Can SpaceX sustain a profitable business model by renting out its AI data center capacity to direct competitors?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 14, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 86%

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

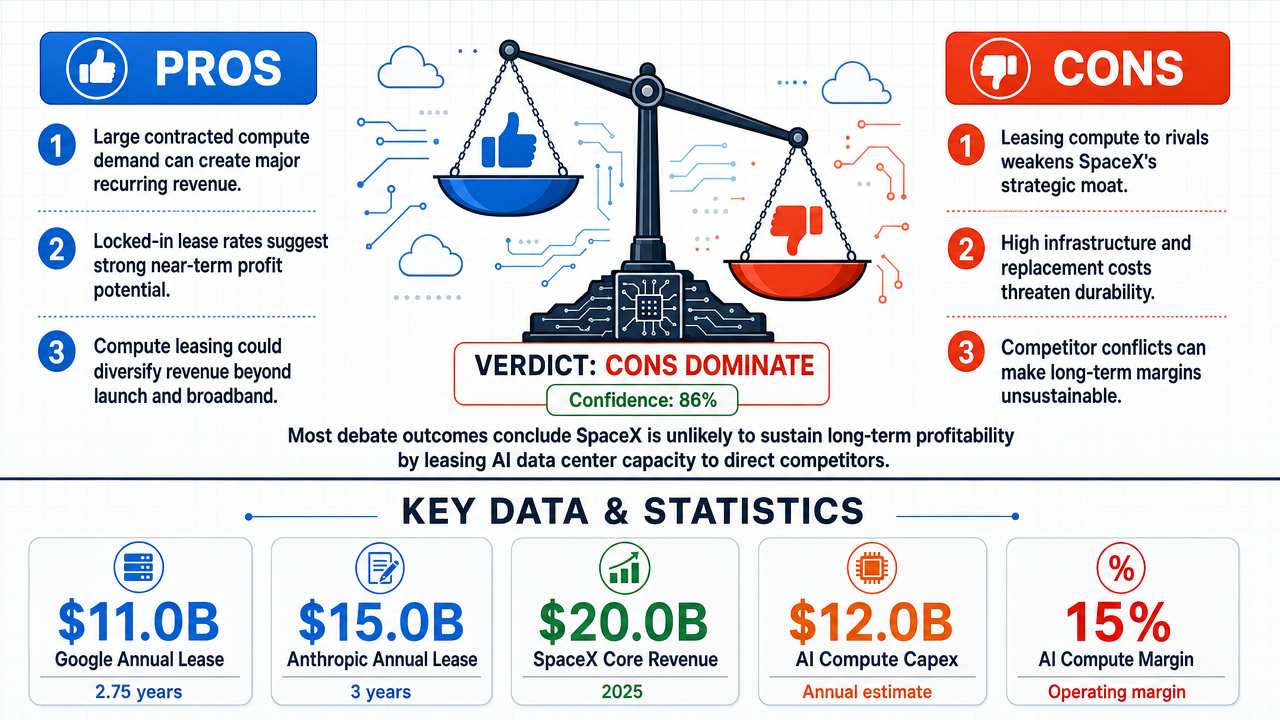

✅ Key PRO arguments:

- ■SpaceX can profitably lease compute capacity through massive contracted revenue streams, with combined annual committed revenue exceeding $25 billion from Google and Anthropic contracts, surpassing SpaceX's core business revenue.

- ■The financial mathematics of SpaceX's compute leasing strategy demonstrate clear profitability potential, with locked-in monthly rates of $1.25 billion from Anthropic and $920 million from Google through 2029, generating $70+ billion in aggregate contracted revenue.

❌ Key ANTI arguments:

- ■Leasing compute to direct competitors is strategically self-destructive, as it arms rivals and undermines SpaceX's competitive moats in launch services and satellite internet, where proprietary infrastructure and data flows are key advantages.

- ■Strategic self-cannibalization: by leasing computational capacity to direct competitors, SpaceX would transfer the very infrastructure advantage that makes it dominant, allowing rivals to optimize their own operations and erode SpaceX's market share.

- ■Strategic conflicts and infrastructure costs make leasing capacity to competitors financially unsustainable; creating a 'coopetition' paradox where marginal profit from leasing is dwarfed by potential loss in Starlink subscriptions or launch contracts.

💭 Conclusion: The tournament results overwhelmingly favored the FALSE side, with 22 out of 25 debates ruling that SpaceX cannot sustain a profitable business model by renting AI data center capacity to direct competitors, and a high confidence-weighted score of 15.40 versus 2.55. The winning anti-arguments consistently highlighted strategic risks, such as arming direct competitors and undermining SpaceX's core competitive advantages in launch and satellite services. The pro side's arguments, while pointing to large contracted revenue ($25B+ annually), failed to overcome the strategic and economic counterarguments presented by multiple diverse models. The high tournament confidence (86%) and near-unanimous verdicts indicate a strong consensus that the strategic drawbacks outweigh potential financial gains. Therefore, the assertion is false.

🔬 DeepResearch Result: FALSE ❌ (86% confidence)

Assertion: Can SpaceX sustain a profitable business model by renting out its AI data center capacity to direct competitors?

⏰ Note: Tournament finalized early after 2/3 rounds due to time constraints. Results are based on completed rounds.

📊 Tournament: 3 voted TRUE, 22 voted FALSE (25 debates played, 11 models)

📊 Weighted scores: TRUE=2.55, FALSE=15.40

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +116

✅ PRO Arguments:

- ■SpaceX can profitably lease compute capacity through massive contracted revenue streams, with combined annual committed revenue exceeding $25 billion from Google and Anthropic contracts, surpassing SpaceX's core business revenue. [qwen/qwen3.5-397b-a17b]

- ■The financial mathematics of SpaceX's compute leasing strategy demonstrate clear profitability potential, with locked-in monthly rates of $1.25 billion from Anthropic and $920 million from Google through 2029, generating $70+ billion in aggregate contracted revenue. [qwen/qwen3.5-397b-a17b]

❌ ANTI Arguments:

- ■Leasing compute to direct competitors is strategically self-destructive, as it arms rivals and undermines SpaceX's competitive moats in launch services and satellite internet, where proprietary infrastructure and data flows are key advantages. [z-ai/glm-5]

- ■Strategic self-cannibalization: by leasing computational capacity to direct competitors, SpaceX would transfer the very infrastructure advantage that makes it dominant, allowing rivals to optimize their own operations and erode SpaceX's market share. [z-ai/glm-5.1]

- ■Strategic conflicts and infrastructure costs make leasing capacity to competitors financially unsustainable; creating a 'coopetition' paradox where marginal profit from leasing is dwarfed by potential loss in Starlink subscriptions or launch contracts. [google/gemini-3-flash-preview]

💭 Reasoning: The tournament results overwhelmingly favored the FALSE side, with 22 out of 25 debates ruling that SpaceX cannot sustain a profitable business model by renting AI data center capacity to direct competitors, and a high confidence-weighted score of 15.40 versus 2.55. The winning anti-arguments consistently highlighted strategic risks, such as arming direct competitors and undermining SpaceX's core competitive advantages in launch and satellite services. The pro side's arguments, while pointing to large contracted revenue ($25B+ annually), failed to overcome the strategic and economic counterarguments presented by multiple diverse models. The high tournament confidence (86%) and near-unanimous verdicts indicate a strong consensus that the strategic drawbacks outweigh potential financial gains. Therefore, the assertion is false.

📋 PRO Facts:

• SpaceX has a contract with Anthropic for AI compute at $1.25 billion per month through May 2029.

• SpaceX has a contract with Google for AI compute at $920 million per month from October 2026 through June 2029.

• Combined annual committed revenue from these contracts exceeds $25 billion, surpassing SpaceX's 2025 total revenue of under $20 billion.

• Aggregate contracted revenue from these deals exceeds $70 billion over the contract terms.

📋 ANTI Facts:

• SpaceX's competitors in launch services include Blue Origin, ULA, and Rocket Lab.

• SpaceX's competitors in satellite internet include Amazon's Project Kuiper, OneWeb, and Telesat.

• Leasing compute to competitors transfers proprietary orbital infrastructure, data flows, and vertically integrated operations advantages.

• Historical tech industry precedents show that relying on a primary competitor for core infrastructure creates strategic vulnerability and can lead to market share losses.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | qwen/qwen3.5-397b-a17b | z-ai/glm-5 | 0.439 | 0.000 | 11 | 11 | TRUE | TRUE | 90% |

| #2 | qwen/qwen3.5-397b-a17b | z-ai/glm-5.1 | 0.356 | 0.000 | 22 | 36 | TRUE | TRUE | 95% |

| #3 | qwen/qwen3.5-397b-a17b | google/gemini-3-flash-preview | 0.000 | 0.064 | 11 | 14 | FALSE | TRUE | 70% |

| #4 | qwen/qwen3.5-397b-a17b | qwen/qwen3-235b-a22b | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #5 | qwen/qwen3.5-397b-a17b | mistralai/mistral-large | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 30% |

| #6 | openai/gpt-5.1 | z-ai/glm-5 | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #7 | openai/gpt-5.2-chat | z-ai/glm-5 | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #8 | openai/gpt-5.2 | z-ai/glm-5 | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #9 | openai/gpt-5.1 | z-ai/glm-5.1 | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #10 | anthropic/claude-sonnet-4.6 | z-ai/glm-5 | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #11 | openai/gpt-5.1 | google/gemini-3-flash-preview | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #12 | openai/gpt-5.2-chat | z-ai/glm-5.1 | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #13 | openai/gpt-5.2 | z-ai/glm-5.1 | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #14 | openai/gpt-5.1 | qwen/qwen3-235b-a22b | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #15 | openai/gpt-5.2-chat | google/gemini-3-flash-preview | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #16 | openai/gpt-5.2 | google/gemini-3-flash-preview | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #17 | anthropic/claude-sonnet-4.6 | z-ai/glm-5.1 | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 30% |

| #18 | openai/gpt-5.1 | mistralai/mistral-large | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 30% |

| #19 | openai/gpt-5.2-chat | qwen/qwen3-235b-a22b | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 30% |

| #20 | openai/gpt-5.2 | qwen/qwen3-235b-a22b | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 30% |

| #21 | anthropic/claude-sonnet-4.6 | google/gemini-3-flash-preview | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 30% |

| #22 | openai/gpt-5.2-chat | mistralai/mistral-large | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #23 | openai/gpt-5.2 | mistralai/mistral-large | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #24 | anthropic/claude-sonnet-4.6 | qwen/qwen3-235b-a22b | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

| #25 | anthropic/claude-sonnet-4.6 | mistralai/mistral-large | 0.000 | 0.000 | 0 | 0 | TRUE | FALSE | 85% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] aggregate contract value — The total monetary value of all contracts combined over their full duration, often used to assess the scale of committed revenue.

[2] AI accelerator — Specialized hardware (e.g., GPUs, TPUs) designed to speed up artificial intelligence computations, particularly training and inference.

[3] bridge capacity — Temporary computational capacity leased to meet short-term demand while permanent infrastructure is being built.

[4] capital allocation — The process of distributing financial resources among different business units or investments to maximize returns.

[5] compute leasing — The practice of renting out computational capacity (e.g., servers, GPUs) to third parties for a fee.

[6] compute-as-a-service — A business model where computational resources (e.g., GPU time) are leased to customers on a subscription or usage basis.

[7] contracted revenue — Revenue guaranteed by legally binding agreements, typically with fixed terms and pricing.

[8] dual monetization strategy — A business approach that generates revenue from the same asset in two ways, such as using infrastructure internally and leasing excess capacity externally.

[9] first-mover advantage — The competitive edge gained by being the first to enter a market, often through brand recognition, customer loyalty, or technological leadership.

[10] hyperscaler — A large-scale cloud service provider (e.g., Google, Amazon, Microsoft) that operates massive data centers and offers computing resources globally.

[11] inference — The process of using a trained AI model to make predictions or decisions on new data.

[12] IPO filing — Initial Public Offering filing — A document submitted to regulators when a company plans to go public, disclosing financials, risks, and business strategies.

[13] mesh networking — A network topology where each node relays data for others, creating a resilient and decentralized communication system.

[14] moat — A sustainable competitive advantage that protects a company from rivals, such as proprietary technology or network effects.

[15] network effects — A phenomenon where a product or service becomes more valuable as more people use it, creating a self-reinforcing growth cycle.

[16] orbital data center — A data center located in space, typically on satellites, used for computational processing in orbit.

[17] orbital lifespan — The duration a satellite remains functional in orbit before it degrades or re-enters Earth's atmosphere.

[18] proprietary AI infrastructure — AI hardware and software systems owned exclusively by a company, providing a competitive edge through unique capabilities.

[19] refresh cycle — The period after which hardware (e.g., GPUs, servers) is replaced with newer models to maintain performance.

[20] scarcity rents — Profits earned from owning a scarce resource, where high demand and limited supply allow premium pricing.

[21] stranded asset economics — A situation where an asset becomes obsolete or underutilized before its expected lifespan, leading to financial losses.

[22] TCO — Total Cost of Ownership — A financial estimate of all direct and indirect costs associated with acquiring, operating, and maintaining an asset over its lifecycle.

[23] terrestrial data center — A data center located on Earth's surface, as opposed to orbital or underwater facilities.

[24] winner-take-all market — A market where the leading firm captures most of the profits and market share, often due to network effects or economies of scale.

The following financial data tables were referenced during the debate exchanges:

| Revenue Stream | Annual Value | Contract Duration | Total Value |

|---|---|---|---|

| Google Compute Lease | $11.0B | 2.75 years | $30.3B |

| Anthropic Compute Lease | $15.0B | 3 years | $45.0B |

| SpaceX Core Business (2025) | $20.0B | N/A | N/A |

Legend: Annual and total contract values for SpaceX compute leasing deals versus 2025 core business revenue. Values in USD billions. Source: IPO filings and regulatory disclosures.

</FinancialData>

| Cost Factor | Terrestrial Data Center | Orbital Data Center | Multiplier |

|---|---|---|---|

| Hardware CapEx | $1.0B | $1.0B | 1.0x |

| Launch/Deployment | $0 | $3.5B+ | ∞ |

| Refresh Cycle (5yr) | $1.0B | $4.5B+ | 4.5x |

| Total 5-Year TCO | $2.0B | $9.0B+ | 4.5x |

| Full Lifecycle TCO | $2.5B | $20B+ | 8.0x |

Legend: Comparative total cost of ownership for equivalent 1GW AI compute capacity over 5-7 year lifecycle. Orbital costs include launch, deployment, and replacement. Source: ABI Research TCO analysis cited in endtropy.substack.com.

</FinancialData>

| Revenue Stream | Monthly Rate | Contract Duration | Total Value |

|---|---|---|---|

| Anthropic Compute Lease | $1.25B | Through May 2029 | ~$45B |

| Google Compute Lease | $920M | Oct 2026 - Jun 2029 | ~$26B |

| SpaceX 2025 Total Revenue | N/A | Annual | <$20B |

Legend: Major SpaceX compute leasing contracts versus historical core business revenue. Values in USD billions. Contract totals estimated from disclosed monthly rates and duration. Source: IPO filings and regulatory disclosures.

</FinancialData>

| Infrastructure Type | CapEx (Relative) | Lifespan (Years) | Launch Cost | TCO vs. Terrestrial |

|---|---|---|---|---|

| Terrestrial Data Center | 1.0x | 10–15 | $0 | Baseline |

| Orbital Data Center | 3.0x | 5–7 | Very High | ~8.0x |

Legend: Comparative cost structure of terrestrial vs. orbital AI compute infrastructure. CapEx and TCO expressed as multiples of terrestrial baseline. Orbital TCO includes launch, replacement cycles, and deorbit costs. Source: lifecycle cost analysis of orbital data center economics.

</FinancialData>

| Infrastructure Type | Est. Annual Capex | Operating Margin | Asset Lifecycle |

|---|---|---|---|

| Specialized AI Compute | $12.0B | 15% | 3 Years |

| Satellite Launch/Starlink | $5.5B | 30% | 7-10 Years |

| Terrestrial Fiber/Data | $3.2B | 22% | 15+ Years |

Legend: Comparison of capital intensity and margins between AI infrastructure and SpaceX's core aerospace operations. Capex in USD; margins are estimated industry averages for 2024-2026.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.