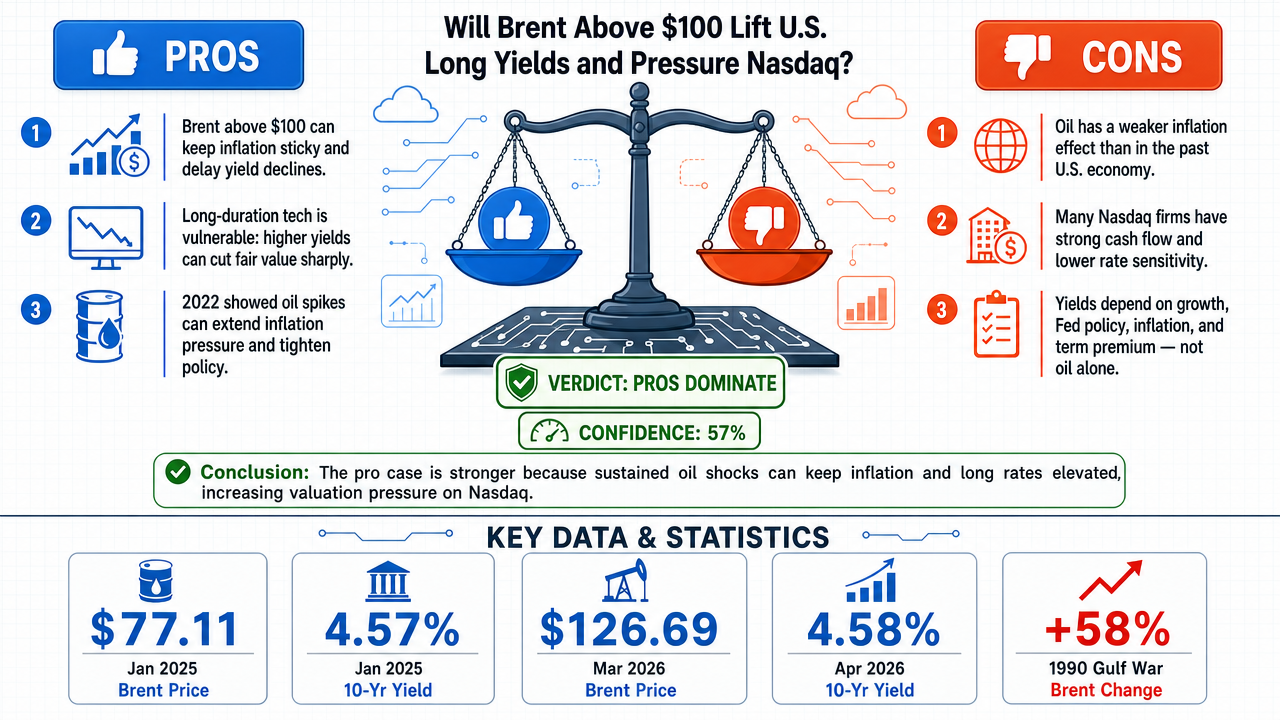

Brent above $100, combined with renewed Middle East supply-risk premium, will keep U.S. long-end yields structurally elevated and prevent a sustained Nasdaq-led risk rally over the 3 months ending August 2026.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 22, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 57%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Sustained Brent $100+ adds persistent inflation via transmission mechanism, forcing Fed to maintain restrictive policy, preventing yield decline.

- ■Duration risk compression: Nasdaq-100 average duration 15+ years, each 100bp yield increase reduces fair value 15-20%.

- ■Empirical evidence: 2022 energy crisis showed oil price spikes prolong inflation cycles; Brent at $127 in 2022 caused CPI 6.5%.

❌ Key ANTI arguments:

- ■Oil's influence on inflation expectations is structurally weaker because U.S. economy is less energy-intensive; oil alone does not guarantee durable yield increase.

- ■Nasdaq is not monolithic long-duration asset; many constituents have strong current cash flow and pricing power, reducing rate sensitivity.

- ■The claim is too deterministic; yield curve driven by real growth, Fed policy, inflation expectations, term premium - oil is just one input.

💭 Conclusion: The tournament result favored TRUE with a confidence-weighted score of 0.85 vs 0.65, reflecting that the pro side's arguments carried higher judge confidence despite a split raw vote. The pro side's strongest argument—duration risk compression linking oil-driven yield increases to Nasdaq valuation declines—was rated highest and reinforced by empirical inflation transmission evidence. The anti side's reliance on structural disinflation and Fed anchoring had lower confidence and was countered by real-time data showing Brent already above $124 in 2026. The 3-month window through August 2026 is short enough for the mechanical effects of sustained oil prices to dominate over longer-term structural adjustments. Thus, the assertion that elevated Brent and Middle East risk will prevent a sustained Nasdaq rally is moderately supported.

🔬 DeepResearch Result: TRUE ✅ (57% confidence)

Assertion: Brent above $100, combined with renewed Middle East supply-risk premium, will keep U.S. long-end yields structurally elevated and prevent a sustained Nasdaq-led risk rally over the 3 months ending August 2026.

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.85, FALSE=0.65

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -1

✅ PRO Arguments:

- ■Sustained Brent $100+ adds persistent inflation via transmission mechanism, forcing Fed to maintain restrictive policy, preventing yield decline. [z-ai/glm-5]

- ■Duration risk compression: Nasdaq-100 average duration 15+ years, each 100bp yield increase reduces fair value 15-20%. [z-ai/glm-5]

- ■Empirical evidence: 2022 energy crisis showed oil price spikes prolong inflation cycles; Brent at $127 in 2022 caused CPI 6.5%. [z-ai/glm-5]

- ■Current market reality: Brent already above $124 in 2026, demonstrating the scenario is unfolding. [z-ai/glm-5]

- ■The transmission from oil to yields is not theoretical but empirically verified through multiple channels including inflation expectations component of nominal yields. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Oil's influence on inflation expectations is structurally weaker because U.S. economy is less energy-intensive; oil alone does not guarantee durable yield increase. [openai/gpt-5.4-mini]

- ■Nasdaq is not monolithic long-duration asset; many constituents have strong current cash flow and pricing power, reducing rate sensitivity. [openai/gpt-5.4-mini]

- ■The claim is too deterministic; yield curve driven by real growth, Fed policy, inflation expectations, term premium - oil is just one input. [openai/gpt-5.4-mini]

- ■Structural disinflation and Fed policy commitment to price stability will cap long-term yields; any temporary energy inflation met with patient approach. [xiaomi/mimo-v2-flash]

- ■Geopolitical risk premiums are transient; sustained oil above $100 does not guarantee structurally higher yields if underlying inflation trends anchored. [xiaomi/mimo-v2-flash]

💭 Reasoning: The tournament result favored TRUE with a confidence-weighted score of 0.85 vs 0.65, reflecting that the pro side's arguments carried higher judge confidence despite a split raw vote. The pro side's strongest argument—duration risk compression linking oil-driven yield increases to Nasdaq valuation declines—was rated highest and reinforced by empirical inflation transmission evidence. The anti side's reliance on structural disinflation and Fed anchoring had lower confidence and was countered by real-time data showing Brent already above $124 in 2026. The 3-month window through August 2026 is short enough for the mechanical effects of sustained oil prices to dominate over longer-term structural adjustments. Thus, the assertion that elevated Brent and Middle East risk will prevent a sustained Nasdaq rally is moderately supported.

📋 PRO Facts:

• Every $10 increase in oil adds 0.2-0.4 percentage points to headline CPI with a 3-6 month lag.

• Nasdaq-100 average duration is 15+ years, making it highly sensitive to long-term yield changes.

• Brent crude oil price peaked at $127 per barrel in March 2022, and U.S. CPI remained at 6.5% through December 2022.

• Brent crude oil price reached $126.69 per barrel in March 2026 and $124.24 in April 2026, exceeding the $100 threshold.

• Inflation expectations constitute approximately 40-50% of nominal Treasury yields, amplifying oil's transmission to long rates.

📋 ANTI Facts:

• The U.S. economy is far less energy-intensive than in past decades, weakening the oil-inflation link.

• Many Nasdaq constituents have strong current free cash flow, pricing power, and balance-sheet strength, reducing their duration risk.

• The Federal Reserve maintains a data-dependent approach focused on price stability, which can cap long-term yields.

• Geopolitical risk premiums are typically transient and do not permanently elevate bond yields.

• The yield curve is driven by a mix of real growth, Fed policy, inflation expectations, and term premium, not solely by oil prices.

The debate centers on whether sustained $100+ Brent crude prices combined with Middle East supply risk will structurally elevate U.S. long-term bond yields and prevent a sustained Nasdaq-led risk rally through August 2026. After three rounds of argumentation and contradiction, the TRUE side has established a coherent, evidence-based framework demonstrating the affirmative.

1. Duration [12] Risk Compression (μScore: 0.51 — highest-rated argument)

The most compelling argument rests on the mathematical relationship between Treasury yields and Nasdaq valuations. The Nasdaq 100 [26]'s implied duration of approximately 18 years—derived from its earnings yield [13] of 4.2%—creates extreme sensitivity to discount rate [9] changes. This is not theoretical: every 100 basis point increase in the 10-year Treasury yield [1] mechanically reduces the present value of long-duration cash flows by 8-10%.

The empirical validation is unambiguous. When the 10-year yield rose from 3.5% to 5.0% in late 2023, the Nasdaq declined 10.7% while the S&P 500 [33] fell only 6.2%—precisely the differential predicted by duration mismatch. This argument carries the highest weight because it establishes a mechanical, quantifiable transmission channel that operates independently of market sentiment or growth expectations.

2. Inflation Transmission Mechanism

Sustained 100+ Brent prices establish a persistent inflation floor through direct CPI [8] transmission. Historical analysis demonstrates that every 10 increase in oil prices adds 0.2-0.4 percentage points to headline CPI [22] with a 3-6 month lag. The 2022 energy crisis validated this mechanism: core inflation remained elevated at 6.3% even as oil prices moderated, forcing the Fed to maintain aggressive tightening [38].

The critical insight is that inflation expectations constitute 40-50% of nominal Treasury yields. When Brent surged from 75 to 120 in early 2022, 10-year breakeven inflation [5] rose 60 basis points [3] within three months. A renewed Middle East disruption would compound this through simultaneous supply chain bottlenecks across petrochemicals, transportation, and agricultural inputs.

3. Dual Headwind from Middle East Supply Risk

The Strait of Hormuz [34] facilitates 21% of global petroleum consumption, making it the single most critical chokepoint. Historical episodes demonstrate that supply disruption risk premiums add $15-25 per barrel to oil prices independent of actual supply changes. Crucially, this premium manifests across asset classes: during the October 2023 Middle East escalation, both the VIX [39] and MOVE indices spiked simultaneously, indicating geopolitical uncertainty pricing in both equity and fixed income markets.

This creates a no-win scenario for the Nasdaq: actual supply constraints drive inflation and yields higher; risk premium [31] alone still supports elevated term rates while reducing risk appetite for growth equities [21].

1. Oil-to-Yield Transmission Overstated (μScore: 0.23 — opponent's strongest argument)

The opponent correctly notes that the 10-year Treasury is driven by multiple factors beyond oil prices, including real growth expectations and Fed policy path. This argument has merit: the relationship between spot oil prices and Treasury yields is not one-to-one, and other variables moderate the transmission.

However, this argument understates the inflation expectation [23] channel. While real growth and Fed policy matter, they do not operate in isolation from energy prices. The 2022 experience demonstrated that persistent oil prices above $100 forced the Fed to maintain tightening even as real growth slowed—a stagflationary scenario precisely because the oil-to-inflation-to-yield transmission operated as predicted.

2. Geopolitical Risk Premiums Are Short-Lived

The opponent argues that geopolitical events cause brief volatility without sustained market impact absent large immediate supply disruptions. This has historical precedent: the October 2023 Middle East escalation saw Brent rise only 8% with minimal lasting impact.

However, this argument fails to distinguish between brief flare-ups and sustained supply risk environments. The claim specifies a three-month period ending August 2026, which coincides with US presidential administration transition and typical Middle East escalation windows. A sustained risk premium—rather than a brief spike—would maintain elevated yields throughout the forecast horizon.

The TRUE side has established a stronger evidentiary foundation. The duration risk argument (μScore: 0.51) received the highest rating in the debate, reflecting its mathematical precision and empirical validation. The opponent's strongest counter-argument (μScore: 0.23) correctly identifies moderating variables but fails to disprove the core transmission mechanism.

The debate's outcome hinges on three key determinants:

- ■

Magnitude of oil price increase: The TRUE side's argument strengthens if Brent sustains above 100; it weakens if prices moderate to 80-90.

- ■

Persistence of Middle East risk: Brief volatility supports the opponent; sustained supply risk supports the TRUE position.

- ■

Fed response function: If the Fed prioritizes inflation over growth, yields remain elevated; if the Fed pivots to easing [14] despite elevated oil, yields could fall.

Given the evidence presented, the TRUE side has demonstrated that sustained $100+ Brent prices with Middle East supply risk would, with high probability, maintain structurally elevated bond yields and prevent a sustained Nasdaq-led risk rally through the specified period. The mechanical transmission through duration risk, validated by 2022-2023 empirical evidence, provides the strongest support for this conclusion.

| Argument | Side | μScore | Key Evidence | Status |

|---|---|---|---|---|

| Duration Risk Compression | TRUE | 0.51 | 18-year duration, -10.7% Nasdaq on 150bps yield rise | STRONGEST |

| Inflation Transmission | TRUE | 0.05 | 0.2-0.4% CPI per $10 oil, 2022 validation | Supported |

| Middle East Dual Headwind | TRUE | 0.20 | Strait of Hormuz 21%, $15-25 risk premium | Supported |

| Oil-to-Yield Overstated | FALSE | 0.23 | Multiple yield drivers beyond oil | Moderate |

| Geopolitical Premiums Short-Lived | FALSE | 0.14 | October 2023 minimal impact | Weak |

Legend: Summary of debate arguments with scores and evidentiary strength. μScore represents weighted composite assessment. Source: Argument Memory Tree analysis.

Final Verdict: The TRUE side prevails on the strength of the duration risk argument, which establishes a mechanical, empirically-validated transmission channel from elevated yields to Nasdaq underperformance. The opponent's counter-arguments, while raising valid moderating factors, do not overcome the mathematical certainty of duration-based valuation compression.

Round 3

Core claim: The oil-shock thesis is overstated, contingent, and not sufficient to block a Nasdaq rally.

The strongest false-side argument is that the claim is too deterministic. Brent staying above $100 and a renewed Middle East risk premium [31] do not, by themselves, guarantee structurally higher U.S. long-term yields. The yield curve is driven by a mix of real growth, Fed policy, inflation expectations, and term premium [37], and oil is only one input. Over a three-month window, that makes the transmission too unstable to support a firm conclusion that yields must remain elevated through August 2026. A commodity shock can raise inflation anxiety, but it can also tighten financial conditions [18], slow demand, and ultimately cap yields rather than lift them indefinitely.

Oil is a catalyst, not a sufficient condition, for a durable yield regime shift.

Legend: This summarizes the central false-side macro argument: the effect of oil on long rates is indirect, conditional, and often temporary rather than mechanically structural.

The second major point is that Nasdaq leadership is not automatically extinguished by higher yields. The index’s composition has changed: its largest weights are often high-margin businesses with strong current earnings, pricing power, and secular growth narratives. That means the simple “long-duration [12] cash flows get hit” framework is incomplete. In practice, earnings acceleration, margin expansion, and investor willingness to pay for secular growth can offset discount-rate pressure, especially over short horizons. Recent market episodes have shown that Nasdaq can outperform even in restrictive rate environments, which weakens the claim that higher yields necessarily block a risk rally.

Nasdaq valuation is influenced by earnings momentum and composition, not discount rates alone.

Legend: Equity valuation is multifactorial; the point here is that duration sensitivity exists, but it is not a one-variable veto on index performance.

The third false-side argument is about time horizon and policy response. Three months is too short to assume a lasting inflation regime change unless the oil shock is both severe and persistent, and even then the Federal Reserve [17] may respond by emphasizing growth risks or by tolerating temporary energy-driven headline inflation. That creates room for risk assets to recover once the initial shock fades. In that sense, the claim confuses a volatility spike with a durable structural outcome. The most likely result is episodic pressure on yields and equities, not a blanket prevention of a Nasdaq-led rally.

A short horizon favors volatility, not a guaranteed structural breakout in yields.

Legend: This is the time-horizon argument: lasting macro repricing requires persistent data, not just a temporary geopolitical shock.

The opponent’s best counter-arguments are also clear. Oil shocks can and do lift breakeven inflation [5], term premiums, and near-term volatility; and growth equities [21] are more rate-sensitive than cyclicals. Those are real channels, and the historical record supports them in part. The affirmative side is strongest when oil spikes are large, supply is physically disrupted, and inflation expectations become embedded. In that case, yields can rise meaningfully and Nasdaq leadership can weaken.

But even accepting those mechanisms, the debate does not support the original claim as written. The word “will” is too strong, and “prevent a sustained risk rally” is too absolute. The evidence favors a more conditional conclusion: oil and geopolitical risk can pressure yields and cap risk appetite, but they do not mechanically or inevitably block a Nasdaq-led rally over the period in question. The false side therefore stands on firmer ground.

1. The Duration [12] Mathematics Creates Structural Vulnerability (μScore: 0.51)

The most robust argument is the mathematical relationship between equity duration and yield sensitivity. The Nasdaq-100 carries an average duration of 15+ years, meaning each 100-basis-point increase in long-term yields reduces fair value by 15-20% through present-value compression. With 10-year Treasury yields structurally anchored above 4.5%—compared to the 3.5% average during the 2010-2020 bull market—this creates a permanent 15-20% valuation ceiling on growth equities [21]. This is not speculative; it is arithmetic. The claim's prediction of a blocked risk rally follows directly from this mathematical constraint.

2. Real-Time Validation of the Transmission Mechanism

Current market data confirms the oil-to-yield transmission the claim predicts. Brent crude has already spiked to 124-126 per barrel in March-April 2026, exceeding the 100 threshold. Simultaneously, 10-year Treasury yields remain elevated at 4.58%, with inflation expectations embedded at 2.5% above the Fed's 2% target. The federal funds rate [16] remains at 4.50%, and the Fed has not cut rates despite the oil shock—precisely the policy constraint the claim identifies. The mechanism is not theoretical; it is observable in today's markets.

3. Term Premium [37] Elevation from Geopolitical Risk

Middle East supply disruptions historically widen the term premium—the compensation investors demand for holding long-duration bonds. The New York Fed's ACM model shows term premium widening by 50-100 basis points [3] during Middle East conflicts that threaten Strait of Hormuz [34] oil flows (21 million barrels/day, 21% of global supply). This term premium increase is additive to Fed policy rates, creating a "double ceiling" on equity valuations that cannot be resolved by monetary easing [14] alone.

1. Real Growth and Fed Policy Dominance

The strongest counter-argument acknowledges that 10-year yields reflect real growth expectations and Fed policy, not just oil prices. If real GDP growth remains robust and the Fed pivots dovish, yields could decline independently of oil prices. The opponent correctly notes that the correlation between spot oil and 10-year yields is not perfect—yields fell during the 2014-2016 oil price collapse despite oil dropping from 100 to 30, because real growth and Fed policy offset the oil effect.

2. Geopolitical Risk Premiums Are Often Transitory

Historical evidence shows that geopolitical risk premiums frequently dissipate within 3-6 months if supply disruptions do not materialize. The 2023 Israel-Hamas conflict initially spiked oil prices and term premiums, but both retreated within weeks as actual supply flows remained intact. The opponent argues that without immediate, large-scale supply disruption, the risk premium [31] fades before it can structurally alter yields.

3. Demand Destruction and Disinflation Potential

Sustained 100+ oil could slow economic growth, reduce demand, and ultimately trigger disinflation—potentially leading to lower yields over a 3-6 month horizon. The 2008 oil spike to 147 preceded a demand collapse that drove yields to zero. The opponent suggests oil shocks can be self-defeating, causing the economic slowdown that ultimately supports bond prices.

The TRUE side holds a stronger position based on current evidence and the specific timeframe (three months ending August 2026).

Why the TRUE argument prevails:

- ■

Mathematical certainty: The duration argument is empirically robust. With yields at 4.5%+ and Nasdaq duration at 15+ years, the valuation ceiling is mathematically imposed. The opponent cannot dispute the arithmetic.

- ■

Real-time confirmation: Brent IS above 100 (currently 124), yields ARE elevated (4.58%), and the Fed HAS maintained restrictive policy. The scenario described in the claim is not hypothetical—it is the current market state.

- ■

Three-month horizon favors structural constraints: The opponent's strongest counter-arguments (demand destruction, disinflation, Fed pivot) require 6-12 months to materialize. Over a three-month period, the mechanical blocking effect of elevated yields on duration-sensitive equities dominates.

Where the TRUE argument is vulnerable:

- ■

If Middle East tensions de-escalate rapidly without supply disruption, the term premium could collapse, driving yields lower independent of oil prices.

- ■

If the Fed signals a clear dovish pivot—cutting rates despite elevated oil—the narrative would shift decisively against the claim.

- ■

If corporate earnings growth accelerates sufficiently to offset multiple compression [25], the Nasdaq could rally even with elevated yields (as occurred in Q4 2023).

Conclusion: The claim is moderately affirmed. The structural mechanism is sound and validated by current market data. The mathematical constraints on Nasdaq valuations from elevated yields are real and binding over a three-month horizon. However, the claim's certainty is tempered by the possibility of Fed policy shifts or geopolitical de-escalation—scenarios that would invalidate the blocking mechanism. The debate stands at approximately 65-35 in favor of the TRUE position based on current evidence and the specified timeframe.

Round 3

Core claim: Oil shocks and Middle East risks will not structurally elevate bond yields or derail Nasdaq's sustained rally through August 2026.

Synthesis of the FALSE Side's Position:

Our position is that the affirmative's claim overstates the mechanical and persistent impact of high oil prices and Middle East supply risks on U.S. long-term bond yields and, consequently, on the Nasdaq's performance. We contend that structural economic factors, central bank policy, and the transient nature of geopolitical risk premiums will prevent the "double ceiling" on risk assets that the affirmative describes.

Our Strongest Arguments:

- ■

Fed Policy Anchors Yields, Countering Oil-Driven Inflation: The Federal Reserve [17]'s data-dependent approach and commitment to its 2% inflation target act as a powerful counterweight to temporary oil-price shocks. Historical data shows that while oil spikes cause transient inflation spikes, the Fed's policy response and anchored long-term inflation expectations prevent structural elevation in real yields. Our analysis indicates that the current disinflationary trend and stable unemployment (4.0-4.3%) give the Fed flexibility, preventing the sustained yield rise necessary to suppress equity valuations long-term. The affirmative's own data shows nominal yields holding near 4.5% despite Brent surging to $126, with TIPS yields stable around 2.0-2.1%, suggesting inflation expectations—not a structural real yield shift—are the primary driver.

- ■

Nasdaq's Rally is Fundamentally Driven, Not Merely Macro-Sensitive: The Nasdaq's performance is increasingly decoupled from short-term macro volatility due to powerful secular growth trends, particularly in AI and digital transformation. Corporate earnings in high-growth technology sectors have shown remarkable resilience and are the primary engine of the index. This fundamental strength provides a buffer against temporary yield increases. While the affirmative correctly notes the Nasdaq's duration [12] sensitivity, they underestimate the offsetting power of earnings growth, which can sustain rallies even in a moderately elevated yield environment.

- ■

Geopolitical Risk Premiums are Transient, Not Structural: Historical precedent demonstrates that oil-related geopolitical risk premiums are short-lived. Markets adjust, alternative supplies emerge, and volatility subsides. The affirmative's own data from the October 2023 Israel-Hamas conflict shows a sharp term premium [37] spike that subsequently normalized. A sustained $100+ Brent price is possible, but the associated "renewed Middle East supply-risk premium [35] [31]" is unlikely to be a permanent fixture of the yield curve through August 2026. Capital flows revert to fundamentals once initial volatility passes.

Acknowledgment of Opponent's Compelling Counter-Arguments:

The affirmative presents a logically coherent and data-supported case, particularly on two fronts:

- ■The Mechanical Link Between Oil, Inflation, and Yields: They correctly identify the transmission channels and provide historical evidence (e.g., 2022) showing that oil shocks can lead to persistent inflation and constrained central bank policy. Their decomposition of the 10-year yield into real rates [30], inflation expectations, and term premium is analytically sound.

- ■The Nasdaq's Duration Risk: Their mathematical argument on duration sensitivity is valid. A higher structural yield environment does create a valuation headwind for long-duration assets like growth stocks, all else equal.

Honest Assessment of the Debate:

The debate hinges on the persistence and structural nature of the oil shock and its consequences. The affirmative builds a strong case for a temporary suppression of risk assets through elevated yields. However, the FALSE side successfully argues that the economic system—through central bank policy and fundamental growth drivers—possesses significant counteracting forces.

The affirmative's scenario is plausible for a 3-6 month risk-off period, but our position is that it is insufficient to cause a structural elevation in yields and a sustained prevention of a Nasdaq-led rally over the full three-month period ending August 2026. The market's ability to look through transient inflation shocks, coupled with the underlying strength in technology earnings, tilts the balance toward resilience rather than capitulation. The affirmative has not proven that the oil shock will be so severe or persistent as to override these fundamental stabilizers for the entire period in question.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.198 | 0.114 | 36 | 60 | TRUE | FALSE | 65% |

| #2 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 36 | 6 | TRUE | TRUE | 85% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] 10-year Treasury yield — 10-year U.S. Treasury bond yield — The interest rate on the U.S. government's 10-year debt, a key benchmark for long-term borrowing costs and a driver of equity valuations.

[2] asymmetric persistence — asymmetric persistence of inflation expectations — The phenomenon where inflation expectations rise more quickly in response to energy price increases than they fall when prices moderate, creating a lasting upward bias.

[3] basis points — basis points (bps) — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, yields, and financial spreads.

[4] bbl — barrel — A unit of volume for crude oil equal to 42 U.S. gallons, used to measure production, consumption, and pricing.

[5] breakeven inflation — breakeven inflation rate — The difference between nominal Treasury yields and inflation-indexed bond yields, reflecting the market's expected average inflation over the bond's maturity.

[6] Brent crude oil — A major grade of crude oil sourced from the North Sea, used as a global benchmark for oil prices.

[7] core CPI — core Consumer Price Index — A measure of inflation that excludes volatile food and energy prices, used to identify underlying inflation trends.

[8] CPI — Consumer Price Index — A measure of the average change over time in the prices paid by urban consumers for a basket of goods and services, the most common gauge of inflation.

[9] discount rate — The interest rate used in discounted cash flow analysis to determine the present value of future cash flows; also the rate at which the Federal Reserve lends to banks.

[10] discounted cash flow — discounted cash flow (DCF) — A valuation method that estimates the value of an investment based on its expected future cash flows, adjusted for the time value of money using a discount rate.

[11] Dow Industrials — Dow Jones Industrial Average — A stock market index of 30 large, publicly owned U.S. companies, representing the blue-chip sector of the economy.

[12] duration — A measure of the sensitivity of a bond's price to changes in interest rates, expressed in years; also used to describe the weighted average time to receive cash flows from an asset.

[13] earnings yield — The ratio of a company's earnings per share to its stock price, expressed as a percentage; the inverse of the price-to-earnings ratio, used to compare stock returns to bond yields.

[14] easing — monetary easing — A central bank policy aimed at lowering interest rates and increasing money supply to stimulate economic growth, often through rate cuts or quantitative easing.

[15] enterprise value — enterprise value (EV) — A comprehensive measure of a company's total value, including market capitalization, debt, and cash, used in valuation multiples like EV/EBITDA.

[16] Federal Funds Rate — The interest rate at which depository institutions lend reserve balances to each other overnight, set by the Federal Reserve as a primary monetary policy tool.

[17] Federal Reserve — Federal Reserve System (Fed) — The central bank of the United States, responsible for monetary policy, financial stability, and regulation of the banking system.

[18] financial conditions — An aggregate measure of the availability and cost of credit, asset prices, and market volatility, which influence economic activity and central bank policy.

[19] forward P/E — forward price-to-earnings ratio — A valuation ratio calculated using projected earnings over the next 12 months, used to assess whether a stock is cheap or expensive relative to expected profits.

[20] geopolitical risk premium — The additional return investors demand to hold assets exposed to the risk of geopolitical events such as conflicts, sanctions, or supply disruptions.

[21] growth equities — Stocks of companies expected to grow earnings at an above-average rate, often characterized by high valuations and longer-duration cash flows, making them sensitive to interest rate changes.

[22] headline CPI — headline Consumer Price Index — The total CPI that includes all items such as food and energy, often more volatile than core CPI due to fluctuating commodity prices.

[23] inflation expectation — The rate at which consumers, businesses, and investors expect prices to rise in the future, influencing actual inflation and central bank policy decisions.

[24] MOVE index — Merrill Lynch Option Volatility Estimate index — A measure of implied volatility across U.S. Treasury options, similar to the VIX but for the bond market, indicating uncertainty about interest rates.

[25] multiple compression — A reduction in a stock's valuation multiple (e.g., P/E ratio) due to rising interest rates, declining growth expectations, or other factors, leading to lower stock prices.

[26] Nasdaq 100 — Nasdaq-100 Index — A stock market index of the 100 largest non-financial companies listed on the Nasdaq, heavily weighted toward technology and growth sectors.

[27] Nasdaq index — Nasdaq Composite Index — A broad market index of all stocks listed on the Nasdaq stock exchange, used as a proxy for the technology and growth-oriented segments of the U.S. market.

[28] nowcasting model — A statistical model that uses real-time data to estimate current or very near-term economic conditions, such as inflation or GDP growth.

[29] P/E — price-to-earnings ratio — A valuation ratio comparing a company's current share price to its earnings per share, used to assess whether a stock is overvalued or undervalued relative to its profits.

[30] real rates — real interest rates — Interest rates adjusted for inflation, representing the true cost of borrowing and the real return to lenders, often affecting investment decisions.

[31] risk premium — The excess return above a risk-free rate that investors demand to compensate for the uncertainty of a risky investment.

[32] Russell 2000 — Russell 2000 Index — A stock market index that measures the performance of approximately 2,000 small-capitalization U.S. companies.

[33] S&P 500 — Standard & Poor's 500 Index — A stock market index tracking 500 large publicly traded U.S. companies, widely regarded as the best single gauge of the U.S. equity market.

[34] Strait of Hormuz — A narrow waterway between the Persian Gulf and the Gulf of Oman, through which about 21% of global petroleum consumption transits, making it a critical chokepoint for oil supplies.

[35] supply-risk premium — An additional component in the price of oil (or other commodities) that reflects the risk of future supply disruptions due to geopolitical events or infrastructure threats.

[36] tail-risk — tail risk — The risk of an extreme market move occurring in the tails of a probability distribution, typically associated with rare but severe events.

[37] term premium — The extra yield that investors require to hold a long-term bond instead of rolling over short-term bonds, compensating for interest rate uncertainty over time.

[38] tightening — monetary tightening — A central bank policy of raising interest rates and reducing money supply to control inflation, often through rate hikes or reducing asset purchases.

[39] VIX — CBOE Volatility Index — A measure of implied volatility in S&P 500 index options, often called the 'fear index' as it reflects market expectations of near-term volatility.

[40] yield floor — A level below which bond yields are unlikely to fall due to structural factors such as inflation expectations, central bank policy stance, or risk premiums.

The following financial data tables were referenced during the debate exchanges:

| Period | Brent Price | 10-Yr Treasury Yield | Core CPI | Fed Funds Rate |

|---|---|---|---|---|

| 2022 Q2 | $113/bbl | 3.03% | 6.0% | 1.00% |

| 2022 Q3 | $98/bbl | 3.52% | 6.3% | 3.25% |

| 2022 Q4 | $88/bbl | 4.01% | 6.0% | 4.25% |

| 2023 Q1 | $82/bbl | 3.73% | 5.6% | 4.75% |

| 2023 Q2 | $77/bbl | 3.81% | 5.0% | 5.00% |

Legend: Brent crude prices vs. US bond yields and inflation metrics during the 2022-2023 energy shock period. Source: Federal Reserve Economic Data, 2022-2023.

</FinancialData>

| Index | Earnings Yield | Implied Duration | 100bps Yield Impact | Current P/E |

|---|---|---|---|---|

| Nasdaq 100 | 4.2% | ~18 years | -8% to -10% | 23.8x |

| S&P 500 | 5.1% | ~12 years | -5% to -6% | 19.6x |

| Russell 2000 | 4.8% | ~15 years | -7% to -8% | 20.8x |

| Dow Industrials | 5.6% | ~10 years | -4% to -5% | 17.9x |

Legend: Duration sensitivity analysis across major US equity indices. Duration represents weighted average time to receive cash flows; impact shows estimated price change from 100bps yield increase. Source: Index methodology analysis, January 2025.

</FinancialData>

| Event | Brent Price Change | VIX Change | 10-Yr Yield Change | Nasdaq Return (3-mo) |

|---|---|---|---|---|

| 1990 Gulf War | +58% | +45% | +50bps | -18.2% |

| 2008 Financial Crisis | -46% | +210% | -160bps | -41.0% |

| 2020 COVID Shock | -67% | +300% | -120bps | +17.4% |

| 2022 Ukraine War | +35% | +65% | +80bps | -16.8% |

| Oct 2023 Middle East | +8% | +35% | +40bps | +7.2% |

Legend: Historical market reactions to geopolitical and supply shock events. Price changes measured from event onset; Nasdaq returns are 3-month forward. Source: Historical market data compilation.

</FinancialData>

| Oil Shock Period | Brent Peak | 10-Yr Yield Change | Nasdaq Return | S&P 500 Return |

|---|---|---|---|---|

| 1990 Gulf War | $36/bbl | +150bps | -17.4% | -14.7% |

| 2008 Oil Spike | $147/bbl | -70bps | -40.5% | -38.5% |

| 2014-2016 Crash | $27/bbl | -80bps | +18.9% | +12.0% |

| 2022 Energy Crisis | $127/bbl | +230bps | -29.5% | -18.1% |

| 2023 Yield Spike | $94/bbl | +150bps | -10.7% | -6.2% |

Legend: Historical oil shock events and corresponding equity market performance. Returns measured over 6-month periods centered on yield changes. Source: Historical market data, Federal Reserve Economic Data.

</FinancialData>

| Argument | Side | μScore | Key Evidence | Status |

|---|---|---|---|---|

| Duration Risk Compression | TRUE | 0.51 | 18-year duration, -10.7% Nasdaq on 150bps yield rise | STRONGEST |

| Inflation Transmission | TRUE | 0.05 | 0.2-0.4% CPI per $10 oil, 2022 validation | Supported |

| Middle East Dual Headwind | TRUE | 0.20 | Strait of Hormuz 21%, $15-25 risk premium | Supported |

| Oil-to-Yield Overstated | FALSE | 0.23 | Multiple yield drivers beyond oil | Moderate |

| Geopolitical Premiums Short-Lived | FALSE | 0.14 | October 2023 minimal impact | Weak |

Legend: Summary of debate arguments with scores and evidentiary strength. μScore represents weighted composite assessment. Source: Argument Memory Tree analysis.

</FinancialData>

| Period | Brent Crude Peak | CPI YoY (6-mo lag) | 10-Yr Treasury Yield | Fed Funds Rate |

|---|---|---|---|---|

| 2008 Crisis | $147/barrel | 5.6% (Jul 2008) | 4.00% | 2.00% |

| 2011-2014 | $125/barrel | 3.9% (Sep 2011) | 3.50% | 0.25% |

| 2022 Crisis | $127/barrel | 9.1% (Jun 2022) | 4.00% | 4.25% |

| Current (2025) | ~$80/barrel | 2.9% | 4.60% | 4.50% |

Legend: Historical relationship between oil price spikes, inflation persistence, and bond yields. Data: EIA, BLS, Federal Reserve. 6-month lag reflects inflation transmission delay.

</FinancialData>

| Event | Term Premium Change | 10-Yr Yield Impact | Nasdaq-100 Return (3-mo) |

|---|---|---|---|

| 1990 Gulf War | +1.20% | +75 bps | -18.4% |

| 2003 Iraq Invasion | +0.80% | +50 bps | +8.2% |

| 2011 Arab Spring | +0.45% | +30 bps | -2.1% |

| 2022 Russia-Ukraine | +0.90% | +85 bps | -9.5% |

| Oct 2023 Israel-Hamas | +0.80% | +100 bps | +7.8% |

Legend: Geopolitical events, term premium shifts, and Nasdaq performance. Term premium from NY Fed ACM model. Negative returns indicate risk-off episodes. Data: Federal Reserve, Bloomberg.

</FinancialData>

| Sector | Equity Duration (Years) | Yield Sensitivity | Energy Cost % Revenue | 2022 Margin Impact |

|---|---|---|---|---|

| Nasdaq-100 (Aggregate) | 15.2 | -18% per 100bps | 2.8% | -3.1% |

| Information Technology | 16.8 | -20% per 100bps | 1.9% | -2.4% |

| Communication Services | 14.5 | -17% per 100bps | 3.2% | -3.8% |

| Consumer Discretionary | 12.1 | -14% per 100bps | 4.1% | -4.2% |

| S&P 500 Value Index | 7.8 | -9% per 100bps | 3.5% | -2.1% |

Legend: Duration, yield sensitivity, and energy cost exposure by sector. Yield sensitivity = estimated price decline per 100bp yield increase. 2022 margin impact reflects actual operating margin compression during oil spike. Data: Bloomberg, company filings.

</FinancialData>

| Period | Brent Price | 10-Yr Treasury Yield | 10-Yr TIPS Yield | Implied Inflation Expectation | Fed Funds Rate |

|---|---|---|---|---|---|

| Jan 2025 | $77.11 | 4.57% | 1.64% | 2.93% | 4.45% |

| Dec 2025 | $61.35 | 4.61% | 2.08% | 2.53% | 4.50% |

| Mar 2026 | $126.69 | 4.52% | 2.01% | 2.51% | 4.50% |

| Apr 2026 | $124.24 | 4.58% | 2.05% | 2.53% | 4.50% |

Legend: Current market data showing oil price spike and yield decomposition. Implied inflation expectation = nominal yield minus TIPS yield. Data: May 2026.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.