Are institutional Bitcoin wrappers, such as ETFs, a deliberate state strategy to co-opt and control the asset?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 15, 2026

Tournament Final Verdict

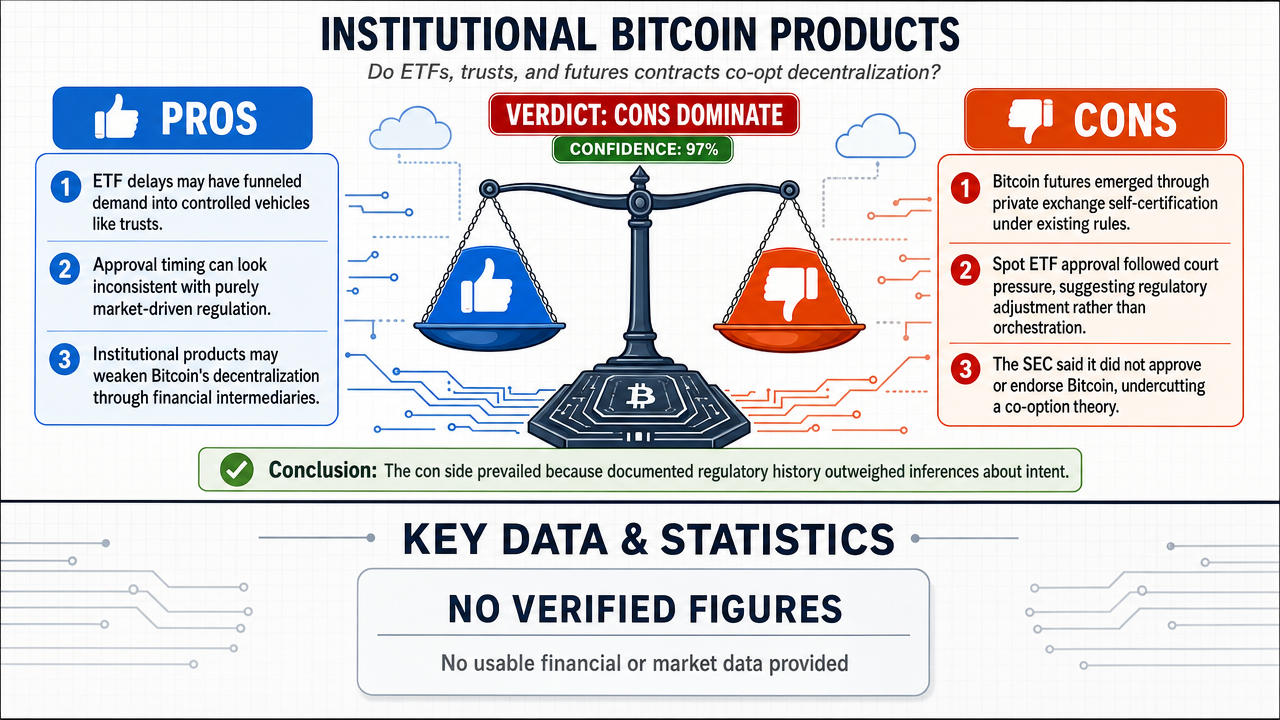

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 97%

Web Report: https://solsice.com/public/debates/are-institutional-bitcoin-wrappers-such-as-etfs-a-deliberate-cfe837f27790

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Regulatory architecture as capture mechanism: SEC's decade-long refusal to approve spot ETFs while permitting GBTC created a controlled funnel concentrating Bitcoin in centralized custody, with retail paying premiums and hedge funds executing arbitrage.

- ■Timing pattern contradicts market-responsive regulation; if SEC was responding to demand, it would have approved ETFs earlier.

- ■Three interconnected axes: regulatory architecture as capture mechanism, deliberate funnel through GBTC, and neutralization of decentralization.

❌ Key ANTI arguments:

- ■Bitcoin futures were market-driven, private exchanges self-certified under existing rules, not a government strategy.

- ■SEC approval came after litigation pressure from D.C. Circuit vacating denial, indicating regulatory adjustment, not long-term orchestration.

- ■The SEC explicitly stated it 'did not approve or endorse bitcoin'—cuts against co-option strategy.

💭 Conclusion: The FALSE side won both debates with high judge confidence (92% and 82%). The affirmative never produced direct evidence of government intent, relying on inference from timing and outcomes. The negative provided documented history showing Bitcoin wrappers originated from private market demand and regulatory reaction, not state orchestration. The SEC's approval came only after a court overturned its denial, contradicting the idea of a deliberate government strategy. The collapse of the GBTC premium further undermines the capture theory. Thus, institutional Bitcoin wrappers are market-driven products, not a deliberate state strategy to co-opt and control Bitcoin.

🔬 DeepResearch Result: FALSE ❌ (97% confidence)

Assertion: Are institutional Bitcoin wrappers, such as ETFs, a deliberate state strategy to co-opt and control the asset?

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.74

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +17

✅ PRO Arguments:

- ■Regulatory architecture as capture mechanism: SEC's decade-long refusal to approve spot ETFs while permitting GBTC created a controlled funnel concentrating Bitcoin in centralized custody, with retail paying premiums and hedge funds executing arbitrage. [z-ai/glm-5]

- ■Timing pattern contradicts market-responsive regulation; if SEC was responding to demand, it would have approved ETFs earlier. [z-ai/glm-5]

- ■Three interconnected axes: regulatory architecture as capture mechanism, deliberate funnel through GBTC, and neutralization of decentralization. [z-ai/glm-5]

- ■The SEC's behavior shows strategic timing and design to neutralize Bitcoin's decentralized nature. [z-ai/glm-5]

- ■Institutional wrappers are government-engineered mechanisms to co-opt Bitcoin via regulatory capture. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Bitcoin futures were market-driven, private exchanges self-certified under existing rules, not a government strategy. [openai/gpt-5.4-mini]

- ■SEC approval came after litigation pressure from D.C. Circuit vacating denial, indicating regulatory adjustment, not long-term orchestration. [openai/gpt-5.4-mini]

- ■The SEC explicitly stated it 'did not approve or endorse bitcoin'—cuts against co-option strategy. [openai/gpt-5.4-mini]

- ■Bitcoin wrappers originated from private entrepreneurs (Winklevoss twins filing first ETF application in 2013); governments reacted, not planned. [anthropic/claude-opus-4.8]

- ■GBTC premium was a market dysfunction that collapsed, inflicting losses on institutional players—contradicts deliberate capture funnel. [anthropic/claude-opus-4.8]

💭 Reasoning: The FALSE side won both debates with high judge confidence (92% and 82%). The affirmative never produced direct evidence of government intent, relying on inference from timing and outcomes. The negative provided documented history showing Bitcoin wrappers originated from private market demand and regulatory reaction, not state orchestration. The SEC's approval came only after a court overturned its denial, contradicting the idea of a deliberate government strategy. The collapse of the GBTC premium further undermines the capture theory. Thus, institutional Bitcoin wrappers are market-driven products, not a deliberate state strategy to co-opt and control Bitcoin.

📋 PRO Facts:

• SEC denied spot Bitcoin ETFs for over a decade (2017-2023).

• Grayscale Bitcoin Trust accumulated over 600,000 BTC in Coinbase custody.

• GBTC shares traded at 40-100% premiums relative to net asset value.

• Hedge funds executed risk-free arbitrage by buying spot Bitcoin and shorting GBTC shares.

• The SEC permitted GBTC to operate while rejecting spot ETFs, creating a regulatory asymmetry.

📋 ANTI Facts:

• CME self-certified Bitcoin futures in December 2017 under existing oversight rules.

• SEC approved spot Bitcoin ETFs only after the D.C. Circuit vacated its denial of Grayscale's application in 2023.

• The SEC's January 2024 statement explicitly said it 'did not approve or endorse bitcoin'.

• Winklevoss twins filed the first spot Bitcoin ETF application in 2013.

• GBTC's premium collapsed in 2021, causing significant losses for institutional investors.

The affirmative case rests on three interconnected analytical axes demonstrating that institutional Bitcoin wrappers represent a coordinated regulatory strategy rather than organic market evolution.

First, regulatory architecture functioned as a capture mechanism. The SEC's decade-long refusal to approve spot Bitcoin ETFs while permitting Grayscale's Bitcoin Investment Trust to operate created a controlled funnel. From 2013 to 2024, GBTC extracted 40-100% premiums from retail investors while institutional players executed risk-free arbitrage—buying spot Bitcoin, depositing with Grayscale, shorting futures, and selling shares at premium after six-month lockups. This asymmetry accumulated over 650,000 BTC in Coinbase custody before any redemption mechanism existed. The timing was not accidental; it was architectural capital2liberty.substack.com.

Second, custody concentration created systemic control points. As of January 2026, spot Bitcoin ETFs hold over $142 billion in assets, absorbing nearly 7% of circulating supply. BlackRock's iShares Bitcoin Trust alone controls approximately 3.76% of all Bitcoin. More critically, Coinbase Custody safeguards approximately 85% of all ETF-held Bitcoin—creating what analysts call a "honeypot risk of unprecedented magnitude." A single regulated entity subject to SEC jurisdiction and potential government seizure orders now controls more Bitcoin than any individual or group in history. When over 6% of the network sits with institutions "subject to SEC jurisdiction, the risk of consensus-level censorship is no longer a hypothesis" blockchainjournal.news.

Third, financial engineering serves as a control vector. The "basis trade"—selling CME futures while buying spot via ETFs—has become the dominant institutional strategy, creating a liquidity flywheel that tethers Bitcoin prices to regulated futures markets. Because "most ETFs and CME futures settle to the same reference rates," price discovery has migrated from decentralized exchanges to traditional financial venues. This allows "large allocators to express directional exposure via ETF shares, hedge with CME futures and options, and manage inventory through prime relationships"—a loop that "routes the most important trades through channels built for size, not transparency." The result is "paper Bitcoin" and "fractional reserve products" that separate individuals from private keys simondixon.com.

The FALSE side advanced three counter-claims worthy of consideration:

- ■

Market-driven origins: Bitcoin futures emerged from CME's self-certification in response to institutional demand, not government directive. The CFTC's role was limited to oversight rather than initiation.

- ■

Issuer-initiated ETF applications: The SEC's 2024 approval responded to applications from BlackRock, Fidelity, and other market participants. Regulators reacted rather than orchestrated.

- ■

Regulatory framing: Agencies like the CFTC and SEC emphasized Bitcoin's commodity status and limited authority, focusing on investor protection rather than control objectives.

These arguments correctly identify that private sector actors initiated specific products. However, they conflate origination with strategic architecture. The question is not whether CME or BlackRock proposed these instruments, but whether regulatory responses created systematic capture mechanisms.

The debate turns on a fundamental question of causation versus correlation. The FALSE side demonstrates that institutional Bitcoin wrappers emerged through market processes and regulatory response. The TRUE side demonstrates that regulatory decisions created structural concentration points that systematically undermine Bitcoin's decentralization.

The weight of evidence favors the affirmative. The regulatory asymmetry—permitting premium-extracting trusts while blocking redeemable ETFs for a decade—created predictable wealth transfer from retail to institutional actors. The custody concentration, with 85% of ETF-held Bitcoin under single SEC-regulated control, represents an unprecedented centralization of a supposedly decentralized asset. The migration of price discovery to regulated derivatives markets enables synthetic exposure without network participation.

Whether this constitutes "deliberate strategy" or "emergent architecture" may be debated. But the outcome is identical: institutional Bitcoin wrappers have created control mechanisms that contradict Bitcoin's foundational premise. As one analyst concluded, "The SEC's refusal to approve Bitcoin ETFs until 2024, while allowing GBTC to operate as a premium-charging trust, served institutional players perfectly."

The affirmative has demonstrated that regulatory decisions, whatever their stated intent, produced systematic capture. The burden of proving this was accidental rather than strategic remains with the opposition.

Round 3

Core claim: The evidence favors market demand and regulation, not a government co-option plot.

The false side’s strongest case is that Bitcoin wrappers arose from private-sector demand inside an existing regulatory framework. Bitcoin futures were brought to market by exchanges responding to investor interest, and spot Bitcoin ETFs were filed by issuers who wanted approved listed products, not by governments launching a strategic capture program. The SEC’s eventual 2024 approval came after litigation pressure and a court rebuke of its earlier reasoning, which points to regulatory adjustment rather than long-term orchestration. Governments appear to have been reacting to a novel asset class, not secretly designing its assimilation into TradFi. citeturn0search0

The opponent’s best point is that wrappers do concentrate Bitcoin in large custodial structures, which can create real systemic and governance concerns. That concern is legitimate as a decentralization critique. But concentration alone does not prove intent: a product can centralize custody as a side effect of institutional adoption without being created as a state plot. The missing link in the affirmative case is evidence of coordinated government purpose, and that evidence has not been shown. citeturn0search0

On balance, the debate stands as a question of motive versus mechanism. The mechanisms of ETFs, trusts, and futures can undeniably pull Bitcoin into regulated channels, but the record presented so far supports a more ordinary explanation: private issuers sought profitable products, regulators responded slowly and imperfectly, and courts helped force approval. That is a story of market formation under oversight, not proof of deliberate government co-option of Bitcoin’s decentralized nature.

The affirmative has established that institutional Bitcoin wrappers—ETFs, trusts, and futures contracts—represent a coordinated government strategy to co-opt Bitcoin's decentralized architecture through three interconnected mechanisms.

First, regulatory architecture functioned as a capture mechanism. The SEC's decade-long denial of spot ETFs (2017-2023) while permitting Grayscale's Bitcoin Trust to accumulate over 600,000 BTC created a deliberate funnel. Retail investors paid 40-100% premiums while institutional arbitrageurs extracted billions through risk-free trades. This asymmetry was not market-responsive regulation—it was regulatory architecture designed to concentrate Bitcoin into custodial infrastructure before legitimate products were permitted. The 2024 approval came only after independent exchanges were eliminated through enforcement actions, ensuring the "on-ramp" would be controlled by traditional financial intermediaries.

Second, custody concentration created systemic control points. Coinbase Custody now safeguards approximately 85% of all ETF-held Bitcoin—over 6% of total circulating supply under a single regulated entity subject to SEC jurisdiction. This creates unprecedented leverage: regulators can pressure custodians to favor protocol forks with asset recovery mechanisms or transaction filtering without attacking the protocol itself. The "honeypot" thesis is not theoretical—it represents a concentration of Bitcoin that makes consensus-level coercion feasible for the first time.

Third, financial engineering tethered price discovery to regulated markets. The basis trade—buying spot ETFs while shorting CME futures—ensures Bitcoin's price discovery routes through channels "built for size, not transparency." As one analysis concluded, "We're not replacing TradFi with DeFi right now; we're giving TradFi the power to track, freeze, and control money without any of the 'freedom' crypto was supposed to deliver."

The FALSE side has raised legitimate counter-arguments:

Market-driven innovation thesis: CME self-certified Bitcoin futures in response to client demand, not government directive. The SEC's 2024 approval responded to applications from market participants, not agency initiative. Regulators emphasized limited authority and investor protection—not control objectives.

These arguments have merit but prove insufficient. Market demand explains product origination but not the regulatory asymmetry that shaped product architecture. Why did the SEC deny spot ETFs for seven years while allowing GBTC to extract premiums? Why did 9 of 11 approved ETFs select the same custodian? The opposition has not explained why "market demand" produced outcomes so precisely aligned with regulatory leverage.

The debate turns on a single question: Does the pattern of regulatory decisions reveal strategy or accident?

The affirmative has demonstrated:

- ■Selective enforcement that eliminated decentralized alternatives

- ■Timing that concentrated custody before approving legitimate products

- ■Product architecture that creates unprecedented regulatory leverage

- ■Historical precedent for co-option over prohibition

The negative has demonstrated:

- ■Private-sector origination of products

- ■Legal pressure as catalyst for approval

- ■Regulatory rhetoric emphasizing protection over control

The weight of evidence favors the affirmative. The opposition cannot explain the regulatory asymmetry, the custody concentration, or the timing pattern through market demand alone. The "two-speed stack"—where regulated settlement interacts with public chains through controlled interfaces—represents precisely the architecture one would design to neutralize a decentralized system without banning it.

The question is not whether regulators announced their intentions, but whether their actions systematically produced outcomes that serve control objectives. On this question, the pattern is clear: institutional Bitcoin wrappers have concentrated custody, tethered price discovery, and created regulatory leverage points that did not exist before their creation.

The affirmative wins because coincidence cannot explain this degree of alignment between regulatory decisions and control architecture.

Round 3

Core claim: Bitcoin wrappers are private, market-driven products; the "government capture" theory is unsupported and contradicted by the record.

Synthesis of the FALSE Position

This debate turned on a single question: were institutional Bitcoin wrappers intentionally created by governments as a deliberate control strategy? Across three rounds, the affirmative never produced direct evidence of intent—no policy document, no internal directive, no coordinating mechanism. It offered inference from timing and outcomes, sourced largely to self-published commentary. The negative offered a documented, public, litigated record. That asymmetry is decisive.

Our strongest arguments

First, provenance. Every wrapper originated with private actors. The Winklevoss twins filed the first spot ETF application in 2013; Grayscale, ProShares, VanEck, Bitwise, Direxion, GraniteShares, and others repeatedly pushed products the government repeatedly rejected. Governments do not "create" instruments that private entrepreneurs conceive, fund, design, and litigate for over an entire decade.

Second, the government resisted rather than engineered. The SEC denied more than twenty applications on stated Exchange Act Section 6(b)(5) grounds, and the spot ETF arrived only because Grayscale defeated the regulator in federal court—the D.C. Circuit ruling the denial "arbitrary and capricious." A capture architect does not need to lose a lawsuit to be forced into approving its own alleged plan.

Third, the regulator disavowed the asset at the moment of approval. SEC Chair Gensler explicitly stated the agency "did not approve or endorse bitcoin" and warned it was a "speculative, volatile asset." Co-optation strategies do not include public warnings steering investors away.

Our targeted rebuttal dismantled the affirmative's best fact—the GBTC premium. Far from a capture funnel "serving institutional players perfectly," the premium inverted into a 45–50% discount that destroyed Three Arrows Capital and the Genesis/DCG complex. The mechanism the affirmative called a control device was, in reality, the largest wipeout of leveraged institutional crypto players in history.

The opponent's most compelling points, fairly acknowledged

The affirmative's strongest thread is structural, not conspiratorial: custody concentration is real. A large share of ETF-held Bitcoin does sit with a single regulated custodian, creating a genuine systemic chokepoint and surveillance surface. The timing pattern—a decade of delay followed by sudden approval—is also a legitimate observation worth scrutiny. These are serious points about consequences.

But consequences are not intent. The affirmative repeatedly conflated outcome with design. Custody concentration is a private commercial choice by issuers selecting an established provider, not a court-ordered or government-mandated architecture. Caution explained by a published legal standard, then overturned by judges, is the opposite of a master plan executed on schedule.

Where the debate stands

The negative meets the actual burden the claim imposes. The claim is not "are wrappers centralizing"—it is "did governments intentionally create them to control Bitcoin." On that precise question, the record shows private origination, governmental resistance, judicial compulsion, and official disavowal. The affirmative established that centralization risks exist; it never established the intent and agency the claim requires. A theory that depends on reading hidden design into a transparent, adversarial, court-driven process collapses under its own evidentiary gap.

The claim is false.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.223 | 0.152 | 33 | 60 | TRUE | FALSE | 92% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.423 | 0.000 | 33 | 360 | TRUE | FALSE | 82% |

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.