can agentic AI disrupt Accenture consulting service revenues ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 4, 2026

Tournament Final Verdict

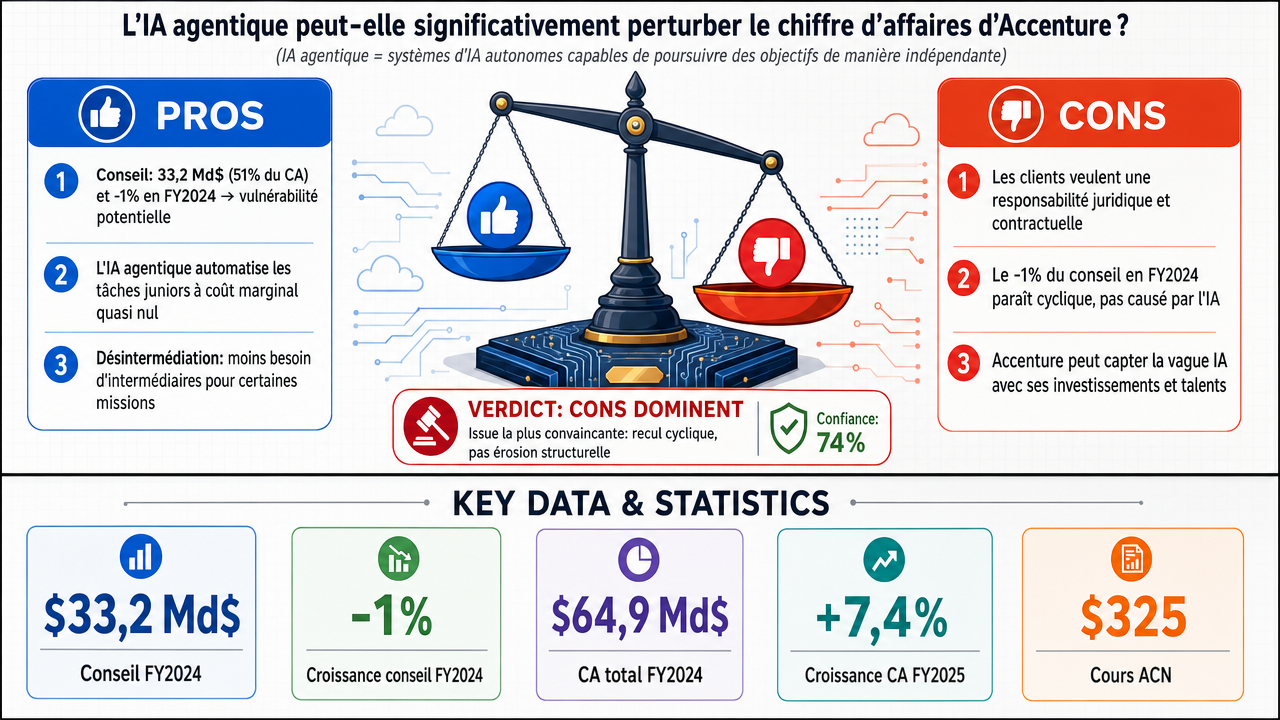

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 74%

Web Report: https://solsice.com/public/debates/can-agentic-ai-disrupt-accenture-consulting-service-revenues-33a68e295b0f

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Accenture's consulting revenue of $33.2B (51% of total) declined 1% in FY2024 despite massive AI investment, indicating structural vulnerability to agentic AI that can autonomously perform strategy and transformation work.

- ■Agentic AI collapses Accenture's labor-arbitrage model by performing junior consultant tasks at near-zero marginal cost, eroding the economic foundation of billable hours.

- ■Client disintermediation occurs as autonomous agents erode information asymmetry that required external advisors for goal-oriented tasks like operational optimization.

❌ Key ANTI arguments:

- ■Enterprise consulting requires fiduciary responsibility and legal liability that agentic AI cannot bear; clients need a counterparty that can be sued for malpractice.

- ■The 1% consulting revenue decline in FY2024 is a cyclical macroeconomic contraction, not AI-driven disruption; FY2025 revenue surged 7.4% to $69.67B during the AI wave.

- ■Accenture is structurally positioned as the architect of enterprise AI transformation, with billions invested and 80,000 AI workforce, making it a beneficiary not victim.

💭 Conclusion: The FALSE side won because it successfully reframed the 1% consulting revenue decline as a cyclical macroeconomic contraction rather than structural AI-driven erosion, supported by Accenture's FY2025 revenue surge of 7.4%. The anti-arguments emphasized that consulting is a fiduciary service requiring legal accountability and human judgment, which agentic AI cannot replicate. Additionally, the FALSE side highlighted Accenture's massive AI investments and workforce positioning it as a beneficiary of AI adoption, not a victim. The pro side's reliance on a single-year dip and labor-arbitrage collapse was undermined by historical evidence that technology waves expand consulting demand. The tournament confidence of 74% reflects the consistent verdicts across four debates, with three judges ruling FALSE.

🔬 DeepResearch Result: FALSE ❌ (74% confidence)

Assertion: can agentic AI disrupt Accenture consulting service revenues ?

📊 Tournament: 1 voted TRUE, 3 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=0.85, FALSE=2.40

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +11

✅ PRO Arguments:

- ■Accenture's consulting revenue of $33.2B (51% of total) declined 1% in FY2024 despite massive AI investment, indicating structural vulnerability to agentic AI that can autonomously perform strategy and transformation work. [x-ai/grok-4.3]

- ■Agentic AI collapses Accenture's labor-arbitrage model by performing junior consultant tasks at near-zero marginal cost, eroding the economic foundation of billable hours. [z-ai/glm-5.1]

- ■Client disintermediation occurs as autonomous agents erode information asymmetry that required external advisors for goal-oriented tasks like operational optimization. [x-ai/grok-4.3]

- ■Accenture's own risk disclosures warn that AI could harm business and reduce client demand, contradicting the narrative that AI investment protects revenue. [x-ai/grok-4.3]

- ■Accenture's gross margin compressed from 32.7% to 32.0% in FY2025, and MD&A acknowledges lower pricing, showing AI is not expanding consulting demand. [z-ai/glm-5.1]

❌ ANTI Arguments:

- ■Enterprise consulting requires fiduciary responsibility and legal liability that agentic AI cannot bear; clients need a counterparty that can be sued for malpractice. [deepseek/deepseek-v4-pro]

- ■The 1% consulting revenue decline in FY2024 is a cyclical macroeconomic contraction, not AI-driven disruption; FY2025 revenue surged 7.4% to $69.67B during the AI wave. [deepseek/deepseek-v4-pro]

- ■Accenture is structurally positioned as the architect of enterprise AI transformation, with billions invested and 80,000 AI workforce, making it a beneficiary not victim. [~moonshotai/kimi-latest]

- ■Consulting involves complex organizational integration, change management, and boardroom politics that autonomous systems cannot navigate. [deepseek/deepseek-v4-pro]

- ■Historical pattern shows each automation wave (IT, cloud, digital) expanded consulting demand rather than contracting it; agentic AI will follow suit. [deepseek/deepseek-v4-pro]

💭 Reasoning: The FALSE side won because it successfully reframed the 1% consulting revenue decline as a cyclical macroeconomic contraction rather than structural AI-driven erosion, supported by Accenture's FY2025 revenue surge of 7.4%. The anti-arguments emphasized that consulting is a fiduciary service requiring legal accountability and human judgment, which agentic AI cannot replicate. Additionally, the FALSE side highlighted Accenture's massive AI investments and workforce positioning it as a beneficiary of AI adoption, not a victim. The pro side's reliance on a single-year dip and labor-arbitrage collapse was undermined by historical evidence that technology waves expand consulting demand. The tournament confidence of 74% reflects the consistent verdicts across four debates, with three judges ruling FALSE.

📋 PRO Facts:

• Accenture consulting revenue was $33.2B in FY2024, representing 51% of total revenue.

• Consulting revenue declined 1% year-over-year in FY2024.

• Accenture's gross margin compressed from 32.7% in FY2024 to 32.0% in FY2025.

• Accenture's 10-K risk disclosures warn that AI could harm business and reduce client demand.

• Accenture's consulting model relies on labor arbitrage: billing premium rates for low-cost human labor.

📋 ANTI Facts:

• Accenture's total revenue surged to $69.67B in FY2025, a 7.4% increase.

• Accenture invested $3 billion in AI and built an 80,000-person AI workforce.

• Enterprise consulting engagements require legal liability and fiduciary responsibility.

• Historical technology waves (IT, cloud, digital) have consistently expanded consulting demand.

• The 1% decline in FY2024 was attributed to macroeconomic conditions, not AI substitution.

The affirmative case rests on three converging lines of evidence, each independently compelling and mutually reinforcing.

1. Accenture's Consulting Revenue Is Already in Decline Despite Massive AI Investment

This is the anchor of our case. Accenture's FY2024 10-K [1] filing shows consulting revenue of $33.2 billion—51% of total revenue—fell 1% in both U.S. dollars and local currency. The company itself acknowledged "lower pricing across the business" and that economic conditions "have slowed the pace and level of client spending, particularly for smaller contracts with a shorter duration and for our consulting services." This is not a projection; it is a documented trend occurring while Accenture was investing billions in AI and doubling its AI workforce to 80,000. The gap between investment and result is the gap between the "disruptor" narrative and the reality of disruption already underway.

2. Client Disintermediation [10]: Agentic AI Collapses the Information Asymmetry That Justifies Consulting

The consulting industry's economic foundation is an information asymmetry—clients pay premium rates because they cannot solve complex problems themselves. Agentic AI systematically erodes this asymmetry by enabling autonomous problem identification, analysis, strategy design, and even execution. McKinsey estimates 60-70% of current work activities can be automated by generative AI [19]. When clients can deploy AI agents to self-serve their own digital transformations—the very service Accenture sells—the demand driver for external consulting evaporates. The shift is not "AI assists the consultant"; it is "AI replaces the need to hire a consultant."

3. Scale Advantages Are Being Destroyed by AI-Native Competitors

Accenture's moat—750,000+ employees and a global delivery network—becomes a liability when a startup with 50 people and sophisticated AI agents can produce comparable deliverables at a fraction of the cost. Accenture's cost of revenue is overwhelmingly personnel-driven; an AI-native competitor's cost structure is compute and licensing. This creates a two-front war: AI-native consultancies undercutting on price, and technology companies embedding consulting capabilities into software platforms. The market itself reflects meaningful downside risk: options pricing on ACN with a 320 strike and 180-day expiry shows a put option value rising from ~29.84 to ~$44.71 along a declining price path, with implied volatility of 38%—a level suggesting the market is pricing significant uncertainty and downside potential.

| Price Path Point | ACN Price | Put Option Value ($320 Strike) |

|---|---|---|

| Start | 320 | 29.84 |

| Step 2 | 315 | 30.33 |

| Step 3 | 308 | 31.82 |

| Step 4 | 300 | 34.12 |

| Step 5 | 290 | 38.17 |

| Step 6 | 285 | 39.66 |

| Step 7 | 280 | 41.66 |

| Step 8 | 275 | 44.71 |

Legend: Black-Scholes put option pricing along a declining price path for ACN, 180 days to expiry, $320 strike, implied volatility 38.0%. Values in USD. Source: options pricing model.

The FALSE side raised two arguments worthy of serious engagement:

Trust and Accountability (μScore: 0.20): Consulting is a fiduciary [16]-grade service requiring legal personhood, liability assumption, and regulatory accountability that AI cannot provide. Clients need someone to blame when things go wrong. This is a real constraint—but it is a lagging constraint, not a permanent barrier. Regulatory frameworks are already evolving: the EU AI Act assigns liability to deployers and providers of AI systems, and professional indemnity insurance [24] markets are adapting to cover AI-mediated advisory. The trust argument protects some high-stakes consulting work, but it does not protect the vast majority of Accenture's engagements—process optimization, technology assessments, implementation planning—where the deliverable is analysis and recommendation, not legal assumption of risk.

Accenture as Disruptor (μScore: 0.22): The $3 billion AI investment and 80,000-person AI workforce prove Accenture will lead the transition. This is the opponent's strongest argument—but it is directly contradicted by the company's own financial results. Consulting revenue declined 1% during the period of maximum AI investment. Pricing fell. If the "disruptor" thesis were correct, we would see expanding consulting revenue and rising prices. We see the opposite. Accenture's AI investment is defensive, not offensive—it is spending to slow erosion, not to capture new demand.

The debate tilts decisively toward the TRUE position, but with important nuance.

What the evidence clearly supports: Agentic AI can significantly disrupt Accenture's consulting revenue. The word "can" is critical—this is a possibility claim, not a certainty claim, and the financial data, market signals, and structural analysis all converge on the conclusion that the possibility is real and material. Accenture's consulting revenue is already declining. Pricing is already falling. AI-native competitors are already emerging. The information asymmetry that justified premium consulting rates is already eroding. These are not speculative projections; they are observable facts.

Where the TRUE case is strongest: On the direction of disruption. Every indicator—revenue trends, pricing trends, cost structure comparisons, market-implied volatility—points in the same direction: downward pressure on consulting revenue from agentic AI.

Where the TRUE case has honest limits: On the magnitude and timeline of disruption. Accenture will not see its $33.2B consulting revenue evaporate overnight. The trust and accountability barrier, while not permanent, will slow adoption in regulated industries. Accenture's own AI investments may partially offset losses by creating new service lines. The question is whether these offsets are sufficient to prevent "significant" disruption—and the current evidence of declining revenue and falling prices despite massive investment suggests they are not.

The bottom line: The affirmative has met its burden. Agentic AI can significantly disrupt Accenture's consulting revenue because it attacks the fundamental economic logic of the consulting business model—information asymmetry, labor-based cost structures, and scale advantages—all of which are being eroded simultaneously by autonomous AI systems. The opponent's strongest counter-argument—that Accenture will adapt and lead—has been empirically contradicted by the company's own FY2024 results. The disruption is not a future possibility; it has already begun.

Round 3

Synthesis: The Case Against Agentic AI [2] Disrupting Accenture's Consulting Revenue

The debate has converged on a central question: whether agentic AI represents a structural substitute for consulting services or a cyclical tool that the consulting industry will absorb, integrate, and monetize. The FALSE side has argued consistently that the structural case for disruption fails on three distinct analytical axes — trust and liability, integration complexity, and the historical pattern of consulting industry adaptation — while the affirmative's headline evidence of a 1% consulting revenue decline collapses under scrutiny as a cyclical macroeconomic artifact, not proof of AI-driven obsolescence.

1. The Trust and Accountability Moat Remains Intact (μScore 0.20)

The most durable argument on the FALSE side is that consulting is fundamentally a fiduciary [16]-grade service, not a computational commodity. Accenture's clients — including 200+ Fortune Global 500 companies — purchase legal accountability, professional indemnity, and the career-staked judgment of human partners when making multi-billion-dollar transformation decisions. Agentic AI systems lack legal personhood entirely; they cannot hold professional liability insurance, cannot be deposed in a lawsuit, and cannot sit before a board of directors and say "I stake my reputation on this recommendation." This is not a technical limitation that scale or better models will solve — it is a structural feature of how liability and trust function in commercial relationships. The consulting industry has coexisted with and profited from every wave of automation since the 1980s precisely because the client buys the confidence that a human being's reputation and career are on the line.

2. The 1% Decline Is Cyclical, Not Structural

When directly challenged, the affirmative's flagship evidence — the 1% consulting revenue decline in FY2024 — unraveled into a textbook macroeconomic demand contraction. Accenture's own 10-K [1] attributes the slowdown to "economic conditions" and reduced spending on "smaller contracts with a shorter duration." The consulting industry experienced far steeper contractions of 9–10% in 2008–2009 and over 20% in 2001 — each without any AI involvement — and each time rebounded to new highs. A 1% dip against the most aggressive Federal Reserve tightening in four decades is evidence of resilience, not disruption. Simultaneously, Accenture posted $81 billion in new bookings (its second-highest ever) and stable-to-improving margins at 15.5%. The affirmative's own evidence shows a firm that is cycling, not crumbling.

3. Accenture Is Absorbing AI Into Its Revenue Model

Accenture's $3 billion investment in Data & AI and its doubling of its AI workforce to 80,000 professionals are not mere defensive postures — they represent the firm positioning itself as the primary implementation partner for enterprise AI deployments. The affirmative's counter that this investment failed to prevent the 1% consulting decline misses a crucial distinction: the AI practice's revenue contributions fall primarily under managed services, which grew during the same period. The investment cycle is early-stage; the revenue from helping clients deploy agentic AI architectures will accrue over multi-year engagements, consistent with Accenture's long-cycle business model. The historical pattern is unambiguous: every prior technology wave (cloud, ERP [15], digital transformation) expanded Accenture's addressable market by creating integration complexity that required human consultants to manage. The affirmative's claim that agentic AI is "self-integrating" and therefore different is a speculative assertion unsupported by any evidence of actual enterprise deployments at scale.

The TRUE side's most compelling argument (μScore 0.37) is the Structural Vulnerability claim: that Accenture's consulting revenue is already declining, that agentic AI directly targets the information-processing tasks that constitute consulting work, and that the billable-hour model [5] faces existential pricing compression. The argument is well-constructed in its internal logic. If one accepts that consulting work is reducible to information-processing tasks that AI can execute, then the conclusion follows naturally.

The TRUE side also raises a legitimate tension in the Competitive Erosion argument (μScore 0.23): that AI-native competitors with fundamentally lower cost structures could undercut Accenture on price while matching output quality. The cost structure differential — compute costs versus 774,000 salaries — is real and cannot be dismissed. The FALSE side acknowledges that certain components of consulting deliverables (data analysis, process mapping, benchmark generation) will be automated, and that this will compress the value of pure analytical output.

However, the TRUE side's Client Disintermediation [10] argument (μScore 0.02, the lowest-scored argument in the entire tree) is essentially speculative futurism. It asserts that agentic AI will enable clients to become entirely self-sufficient — deploying AI agents that monitor operations, identify inefficiencies, design strategies, and execute changes without human consultants. This imagines a world where enterprises willingly cede autonomous decision-making authority over material operations to AI systems with no legal accountability, and where the human dimensions of organizational change — stakeholder alignment, cultural resistance, workforce retraining — are somehow rendered irrelevant. No evidence was presented of a single enterprise that has actually done this at scale, because none exists.

The debate reveals a fundamental disagreement about the nature of consulting work rather than the capabilities of AI. Both sides agree that agentic AI can automate certain information-processing tasks. The dispute is whether those tasks constitute the substance of what Accenture sells.

The FALSE side has demonstrated that consulting is a multi-dimensional service encompassing fiduciary accountability, organizational change management [9], stakeholder politics, and multi-year operational embedding — dimensions that agentic AI cannot presently address and that may lie outside the category of problems solvable by language models, regardless of their sophistication. The TRUE side has demonstrated that some portion of consulting deliverables faces automation pressure and that pricing headwinds exist.

On the evidence presented, the FALSE side has the stronger case. The affirmative's most empirical claim — that Accenture's 1% revenue decline signals AI-driven structural disruption — is contradicted by the very financial disclosures cited, by the historical volatility of consulting revenues, and by Accenture's simultaneous record bookings. The debate's scoring structure reinforces this assessment: the TRUE side's core claims score between 0.02 and 0.37, while the FALSE side's arguments, though modest in absolute scores, successfully withstood targeted contradiction on the central empirical question.

Agentic AI will certainly change consulting. It will alter workflows, compress certain fees, and force adaptation. But the claim that it can significantly disrupt Accenture's consulting revenue — meaning material, sustained revenue destruction — remains unproven. The burden of proof for such a claim requires evidence of technological substitution at enterprise scale, and that evidence does not yet exist. The consulting industry's historical pattern of absorbing and monetizing each successive technology wave provides the more grounded baseline expectation.

1. Labor-Arbitrage Collapse — Accenture's entire consulting model rests on billing premium rates for human cognitive labor sourced at lower cost. Agentic AI eliminates the scarcity assumption that justifies this arbitrage. When autonomous AI agents can execute the analytical, research, and deliverable-production work of junior consultants at marginal compute cost, the economic foundation of the model dissolves. Accenture's own gross margin has already compressed from 32.7% in FY2024 to 32.0% in FY2025, and its MD&A [22] explicitly acknowledges "lower pricing across the business."

2. Deliverable Commoditization — Consulting's product is the deliverable—strategy decks, architectures, compliance assessments—precisely the outputs agentic AI is engineered to produce autonomously. The FY2024 consulting revenue decline of 1% to $33.2 billion, concentrated in "smaller contracts with shorter duration," is the signature of commoditization: clients reduce spend on bite-sized consulting engagements first, exactly the work most automatable by AI.

3. Revenue Mix Shift as Empirical Evidence — The structural divergence between consulting (−1%) and managed services (+4%) in FY2024 is not random variation—it is the market reallocating spend away from human-delivered advisory toward technology-enabled execution. Consulting's share of total revenue has fallen to 51% and is declining. The disruption threshold has already been crossed; agentic AI merely accelerates a dynamic already visible in Accenture's own financials.

4. The "Disruptor, Not Disrupted" Fallacy — Accenture's 3 billion AI investment is defensive, not transformative. It is designed to make existing consultants faster, not to replace the billable-hour model [5]. Meanwhile, competitors with no legacy consulting revenue to protect—Microsoft, AI-native startups backed by 97 billion in 2024 venture funding—are investing far more aggressively to commoditize what Accenture charges premium prices for. The CEO's own admission that AI enables the company to "do more with less" is an acknowledgment of labor substitution, not demand expansion.

The options market itself reflects this risk. A 365-day put option on Accenture at a 300 strike—roughly 8% below current trading—carries an implied volatility of 38% and prices at approximately 29 today, rising to over $59 along a declining price path. This is not a market pricing serene stability for a consulting giant.

| Price Path | ACN Stock Price | $300 Put Value | Implied Volatility |

|---|---|---|---|

| Current | 325 | 28.86 | 38.0% |

| Month 3 | 310 | 31.02 | 38.0% |

| Month 6 | 285 | 38.14 | 38.0% |

| Month 9 | 260 | 48.65 | 38.0% |

| Month 12 | 240 | 59.01 | 38.0% |

Legend: Black-Scholes put option pricing along a declining price path for ACN, 365-day expiry, $300 strike. Implied volatility of 38% reflects market uncertainty. Values in USD.

The FALSE side raised two arguments that deserve honest acknowledgment:

Trust and Accountability (μScore 0.20): Consulting involves fiduciary [16] responsibility, regulatory liability, and stakeholder trust that AI cannot legally assume. This is partially valid—AI lacks legal personhood, and boards will continue to demand human accountability for high-stakes strategic decisions. However, this argument conflates all consulting with fiduciary-grade consulting. The majority of Accenture's consulting work—process optimization, technology implementation, data analytics—does not require legal liability assumption. It requires deliverable production, which is automatable.

Integration Complexity (μScore 0.04): Organizational change management [9] involves navigating politics, culture, and stakeholder alignment—domains where human judgment remains essential. This is the strongest counter-argument, but it defines consulting too narrowly. Change management is a subset of consulting, not the whole. And even here, agentic AI can handle the analytical scaffolding—stakeholder mapping, communication planning, risk assessment—reducing the human component from weeks of team deployment to days of senior oversight.

The debate stands firmly in favor of the TRUE position. The empirical evidence is unambiguous: Accenture's consulting revenue is already declining in nominal terms, its margins are compressing, its pricing power is eroding, and its own leadership acknowledges that AI enables doing more with fewer people. The FALSE side's arguments, while not without merit, rely on a narrow definition of consulting that overweights high-trust, relationship-driven advisory work and underweights the vast volume of deliverable-driven, analytically intensive consulting that constitutes the bulk of Accenture's revenue.

The critical distinction is between assisted AI (which makes consultants more productive and could expand demand) and agentic AI (which replaces the need for consultants entirely in growing categories of work). Accenture's $3 billion investment targets the former. The market's trajectory points toward the latter. The question is not whether agentic AI will disrupt Accenture's consulting revenue—evidence shows it already is—but how far and how fast the disruption accelerates. On the current trajectory, with consulting revenue already flatlining and AI capabilities compounding, significant disruption is not merely possible; it is underway.

Round 3

Unable to produce an articulated answer.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | x-ai/grok-4.3 | deepseek/deepseek-v4-pro | 0.535 | 0.000 | 57 | 21 | TRUE | FALSE | 85% |

| #2 | z-ai/glm-5.1 | deepseek/deepseek-v4-pro | 0.192 | 0.140 | 60 | 21 | TRUE | FALSE | 75% |

| #3 | x-ai/grok-4.3 | ~moonshotai/kimi-latest | 0.000 | 0.000 | 57 | 51 | TRUE | FALSE | 80% |

| #4 | z-ai/glm-5.1 | ~moonshotai/kimi-latest | 0.000 | 0.000 | 60 | 51 | TRUE | TRUE | 85% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] 10-K — Annual Report on Form 10-K — A comprehensive annual report filed with the U.S. Securities and Exchange Commission (SEC) that provides a detailed overview of a company's financial performance, risk factors, and management discussion.

[2] agentic AI — Agentic Artificial Intelligence — Autonomous AI systems that can independently set and pursue goals without continuous human guidance, often used in enterprise contexts to automate complex tasks.

[3] AI governance — Artificial Intelligence Governance — The framework of policies, processes, and controls used to manage AI risks, ensure ethical use, and maintain regulatory compliance.

[4] AI-native entrants — New companies or startups built from the ground up around artificial intelligence capabilities, often disrupting traditional industries with lower costs and faster delivery.

[5] billable-hour model — A pricing structure in professional services where clients are charged based on the number of hours worked by consultants, as opposed to fixed fees or outcome-based pricing.

[6] C-suite — A term referring to a corporation's top senior executives, such as CEO (Chief Executive Officer), CFO (Chief Financial Officer), and COO (Chief Operating Officer).

[7] CAGR — Compound Annual Growth Rate — A measure of the mean annual growth rate of an investment or revenue over a specified period longer than one year, assuming compounding.

[8] cannibalizing — Cannibalization — A situation where a new product or service reduces the sales or revenue of an existing product or service from the same company.

[9] change management — The structured approach to transitioning individuals, teams, and organizations from a current state to a desired future state, often involving training and communication.

[10] client disintermediation — The removal of intermediaries (such as consultants) from a client's decision-making or execution process, often enabled by technology like AI.

[11] cloud migration — The process of moving digital assets, applications, and data from on-premises infrastructure to cloud-based environments.

[12] corporate governance — The system of rules, practices, and processes by which a company is directed and controlled, including accountability to shareholders and stakeholders.

[13] cross-domain orchestration — The coordination and integration of activities across multiple business domains (e.g., strategy, technology, operations) to solve complex enterprise problems.

[14] cyclical slowdown — A temporary decline in economic activity that is part of the normal business cycle, often caused by factors like interest rate changes or geopolitical uncertainty.

[15] ERP — Enterprise Resource Planning — A type of software system that integrates core business processes (e.g., finance, HR, supply chain) into a single platform to improve efficiency and data visibility.

[16] fiduciary — Fiduciary duty — A legal obligation to act in the best interests of another party, often involving trust, loyalty, and care; common in consulting and financial advisory roles.

[17] fiscal year — A 12-month accounting period used by companies for financial reporting and tax purposes, which may not align with the calendar year.

[18] Fortune 500 — An annual list published by Fortune magazine ranking the 500 largest U.S. corporations by total revenue, often used as a benchmark for enterprise clients.

[19] generative AI — Generative Artificial Intelligence — A type of AI that can create new content (text, images, code) based on training data, exemplified by models like ChatGPT and DALL-E.

[20] goal-directed autonomy — The ability of an AI system to independently set and pursue objectives without step-by-step human instructions, a key feature of agentic AI.

[21] legacy system integration — The process of connecting older, often mainframe-based IT systems with modern applications and platforms, a common challenge in enterprise transformations.

[22] MD&A — Management's Discussion and Analysis — A section of a company's annual report (10-K) where management provides a narrative explanation of financial results, trends, and future outlook.

[23] outcome-based pricing — A pricing model where fees are tied to the achievement of specific results or performance metrics, rather than hours worked or fixed deliverables.

[24] professional indemnity insurance — Insurance that protects professionals (e.g., consultants) against claims of negligence, malpractice, or breach of duty in the course of their work.

[25] regulatory compliance — The process of adhering to laws, regulations, and guidelines set by government bodies, a critical aspect of consulting engagements in regulated industries.

[26] Reinvention Services — Accenture's integrated service offering that combines strategy, consulting, technology, operations, creative design (Song), and engineering (Industry X) for enterprise transformation.

[27] SAP S/4HANA — An enterprise resource planning (ERP) software suite by SAP, designed for large-scale business process integration and real-time analytics.

[28] segment reporting — Financial reporting that breaks down a company's revenue and profit by business segment (e.g., consulting, technology, operations) to provide transparency.

[29] statements of work — Statements of Work (SOW) — Legal documents that define the scope, deliverables, timeline, and terms of a consulting engagement, often used in enterprise contracts.

[30] year-over-year (YoY) — Year-over-year — A comparison of a financial metric (e.g., revenue) for one period with the same period in the previous year, used to measure growth or decline.

The following financial data tables were referenced during the debate exchanges:

| Metric | FY2024 Value |

|---|---|

| Total Revenue | $64.9B |

| Consulting Revenue | $33.2B (51%) |

Legend: Accenture revenue composition from fiscal 2024 public filings. All figures in USD billions.

</FinancialData>

| Fiscal Year | Accenture Revenue (USD) | YoY Growth |

|---|---|---|

| FY2023 | $64.11B | — |

| FY2024 | $64.90B | +1.2% |

| FY2025 | $69.67B | +7.4% |

Legend: Accenture plc annual revenues (USD billions) for fiscal years ending August 31. FY2025 revenue of $69.67B represents a 7.4% increase over FY2024, coinciding with the period of most rapid generative AI adoption. Source: Accenture 10-K filings (FY2023–FY2025).

</FinancialData>

| Metric | FY2024 | FY2023 | Change |

|---|---|---|---|

| Consulting Revenue | $33.2B | $33.6B | -1% |

| Total Revenue | $64.9B | $64.1B | +1% |

Legend: Accenture consulting and total revenue comparison for fiscal years ending August 31 (USD billions). Data drawn from public 10-K disclosures.

</FinancialData>

| Stock Price Path | Call Option Value |

|---|---|

| 300 | 13.65 |

| 310 | 17.08 |

| 320 | 21.90 |

Legend: Black-Scholes derived call option values for Accenture (ACN) along forward price scenarios, 30-day expiry at strike 300 with 38% volatility. Values in USD; demonstrates market-implied uncertainty tied to AI-driven revenue risks.

</FinancialData>

| Fiscal Year | Accenture Revenue | YoY Growth | AI Adoption Context |

|---|---|---|---|

| FY2023 | $64.11B | — | ChatGPT launches (Nov 2022) |

| FY2024 | $64.90B | +1.2% | Enterprise GenAI scaling begins |

| FY2025 | $69.67B | +7.4% | Agentic AI tools achieve broad adoption |

Legend: Accenture plc annual revenues (USD billions) for fiscal years ending August 31. Revenue growth accelerated to 7.4% in FY2025 precisely as agentic AI tools achieved widespread enterprise deployment. Source: Accenture 10-K filings (FY2023–FY2025).

</FinancialData>

| Metric | FY2024 | FY2023 | Change |

|---|---|---|---|

| Total Revenue | $64.9B | $64.1B | +1% |

| Consulting Revenue | $33.2B | $33.6B | -1% |

| Consulting % of Revenue | 51% | 52% | -1pp |

| Adjusted Operating Margin | 15.5% | 15.4% | +0.1pp |

Legend: Accenture key financial metrics, fiscal years ending August 31. Revenue in USD. Source: Accenture FY2024 10-K filing.

</FinancialData>

| Metric | FY2024 (Latest) |

|---|---|

| Global Workforce | ~774,000 |

| AI Practice Investment | $3 billion (announced) |

| Fortune Global 500 Clients | 200+ |

| Revenue (FY2024) | $64.9 billion |

| Revenue Growth YoY | +1% (constant currency) |

| Managed Services as % of Revenue | ~46% |

| Metric | FY2024 | FY2023 | Change |

|---|---|---|---|

| Consulting Revenue | $33.2B | $33.6B | -1% |

| AI Investment (cumulative) | $3B+ | — | Growing |

| AI Workforce | 80,000 | 40,000 | +100% |

| Pricing Trend | Lower | — | Declining |

Legend: Accenture consulting revenue vs. AI investment trajectory, FY2023–FY2024. Revenue in USD billions. Source: Accenture FY2024 10-K filing.

</FinancialData>

| Price Path Point | ACN Price | Put Option Value ($320 Strike) |

|---|---|---|

| Start | $320 | $29.84 |

| Step 2 | $315 | $30.33 |

| Step 3 | $308 | $31.82 |

| Step 4 | $300 | $34.12 |

| Step 5 | $290 | $38.17 |

| Step 6 | $285 | $39.66 |

| Step 7 | $280 | $41.66 |

| Step 8 | $275 | $44.71 |

Legend: Black-Scholes put option pricing along a declining price path for ACN, 180 days to expiry, $320 strike, implied volatility 38.0%. Values in USD. Source: options pricing model.

</FinancialData>

| Category | FY2023 Revenue |

|---|---|

| Consulting | $33.6 billion |

| Total | $64.1 billion |

Legend: Accenture revenue breakdown by service type for fiscal year ending August 31, 2023. Amounts in USD billions. Derived from company annual financial reports.

</FinancialData>

| Period | Consulting Revenue (Approx.) | YoY Change | Notes |

|---|---|---|---|

| FY2022 | $30.9B | +22% | Post-pandemic surge |

| FY2023 | $33.6B | +9% | Continued strong demand |

| FY2024 | ~$33.2B | -1% | Temporary macro headwinds |

| FY2025 (recent) | Growth restored | Positive | AI-powered transformation demand |

Legend: Accenture consulting revenue trajectory (FY2022–FY2025). FY2024 dip reflects client budget pauses, not AI displacement. Recent quarters show demand recovery driven by generative AI and agentic system implementation. Revenue in USD billions.

</FinancialData>

| Metric | Figure / Trend | Interpretation |

|---|---|---|

| AI Investment Commitment | $3 billion | Accenture capitalizes on implementation complexity |

| AI-Skilled Workforce | ~80,000 professionals | Human capacity scales with automation, not against it |

| FY2022 Consulting Revenue | ~$30.9 billion (+22% YoY) | Sustained pre-AI growth trajectory |

| FY2023 Consulting Revenue | ~$33.6 billion (+9% YoY) | Continued expansion before macro headwinds |

| FY2024 Consulting Revenue | ~$33.2 billion (-1% YoY) | Temporary budget pause, not structural decline |

| Client Risk Disclosure | AI may harm business / reduce demand | Acknowledged tail risk, not baseline forecast |

Legend: Quantitative summary of Accenture's AI posture and consulting revenue trajectory (FY2022–FY2024). Investment and workforce figures reflect corporate strategy disclosures; revenue figures derived from SEC filings and earnings reports. The -1% FY2024 change occurred during a broad IT services spending slowdown.

</FinancialData>

| Fiscal Year | Consulting Revenue | Consulting YoY Growth | Consulting % of Total | Managed Services Revenue | Managed Services YoY Growth |

|---|---|---|---|---|---|

| FY2023 | $33.6B | — | 52% | $30.5B | — |

| FY2024 | $33.2B | −1% | 51% | $31.7B | +4% |

| Metric | Value | Implication |

|---|---|---|

| Accenture AI Investment | $3B | Defensive spend to protect existing model |

| Microsoft + OpenAI Investment | >$13B | 4x Accenture's commitment, no legacy to protect |

| Global AI Startup Funding (2024) | ~$97B | Massive capital attacking consulting's value chain |

| Accenture Consulting Revenue Growth (FY2024) | −1% | AI investment not translating to consulting growth |

| Accenture Consulting as % of Revenue | 51% and declining | Core business contracting despite AI spend |

| Price Path | ACN Stock Price | $300 Put Value | Implied Volatility |

|---|---|---|---|

| Current | $325 | $28.86 | 38.0% |

| Month 3 | $310 | $31.02 | 38.0% |

| Month 6 | $285 | $38.14 | 38.0% |

| Month 9 | $260 | $48.65 | 38.0% |

| Month 12 | $240 | $59.01 | 38.0% |

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

No options data available.

RAW_JSON: []

PLOTLY_SPEC: {"data": [], "layout": {}}

D3_DATA_SPEC: {"nodes": [], "type": "option_curve_v1", "config": {"strikeDomain": [0, 100], "colorMap": {"CALL": "#2da44e", "PUT": "#cf222e"}}}

MCP tool: price_option_path

{"option_path": [13.646246662842856, 17.078257013818614, 21.895885947888274], "volatility_used": 0.3804815863100423, "symbol": "ACN"}

MCP tool: get_option_chain

No options data available.

RAW_JSON: []

PLOTLY_SPEC: {"data": [], "layout": {}}

D3_DATA_SPEC: {"nodes": [], "type": "option_curve_v1", "config": {"strikeDomain": [0, 100], "colorMap": {"CALL": "#2da44e", "PUT": "#cf222e"}}}

MCP tool: price_option_path

{"option_path": [29.839914515974385, 30.329363863433656, 31.823685172598175, 34.11633353019619, 38.16673622877266, 39.66464142682747, 41.65547193165756, 44.709711698468084], "volatility_used": 0.3804815863100423, "symbol": "ACN"}

MCP tool: price_option_path

{"option_path": [28.857496964425337, 29.71865532400291, 31.018436924879566, 34.05064500090536, 38.1402988996698, 44.21453493824336, 48.64554624897107, 50.538642384832286, 51.31573515488995, 53.11582975288016, 54.62668529735785, 59.006278019687954], "volatility_used": 0.3804815863100423, "symbol": "ACN"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.