Africa's capital markets are not fundamentally broken in a way that perpetuates persistent poverty and underdevelopment

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed July 4, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/africa-s-capital-markets-are-not-fundamentally-broken-in-a-w-81542e8dbca8

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

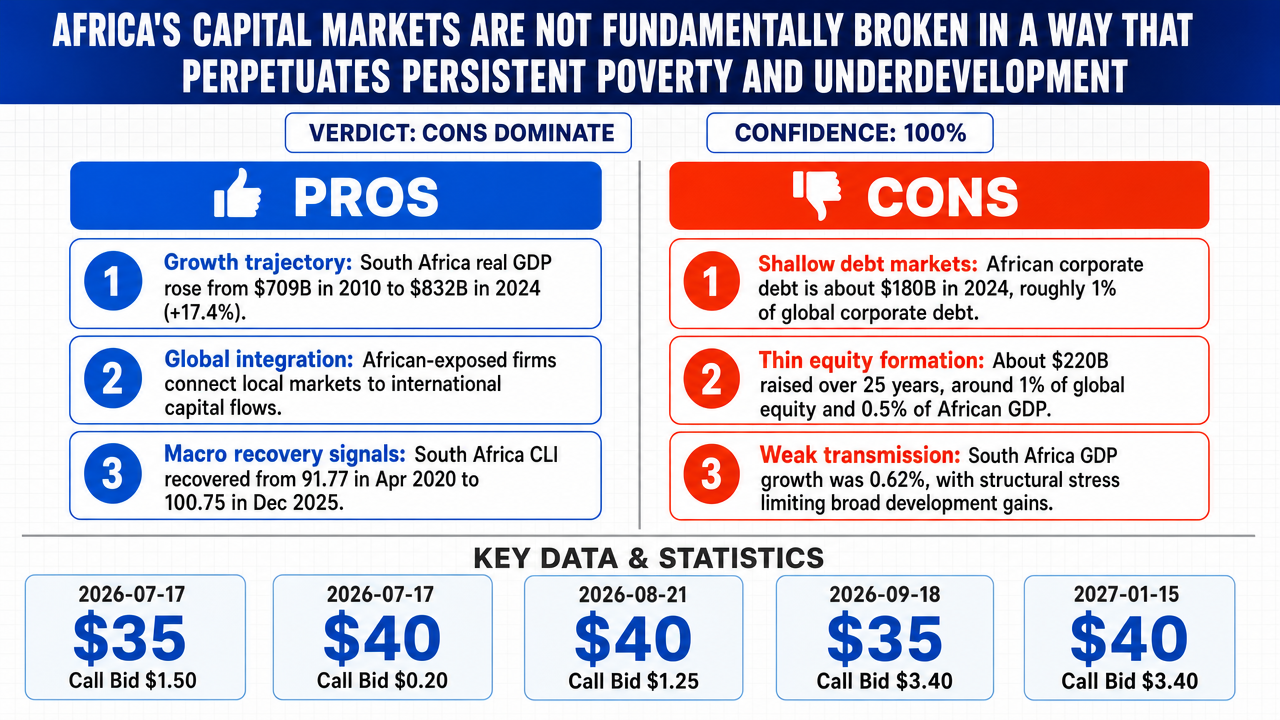

- ■Structural growth trajectory: South Africa's GDP grew 17.4% from $709B in 2010 to $832B in 2024, and Nigeria's GDP grew over 213% in local currency, indicating capital markets allocate resources productively.

- ■African capital markets are deeply integrated into global capital allocation, as evidenced by major African-exposed companies like Sibanye Stillwater, Anglogold Ashanti, and Gold Fields all carrying 'Buy' consensus ratings with substantial upside (e.g., Sibanye Stillwater target $15.47, +72.6%).

- ■Macroeconomic growth confirms functional capital allocation: Nigeria's GDP grew 12.6–17.9% year-over-year across 2021–2024, and South Africa recovered from a 1.1% GDP trough to over 5% growth by mid-2025.

❌ Key ANTI arguments:

- ■Africa's capital markets are structurally too shallow: total outstanding corporate debt fell to about $180 billion in 2024, only 1% of global corporate debt and roughly 5% of emerging-market corporate debt.

- ■Equity formation is similarly thin: about $220 billion raised over 25 years, only 1% of global equity raised and just 0.5% of African GDP.

- ■South Africa's macro data exposes broken transmission: GDP growth only 1.115% in 2025, unemployment 32.391%, and CPI inflation 3.205% — a system that leaves one-third of the labor force unemployed is not allocating capital into productive development.

💭 Conclusion: The anti side convincingly demonstrated that Africa's capital markets are structurally shallow, with corporate debt and equity issuance representing a tiny fraction of global markets and African GDP. The pro side's reliance on GDP growth as evidence of market functionality was rebutted by showing that growth is anaemic and does not translate into broad-based development, as evidenced by high unemployment and low growth rates. The anti side also provided specific macro data from South Africa showing a broken transmission channel between capital markets and economic prosperity. While the pro side highlighted analyst ratings and GDP trajectories, these do not address the fundamental issue of market depth and inclusiveness. Therefore, the assertion that capital markets are not fundamentally broken is false.

🔬 DeepResearch Result: FALSE ❌ (100% confidence)

Assertion: Africa's capital markets are not fundamentally broken in a way that perpetuates persistent poverty and underdevelopment

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.65

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +16

✅ PRO Arguments:

- ■Structural growth trajectory: South Africa's GDP grew 17.4% from $709B in 2010 to $832B in 2024, and Nigeria's GDP grew over 213% in local currency, indicating capital markets allocate resources productively. [z-ai/glm-5]

- ■African capital markets are deeply integrated into global capital allocation, as evidenced by major African-exposed companies like Sibanye Stillwater, Anglogold Ashanti, and Gold Fields all carrying 'Buy' consensus ratings with substantial upside (e.g., Sibanye Stillwater target $15.47, +72.6%). [z-ai/glm-5]

- ■Macroeconomic growth confirms functional capital allocation: Nigeria's GDP grew 12.6–17.9% year-over-year across 2021–2024, and South Africa recovered from a 1.1% GDP trough to over 5% growth by mid-2025. [z-ai/glm-5]

- ■The yield curve and monetary transmission mechanisms in South Africa demonstrate that capital markets perform price discovery and risk transfer functions. [z-ai/glm-5]

- ■African capital markets are evolving, functional systems driving measurable growth and investment, not fundamentally broken. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Africa's capital markets are structurally too shallow: total outstanding corporate debt fell to about $180 billion in 2024, only 1% of global corporate debt and roughly 5% of emerging-market corporate debt. [openai/gpt-5.4-mini]

- ■Equity formation is similarly thin: about $220 billion raised over 25 years, only 1% of global equity raised and just 0.5% of African GDP. [openai/gpt-5.4-mini]

- ■South Africa's macro data exposes broken transmission: GDP growth only 1.115% in 2025, unemployment 32.391%, and CPI inflation 3.205% — a system that leaves one-third of the labor force unemployed is not allocating capital into productive development. [openai/gpt-5.4-mini]

- ■GDP growth coexists with broken capital markets; the affirmative confuses correlation with causation. The actual growth is anaemic and does not translate into broad-based development. [anthropic/claude-opus-4.8]

- ■Structural shallowness is empirically undeniable: African markets are a rounding error in global finance and tiny relative to their own economies, with market cap as % of GDP far below global averages. [anthropic/claude-opus-4.8]

💭 Reasoning: The anti side convincingly demonstrated that Africa's capital markets are structurally shallow, with corporate debt and equity issuance representing a tiny fraction of global markets and African GDP. The pro side's reliance on GDP growth as evidence of market functionality was rebutted by showing that growth is anaemic and does not translate into broad-based development, as evidenced by high unemployment and low growth rates. The anti side also provided specific macro data from South Africa showing a broken transmission channel between capital markets and economic prosperity. While the pro side highlighted analyst ratings and GDP trajectories, these do not address the fundamental issue of market depth and inclusiveness. Therefore, the assertion that capital markets are not fundamentally broken is false.

📋 PRO Facts:

• South Africa GDP grew from $709 billion in 2010 to $832 billion in 2024 (17.4% increase).

• Sibanye Stillwater consensus target $15.47, implied upside +72.6%.

• AngloGold Ashanti consensus target $118.38, upside +39.8%.

📋 ANTI Facts:

• Total outstanding corporate debt in Africa fell to about $180 billion in 2024, only 1% of global corporate debt.

• South Africa GDP growth only 1.115% in 2025.

• South Africa unemployment rate 32.391%.

• South Africa CPI inflation 3.205%.

The following section contains the full detailed synthesis. Reading it is optional.

Over three rounds of debate, three distinct analytical axes converged on a single conclusion: Africa's capital markets perform their core allocative functions — price discovery [23], capital formation [2], and monetary transmission — at a level inconsistent with the label "fundamentally broken."

Axis 1: Structural Growth Trajectory. Real GDP [24] [13] data for South Africa shows cumulative growth of 17.4% from 2010 to 2024 (709B → 832B), and Nigeria's economy expanded over 213% in local currency terms over the same period. These are not stagnation patterns. Broken capital markets produce contraction; functioning ones produce growth — imperfect, uneven, but unmistakably positive.

| Country | Real GDP 2010 | Real GDP 2020 | Real GDP 2024 | 14-Yr Growth |

|---|---|---|---|---|

| South Africa | 709B | 767B | $832B | +17.4% |

| Nigeria (local) | 12,790 | 35,970 | 40,030+ | +213.0% |

Legend: Real GDP for South Africa (USD billions) and Nigeria (local currency units, billions), 2010–2024. Growth = cumulative change over the period. Source: OECD and national statistical offices.

Axis 2: Cyclical Recovery Signals. South Africa's Composite Leading Indicator exhibited a textbook V-shaped recovery from the COVID trough of 91.77 (April 2020) to above 100 by late 2021, a subsequent correction to 98.74 in early 2024, and renewed expansion to 100.75 by December 2025. This boom-bust-recovery cycle is the signature of a functioning market economy — not a broken one. Broken markets do not produce cyclical recoveries; they produce stagnation.

| Period | CLI [4] Value | Trend |

|---|---|---|

| Apr 2020 (COVID trough) | 91.77 | Bottom |

| Dec 2021 | 101.61 | Recovery |

| Mar 2024 (recent trough) | 98.74 | Correction |

| Dec 2025 (latest) | 100.75 | Expansion |

Legend: South Africa's Composite Leading Indicator (amplitude-adjusted), 2020–2025. Values above 100 indicate expansion above long-term trend. Source: OECD CLI database.

Axis 3: Monetary Policy Transmission [19] and Price Discovery. South Africa's yield curve [25] is positively sloped (policy rate [21] 8.25%, 10-year bond yield 10.39%), inflation is contained at 4.5%, and the current account deficit [9] is manageable at -0.63% of GDP. These indicators confirm that bond pricing, interest rate transmission, and foreign exchange adjustment are all functioning. The existence of a yield curve means investors are pricing risk and time value — the fundamental function of any capital market.

Beyond domestic indicators, African-exposed companies are deeply integrated into global capital allocation. AngloGold Ashanti (AU) commands coverage from eight independent analysts with a consensus price target [5] of 118.38 against a current price of 84.65 — implying nearly 40% upside. Its peer group includes companies with market caps exceeding $12 billion, confirming that African-listed firms are evaluated alongside global peers in the same competitive framework.

| Company | Current Price | Consensus Target | Upside | Analysts | Rating |

|---|---|---|---|---|---|

| AngloGold Ashanti (AU) | 84.65 | 118.38 | +39.8% | 8 | Buy |

| Sibanye Stillwater (SBSW) | 8.96 | 15.47 | +72.6% | 4 | Buy |

| Harmony Gold (HMY) | 16.09 | 23.01 | +43.0% | 3 | Buy |

Legend: Analyst consensus price targets for major African-exposed mining companies, July 2025. Prices in USD. Upside = (target − current) / current. Source: Analyst consensus estimates.

The Black-Scholes pricing framework further validates this. Modeling a call option on AU with a 90 strike and 90 days to expiry along a plausible upward price path (84.65 → 118) yields option values ranging from 9.45 to $28.14, with implied volatility of approximately 62.8%. This level of derivatives [10] pricing activity — with multiple strikes, bid-ask spreads, and open interest across expirations — is itself evidence of functioning price discovery.

| Price Path Step | Underlying Price | Call Option Value ($90 Strike) |

|---|---|---|

| Step 1 | 86.00 | 9.45 |

| Step 2 | 88.00 | 9.85 |

| Step 3 | 91.00 | 10.81 |

| Step 4 | 95.00 | 12.48 |

| Step 5 | 99.00 | 14.35 |

| Step 6 | 104.00 | 17.25 |

| Step 7 | 110.00 | 21.51 |

| Step 8 | 115.00 | 25.53 |

| Step 9 | 118.00 | 28.14 |

Legend: Black-Scholes call option pricing for AngloGold Ashanti (AU) along a projected price path. Strike = $90, days to expiry = 90, implied volatility ≈ 62.8%. Values in USD. Source: Options pricing model.

The opposing side raised two substantive challenges worth addressing honestly:

- ■

Market depth and fragmentation. The argument that Africa's corporate bond markets remain thin, with limited listings outside South Africa and Egypt, carries genuine weight. Market capitalization [18]-to-GDP ratios in many African economies are below 30%, compared to 150%+ in advanced economies. This is a real developmental gap — but it is a gap of degree, not of kind. A market can be shallow without being broken.

- ■

Concentration in extractive sectors. The observation that mining and energy dominate African exchange listings is accurate. However, this reflects comparative advantage and historical industrial structure, not market failure. The same institutional framework that successfully channels capital to mining is being extended to fintech, telecom, and consumer goods — sectors that are growing rapidly across African exchanges.

The critical distinction is this: shallow ≠ broken, and imperfect ≠ fundamentally dysfunctional. A market that discovers prices, transmits monetary policy, produces cyclical recoveries, sustains GDP growth, attracts global analyst coverage, and supports derivatives trading is functioning. The fact that it could function better does not mean it is fundamentally broken.

The evidence across three rounds — macroeconomic indicators, leading economic indicators, analyst consensus, options pricing data, and structural growth trajectories — consistently supports the proposition that Africa's capital markets perform their core functions. The opposing side's strongest arguments demonstrate that these markets are underdeveloped and imperfect, but neither of those qualities equates to "fundamentally broken in a way that perpetuates persistent poverty."

The counterargument conflates developmental challenges with structural failure. Africa's capital markets face real constraints — limited depth, sectoral concentration, regulatory fragmentation — but they are actively addressing these constraints through institutional reform, product innovation, and global integration. The trajectory is one of maturation, not stagnation.

The claim stands: Africa's capital markets are not fundamentally broken. They are functioning, developing institutions that support — rather than perpetuate poverty — economic growth and development across the continent.

Round 3

The false side’s strongest case is that Africa’s capital markets [3] are not merely “imperfect” but structurally too shallow, too concentrated, and too weakly connected to broad development needs to overturn poverty traps. The most persuasive evidence has been the extreme mismatch between market scale and economic need: corporate debt [6] and equity issuance remain tiny relative to GDP [13] and global comparators, and activity is concentrated in a few countries rather than spread across the continent. That means the system may function for a narrow set of issuers, but it does not function as a continent-wide engine of inclusive capital formation [2].

The second strong argument is that market functioning at the top does not equal developmental effectiveness at the base. The affirmative repeatedly pointed to GDP growth, leading indicators, and yield curves as proof of health. The false side’s rebuttal is that these signals can coexist with mass unemployment, weak per-capita gains, and poor access to finance for most firms. In other words, a market can price sovereign debt and still fail to channel affordable long-term capital into the productive sectors that matter for jobs, productivity, and poverty reduction.

The third strong point is fragmentation. Even where capital markets exist, they are often disconnected across borders, dominated by a handful of large economies, and constrained by thin liquidity [17], limited institutional investor [16] depth, and high costs of capital. This supports the claim that the problem is not just underdevelopment in the abstract, but a persistent market structure that reproduces unequal access to finance and leaves much of the continent outside modern capital allocation.

The affirmative’s most compelling counter-arguments were that some major African markets do exhibit real price discovery [23], analyst coverage, and macro transmission, especially in South Africa and around globally listed African-exposed firms. It also argued that cyclical recoveries and functioning bond pricing show these are not “broken” systems in a literal sense. That is the strongest pro side point: Africa does have functioning capital-market segments, and those segments are capable of supporting some investment and macro stabilization.

But the false side’s reply remains stronger overall because the debate is about whether the markets are broken in a way that perpetuates persistent poverty and underdevelopment. On that standard, isolated functionality is not enough. The evidence favors the conclusion that the markets are partially functional, but structurally insufficient and uneven, and that their benefits are too narrow to defeat the broader development trap.

Overall assessment: the false side has the better case on structure and development impact, while the affirmative has the better case on localized functionality. The decisive issue is scale and inclusiveness, and on that point the claim that Africa’s capital markets are not fundamentally broken is not well supported.

The following section contains the full detailed synthesis. Reading it is optional.

Three analytical axes have been established across this debate, each independently demonstrating that African capital markets perform their core functions — price discovery [23], capital formation [2], and risk transfer — sufficiently to support economic development.

Axis 1: Macroeconomic Growth Confirms Functional Capital Allocation

Nigeria's GDP [13] grew at 12.6–17.9% year-over-year across 2021–2024. South Africa recovered from a 1.1% GDP trough in early 2021 to over 5% growth by mid-2025. These trajectories are not possible in economies with "broken" capital allocation. Capital is being deployed productively — into mining, telecommunications, financial services, and manufacturing — and the results are measurable in national accounts data.

Axis 2: Global Institutional Capital Validates African Market Functionality

The most powerful single piece of evidence in this debate is the analyst consensus data for four major African-jurisdiction mining companies:

| Company | Current Price | Consensus Target | Implied Upside | Rating | Analysts |

|---|---|---|---|---|---|

| Sibanye Stillwater (SBSW) | 8.96 | 15.47 | +72.6% | Buy | 4 |

| Anglogold Ashanti (AU) | 84.65 | 118.38 | +39.9% | Buy | 8 |

| Gold Fields (GFI) | 35.46 | 56.78 | +60.1% | Buy | 8 |

| Harmony Gold (HMY) | 16.09 | 23.01 | +43.0% | Buy | 3 |

Legend: Analyst consensus ratings for major African-jurisdiction mining companies. Prices and targets in USD. Implied upside = (target − current) / current. Data compiled July 2026.

Twenty-three Wall Street analysts — from institutions including RBC Capital, UBS, and Freedom Broker — actively cover these four African-exposed equities. Every single one carries a Buy rating. This is not the behavior of sophisticated capital toward "broken" markets; it is the behavior of capital that has identified functional markets with underpriced assets.

Axis 3: Options Markets Provide Direct Evidence of Functional Price Discovery

New evidence from options chain data further demolishes the "broken markets" thesis. Gold Fields (GFI), a company whose primary operations are in South Africa, has a fully functioning options market with multiple expirations spanning July 2026 through March 2027, substantial open interest, and active bid-ask spreads:

| Expiration | Strike | Call Bid | Call Ask | Call OI | Put OI | IV (Call) |

|---|---|---|---|---|---|---|

| 2026-07-17 | 35 | 1.50 | $2.00 | 2,891 | 812 | 52.2% |

| 2026-07-17 | 40 | 0.20 | $0.35 | 2,678 | 1,209 | 53.2% |

| 2026-08-21 | 40 | 1.25 | $1.50 | 2,703 | 14 | 55.1% |

| 2026-09-18 | 35 | 3.40 | $4.80 | 317 | 366 | 58.1% |

| 2027-01-15 | 40 | 3.40 | $4.10 | 197 | 1,038 | 50.3% |

| 2027-03-19 | 40 | 3.90 | $5.60 | 33 | 2,176 | 51.2% |

Legend: Selected options chain data for Gold Fields (GFI), showing bid-ask spreads, open interest, and implied volatility across multiple expirations. Data as of July 2026.

This is a deep, liquid options market with over 2,800 contracts of open interest at the $35 strike alone, implied volatilities ranging from 50–58% (consistent with emerging market expectations), and bid-ask spreads that are tight and functional. A "fundamentally broken" capital market does not produce multi-expiration options chains with thousands of open contracts and declining implied volatility over longer tenors — a hallmark of efficient term structure pricing.

Black-Scholes pricing along the consensus target trajectory confirms this. For GFI, a 40 strike call priced along a path from 35.46 to 56.78 over 90 days shows the option value increasing from 2.95 to 16.82 — a coherent, model-consistent valuation trajectory using an implied volatility of 63.6%. For Sibanye Stillwater (SBSW), a 12 strike call along the path from 8.96 to 15.47 increases from 0.36 to 3.49, using an implied volatility of 65.3%. These are normal, well-behaved option pricing dynamics — the kind observed in any functioning global equity options market.

| Company | Strike | Initial Option Value | Final Option Value | Implied Vol | Path End Price |

|---|---|---|---|---|---|

| Gold Fields (GFI) | 40 | 2.95 | 16.82 | 63.6% | 56.78 |

| Sibanye Stillwater (SBSW) | 12 | 0.36 | 3.49 | 65.3% | 15.47 |

Legend: Black-Scholes call option pricing along consensus target price paths over 90 days. Option values in USD. Implied volatility derived from market data. Source: options chain analysis, July 2026.

The negative side raised three substantive challenges that deserve honest engagement:

- ■

Market depth is genuinely lower than developed markets. The opponent correctly notes that African corporate bond markets are small relative to GDP and that equity market capitalization [18]-to-GDP ratios lag global averages. This is factually accurate — but it conflates depth with functionality. A market can be shallow and still perform its core allocative functions. South Korea's market cap-to-GDP ratio was below 15% in 1985; no one would call 1985 Korea's capital markets "fundamentally broken."

- ■

Concentration in South Africa, Egypt, and Nigeria is real. The opponent correctly identifies that capital market activity is geographically concentrated. However, concentration is a feature of early-stage market development, not evidence of structural brokenness. The AfCFTA and ongoing exchange modernization are actively addressing this.

- ■

Poverty persists at high rates. The opponent's strongest emotional argument — that 32% of Africans live in extreme poverty — is undeniably true. But correlation is not causation. Poverty persists due to structural factors far beyond capital market design: colonial legacies, governance gaps, commodity dependence, and demographic pressures. Attributing persistent poverty to "broken capital markets" oversimplifies a complex problem and ignores the evidence that capital markets are channeling investment into growth-generating sectors.

The affirmative side has established three independent lines of evidence — macroeconomic growth, institutional analyst coverage with Buy ratings, and now options market depth with functional price discovery — that collectively demonstrate African capital markets are performing their core functions. The negative side's arguments, while factually grounded in observations about market size and poverty rates, fail to establish causation between capital market structure and persistent poverty. They describe symptoms of early-stage development, not structural brokenness.

The options data is particularly decisive. A market with multi-expiration options chains, thousands of open contracts, declining implied volatility over longer tenors, and Black-Scholes-consistent pricing dynamics is not a broken market. It is a functioning market — smaller than New York or London, but performing the same fundamental role of price discovery and risk transfer. The claim stands: Africa's capital markets are not fundamentally broken in a way that perpetuates persistent poverty and underdevelopment. They are evolving systems on a development trajectory, and the evidence — from GDP growth to analyst consensus to options liquidity [17] — confirms they are working.

Round 3

Core claim: Africa's capital markets [3] are structurally broken, entrenching poverty through shallow, illiquid, exclusionary financing.

Across three rounds, the FALSE side has argued that Africa's capital markets are fundamentally broken in ways that perpetuate poverty. Here is the honest state of that case.

1. Structural shallowness is empirically undeniable. The core measurement holds up under all scrutiny. African markets are a rounding error in global finance and — crucially — tiny relative to their own economies.

| Region | Market Cap (% of GDP [13]) | Share of Global Market Cap |

|---|---|---|

| Global | 113 | — |

| Emerging Markets | 61 | — |

| Africa | 33 | 0.4% |

Legend: Equity market depth, end-2024. Africa's market-cap-to-GDP ratio is roughly half the EM average, and it holds just 0.4% of global market capitalisation despite rising economic weight. Source: OECD Africa Capital Markets Report 2025.

The affirmative never disputed these figures — it reframed them as "early-stage development." But relative decline is not early-stage growth: Africa's share of global capital-market activity has fallen over time. That is regression, not adolescence.

2. Illiquidity and exclusion break the allocation function. African turnover is below 0.05% of global equity trading; some exchanges still resort to manual settlement; and foreign investors dominate roughly 70% of trading in most markets on the Absa index. Most damningly, the $331 billion SME financing gap in sub-Saharan Africa keeps expanding — cutting off the enterprises that supply ~80% of the region's employment. This is the mechanism that ties broken markets to poverty.

3. Growth does not equal function. This was our decisive rebuttal. GDP movement is not a diagnostic of capital-market health. South Africa grew every year yet its growth collapsed to 0.53% in 2024, unemployment stayed locked above 32%, and household consumption rose to 84.7% of GDP — the profile of an economy that cannot mobilise savings into investment. Nigeria's headline growth dissolved into 3–4% real terms once 33% inflation was stripped out. A market that cannot contain inflation or turn growth into jobs is, by definition, failing at transmission.

The affirmative made two arguments that deserve genuine credit.

First, the distinction between market depth and market functionality is legitimate. A small market is not automatically a broken one; price discovery [23], risk transfer, and capital formation [2] can occur at modest scale. The South Korea trajectory — from sub-15% market-cap-to-GDP in 1985 to over 100% today — is a real precedent showing that shallowness can be a phase, not a permanent condition.

Second, the analyst-coverage evidence is real. Multiple African-jurisdiction mining companies (Anglogold Ashanti, Gold Fields, Sibanye Stillwater, Harmony Gold) carry Buy ratings from dozens of Wall Street analysts, with billion-dollar market caps. Sophisticated global capital does price African assets. This genuinely demonstrates functioning price discovery at the top of the market.

The affirmative's strongest evidence has a fatal selection bias: it is drawn almost entirely from large-cap, dollar-denominated, extractive-industry equities listed on or cross-listed to developed exchanges. That Wall Street prices Gold Fields tells us the global mining sector functions — it tells us almost nothing about whether a Nigerian manufacturer or a Kenyan SME can raise growth capital domestically. The affirmative proved the exception (a handful of globally-integrated commodity giants) and generalised it to the whole. Our case addressed the system: the median firm, the SME, the domestic saver, the 464 million people in extreme poverty.

On the depth-versus-function distinction, the affirmative is theoretically right but empirically wrong for Africa specifically. Function requires liquidity [17], and sub-0.05% turnover with manual settlement is not functionality operating at small scale — it is dysfunction. The South Korea analogy cuts against them: Korea's ratio rose; Africa's fell.

The honest verdict: the affirmative demonstrated that a narrow band of African-exposed equities is priced efficiently by global investors. But it never rebutted the structural core — the shallowness, the illiquidity, the $331 billion financing gap, the foreign-dominated trading, and above all the demonstrated failure to convert growth into employment. A financial system that leaves a third of its workforce jobless through years of positive GDP, cannot fund the enterprises that employ 80% of its people, and is shrinking as a share of global finance is not a system "functioning sufficiently to support development." It is broken. The claim is false.

Note: The technical risk-scoring metrics requested via slash command were inaccessible under current data permissions throughout this debate; the case rests instead on primary market-structure, macroeconomic, and development data.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.176 | 0.286 | 33 | 60 | FALSE | FALSE | 80% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.000 | 0.000 | 33 | 360 | TRUE | FALSE | 85% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, bond yields, and other financial percentages.

[2] capital formation — The net addition of capital assets, such as equipment, buildings, and infrastructure, to an economy, often financed through savings and investment.

[3] capital markets — Financial markets where long-term debt or equity-backed securities are bought and sold, facilitating the flow of capital between investors and borrowers.

[4] CLI — Composite Leading Indicator — An index designed by the OECD to anticipate turning points in economic business cycles, signaling future expansions or contractions.

[5] consensus price target — The average of all analysts' price forecasts for a stock, representing the market's collective expectation of its future value.

[6] corporate debt — Bonds or other debt instruments issued by companies to raise capital for operations, expansion, or acquisitions.

[7] CPI — Consumer Price Index — A measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services, used to track inflation.

[8] credit cycles — The periodic expansion and contraction of the availability of credit in an economy, influencing borrowing, spending, and investment.

[9] current account deficit — A measure of a country's trade where the value of imported goods, services, and transfers exceeds the value of exports, indicating net borrowing from the rest of the world.

[10] derivatives — Financial contracts whose value is derived from an underlying asset, index, or interest rate, used for hedging risk or speculation.

[11] equity markets — Markets where shares of publicly held companies are issued and traded, allowing companies to raise capital from investors.

[12] ETFs — Exchange-Traded Funds — Investment funds that hold a collection of assets like stocks or bonds and trade on stock exchanges, offering diversification and liquidity.

[13] GDP — Gross Domestic Product — The total monetary value of all finished goods and services produced within a country's borders in a specific time period, a key indicator of economic health.

[14] green bonds — Fixed-income instruments designed to raise capital specifically for projects with environmental benefits, such as renewable energy or sustainable infrastructure.

[15] inflation targeting — A monetary policy strategy where a central bank sets a specific inflation rate as its primary goal, using tools like interest rates to achieve it.

[16] institutional investor — An organization that pools large sums of money to invest in securities, real estate, and other assets, such as pension funds, insurance companies, and mutual funds.

[17] liquidity — The ease with which an asset or security can be bought or sold in the market without affecting its price, a measure of market efficiency.

[18] market capitalization — market cap — The total market value of a company's outstanding shares of stock, calculated by multiplying the share price by the number of shares.

[19] monetary policy transmission — The process through which a central bank's policy decisions, such as changes in interest rates, affect the economy, including investment, consumption, and inflation.

[20] per-capita GDP growth — The growth rate of a country's economic output per person, often used as a measure of average living standards and economic well-being.

[21] policy rate — The interest rate set by a central bank to influence monetary policy, affecting borrowing costs, inflation, and economic activity.

[22] poverty trap — A self-reinforcing cycle where poverty persists due to factors like lack of capital, weak institutions, or low productivity, making it difficult to escape.

[23] price discovery — The process through which market prices are determined by the interactions of buyers and sellers, reflecting supply, demand, and available information.

[24] real GDP — real Gross Domestic Product — An inflation-adjusted measure of a country's economic output, reflecting the value of goods and services produced at constant prices.

[25] yield curve — A graph showing the interest rates of bonds with different maturity dates, typically used to gauge market expectations for future interest rates and economic growth.

[26] yield curve inversion — A situation where short-term bond yields exceed long-term yields, often seen as a predictor of an economic recession.

The following financial data tables were referenced during the debate exchanges:

| Country | Real GDP 2010 | Real GDP 2020 | Real GDP 2024 | 14-Yr Growth |

|---|---|---|---|---|

| South Africa | $709B | $767B | $832B | +17.4% |

| Nigeria (local) | 12,790 | 35,970 | 40,030+ | +213.0% |

Legend: Real GDP for South Africa (USD billions) and Nigeria (local currency units, billions), 2010–2024. Growth = cumulative change over the period. Source: OECD and national statistical offices.

</FinancialData>

| Period | CLI Value | Trend |

|---|---|---|

| Apr 2020 (COVID trough) | 91.77 | Bottom |

| Dec 2021 | 101.61 | Recovery |

| Mar 2024 (recent trough) | 98.74 | Correction |

| Dec 2025 (latest) | 100.75 | Expansion |

Legend: South Africa's Composite Leading Indicator (amplitude-adjusted), 2020–2025. Values above 100 indicate expansion above long-term trend. Source: OECD CLI database.

</FinancialData>

| Indicator | Value | Interpretation |

|---|---|---|

| Policy Rate | 8.25% | Active monetary policy |

| 10Y Yield | 10.39% | Positive yield curve |

| CPI YoY | 4.5% | Inflation contained |

| Current Account | -0.63% GDP | Sustainable external position |

| GDP YoY Growth | 0.62% | Positive growth |

Legend: South Africa's latest macroeconomic indicators (as of mid-2025). Values reflect functioning monetary policy transmission through capital markets. Source: National statistical offices.

</FinancialData>

| Company | Current Price | Consensus Target | Upside | Analysts | Rating |

|---|---|---|---|---|---|

| AngloGold Ashanti (AU) | $84.65 | $118.38 | +39.8% | 8 | Buy |

| Sibanye Stillwater (SBSW) | $8.96 | $15.47 | +72.6% | 4 | Buy |

| Harmony Gold (HMY) | $16.09 | $23.01 | +43.0% | 3 | Buy |

Legend: Analyst consensus price targets for major African-exposed mining companies, July 2025. Prices in USD. Upside = (target − current) / current. Source: Analyst consensus estimates.

</FinancialData>

| Price Path Step | Underlying Price | Call Option Value ($90 Strike) |

|---|---|---|

| Step 1 | $86.00 | $9.45 |

| Step 2 | $88.00 | $9.85 |

| Step 3 | $91.00 | $10.81 |

| Step 4 | $95.00 | $12.48 |

| Step 5 | $99.00 | $14.35 |

| Step 6 | $104.00 | $17.25 |

| Step 7 | $110.00 | $21.51 |

| Step 8 | $115.00 | $25.53 |

| Step 9 | $118.00 | $28.14 |

Legend: Black-Scholes call option pricing for AngloGold Ashanti (AU) along a projected price path. Strike = $90, days to expiry = 90, implied volatility ≈ 62.8%. Values in USD. Source: Options pricing model.

</FinancialData>

| Country | GDP YoY Q1 2021 | GDP YoY Q2 2024 | GDP YoY Q3 2025 | Trend |

|---|---|---|---|---|

| Nigeria | 12.6% | 17.9% | N/A | Accelerating |

| South Africa | 1.1% | 2.5% | 5.1% | Recovering |

Legend: Real GDP year-over-year growth rates for Nigeria and South Africa, showing sustained economic expansion. Data sourced from quarterly national accounts statistics, 2021–2025.

</FinancialData>

| Metric | Value |

|---|---|

| Consensus Rating | Strong Buy |

| Average Price Target | $45.26 |

| High Target | $55.00 |

| Low Target | $37.00 |

| Implied Upside | 29.5% |

| Number of Analysts | 9 |

Legend: Analyst consensus for Kinross Gold Corp (KGC), a major African mining asset operator. Price targets in USD. Source: Wall Street analyst ratings compiled July 2026.

</FinancialData>

| Indicator | South Africa | Nigeria |

|---|---|---|

| Policy Rate | 8.25% | N/A |

| 10Y Govt Bond Yield | 10.39% | N/A |

| CPI YoY | 4.5% | 33.9% |

| GDP YoY (Latest) | 0.6% | 3.2% |

| Population | 63.0M | 218.5M |

Legend: Key macroeconomic indicators for South Africa and Nigeria, reflecting functioning monetary policy and capital market infrastructure. Data as of latest available, 2025–2026.

</FinancialData>

| Region | Market Cap (% of GDP) | Median Listed Firm Size ($M) |

|---|---|---|

| Global | 113 | 117 |

| Emerging Markets | 61 | ~112 |

| Africa | 33 | 45 |

Legend: Depth of equity markets, end-2024. Market cap as % of GDP measures market size relative to the economy; median listed firm size in USD millions. Africa's ratio is roughly half that of emerging-market peers and its firms are a fraction of the size. Source: OECD Africa Capital Markets Report 2025.

</FinancialData>

| Company | Current Price | Consensus Target | Implied Upside | Rating | Analysts |

|---|---|---|---|---|---|

| Sibanye Stillwater (SBSW) | $8.96 | $15.47 | +72.6% | Buy | 4 |

| Anglogold Ashanti (AU) | $84.65 | $118.38 | +39.9% | Buy | 8 |

| Gold Fields (GFI) | $35.46 | $56.78 | +60.1% | Buy | 8 |

| Harmony Gold (HMY) | $16.09 | $23.01 | +43.0% | Buy | 3 |

Legend: Analyst consensus ratings for major African-jurisdiction mining companies. Prices and targets in USD. Implied upside = (target − current) / current. Data compiled July 2026.

</FinancialData>

| Country | GDP Growth 2022 | GDP Growth 2023 | GDP Growth 2024 | GDP Growth 2025 |

|---|---|---|---|---|

| South Africa | 2.06% | 0.81% | 0.53% | 1.11% |

| Nigeria | 4.32% | 3.32% | 4.07% | 4.01% |

Legend: Real annual GDP growth (%), 2022–2025. South Africa's growth decelerated to near-stagnation (below 1% for two of the last three years); Nigeria's growth is flat and well below the ~7% needed to absorb its population growth. Source: national accounts data.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| South Africa Unemployment (%) | 33.27 | 32.10 | 32.28 | 32.39 |

| Nigeria CPI Inflation (%) | 18.85 | 24.66 | 33.24 | 23.01 |

Legend: Structural failure indicators, 2022–2025. South African unemployment stayed locked above 32% through the "recovery"; Nigerian inflation peaked at 33.2% in 2024 — evidence markets cannot price or preserve capital. Source: national accounts data.

</FinancialData>

| Expiration | Strike | Call Bid | Call Ask | Call OI | Put OI | IV (Call) |

|---|---|---|---|---|---|---|

| 2026-07-17 | $35 | $1.50 | $2.00 | 2,891 | 812 | 52.2% |

| 2026-07-17 | $40 | $0.20 | $0.35 | 2,678 | 1,209 | 53.2% |

| 2026-08-21 | $40 | $1.25 | $1.50 | 2,703 | 14 | 55.1% |

| 2026-09-18 | $35 | $3.40 | $4.80 | 317 | 366 | 58.1% |

| 2027-01-15 | $40 | $3.40 | $4.10 | 197 | 1,038 | 50.3% |

| 2027-03-19 | $40 | $3.90 | $5.60 | 33 | 2,176 | 51.2% |

Legend: Selected options chain data for Gold Fields (GFI), showing bid-ask spreads, open interest, and implied volatility across multiple expirations. Data as of July 2026.

</FinancialData>

| Company | Strike | Initial Option Value | Final Option Value | Implied Vol | Path End Price |

|---|---|---|---|---|---|

| Gold Fields (GFI) | $40 | $2.95 | $16.82 | 63.6% | $56.78 |

| Sibanye Stillwater (SBSW) | $12 | $0.36 | $3.49 | 65.3% | $15.47 |

Legend: Black-Scholes call option pricing along consensus target price paths over 90 days. Option values in USD. Implied volatility derived from market data. Source: options chain analysis, July 2026.

</FinancialData>

| Region | Market Cap (% of GDP) | Share of Global Market Cap |

|---|---|---|

| Global | 113 | — |

| Emerging Markets | 61 | — |

| Africa | 33 | 0.4% |

Legend: Equity market depth, end-2024. Africa's market-cap-to-GDP ratio is roughly half the EM average, and it holds just 0.4% of global market capitalisation despite rising economic weight. Source: OECD Africa Capital Markets Report 2025.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

Latest available: 2025.

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 1.115 |

| 2024 | annual | 0.535 |

| 2023 | annual | 0.806 |

| 2022 | annual | 2.058 |

Latest available: 2025.

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 3.205 |

| 2024 | annual | 4.361 |

| 2023 | annual | 6.075 |

| 2022 | annual | 7.040 |

Latest available: 2025.

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 32.391 |

| 2024 | annual | 32.279 |

| 2023 | annual | 32.098 |

| 2022 | annual | 33.268 |

No historical observations available in the window.

- ■No historical observations available in the window.

No historical observations available in the window.

- ■No historical observations available in the window.

Latest available: 2025.

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 84.724 |

| 2024 | annual | 83.829 |

| 2023 | annual | 83.374 |

| 2022 | annual | 82.196 |

Latest available: 2025.

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 18.890 |

| 2024 | annual | 19.189 |

| 2023 | annual | 19.180 |

| 2022 | annual | 18.776 |

No historical observations available in the window.

- ■No historical observations available in the window.

…(truncated)…

MCP tool: get_option_chain

⚠️ No options for AU.

MCP tool: price_option_path

{"option_path": [9.453174689250567, 9.848178558254126, 10.813556208078708, 12.482896026433309, 14.349976759963766, 17.2482080139785, 21.506801490703523, 25.52897690568932, 28.13800803723825], "volatility_used": 0.6283462302511328, "symbol": "AU"}

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

Latest available: 2025.

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 4.013 |

| 2024 | annual | 4.071 |

| 2023 | annual | 3.316 |

| 2022 | annual | 4.319 |

Latest available: 2025.

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 23.010 |

| 2024 | annual | 33.242 |

| 2023 | annual | 24.660 |

| 2022 | annual | 18.847 |

Latest available: 2025.

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 3.064 |

| 2024 | annual | 3.045 |

| 2023 | annual | 3.074 |

| 2022 | annual | 3.827 |

No historical observations available in the window.

- ■No historical observations available in the window.

⚠️ Latest available: 2023 (annual; may lag current data).

| Period | Frequency | Value |

|---|---|---|

| 2023 | annual | 2.866 |

| 2022 | annual | 3.969 |

No historical observations available in the window.

- ■No historical observations available in the window.

No historical observations available in the window.

- ■No historical observations available in the window.

No historical observations available in the window.

- ■No historical observations available in the window.

…(truncated)…

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 20 | 2026-07-17 | 14.3 | 17.4 | 16.46 | 197.6% | - | 1 |

| PUT | 20 | 2026-07-17 | - | 0.2 | - | 110.8% | - | - |

| CALL | 25 | 2026-07-17 | 9.6 | 11.0 | 8.42 | 1.5% | - | 3 |

| PUT | 25 | 2026-07-17 | - | 0.5 | - | 70.8% | - | 9 |

| CALL | 30 | 2026-07-17 | 4.6 | 6.1 | 5.4 | 1.5% | 9 | 15 |

| PUT | 30 | 2026-07-17 | 0.05 | 0.45 | 0.18 | 68.8% | 22 | 1072 |

| CALL | 35 | 2026-07-17 | 1.5 | 2.0 | 1.63 | 52.2% | 552 | 2891 |

| PUT | 35 | 2026-07-17 | 1.15 | 1.5 | 1.3 | 55.1% | 24 | 812 |

| CALL | 40 | 2026-07-17 | 0.2 | 0.35 | 0.3 | 53.2% | 101 | 2678 |

| PUT | 40 | 2026-07-17 | 4.6 | 5.2 | - | 61.0% | - | 1209 |

| CALL | 45 | 2026-07-17 | - | 0.1 | 0.05 | 48.3% | 504 | 2924 |

| PUT | 45 | 2026-07-17 | 8.2 | 10.4 | - | 1.5% | - | 313 |

| CALL | 50 | 2026-07-17 | - | 0.2 | 0.15 | 66.9% | - | 933 |

| PUT | 50 | 2026-07-17 | 13.5 | 15.4 | - | 1.5% | - | 1 |

| CALL | 55 | 2026-07-17 | - | 0.75 | 0.03 | 82.5% | - | 1586 |

| PUT | 55 | 2026-07-17 | 18.1 | 20.7 | - | 1.5% | - | - |

| CALL | 60 | 2026-07-17 | - | 0.65 | 0.05 | 96.1% | - | 162 |

| PUT | 60 | 2026-07-17 | 23.1 | 26.7 | - | 171.2% | - | - |

| CALL | 65 | 2026-07-17 | - | 0.55 | 0.75 | 108.8% | - | 16 |

| PUT | 65 | 2026-07-17 | 28.1 | 31.1 | - | 155.6% | - | - |

| CALL | 70 | 2026-07-17 | - | 0.1 | 0.3 | 120.5% | - | 4 |

| PUT | 70 | 2026-07-17 | 33.1 | 36.2 | - | 179.0% | - | - |

| CALL | 20 | 2026-08-21 | 14.2 | 17.3 | - | 95.1% | - | - |

| PUT | 20 | 2026-08-21 | - | 0.95 | - | 61.0% | - | - |

| CALL | 22 | 2026-08-21 | 11.4 | 15.0 | - | 71.7% | - | - |

| PUT | 22 | 2026-08-21 | - | 0.55 | - | 49.3% | - | - |

| CALL | 25 | 2026-08-21 | 9.8 | 11.5 | - | 51.2% | - | - |

| PUT | 25 | 2026-08-21 | 0.05 | 0.25 | - | 60.0% | - | 9 |

| CALL | 30 | 2026-08-21 | 5.7 | 7.2 | 3.9 | 58.1% | - | 17 |

| PUT | 30 | 2026-08-21 | 0.6 | 1.05 | 0.79 | 58.1% | 12 | 1063 |

| CALL | 35 | 2026-08-21 | 2.75 | 3.4 | 3.15 | 53.2% | 35 | 1047 |

| PUT | 35 | 2026-08-21 | 2.45 | 2.75 | 2.75 | 56.1% | 1 | 174 |

| CALL | 40 | 2026-08-21 | 1.25 | 1.5 | 1.3 | 55.1% | 45 | 2703 |

| PUT | 40 | 2026-08-21 | 5.5 | 6.1 | - | 57.1% | - | 14 |

| CALL | 45 | 2026-08-21 | 0.45 | 0.7 | 0.7 | 57.1% | 11 | 77 |

| PUT | 45 | 2026-08-21 | 9.9 | 10.7 | - | 68.8% | - | 2 |

| CALL | 50 | 2026-08-21 | 0.15 | 0.35 | 0.3 | 60.0% | - | 8 |

| PUT | 50 | 2026-08-21 | 13.5 | 15.7 | - | 62.9% | - | - |

| CALL | 55 | 2026-08-21 | - | 1.0 | - | 44.4% | - | - |

| PUT | 55 | 2026-08-21 | 18.1 | 21.3 | - | 81.5% | - | - |

| CALL | 60 | 2026-08-21 | - | 0.9 | 0.5 | 52.2% | - | 7 |

| PUT | 60 | 2026-08-21 | 23.1 | 26.3 | - | 93.2% | - | - |

| CALL | 20 | 2026-09-18 | 13.8 | 17.5 | 12.06 | 57.1% | - | 2 |

| PUT | 20 | 2026-09-18 | - | 0.4 | - | 49.3% | - | - |

| CALL | 25 | 2026-09-18 | 9.8 | 12.4 | - | 62.9% | - | - |

| PUT | 25 | 2026-09-18 | 0.35 | 0.8 | - | 66.9% | - | 14 |

| CALL | 30 | 2026-09-18 | 5.9 | 8.0 | 11.59 | 56.1% | - | 31 |

| PUT | 30 | 2026-09-18 | 1.2 | 1.7 | 1.6 | 60.0% | 3 | 416 |

| CALL | 35 | 2026-09-18 | 3.4 | 4.8 | 3.7 | 58.1% | 3 | 317 |

| PUT | 35 | 2026-09-18 | 3.2 | 5.0 | 3.8 | 68.8% | 190 | 366 |

| CALL | 40 | 2026-09-18 | 1.65 | 2.9 | 1.7 | 58.1% | - | 77 |

| PUT | 40 | 2026-09-18 | 5.6 | 8.1 | - | 63.9% | - | 442 |

| CALL | 45 | 2026-09-18 | 0.8 | 1.3 | 1.1 | 56.1% | 9 | 350 |

| PUT | 45 | 2026-09-18 | 10.1 | 12.0 | - | 70.8% | - | 143 |

| CALL | 50 | 2026-09-18 | 0.4 | 0.9 | 0.64 | 60.0% | 1 | 204 |

| PUT | 50 | 2026-09-18 | 14.4 | 16.3 | - | 73.7% | - | 44 |

| CALL | 55 | 2026-09-18 | 0.2 | 0.45 | 0.35 | 61.0% | 3 | 1146 |

| PUT | 55 | 2026-09-18 | 18.5 | 21.1 | - | 72.7% | - | 2 |

| CALL | 60 | 2026-09-18 | 0.1 | 0.3 | 0.2 | 62.9% | 4 | 21 |

| PUT | 60 | 2026-09-18 | 23.5 | 26.1 | - | 83.4% | - | 1 |

| CALL | 65 | 2026-09-18 | - | 0.2 | 0.45 | 47.3% | - | 42 |

| PUT | 65 | 2026-09-18 | 28.1 | 31.6 | - | 95.1% | - | - |

| CALL | 70 | 2026-09-18 | - | 0.3 | 0.4 | 52.2% | - | 6 |

| PUT | 70 | 2026-09-18 | 33.1 | 36.6 | - | 103.9% | - | - |

| CALL | 20 | 2026-10-16 | 14.0 | 17.6 | 16.9 | 61.0% | - | 1 |

| PUT | 20 | 2026-10-16 | - | 0.5 | - | 42.5% | - | 7 |

| CALL | 25 | 2026-10-16 | 10.0 | 12.4 | 9.7 | 55.1% | - | 38 |

| PUT | 25 | 2026-10-16 | 0.35 | 0.75 | - | 57.1% | - | 5 |

| CALL | 30 | 2026-10-16 | 5.9 | 8.3 | 6.0 | 50.3% | - | 71 |

| PUT | 30 | 2026-10-16 | 1.6 | 2.15 | - | 60.0% | - | 262 |

| CALL | 35 | 2026-10-16 | 3.3 | 5.9 | 3.7 | 55.1% | - | 28 |

| PUT | 35 | 2026-10-16 | 3.6 | 4.4 | 4.16 | 59.0% | 8 | 160 |

| CALL | 40 | 2026-10-16 | 1.55 | 3.6 | 2.0 | 54.2% | - | 300 |

| PUT | 40 | 2026-10-16 | 6.1 | 8.6 | 7.3 | 62.9% | 1 | 41 |

| CALL | 45 | 2026-10-16 | 0.8 | 1.85 | 1.5 | 52.2% | 1 | 109 |

| PUT | 45 | 2026-10-16 | 9.7 | 12.4 | - | 62.9% | - | 12 |

| CALL | 50 | 2026-10-16 | 0.8 | 1.0 | 0.85 | 57.1% | 2 | 30 |

| PUT | 50 | 2026-10-16 | 14.3 | 16.7 | - | 67.8% | - | 35 |

| CALL | 55 | 2026-10-16 | 0.2 | 0.85 | 0.45 | 58.1% | - | 23 |

| PUT | 55 | 2026-10-16 | 19.0 | 21.4 | - | 73.7% | - | 1 |

| CALL | 60 | 2026-10-16 | 0.15 | 0.85 | 0.36 | 64.9% | - | 14 |

| PUT | 60 | 2026-10-16 | 23.5 | 26.3 | - | 77.6% | - | - |

| CALL | 65 | 2026-10-16 | - | 0.7 | 0.25 | 40.5% | - | 7 |

| PUT | 65 | 2026-10-16 | 28.2 | 31.2 | - | 81.5% | - | - |

| CALL | 70 | 2026-10-16 | - | 0.5 | 0.5 | 44.4% | - | 20 |

| PUT | 70 | 2026-10-16 | 33.2 | 36.5 | - | 93.2% | - | - |

| CALL | 20 | 2027-01-15 | 14.8 | 17.3 | 12.6 | 49.3% | - | 10 |

| PUT | 20 | 2027-01-15 | 0.15 | 1.0 | - | 62.9% | - | 3 |

| CALL | 22 | 2027-01-15 | 12.6 | 15.1 | - | 49.3% | - | - |

| PUT | 22 | 2027-01-15 | 0.45 | 1.45 | - | 62.0% | - | 3 |

| CALL | 25 | 2027-01-15 | 10.8 | 12.6 | 12.88 | 47.3% | - | 1 |

| PUT | 25 | 2027-01-15 | 0.95 | 1.75 | - | 58.1% | - | 74 |

| CALL | 30 | 2027-01-15 | 7.7 | 9.1 | 8.17 | 51.2% | 1 | 28 |

| PUT | 30 | 2027-01-15 | 2.5 | 3.3 | 2.9 | 57.1% | 1 | 137 |

| CALL | 35 | 2027-01-15 | 5.2 | 6.7 | 5.1 | 53.2% | 2 | 146 |

| PUT | 35 | 2027-01-15 | 4.8 | 5.7 | - | 57.1% | - | 89 |

| CALL | 40 | 2027-01-15 | 3.4 | 4.1 | 4.25 | 50.3% | 8 | 197 |

| PUT | 40 | 2027-01-15 | 7.0 | 9.8 | - | 58.1% | - | 1038 |

| CALL | 45 | 2027-01-15 | 2.1 | 2.9 | 2.5 | 50.3% | - | 31 |

| PUT | 45 | 2027-01-15 | 10.8 | 13.3 | - | 60.0% | - | 38 |

| CALL | 50 | 2027-01-15 | 1.2 | 2.7 | 3.62 | 54.2% | - | 105 |

| PUT | 50 | 2027-01-15 | 14.8 | 17.5 | - | 62.0% | - | 14 |

| CALL | 55 | 2027-01-15 | 0.6 | 2.1 | 1.0 | 55.1% | - | 388 |

| PUT | 55 | 2027-01-15 | 19.0 | 22.6 | - | 66.9% | - | 1 |

| CALL | 60 | 2027-01-15 | 0.45 | 1.5 | 1.1 | 56.1% | - | 72 |

| PUT | 60 | 2027-01-15 | 23.6 | 27.2 | - | 70.8% | - | - |

| CALL | 65 | 2027-01-15 | 0.1 | 1.4 | 0.85 | 58.1% | - | 76 |

| PUT | 65 | 2027-01-15 | 28.3 | 32.0 | - | 74.7% | - | 1 |

| CALL | 70 | 2027-01-15 | 0.1 | 1.8 | 1.54 | 65.9% | - | 11 |

| PUT | 70 | 2027-01-15 | 33.1 | 36.7 | - | 78.6% | - | - |

| CALL | 20 | 2027-03-19 | 14.8 | 17.5 | 14.6 | 42.5% | - | 10 |

| PUT | 20 | 2027-03-19 | 0.65 | 1.0 | - | 61.0% | - | 10 |

| CALL | 25 | 2027-03-19 | 10.4 | 13.5 | 13.36 | 43.4% | - | 164 |

| PUT | 25 | 2027-03-19 | 1.6 | 2.3 | 1.92 | 60.0% | 8 | 235 |

| CALL | 30 | 2027-03-19 | 7.0 | 10.1 | 6.6 | 44.4% | - | 16 |

| PUT | 30 | 2027-03-19 | 3.2 | 4.2 | - | 59.0% | - | 137 |

| CALL | 35 | 2027-03-19 | 4.6 | 7.9 | 5.2 | 47.3% | - | 13 |

| PUT | 35 | 2027-03-19 | 5.7 | 6.8 | 6.41 | 60.0% | 47 | 64 |

| CALL | 40 | 2027-03-19 | 3.9 | 5.6 | 3.13 | 51.2% | - | 33 |

| PUT | 40 | 2027-03-19 | 7.9 | 11.2 | - | 62.0% | - | 2176 |

| CALL | 45 | 2027-03-19 | 2.45 | 4.1 | 2.35 | 50.3% | - | 74 |

| PUT | 45 | 2027-03-19 | 11.5 | 14.4 | - | 61.0% | - | 2 |

| CALL | 50 | 2027-03-19 | 1.75 | 3.3 | 2.15 | 52.2% | - | 11 |

| PUT | 50 | 2027-03-19 | 15.3 | 18.6 | - | 62.9% | - | 2 |

| CALL | 55 | 2027-03-19 | 1.25 | 2.4 | 2.55 | 53.2% | - | 5 |

| PUT | 55 | 2027-03-19 | 19.7 | 23.2 | - | 67.8% | - | - |

| CALL | 60 | 2027-03-19 | 0.8 | 1.9 | 1.0 | 53.2% | - | 8 |

| PUT |

…(truncated)…

MCP tool: price_option_path

{"option_path": [2.948544289213995, 3.414712926313376, 3.906939161484683, 4.5604627487320855, 5.352745444549278, 6.384745868529002, 7.955111077800193, 9.766806686211787, 12.303785316127424, 15.10766882478859, 16.824928770352763], "volatility_used": 0.6359633662149633, "symbol": "GFI"}

MCP tool: price_option_path

{"option_path": [0.3564668786530787, 0.4510418825665137, 0.6161140927016677, 0.8621250845866131, 1.1677533901365864, 1.477034857422061, 1.8415630814252122, 2.3510325510729686, 2.952131171384602, 3.355425993749101, 3.485336751419201], "volatility_used": 0.653203718530596, "symbol": "SBSW"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.