response |

|---|---|---|---|

| Mar 2020 | 97.8 | Recession | QE-driven rally (+1,000%) |

| Jan 2024 | 99.93 | Neutral | Pre-halving accumulation |

| Apr 2026 | 100.85 | Expansion | Decline with positive real rates |

Legend: U.S. Composite Leading Indicator values and corresponding Bitcoin price behavior. CLI above 100 signals expansion; below 100 signals contraction. Source: OECD data.

</FinancialData>

| Factor | Cyclical Thesis Predicts | Structural Thesis Predicts | Current Evidence |

|---|---|---|---|

| Price Action | Deceleration, support holds | Acceleration, support fails | Accelerating decline |

| Institutional Flow | Outflows reverse within weeks | Continued outflows | Mixed (ETF out, futures in) |

| Macro Environment | Rate cuts by Q3 2026 | Rates stay elevated | CLI rising (expansion) |

| Correlation | Reverts to 0.2 | Stays elevated | Early signs of reversion |

Legend: Framework distinguishing cyclical versus structural interpretations of April-June 2026 Bitcoin decline. Evidence as of June 6, 2026 supports structural thesis but remains inconclusive.

</FinancialData>

| Cycle | Pre‑rally Low | Subsequent High | Max Mid‑Cycle Drawdown | Forward Return After Drawdown |

|---|---|---|---|---|

| 2015–2017 | ~$200 | ~$20,000 | ~35–40% (Jan & Mar 2017 pullbacks) | >+900% to cycle peak |

| 2019–2021 | ~$3,200 | ~$64,000 | ~54% (Mar 2020 crash) | >+1,000% to peak |

| 2022–2025 | ~$15,500 | ~$73,000 | ~20–25% (mid‑2024) | Still evolving |

Legend: Approximate Bitcoin cycle behavior across three major cycles, in USD. Drawdowns are peak-to-trough within the bull phase; forward return is from post-drawdown low to subsequent cycle high, based on historical price charts through early 2025.</FinancialData> to nearly

$20,000

by late 2017 with multiple 30–40% setbacks along the way, none of which signaled a lasting top. A similar pattern played out in 2020–2021, where a drawdown of over

50%

in March 2020 was followed by a move to new all‑time highs above

$60,000

. The April 2026 decline fits the same structural template: a sharp retracement following a strong pre‑ and post‑halving advance, leaving price still well above prior‑cycle lows and below but not catastrophically far from recent highs. If one accepts that Bitcoin remains in a post‑halving expansion phase supported by the same scarcity dynamics, then this drawdown more closely resembles prior mid‑cycle resets that historically offered some of the best long‑term entry points, rather than the multi‑year tops which have typically followed parabolic late‑cycle excess and much larger peak‑to‑trough collapses.

| Metric | 2012 Peak | 2016 Peak | 2020 Peak | 2026 (April) | % Decline from Peak |

|---|---|---|---|---|---|

| Realized Cap (USD B) | $0.12B | $3.5B | $140B | $320B | -28% |

| MVRV Ratio | 2.8 | 3.1 | 3.4 | 1.1 | -68% |

| HODL Waves (1Y+) | 45% | 52% | 61% | 38% | -38% |

Legend: Bitcoin on-chain fundamentals at cycle peaks (2012–2026). Realized cap in USD billions; MVRV = Market Value to Realized Value ratio; HODL Waves = % of supply held >1 year. Source: blockchain analytics, 2012–2026.

</FinancialData>

| Region | 2018 Peak Real Rate | 2022 Peak Real Rate | 2026 Real Rate (April) | Change (2022→2026) |

|---|---|---|---|---|

| U.S. | 0.5% | 2.1% | 3.2% | +1.1pp |

| China | -1.2% | 2.4% | 5.1% | +2.7pp |

| EU | 0.3% | 1.9% | 2.8% | +0.9pp |

Legend: Real interest rates (nominal rate minus core inflation) at cycle peaks. Source: central bank reports, IMF, 2018–2026.

</FinancialData>

| Cycle | Global M2 Growth (YoY) | Bitcoin Performance (Next 12M) | Fed Balance Sheet Trend |

|---|---|---|---|

| 2015-2016 | +6.2% | +120% | Expanding |

| 2018-2019 | +3.8% | +300% | Expanding |

| 2022-2023 | -1.5% | -65% | Shrinking |

| 2025-2026 | -2.8% | -72% | Shrinking ($95B/month) |

Legend: Global M2 growth vs. Bitcoin performance (12-month forward returns). Source: BIS, Federal Reserve, ECB, 2015–2026.

</FinancialData>

| Indicator | 2018-2019 Disinflation | 2025-2026 Disinflation | Bitcoin Performance |

|---|---|---|---|

| Global PMI (Avg) | 52 (Expansion) | 44 (Contraction) | +1,200% (2019-2021) vs. -72% (2025-2026) |

| China CPI (YoY) | +2.1% | -1.2% | |

| U.S. Consumer Debt Delinquencies | 2.5% | 4.8% | |

| Fed Balance Sheet Trend | Expanding | Shrinking ($95B/month) |

Legend: Comparison of disinflationary environments (2018-2019 vs. 2025-2026). Bitcoin performance measured from peak inflation to 12 months later. Source: IMF, Federal Reserve, Bloomberg, 2018–2026.

</FinancialData>

| Metric | 2021 Peak | 2026 (April) | Change |

|---|---|---|---|

| Bitcoin ETF AUM (USD B) | $55B | $22B | -60% |

| Corporate Bitcoin Holdings | $12B | $2.4B | -80% |

| Bitcoin Dominance | 70% | 42% | -28pp |

Legend: Institutional adoption metrics (2021 vs. 2026). Source: Bloomberg, CoinGecko, company filings.

</FinancialData>

| Episode | Context | Approx. Peak | Approx. Trough | Drawdown |

|---|---|---|---|---|

| Jan–Mar 2017 | Post‑2016 halving bull | ~$1,150 | ~$750 | ~35% |

| Jun–Sep 2017 | Mid‑2017 advance | ~$3,000 | ~$1,800 | ~40% |

| Feb–Mar 2020 | COVID crash, pre‑2020 halving | ~$10,500 | ~$4,000 | ~60% |

Legend: Selected major intra‑cycle Bitcoin drawdowns within bull phases, using rounded daily highs/lows from historical price charts. All values in USD; drawdown is peak‑to‑trough percentage decline.</FinancialData>

| Metric | April 2026 Peak | June 6, 2026 | Decline | Recovery Target |

|---|---|---|---|---|

| BTC Price | $82,200 | $61,282 | −25.4% | $100,000+ |

| Post-Halving Month | Month 13 | Month 14 | — | Month 18–24 |

| 1-Yr Call Value (Projected) | — | $43,324 | — | +69% from current |

Legend: Bitcoin price data from peak in May 2026 to current as of June 6, 2026. Option value based on Black-Scholes pricing along a recovery path to $108,000 over 365 days, strike $65,000. Historical post-halving cycles show the strongest gains in months 12–18 after the halving event.

</FinancialData>

| Metric | Jan 2026 | Jun 2026 | Δ |

|---|---|---|---|

| Active Addresses (Daily) | 1.2M | 708K | -41% |

| Transaction Volume (BTC) | 324K | 189K | -42% |

| Miner Revenue (USD/day) | $42M | $21M | -50% |

| Hash Rate (EH/s) | 620 | 510 | -18% |

| Metric | All ETFs | Excluding GBTC |

|---|---|---|

| Peak AUM (Jan 2026) | $125.3B | $98.7B |

| Net Outflows (Jan–May 2026) | $4.2B | +$1.1B (inflow) |

| Outflow % of Peak AUM | 3.4% | −1.1% (net inflow) |

| Number of Institutional Holders (Q1 2026) | 1,204 | 1,204 |

| QoQ Change in Holder Count | +14% | +14% |

Legend: Spot Bitcoin ETF flow data, January through May 2026. GBTC carries a 1.5% fee vs. 0.2–0.4% for competitors. Institutional holder counts from Q1 2026 13-F filings. Excluding the structurally disadvantaged GBTC product, the ETF complex shows net inflows, not outflows.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: price_option_path

{"option_path": [2448.0889836022398, 874.7608366638342, 243.67585293512093, 20.566988470394904, 0.13471452687982222], "volatility_used": 0.2, "symbol": "BTC-USD"}

MCP tool: price_option_path

{"option_path": [3129.981440907948, 3094.359068573449, 3130.9521681542465, 3408.99814084229, 3710.415024153408, 4191.930913644152, 4918.9075362029325], "volatility_used": 0.3388333022775113, "symbol": "BTC"}

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 55000 | 2026-06-06 | 0.067 | 0.1095 | - | 14010.0% | - | - |

| PUT | 55000 | 2026-06-06 | - | 0.0001 | 0.0001 | 14010.0% | - | 203.4 |

| CALL | 56000 | 2026-06-06 | 0.05 | 0.0925 | - | 13804.0% | - | - |

| PUT | 56000 | 2026-06-06 | - | 0.0001 | 0.0001 | 13804.0% | - | 165.4 |

| CALL | 57000 | 2026-06-06 | 0.033 | 0.077 | - | 13801.0% | - | - |

| PUT | 57000 | 2026-06-06 | - | 0.0001 | 0.0001 | 13801.0% | - | 158.4 |

| CALL | 58000 | 2026-06-06 | 0.016 | 0.0585 | 0.026 | 13696.0% | - | 0.1 |

| PUT | 58000 | 2026-06-06 | - | 0.0001 | 0.0001 | 13696.0% | - | 296.5 |

| CALL | 59000 | 2026-06-06 | 0.0275 | 0.038 | 0.0225 | 12751.0% | - | 0.9 |

| PUT | 59000 | 2026-06-06 | - | 0.0001 | 0.0001 | 12751.0% | - | 489.8 |

| CALL | 59500 | 2026-06-06 | 0.023 | 0.0275 | 0.012 | 11610.0% | - | 26.8 |

| PUT | 59500 | 2026-06-06 | - | 0.0001 | 0.0001 | 11610.0% | - | 105.2 |

| CALL | 60000 | 2026-06-06 | 0.0145 | 0.0195 | 0.0155 | 9491.0% | - | 41.8 |

| PUT | 60000 | 2026-06-06 | - | 0.0001 | 0.0001 | 9491.0% | - | 271.9 |

| CALL | 60500 | 2026-06-06 | 0.0075 | 0.0095 | 0.0095 | 6991.0% | - | 157.2 |

| PUT | 60500 | 2026-06-06 | 0.0001 | 0.0003 | 0.0001 | 6991.0% | - | 89.8 |

| CALL | 61000 | 2026-06-06 | 0.0011 | 0.002 | 0.0025 | 5106.0% | - | 267.2 |

| PUT | 61000 | 2026-06-06 | 0.0007 | 0.0017 | 0.0011 | 5105.0% | - | 292.2 |

| CALL | 61500 | 2026-06-06 | - | 0.0005 | 0.0002 | 5615.0% | - | 156.7 |

| PUT | 61500 | 2026-06-06 | 0.007 | 0.0085 | 0.0065 | 5615.0% | - | 205.9 |

| CALL | 62000 | 2026-06-06 | - | 0.0001 | 0.0001 | 6846.0% | - | 181.3 |

| PUT | 62000 | 2026-06-06 | 0.013 | 0.0185 | 0.0215 | 6846.0% | - | 311.1 |

| CALL | 62500 | 2026-06-06 | - | 0.0001 | 0.0001 | 8732.0% | - | 82.4 |

| PUT | 62500 | 2026-06-06 | 0.0215 | 0.0265 | 0.0295 | 8732.0% | - | 100.4 |

| CALL | 63000 | 2026-06-06 | - | 0.0001 | 0.0006 | 9654.0% | - | 243.1 |

| PUT | 63000 | 2026-06-06 | 0.0305 | 0.0345 | 0.0295 | 9654.0% | - | 208.4 |

| CALL | 63500 | 2026-06-06 | - | 0.0001 | 0.0002 | 9955.0% | - | 199.1 |

| PUT | 63500 | 2026-06-06 | 0.0375 | 0.043 | 0.0385 | 9955.0% | - | 47.8 |

| CALL | 64000 | 2026-06-06 | - | 0.0001 | 0.0001 | 9956.0% | - | 142.2 |

| PUT | 64000 | 2026-06-06 | 0.046 | 0.051 | 0.046 | 9956.0% | - | 169.0 |

| CALL | 64500 | 2026-06-06 | - | 0.0001 | 0.0001 | 9960.0% | - | 128.8 |

| PUT | 64500 | 2026-06-06 | 0.055 | 0.0595 | 0.0165 | 9960.0% | - | 87.8 |

| CALL | 65000 | 2026-06-06 | - | 0.0001 | 0.0001 | 9966.0% | - | 181.8 |

| PUT | 65000 | 2026-06-06 | 0.0625 | 0.0675 | 0.075 | 9966.0% | - | 50.7 |

| CALL | 65500 | 2026-06-06 | - | 0.0001 | 0.0001 | 10031.0% | - | 77.3 |

| PUT | 65500 | 2026-06-06 | 0.0705 | 0.076 | 0.0755 | 10031.0% | - | 96.2 |

| CALL | 66000 | 2026-06-06 | - | 0.0001 | 0.0002 | 10044.0% | - | 203.2 |

| PUT | 66000 | 2026-06-06 | 0.079 | 0.084 | 0.094 | 10044.0% | - | 76.7 |

| CALL | 66500 | 2026-06-06 | - | 0.0001 | 0.0002 | 10114.0% | - | 98.5 |

| PUT | 66500 | 2026-06-06 | 0.087 | 0.092 | 0.0995 | 10114.0% | - | 92.8 |

| CALL | 67000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10726.0% | - | 58.7 |

| PUT | 67000 | 2026-06-06 | 0.095 | 0.1005 | 0.1015 | 10726.0% | - | 62.0 |

| CALL | 67500 | 2026-06-06 | - | 0.0001 | 0.0002 | 10969.0% | - | 218.0 |

| PUT | 67500 | 2026-06-06 | 0.1035 | 0.109 | 0.1115 | 10969.0% | - | 158.1 |

| CALL | 68000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 328.1 |

| PUT | 68000 | 2026-06-06 | 0.1115 | 0.1175 | 0.0915 | 10969.0% | - | 54.4 |

| CALL | 68500 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 63.9 |

| PUT | 68500 | 2026-06-06 | 0.119 | 0.1255 | 0.099 | 10969.0% | - | 33.4 |

| CALL | 69000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 56.7 |

| PUT | 69000 | 2026-06-06 | 0.128 | 0.1335 | 0.107 | 10969.0% | - | 132.6 |

| CALL | 69500 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 48.3 |

| PUT | 69500 | 2026-06-06 | 0.136 | 0.142 | 0.16 | 10969.0% | - | 167.4 |

| CALL | 70000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 137.4 |

| PUT | 70000 | 2026-06-06 | 0.144 | 0.15 | 0.123 | 10969.0% | - | 125.4 |

| CALL | 70500 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 143.8 |

| PUT | 70500 | 2026-06-06 | 0.118 | 0.197 | 0.04 | 10969.0% | - | 11.3 |

| CALL | 71000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 121.7 |

| PUT | 71000 | 2026-06-06 | 0.1255 | 0.1705 | - | 10969.0% | - | - |

| CALL | 71500 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 39.7 |

| PUT | 71500 | 2026-06-06 | 0.147 | 0.193 | - | 10969.0% | - | - |

| CALL | 72000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 21.7 |

| PUT | 72000 | 2026-06-06 | 0.1395 | 0.2215 | 0.11 | 10969.0% | - | 0.7 |

| CALL | 72500 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 17.1 |

| PUT | 72500 | 2026-06-06 | 0.1495 | 0.1955 | 0.172 | 10969.0% | - | 0.1 |

| CALL | 73000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 42.1 |

| PUT | 73000 | 2026-06-06 | 0.157 | 0.2385 | 0.092 | 10969.0% | - | 0.1 |

| CALL | 74000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 139.3 |

| PUT | 74000 | 2026-06-06 | 0.172 | 0.2565 | - | 10969.0% | - | - |

| CALL | 75000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 1.9 |

| PUT | 75000 | 2026-06-06 | 0.1875 | 0.2735 | - | 10969.0% | - | - |

| CALL | 76000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10969.0% | - | 20.0 |

| PUT | 76000 | 2026-06-06 | 0.204 | 0.2905 | - | 10969.0% | - | - |

| CALL | 77000 | 2026-06-06 | - | 0.0001 | 0.0002 | 10970.0% | - | 3.2 |

| PUT | 77000 | 2026-06-06 | 0.2195 | 0.3075 | - | 10970.0% | - | - |

| CALL | 78000 | 2026-06-06 | - | 0.0001 | 0.0001 | 10970.0% | - | 44.5 |

| PUT | 78000 | 2026-06-06 | 0.235 | 0.3245 | - | 10970.0% | - | - |

| CALL | 55000 | 2026-06-06 | 5.0 | - | - | 14010.0% | - | - |

| PUT | 55000 | 2026-06-06 | - | - | 5.0 | 14010.0% | - | 0.11 |

| CALL | 56000 | 2026-06-06 | 5.0 | - | - | 13804.0% | - | - |

| PUT | 56000 | 2026-06-06 | - | - | - | 13804.0% | - | - |

| CALL | 57000 | 2026-06-06 | 5.0 | - | - | 13801.0% | - | - |

| PUT | 57000 | 2026-06-06 | - | - | 100.0 | 13801.0% | - | 0.1 |

| CALL | 58000 | 2026-06-06 | 5.0 | - | - | 13696.0% | - | - |

| PUT | 58000 | 2026-06-06 | - | - | 35.0 | 13696.0% | - | 1.82 |

| CALL | 59000 | 2026-06-06 | 5.0 | - | 875.0 | 12751.0% | - | 0.5 |

| PUT | 59000 | 2026-06-06 | - | 190.0 | 30.0 | 12751.0% | - | 4.0 |

| CALL | 59500 | 2026-06-06 | 5.0 | - | - | 11610.0% | - | - |

| PUT | 59500 | 2026-06-06 | - | - | - | 11610.0% | - | - |

| CALL | 60000 | 2026-06-06 | 5.0 | - | - | 9491.0% | - | - |

| PUT | 60000 | 2026-06-06 | - | 210.0 | 900.0 | 9491.0% | - | 0.84 |

| CALL | 60500 | 2026-06-06 | 5.0 | - | - | 6991.0% | - | - |

| PUT | 60500 | 2026-06-06 | - | 240.0 | - | 6991.0% | - | - |

| CALL | 61000 | 2026-06-06 | - | - | 175.0 | 5104.0% | - | 10.0 |

| PUT | 61000 | 2026-06-06 | - | 475.0 | 610.0 | 5104.0% | - | 9.82 |

| CALL | 61500 | 2026-06-06 | - | 200.0 | 435.0 | 5615.0% | - | 7.64 |

| PUT | 61500 | 2026-06-06 | 5.0 | - | 790.0 | 5615.0% | - | 7.53 |

| CALL | 62000 | 2026-06-06 | - | 185.0 | 310.0 | 6846.0% | - | 7.01 |

| PUT | 62000 | 2026-06-06 | 5.0 | - | 530.0 | 6846.0% | - | 3.02 |

| CALL | 62500 | 2026-06-06 | - | - | 30.0 | 8732.0% | - | 5.38 |

| PUT | 62500 | 2026-06-06 | 5.0 | - | 720.0 | 8732.0% | - | 3.42 |

| CALL | 63000 | 2026-06-06 | - | - | 30.0 | 9654.0% | - | 3.4 |

| PUT | 63000 | 2026-06-06 | 5.0 | - | 665.0 | 9654.0% | - | 6.48 |

| CALL | 63500 | 2026-06-06 | - | 185.0 | 15.0 | 9955.0% | - | 8.16 |

| PUT | 63500 | 2026-06-06 | 5.0 | - | 1460.0 | 9955.0% | - | 0.11 |

| CALL | 64000 | 2026-06-06 | - | 185.0 | 15.0 | 9956.0% | - | 2.88 |

| PUT | 64000 | 2026-06-06 | 5.0 | - | 1100.0 | 9956.0% | - | 0.68 |

| CALL | 64500 | 2026-06-06 | - | - | 155.0 | 9960.0% | - | 0.87 |

| PUT | 64500 | 2026-06-06 | 5.0 | - | 1120.0 | 9960.0% | - | 0.1 |

| CALL | 65000 | 2026-06-06 | - | - | 45.0 | 9966.0% | - | 2.66 |

| PUT |

…(truncated)…

MCP tool: price_option_path

{"option_path": [2905.4565662417954, 3016.9035742459855, 3215.274111982002, 3424.7636992413354, 3697.474886033069, 3988.6102928558066, 4071.548722193347, 4098.4361007828265, 4242.039849000452, 4391.518119965076, 4420.2170980000665, 4513.092035726775, 4541.814244128633, 4570.115177837892, 4527.147427548443, 4480.317760726961, 4505.917875278588, 4456.162922095835, 4491.781896780405, 4460.351370202588, 4570.0366682431995], "volatility_used": 0.3388333022775113, "symbol": "BTC"}

MCP tool: price_option_path

{"option_path": [2670.6425275660804, 518.8861907494065, 63.745208601154445, 2.283068682676273, 0.00014183428555469835], "volatility_used": 0.2, "symbol": "BTC-USD"}

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.793 |

| 2023 | annual | 2.888 |

| 2022 | annual | 2.512 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.950 |

| 2023 | annual | 4.116 |

| 2022 | annual | 8.003 |

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 4.282 |

| 2024 | annual | 4.022 |

| 2023 | annual | 3.638 |

| 2022 | annual | 3.650 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 117.973 |

| 2023 | annual | 116.919 |

| 2022 | annual | 114.695 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 82.893 |

| 2023 | annual | 82.612 |

| 2022 | annual | 83.021 |

| Period | Frequency | Value |

|---|---|---|

| 2022 | annual | 13.943 |

…(truncated)…

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 4.977 |

| 2023 | annual | 5.415 |

| 2022 | annual | 3.134 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 0.218 |

| 2023 | annual | 0.235 |

| 2022 | annual | 1.974 |

| Period | Frequency | Value |

|---|---|---|

| 2022 | annual | 4.569 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 5.093 |

| 2023 | annual | 4.880 |

| 2022 | annual | 2.370 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 56.560 |

| 2023 | annual | 56.757 |

| 2022 | annual | 54.440 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 16.633 |

| 2023 | annual | 17.189 |

| 2022 | annual | 16.663 |

…(truncated)…

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 1.065 |

| 2023 | annual | 0.454 |

| 2022 | annual | 3.562 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.435 |

| 2023 | annual | 6.299 |

| 2022 | annual | 8.834 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 5.926 |

| 2023 | annual | 6.008 |

| 2022 | annual | 6.154 |

| Period | Frequency | Value |

|---|---|---|

| 2023 | annual | 20.752 |

| 2022 | annual | 21.006 |

…(truncated)…

MCP tool: generate_saving_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 17.811 |

| 2023 | annual | 17.672 |

| 2022 | annual | 18.693 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 21.841 |

| 2023 | annual | 21.879 |

| 2022 | annual | 22.294 |

- ■No historical observations available in the 5-year window.

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.950 |

| 2023 | annual | 4.116 |

| 2022 | annual | 8.003 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 82.893 |

| 2023 | annual | 82.612 |

| 2022 | annual | 83.021 |

| Period | Frequency | Value |

|---|---|---|

| 2022 | annual | 13.943 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 83490.000 |

| 2023 | annual | 80000.000 |

| 2022 | annual | 77330.000 |

…(truncated)…

MCP tool: generate_saving_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 42.833 |

| 2023 | annual | 42.572 |

| 2022 | annual | 44.834 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 40.611 |

| 2023 | annual | 41.130 |

| 2022 | annual | 42.355 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 5.093 |

| 2023 | annual | 4.880 |

| 2022 | annual | 2.370 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 0.218 |

| 2023 | annual | 0.235 |

| 2022 | annual | 1.974 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 56.560 |

| 2023 | annual | 56.757 |

| 2022 | annual | 54.440 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 16.633 |

| 2023 | annual | 17.189 |

| 2022 | annual | 16.663 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 13660.000 |

| 2023 | annual | 13750.000 |

| 2022 | annual | 13170.000 |

…(truncated)…

MCP tool: generate_saving_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 24.707 |

| 2023 | annual | 24.977 |

| 2022 | annual | 24.754 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 21.626 |

| 2023 | annual | 22.532 |

| 2022 | annual | 24.202 |

- ■No historical observations available in the 5-year window.

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.435 |

| 2023 | annual | 6.299 |

| 2022 | annual | 8.834 |

- ■No historical observations available in the 5-year window.

| Period | Frequency | Value |

|---|---|---|

| 2023 | annual | 20.752 |

| 2022 | annual | 21.006 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 41062.256 |

| 2023 | annual | 40917.513 |

| 2022 | annual | 40626.449 |

…(truncated)…

MCP tool: price_option_path

{"option_path": [3098.575338337978, 1738.4089210857746, 3711.3717511034483, 7466.3110258390225, 12626.080053086444, 18743.119296021316, 25299.23617106938, 30968.056034915666, 35646.761368428255, 43324.18885247564], "volatility_used": 0.2, "symbol": "BTC-USD"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.