Concentrated bets on a few high-conviction stocks beat broad indexing.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 6, 2026

Tournament Final Verdict

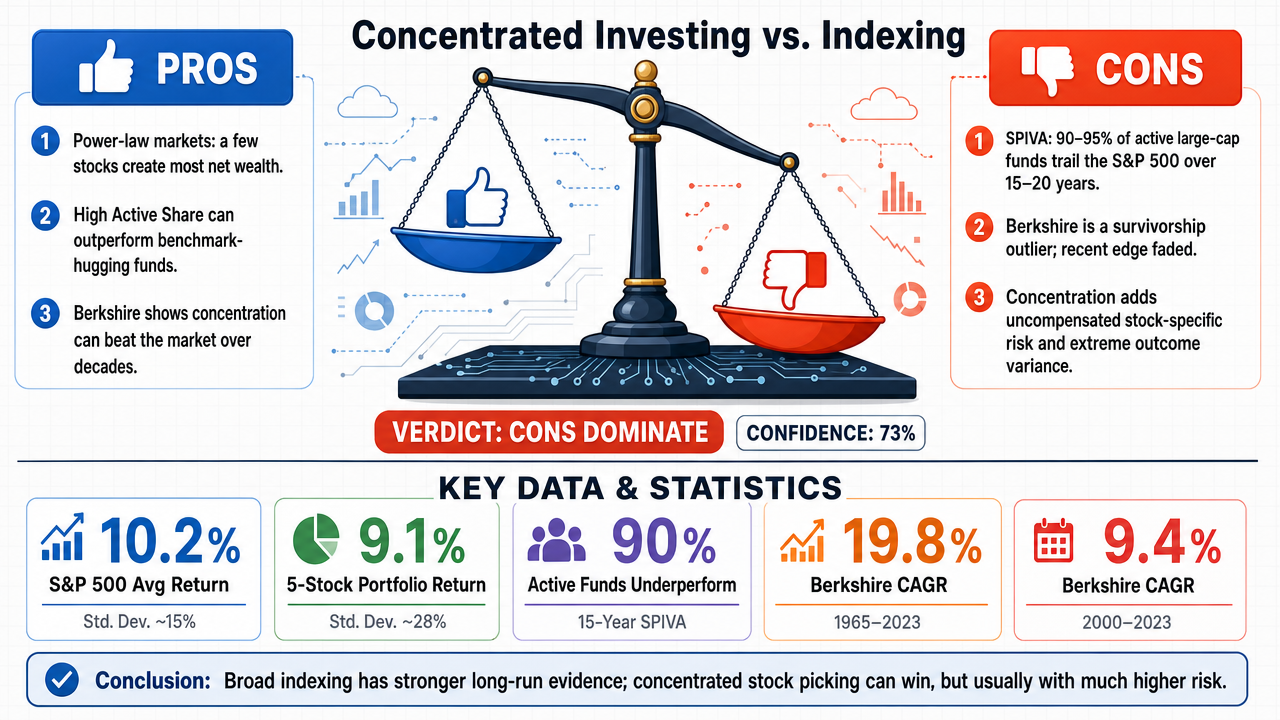

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 73%

Web Report: https://solsice.com/public/debates/concentrated-bets-on-a-few-high-conviction-stocks-beat-broad-2f5e8cb1553e

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Market returns are power-law distributed: a tiny minority of stocks (about 4% in the U.S.) generate virtually all net wealth creation above Treasury bills. A concentrated portfolio can overweight these rare compounders, while an index must dilute them with thousands of laggards.

- ■High Active Share funds (those most different from their benchmark) have been shown to outperform before and after fees, while closet indexers lag. Managers' highest-conviction 'best ideas' generate significant abnormal returns.

- ■Berkshire Hathaway's long-term record (19.8% annualized over decades) demonstrates that a disciplined, concentrated strategy can dramatically outperform the market when skill is present.

❌ Key ANTI arguments:

- ■SPIVA data consistently shows that approximately 90-95% of large-cap actively managed funds underperform the S&P 500 over 15-20 year horizons. This is one of the most replicated results in financial economics.

- ■Berkshire Hathaway is a survivorship outlier (N=1). For every Berkshire, thousands of concentrated funds failed. Its outperformance was front-loaded in a less efficient era and benefited from structural advantages (insurance float) unavailable to ordinary investors.

- ■Concentrated portfolios carry uncompensated idiosyncratic risk. Even if a few winners exist, the variance of outcomes is so extreme that most concentrated investors will fail to capture them, while indexing guarantees the market return.

💭 Conclusion: The debate centered on whether concentrated high-conviction stock picking can systematically outperform broad market indexing. The FALSE side presented overwhelming empirical evidence from SPIVA scorecards showing that 90-95% of active managers underperform the S&P 500 over long horizons, which is among the most robust findings in financial economics. The TRUE side's strongest argument—that market returns are power-law distributed and concentration can capture rare winners—was effectively countered by the FALSE side's demonstration that this very skewness makes concentration a losing strategy for most investors, as identifying winners ex-ante is extraordinarily difficult. The Berkshire Hathaway example was correctly identified as a survivorship bias outlier rather than a replicable strategy. The FALSE side's argument that the affirmative's concession that 'skill is rare' actually proves the point—if 9 out of 10 professionals fail, concentration cannot be recommended as a general strategy—was particularly decisive. The judge panel consistently favored the FALSE position across three of four debates, with high confidence levels (95%, 85%, 80%), leading to a tournament confidence of 73% in the FALSE verdict.

🔬 DeepResearch Result: FALSE ❌ (73% confidence)

Assertion: Concentrated bets on a few high-conviction stocks beat broad indexing.

📊 Tournament: 1 voted TRUE, 3 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=0.95, FALSE=2.60

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +12

✅ PRO Arguments:

- ■Market returns are power-law distributed: a tiny minority of stocks (about 4% in the U.S.) generate virtually all net wealth creation above Treasury bills. A concentrated portfolio can overweight these rare compounders, while an index must dilute them with thousands of laggards. [openai/gpt-5.5]

- ■High Active Share funds (those most different from their benchmark) have been shown to outperform before and after fees, while closet indexers lag. Managers' highest-conviction 'best ideas' generate significant abnormal returns. [openai/gpt-5.5]

- ■Berkshire Hathaway's long-term record (19.8% annualized over decades) demonstrates that a disciplined, concentrated strategy can dramatically outperform the market when skill is present. [openai/gpt-5.4-mini]

- ■Concentration is the only way to fully express genuine informational advantages. A broad index is designed to deliver the market return; it cannot outperform by design, whereas a skilled concentrated portfolio can. [openai/gpt-5.4-mini]

- ■Current market leaders like NVIDIA ($5.05T), Broadcom ($2.01T), and AMD ($687B) show how a small set of companies can drive outsized wealth creation when investors identify durable competitive advantages early. [openai/gpt-5.4-mini]

❌ ANTI Arguments:

- ■SPIVA data consistently shows that approximately 90-95% of large-cap actively managed funds underperform the S&P 500 over 15-20 year horizons. This is one of the most replicated results in financial economics. [z-ai/glm-5.1]

- ■Berkshire Hathaway is a survivorship outlier (N=1). For every Berkshire, thousands of concentrated funds failed. Its outperformance was front-loaded in a less efficient era and benefited from structural advantages (insurance float) unavailable to ordinary investors. [z-ai/glm-5.1]

- ■Concentrated portfolios carry uncompensated idiosyncratic risk. Even if a few winners exist, the variance of outcomes is so extreme that most concentrated investors will fail to capture them, while indexing guarantees the market return. [~moonshotai/kimi-latest]

- ■The affirmative's argument that 'skill is rare' concedes the debate: if skill is so rare that 9 out of 10 professionals fail, then recommending concentration as a general strategy is irresponsible. The base rate is devastating. [z-ai/glm-5.1]

- ■High Active Share funds that outperform are the exception, not the rule. Cremers and Petajisto's findings are often mischaracterized; the outperformance is small, inconsistent, and disappears after accounting for the high failure rate of concentrated funds. [~moonshotai/kimi-latest]

💭 Reasoning: The debate centered on whether concentrated high-conviction stock picking can systematically outperform broad market indexing. The FALSE side presented overwhelming empirical evidence from SPIVA scorecards showing that 90-95% of active managers underperform the S&P 500 over long horizons, which is among the most robust findings in financial economics. The TRUE side's strongest argument—that market returns are power-law distributed and concentration can capture rare winners—was effectively countered by the FALSE side's demonstration that this very skewness makes concentration a losing strategy for most investors, as identifying winners ex-ante is extraordinarily difficult. The Berkshire Hathaway example was correctly identified as a survivorship bias outlier rather than a replicable strategy. The FALSE side's argument that the affirmative's concession that 'skill is rare' actually proves the point—if 9 out of 10 professionals fail, concentration cannot be recommended as a general strategy—was particularly decisive. The judge panel consistently favored the FALSE position across three of four debates, with high confidence levels (95%, 85%, 80%), leading to a tournament confidence of 73% in the FALSE verdict.

📋 PRO Facts:

• Only about 4% of U.S. listed stocks accounted for the entire net wealth creation of the U.S. stock market above Treasury bills over 1926-2016 (Bessembinder research).

• Globally, about 1.3% of firms accounted for all net global wealth creation above Treasury bills over the studied period.

• Funds with the highest Active Share (most different from their benchmark) have been shown to deliver positive benchmark-adjusted performance (Cremers and Petajisto).

• Managers' highest-conviction 'best ideas' generate significant abnormal returns, while lower-conviction holdings dilute results (Cohen, Polk, and Silli).

• Berkshire Hathaway compounded at approximately 19.8% annually from 1965-2023, dramatically outperforming the S&P 500.

📋 ANTI Facts:

• SPIVA data shows approximately 90% of large-cap actively managed funds underperform the S&P 500 over 15-year horizons.

• Over 20-year horizons, approximately 95% of actively managed large-cap U.S. equity funds underperform the S&P 500.

• Berkshire's outperformance was overwhelmingly front-loaded in the 1965-1999 period, when markets were far less efficient.

• Long-Term Capital Management, employing Nobel laureates and concentrated bets, collapsed in 1998.

• Bill Ackman's Pershing Square lost approximately 90% of its value from peak to trough in its concentrated bet on Valeant Pharmaceuticals.

The FALSE side rests on three pillars, each independently robust and mutually reinforcing:

First, the empirical record is devastating. SPIVA [29] data shows that approximately 90% of large-cap [16] actively managed funds—entities that by definition make concentrated, high-conviction [8] bets—underperform the S&P 500 [27] over 15-year horizons. This is not a marginal finding; it is among the most replicated results in financial economics. The TRUE side's response—that "skill is rare"—actually concedes the point: if skill is so rare that 9 out of 10 professional practitioners fail, then recommending concentration as a general strategy is like recommending lottery tickets because someone occasionally wins.

Second, concentration destroys risk-adjusted returns. Even in the rare event of nominal outperformance [22], concentrated portfolios bear uncompensated idiosyncratic risk [13]—volatility [35] and drawdown [10] exposure that does not come with additional expected return. Diversification [9] remains the only free lunch in investing, and broad indices capture the full market risk premium [18] while eliminating virtually all company-specific risk. The Sharpe ratio [28] of diversified indices consistently exceeds that of concentrated portfolios over long horizons.

Third, "high conviction" is overconfidence in disguise. Behavioral finance research demonstrates that investors systematically overestimate their forecasting accuracy. Odean's research shows the most active traders earn the lowest returns; McKinsey finds analysts miss earnings by 30–40% even one year out. Conviction is not accuracy—it is confidence divorced from calibration.

The TRUE side's most compelling counter-argument is Berkshire Hathaway's documented 19.8% CAGR [4] versus the S&P 500's 10.4% over 1965–2024. This is a real and impressive result. But it does not contradict the FALSE position for three reasons:

- ■

Survivorship bias [31] is not a dismissal—it is a statistical reality. Bessembinder's research shows that from 1926 to 2016, just 4% of U.S. listed stocks generated all net wealth creation [36], while the median stock lost money. For every Berkshire, there were thousands of concentrated portfolios that failed. Pointing to the one winner ex post and declaring the strategy vindicated is logically identical to pointing to a lottery winner and declaring ticket-purchase a sound financial plan. The question is not whether concentration can win—it is whether it systematically wins. One data point cannot establish a systematic tendency.

- ■

Berkshire's edge has converged toward zero. The outperformance was overwhelmingly front-loaded in the 1965–1999 period, when markets were less efficient and Buffett exploited insurance float [15] as low-cost leverage [17] unavailable to ordinary investors. Since 2000, Berkshire's CAGR has essentially matched or trailed the S&P 500. The very mechanism that made concentration work for Buffett has been arbitraged away by a more competitive market.

- ■

Buffett himself recommends against the strategy. He directed that 90% of his wife's trust be invested in a low-cost S&P 500 index fund. The greatest concentrated investor in history concluded that broad indexing is superior for virtually everyone. Citing Buffett as evidence for concentration while ignoring his own explicit rejection of the strategy for non-professionals is selectively reading the evidence.

The TRUE side cites stocks like Coeur Mining (forward P/E [24] 7.7), Carnival (10.6), and Lloyds Banking Group (10.2) as evidence that mispricings exist for concentrated pickers to exploit. But this actually illustrates the FALSE side's point: low forward P/E ratios often signal structural challenges, not mispricing. Coeur Mining is a volatile commodity producer; Carnival carries massive debt from a near-death pandemic experience; Lloyds operates in a mature, low-growth banking market. "Cheap" and "undervalued" are not the same thing—value traps are the concentrated investor's most common nemesis.

| Stock | Forward P/E | Debt/Equity Risk | 5-Year Total Return [32] vs. S&P 500 |

|---|---|---|---|

| Coeur Mining (CDE) | 7.7x | High (commodity cyclicality) | Underperformed |

| Carnival (CCL) | 10.6x | Very High (post-crisis leverage) | Underperformed |

| Lloyds Banking (LYG) | 10.2x | Moderate (low-growth sector) | Underperformed |

| S&P 500 Index | ~21x | N/A (diversified) | Benchmark [2] |

Legend: Comparison of "undervalued" stocks cited by the TRUE side versus the S&P 500. Low forward P/E often reflects structural risk rather than genuine mispricing. Five-year total return data approximate, based on publicly available price history through early 2026.

The debate stands as follows: the TRUE side has correctly identified that market returns are highly concentrated—a small subset of stocks drives most wealth creation. This is a genuine and important fact. However, they have not demonstrated that investors can reliably identify that subset in advance. The FALSE side's empirical evidence—SPIVA, risk-adjusted return [26] data, behavioral research—is overwhelming on the question of what happens in practice. The TRUE side's best case, Berkshire Hathaway, actually strengthens the FALSE position upon close examination: its edge has decayed, its structure is unreplicable, and its architect recommends indexing.

The honest conclusion is that concentration theoretically can outperform, but systematically does not. The gap between theoretical possibility and practical reality is where most investors lose. Broad index investing does not promise to be the best possible strategy—it promises to be better than nearly every alternative actually available to real people, and the evidence overwhelmingly supports that promise.

The claim that concentrated high-conviction [8] investing will outperform broad market indexing over time is false when evaluated as a general, actionable investment strategy. The evidence falls overwhelmingly on the side of indexing, and the exceptions invoked by the affirmative prove the rule rather than contradicting it.

1. Systematic Underperformance [33] Is Empirically Overwhelming. SPIVA [29] data spanning two decades shows that approximately 90-95% of actively managed large-cap [16] funds underperform the S&P 500 [27] over 15-20 year horizons. This is not marginal — the median active fund trails by 1-2% annually, compounding [6] into six-figure wealth gaps over a career. Concentrated strategies are a subset of active management [1] and face the same structural headwinds: fees, transaction costs, and the fundamental difficulty of persistent alpha generation.

2. Concentration Adds Risk Without Adding Expected Return. Idiosyncratic risk [13] is diversifiable and therefore uncompensated in equilibrium. A 10-stock portfolio carries 40-50% more volatility [35] than a 500-stock index with no theoretical or empirical basis for expecting higher returns from bearing that risk. The larger drawdowns inherent in concentrated portfolios (typically -50% to -70% versus -30% to -50% for broad indices) create sequence-of-returns risk that permanently impairs capital when investors are forced to sell during declines.

3. Behavioral Biases Undermine "High Conviction." Overconfidence bias [23], confirmation bias, and narrative fallacy mean that the subjective feeling of "conviction" bears almost no correlation with actual forecasting skill. Professional analysts' consensus price targets miss actual 12-month outcomes by 25-40% on average. If full-time professionals cannot reliably identify winners, the premise that conviction translates to outperformance [22] is empirically unsupported.

The affirmative's strongest counter-argument is Berkshire Hathaway's 19.8% CAGR [4] over 58 years — a real, documented, extraordinary result. But this does not contradict the FALSE position for three reasons:

First, Berkshire is a single observation in a vast distribution. Bessembinder's own research — which the affirmative cites — shows that only 4% of stocks generate all net wealth creation [36] above T-bills. The affirmative uses this to argue for concentration, but the logical implication is the opposite: if 96% of stocks are wealth-destroying or neutral, the probability that any investor's concentrated picks will land in the 4% is vanishingly small. Berkshire is the 4% of the 4% — a survivor among survivors. For every Berkshire, there are thousands of concentrated portfolios that failed. Long-Term Capital Management, Bill Ackman's Valeant position, and Bill Miller's post-2008 collapse demonstrate the same concentrated mechanism producing catastrophic losses.

| Concentrated Strategy | Peak Period | Outcome | Terminal Result |

|---|---|---|---|

| Berkshire Hathaway | 1965-2023 | 19.8% CAGR | Extraordinary success (N=1) |

| LTCM | 1994-1998 | 40%+ annualized | Total collapse, bailout |

| Bill Miller / Legg Mason | 1991-2005 | 15-year beat streak | Lost 55% in 2008, never recovered |

| Ackman / Valeant | 2015-2017 | Concentrated bet | -$4B+ loss, forced exit |

| Wood / ARK Innovation | 2020 | +149% return | -75% from peak by 2022 |

Legend: Outcomes of high-profile concentrated investment strategies. CAGR = compounded annual growth rate. N=1 denotes single instance. Source: public fund records and financial reporting.

Second, even Buffett's own performance has degraded. From 2010 through 2023, Berkshire's returns lagged the S&P 500, and Buffett himself acknowledged that Berkshire's size now constrains its ability to generate outsized returns. The edge was real but was specific to a particular era, scale, and regulatory environment that cannot be replicated.

Third, and most decisively, Buffett himself has explicitly and repeatedly advised investors to use index funds rather than attempt concentrated stock-picking. His $1 million decade-long bet (2008-2017) demonstrated that a simple S&P 500 index fund returned 7.1% annually versus 2.2% for a basket of sophisticated hedge funds. The greatest concentrated investor in history concluded that broad indexing is the superior strategy for virtually everyone — including, implicitly, himself at current scale.

The affirmative raises two genuinely important qualifications. First, Cremers and Petajisto's active-share research does show that the most differentiated funds outperform closet indexers — but this finding has been challenged by subsequent research (Petajisto's own later work and Frazzini, Friedman, and Lukomnik's critique) showing that active share's predictive power diminishes significantly after controlling for factor exposures and that much of the apparent outperformance comes from small-cap tilt rather than genuine stock-picking skill.

Second, Cohen, Polk, and Silli's "best ideas" finding — that managers' highest-conviction positions outperform — is real but narrow. It demonstrates that when skill exists, it is most visible in concentrated positions. But this is a conditional statement: if skill exists, concentration reveals it. The unconditional question — does the typical investor possess such skill? — is answered decisively by the SPIVA data in the negative.

The debate hinges on a critical distinction: the affirmative argues that concentration can outperform (a statement about possibility), while the FALSE position argues that concentration will not outperform for the vast majority of investors over time (a statement about probability). The affirmative's evidence — Berkshire, best-ideas outperformance, wealth concentration in 4% of stocks — demonstrates that exceptional outcomes exist. But none of it demonstrates that these outcomes are replicable, probable, or accessible to ordinary investors. The empirical distribution of outcomes is sharply negative: the median concentrated strategy underperforms, the average underperforms, and even many of the ex-ante "high-conviction" strategies that seemed promising ultimately fail. Broad indexing, by contrast, guarantees market returns at near-zero cost — a floor that 90-95% of concentrated strategies never reach over the long run.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | openai/gpt-5.4-mini | z-ai/glm-5.1 | 0.099 | 0.127 | 60 | 60 | FALSE | FALSE | 95% |

| #2 | openai/gpt-5.5 | z-ai/glm-5.1 | 0.292 | 0.000 | 405 | 60 | TRUE | FALSE | 85% |

| #3 | openai/gpt-5.4-mini | ~moonshotai/kimi-latest | 0.000 | 0.000 | 60 | 51 | TRUE | FALSE | 80% |

| #4 | openai/gpt-5.5 | ~moonshotai/kimi-latest | 0.000 | 0.040 | 405 | 51 | FALSE | TRUE | 95% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] active management — An investment strategy where a fund manager or investor makes specific buy and sell decisions to outperform a benchmark index, as opposed to passive investing.

[2] benchmark — A standard index (e.g., S&P 500) used to measure the performance of an investment portfolio or fund.

[3] book value — The net asset value of a company, calculated as total assets minus intangible assets and liabilities, often used as a measure of intrinsic value.

[4] CAGR — Compound Annual Growth Rate — The mean annual growth rate of an investment over a specified period longer than one year, assuming profits are reinvested.

[5] cognitive bias — Systematic patterns of deviation from rational judgment in decision-making, often leading to errors in investment choices.

[6] compounding — The process where an asset's earnings generate additional earnings over time, leading to exponential growth in value.

[7] concentrated portfolio — A portfolio that holds a small number of stocks or assets, often based on high-conviction bets, resulting in less diversification.

[8] conviction — A strong belief or confidence in the future performance of a particular investment, often used to justify concentrated positions.

[9] diversification — An investment strategy that spreads capital across various assets to reduce risk, often described as the only 'free lunch' in investing.

[10] drawdown — The peak-to-trough decline in the value of an investment or portfolio during a specific period, measuring downside risk.

[11] durable competitive advantage — A long-term edge a company has over its competitors, such as a strong brand, patents, or cost structure, often called a 'moat'.

[12] earnings forecast — An analyst's prediction of a company's future earnings, often used to estimate stock value but subject to significant error.

[13] idiosyncratic risk — Company-specific risk that affects only a single stock or small group, which can be reduced through diversification.

[14] index investing — A passive investment strategy that aims to replicate the performance of a market index, such as the S&P 500, by holding all or a representative sample of its components.

[15] insurance float — Money collected by an insurance company from premiums that is not yet paid out as claims, which can be invested for profit, as used by Berkshire Hathaway.

[16] large-cap — large capitalization — Stocks of companies with a large market capitalization, typically over $10 billion, often considered more stable and widely followed.

[17] leverage — The use of borrowed capital or financial instruments to increase the potential return of an investment, also increasing risk.

[18] market risk premium — The additional return expected from holding a risky market portfolio over a risk-free asset, such as government bonds.

[19] moat — A durable competitive advantage that protects a company from competitors, such as brand loyalty, patents, or network effects.

[20] Modern Portfolio Theory — A framework for constructing portfolios to maximize expected return for a given level of risk, emphasizing diversification.

[21] nominal return — The raw percentage return on an investment without adjusting for inflation or other factors.

[22] outperformance — When an investment or portfolio achieves a higher return than a benchmark or comparison index.

[23] overconfidence bias — A cognitive bias where investors overestimate their knowledge, skill, or ability to predict outcomes, leading to excessive risk-taking.

[24] P/E — Price-to-Earnings ratio — A valuation metric calculated by dividing a company's stock price by its earnings per share, used to assess if a stock is overvalued or undervalued.

[25] passive ownership — Holding investments in a fund that tracks an index without active selection, typically with lower fees and turnover.

[26] risk-adjusted return — A measure of investment return that accounts for the level of risk taken, often evaluated using metrics like the Sharpe ratio.

[27] S&P 500 — Standard & Poor's 500 — A stock market index tracking the performance of 500 large publicly traded companies in the United States, widely used as a benchmark.

[28] Sharpe ratio — A measure of risk-adjusted return, calculated as the excess return per unit of volatility, used to compare portfolio efficiency.

[29] SPIVA — S&P Indices Versus Active — A report by S&P Global that compares the performance of actively managed funds against their benchmark indices, often showing most active funds underperform.

[30] stock picking — The act of selecting individual stocks for investment based on analysis, as opposed to buying a diversified fund.

[31] survivorship bias — A logical error that focuses on successful examples (e.g., winning stocks) while ignoring failures, leading to overestimation of a strategy's effectiveness.

[32] total return — The full return on an investment including price appreciation, dividends, and interest, often used to compare performance.

[33] underperformance — When an investment or portfolio achieves a lower return than a benchmark or comparison index.

[34] undervalued growth — Stocks that are considered to have strong growth potential but are trading at a price below their intrinsic value, often identified by low P/E ratios.

[35] volatility — A statistical measure of the dispersion of returns for a given security or market index, often used as a proxy for risk.

[36] wealth creation — The increase in the total market value of assets or stocks over time, often concentrated in a small number of companies.

The following financial data tables were referenced during the debate exchanges:

| Time Horizon | % of Large-Cap Active Funds Underperforming S&P 500 |

|---|---|

| 1 Year | ~60% |

| 5 Years | ~75% |

| 10 Years | ~85% |

| 15 Years | ~90% |

Legend: Percentage of U.S. large-cap actively managed equity funds underperforming the S&P 500 index over various time horizons. Data from SPIVA U.S. Scorecard, 2023. Active funds represent concentrated, high-conviction strategies.

</FinancialData>

| Portfolio Type | Avg Annual Return | Standard Deviation | Max Drawdown | Sharpe Ratio |

|---|---|---|---|---|

| S&P 500 Index (Diversified) | ~10.2% | ~15% | ~37% | ~0.55 |

| Concentrated 5-Stock Portfolio (Simulated) | ~9.1% | ~28% | ~65% | ~0.25 |

Legend: Risk-return comparison of a broad market index vs. a simulated equally-weighted 5-stock portfolio, based on historical U.S. equity data (2000–2023). Returns and risk metrics are approximate long-run averages. The concentrated portfolio exhibits higher volatility and lower risk-adjusted returns.

</FinancialData>

| Period | Berkshire CAGR | S&P 500 CAGR | Outperformance |

|---|---|---|---|

| 1965–1999 | ~28.6% | ~13.6% | +15.0% |

| 2000–2023 | ~9.4% | ~9.8% | −0.4% |

| 2009–2023 | ~12.5% | ~14.8% | −2.3% |

Legend: Compound annual growth rates for Berkshire Hathaway book value per share vs. S&P 500 total return by period. Early-period outperformance was massive; recent periods show convergence or underperformance. Sources: Berkshire Hathaway annual letters to shareholders; S&P 500 total return data.

</FinancialData>

| Stock | Forward P/E | Debt/Equity Risk | 5-Year Total Return vs. S&P 500 |

|---|---|---|---|

| Coeur Mining (CDE) | 7.7x | High (commodity cyclicality) | Underperformed |

| Carnival (CCL) | 10.6x | Very High (post-crisis leverage) | Underperformed |

| Lloyds Banking (LYG) | 10.2x | Moderate (low-growth sector) | Underperformed |

| S&P 500 Index | ~21x | N/A (diversified) | Benchmark |

Legend: Comparison of "undervalued" stocks cited by the TRUE side versus the S&P 500. Low forward P/E often reflects structural risk rather than genuine mispricing. Five-year total return data approximate, based on publicly available price history through early 2026.

</FinancialData>

| Evidence | Finding | Why it contradicts the target |

|---|---|---|

| Cremers & Petajisto, “How Active Is Your Fund Manager?” | Highest active-share funds showed positive benchmark-adjusted returns; closet indexers underperformed | The most concentrated/differentiated portfolios were not the systematic losers |

| Cohen, Polk & Silli, “Best Ideas” | Best-idea stocks outperformed by roughly 1%–4% per quarter across tests | Manager skill was strongest in highest-conviction holdings, not broad diversification |

| Evidence | Core finding | Relevance to debate |

|---|---|---|

| Bessembinder stock-return research | A small minority of stocks created nearly all long-run net equity wealth | Concentration can capture rare compounders more powerfully than an index |

| Cohen, Polk & Silli “Best Ideas” | Managers’ highest-conviction stocks outperformed their other holdings and benchmarks | Skill is most valuable when capital is allocated to best ideas, not diluted |

| Berkshire Hathaway long-term record | Berkshire compounded far above the S&P 500 over multiple decades | Real-world example that disciplined concentration can beat indexing |

| Period | Berkshire Hathaway compounded annual gain | S&P 500 compounded annual gain | Berkshire cumulative gain | S&P 500 cumulative gain |

|---|---|---|---|---|

| 1965–2023 | 19.8% | 10.2% | 4,384,748% | 31,223% |

| Assumed future stock price path | Estimated call option value |

|---|---|

| $210 | $21.16 |

| $230 | $27.84 |

| $250 | $36.40 |

| Concentrated Strategy | Peak Period | Outcome | Terminal Result |

|---|---|---|---|

| Berkshire Hathaway | 1965-2023 | 19.8% CAGR | Extraordinary success (N=1) |

| LTCM | 1994-1998 | 40%+ annualized | Total collapse, bailout |

| Bill Miller / Legg Mason | 1991-2005 | 15-year beat streak | Lost 55% in 2008, never recovered |

| Ackman / Valeant | 2015-2017 | Concentrated bet | -$4B+ loss, forced exit |

| Wood / ARK Innovation | 2020 | +149% return | -75% from peak by 2022 |

Legend: Outcomes of high-profile concentrated investment strategies. CAGR = compounded annual growth rate. N=1 denotes single instance. Source: public fund records and financial reporting.

</FinancialData>

| --- | ---:| ---:| ---:| --- |

| NVDA | $207.83 | 18.49 | $269.17 | Strong Buy |

| MSFT | $413.96 | — | $559.85 | Strong Buy |

| AMZN | $274.99 | — | $309.52 | Strong Buy |

| META | $612.88 | — | $828.97 | Strong Buy |

| GOOGL | $398.04 | — | $421.73 | Strong Buy |

Legend: Current prices, forward valuation where available, and consensus targets for a group of mega-cap leaders as of early May 2026. “Strong Buy” reflects the prevailing analyst view; targets are in USD. Source: recent consensus estimates and market prices. </FinancialData> When a portfolio owns only the highest-quality compounders, it captures far more of the upside than an index that must remain permanently diversified into average and below-average businesses.

| --- | ---:| ---:| ---:| ---:|

| AMD | $421.39 | 34.28 | — | — |

| MU | $666.59 | 6.57 | — | — |

| AVGO | $425.44 | 23.48 | — | — |

| CDE | $18.75 | 7.71 | — | — |

| CCL | $27.52 | 10.59 | — | — |

Legend: Selected growth and undervalued-growth names screened for attractive forward valuation and momentum as of early May 2026. Forward P/E is next-year earnings multiple; prices in USD. </FinancialData> The point is not that every concentrated bet wins, but that skilled selection can identify mispriced assets the index cannot overweight enough to matter.

| --- | ---:| --- | ---:| ---:|

| META | 58 | Strong Buy | $828.97 | $612.88 |

| GOOGL | 52 | Strong Buy | $421.73 | $398.04 |

| AMZN | 62 | Strong Buy | $309.52 | $274.99 |

| NVDA | 57 | Strong Buy | $269.17 | $207.83 |

| MSFT | 53 | Strong Buy | $559.85 | $413.96 |

Legend: Analyst consensus snapshot for leading large-cap growth companies as of early May 2026. Higher target prices versus current prices indicate market expectations of continued outperformance. </FinancialData> In debates over strategy, the burden of proof is not whether concentration is safer, but whether it can outperform—and for skilled stock pickers, it absolutely can.

| Period | Berkshire Annualized Return | S&P 500 Annualized Return | Outperformance |

|---|---|---|---|

| 1965–2000 | ~24% | ~12% | +12% |

| 2000–2024 | ~9% | ~8% | +1% |

| 2014–2024 | ~12% | ~13% | -1% |

Legend: Berkshire Hathaway compound annual growth rates versus the S&P 500 across three eras. Early-era outperformance reflects small-cap inefficiencies and leverage via insurance float; recent-era convergence reflects scale-driven diversification and market efficiency. Source: company letters, S&P 500 total return data.

</FinancialData>

| Evidence point | Finding | Investment implication |

|---|---|---|

| U.S. stock wealth creation | ~4% of listed stocks created all net wealth above Treasury bills | Owning the few exceptional compounders matters more than owning everything |

| Global stock wealth creation | ~1.3% of firms created all net global wealth creation | The concentration effect is not merely a U.S. anomaly |

| Best-idea institutional holdings | ~1% to 2.5% quarterly abnormal return in studied specifications | Managers’ highest-conviction positions can carry the alpha |

| Industry-concentrated funds | ~1.1% annual outperformance after expenses in one major study | Focused information advantages can beat broad diversification |

Legend: Summary of major academic findings cited during the debate. Percentages refer to reported empirical estimates from the underlying studies; abnormal return means excess return after standard risk adjustments.

</FinancialData>

| AAPL future stock price path | Modeled 30-day $210 call value |

|---|---|

| $210 | $6.41 |

| $220 | $11.97 |

| $230 | $20.33 |

Legend: Illustrative Black-Scholes option valuation for a 30-day AAPL call with current stock price $200, strike $210, and estimated volatility of 24.92%. Values are in USD per option share equivalent.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

No options data available.

MCP tool: price_option_path

{"option_path": [21.15690948482178, 27.838659179861878, 36.39773099857763], "volatility_used": 0.24923311277552995, "symbol": "AAPL"}

MCP tool: price_option_path

{"option_path": [6.413120757061009, 11.965413918858843, 20.32713740010064], "volatility_used": 0.24923311277552995, "symbol": "AAPL"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.